transform purdue general ledger go-live (7/9/2018)€¦ · transform purdue general ledger go-live...

TRANSCRIPT

TRANSFORM PURDUEGENERAL LEDGER GO-LIVE

(7/9/2018)

Department Heads and Deans

Presented - July 30, 2018

AGENDA

Post Go-Live Assessment Finance Structure and Metrics Financial Transparency – Faculty Allocations New Scholarship Accounting Process Gift Consolidation Transfers Other Key Process Changes Q & A

2

TRANSFORM PURDUE - 21 DAYS POST GO-LIVE

3

What Has Gone Well? What are pain points?

• Major systems and interfaces worked as expected to support ongoing operational needs

• Validation of accounts pre-/post-conversion has created new transparency and understanding across central offices and business units

• Initial go-live reporting requirements have been met with updated suite of reports released

• Feedback, Incident reporting has been effective and resolution of problems is ongoing

• Training / Understanding of both system and process changes is always a challenge

• Financial postings into new account structures are a direct result of account mappings and we are finding issues that need to be resolved…

• While overall systems work we have pain experienced by users that are a result of system defects or problems that we are addressing during this stabilization period

• Perfection will take some time…..everyone is learning a new way of operating

TRANSFORM PURDUE – POST GO LIVE INCIDENT METRICSIncidents Trending in Right Direction

4

48

32

22

1

2820

9

0

19

0

10

20

30

40

50

7/8/2018 7/15/2018 7/22/2018 7/29/2018

35

2

# Incidents Reported

47

147

0

24 26

0

Logged Incidents

334

104

230

0

50

100

150

200

250

300

350

OpenResolved

# Incidents

Incidents

-69%% of Incidents

Closed (71% last week)

