training - presentation 28.02

TRANSCRIPT

Training session

EU Funded Grant Agreements in Nepal

FEBRUARY 2013

EUROPEAN UNION

Training session – February 2013Page 1

European Union

Agenda

► Welcome► Introduction► Grant Contracts► Expenditure verifications► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 2

European Union

Agenda

► Welcome► Introduction► Grant Contracts► Expenditure verifications► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 3

European Union

Introduction Current Programme and Funding sources

► Country Programme (2011-2013)► Focal sector 1: Education► Focal sector 2: Stability, Peace Building and Governance► Focal sector 3: Trade and Economic Capacity Building

► Thematic / Regional instruments (3 “types” of Calls):► Non-state Actors and Local Authorities► European Instrument for Democracy and Human Rights

► Food Security Thematic Programme/ EU Food Facility► Environment, Sustainable Development and Natural Resources► Investing in People► Migration and Asylum

► Regional Programme

Training session – February 2013Page 4

European Union

IntroductionProgrammes for 2011-2013

► Focal Sector 1: ► School Sector Reform Programme

€ 31.6 million (NPR 3.6 billion)

► Focal Sector 2 ► Support to the Election Commission

€ 8 million (NPR 925 million)► PFM Reform Programme

€ 10 million (NPR 1.16 billion)

► Focal Sector 3 ► Trade programme

€ 6 million (NPR 694 million)

Training session – February 2013Page 5

European Union

IntroductionThematic / Regional instruments

► European Instrument for Democracy and Human Rights : €1,5 million call in 2012

► Non-state Actors and Local Authorities: about €2 million a year –seek complementarity with Country Programme

Training session – February 2013Page 6

European Union

IntroductionQuizz

► True or false?

► The objective of an audit is to express an opinion on the Financial report � True

► All reports prepared by auditors contain an audit opinion� False

Training session – February 2013Page 7

European Union

Introduction Basic concept : Audit vs Expenditure verification

� To form an opinion on the financial statements based on an evaluation of the conclusions drawn from the audit evidence obtained.

� To express clearly that opinion through a written report that also describes the basis for that opinion.

ISA 700

► In an audit, the objectives of the auditor are:

Training session – February 2013Page 8

European Union

Introduction Basic concept : Audit vs Expenditure verification

► In an Expenditure verification, the objectives are:

� to carry out procedures of an audit nature to which the auditor and the entity and any appropriate third parties have agreed and to report on factual findings.

� As the auditor simply provides a report of the factual findings of the agreed-upon procedures, no audit assurance is expressed

� The report user forms his own opinion based on the factual information reported by the audit professional

ISRS 4400

Training session – February 2013Page 9

European Union

► Main differences

IntroductionBasic concept : Audit vs Expenditure verification

Audit (ISA 700) Expenditure verification (ISRS 4400)

Audit opinion report Report of factual findings

Reasonable assurance No assurance expressed / No opinion

The auditor uses professional judgement to design type, nature and extent of testing

The auditor uses professional skills and carries out agreed-upon procedures

Audit report is public The Report may be used only by the parties concerned

Training session – February 2013Page 10

European Union

Agenda

► Welcome► Introduction► Grant Contracts► Expenditure verifications► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 11

European Union

Grant ContractOverview

► Main articles:► Article 1 – Purpose of the Action► Article 2 – Implementation period► Article 3 – Financing of the Action► Article 4 – Obligation to submit Narrative and Financial reports► Article 5 – Contact addresses► Article 6 – Annexes ► Article 7 – Other specific conditions

Training session – February 2013Page 12

European Union

Grant contractsList of the annexes

► Annexes:► Annex I: Description of the Action► Annex II: General Conditions applicable to European Community-financed

grant contracts for external Actions► Annex III: Budget for the Action► Annex IV: Contract award procedures► Annex V: Standard request for payment and financial identification form► Annex VI: Model narrative and financial report► Annex VII: Model report of factual findings and terms of reference for an

expenditure verification of an EC financed grant contract for external actions

► Annex VIII: Model financial guarantee

Training session – February 2013Page 13

European Union

Grant contractsAnnex I: Description of the Action

► Information about the Action and the Beneficiary such as:► Title, location and duration of the Action► Main and specific objectives of the Action► Relevance, description and effectiveness of the Action► Methodology, etc

The annex I is usually part of the offer submitted by the beneficiary

Training session – February 2013Page 14

European Union

Grant contractsList of the annexes

► Annexes:► Annex I: Description of the Action► Annex II: General Conditions applicable to European Community-

financed grant contracts for external Actions► Annex III: Budget for the Action► Annex IV: Contract award procedures► Annex V: Standard request for payment and financial identification form► Annex VI: Model narrative and financial report► Annex VII: Model report of factual findings and terms of reference for an

expenditure verification of an EC financed grant contract for external actions

► Annex VIII: Model financial guarantee

Training session – February 2013Page 15

European Union

Grant contractsAnnex II: General Conditions – Important clauses

► General and administrativeProvisions

� Article 2 – Obligation to provide information and financial and narrative reports

� Article 6 – EU visibility� Article 9 – Amendment of the

contract� Article 11 – Implementation period

of the Action, extension, suspension, force majeure and end date

► Financial Provisions

� Article 14 – Eligible costs� Article 15 – Payment and interest

on late payment� Article 16 – Accounts and

technical and financial checks� Article 17 – Final amount of

financing by the Contracting Authority

Financial provisions are key contractual information

Training session – February 2013Page 16

European Union

Grant contractsAnnex II: Financial provisions (Article 14)

► Article 14► Article 14.1 – “Eligible costs are costs actually incurred by the beneficiary of this grant

which meet …”

► Article 14.2 – “Subject to the above and where relevant to the provisions of Annex IV being respected, the following direct costs of the Beneficiary and his partners shall be eligible…”

► Article 14.3 – “A contingency reserve not exceeding 5 % of the direct eligible costs may be included in the Budget of the Action. It can be used only with the prior written authorisation of the Contracting Authority”.

► Article 14.4 – “A fixed percentage not exceeding 7% of the total amount of eligible costs of the Action may be claimed as indirect costs to cover the administrative overheads incurred by the Beneficiary for the Action….”

► Article 14.6 – “The following costs shall not be considered eligible (see list)”

Training session – February 2013Page 17

European Union

Grant contractsAnnex II: Financial provisions (Article 15)

► Article 15► Article 15.6 – “A report on the verification of the Action’s expenditure, produced by an

approved auditor who is a member of an internationally recognised supervisory body for statutory auditing, shall be attached to…”

► Article 15.9 – “The Contracting Authority shall make payments in the currency of the country to which it belongs or in euro, in accordance with the Special Conditions”

Training session – February 2013Page 18

European Union

Grant contractsAnnex II: Financial provisions (Article 16)

► Article 16► Article 16.1 – “The Beneficiary shall keep accurate and regular accounts of the

implementation of the action using an appropriate accounting and double-entry book-keeping system…”

► Article 16.2 – “The Beneficiary will allow the European Commission, the EuropeanAnti-Fraud Office, the European Court of Auditors and any external auditor carrying out verifications as required per Article 15.6…”

Training session – February 2013Page 19

European Union

Grant contractsAnnex II: Financial provisions (Article 17)

► Article 17► Article 17.1 – “The total amount to be paid by the Contracting Authority to the

Beneficiary may not exceed the maximum grant laid down in Article 3.2 of the Special Conditions, even if the total of actual eligible expenditure exceeds the estimated total budget set out in Annex III”.

