transformation through organic growth and …68e603cc-9915-4b9f-816e...1 transformation through...

TRANSCRIPT

1

Transformation through Organic Growth and Operational Excellence

Steve de Kruijff, COO Xstrata Copper North QueenslandAnalyst Visit Ernest Henry Mining – April 2011

2

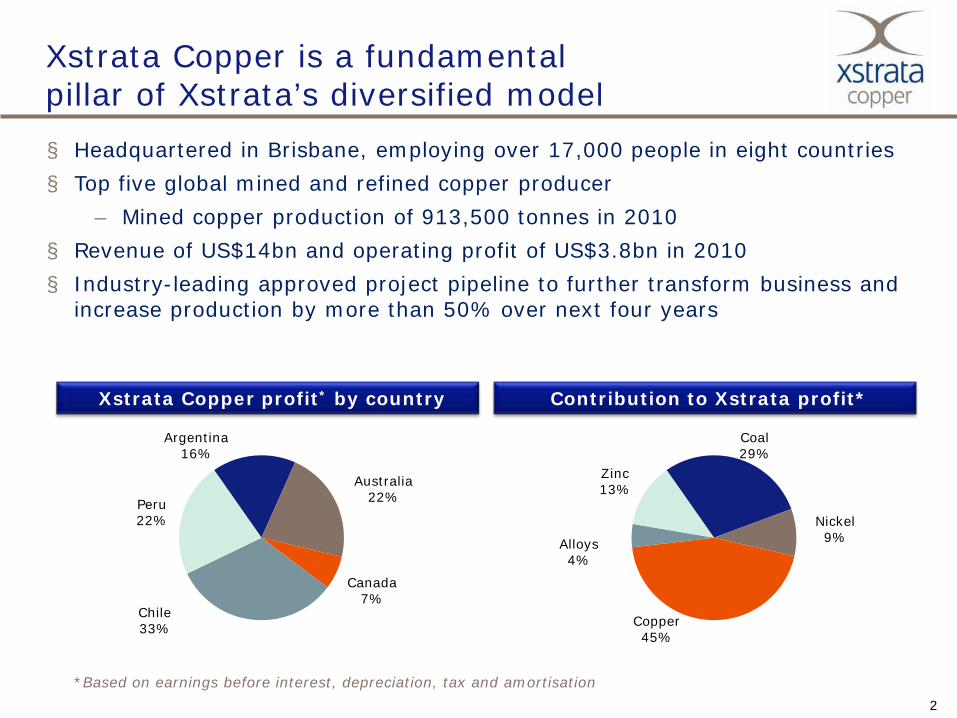

Xstrata Copper is a fundamental pillar of Xstrata’s diversified model

Contribution to Xstrata profit*

Coal29%

Nickel 9%

Copper45%

Alloys4%

Zinc13%

Xstrata Copper profit* by country

Argentina16%

Australia22%

Canada7%

Chile33%

Peru22%

*Based on earnings before interest, depreciation, tax and amortisation

§ Headquartered in Brisbane, employing over 17,000 people in eight countries§ Top five global mined and refined copper producer

– Mined copper production of 913,500 tonnes in 2010§ Revenue of US$14bn and operating profit of US$3.8bn in 2010§ Industry-leading approved project pipeline to further transform business and

increase production by more than 50% over next four years

3

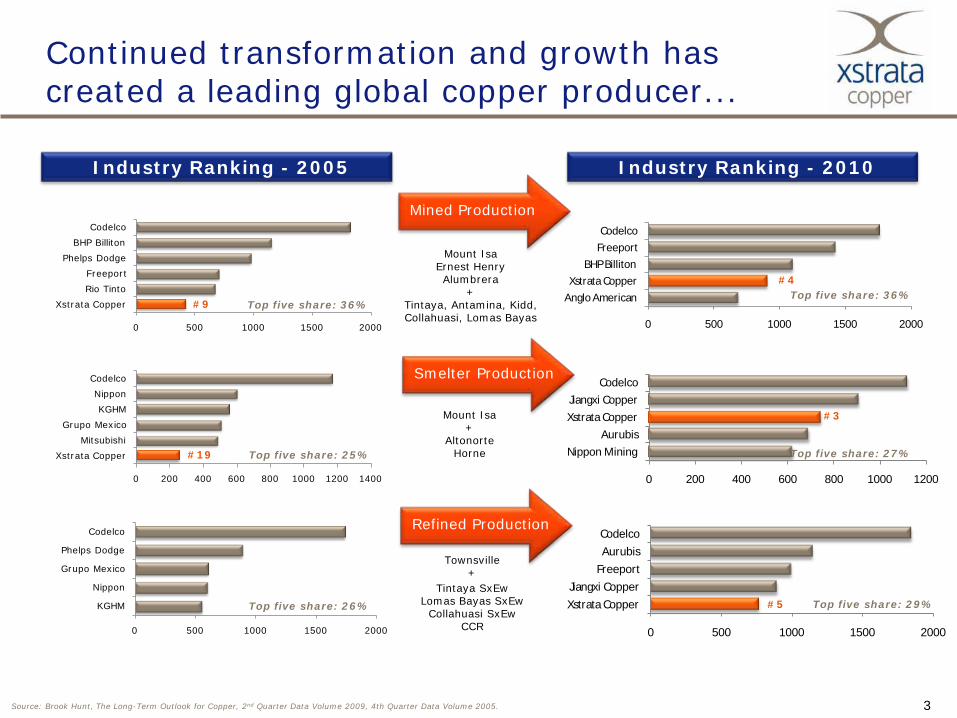

0 500 1000 1500 2000

Xstrata CopperJiangxi Copper

FreeportAurubisCodelco

0 200 400 600 800 1000 1200

Nippon MiningAurubis

Xstrata CopperJiangxi Copper

Codelco

0 500 1000 1500 2000

Anglo AmericanXstrata Copper

BHP BillitonFreeportCodelco

0 500 1000 1500 2000

Xstrata CopperRio TintoFreeport

Phelps DodgeBHP Billiton

Codelco

Continued transformation and growth hascreated a leading global copper producer...

Townsville+

Tintaya SxEwLomas Bayas SxEw

Collahuasi SxEwCCR

Mount IsaErnest HenryAlumbrera

+Tintaya, Antamina, Kidd, Collahuasi, Lomas Bayas

Mount Isa+

AltonorteHorne

Industry Ranking - 2010

Top five share: 36%

Top five share: 29%

Top five share: 27%

Source: Brook Hunt, The Long-Term Outlook for Copper, 2nd Quarter Data Volume 2009, 4th Quarter Data Volume 2005.

