trademark fee cost analysis status update for tpac november 2009

TRANSCRIPT

Trademark Fee Cost Analysis Status Update for TPAC

November 2009

2

Agenda

• Trademark Fee Cost Analysis- Objective Timeframe Project Plan Overview Accomplishments Status Information Available Sample Display Challenges Next Steps Questions

3

Trademark Fee Cost Analysis - Objective

• The Trademark Fee Cost Analysis is a joint effort between CFO and Trademarks to identify the actual cost of work performed for Trademark and TTAB Processing Fees.

• OMB Circular A-25 requires Fee Studies• Objectives:

Revise existing Trademark and TTAB models to provide better cost information to support management decision making.

Develop a method for determining the cost per fee for all Trademark and TTAB processing fee codes, including both direct and indirect costs.

Use cost information for making management decisions including future fee setting.

4

Current Timeframe - Revised

• Executive level kick-off – January 2009• Formal cost study team kick-off – March

2009• Costing model complete – September 2009• 1st, 2nd, and 3rd iterations of fee calculation –

October 2009• Fee Cost Analysis complete – November

2009• Other costing requirements – September-

TBD

5

Step 1AProject

Initiation

Establish team

Identify functional, process, data and shared service SMEs

Kick-off Meeting

Define methodology including Pilbara input

Hold facilitation sessions with Trademark Process Owners & Shared service SMEs

Map PPA codes to ABI activities and fee codes

Step 1BMethodol-

ogy

Produce initial set of results and displays

Review and revise

Step 2BCost

Allocation

Develop draft fee unit cost calculations

o Validation of unit cost results

o Finalize fee unit costs

Step 2CWorkload

Data

Step 2AActivity

Dictionary

Finalize rules for indirect & secondary cost allocation

Finalize workload data

Finalize model hierarchy

Gain Pilbara input

Incorporate work in process

o Develop additional cost displays

Step 2DNew ABI

Model

Project management, communication, and interim validations

Trademark Project Plan Overview

Phase 1: Project Initiation & Planning

Phase 3: Fee Cost Analysis

Phase 2: Model Revision Phase 4: Other Costing

Step 3ACollect

Fee Data

Step 3BResults & Displays

Step 3CReview & Validate

Step 4AWork in Process

Legend:

Completed

o In process

6

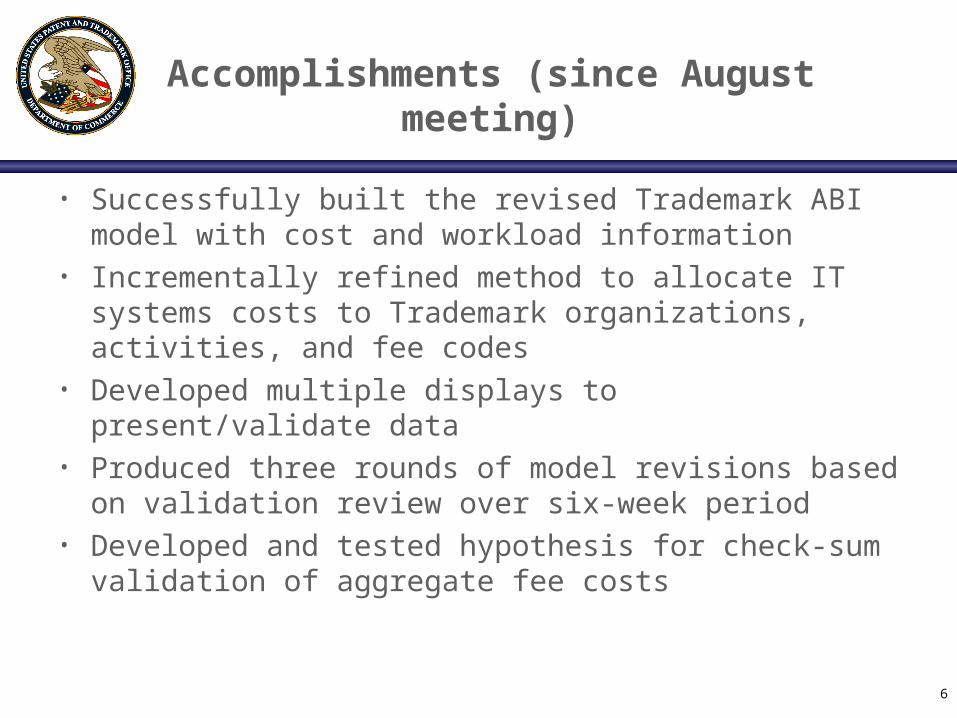

Accomplishments (since August meeting)

• Successfully built the revised Trademark ABI model with cost and workload information

• Incrementally refined method to allocate IT systems costs to Trademark organizations, activities, and fee codes

• Developed multiple displays to present/validate data

• Produced three rounds of model revisions based on validation review over six-week period

• Developed and tested hypothesis for check-sum validation of aggregate fee costs

7

Current Status

• The ABI team produced the first displays of the initial fee cost model at the end of September. The displays provided total and unit fee cost breakdowns at various levels.