Training session – February 2013Page 20

European Union

Grant contractsList of the annexes

► Annexes:► Annex I: Description of the Action► Annex II: General Conditions applicable to European Community-financed

grant contracts for external Actions► Annex III: Budget for the Action► Annex IV: Contract award procedures► Annex V: Standard request for payment and financial identification form► Annex VI: Model narrative and financial report► Annex VII: Model report of factual findings and terms of reference for an

expenditure verification of an EC financed grant contract for external actions

► Annex VIII: Model financial guarantee

Training session – February 2013Page 21

European Union

Grant contractsAnnex III: Budget for the Action

► The Budget for the Action is a key document for the auditor.► It must be presented according to a specific template.

� Expenses ���� need to be presented by budget lines

� Revenues � need to be presented in EUR and percentage of total

Training session – February 2013Page 22

European Union

Grant contractsAnnex III: Budget

► Main budget lines:� Human resources: salary of local and expatriate staff + per diems for missions.� Travel: International and local travels.

� Equipment and supplies: Vehicles, furniture, machines, etc.

� Local office: office rent and office supplies, etc.� Other costs and services: publications, studies, auditing costs, costs of conference,

visibility actions, etc.� Other: Other costs necessary for the implementation of the Action.

� Provision for contingency reserve: maximum 5% of direct eligible costs of the Action (Reference to Art.14.3 of CG)

� Administrative costs: maximum 7% of direct eligible costs of the Action. (Reference to Art.14.4 of CG)

Training session – February 2013Page 23

European Union

Grant contractsAnnex III: Budget

► Additional requirements:� The Budget must cover all eligible costs of the Action, not just the Contracting

Authority's contribution (EC contribution)

� The description of items must be sufficiently detailed� Breakdown for all years and year 1 (if the Action implemented over a period of more

than 12 months)

� Indication of number units/unit rate (in EUR) and total costs (in EUR) (example of unit: per month, per travel, etc)

� Indicate the country where the per diems are incurred and the applicable rates (which must not exceed the scales published by the EC)

� Denominated in the currency specified in the contract (usually EUR)

Training session – February 2013Page 24

European Union

Grant contractsAnnex III: Budget

► Revenues (sources of funding) in EUR and percentage of total for:► Applicant's financial contribution► Commission contribution► Contributions from other European Institutions or EU Member States► Contributions from other organisations► Direct revenue from the Action (sales of consumables, subscription of

conferences, seminar,…)

Training session – February 2013Page 25

European Union

Grant contractList of the annexes

► Annexes:► Annex I: Description of the Action► Annex II: General Conditions applicable to European Community-financed

grant contracts for external Actions► Annex III: Budget for the Action► Annex IV: Contract award procedures► Annex V: Standard request for payment and financial identification form► Annex VI: Model narrative and financial report► Annex VII: Model report of factual findings and terms of reference for an

expenditure verification of an EC financed grant contract for external actions

► Annex VIII: Model financial guarantee

Training session – February 2013Page 26

European Union

Grant contractsAnnex IV: Contract award procedures

► Main principles:� The contract must be awarded to the most economically advantageous tender

(ie, the tender offering the best price-quality ratio)

� In accordance with the principles of transparency � Fair competition for potential contractors and � Taking care to avoid any conflicts of interest

► If failure to comply with the rules:� The expenditure of the transaction in question is not eligible for Community

financing

Training session – February 2013Page 27

European Union

Grant contractsAnnex IV: Nationality rule

Training session – February 2013Page 28

European Union

Grant contractsAnnex IV: Rule of origin

► Main principles► Origin:

� Is the country where the goods were last produced or assembled. (i.e. not necessarily the country of the supplier!)

► Certificate of origin: � the origin of the goods must be attested by a “certificate of origin”� It is an official document delivered by the relevant authorities of the country of

origin of the supplies (for example, a Chamber of Commerce).� It is only required for equipment or vehicles with a unit cost in excess of EUR 5.000

(but the rule of origin must be respected even for expenditure below this amount)

Training session – February 2013Page 29

European Union

Grant contractsAnnex IV: Procurement procedures

► Main rules► Tender documents must be drafted in accordance with best international

practice.► Time-limits for receipt of tenders and requests to participate must be long

enough► All requests to participate and tenders declared as satisfying the requirements

must be evaluated and ranked by an evaluation committee► Evaluation committee: composed by an odd number of members, at least

three, with all the technical and administrative capacities necessary to give an informed opinion on the tenders

Training session – February 2013Page 30

European Union

Grant contractsAnnex IV: Procurement procedures

► Service contracts► Contract value > € 200 000

� International restricted tender procedure following publication of a procurement notice

► Contract value < € 200 000� Consultation in writing of at least 3 suppliers

� No publication required

► Contract value < € 10 000� the Beneficiary may place orders on the basis of a single tender.

Training session – February 2013Page 31

European Union

Grant contractsAnnex IV: Procurement procedures

► Supply contracts► Contract value > € 150 000

� International open tender procedure following publication of a procurement notice

► Contract value between € 60 000 and € 150 000 � Open tender procedure published locally

► Contract value < € 60 000 � Consultation in writing of at least 3 suppliers

� No publication required

► Contract value < € 10 000 � The Beneficiary may place orders on the basis of a single tender