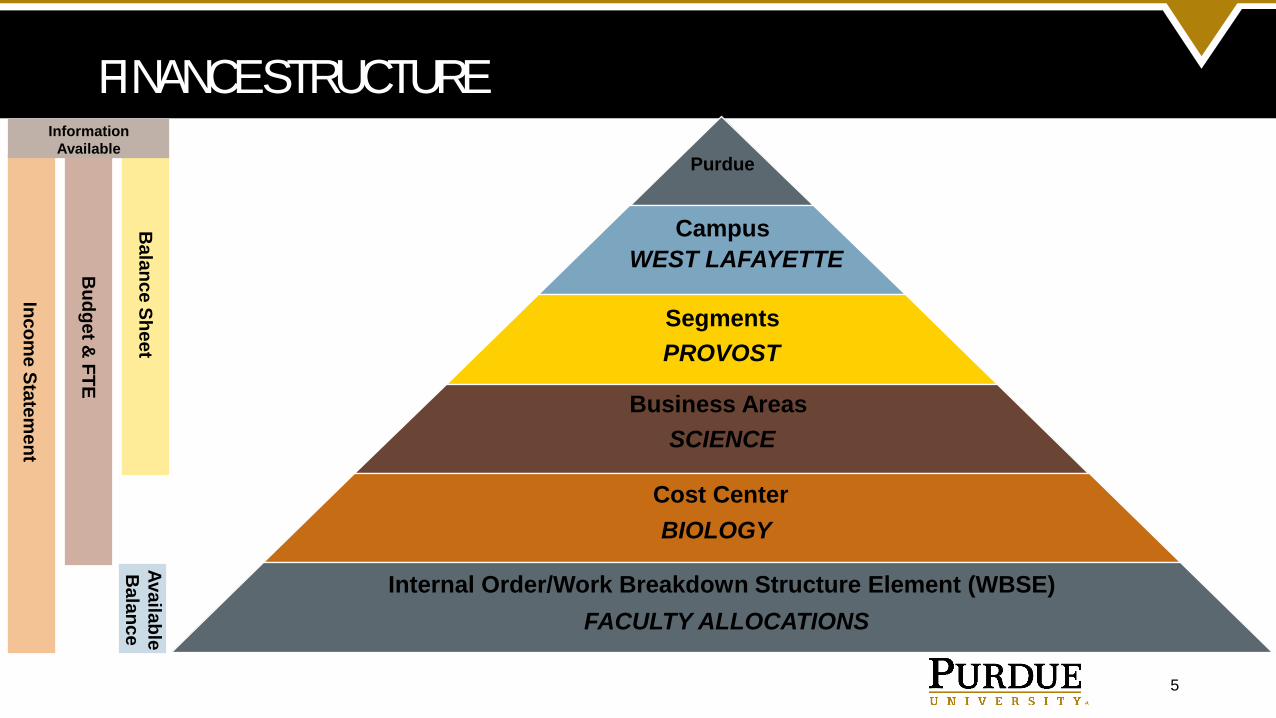

FINANCE STRUCTURE

5

Internal Order/Work Breakdown Structure Element (WBSE)