Industry Ranking - 2005

0 200 400 600 800 1000 1200 1400

Xstrata CopperMitsubishi

Grupo MexicoKGHM

NipponCodelco

0 500 1000 1500 2000

KGHM

Nippon

Grupo Mexico

Phelps Dodge

Codelco

Top five share: 36%

Top five share: 26%

Top five share: 25%

#9

#19

#4

#3

#5

Mined Production

Smelter Production

Refined Production

4

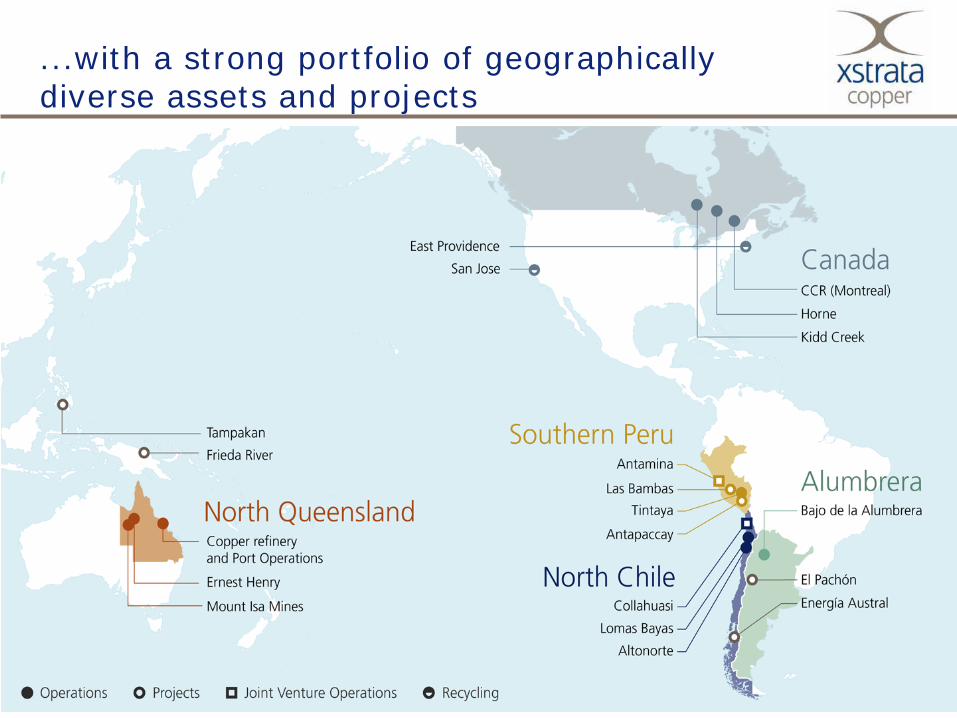

...with a strong portfolio of geographically diverse assets and projects

5

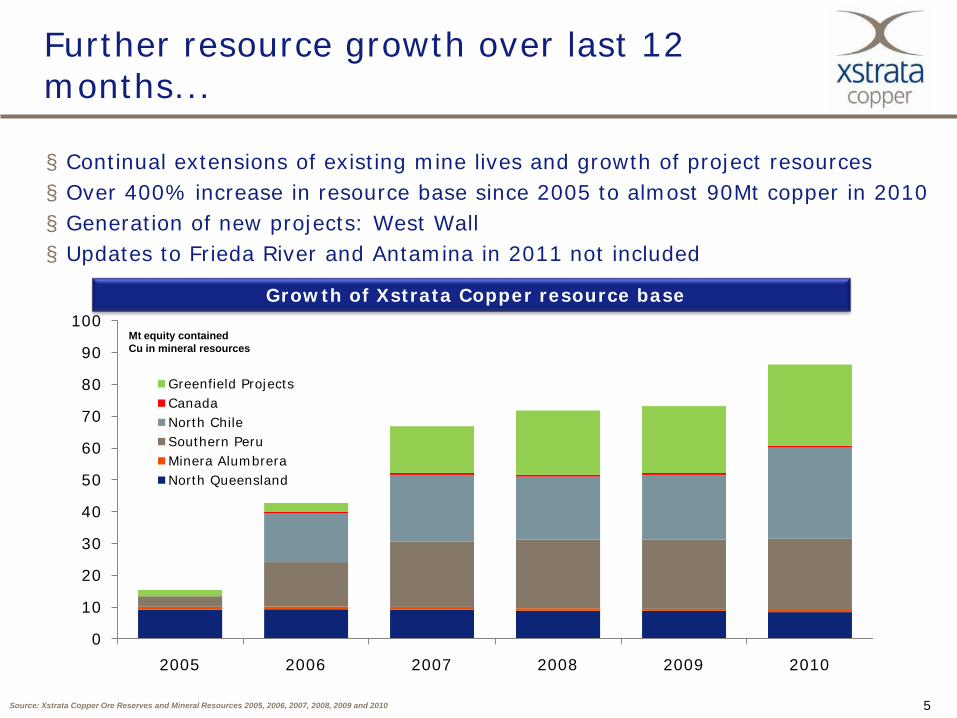

Further resource growth over last 12 months...

Mt equity contained Cu in mineral resources

Source: Xstrata Copper Ore Reserves and Mineral Resources 2005, 2006, 2007, 2008, 2009 and 2010

§ Continual extensions of existing mine lives and growth of project resources§ Over 400% increase in resource base since 2005 to almost 90Mt copper in 2010 § Generation of new projects: West Wall§ Updates to Frieda River and Antamina in 2011 not included

Growth of Xstrata Copper resource base

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010

Greenfield ProjectsCanadaNorth ChileSouthern PeruMinera AlumbreraNorth Queensland

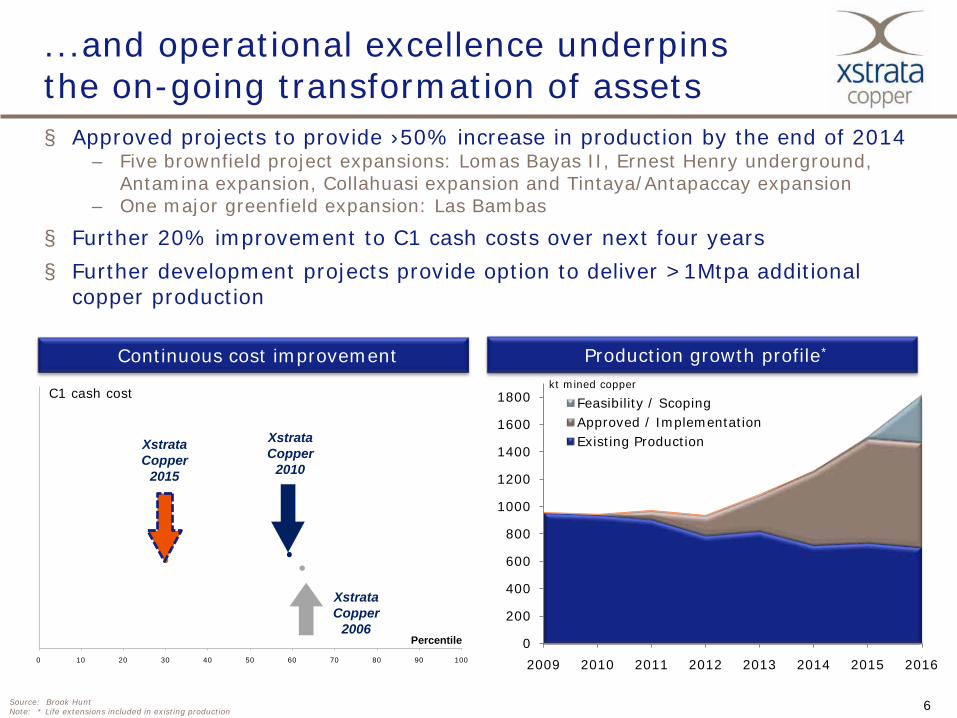

6Source: Brook HuntNote: * Life extensions included in existing production

...and operational excellence underpins the on-going transformation of assets

Continuous cost improvement

0 10 20 30 40 50 60 70 80 90 100

XstrataCopper

2010

C1 cash cost

Percentile

XstrataCopper

2015

XstrataCopper

2006

kt mined copper

Production growth profile*

§ Approved projects to provide ›50% increase in production by the end of 2014– Five brownfield project expansions: Lomas Bayas II, Ernest Henry underground,

Antamina expansion, Collahuasi expansion and Tintaya/Antapaccay expansion– One major greenfield expansion: Las Bambas

§ Further 20% improvement to C1 cash costs over next four years§ Further development projects provide option to deliver >1Mtpa additional

copper production

0

200

400

600

800

1000

1200

1400

1600

1800

2009 2010 2011 2012 2013 2014 2015 2016

Feasibility / ScopingApproved / ImplementationExisting Production

77

Further growth optionality§ Collahuasi progressing concept studies into brownfield expansion to >1

million tonnes per annum (100%) copper production§ Potential for >1 million tonnes per annum (100%) initial copper production

from three major greenfield projects in final feasibility studies§ Evaluation of potential new projects to add to Xstrata Copper’s development

portfolio – West Wall, Agua Rica

¹ Average production over first five years

Project Country Development Stage Mineral ResourceIndicative Annual

Production (100%)¹El Pachón Argentina Final Feasibility 1.8Bt @ 0.51% Cu ~400ktTampakan Philippines Final Feasibility 2.4Bt @ 0.60% Cu ~450ktFrieda River PNG Final Feasibility 1.9Bt @ 0.45% Cu ~260ktCollahuasi exp Chile Concept studies 7.1Bt @ 0.82% Cu ~500ktEnergia Austral Chile Feasibility n/a ~1,100 MWWest Wall Chile Advanced Exploration 750Mt @ 0.54% Cu

8

North Queensland DivisionProduction capacity

§ Regional office−Mount Isa§ Mount Isa Underground mines −170,000tpa Cu in

concentrate§ Mount Isa smelter −280,000tpa copper anodes§ Ernest Henry open cut mine−90,000tpa Cu in concentrate−110,000ozpa Au in

concentrate§ Townsville Refinery & Port−300,000tpa of copper

cathodes

9

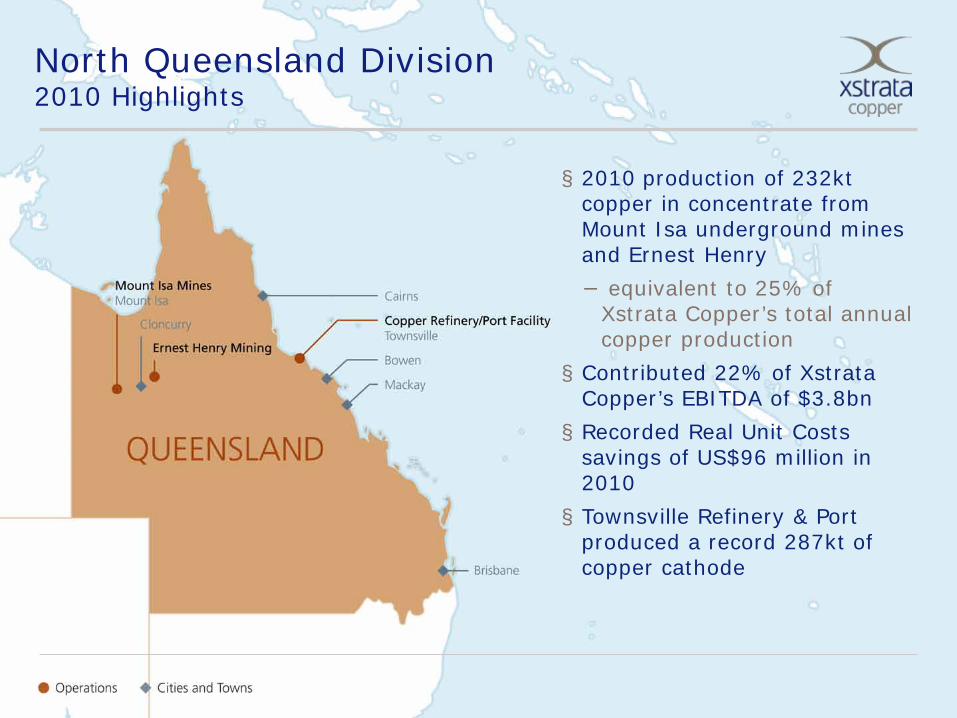

North Queensland Division2010 Highlights

§ 2010 production of 232kt copper in concentrate from Mount Isa underground mines and Ernest Henry − equivalent to 25% of