Training session – February 2013Page 32

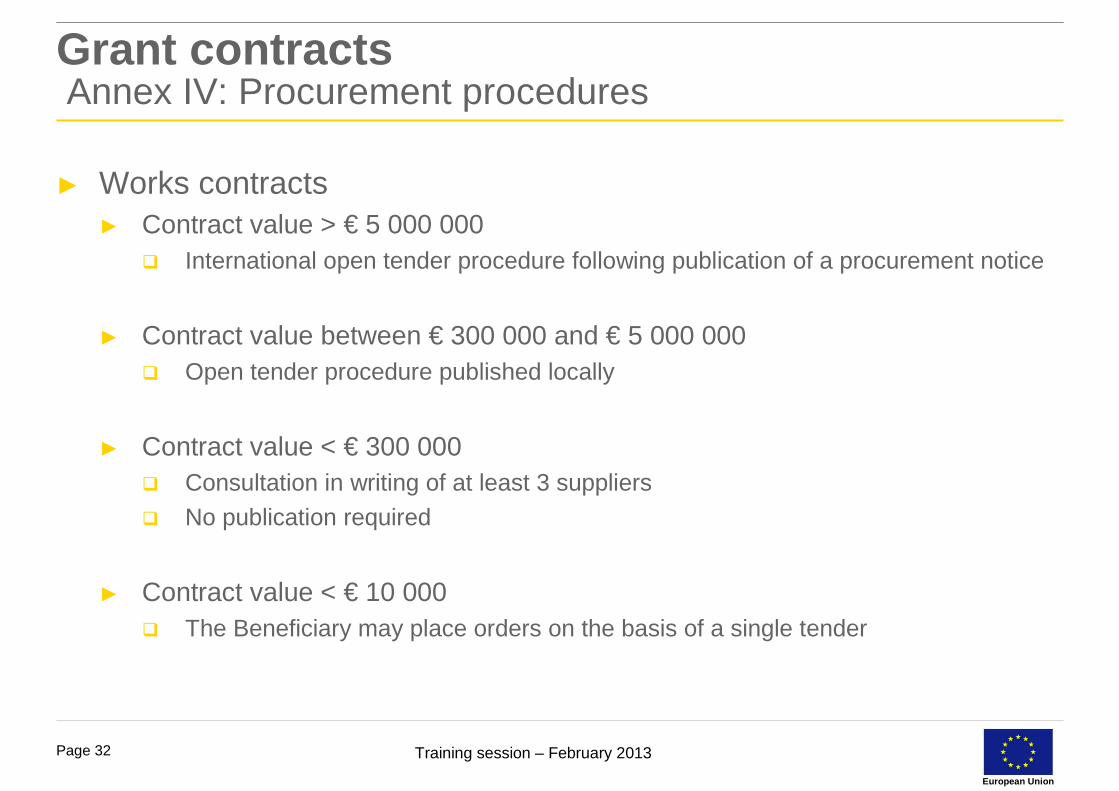

European Union

Grant contractsAnnex IV: Procurement procedures

► Works contracts► Contract value > € 5 000 000

� International open tender procedure following publication of a procurement notice

► Contract value between € 300 000 and € 5 000 000 � Open tender procedure published locally

► Contract value < € 300 000 � Consultation in writing of at least 3 suppliers

� No publication required

► Contract value < € 10 000 � The Beneficiary may place orders on the basis of a single tender

Training session – February 2013Page 33

European Union

Grant contractsProcurement procedures

► Other important aspects► Process should be documented

� The Beneficiary should be able to show how they have managed the entire process

► Contract must be signed during the correct period� the contract may not be awarded outside of the official implementation period

► Rule of origin must be followed� Failure to comply is a frequent cause of ineligibility

Training session – February 2013Page 34

European Union

► True or false?

► The General conditions overruled the special conditions� False

► Administrative costs can exceed 7% of the total direct eligible costs in certain case� False

► The budget of a grant contract contains expenses and revenues � True

Grant contractsQuizz

Training session – February 2013Page 35

European Union

► True or false?

► The budget must cover only the expenses financed by the Contracting Authority� False

► The budget must be presented in EUR currency� True

► The equipment for a unit price > 5.000 EUR must be attested by a “certificate of origin”� True

Grant contractsQuizz

Training session – February 2013Page 36

European Union

► True or false?

► The procurement procedure is different for services/supply/works contracts� True

Grant contractsQuizz

Training session – February 2013Page 37

European Union

Agenda

► Welcome► Introduction► Grant Contracts► Expenditure verifications► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 38

European Union

Expenditure verificationsActors and responsibilities

► Actors involved� The Contracting Authority refers to the European Commission

� The Beneficiary refers to the organisation that is receiving the grant funding and that has signed the Grant Contract with the Contracting Authority

� The Auditor refers to the Audit Professional who is responsible for performing the agreed-upon procedures as specified in the ToR

► The Beneficiary is responsible� For providing a Financial report for the Action.� For ensuring that the Financial report is properly reconciled to the Beneficiary’s accounting

and bookkeeping system.

� for providing full and free access to the Beneficiary’s staff and its accounting and other relevant records.

Training session – February 2013Page 39

European Union

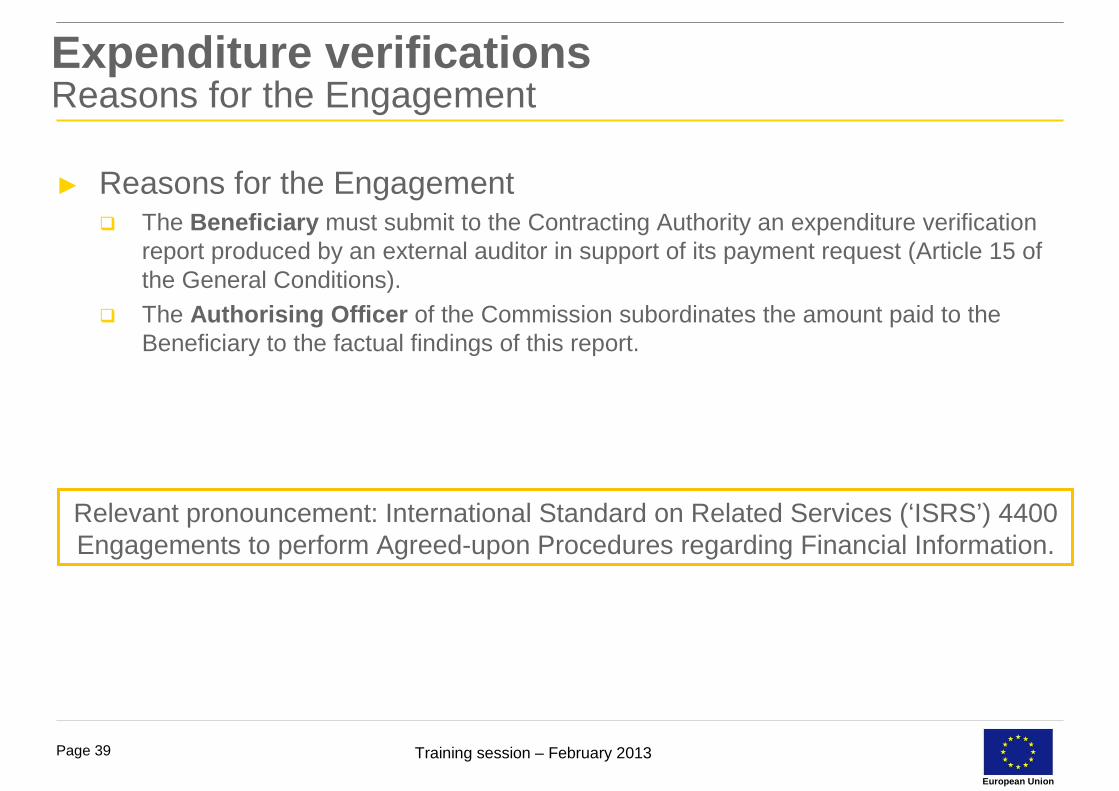

Expenditure verificationsReasons for the Engagement

► Reasons for the Engagement� The Beneficiary must submit to the Contracting Authority an expenditure verification

report produced by an external auditor in support of its payment request (Article 15 of the General Conditions).

� The Authorising Officer of the Commission subordinates the amount paid to the Beneficiary to the factual findings of this report.