Cost Center

Business Areas

Segments

Campus

Purdue

WEST LAFAYETTE

PROVOST

SCIENCE

BIOLOGY

FACULTY ALLOCATIONS

Information Available

Income Statem

ent

Budget &

FTE

Balance Sheet

Available B

alance

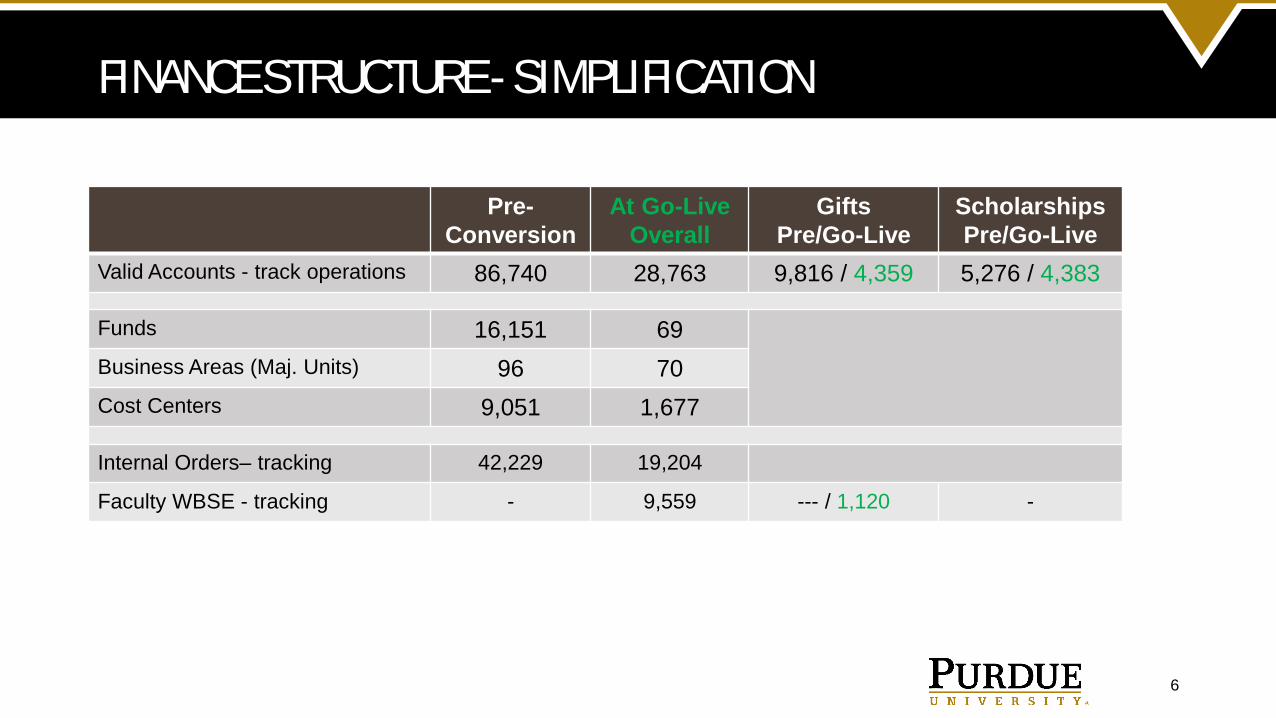

FINANCE STRUCTURE - SIMPLIFICATION

Pre-Conversion

At Go-LiveOverall

GiftsPre/Go-Live

ScholarshipsPre/Go-Live

Valid Accounts - track operations 86,740 28,763 9,816 / 4,359 5,276 / 4,383

Funds 16,151 69Business Areas (Maj. Units) 96 70Cost Centers 9,051 1,677

Internal Orders– tracking 42,229 19,204

Faculty WBSE - tracking - 9,559 --- / 1,120 -

6

FACULTY ALLOCATIONS – DEFINITIONS OF NODES

7

Grants

• Sponsored programs tied to faculty

• Same as reported in GM AIMS

Discretionary

• Examples:• Research

discretionary• Faculty

Scholar Allocations

• Grant residuals

• Digital Education residuals

• Faculty Awards• Professorships

• No restrictions except for University policy

Start-Up

• Faculty member start-up allocations

• Plan represents the entire package

• Reporting now available for “End Date” of package

Restricted

• Examples:• Research

Seed Grant• Research Lab

Upgrade• IMPACT

Allocations• Professorships

• Use of funds limited for specific purpose or types of expenses

FINANCE STRUCTURE – FACULTY ALLOCATIONSNew Transparency for Faculty Activities

OverallFederal

Appropriations Discretionary Start-up RestrictedFaculty WBSE –Tracking

9,559 1,817 5,177 895 1,670

# Faculty with Allocations

2,789 490 2,454 592 1,110

Average # Allocations per Faculty

3.4 3.7 2.1 1.5 1.5

8

FINANCE STRUCTUREHOW DOES THE NEW STRUCTURE BENEFIT THE UNITS? The structure is now consistent across the entire Purdue System

‒ Simplifies Reporting‒ Allows for separation of Department Operating Funds and Faculty Allocations‒ Shows available/flexible funds for use at Department Head’s discretion‒ Financial information will be accessible and understandable to other business

office staff during turnover Data and reporting is available real time Response time to serve our faculty is greatly reduced

9

NEW FINANCIAL TRANSPARENCY EXAMPLESAutomated Reports/Real Time/Consistent Across Units Available Balance Listing

‒ Push Button Access‒ Financial Units and Sub-Units‒ Replaces 100s or 1000s of manual steps or excel spreadsheets‒ Clarity into who “owns” an allocation

Faculty Allocations‒ Faculty Portfolio of Balances and Activity‒ Clarity of Start-up and Professorships‒ Insights into Discretionary vs. Restricted funds

10

COLLEGE OF PHARMACY – PRE CONVERSIONAvailability of ReportingFour departments & six sub-departments

‒ 269 different cost centers

11

Availability of Reporting

Automated Manual

GLOBAL HEALTH EXAMPLE – PRE-CONVERSIONReporting is Entirely Manual

12

• Clerk exports 25 individual transaction reports from SAP to Excel • Copies and pastes account balances to a summary tab• Month-end spreadsheet emailed to program leadership

• Usually middle of the next month (if it happens)

GLOBAL HEALTH EXAMPLE – POST-CONVERSIONReporting is Automated/Available Real Time

13

• Now Real-time reporting with no manual intervention• Interactive and drillable for more granular details• Consolidated accounts by ~50%

VISIBILITY OF ACCOUNT OWNERSDepartment / Faculty Allocations – No pre-conversion visibility

14Position responsible for

account

FACULTY ALLOCATION REPORTINGAutomated/Real Time

15

Faculty ABCDEFGHIJ

FACULTY ALLOCATIONS – START UP

16

2 Start Up I/Os(Accounts)

Validity Date

Package Activity Plan Balance

Start up – Next Level of Detail

Faculty A

Faculty A – Start –up Ext/Engage

Faculty A – Start –up Research

Faculty A Faculty A – Ext/Egage

Faculty A – Research

FACULTY ALLOCATIONS – START UP

17

Back to the Department View – How are we funded?

