trade performance and competitiveness: selected issues relevant for asian developing economies

TRANSCRIPT

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 1/215

ARTNeT

TRADE PERFORMANCE AND COMPETITIVENESS:SELECTED ISSUES RELEVANT FOR

ASIAN DEVELOPING ECONOMIES

A study by the Asia-Pacific Research and Training Network on Trade

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 2/215

The secretariat of the ESCAP is the regional development arm of the United Nations and

serves as the main economic and social development centre of the United Nations in Asia

and the Pacific. Its mandate is to foster cooperation between its 53 members and

9 associate members. It provides the strategic link between global and country-level

programmes and issues. It supports governments of countries in the region in consolidatingregional positions and advocates regional approaches to meeting the region’s unique

socio-economic challenges in a globalizing world. The ESCAP secretariat is located in

Bangkok, Thailand. Please visit the ESCAP website at www.unescap.org for further

information.

Asia-Pacific Research and Training Network on Trade (ARTNeT) is an open regional

network of research and academic institutions specializing in international trade policy and

facilitation issues. Network members currently include over 40 leading national trade

research and academic institutions from 23 developing countries from East, South, and

Southeast Asia and the Pacific. IDRC, UNCTAD, UNDP, ESCAP and the WTO, as core

network partners, provide substantive and/or financial support to the network. The Trade

and Investment Division of ESCAP, the regional branch of the United Nations for Asia andthe Pacific, provides the Secretariat of the network and a direct regional link to trade

policymakers and other international organizations. For more information, please contact

the ARTNeT Secretariat at [email protected] or visit artnet.unescap.org.

The shaded areas of the map are ESCAP members and associate members.

ARTNeT

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 3/215

ARTNeT

Trade performance andcompetitiveness: Selected

issues relevant for Asian

developing economies

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 4/215

TRADE PERFORMANCE AND COMPETITIVENESS:

SELECTED ISSUES RELEVANT FOR ASIAN DEVELOPING

ECONOMIES

A STUDY OF THE ASIA-PACIFIC RESEARCH AND TRAINING NETWORK ON TRADE

United Nations publication

Sales No. E.14.II.F.3

Copyright @ United Nations 2013

All rights reserved

Manufactured in Thailand

ISBN: 978-92-1-120673-9

eISBN: 978-92-1-056600-1

ST/ESCAP/2686

Reference to dollars ($) are to United Stated dollars unless otherwise stated.

Disclaimer

The designations employed and the presentation of the material in this publication do notimply the expression of any opinion whatsoever on the part if the Secretariat of the United

Nations concerning the legal status of any country, territory, city or area of its authorities, or

concerning the delimitation of its frontiers or boundaries.

The opinions, figures and estimates set forth in this publication are the responsibility of the

authors and should not necessarily be considered as reflecting the views or carrying the

endorsement of the United Nations.

Mention of firm names and commercial products does not imply the endorsement of the

United Nations.

All material in this publication may be freely quoted or reprinted, but acknowledgment is

required, together with a copy of the publication containing the quotation or reprint.

The use of this publication for any commercial purpose, including resale, is prohibited

unless permission is first obtained from the secretary of the Publication Board, United

Nations, New York.

Request for permission should state the purpose and the extent of the reproduction.

This publication has been issued without formal editing.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 5/215

iii

Foreword

This volume comprises four selected research essays on different aspects of trade

and industry issues in the Asian region.1 They are written by researchers in Asian

countries, brought together by the Asia-Pacific Research and Training Network on Trade(ARTNeT) which from April 2011 until September 2013 has implemented its Phase III under

the topic of “Drivers of Competitiveness and Strategies for Economic Diversification for

Developing Countries – Building Policy Making Capacity in Asia and the Pacific”. The latest

phase of ARTNeT reflects the diversity and breadth of research interests, as well as the

depth of research talent, available in the region and harnesses these assets in addressing

the major development policy issues facing developing Asian countries. Since its

establishment ARTNeT has focused the efforts of the network on ensuring that research

institutions of the Asia-Pacific region, particularly those in least developed countries,

provide more relevant and higher-quality applied research and policy recommendations topolicymakers. ARTNeT and its members and associates have endeavored to produce high

quality and relevant studies on trade issues on the basis of a demand-driven research

programme, to improve the communication and dissemination of research study results of

research institutions to policymakers; and to increase the capacity of research institutions in

the region, especially in the least developed countries. All of this has been done with the

aim of making trade and investment related research more useful and accessible to

policymakers who are thus better informed and able to design and prepare for

implementation of coherent trade and investment related policies for inclusive development.

With the success of the previous phases ARTNeT has evolved to be one of the

leading networks of researchers, analysts and policymakers in the region. Its acceptance

as an active and unique network seems fully justified when viewed from its membership

which is cohesive, professionally credible and mutually supportive. The growth and

extensive outputs of the network in itself speaks volumes about the relevance of the

network and the demand for its quality outputs. The interest in the capacity building and

training conducted by ARTNeT has grown at a similar pace and it testifies to the strong

need for organizations like ARTNeT to continue addressing gaps in capacity within the

Asia-Pacific.

The studies in this volume and other research produced under the ARTNeT

Phase III Research programme (available through ARTNeT’s website) are produced with

the aim of addressing these explicit and implicit demands of the Asia-Pacific countries and

to fill in the gaps in capacity and knowledge. The studies are of significance and interest to

researchers and policy analysts alongside policymakers. This is primarily because they

look at previously unexplored issues using new and innovative analytical and

methodological approaches, which can be drawn on to conduct similar studies in the

region. We hope that these will stimulate further work on these important issues.

1 The volume carries only several of the studies that were conducted under this programme phase reflecting

the efforts towards reducing the volume of printed publications and a gradual shift to online release only. The

other studies undertaken under this phase are available in electronic copies.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 6/215

iv

Acknowledgments

The authors of the studies and the ARTNeT secretariat received invaluable

research guidance, constructive comments and suggestions from advisor to this project

Professor Sisira Jayasuriya, Monash University, Australia, and other experts whom theauthors have acknowledged for specific studies. The project was coordinated by Dr. Mia

Mikic, Chief, Trade Policy and Analysis Section, ESCAP under the general guidance of

Dr. Ravi Ratnayake, Director, Trade and Investment Division, ESCAP. The authors have

also had the opportunity to discuss their methodology and preliminary findings during the

ARTNeT conference on “Empirical and policy issues of integration in Asia and the Pacific”

on 1 to 2 November 2012 held in Colombo, Sri Lanka, in which the discussants, Mr. Denis

Hew, Mr. Jason Lao, Mr. Sarath Rajapatirana, Dr. Nagesh Kumar and other participants

provided very useful comments and suggestions. Notwithstanding this, any remaining

errors and omissions in this publication should be attributed to the authors only and not tothe advisors and benevolent commentators. There are many other people that needed to

be thanked, without implicating them in the views expressed in this volume, for assisting

through the process, since the design of ARTNeT Phase III until preparation of these

selected studies for the publication. These include Ms. Melanie Ramjoue who contributed

to the formulation of the Phase III programme and Mr. Adam Heal who has coordinated the

preparation of the book for print. The studies in the book were edited by Ms. Nicole Colmar

and other research under the programme by Mr. Robert Oliver both of whom should

be thanked for more uniform style of the material presented but should not be blamed

for the content remaining. Ms. Panjai Limchupong, Ms. Tavitra Ruyaphorn andMs. Chaveemon Sukpaibool have all contributed in different but important ways towards

the fruition of the project. Mr. Teemu Alexander Puutio has provided technical support to the

ARTNeT Secretariat and also, with Yisi Chen, the idea for the cover page of the book. The

International Development Research Centre’s support since the establishment of ARTNeT

and during this phase is gratefully acknowledged. This support proved to have been the

factor that made an important difference in the effectiveness of research capacity-building

in the trade and trade-related areas under ARTNeT since 2004. This, combined with

a significant substantive contribution from the ESCAP secretariat as well as a technical

support in the implementation of the projects, have been instrumental in the growingpresence of ARTNeT in the region.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 7/215

v

Contents

Page

Foreword ................................................................................................................ iii

Acknowledgments ................................................................................................ iv

List of contributors ............................................................................................... xi

Acronyms and Abbreviations .............................................................................. xiii

Overview ................................................................................................................ xv

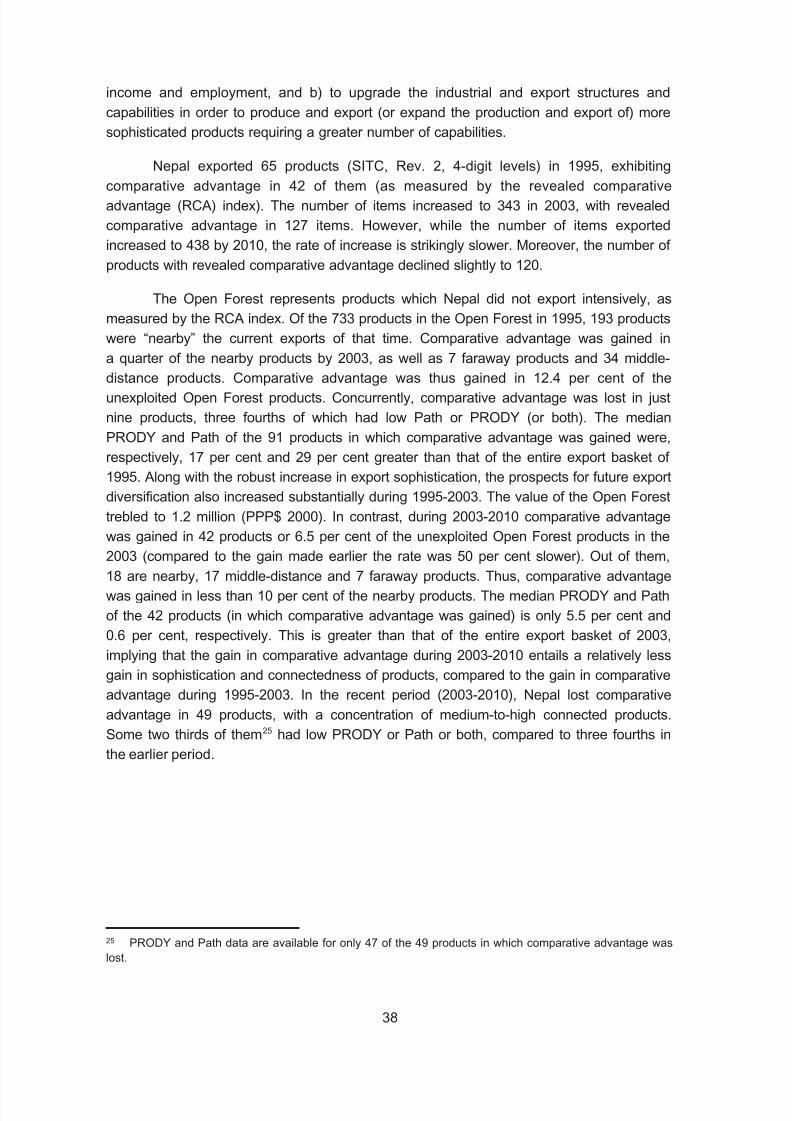

I. Structural transformation and trade policy: Case of Nepal .................... 1

Paras Kharel

A. Review of literature on structural transformation .................................... 2

B. Nepal’s economic and export performance: A preliminary analysis ....... 9

C. Structural change and productivity growth in Nepal’s economy ............. 19

D. Nepal’s trade and industrial policies in the context of structural

transformation ........................................................................................ 24

E. Methodology for assessing structural transformation through the

“export” lens ........................................................................................... 30

F. Analysis of export baskets and identified products ................................ 34

G. Analysis of targeted products ................................................................. 45

H. Discussion .............................................................................................. 57

Conclusion ..................................................................................................... 66

References .................................................................................................... 69