Relevant pronouncement: International Standard on Related Services (‘ISRS’) 4400 Engagements to perform Agreed-upon Procedures regarding Financial Information.

Training session – February 2013Page 40

European Union

Expenditure verificationsReason for the Engagement

► The objectives of the audit professional are:

� to carry out procedures of an audit nature which are specified in Annex VII of the Grant Contract

� to provide a report of factual findings of the agreed-upon procedures

� the audit professional expresses no opinion in his report. The report user forms his own opinion based on the factual information reported by the audit professional

Training session – February 2013Page 41

European Union

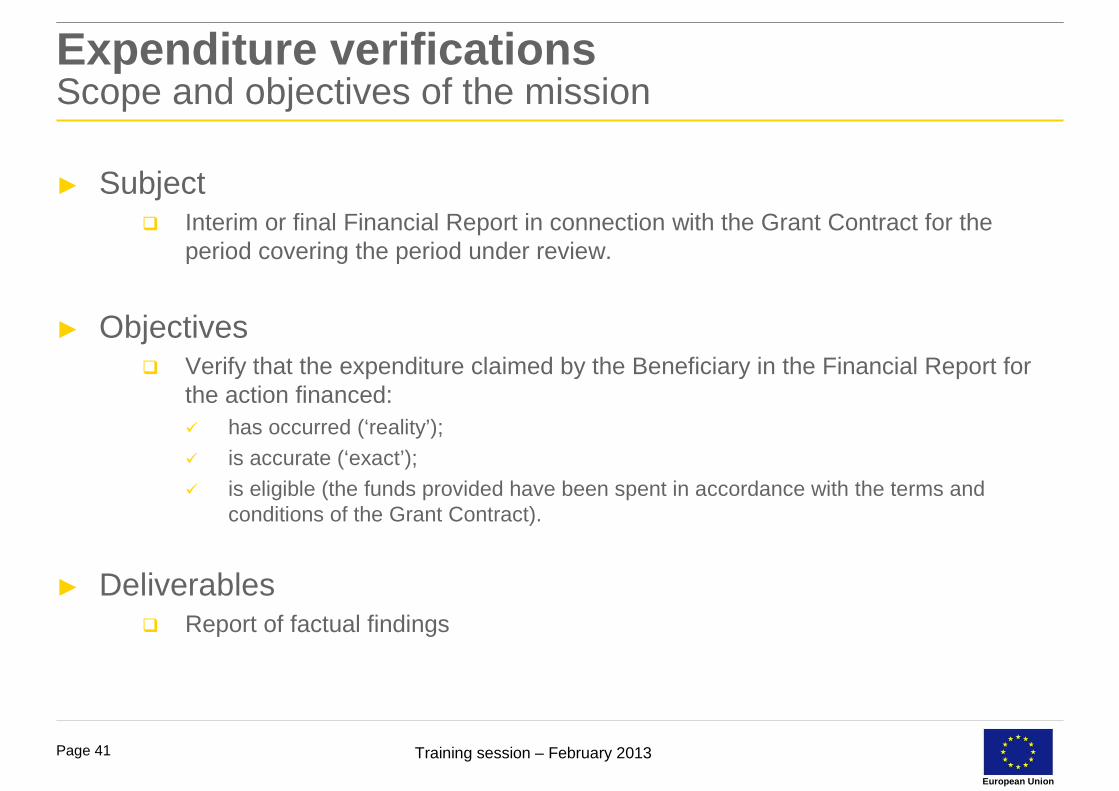

Expenditure verificationsScope and objectives of the mission

► Subject � Interim or final Financial Report in connection with the Grant Contract for the

period covering the period under review.

► Objectives� Verify that the expenditure claimed by the Beneficiary in the Financial Report for

the action financed:� has occurred (‘reality’);

� is accurate (‘exact’);

� is eligible (the funds provided have been spent in accordance with the terms and conditions of the Grant Contract).

► Deliverables � Report of factual findings

Training session – February 2013Page 42

European Union

Expenditure verificationsProcedures to be performed

► Obtaining a sufficient Understanding of the Action and of the Terms and Conditions of the Grant Contract

� The Auditor obtains a sufficient understanding of the terms and conditions of the Grant Contract.

� The Auditor ensures with the Beneficiary that the applicable nationality and origin rules are identified and understood.

► General Procedures� The Financial Report complies with the conditions of the Grant Contract (form and language).

� The Beneficiary has complied with the rules for accounting and record keeping of the Grant Contract, notably with Article 16 of the General Conditions.

� Reconciliation of the information in the Financial Report to the Beneficiary’s accounting system and records.

� Verification that the correct exchange rates have been applied for currency conversions.

Training session – February 2013Page 43

European Union

Expenditure verificationsProcedures to be performed

► Conformity of Expenditure with the Budget and Analytical Review � Verification that the budget in the Financial Report corresponds with the Budget of

the Grant Contract and that the expenditure incurred was foreseen in the budget.

� Verification that the total amount claimed for payment by the Beneficiary does not exceed the maximum budgetary amount (in total and by budget line)

� Verification that any amendments to the Budget comply with the conditions for such amendments.

� Verification that Article 17.3 of the General Conditions is respected (absence of profit).

Training session – February 2013Page 44

European Union

Expenditure verificationsProcedures to be performed

► Selecting Expenditure for Verification� The Auditor selects high value expenditure items to ensure an appropriate

coverage of expenditure.

� the Auditor select other specific expenditure items or classes of expenditure items according to. � his knowledge of the action;� the characteristics of the expenditure categories and the items being verified (e.g.

unusual, inherently risky or error prone transactions).

Training session – February 2013Page 45

European Union

Expenditure verificationsProcedures to be performed

► Verification of Expenditure � The Auditor verifies the expenditure and reports all the exceptions resulting from

this verification. � Verification exceptions are all verification deviations found when performing the

procedures.

� In all cases the Auditor assesses the (estimated) financial impact of exceptions in terms of ineligible expenditure.

� The Auditor reports all exceptions found including the ones for which he cannot measure the financial impact.

Training session – February 2013Page 46

European Union

Expenditure verificationsProcedures to be performed

HOW DO YOU VERIFY THE EXPENDITURE ?

Training session – February 2013Page 47

European Union

Expenditure verificationsProcedures to be performed

► Eligibility of Direct Costs► The Auditor verifies the eligibility of direct costs with the terms and conditions

of the Grant Contract notably Article 14 of the General Conditions. He verifies that these costs:

� are necessary for carrying out the action. � have actually been incurred during the implementation period of the Action

� are recorded in the accounts and are identifiable, verifiable and substantiated by originals of supporting evidence.

The Auditor also considers non-eligible costs as described in Article 14.6 of the General Conditions. In this respect the Auditor verifies in particular whether

expenditure includes certain taxes, including VAT.

Training session – February 2013Page 48

European Union

Expenditure verificationsProcedures to be performed

► Coverage of Sample

� The Auditor ensures a systematic and representative verification.

� The Auditor may apply statistical sampling techniques.