Start up Package Fully Funded

Unfunded portion of Start Up

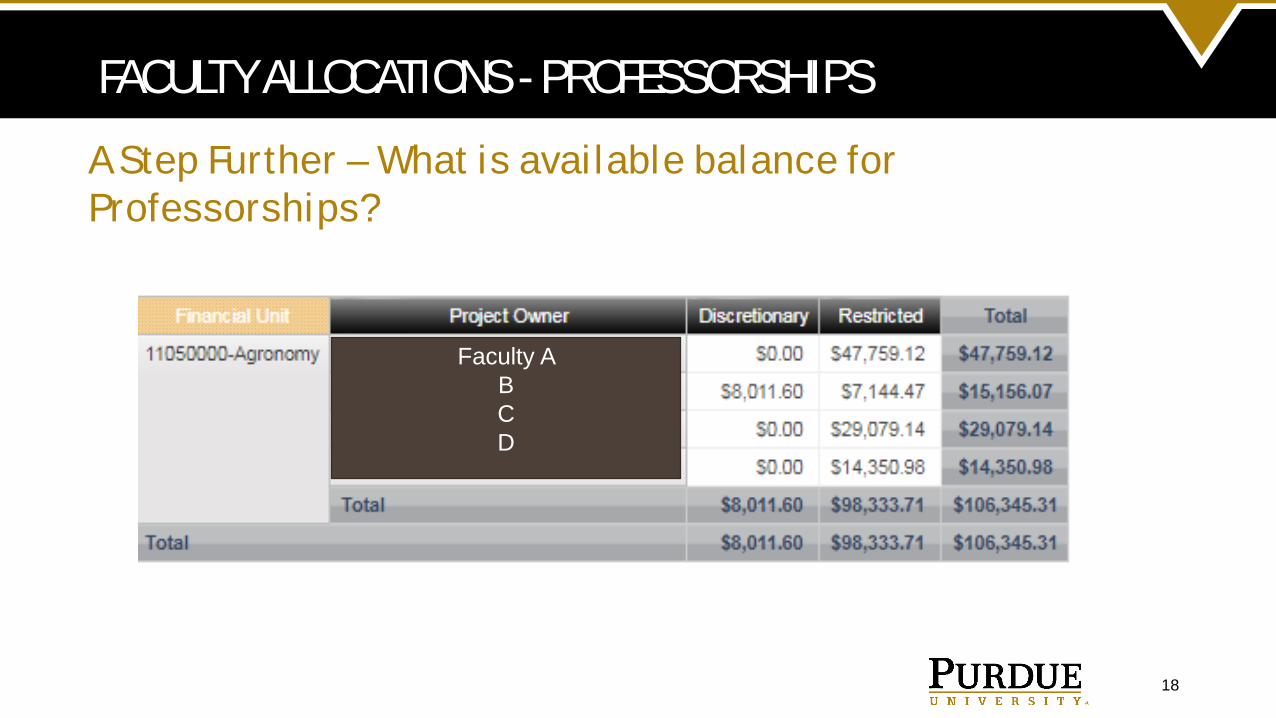

FACULTY ALLOCATIONS - PROFESSORSHIPS

18

A Step Further – What is available balance for Professorships?

Faculty A BCD

REPORTING – UPCOMING RELEASES

• Statement of Financial Activities Sep 1

• Operating Classifications• Departmental – Operating• Departmental – Allocated• Income Producing• Restricted – Gifts• State & Federal Appropriations• Student Aid

• Department Head Dashboard TBD

19

What can you expect in the future?

What units and activities are responsible for the $4.6M year-end balance for a Major Unit (College)?

Statement of Financial Activities

20

FY2017 Year-end Balance

Department NameUnrestricted to

DeptRestricted-State Line

Income Producing Scholarships Restricted Gifts Faculty Grand Total

Polytechnic Anderson $ 106,264.62 $ (222,987.17) $ 10,735.45 $ (509.02) $ (106,496.12)

Polytechnic Columbus $ 1,678.34 $ (7,025.66) $ 5,129.07 $ 6,441.49 $ 12,527.04 $ 21,583.06 $ 40,333.34

Polytechnic Indianapolis $ 2,000.00 $ 71,881.76 $ 10,000.00 $ 259.73 $ 84,141.49

Polytechnic Kokomo $ 20,283.14 $ 54,949.43 $ 6,648.51 $ 139,677.60 $ 29,733.23 $ 251,291.91