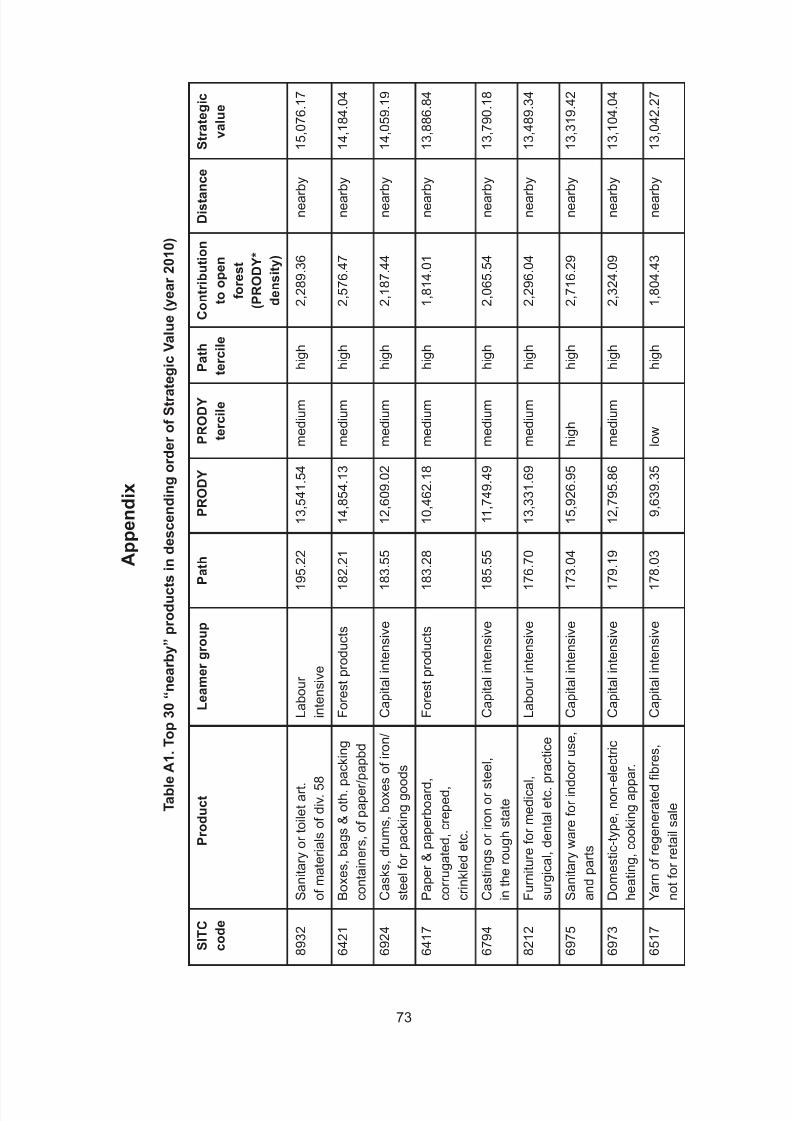

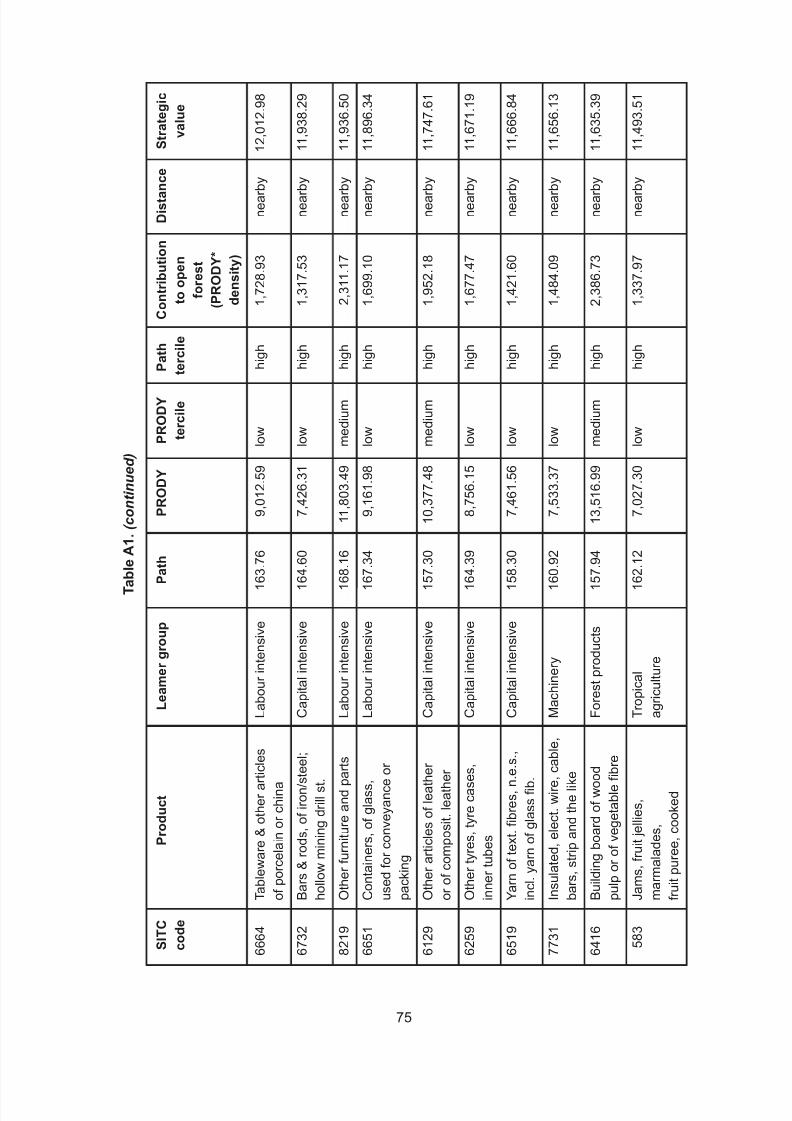

Appendix ....................................................................................................... 73

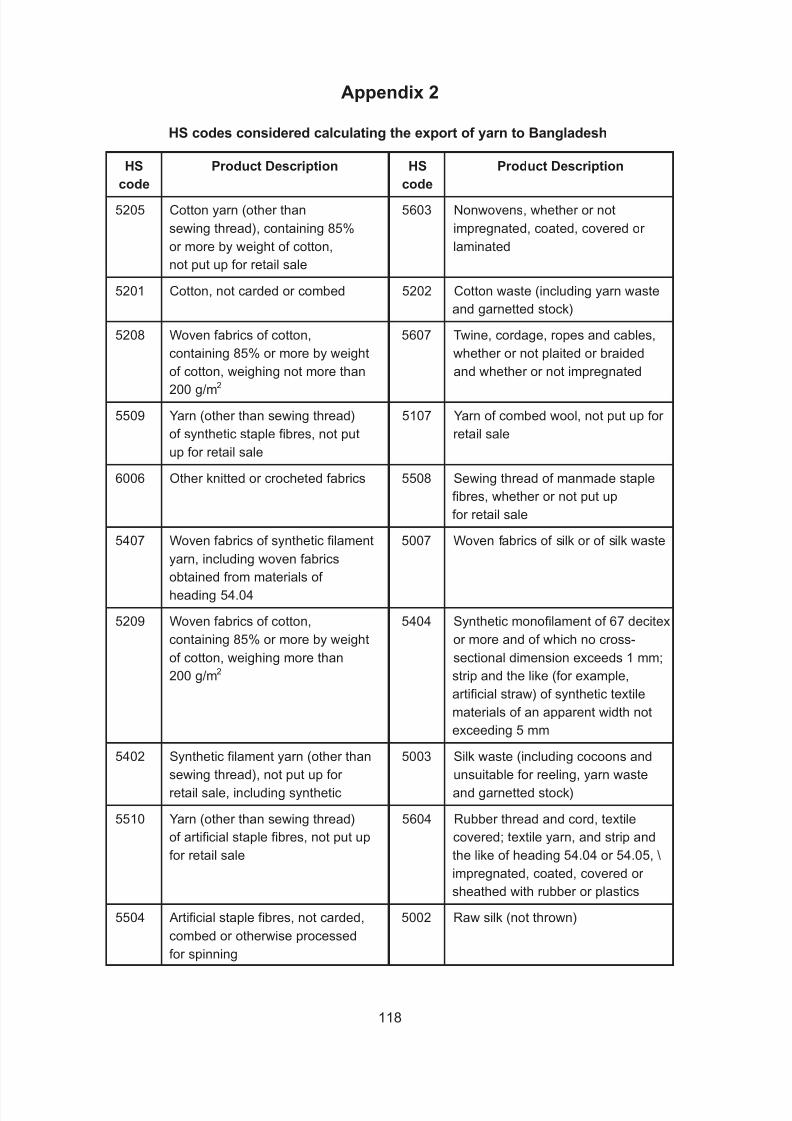

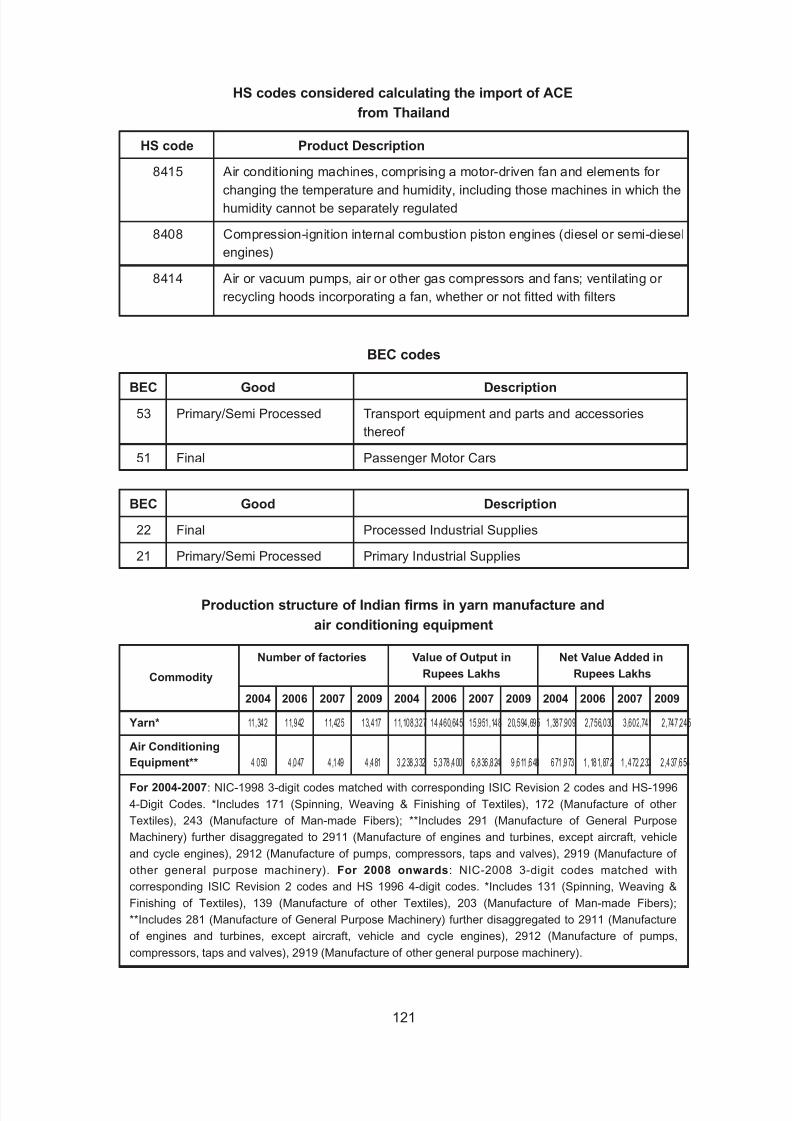

II. Logistics performance and trade: An analysis of India’s trade inintermediates with Bangladesh and Thailand .......................................... 91

Prabir De and Amrita Saha

A. Logistics services and production networks: Literature review .............. 92

B. Data and methodology ........................................................................... 95

C. India’s trade with Bangladesh and Thailand........................................... 97

D. Measuring logistics performance ........................................................... 103

E. Does improvement in logistical services lead to higher trade inintermediate goods? ............................................................................... 106

Summary and implications ............................................................................ 112

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 8/215

vi

References .................................................................................................... 114

Appendix ....................................................................................................... 117

III. An analysis of export performance of manufacturing and service

sector enterprises in Sri Lanka .................................................................. 131

JeevikaWeerahewa, Sarath S. Kodithuwakku and Rifana Buhary

A. A model to assess determinants of export performance ........................ 132

B. Data description ..................................................................................... 133

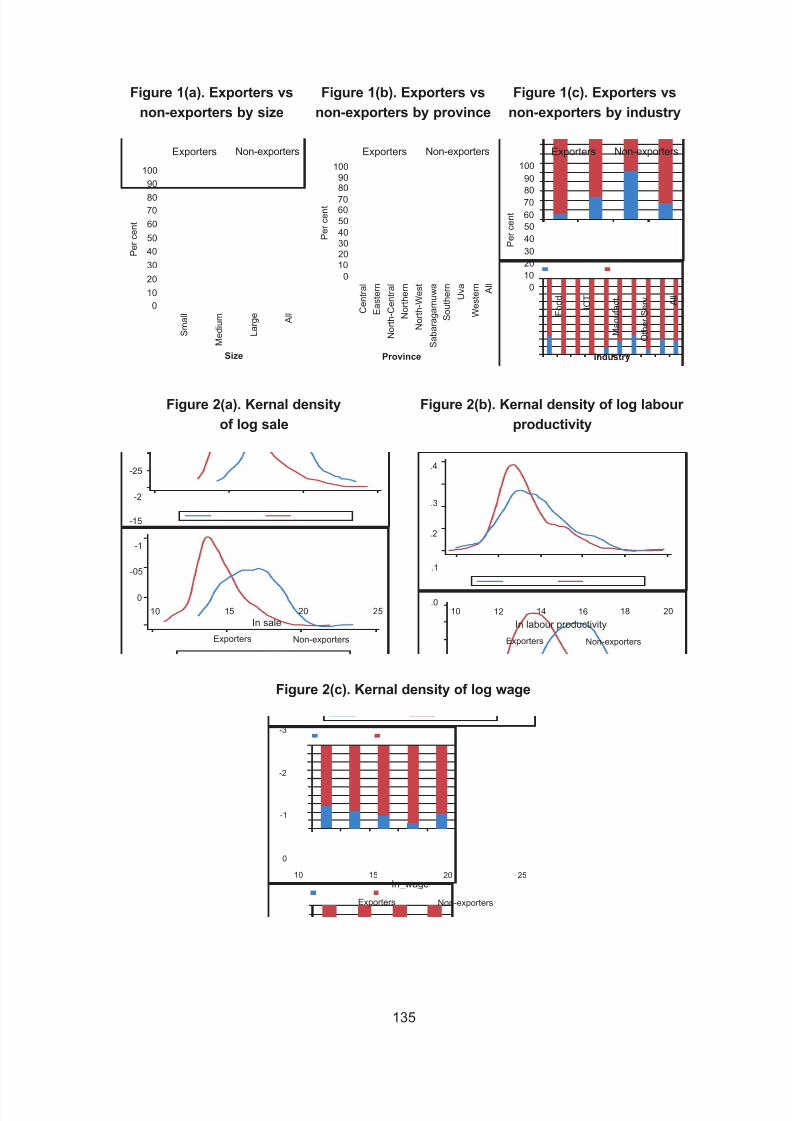

C. Characterization of exporting firms versus non exporting firms ............. 134

D. Results of the estimation of Heckman model ......................................... 139

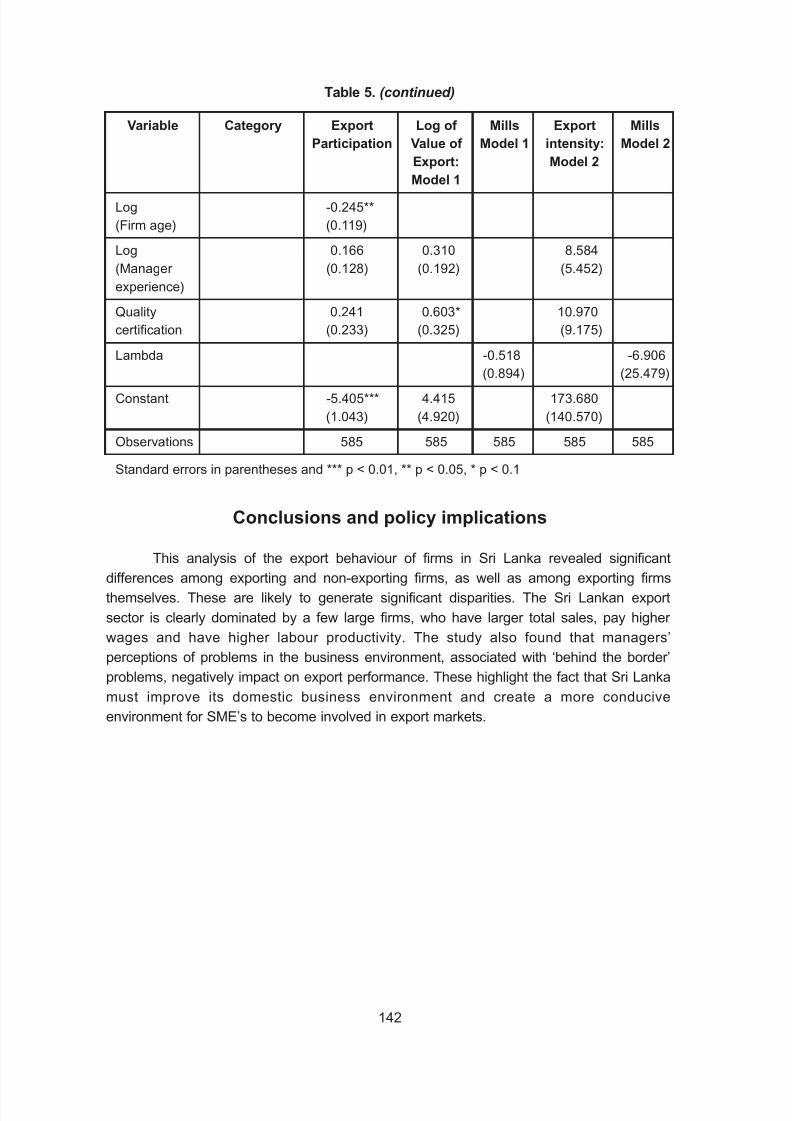

Conclusions and policy implications .............................................................. 142