► Expenditure Coverage Ratio (‘ECR’)

� Total amount verified by the Auditor expressed as a percentage of the total expenditure in the Financial Report.

� The Auditor ensures that the overall ECR is at least 65%. � If the exception rate found is higher than 10%, the Auditor extends his sample until the

ECR is at least 85%.

� The Auditor ensures that the ECR for each budgetary heading and subheading in the Financial Report is at least 10% of the heading/subheading.

Training session – February 2013Page 49

European Union

Expenditure verificationsProcedures to be performed

► Accuracy and Recording

The Auditor verifies that

► The expenditure for a transaction is accurately and properly recorded in the accounting system and in the Financial Report

► The expenditure for a transaction is supported by appropriate evidence and supporting documents.

► This includes proper valuation and the use of correct exchange rates.

Training session – February 2013Page 50

European Union

Expenditure verificationsProcedures to be performed

Training session – February 2013Page 51

European Union

Expenditure verificationsProcedures to be performed

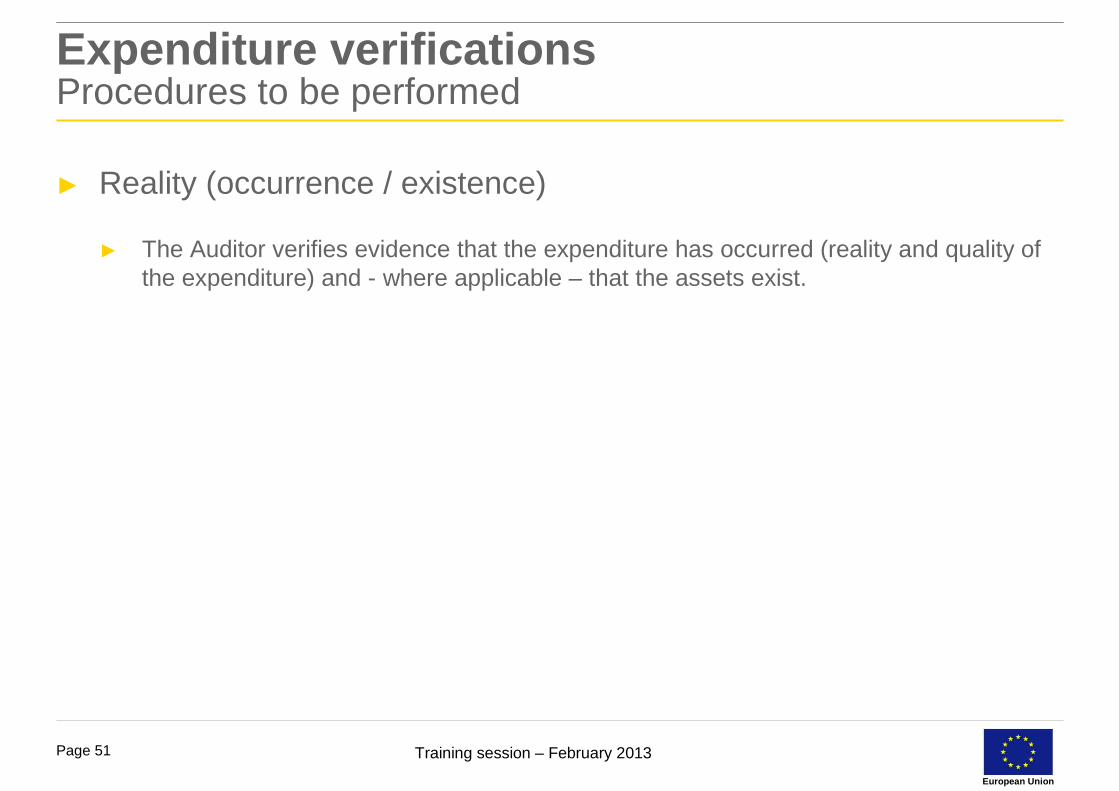

► Reality (occurrence / existence)

► The Auditor verifies evidence that the expenditure has occurred (reality and quality of the expenditure) and - where applicable – that the assets exist.

Training session – February 2013Page 52

European Union

Expenditure verificationsProcedures to be performed

► Compliance with Procurement, Nationality and Origin Rules

► The Auditor checks which procurement, nationality and origin rules apply for a certain expenditure heading, subheading, a class of expenditure items or an expenditure item.

Training session – February 2013Page 53

European Union

Expenditure verificationsProcedures to be performed

► Administrative costs

► The Auditor verifies that the administrative costs do not exceed a maximum of 7% of the total direct eligible actual costs of the action.

Training session – February 2013Page 54

European Union

Expenditure verificationsProcedures to be performed

► Contingencies

► The Auditor verifies that contingencies do not exceed 5% of the total eligible costs (direct and indirect) of the Action.

► When the contingency line has been utilised, the Auditor verifies that the Beneficiary has obtained approval from the Contracting Authority.

Training session – February 2013Page 55

European Union

Expenditure verificationsProcedures to be performed

► Verification of Revenues of the Action

► The Auditor verifies that revenues have been appropriately allocated to the Action and correctly disclosed in the Financial Report.

� As this engagement is not an audit, the Auditor is not requested to assess the completeness of revenues.

� Specific point of attention: interest yielded by the pre-financing.

Training session – February 2013Page 56

European Union

► True or false?

► An expenditure verification is mandatory for all grant contract� False

► The audit report is the deliverable in case of expenditure verification� False

► According to the ToR, overall ECR must be at least 65% � True

Expenditure verifications Quizz

Training session – February 2013Page 57

European Union

► True or false?

► In an expenditure verification, only the deviation above a threshold must be reported� False

► The Beneficiary is responsible for providing the financial report� True

Expenditure verifications Quizz

Training session – February 2013Page 58

European Union

► If the Beneficiary has adjusted his financial report for the findings found during expenditure verification, does the audit professional need to report in his report of factual findings?

Expenditure verifications Quizz

Training session – February 2013Page 59

European Union

Agenda

► Welcome► Introduction► Grant Contract► Expenditure verification► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 60

European Union

Case study

► Division of the total group in 6 different teams

► Group 1: Salary► Group 2: Travels► Group 3: Equipment and supplies► Group 4: Local office► Group 5: Other costs, services► Group 6: Procurement procedures

Training session – February 2013Page 61

European Union

Case study

► PART 1

Rules to follow:► Selection of high value expenditure items to ensure an appropriate coverage of

expenditure.► Selection of other specific expenditure items or classes of expenditure items.

► Verification that the overall ECR is at least 65%. ► Verification that the ECR for each expenditure heading and subheading in the Financial

Report is at least 10%

Timing: 15 minutes

Presentation of the sample selection

Based on the final financial report of the Action “ABC“, prepare the sample selection for the expenditure verification

Training session – February 2013Page 62

European Union

Case study

► PART 2

Reminder concerning the procedures to perform:► Accuracy and Recording

► Classification

► Reality (occurrence / existence)► Compliance with Procurement (nationality and origin rules)

Timing: 15 minutes

Presentation of the results (one person per group)

Prepare a list of supporting documents necessary for carrying out the expenditure verification.