Polytechnic Lafayette $ 142,645.72 $ 52,326.16 $ (29,192.72) $ 9,433.88 $ 175,213.04

Polytechnic New Albany $ 46,697.87 $ 117,474.62 $ (5,804.85) $ 8,355.49 $ 9,557.66 $ 24,801.92 $ 201,082.71

Polytechnic Richmond $ 9,964.79 $ 87,464.97 $ 122.38 $ 23,315.68 $ 120,867.82

Polytechnic South Bend $ 28,112.30 $ 49,152.53 $ 21,864.89 $ 10,759.98 $ 312,541.75 $ 35,473.40 $ 457,904.85

Polytechnic Statewide Technology $ 35,913.08 $ 3,544,831.76 $ 3,497.00 $ (214,124.26) $ 1,432.43 $ 3,371,550.01

Polytechnic Vincennes $ 597.50 $ (54,271.39) $ 21,329.17 $ 6,093.23 $ (26,251.49)

$ 394,157.36 $ 3,693,797.01 $ 33,471.07 $ (38,031.87) $ 334,626.45 $ 151,617.54 $ 4,569,637.56

Depart. ABCDEFGH

GIFTS & SCHOLARSHIPS

21

Provost, University Development Office and Treasurer have been working on a better way to manage scholarships and gifts.

Goals ‒ Simplify account structure

‒ Effectively award and steward scholarships

‒ Maximize return on cash balances

FY 2018 Budget. $ in millions

0

5

10

15

20

25

30

35

40

45

General fundallocation

Purdue Moves EndowmentDist

Gifts Reserves Summer stateapprop

Enrollment Mgt Sources - $75.6

0

2

4

6

8

10

12

14

Colleges Sources - $19.8

Large percentage of accounts with small balances … significant administrative burden