References .................................................................................................... 143

Appendix ....................................................................................................... 145

IV. Evaluation of business association membership on small and

medium enterprises’ growth performance: Evidence from enterprisesurvey of Cambodia .................................................................................... 147

Vathana Roth

A. Literature review and theoretical aspects ............................................... 149

B. Econometric specifications and variables measurement ....................... 152

C. Data source and descriptive statistics .................................................... 156

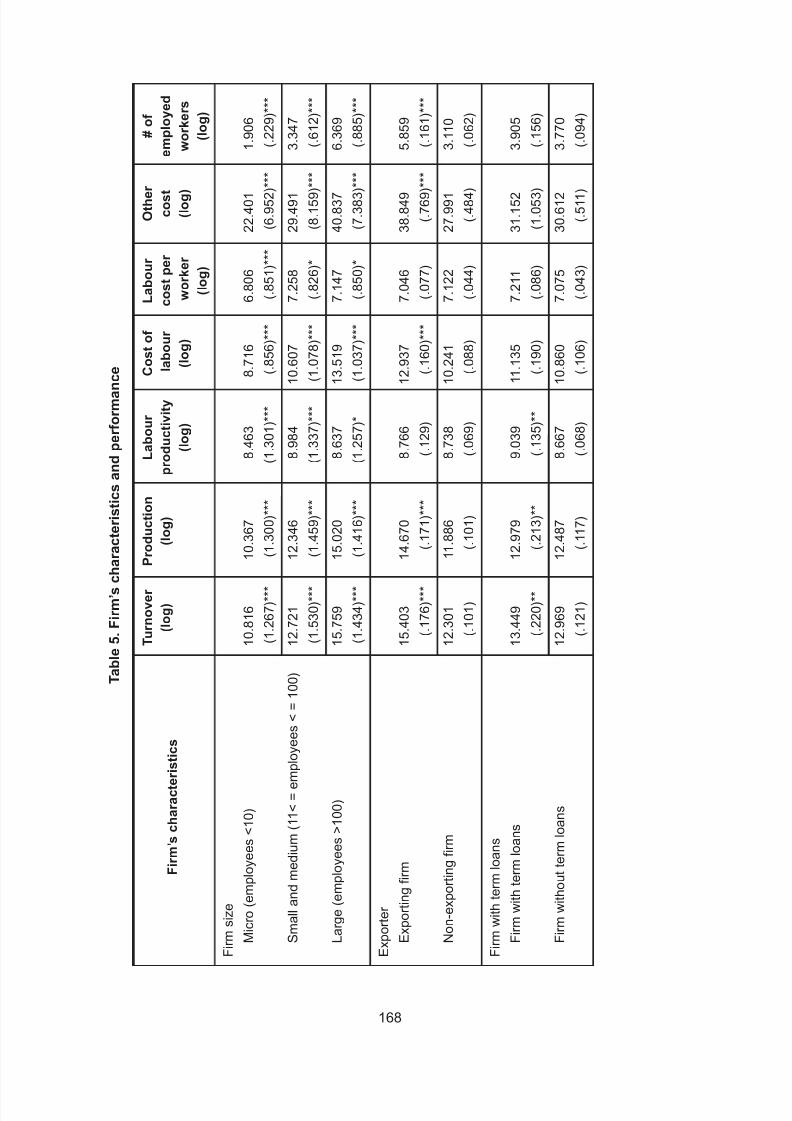

D. Regression results and discussion ......................................................... 158

E. Limitations .............................................................................................. 162

Conclusion and areas for future research ..................................................... 162

Annex ............................................................................................................ 164

References .................................................................................................... 188

Contents (continued)

Page

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 9/215

vii

List of Tables

Chapter I

Table 1. Nepal in comparative perspective: Trade performance .......................... 13

Table 2. Decomposition of Nepal’s labour productivity growth during 1999-2008 20

Table 3. Sectoral employment, value added shares and their change, and

productivity level and growth (Nepal) ..................................................... 22

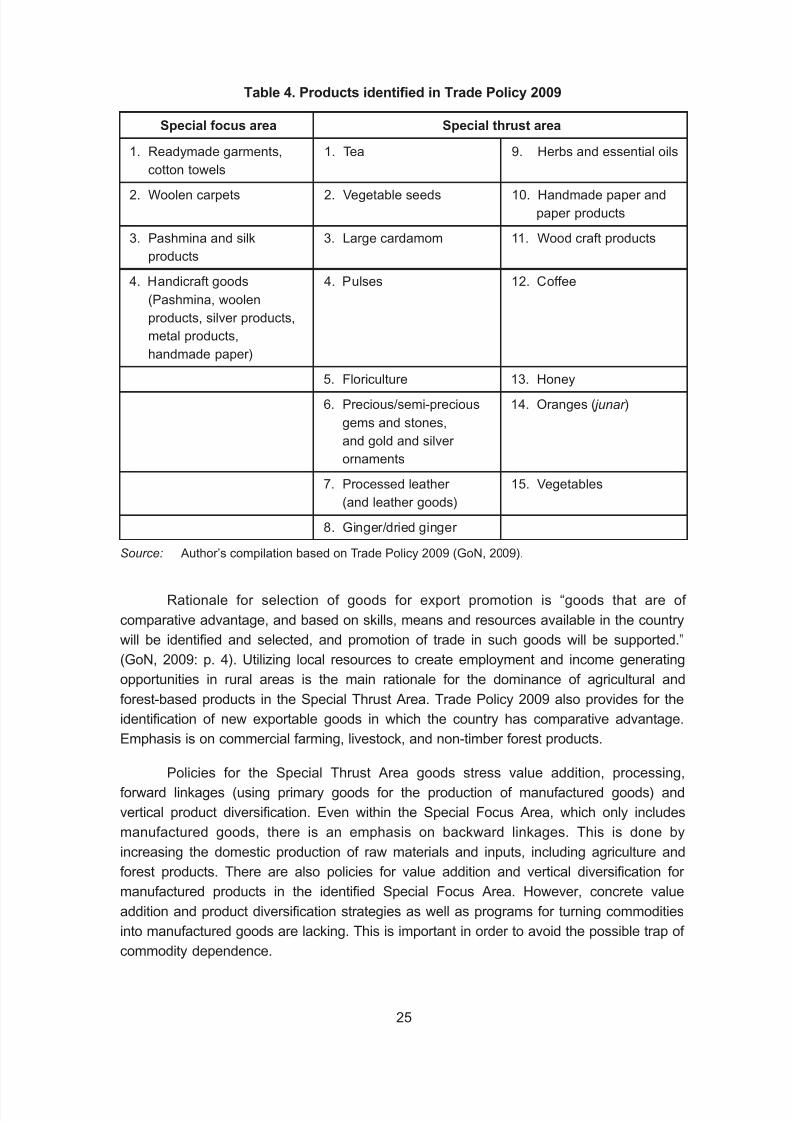

Table 4. Products identified in Trade Policy 2009 ................................................ 25

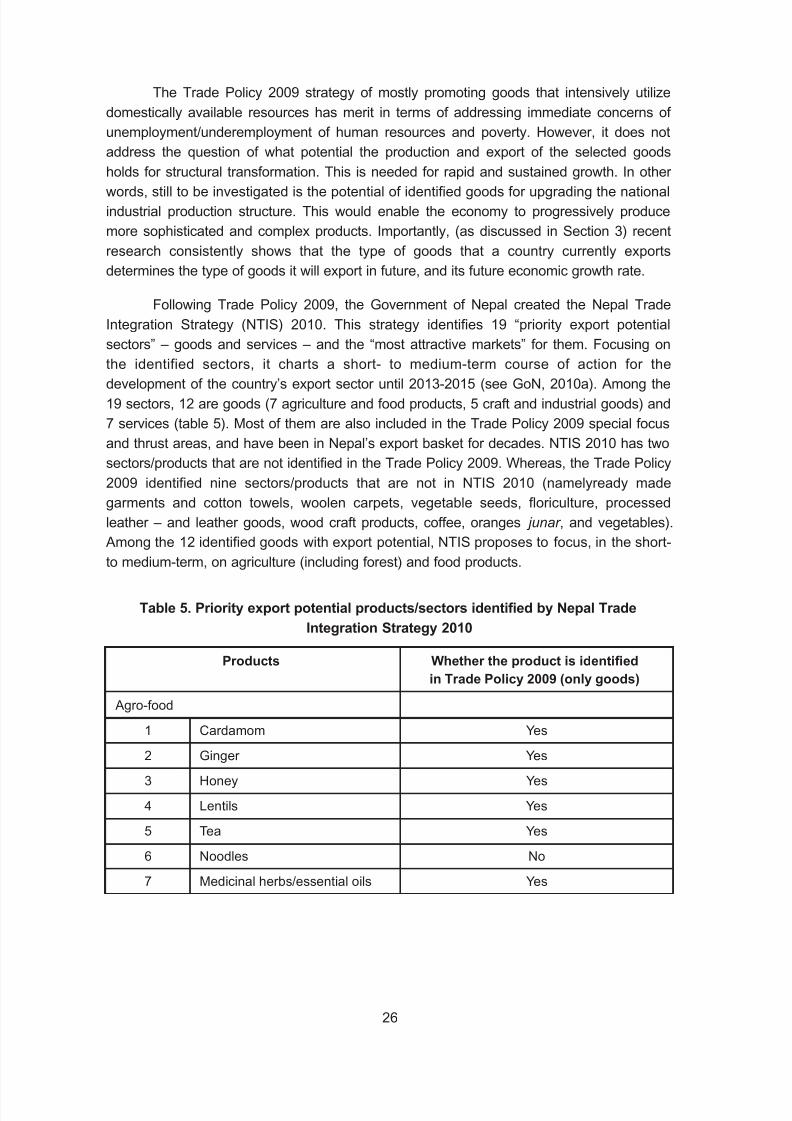

Table 5. Priority export potential products/sectors identified by Nepal TradeIntegration Strategy 2010 ....................................................................... 26

Table 6. Features of export basket in 2010.......................................................... 40

Table 7. Top 10 nearby products, ordered by Strategic Value ............................. 41

Table 8. Top 10 middle-distance products, ordered by Strategic Value ............... 42

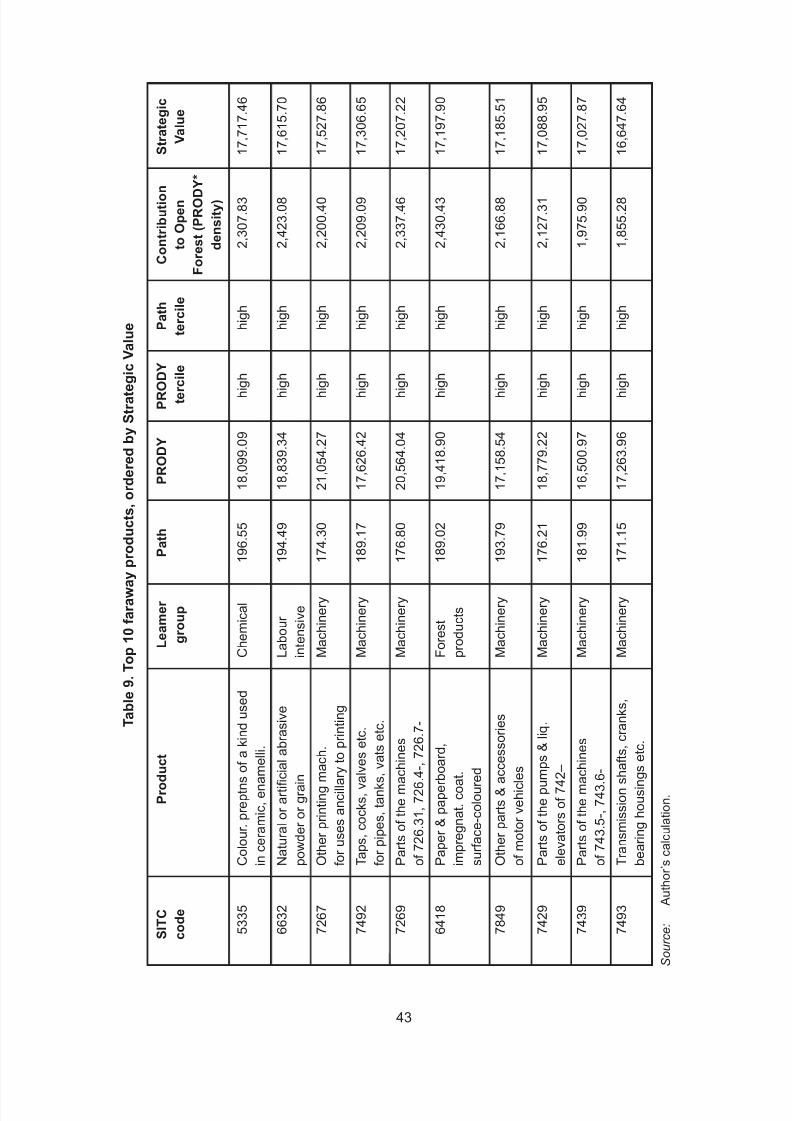

Table 9. Top 10 faraway products, ordered by Strategic Value............................ 43

Table 10. Products in Open Forest according to Leamer classification ................. 44

Table 11. Summary features of NTIS-identified products ...................................... 46