Explain why these documents are relevant in case of an expenditure verification.

Training session – February 2013Page 63

European Union

Case study

PRESENTATION OF THE RESULTS

Training session – February 2013Page 64

European Union

Agenda

► Welcome► Introduction► Grant Contract► Expenditure verification► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 65

European Union

Local accounting rules

► Accounting rules - Universal► Proper bill/invoice – VAT or PAN ► Respect the local laws regarding registration► Authenticity of VAT/PAN

� http://www.ird.gov.np/ird/index/pan-details.html

Training session – February 2013Page 66

European Union

Agenda

► Welcome► Introduction► Grant Contract► Expenditure verification► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 67

European Union

Errors frequently met

► Main objective► Presentation of errors frequently met in Nepal

� Financial findings� Internal control findings

� Other compliance findings

► Comparison Nepal vs world

Training session – February 2013Page 68

European Union

Errors frequently metGroup discussion

FINANCIAL FINDINGS

Training session – February 2013Page 69

European Union

Errors frequently metGroup discussion

As per article 2.2 of the Grant Contract, the implementation period of the project started on 1 June 2012. Expenditure concerning the purchase of office equipment, the advertisement for a vacancy and salaries were incurred for the project in April and May 2012.

Article 14.1 of Annex II of the Grant Contract foresees that “Eligible costs are … incurred during the implementation of the action as specified in article 2 of the Special Conditions with the exception of costs relating to final reports and expenditure verification”.

Training session – February 2013Page 70

European Union

Errors frequently metGroup discussion

The entity has procured 223 pieces of radio for community people for which there was no budget line. This expense has been booked under the budget line “supply of medicines”. There was no provision for the procurement of radio sets in the original budget of the Action.

Article 14.1 of Annex II of the Grant Contract foresees that “Eligible costs are … have to be indicated in the estimated budget of the Action”.

Training session – February 2013Page 71

European Union

Errors frequently metGroup discussion

The entity purchased a digital camera for the project. During the project lifetime, this item was stolen from the possession of anemployee while he was on visit in a project funded by the World Bank in a remote area in Nepal.

Article 14.1 of Annex II of the Grant Contract foresees that “Eligible costs are … have to be necessary for the implementation of the Action which is subject of the grant”.

Training session – February 2013Page 72

European Union

Errors frequently metGroup discussion

As per the final financial report of the project, the total expenditure declared under budget heading “travel” exceeds the original budgeted amount by 21%.

Article 9 of Annex II of the Grant Contract foresees that “where the amendment to the Budget does not affect the basic purpose of theAction and the financial impact is limited to a transfer between main budget headings involving a variation of 15% or less of the amount originally entered (or as modified by addendum) in relation to each concerned main heading for eligible costs, the Beneficiary may amend the budget and inform in writing without delay the Contracting Authority accordingly”.

Training session – February 2013Page 73

European Union

Errors frequently metGroup discussion

The project manager’s position was vacant for the month of April 2011 to September 2011. During this period, the finance manager has acted as project manager and was paid with the salary of a Project manager. According to the budget of the project, the foreseen salary of the project manager was 1,000 € per month and the foreseen salary of the finance manager was 700 € per month.

Article 14.1 of Annex II of the Grant Contract foresees that “Eligible costs are … have to be reasonable, justified and comply with the requirements of sound financial management, in particular regarding economy and efficiency”.

Training session – February 2013Page 74

European Union

Errors frequently metNepal - Statistics

Training session – February 2013Page 75

European Union

Errors frequently metNepal – Financial findings

► Expenditure not for project purpose (16 cases)

► Expenses paid for tender evaluation meeting► Expenses paid to non-local personnel for study tours/workshops► Expenses reported for closed offices► Costs of event cancelled reported► Attendance allowances paid to Government seconded staff► Costs of non-budgeted items reported► Costs of travel non for project purpose► Costs of travel cancelled reported► Excess of consultancy fee charged for final evaluation► “Festivity allowance” should be pro-rated in accordance with actual time spent

on the project

Training session – February 2013Page 76

European Union

Errors frequently metNepal – Financial findings

► Other (7 cases)

► Double-booking of expenses� recorded as payable and then as expense again rather than being matched

against outstanding payable.► Expenditure reported includes non-disbursed cost.

► Absence of timesheet for staff partially employed for the Project

► Currency exchange losses reported► Overstatement of administrative costs due to ineligible expenditures

� In case of financial finding, the administrative costs will be everytime impacted

Training session – February 2013Page 77

European Union

Errors frequently metNepal – Financial findings

► Missing / inadequate documentation (7 cases)

► Expense with no supporting evidence► Salary paid without employment contract► Expenses not supported by appropriate receipts/bills/invoices► Absence of boarding passes

Training session – February 2013Page 78

European Union

Errors frequently metNepal – Financial findings

► Incorrect procurement procedure applied (2 cases)

► No evidence of procurement procedures for a supply contract > 10.000 EUR

► Expenditure includes VAT/Other taxes (2 cases)

► Value added tax (VAT) charged to the project

► Income not declared / not reported (2)

► Miscalculation of interest reported► Interest income not reported

Training session – February 2013Page 79

European Union

Errors frequently metNepal – Financial findings

► Expenditure outside contractual period (1)

► Expenses incurred before project commencement (before or after contractual date)� Note that some cost can occurred after ending date of project

► Incorrect exchange rate used (1)

► Incorrect exchange rate applied for expenditure reporting.� Can be at the advantage of the Beneficiary

► Budget exceeded (1)

► Budget exceeded by more than 15% without proper amendment.

Training session – February 2013Page 80

European Union

Errors frequently metGroup discussion

INTERNAL CONTROL FINDINGS

Training session – February 2013Page 81

European Union

Errors frequently metGroup discussion

Expenses were recorded under a budget line of which the description is not properly reflecting the actual nature of the expense. For example, travel costs (budget line 2.2) were recorded under salaries (budget line 1.1) and construction materials under salaries (budget line 1.1).

Training session – February 2013Page 82

European Union

Errors frequently metGroup discussion

Perceived riskIn case expenses are not allocated to the appropriate budget line that covers the actual nature of the expense, a budget versus actual expenditure verification as part of the standard internal control system becomes complicated and budget over-runs may remain undetected.

RecommendationExpenses should be allocated to the appropriate budget line as planned in the overall budget of the action in order to allow a proper budget versus actual expenditure verification.

Training session – February 2013Page 83

European Union

Errors frequently metGroup discussion

Expenses were not supported by delivery note or goods delivery note. The project failed to archive these documents in order to support the actual delivery of goods/supplies.

Perceived riskWithout the systematic availability of such supporting documentation, the proof of existence of the goods and supplies is less evidenced.

RecommendationWe recommend putting in place a systematic and relevant proof ofdelivery for the goods and supplies.

Training session – February 2013Page 84

European Union

Errors frequently metGroup discussion

The Entity and its partner NGO did not maintain a proper stock register showing the stock of materials which were used in the different schemes. Materials movement register was also not maintained, as a result of which the proper and complete utilisation of the materials cannot be ensured.