23

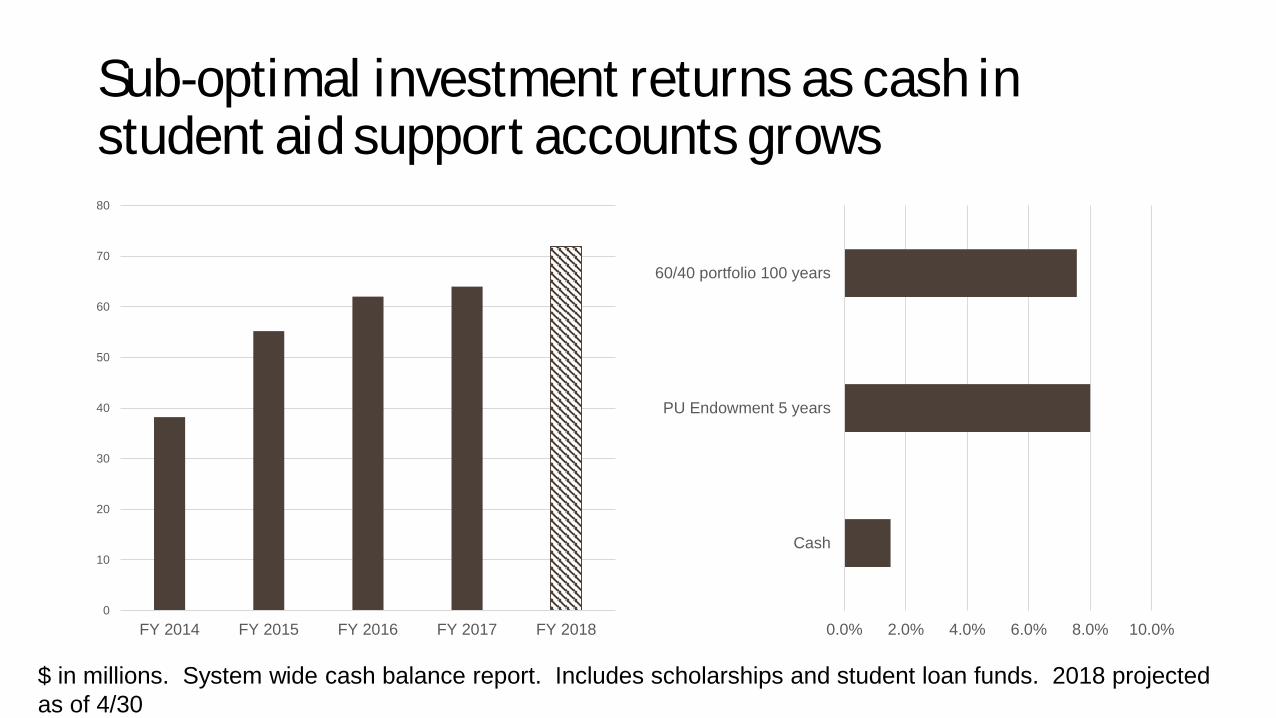

Sub-optimal investment returns as cash in student aid support accounts grows

0

10

20

30

40

50

60

70

80

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

$ in millions. System wide cash balance report. Includes scholarships and student loan funds. 2018 projected as of 4/30

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

Cash

PU Endowment 5 years

60/40 portfolio 100 years

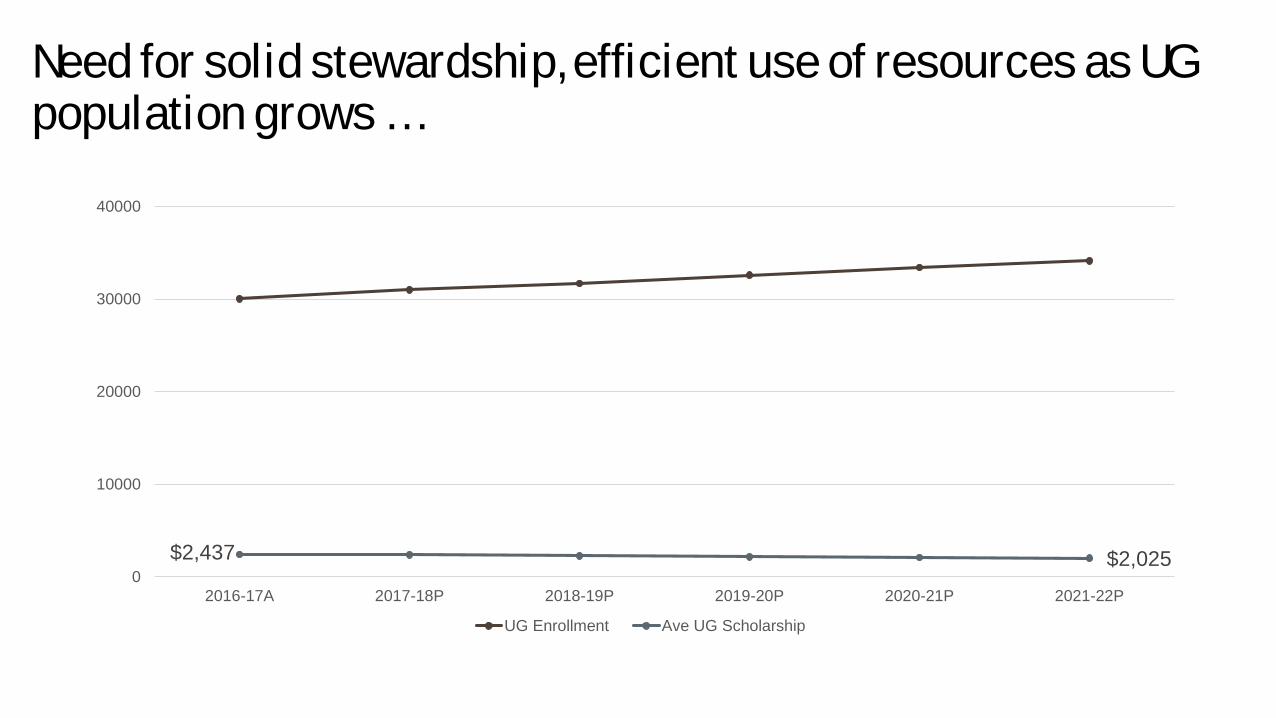

Need for solid stewardship, efficient use of resources as UG population grows …

$2,437 $2,025 0

10000

20000

30000

40000

2016-17A 2017-18P 2018-19P 2019-20P 2020-21P 2021-22P

UG Enrollment Ave UG Scholarship

Endowed Scholarships – New process

Student Information

System (SIS)