Xstrata Copper’s total annual copper production

§ Contributed 22% of Xstrata Copper’s EBITDA of $3.8bn § Recorded Real Unit Costs

savings of US$96 million in 2010§ Townsville Refinery & Port

produced a record 287kt of copper cathode

1010

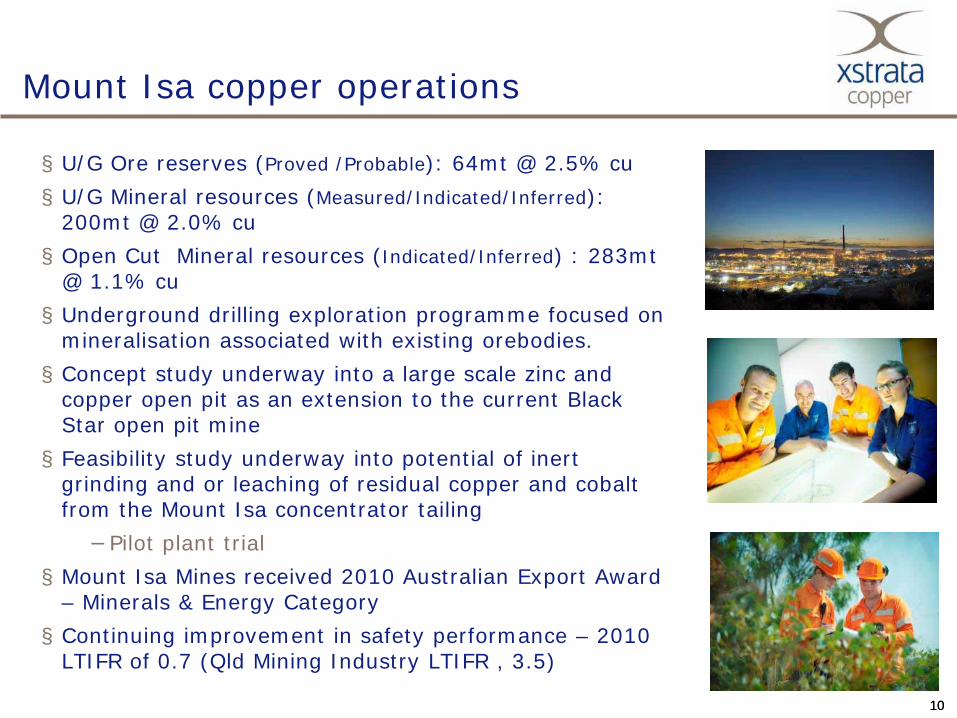

Mount Isa copper operations

§ U/G Ore reserves (Proved /Probable): 64mt @ 2.5% cu§ U/G Mineral resources (Measured/Indicated/Inferred):

200mt @ 2.0% cu§ Open Cut Mineral resources (Indicated/Inferred) : 283mt

@ 1.1% cu§ Underground drilling exploration programme focused on

mineralisation associated with existing orebodies. § Concept study underway into a large scale zinc and

copper open pit as an extension to the current Black Star open pit mine§ Feasibility study underway into potential of inert

grinding and or leaching of residual copper and cobalt from the Mount Isa concentrator tailing−Pilot plant trial

§ Mount Isa Mines received 2010 Australian Export Award – Minerals & Energy Category§ Continuing improvement in safety performance – 2010

LTIFR of 0.7 (Qld Mining Industry LTIFR , 3.5)

11

Copper market update

1212

0

2000

4000

6000

8000

10000

12000

14000

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

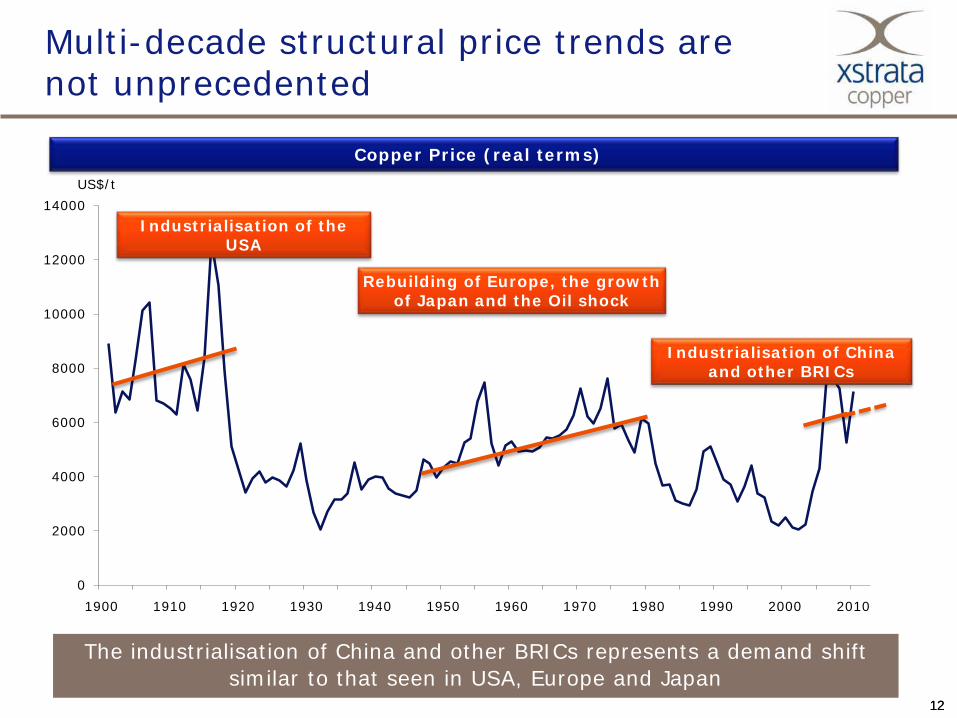

Multi-decade structural price trends are not unprecedented

Copper Price (real terms)

Industrialisation of the USA

Rebuilding of Europe, the growth of Japan and the Oil shock

Industrialisation of China and other BRICs

The industrialisation of China and other BRICs represents a demand shift similar to that seen in USA, Europe and Japan

US$/t

1313

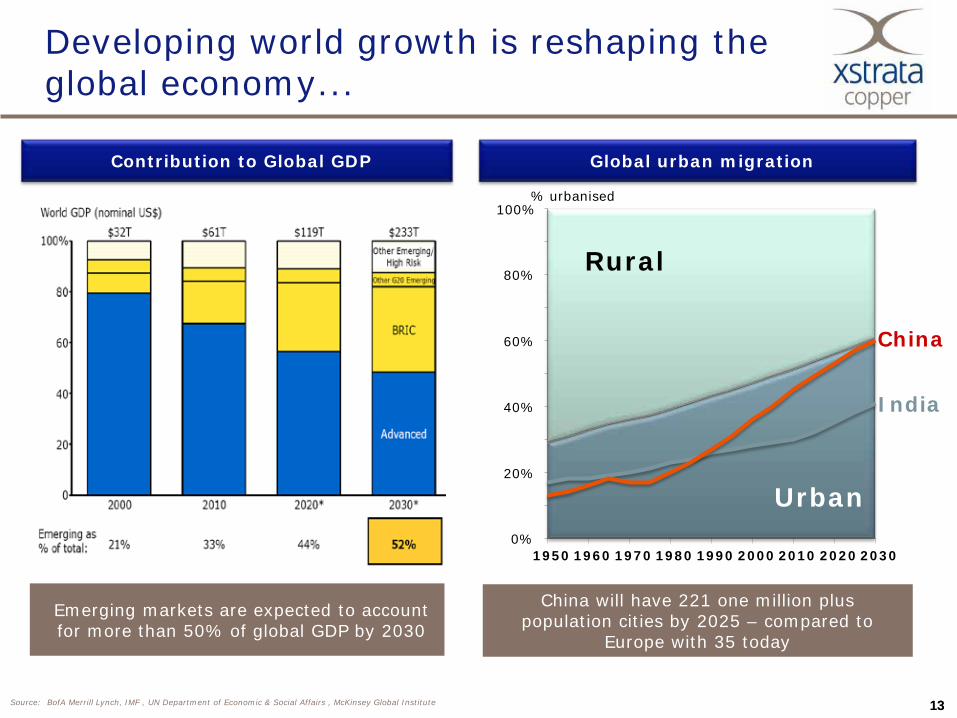

Developing world growth is reshaping the global economy...

Global urban migration

Source: BofA Merrill Lynch, IMF , UN Department of Economic & Social Affairs , McKinsey Global Institute

Contribution to Global GDP

Urban

Rural

India

China

0%

20%

40%

60%

80%

100%

1950 1960 1970 1980 1990 2000 2010 2020 2030

% urbanised

China will have 221 one million plus population cities by 2025 – compared to

Europe with 35 today

Emerging markets are expected to account for more than 50% of global GDP by 2030

1414

... generating a structural shift in commodity demand

Source: IMF, USGS, CIA FactbookNote: 1 Stylised intensity curves based on developed countries

0

5'000

10'000

15'000

0 2'000 4'000

Population (cumulative bn)

Energy consumption per capita (kWh/capita)

Populous nations have a multiplier effect on commodity demand

Indonesia

India

China: 3,438bn kWh

Japan

Europe

USA: 3,873bn kWh

China: ~7,000bn kWh by 2020

Commodity intensity¹(Indexed to 100 at maximum)

Mid-cycle commoditiese.g. Copper, lead and zinc

Late cycle commoditiese.g. Platinum, nickel

0

20

50

75

100

0 5 10 15 20 25 30 35 40 45 $50k

GDP per capita (real, 2005 USD)

Early cycle commoditiese.g. Steel, iron ore

Chinese GDP: ~$2.5k/capita

Indian GDP: ~$1k/capita

US GDP: ~$50k/capita

Increasing intensities generate a demand shift for commodities in emerging markets