Table 12. Summary statistics of PRODY, Path and Strategic Value of across

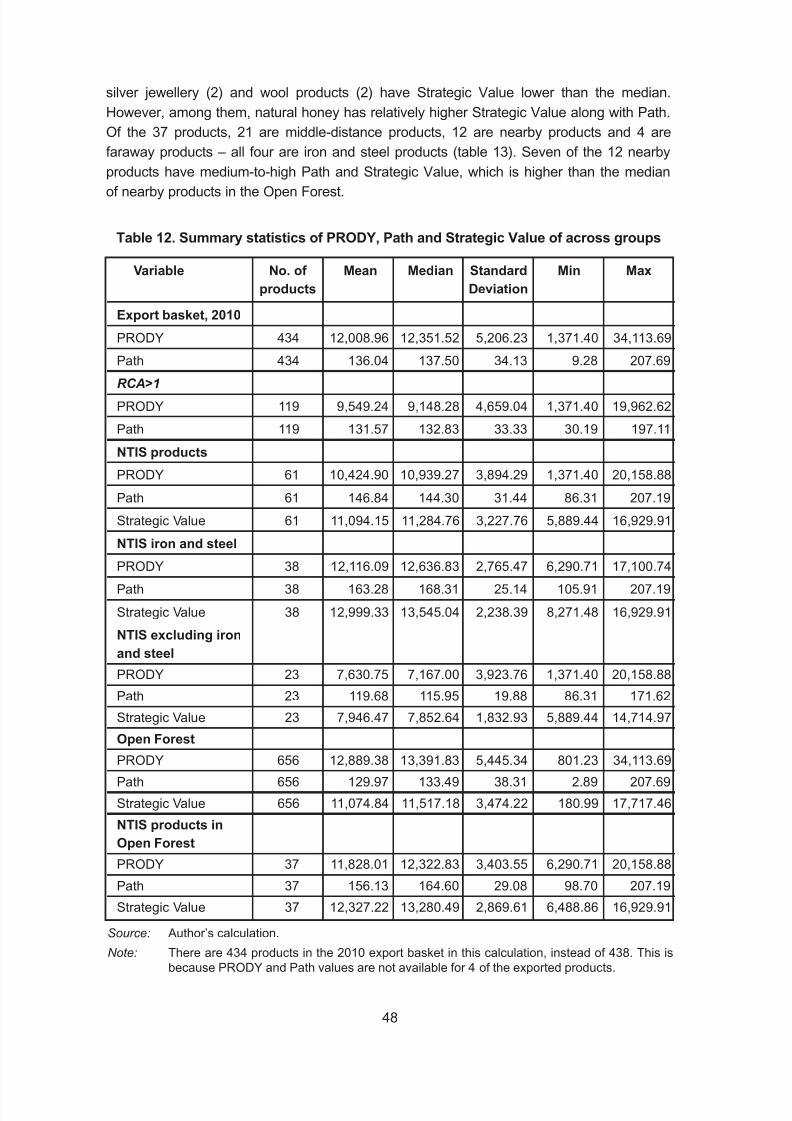

groups .................................................................................................... 48

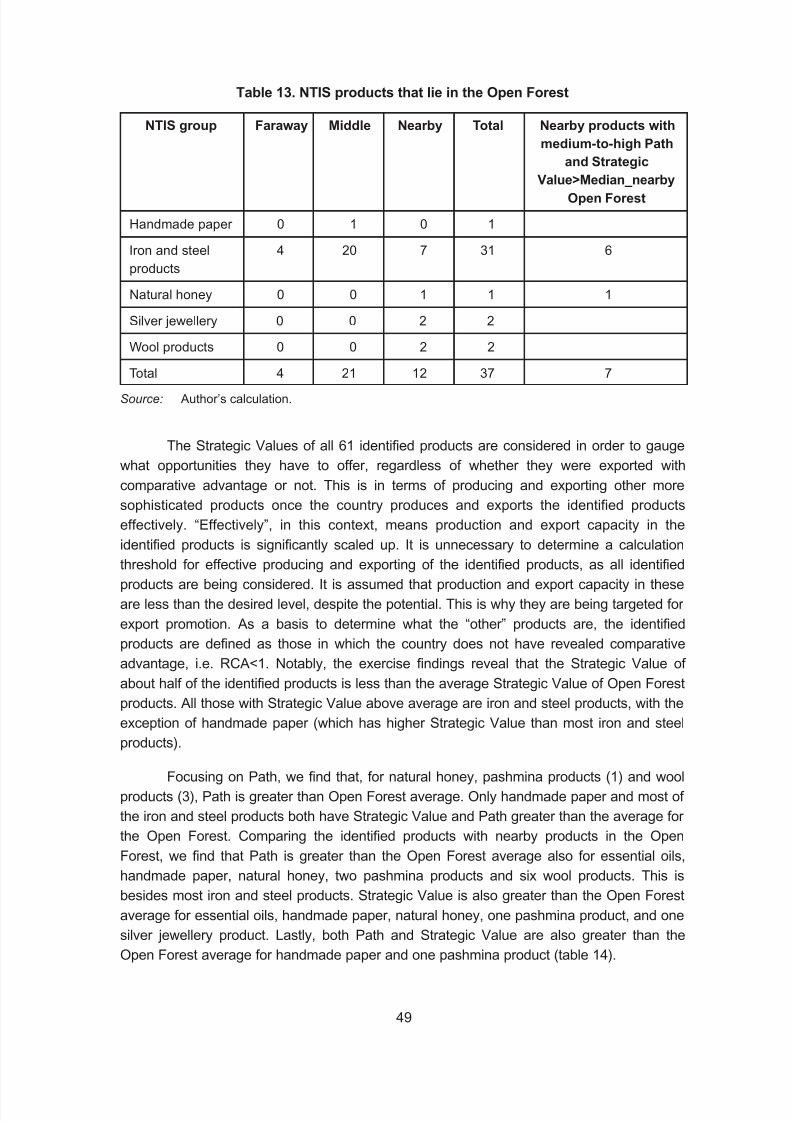

Table 13. NTIS products that lie in the Open Forest .............................................. 49

Table 14. Comparison of NTIS products with export basket and Open Forest ...... 50

Table 15. Summary statistics of Trade Policy identified products .......................... 51

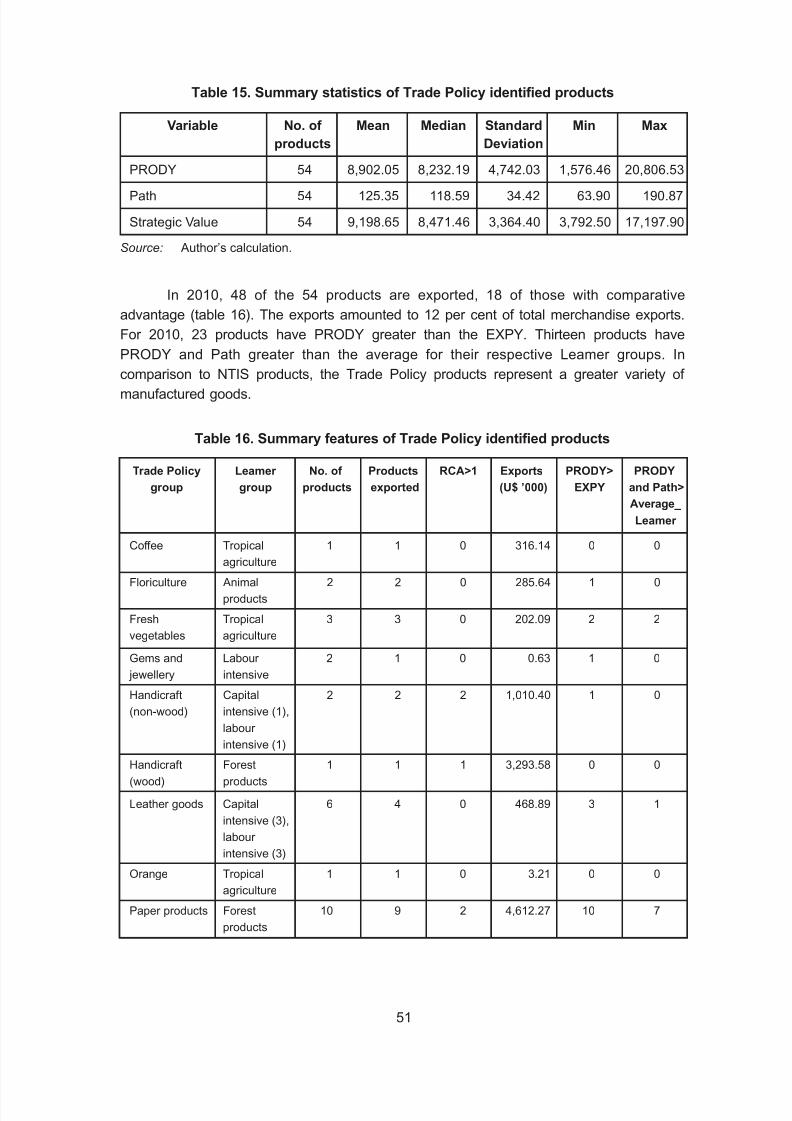

Table 16. Summary features of Trade Policy identified products ........................... 51

Table 17. Distribution of Trade Policy identified products across path terciles ...... 53

Table 18. Number of products exceeding median values of comparator groups ... 54

Table 19. Trade Policy products that lie in the Open Forest .................................. 55

Table 20. Features of “other” NTIS products ......................................................... 56

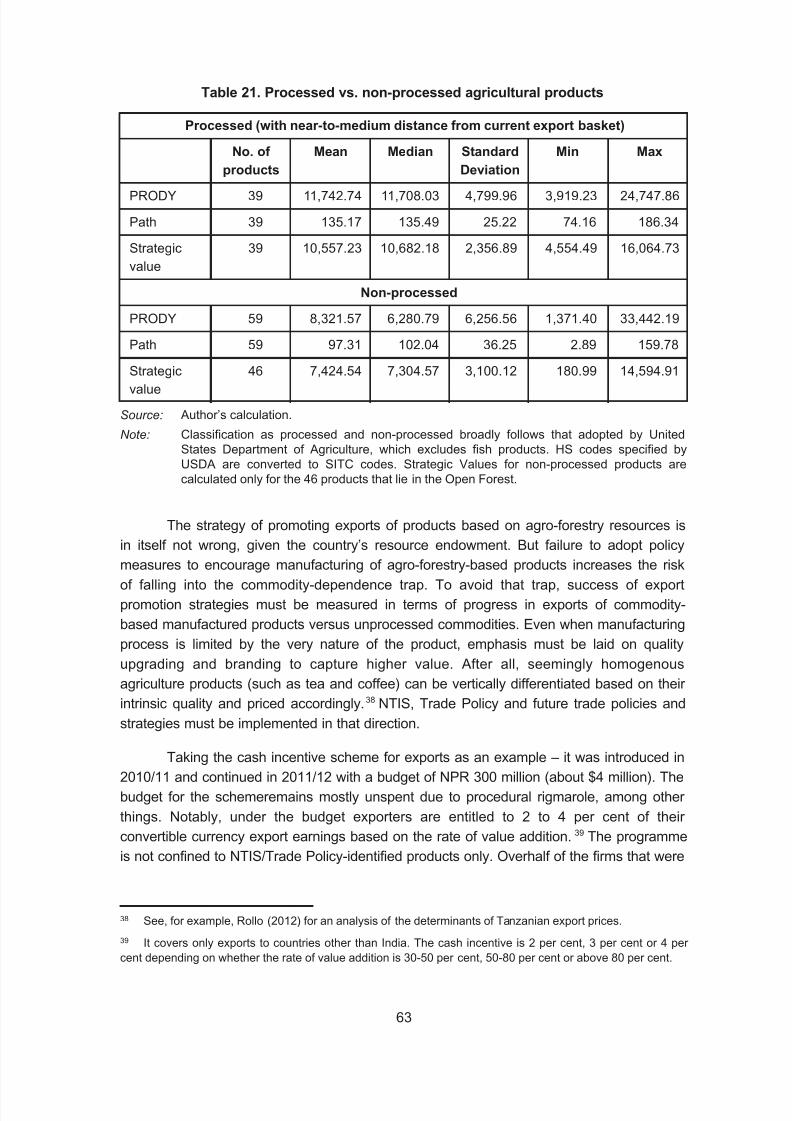

Table 21. Processed vs. non-processed agricultural products .............................. 63

Chapter II

Table 1. India’s imports of ACE from Thailand and export of yarn toBangladesh: 2000-2010 ......................................................................... 98

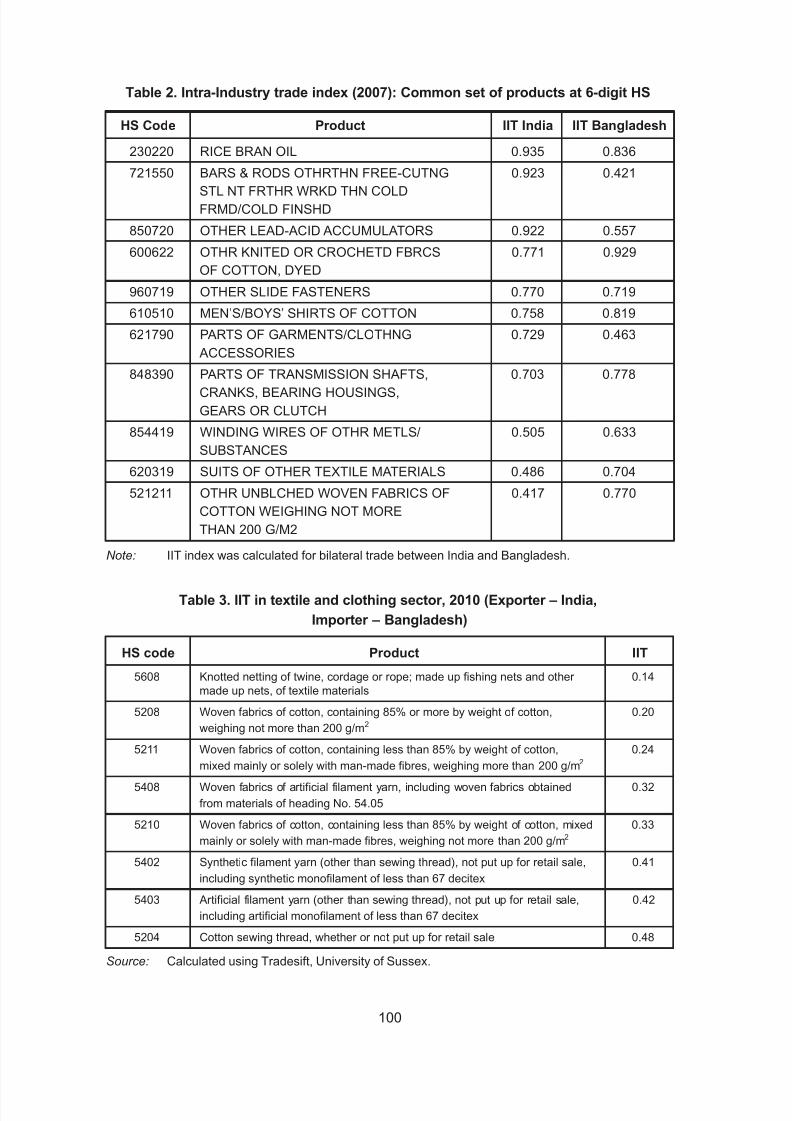

Table 2. Intra-Industry trade index (2007): Common set of products at 6-digit HS 100

Contents (continued)