SAP -Internal Order Tracking

Expense pushed to SAP

Endowment - PRF

Distribute cash to cover awards (1:1)

Excess distribution above expenses reinvested back

in endowment

College/Unit TrackingAward Determination @ Colleges/Units

• Units maintain role in selection of recipients and donor stewardship• Units budget up to the Endowment spending policy; actual expenses pushed

to SAP• Ensures excess cash reinvested to maximize return• Requires only 1 financial account for every Business Area (College/Unit)

• 25-30 accounts for University

Non-endowed Scholarships – New Process

• Units maintain selection and stewardship of unrestricted support account

• Requires only 1 financial account for every Academic cost center• ~250 accounts for University

Review to Determine

• Spend and close or consolidate

• Maintain until donor commitment complete

Step 1: UDO Review of Existing

Accounts

Step 2: Account Changes Fall 2018

Department Account Structure

• 1 unrestricted support account

• All income (gifts) deposited here

Step 3: Existing Cash Balances (in

accounts)

Enrollment Management (EM) and Colleges/Units

• Any Unit accounts to spend, close or consolidate – funds transferred to the unrestricted account

• Activity and cash balance in unrestricted accounts monitored annually to ensure timely use

• If not timely used, excess funds may be periodically transferred to EM or University wide quasi endowment for scholarships

GIFTS & SCHOLARSHIPS

Separate accounts for new non-endowed gift and scholarship revenues will not be created, except by approval of the VP for Development and Comptroller.‒ This does not include voluntary support (gifts restricted to faculty administered

through SPS) For new non-scholarship endowments, new support accounts will not

automatically be established by PRF.‒ Units will first be asked if they have an existing support account with the same

purpose/restrictions as the new endowment or if a new account is needed.‒ Quick responses to these questions are necessary.

28

TRANSFERS

There are significant administrative costs associated with transfers ‒Over 49,000 line items of transfers ‒ 71% of transfers line items are processed as Transfers-Other

Implementing some new guidelines will allow more transparency and allow to us gather more data around transfers‒ Example: directly transferring funds from the area funding‒ Specific transfer categories

29

TRANSFERS

30

We need assistance from Department Heads and Deans to reduce and simplify the number of transfers‒ Track meaningful activity – not nickel and dimes ‒Splitting of Sponsorships/Events by areas must be minimum $1,000

Generally speaking, transfers less than $1,000 will not be permitted except in the following circumstances:‒Conference & Residual Transfers‒ Impactful Faculty/Staff Allocations ‒Account Closing & Consolidation‒Cost Sharing

FISCAL APPROVAL & WORKFLOWSWhat will Faculty and Department Heads approve in SAP?

31

Faculty and Department Heads will approve items via electronic workflow:‒ Faculty will approve subcontract payments via electronic workflow

• Today this approval is handled via email• Faculty with active grants that have a subcontract have been notified of the process

change and the requirement for Two-Factor Authentication.

‒ No additional or significant workflow changes impacting our faculty or departments related to this. Workflow impacts will be greater with HCM project activities and will be reviewed with you separately.

FISCAL APPROVAL & WORKFLOW

32

Annual External Transactions Count Value

% of ExternalSpend

Transactions < $1,000 405,000 $75M 7%

Transactions > $1,000 65,000 $945M 93%

TOTAL 470,000 $1,020M

Fiscal Approver for <$1,000 Transactions No Longer Required• In the past we have spent the majority of the effort on a small percentage of spend

• Post – audits through standard reports will be used to review transactions

FISCAL APPROVAL & WORKFLOW Ariba Purchase Orders

‒ Requisitions < $1,000 will not require fiscal approval. • However in most departments, business office staff will still be entering orders• Non-business office users that consistently use ARIBA can continue to use ARIBA

but will be responsible for the orders‒ Other special commodity approvers will remain (regulatory and Information

Technology)‒ If a requestor cannot produce accurate POs < $1,000, the Ariba Requestor role

should be removed. Concur approval process has not changed Direct Invoice Vouchers are now routing electronically – no paper!

33

34