• As a percentage of US intensity peak, China today is: 12% Copper, 1% nickel and 30% iron ore

China’s per capita energy consumption is expected to double by 2020

• Demand is also expected to grow strongly in India, Indonesia and Brazil

1515

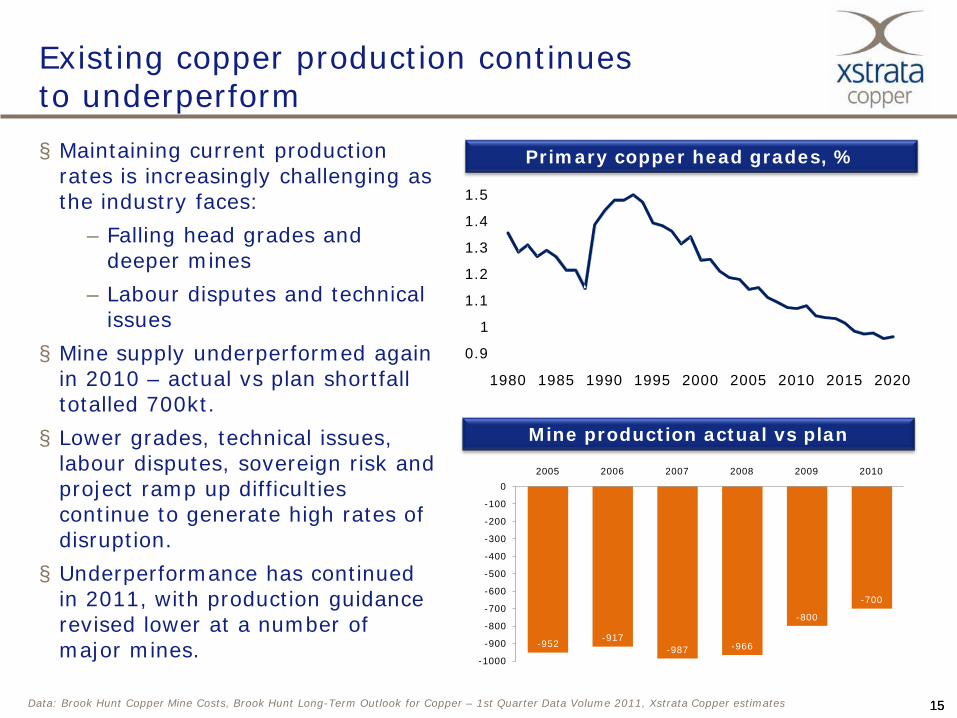

-952 -917-987 -966

-800

-700

-1000

-900

-800

-700

-600

-500

-400

-300

-200

-100

02005 2006 2007 2008 2009 2010

Existing copper production continues to underperform

0.9

1

1.1

1.2

1.3

1.4

1.5

1980 1985 1990 1995 2000 2005 2010 2015 2020

Primary copper head grades, %

Mine production actual vs plan

§ Maintaining current production rates is increasingly challenging as the industry faces:

– Falling head grades and deeper mines

– Labour disputes and technical issues

§ Mine supply underperformed again in 2010 – actual vs plan shortfall totalled 700kt.§ Lower grades, technical issues,

labour disputes, sovereign risk and project ramp up difficulties continue to generate high rates of disruption. § Underperformance has continued

in 2011, with production guidance revised lower at a number of major mines.

Data: Brook Hunt Copper Mine Costs, Brook Hunt Long-Term Outlook for Copper – 1st Quarter Data Volume 2011, Xstrata Copper estimates

1616

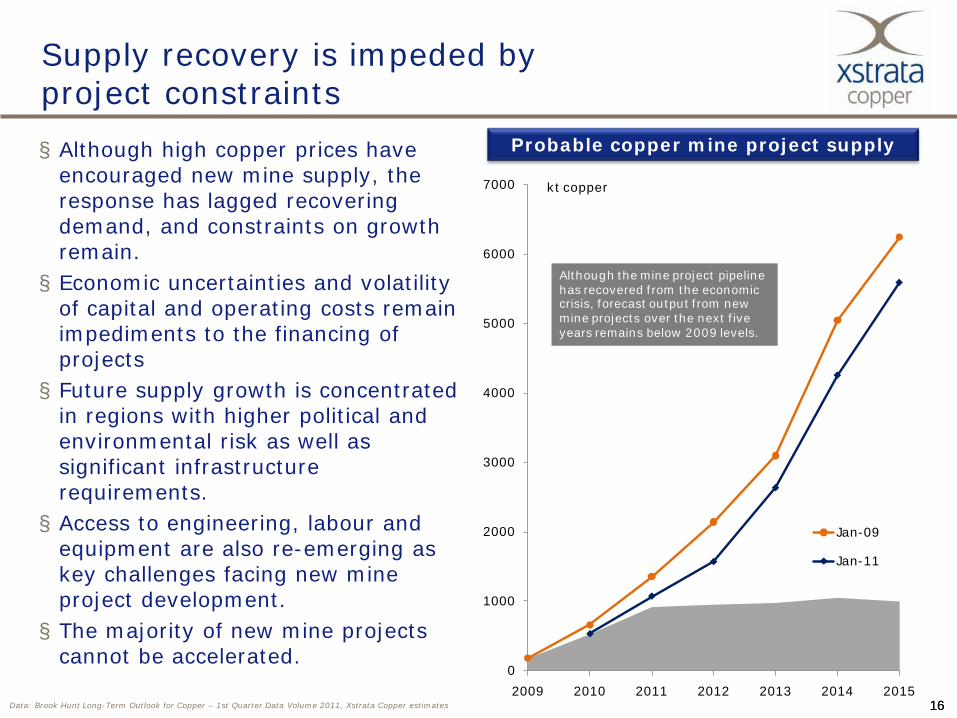

Supply recovery is impeded by project constraints

Probable copper mine project supply§ Although high copper prices have encouraged new mine supply, the response has lagged recovering demand, and constraints on growth remain. § Economic uncertainties and volatility

of capital and operating costs remain impediments to the financing of projects§ Future supply growth is concentrated

in regions with higher political and environmental risk as well as significant infrastructure requirements.§ Access to engineering, labour and

equipment are also re-emerging as key challenges facing new mine project development.§ The majority of new mine projects

cannot be accelerated.

Data: Brook Hunt Long-Term Outlook for Copper – 1st Quarter Data Volume 2011, Xstrata Copper estimates

0

1000

2000

3000

4000

5000

6000

7000

2009 2010 2011 2012 2013 2014 2015

Jan-09

Jan-11

Although the mine project pipeline has recovered from the economic crisis, forecast output from new mine projects over the next five years remains below 2009 levels.

kt copper

1717

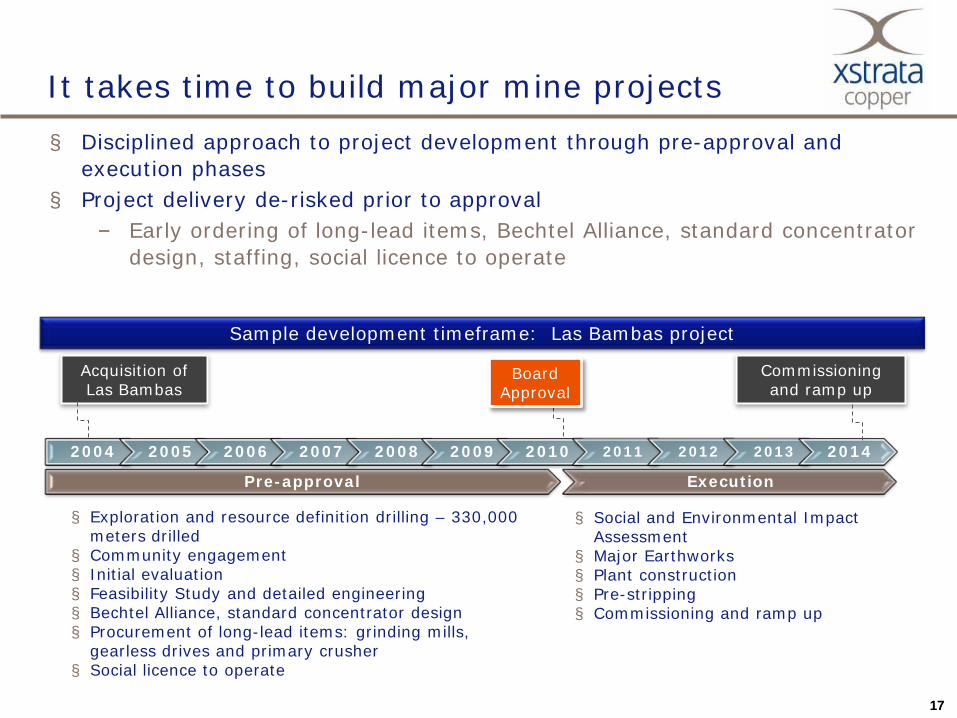

It takes time to build major mine projects§ Disciplined approach to project development through pre-approval and

execution phases§ Project delivery de-risked prior to approval

‒ Early ordering of long-lead items, Bechtel Alliance, standard concentrator design, staffing, social licence to operate