Page

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 10/215

viii

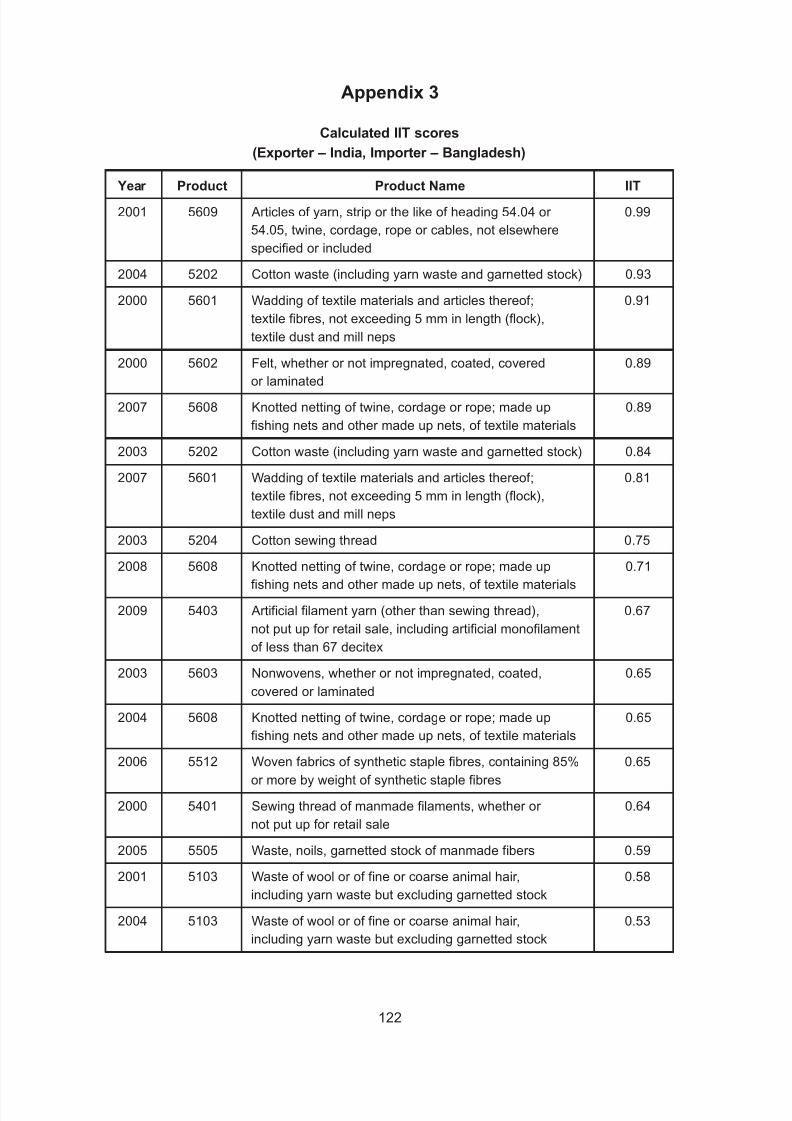

Table 3. IIT in textile and clothing sector, 2010 (Exporter – India, Importer –

Bangladesh) ........................................................................................... 100

Table 4. IIT in air conditioning equipment (Importer – India, Exporter – Thailand) 101

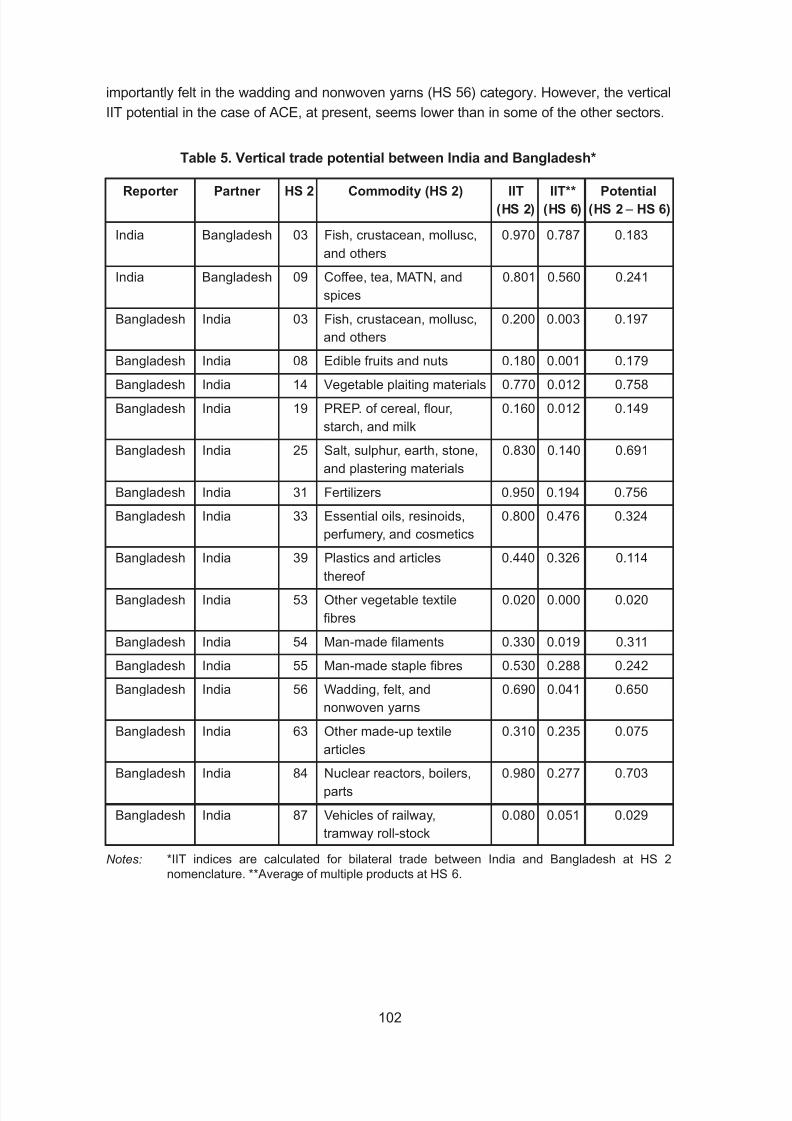

Table 5. Vertical trade potential between India and Bangladesh ......................... 102

Table 6. Vertical trade potential between India and Thailand .............................. 103

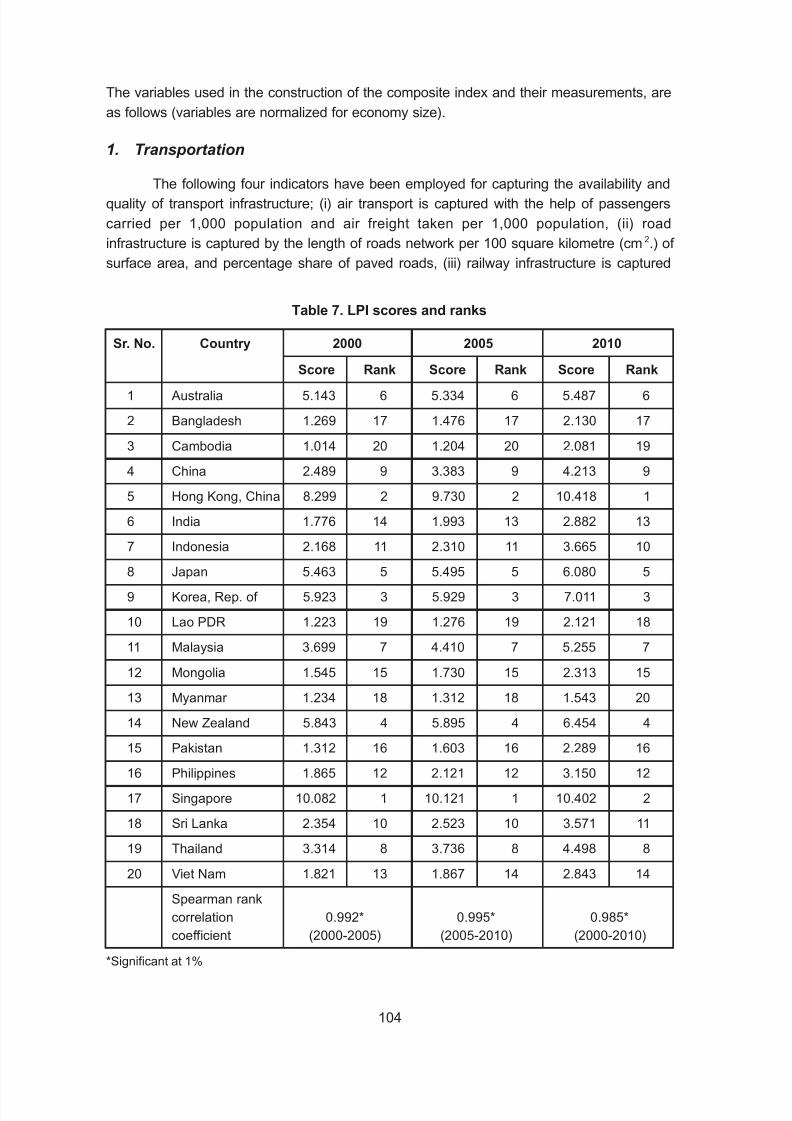

Table 7. LPI scores and ranks ............................................................................. 104

Table 8. Baseline regression (OLS): Fixed effect model ...................................... 106

Table 9. Arellano-Bover dynamic panel-data estimation (System GMM) ............ 108

Table 10. Im, Pesaran and Shin (IPS) panel unit root test (Period: 2000-2010) .... 109

Table 11(a). India’s exports of yarn to Bangladesh: Westerlund panel

co-integration test (Period: 2000-2010) ............................................. 110

Table 11(b). India’s exports of yarn to Bangladesh: Westerlund panel

co-integration test (Period: 2000-2010) ............................................. 111

Table 12. Panel Granger causality test between trade and LPI ............................. 112

Chapter III

Table 1. Heterogeneity of firms by size ................................................................ 136

Table 2. Heterogeneity of firms by industry .......................................................... 136

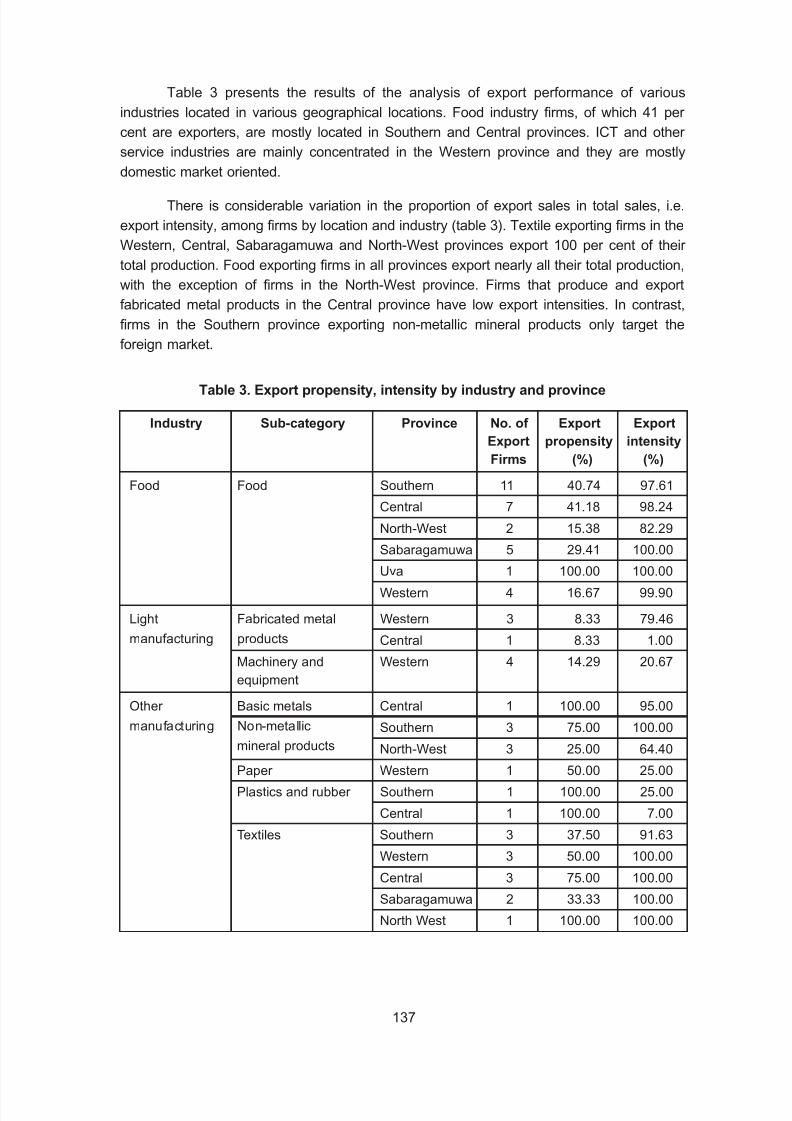

Table 3. Export propensity, intensity by industry and province ............................ 137

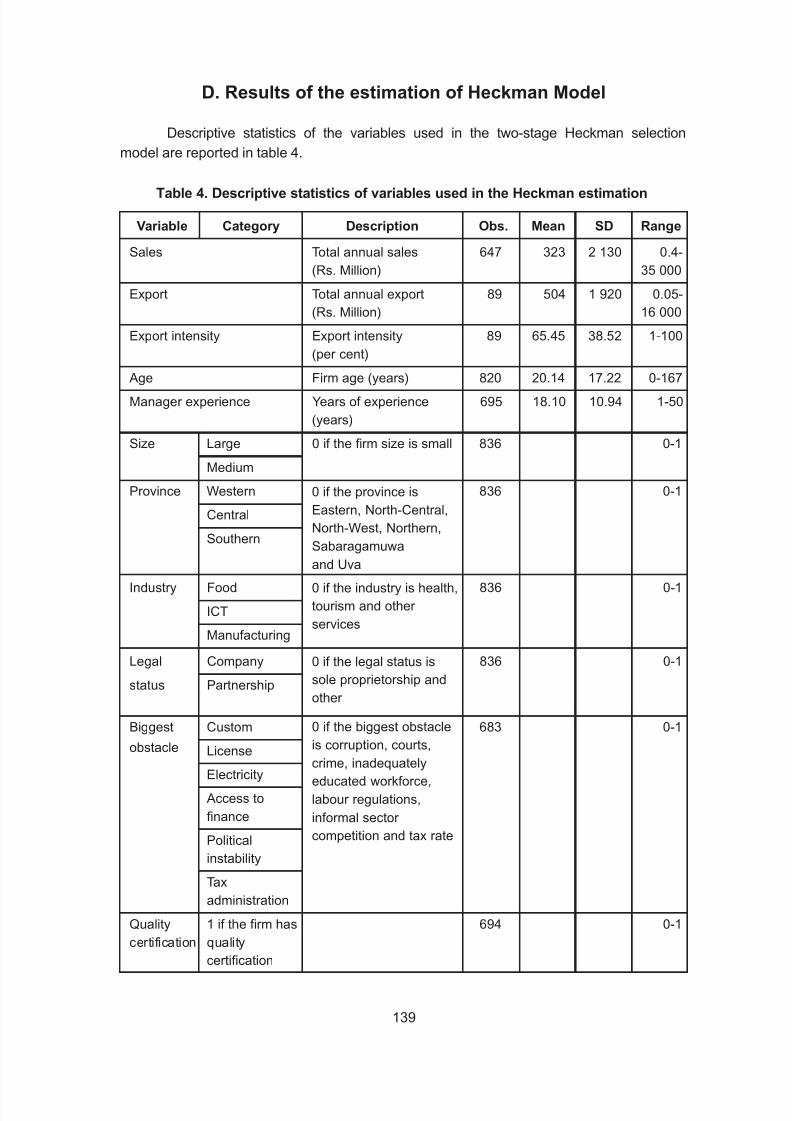

Table 4. Descriptive statistics of variables used in the Heckman estimation ....... 139