• The Trademark team identified corrections/changes and updates to mappings, workload and driver data.

• The ABI model was updated for a second time and revised results reviewed; more corrections/refinements proposed.

• The ABI team is in the process of completing the third version of the fee cost model incorporating requested changes.

• Updated displays will be provided to the Trademark team for final review before sending to Executives for comment.

8

Types of information available

• Full and unit cost of Trademark activities • Full and unit cost of Trademark processing fees• Full and unit cost of Fees by contributing:

Trademark activity (e.g., Process Trademark Mail, Review and classify new application, Examine Statement of Use)

CIO managed system (e.g., TRAM, TICRS, TRADEUPS) Other allocated cost such as Rent, OPM, and costs

from support organizations (e.g., CFO, CAO and Policy)

• Comparison between fee revenue and cost per fee • Comparison of paper and electronic activities by fee

code

9

Fee Unit Cost – Sample Display

10

Fee Unit Cost Detail – Sample Display

11

Challenges

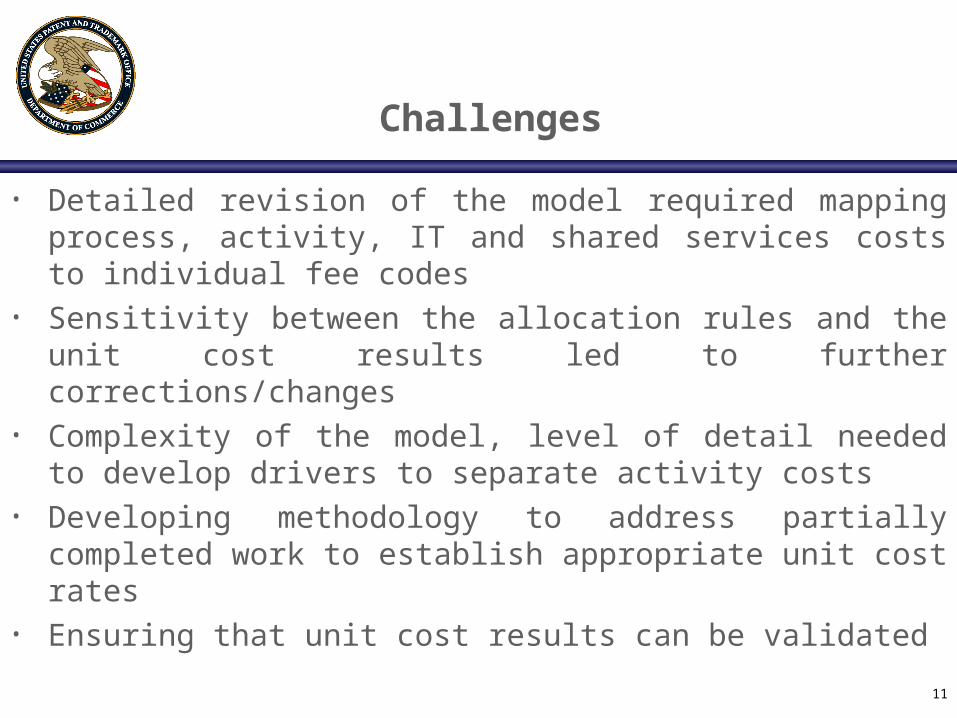

• Detailed revision of the model required mapping process, activity, IT and shared services costs to individual fee codes

• Sensitivity between the allocation rules and the unit cost results led to further corrections/changes

• Complexity of the model, level of detail needed to develop drivers to separate activity costs

• Developing methodology to address partially completed work to establish appropriate unit cost rates

• Ensuring that unit cost results can be validated

12

Next Steps

• Develop final set of fee unit cost results• Finalize check sum methodology• Review and validate• Develop briefing packages for broader review

and executive presentations• Revise model as needed – November 30th • Begin 2009 fee cost analysis – November 9th

(4 week duration)• Begin 2007 fee cost analysis – December• Provide recommendations for management

action – December/January 2010

13

Questions…

Thank you!Thank you!