Sample development timeframe: Las Bambas project

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Pre-approval Execution

Board Approval

Acquisition of Las Bambas

Commissioning and ramp up

§ Exploration and resource definition drilling – 330,000 meters drilled

§ Community engagement§ Initial evaluation§ Feasibility Study and detailed engineering§ Bechtel Alliance, standard concentrator design§ Procurement of long-lead items: grinding mills,

gearless drives and primary crusher§ Social licence to operate

§ Social and Environmental Impact Assessment

§ Major Earthworks§ Plant construction§ Pre-stripping§ Commissioning and ramp up

1818

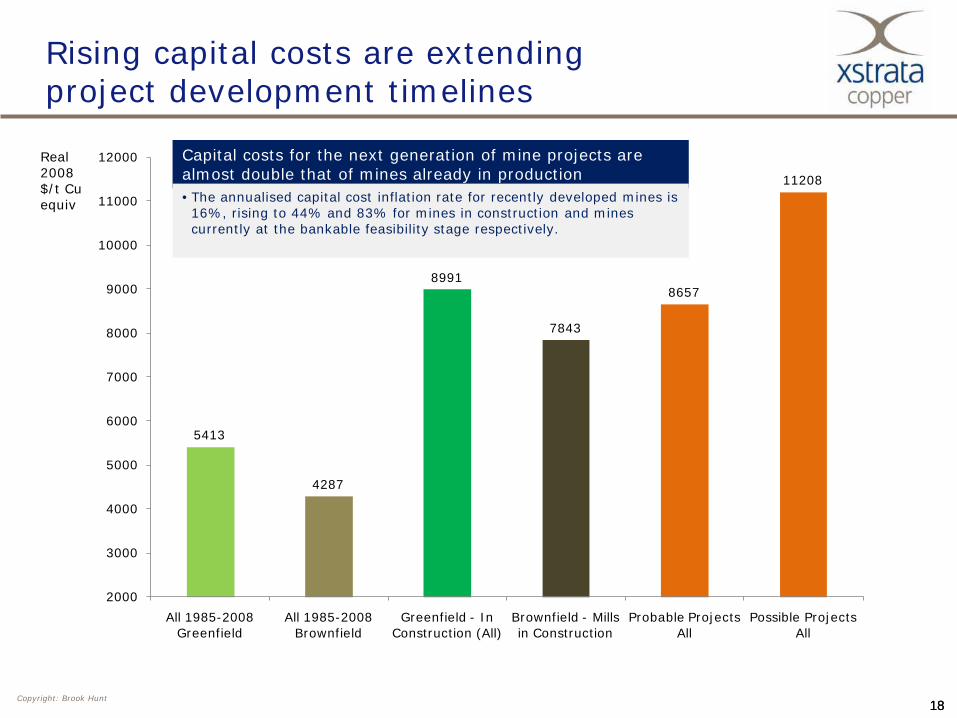

Rising capital costs are extending project development timelines

5413

4287

8991

7843

8657

11208

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

All 1985-2008 Greenfield

All 1985-2008 Brownfield

Greenfield - In Construction (All)

Brownfield - Mills in Construction

Probable Projects All

Possible Projects All

Real 2008$/t Cu equiv

Capital costs for the next generation of mine projects are almost double that of mines already in production• The annualised capital cost inflation rate for recently developed mines is 16%, rising to 44% and 83% for mines in construction and mines currently at the bankable feasibility stage respectively.

Copyright: Brook Hunt

1919

0200400600800

100012001400160018002000

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011e

net imports

production

Copper’s fundamentals remain robust

Chinese apparent consumption robust

Western PMIs point to strong demand

§ A weaker spot market in China is not necessarily indicative of weak overall demand - higher domestic production has largely offset the reduction in cathode imports over the year to date.

§ Chinese end-use and semi-fabricating data point to another robust year for copper demand.

§ Western markets are gaining strength with PMIs at multi-year highs. Semi-fabricators are reporting strong demand, particularly from the power sector.

§ Increases in scrap consumption have displaced some cathode demand, but availability is not unlimited and fabricators must compete with smelters for material.

Data: Chinese trade statistics, Analyst reports, Xstrata Copper estimates

kt

30

35

40

45

50

55

60

65

2004 2005 2006 2007 2008 2009 2010 2011

Growth

Contraction

2020

Summary: Above trend copper pricing outlook remains intact

Demand§ Demand growth remains driven by developing economies, which are

investing heavily in copper-intensive sectors such as power infrastructure and construction § Demand in mature economies will see continued growth this year as the

economic recovery broadens.§ Although high prices may encourage some demand rationing; positive

substitution is also ongoing.

Supply§ High rates of disruption and underperformance among operating mines

continue to constrain supply.§ Although high prices have encouraged new projects, development hurdles

mean the risk of delays remains high.§ In the long term, the current pipeline of projects remains insufficient to

meet demand requirements.

21

Xstrata Copper Case Study:Ernest Henry

Myles Johnston, General Manager Ernest Henry Mining

22

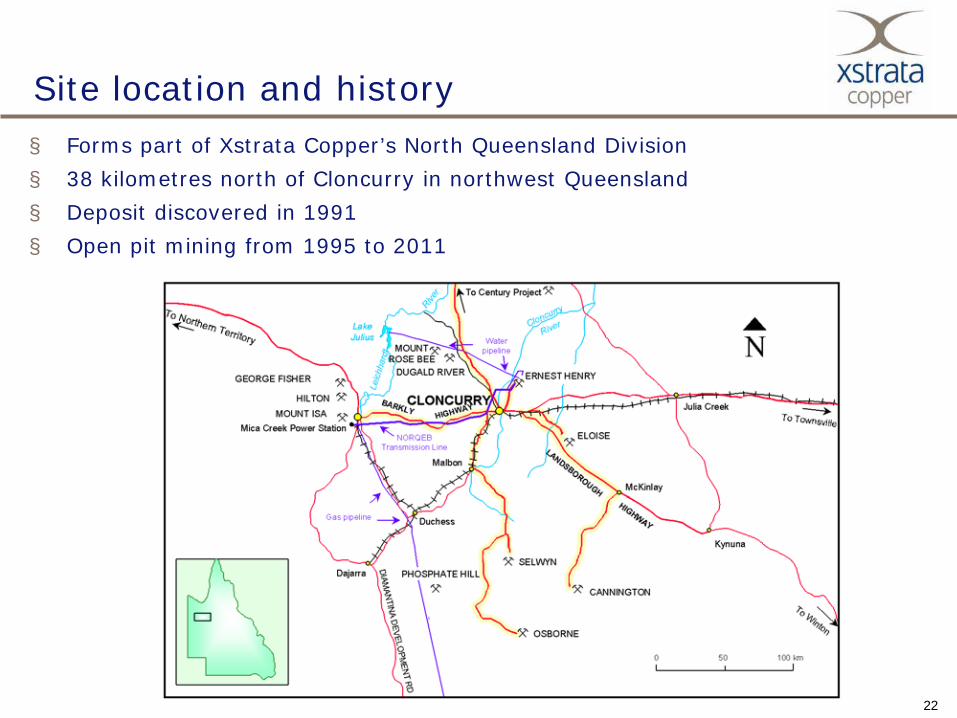

Site location and history§ Forms part of Xstrata Copper’s North Queensland Division§ 38 kilometres north of Cloncurry in northwest Queensland§ Deposit discovered in 1991§ Open pit mining from 1995 to 2011