Table 5. Results of the Heckman Model estimation ............................................. 141

Chapter IV

Table 1. Classification of enterprises in Cambodia .............................................. 164

Table 2. Distribution of participating and non-participating groups by firm size

and sub-sector ....................................................................................... 164

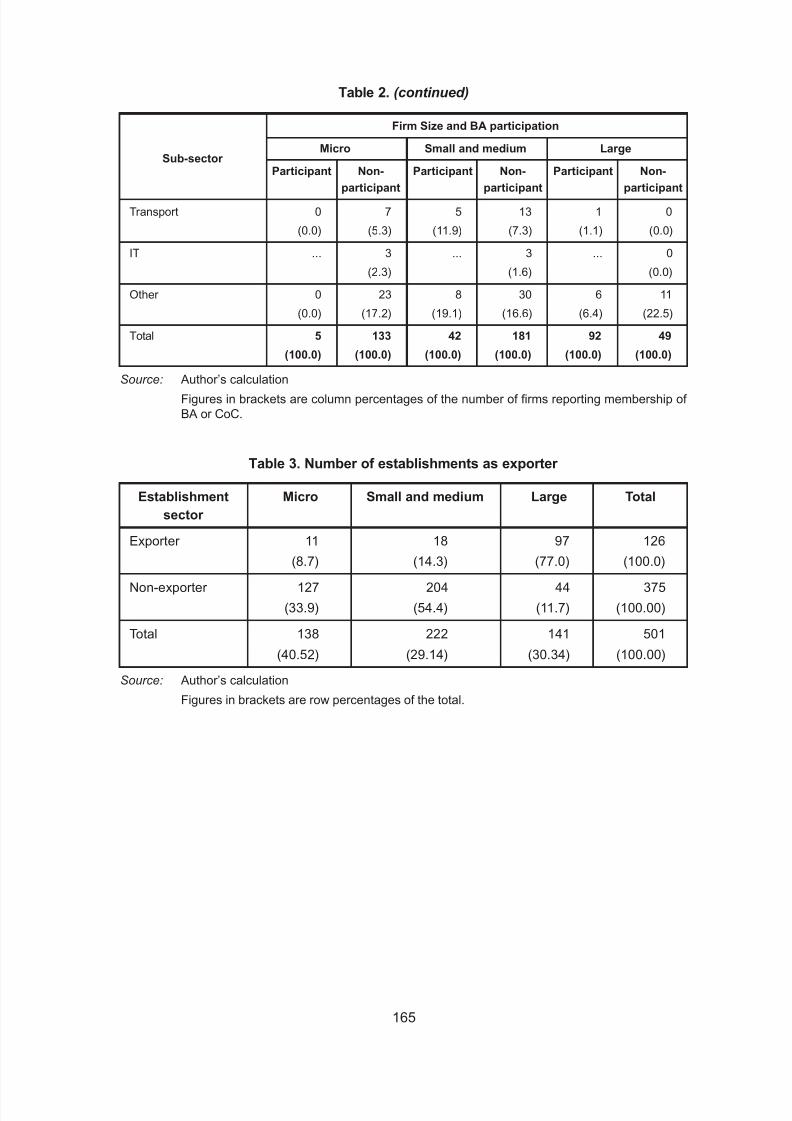

Table 3. Number of establishments as exporter .................................................. 165

Table 4. Membership in business association or chamber of commerce by

firm’s characteristics ............................................................................... 166

Table 5. Firm’s characteristics and performance ................................................. 168

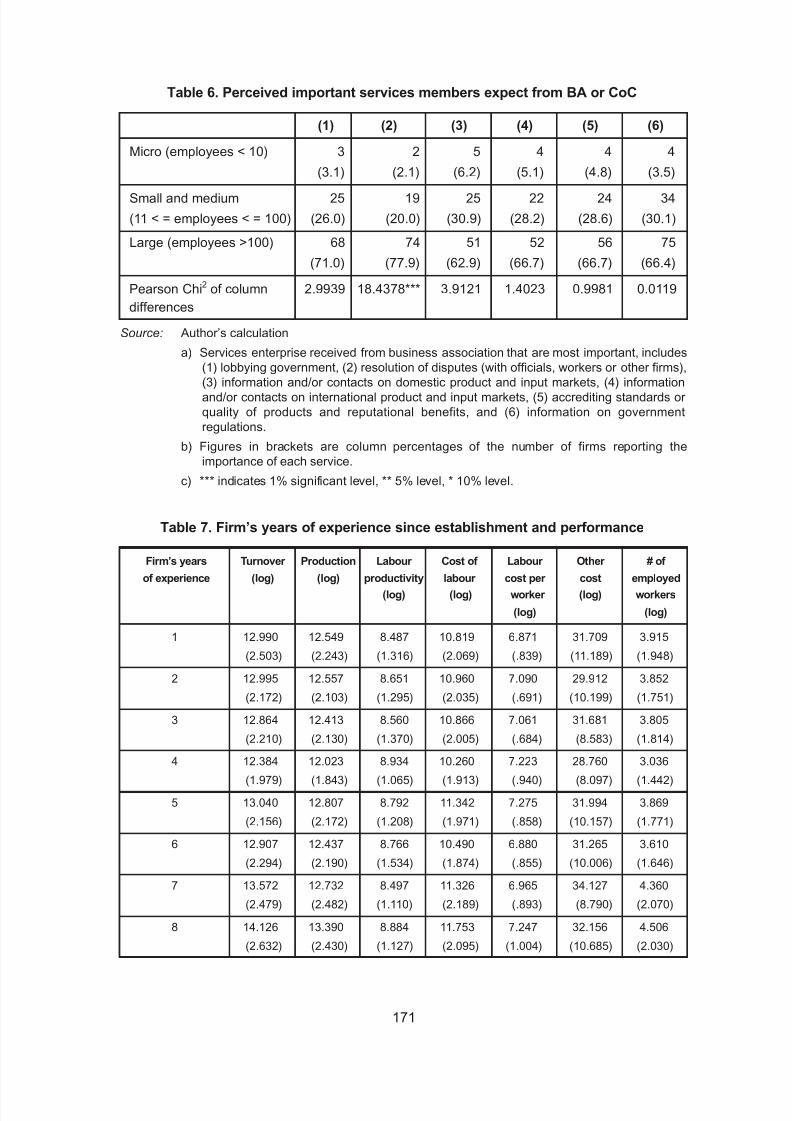

Table 6. Perceived important services members expect from BA or CoC ........... 171

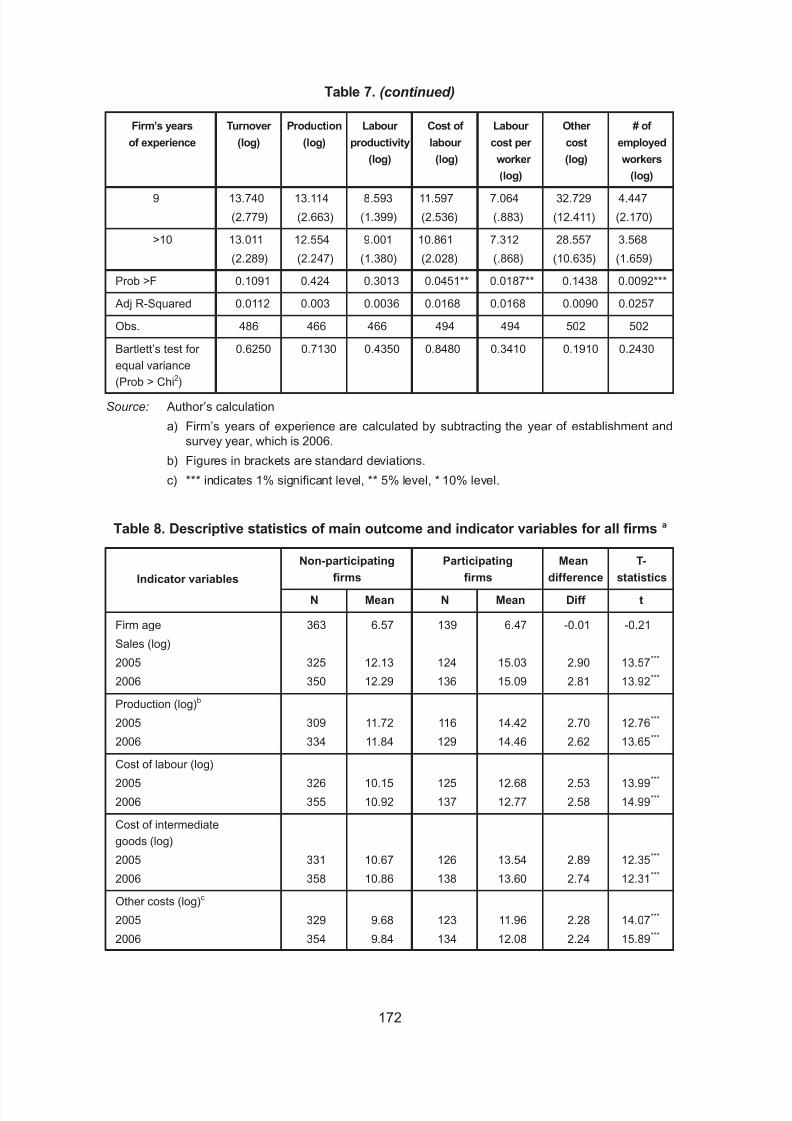

Table 7. Firm’s years of experience since establishment and performance ........ 171

Contents (continued)

Page

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 11/215

ix

Table 8. Descriptive statistics of main outcome and indicator variables for all

firms ....................................................................................................... 172

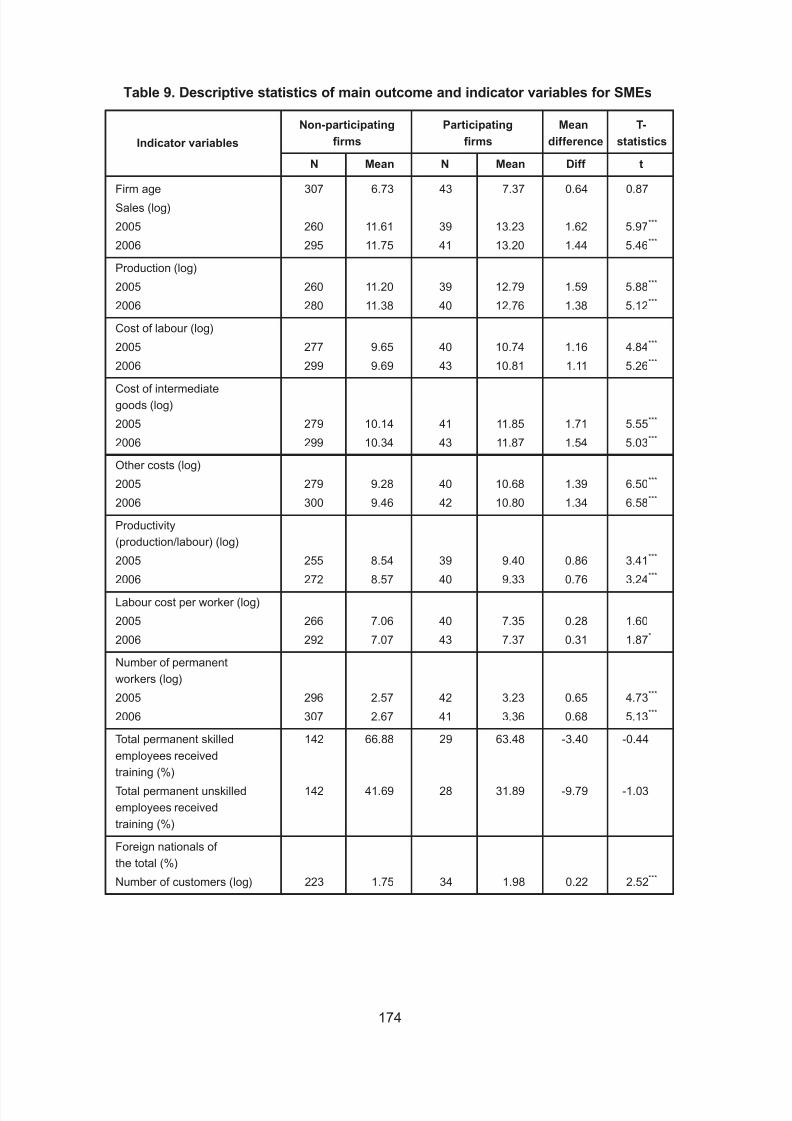

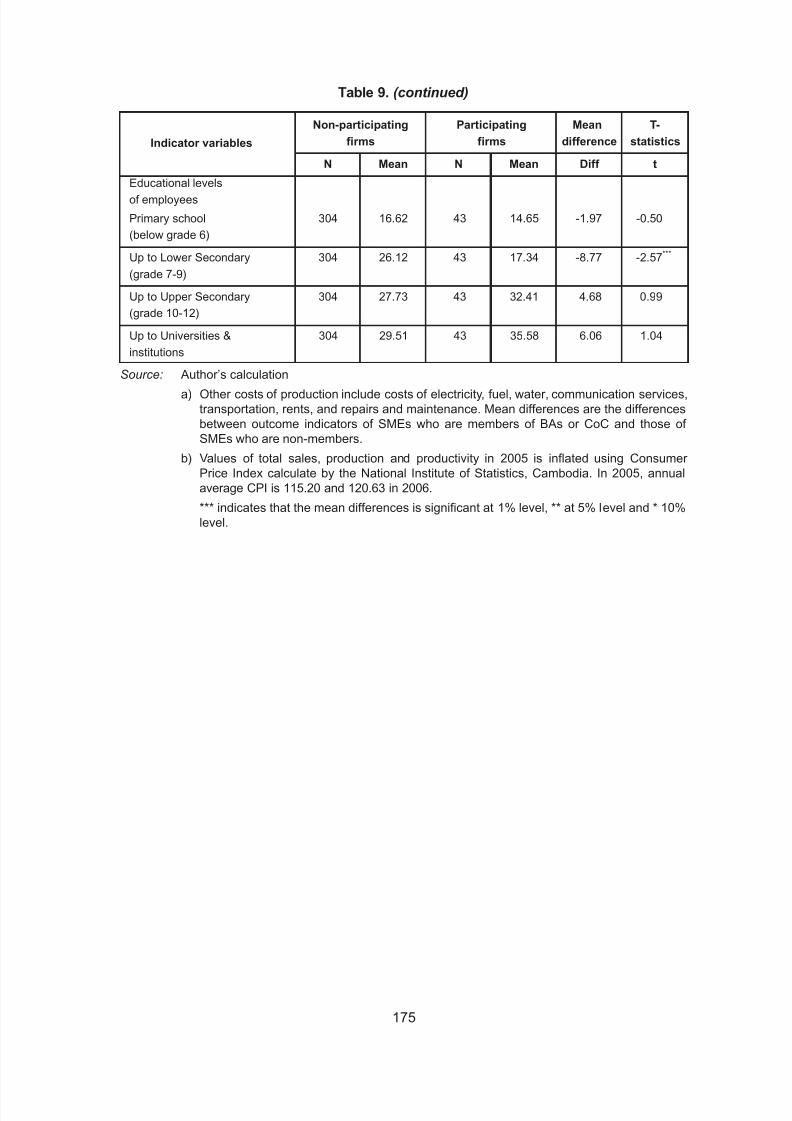

Table 9. Descriptive statistics of main outcome and indicator variables for SMEs 174