Training session – February 2013Page 85

European Union

Errors frequently metGroup discussion

Perceived riskWithout the systematic update of the stock register, the use of materials for the action is less evidenced.

Recommendation In order to ensure proper inventory management it is recommendedthat the entities maintain proper inventory record showing the receipts, issues and closing inventory.

Training session – February 2013Page 86

European Union

Errors frequently metGroup discussion

As per the applicable procurement rules (Annex IV of the grant contract), competitive bid was organized for the purchase of materials. Nevertheless, the request for offers was not fully complete (no unit price with/without VAT, transportation costs,…). As a result the contractual price was higher that bidding price due to unforeseen additional transport costs.The contract was awarded to the lowest bidder. However failing sufficiently detailed itemized unite prices for the transport costs, it is not possible to ensure whether the other participants to the tendering process would have offered more competitive transport costs.

Training session – February 2013Page 87

European Union

Errors frequently metGroup discussion

Perceived riskThe contract is not awarded to the most economically advantageous tender (ie, the tender offering the best price-quality ratio) as requested by the Annex IV (Contract award procedures).

Recommendation Provide detailed pricing specifications in request for quotations in order to enable better decision in the procurement procedure (full transparency in bid comparison and evaluation).

Training session – February 2013Page 88

European Union

Errors frequently metGroup discussion

Approximately 10 persons work part time for the project. These were persons employed in the Beneficiary central office staff in Kathmandu where several projects are managed simultaneously. Their salary expenses have been charged to the project month-wise based on a fixed allocation percentage. The actual percentage of time allocated to the EU-funded project resulting from the monthly timesheets is usually different from this fixed percentage.

Training session – February 2013Page 89

European Union

Errors frequently metGroup discussion

Perceived riskIn case the allocation of salary expenses of part-time employees to the project is not based on the actual time spent for the project according to timesheets, the salary expenses allocated to the project may be incorrect

Recommendation:The actual time allocated to a project (based on timesheets) should be the basis for the allocation of salary expenses to a project.

Training session – February 2013Page 90

European Union

Errors frequently metNepal - Statistics

Training session – February 2013Page 91

European Union

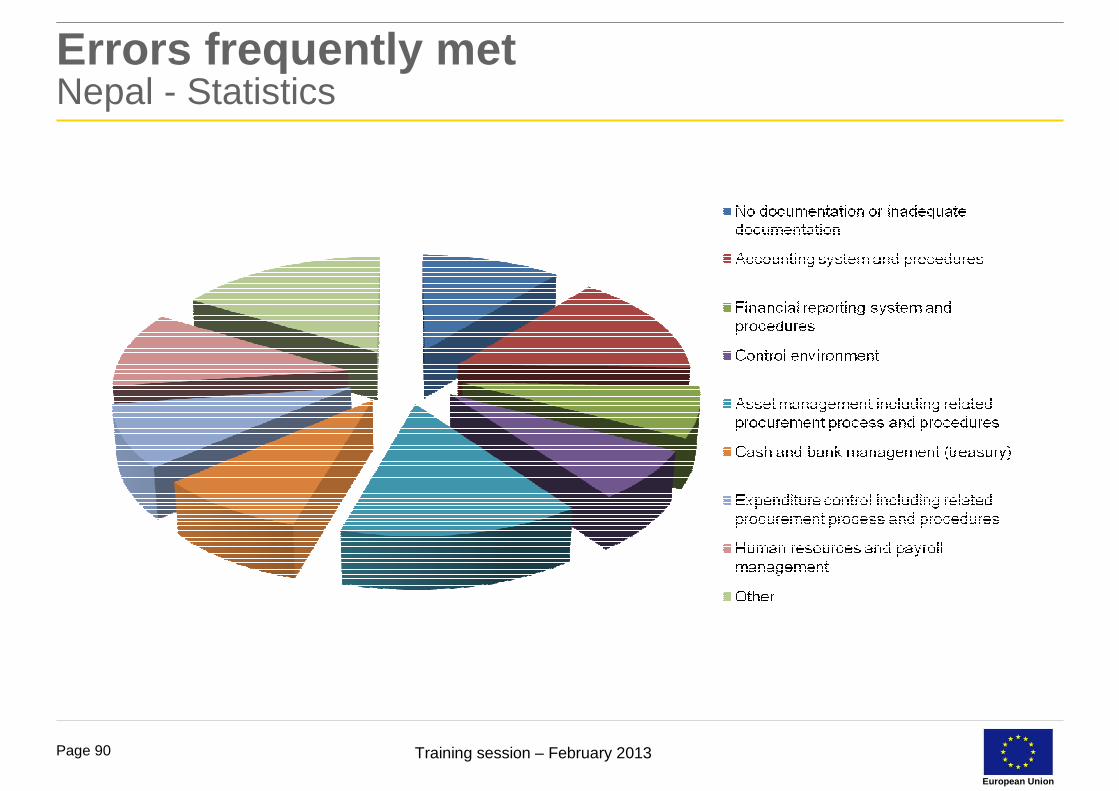

Errors frequently metNepal – Management control findings

► Other (9)

► Disproportionate level of control for certain expenditure

► Absence of delivery receipts

► No formal policy for per diems► Strengthening of inventory management

► Possibility of conflict of interest

► Asset management including related procurement process and procedures (8)

► Fixed assets not properly insuranced► Insurance cover of fixed assets expired

► Competitive bidding not followed for procurement of supplies and services

► Procurement policy not comprehensive

Training session – February 2013Page 92

European Union

Errors frequently metNepal – Management control findings

► Accounting system and procedures (8)

► Accounting kept manually or maintained on excel only

► Transactions recorded on the basis of unapproved vouchers

► Chart of accounts not maintained► Insufficiently detailed accounting entries

► Lack of evidence for allocation of general expenses

► No documentation or inadequate documentation (6)

► Absence of supporting documents► Expenses recorded without sufficient supporting documents

► Rent agreements of office not complete

Training session – February 2013Page 93

European Union

Errors frequently metNepal – Management control findings

► Human resources and payroll management (6)

► Weak payroll processing

► Recruitment process not followed

► Festivity bonus reported incorrectly► Lack of Project officer timesheet

► Expenditure control including related procurement process and procedures (5)

► Weak budgetary control system

► Variance analysis of budget versus actual expenses not performed regularly► Reconciliation of commercial invoices with purchase orders

► Full payment made without receving service from consultant

Training session – February 2013Page 94

European Union

Errors frequently metNepal – Management control findings

► Cash and bank management (treasury) (5)

► Dedicated bank account for the project not maintained

► Bank reconciliations are not prepared on a monthly basis. Cash flow statement not available at closing date

► Non existing cash balance

► Lack of supporting evidence of interest rate calculation

► Financial reporting system and procedures (4)

► Financial report not properly prepared based on the trial balance

► Reports prepared manually► Format of the Financial report non respected

Training session – February 2013Page 95

European Union

Errors frequently metNepal – Management control findings

► Control environment (4)

► Staff turnover for key positions

► Weak monitoring of cluster office activities

► Policies not in existence till July 1, 2010

Training session – February 2013Page 96

European Union

Errors frequently metGroup discussion

OTHER COMPLIANCE FINDINGS

Training session – February 2013Page 97

European Union

Errors frequently metGroup discussion

No external visibility with a clear reference to the European Union’s financial contribution was set in place during the project lifetime (absence of EU flag on training materials and on the two schoolsbuilt)

Perceived riskNon respect of the contractual requirement for visibility as mentioned in the Article 6 of the General Conditions).