23

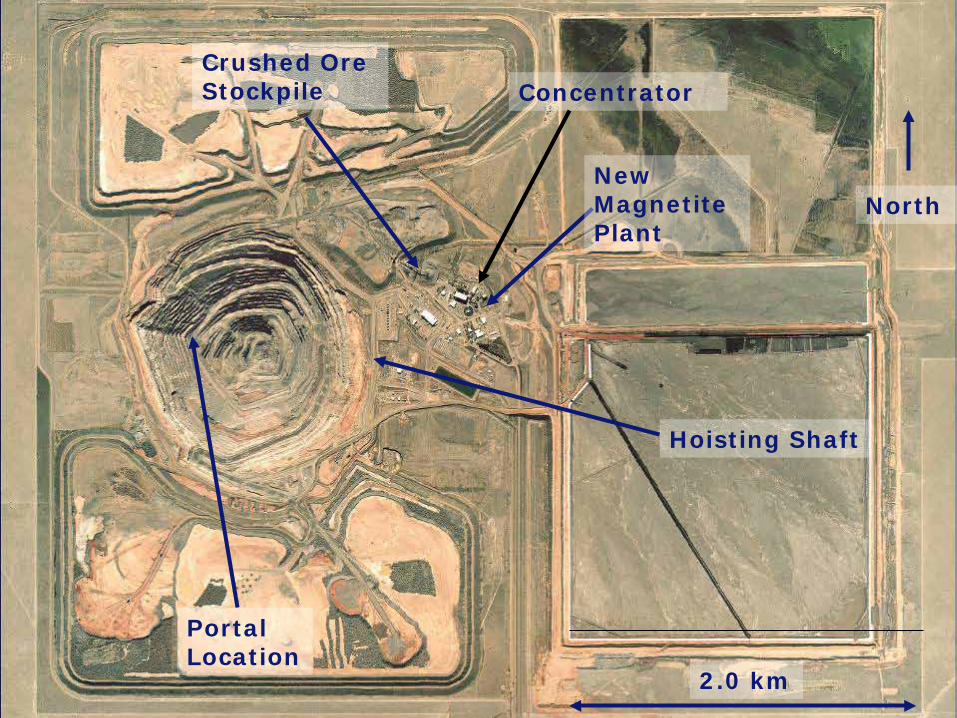

Portal Location

Hoisting Shaft

Concentrator

North

2.0 km

Crushed Ore Stockpile

New Magnetite Plant

24

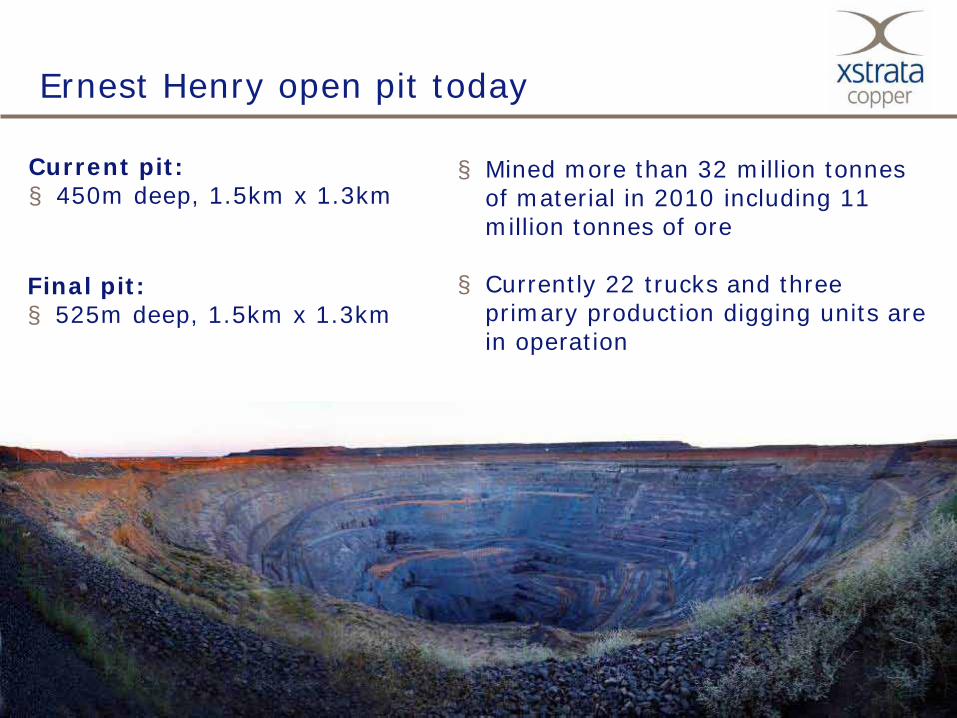

Ernest Henry open pit today

Final pit:§ 525m deep, 1.5km x 1.3km

Current pit:§ 450m deep, 1.5km x 1.3km

§ Mined more than 32 million tonnes of material in 2010 including 11 million tonnes of ore

§ Currently 22 trucks and three primary production digging units are in operation

25

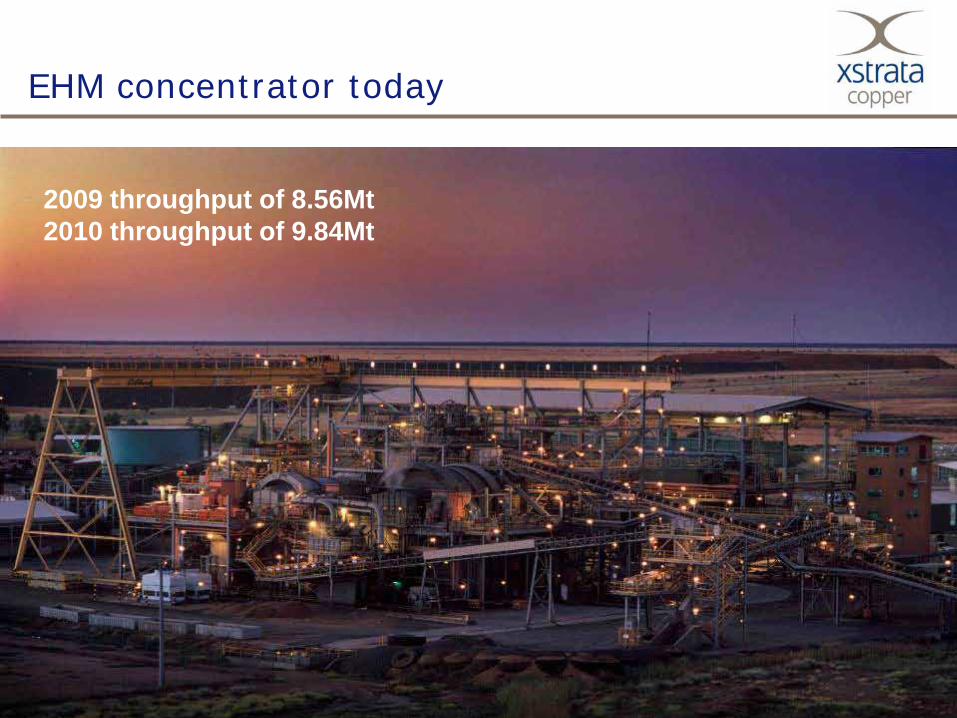

EHM concentrator today

2009 throughput of 8.56Mt2010 throughput of 9.84Mt

26

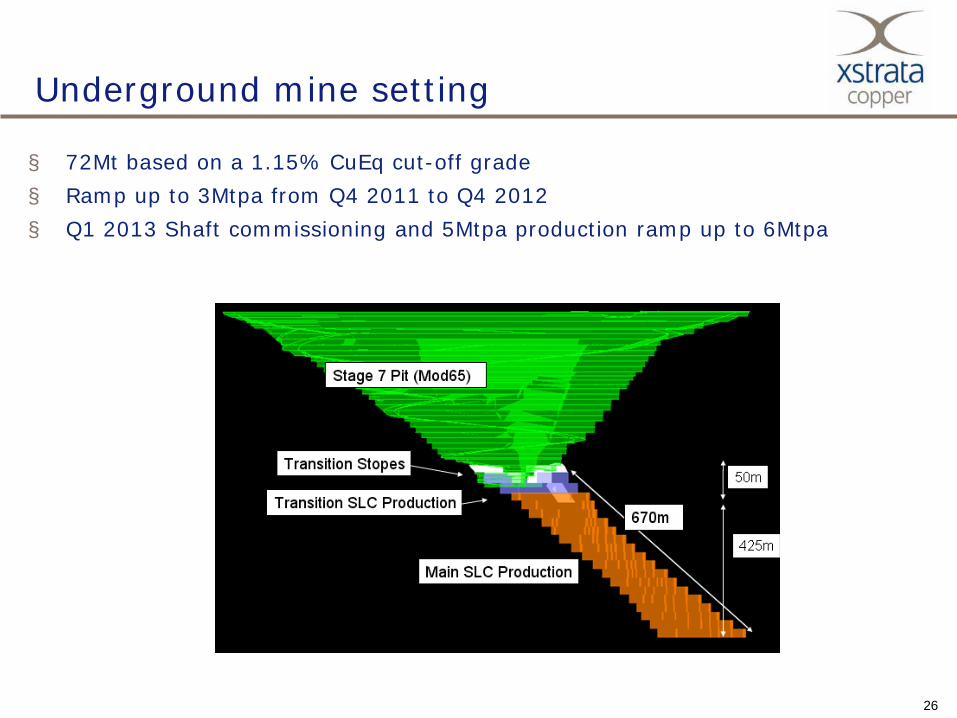

Underground mine setting

§ 72Mt based on a 1.15% CuEq cut-off grade§ Ramp up to 3Mtpa from Q4 2011 to Q4 2012§ Q1 2013 Shaft commissioning and 5Mtpa production ramp up to 6Mtpa

27

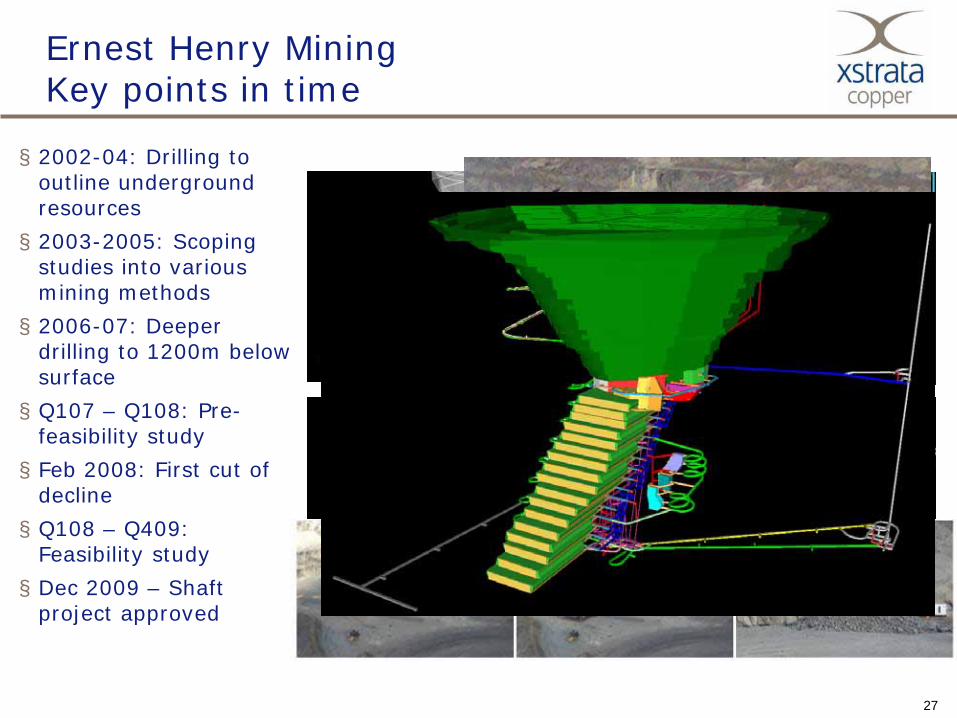

§ 2002-04: Drilling to outline underground resources§ 2003-2005: Scoping

studies into various mining methods§ 2006-07: Deeper

drilling to 1200m below surface§ Q107 – Q108: Pre-

feasibility study§ Feb 2008: First cut of

decline§ Q108 – Q409:

Feasibility study§ Dec 2009 – Shaft

project approved

Ernest Henry Mining Key points in time

28

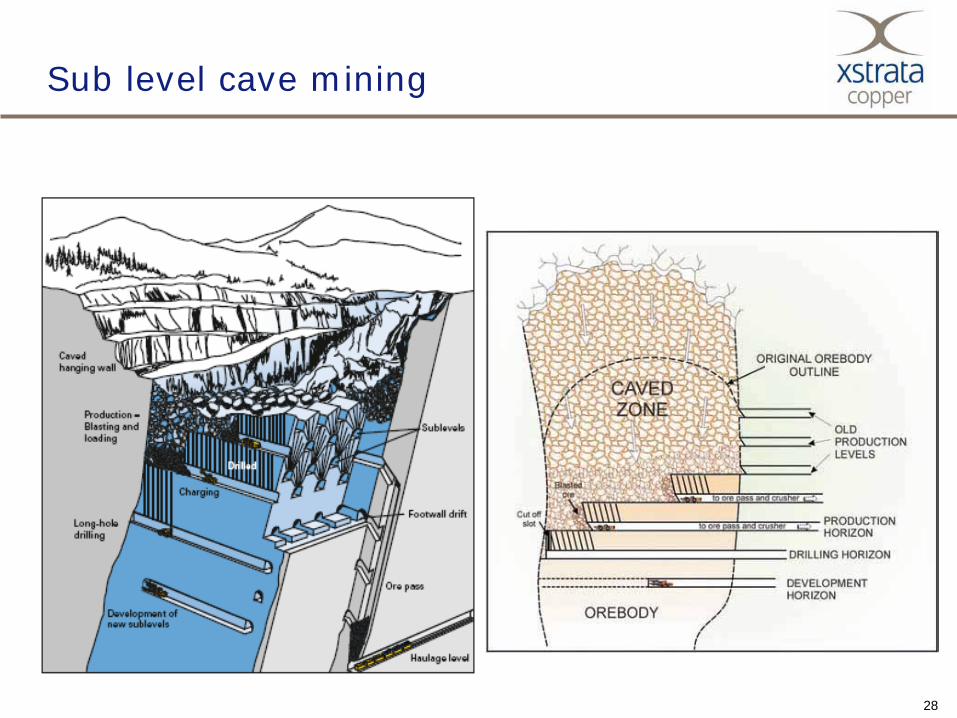

Sub level cave mining

29

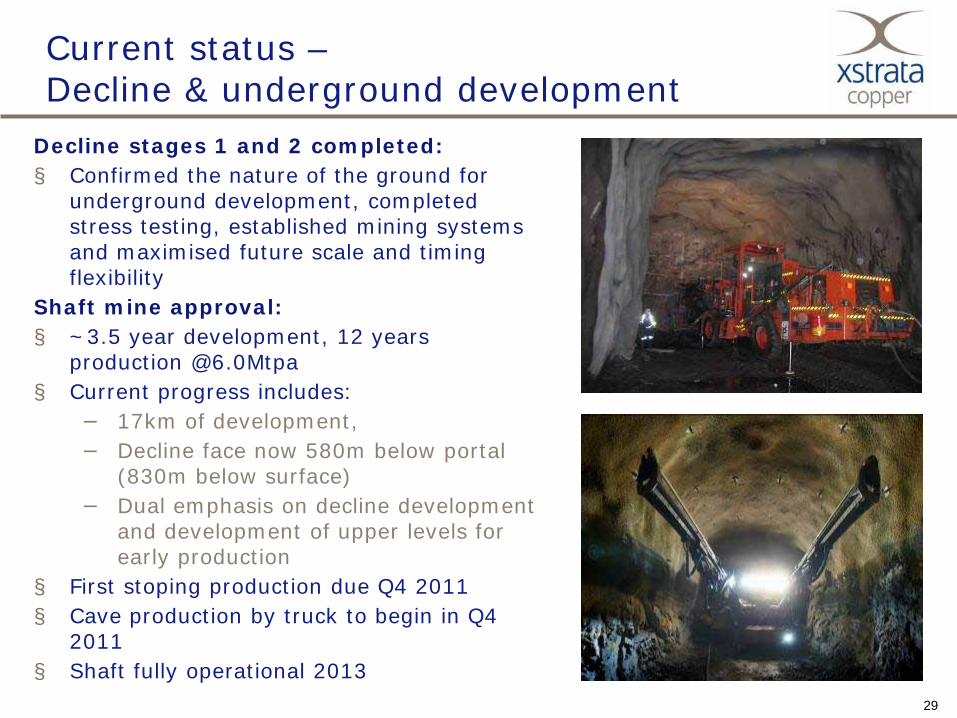

Current status –Decline & underground development

Decline stages 1 and 2 completed:§ Confirmed the nature of the ground for

underground development, completed stress testing, established mining systems and maximised future scale and timing flexibility

Shaft mine approval:§ ~3.5 year development, 12 years

production @6.0Mtpa§ Current progress includes:

− 17km of development, − Decline face now 580m below portal

(830m below surface)− Dual emphasis on decline development

and development of upper levels for early production

§ First stoping production due Q4 2011§ Cave production by truck to begin in Q4

2011§ Shaft fully operational 2013

30

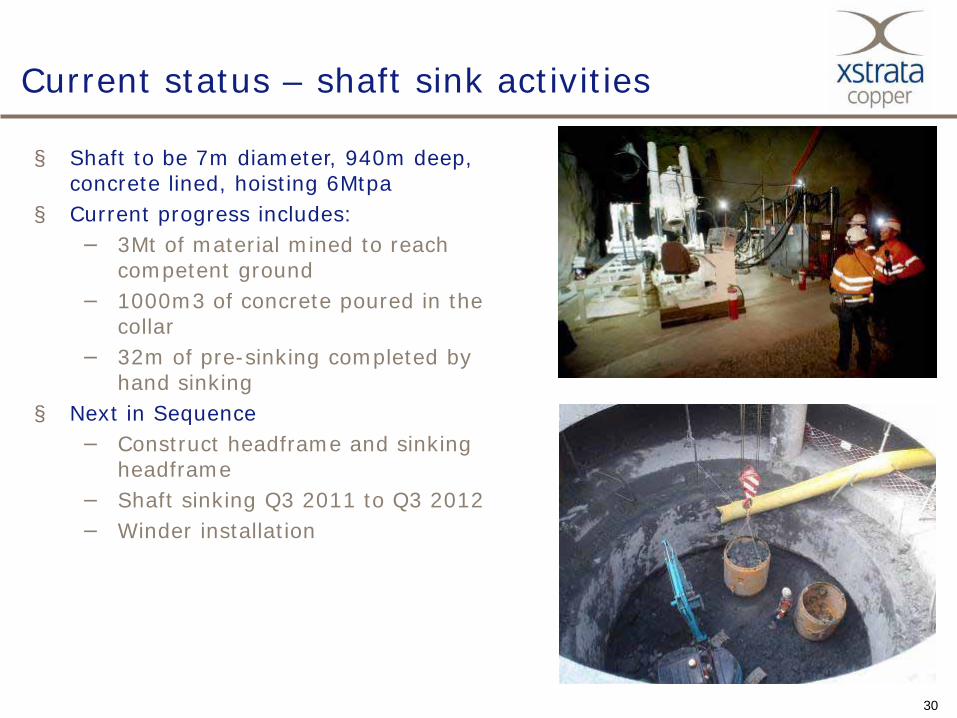

Current status – shaft sink activities

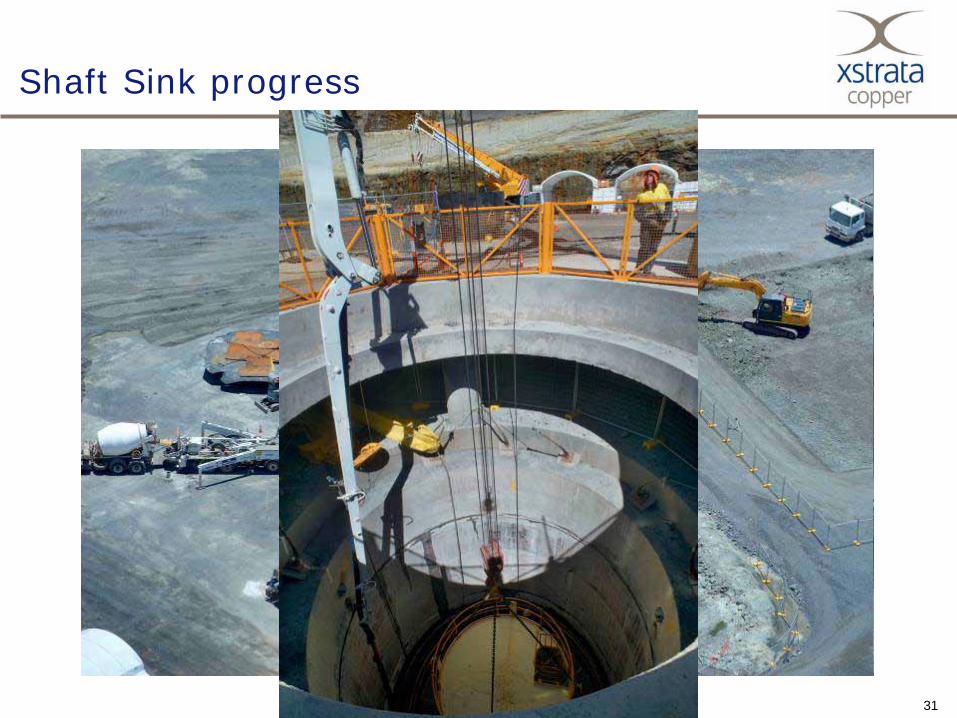

§ Shaft to be 7m diameter, 940m deep, concrete lined, hoisting 6Mtpa

§ Current progress includes:− 3Mt of material mined to reach

competent ground− 1000m3 of concrete poured in the

collar− 32m of pre-sinking completed by

hand sinking§ Next in Sequence

− Construct headframe and sinking headframe

− Shaft sinking Q3 2011 to Q3 2012− Winder installation

31

Shaft Sink progress

32

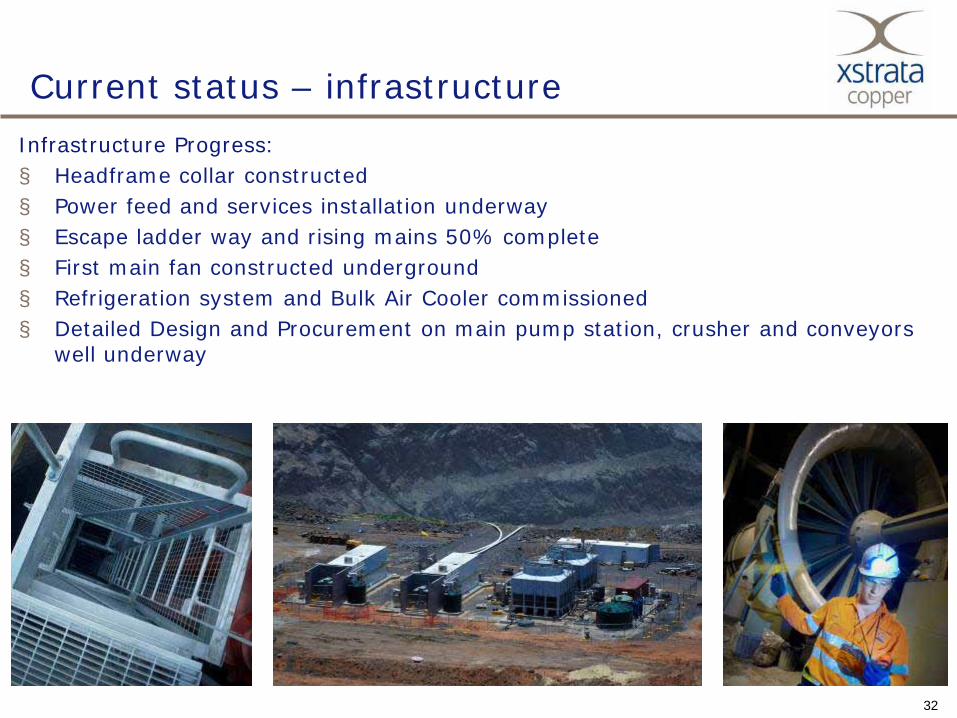

Current status – infrastructure Infrastructure Progress:§ Headframe collar constructed§ Power feed and services installation underway§ Escape ladder way and rising mains 50% complete§ First main fan constructed underground§ Refrigeration system and Bulk Air Cooler commissioned§ Detailed Design and Procurement on main pump station, crusher and conveyors

well underway

33

Magnetite plant progress

Base Plant - Dewatering Building (complete)

First Production – 31st Dec 2010

Base Plant - Extraction Building (complete)

Magnetite Filter in operation

§ Overall project 85% complete

§ Good safety performance§ Base plant and regrind civil

construction complete§ First production - 31st Dec

2010§ Commissioning and

optimisation ongoing Q1§ Regrind construction to

commence April 2011§ First rail planned Q2 2011 § Costs on budget

Regrind – civil works (complete) Mechanical works starting April

34

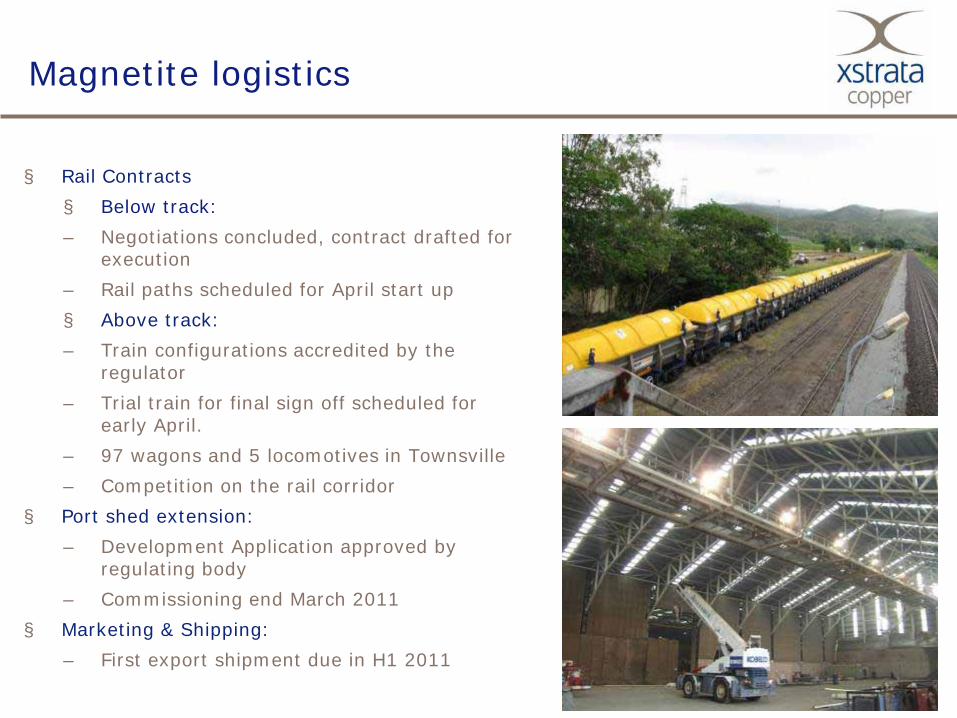

Magnetite logistics

§ Rail Contracts§ Below track: – Negotiations concluded, contract drafted for

execution– Rail paths scheduled for April start up§ Above track:– Train configurations accredited by the

regulator– Trial train for final sign off scheduled for

early April.– 97 wagons and 5 locomotives in Townsville– Competition on the rail corridor

§ Port shed extension:– Development Application approved by

regulating body– Commissioning end March 2011

§ Marketing & Shipping:– First export shipment due in H1 2011

35

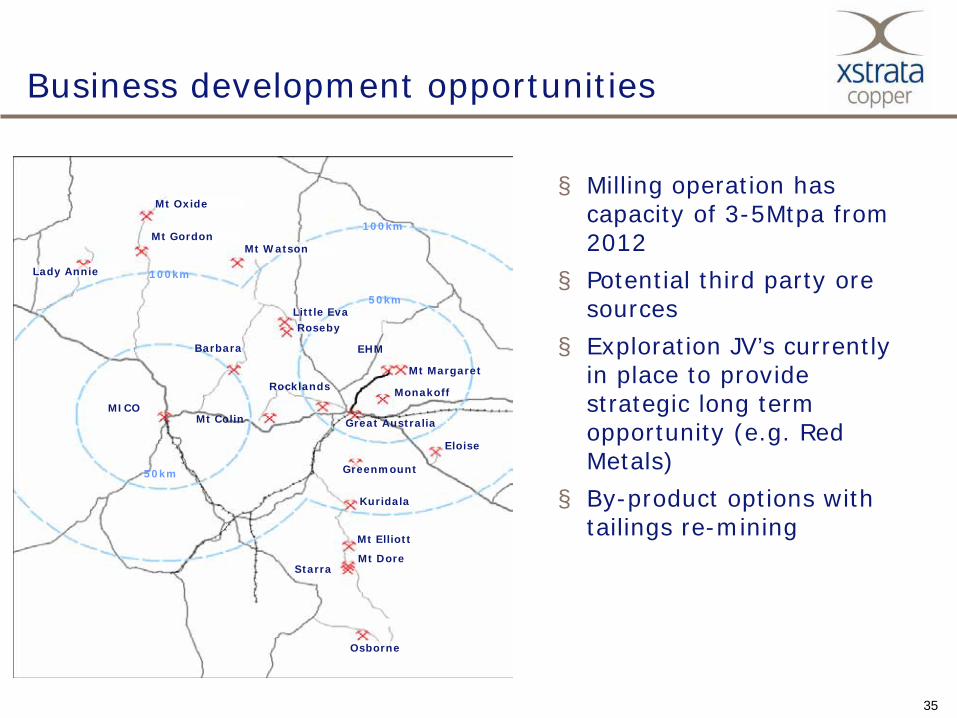

Business development opportunities

§ Milling operation has capacity of 3-5Mtpa from 2012

§ Potential third party ore sources

§ Exploration JV’s currently in place to provide strategic long term opportunity (e.g. Red Metals)

§ By-product options with tailings re-mining

Mt Oxide

Mt Gordon

Lady Annie

Mt Watson

Roseby

EHM

Mt Margaret

Eloise

Osborne

StarraMt Dore

Mt Elliott

Kuridala

Greenmount

Mt Colin

Rocklands

Great Australia

Barbara

MICOMonakoff

50km

50km

100km

100km

Little Eva

36

SD Commitment Key Initiatives§ Mine Transition to underground§ Environmental initiatives/technology

– IsaMillTM energy efficiency§ Local Employment§ Indigenous Traineeship§ New XCPPNQ partnerships

37

Questions?

38

Xstrata plcBloomberg: XTA LN Equity

Reuters: XTA.L

Websites: www.xstrata.com

www.xstratacopper.com

Xstrata Copper Head Office:Level 9, Riverside Centre

123 Eagle Street, GPO Box 1433Brisbane, Queensland