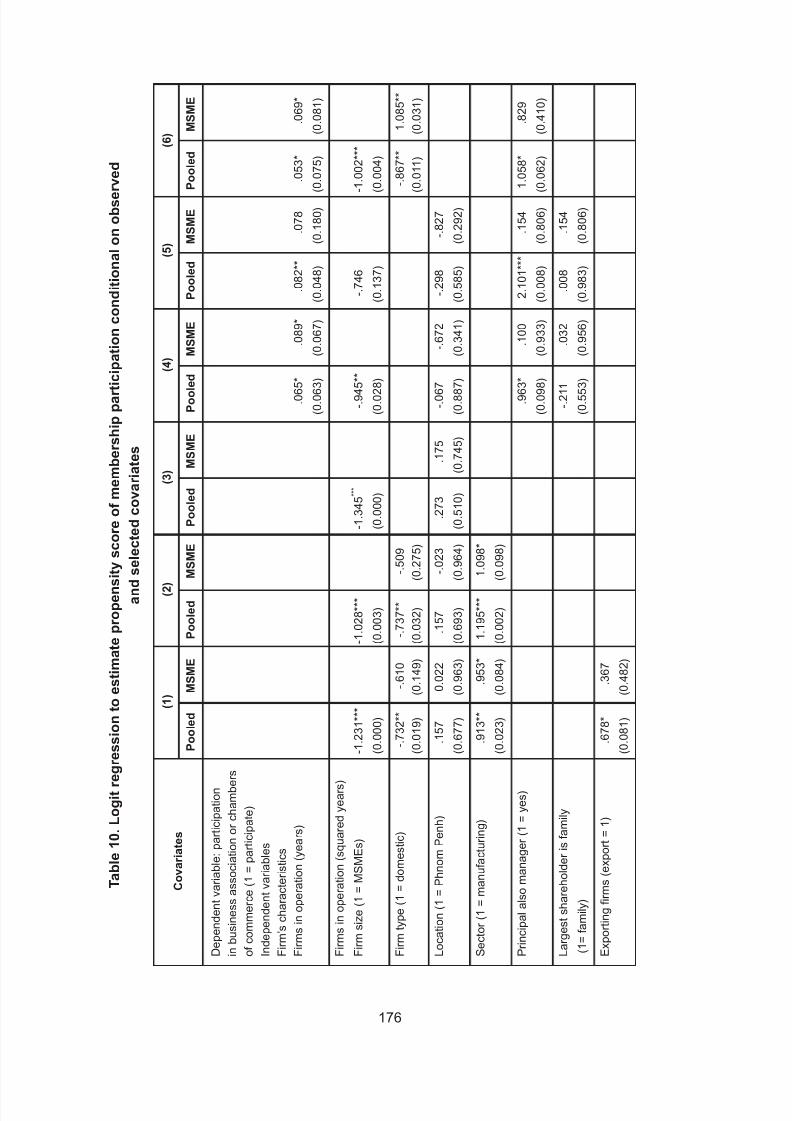

Table 10. Logit regression to estimate propensity score of membership

participation conditional on observed and selected coveriates .............. 176

Table 11. PSM estimation results of memberships in business associations or

chambers of commerce (pooled) ........................................................... 181

Table 12. PSM estimation results of memberships in business associations or

chambers of commerce (SMEs) ............................................................. 182Table 13. OLS estimation results of memberships in business associations or

chambers of commerce .......................................................................... 183

Table 14. PSM & OLS estimation results of memberships in business

associations or chambers of commerce................................................. 184

List of Figures

Chapter I

Figure 1. The product space ............................................................................... 4

Figure 2. Nepal per capita GDP growth performance ......................................... 10

Figure 3. Nepal in comparative perspective: Growth of GDP per capita............. 10

Figure 4. Nepal in comparative perspective: Manufacturing, value added

(per cent of GDP), 2009 ....................................................................... 11

Figure 5. Share of manufacturing in Nepal’s GDP over time .............................. 12

Figure 6. Nepal’s trade performance................................................................... 12

Figure 7. Nepal’s exports of goods and services ................................................ 13

Figure 8. Nepal’s export composition (in terms SITC 1-digit categories) ............ 14

Figure 9. Nepal’s export composition in terms of Leamer categories ................. 15

Figure 10. Comparative export composition – Leamer categories 2010 .............. 17

Figure 11. Major exports ....................................................................................... 17

Figure 12. Nepal’s export composition – Lall classification ................................... 18

Figure 13. Nepal in comparative perspective: Export composition – Lall

classification, 2010 .............................................................................. 19

Contents (continued)

Page

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 12/215

x

Figure 14. Correlation between sectoral productivity and change in employment

shares in Nepal (1999-2008) ............................................................... 21

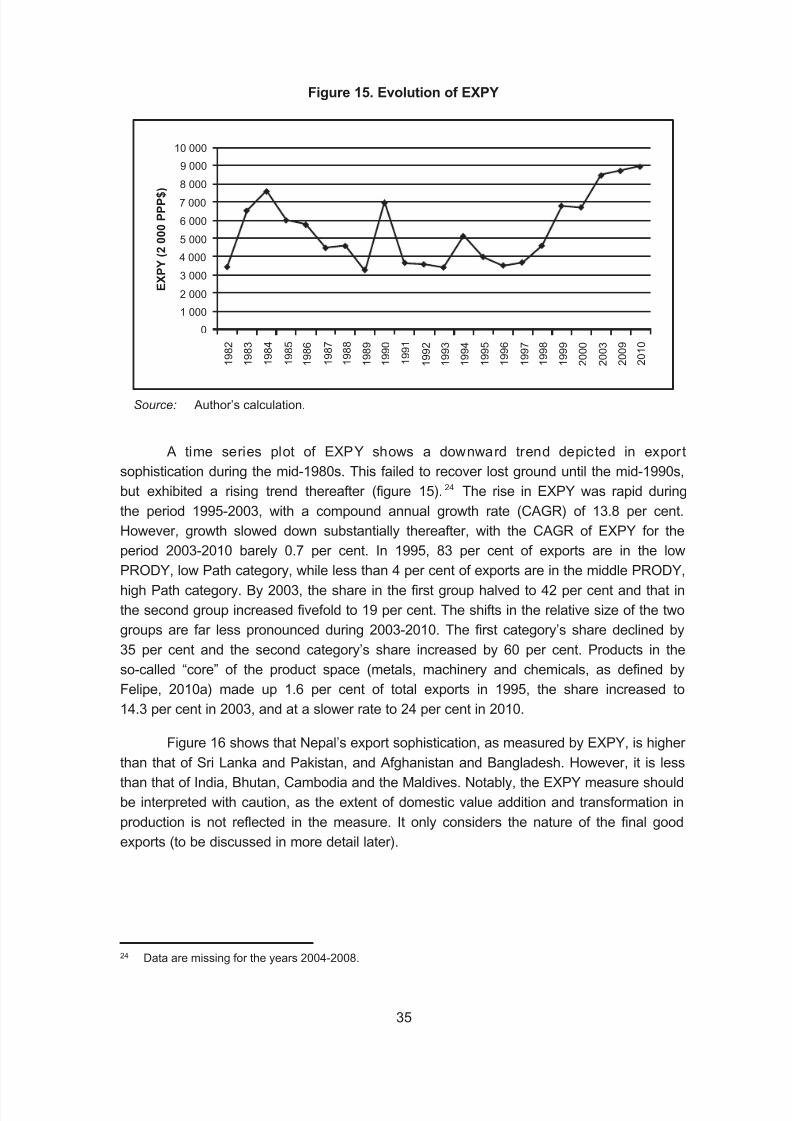

Figure 15. Evolution of EXPY ............................................................................... 35

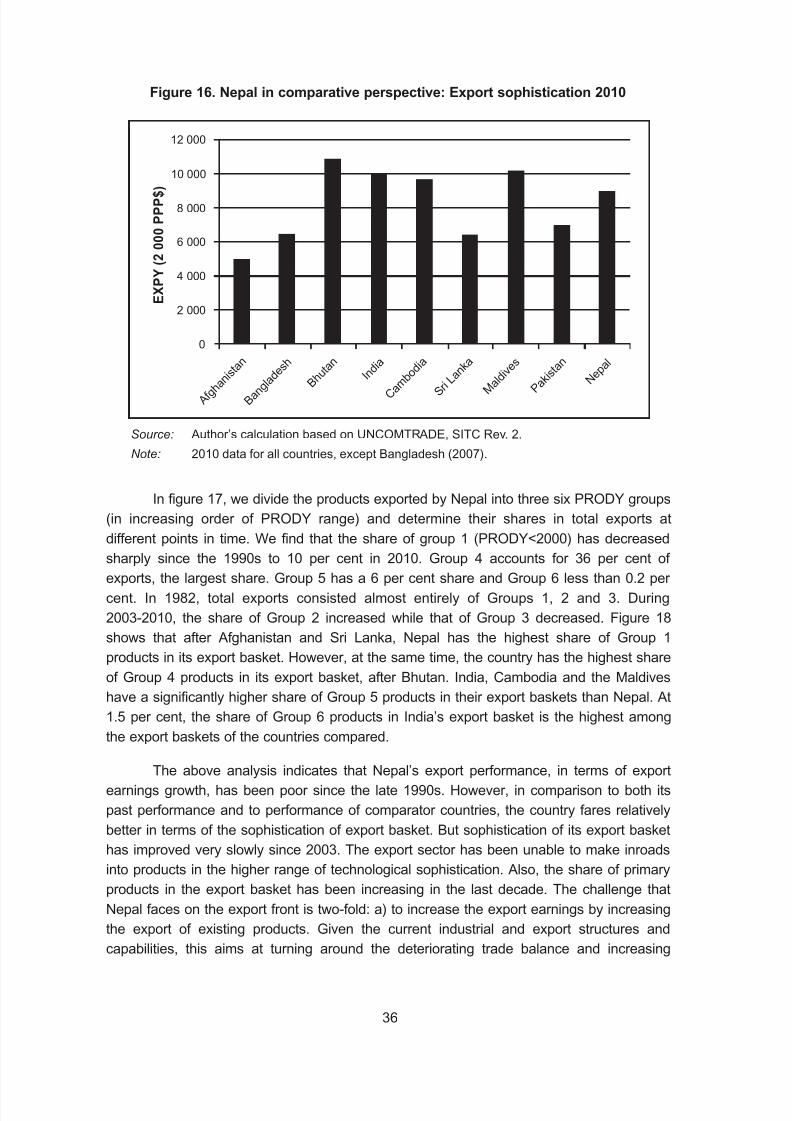

Figure 16. Nepal in comparative perspective: Export sophistication 2010 ........... 36

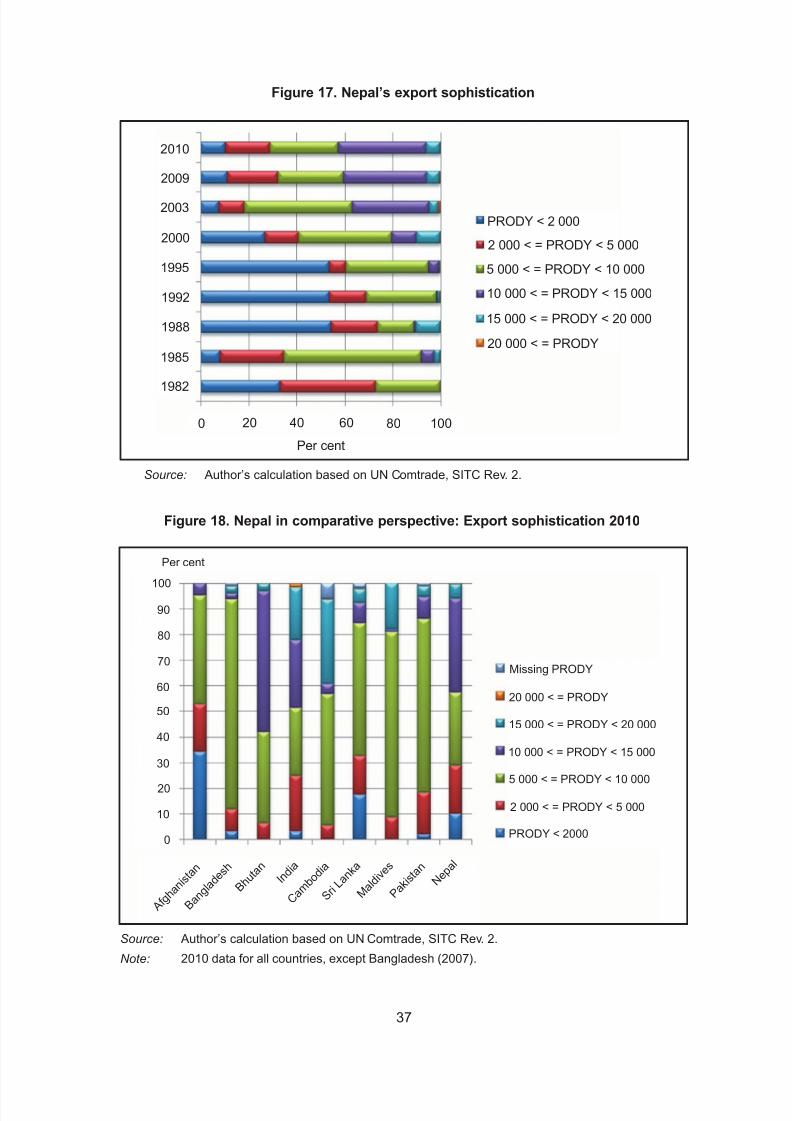

Figure 17. Nepal’s export sophistication ............................................................... 37

Figure 18. Nepal in comparative perspective: Export sophistication 2010 ........... 37

Figure 19. Strategic Value against density of unexploited products, 2010............ 44

Figure 20. Sophistication and connectivity of NTIS-identified products ................ 47

Figure 21. Sophistication and connectivity of Trade Policy products .................... 53

Chapter II

Figure 1. Production blocks and logistics service links ....................................... 94

Figure 2. Trends in trade shares: India’s export of yarn to Bangladesh and

import of ACE from Thailand ................................................................ 98

Chapter III

Figure 1(a). Exporters vs non-exporters by size ..................................................... 135

Figure 1(b). Exporters vs non-exporters by province .............................................. 135

Figure 1(c). Exporters vs non-exporters by industry ............................................... 135

Figure 2(a).Kernal density of log sale ..................................................................... 135

Figure 2(b). Kernal density of log labour productivity .............................................. 135

Figure 2(c). Kernal density of log wage .................................................................. 135

Figure 3. Export concentration by value of exports and total sales .................... 138

Contents (continued)

Page

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 13/215

xi

List of contributors

Rifana Buhary is staff at the Department of Agricultural Economics and Business

Management, Faculty of Agriculture, University of Peradeniya, Sri Lanka.