Training session – February 2013Page 98

European Union

Errors frequently metGroup discussion

Salary income taxes have been duly deducted from the salaries ofproject staff. However the Beneficiary has not paid these taxes to the Government as requested by local legislation.

Perceived riskIn case of non-payment and/or non-declaration of taxes, the government could issue a penalty or reclaim this amount.

Training session – February 2013Page 99

European Union

Errors frequently metNepal - Statistics

Training session – February 2013Page 100

European Union

Errors frequently metNepal – Compliance findings

► Other (10)

► Subcontracting of implementation activity► EC approval not obtained► Incompliance with local income tax legislation

� insufficient deduction of withholding tax

� delay in deposit withholding tax� Income tax deducted at source but not paid to gouvernment

� Income tax not deducted at source for expatriate staff

Training session – February 2013Page 101

European Union

Errors frequently metNepal – Compliance findings

► Contractual requirements for visibility and publicity not respected (6)

► Visibility guidelines not properly implemented

► Insufficient visibility of the action

► Lack of formal visibility rules and requirements for programme deliverables

► Delays in (financial/non-financial) project reporting to the Commission (1)

► Expiry of implementation period as per the Financial Agreement

Training session – February 2013Page 102

European Union

Errors frequently metComparison Nepal vs World

Nepal World

Financial Findings

Training session – February 2013Page 103

European Union

Errors frequently metComparison Nepal vs World

Nepal World

Internal Control Findings

Training session – February 2013Page 104

European Union

Errors frequently metComparison Nepal vs World

Nepal World

Compliance Findings

Training session – February 2013Page 105

European Union

Agenda

► Welcome► Introduction► Grant Contract► Expenditure verification► Case study (practical situation)► Local accounting rules► Errors frequently met► Conclusion

Training session – February 2013Page 106

European Union

ConclusionUseful information

► Financial Management Toolkit for recipients of EU funds for external actions.

► Module 1: Internal Controls► Module 2: Documentation, Filing and Record Keeping► Module 3: Procurement► Module 4: Asset Management► Module 5: Payroll and Time Management► Module 6: Cash and Bank Management► Module 7: Accounting► Module 8: Financial Reporting

Based on the 2009 release of the Commission’s contract models and guides

Training session – February 2013Page 107

European Union

ConclusionUseful information

► Development and Cooperation – EuropeAid► http://ec.europa.eu/europeaid/index_en.htm

► Contractual information► http://ec.europa.eu/europeaid/work/procedures/implementation/index_en.htm

► Frequently asked questions► http://ec.europa.eu/europeaid/work/procedures/faq/index_en.htm

► Practical Guide► http://ec.europa.eu/europeaid/prag/document.do?locale=en

► Per diems rate► http://ec.europa.eu/europeaid/work/procedures/implementation/per_diems/ind

ex_en.htm

Training session – February 2013Page 108

European Union

ConclusionUseful information

► Official exchange rate website (InforEuro)► http://ec.europa.eu/budget/contracts_grants/info_contracts/inforeuro/inforeuro

_en.cfm

► Financial Management Toolkit► http://ec.europa.eu/europeaid/financial_management_toolkit/

Training session – February 2013Page 109

European Union

Conclusion

Questions ?

Training session – February 2013Page 110

European Union

Conclusion

THANK YOU !

Training session – February 2013Page 111

European Union

Additional InformationVAT

► Different regulations to respect (reflected in the respected General Conditions of your Call – please check)

► 1) EIDHR► 2) DCI (covering NSA, Investing in people, environment)► 3) FOOD FACILITY

2 conditions need to be fulfilled for the VAT to be eligible:VAT is considered eligible where the Regulation and/or Financing Agreement with the third country under which the Contract is financed do not exclude coverage of taxes and the Beneficiary can show it cannot reclaim.

Training session – February 2013Page 112

European Union

Additional InformationVAT 1) EIDHR► Guidelines launched in 2010VAT is INELIGIBLEGeneral Conditions Art 14.6 refer to the applicable regulation 1889/2006 where VAT is

not allowed according Art 13.6

► Guidelines launched in 2011VAT is INELIGIBLE but ACCEPTABLE as co-financing from beneficiaryGeneral Conditions Art 14.2 and Guidelines 2.1.4 ALLOW VAT as co-finaning

of the beneficiary if put in the Budget line 12; Differentiation of “eligible”and “accepted” costs

► Guidelines launched in 2012VAT is ELIGIBILE for EU funding as the regulation changed (Regulation

1340/2011 amending regulation 1889/2006; see also General Conditions 14.2, guidelines 2.1.4; Annex 7

Training session – February 2013Page 113

European Union

Additional InformationVAT 2) DCI (governing NSA, investing in people, environment)

► Guidelines launched up until and in 2010VAT is INELIGIBLEThe applicable regulation 1905/2006 forbid the coverage of VAT in its Art

13.6

► Guidelines launched in 2011VAT is INELIGIBLE but ACCEPTABLE as co-financing from beneficiaryGeneral Conditions Art 14.2 and Guidelines 2.1.4 ALLOW VAT as co-finaning

of the beneficiary if put in the Budget line 12; Differentiation of “eligible”and “accepted” costs

► Guidelines launched in 2012VAT is ELIGIBILE for EU funding as the regulation changed (Regulation

1339/2011 amending regulation 1905/2006;

Training session – February 2013Page 114

European Union

Additional InformationVAT 3) FOOD FACILITY► Guidelines launched in 2009 and later

The food facility regulation 1337/2008 allows in Art 6.4 in principle the coverage of taxes

Training session – February 2013Page 115

European Union

Additional InformationVAT

► In case the regulation allows the coverage of taxes (DCI and EIDHR from of 2011) the beneficiary must show that he cannot reclaim them.

► Except:► The Beneficiary will not have to show it cannot reclaim taxes in any of the

following cases:� where the amount of taxes per invoice is less than EUR 200, within a maximum of EUR 2

500, representing not more than 5% of the Contracting Authority's contribution;

� where the Beneficiary can demonstrate that the steps necessary for recovery of taxes oblige it to incur costs in a country where it only performs the relevant operations on an ad hoc and isolated basis; and that these costs for recovery clearly exceed the amount of the taxes declared to the Contracting Authority;

� where a country has been declared in crisis situation or in the need for emergency and post-emergency assistance by the European Commission. (limited to the period in which the declaration is in force and written approval

� Where the Action relates to the protection of fundamental rights of peoples.