Prabir De is a Senior Fellow at the Research and Information System for Developing

Countries (RIS). De works in the field of international economics and has research interests

in international trade and development. He was a visiting research scholar of the Asian

Development Bank Institute (ADBI), Tokyo; Korea Institute of International Economic Policy

(KIEP), Seoul; and United Nations Economic and Social Commission for Asia and the

Pacific (ESCAP), Bangkok. He is also a visiting faculty member of the Institute of Foreign

Policy Studies (IFPS), Calcutta University, Kolkata, where he has been teaching trade and

regional cooperation. He has been conducting policy research for the Government of India

and several international organizations. De has a Ph.D. in Economics from the Jadavpur University, Calcutta. He has contributed several research papers in international journals

and written books on trade and development. He is the managing editor of South Asia

Economic Journal, published by Sage, and edits a policy brief series, called Mekong –

Ganga Policy Brief. e-mail: [email protected]

Sisira Jayasuriya is a Professor of Economics in the Department of Economics, Monash

University, Melbourne, Australia and an Adjunct Professor at the Arndt-Corden Department

of Economics at the Australian National University, Canberra, Australia. He has held

previous appointments at the Australian National University, La Trobe University, University

of Melbourne and the International Rice Research Institute, Philippines. Hisresearch

interests are in policy-oriented development economics, and he has published extensively

on trade, macroeconomics, resource and environmental issues of developing countries,

with a primary focus on Asia. He has been a consultant to World Bank, Asian Development

Bank, International Food Policy Research Institute, Food and Agriculture Organization

(FAO) and several other UN agencies), and to government agencies in both Australia and

overseas. e-mail: [email protected]

Paras Kharel is a trade economist. His research interests include trade costs, trade

facilitation including transit issues, competitiveness, aid for trade, trade and climate change

linkages, trade and transit issues related to least developed countries (LDCs) and

landlocked developing countries (LLDCs) and services trade. He has worked as

programme officer and senior programme officer at South Asia Watch on Trade, Economics

& Environment (SAWTEE) since 2007. e-mail: [email protected]

Sarath S. Kodithuwakku has obtained his BS in agriculture with specialization in

agricultural economics from the University of Peradeniya, Sri Lanka in 1990. He obtained

his Masters of Business Administration in Marketing and Ph.D. in entrepreneurship from the

University of Stirling, United Kingdom in 1993 and 1997, respectively. He currently servesas a Professor in the University of Peradeniya. He founded the MBA programme offered by

the University of Peradeniya and he has been the Coordinator of the programme since its

inception in 1998, in addition to serving as the Chairman of the Board of Study in Business

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 14/215

xii

Administration, PGIA since its inception in 2002. He was also the Director of the

Agribusiness Centre, the outreach arm of the Faculty of Agriculture, since its inception until

September 2011. At national level, he has been serving as the Senior Vice President of the

Sri Lanka Institute of Management, the premier professional body for Sri Lankan

management professionals since 2003 and as a member of Board of Study of the Sri LankaInstitute of Marketing, the premier professional body for Sri Lankan marketing professionals

since 2002. e-mail: [email protected]

Amrita Saha is a Ph.D. student working on issues in international trade and trade policy.

Her research is funded by the Commonwealth Scholarship Commission, United Kingdom.

Prior to joining the research programme at Sussex, she has worked with the Foreign Trade

Division at Ministry of Commerce, India. She has also pursued several research projects in

India, under the MacArthur fellowship at the Indian Council for Research in International

Economic Relations (ICRIER) New Delhi, the Sir Ratan Tata Fellowship at the Institute for

Social and Economic Change (ISEC) Bangalore, at the Reserve Bank of India (RBI)

Bangalore and the National Council for Applied Economic Research (NCAER) New Delhi.

She has completed Bachelors (Honours) in Economics from Delhi University, India and

Master Degree in Economics from the University of Hyderabad, India.

Jeevika Weerahewa is a Professor at the Department of Agricultural Economics and

Business Management, Faculty of Agriculture, University of Peradeniya, Sri Lanka. She

has a B.Sc. and M.Phil. in Agriculture from the University of Peradeniya and a Ph.D. in

Agricultural Economics from the University of Guleph, Canada. She has been teaching

fundamental and applied courses in Economics with a special focus placed on agricultureand allied fields at the University of Peradeniya since 1987. Her primary research area is

Quantitative Policy Analysis and applications are extended to analysis of various economic

and distributional impacts of trade, agricultural production and marketing policies. She is

a Collaborator of the International Food Policy Research Institute (IFPRI), a Hewlett Fellow

of the International Agricultural Trade Research Consortium (IATRC), a Fellow of the

Canadian Agricultural Trade Policy Research Network (CATPRN) and a Focal Point of the

Asia-Pacific Research and Training Network on Trade (ARTNeT). e-mail: jeevikaw@

gmail.com

Vathana Roth is a research associate at Cambodia Development Resource Institute

working on issues such as economic growth, poverty, inequality and private sector

development. He is also a lecturer of economics at the Department of International Studies,

Institute of Foreign Languages. He previously served as Assistant to Deputy Country

Director (Programme) of the United Nations Development Programme, Cambodia. e-mail:

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 15/215

xiii

Acronyms and Abbreviations

AB Arellano-Bond

ACE Air-Conditioning Equipment

ADB Asian Development Bank ADF Augmented Dickey-fuller

ARTNeT Asia-Pacific Research and Training Network on Trade

ASEAN Association of Southeast Asian Nations

ATE Average Treatment Effects

BAs Business Associations

BEC Broad Economic Categories

CAGR Compound Annual Growth Rate

CES Constant Elasticity of Substitution

CoC Chamber of CommerceDCS Department of Census and Statistics of Sri Lanka

DID difference-in-differences

EHS Early Head Start

ERIA Economic Research Institute for ASEAN and East Asia

ESCAP Economic and Social Commission for Asia and the Pacific

EXPY export basket of a country

FEM Finite Element Method

FTAs Free Trade Agreements

GDP Gross domestic productHS Harmonized System

CIC Industry and Commerce

ICT Information and Communication Technology

IDE-JETRO Institute of Developing Economies-Japan External Trade Organization

IIT Intra-Industry Trade

IoO Index of Opportunities

ISIC International Standard Industrial Classification of All Economic Activities

IT Information technology

ITC International Trade CentreLDCs Least Developed Countries

LPI Logistics Performance Index

MNEs Multinational Entities

MSMEs Micro, small, and medium Enterprises

NAFTA North America Free Trade Agreement

NBER National Bureau of Economic Research

NIC National Industrial Classification

NTIS Nepal Trade Integration Strategy

OLS Ordinary Least SquaresPCA Principal Component Analysis

Pce per capita consumption of electricity

PSM Propensity score matching

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 16/215

xiv

RCA Revealed comparative advantage

SAFTA South Asian Free Trade Area

SEZ Special Economic Zone

SITC Standard International Trade Classification

SMEs Small and Medium EnterprisesSSCs Supply-side constraints

SV Strategic Value

UNCTAD United Nations Conference on Trade and Development

USDA United States Department of Agriculture

WDI World Development Indicators

WITS World Integrated Trade Solution

WTO World Trade Organization

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 17/215

xv

Overview

The first essay on “Structural transformation and trade policy: The Case of Nepal”

by Paras Kharel reviews recent trade and industry policy initiatives in Nepal. This is in the

context of recent literature pioneered by Dani Rodrik, Ricardo Hausmann and colleagues,suggesting that some patterns of production and trade may be more conducive to structural

transformation and industrialization. The essay provides an excellent overview of this new

literature, which is starting to have an important influence in both academic and policy

circles. It also provides an application of some of the approaches using network analysis to

develop a graphical representation of the product space in Nepal. Based on a very detailed

and comprehensive analysis, Kharel draws important implications for trade and industry

policy. He argues that there is scope for better targeting of Nepalese trade and industry

promotion policies.

Kharel’s discussion raises some of the unresolved and difficult issues in targeted

government interventions of this type. These issues have a long history; from the time

when import substitution industrialization (ISI) policies held sway in much of the developing

world, and that continue today to have relevance for policy debates. This is not only in

Nepal, but also for many other countries grappling with the challenges of sustaining

industrialization and development over the longer term. The long history of ISI policies

provides plenty of examples where government interventions to guide the industrialization

process through targeted support has resulted in costly misallocation of resources, which

often trap economies in “infant industries that never grow up”. While making a case for governments to pay attention to the potential benefits of well-directed industry promotion,

Kharel also points to the potential tension between assisting industries with the highest

potential for export earnings and employment and, on the other hand, assistance for

upgrading the industrial and export structures, and capabilities to be able to produce and

export (or expand) the production and export of, more sophisticated products requiring

a greater number of capabilities. For a country like Nepal, traditional labour-intensive

industries (such as garments) may offer the best potential in terms of maximising export

earnings and employment. However, it may not be most helpful for industry upgrading and

a progressive shift into more sophisticated manufactured products.

In the second essay, “Logistics performance, trade and production fragmentation:

An analysis of India’s trade with Bangladesh and Thailand”, Prabir De and Amrita Saha

investigate the important issue of logistical services for successful industrialization and

export growth. They analyse the link between logistical performance and trade in parts and

components in the manufacturing industries. This is central to the growth of international

production linkages and networks associated with the phenomenon of international

production fragmentation. They focus specifically on trade in two commodities – India’s

export of yarn to Bangladesh and India’s import of air-conditioning equipment from

Thailand, in the context of the broader regional trading context.

Logistics involves a multiplicity of services including various forms of transport,

communications and quality of human resources. They develop a logistical services index

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 18/215

xvi

for 20 Asia-Pacific countries based on data on a wide range of such services. This is to

quantify the link between logistic services and trade. They demonstrate not only that

improved logistical services have a positive impact on trade, but also that there is a two-

way relationship between trade and logistical services in that increased trade, in turn, tends

to enhance the quality of logistical services. Although the precise mechanism throughwhich this occurs is not explored in the paper, it is likely that expanded trade in turn may

induce market and government policy responses. The wide differences observed in quality

of logistical service among the countries studied indicate that there is a large potential for

improvement in logistics. In turn, this contributes to beneficial expansion of trade and

fosters closer and deeper regional production linkages.

The pace and impact of progress in trade and industrialization in the region

ultimately depends on the extent to which firms can address the challenges of competing

and succeeding in markets where policy liberalization and the resulting pressures from

globalization intensify competitive pressures, even as they open up broader opportunities.

The importance of firm level differences in critically influencing outcomes when economies

are opened up to international competition has been highlighted in recent literature on

international trade following Melitz (2003). The next two essays explore firm level issues

related to competing in globalized markets.

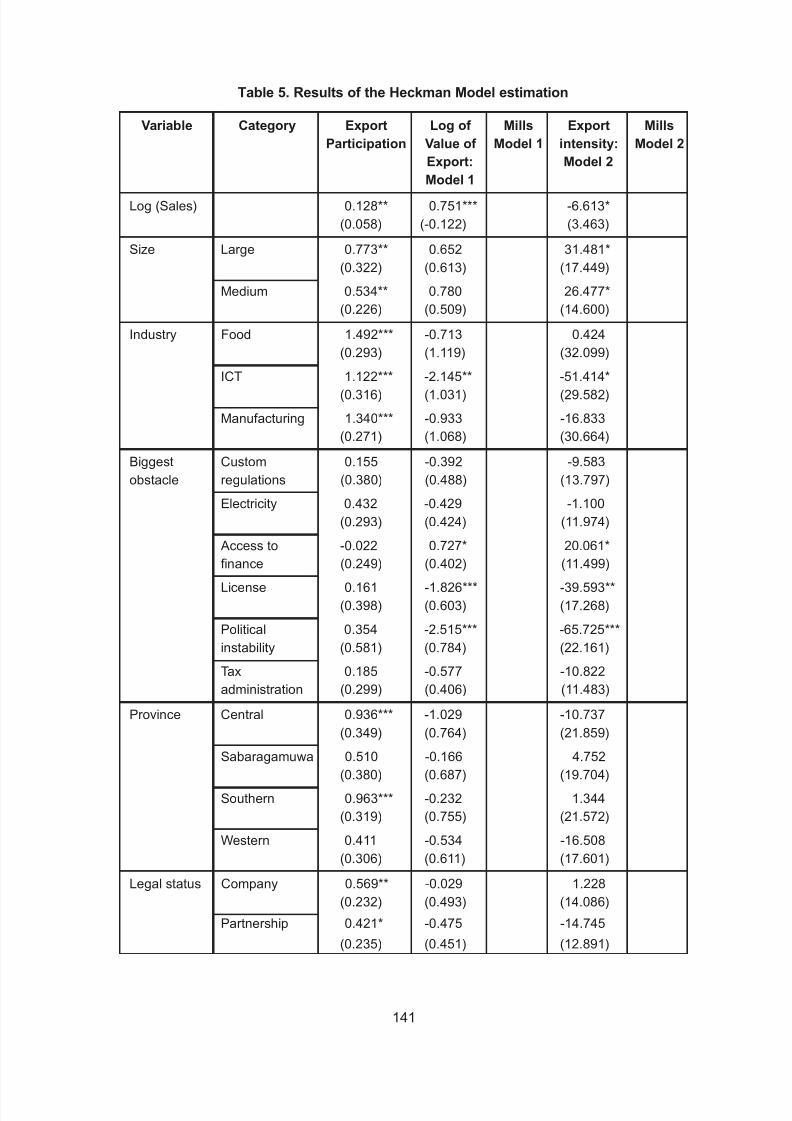

In the third essay, “An analysis of export performance of manufacturing and service

sector enterprises in Sri Lanka”, Jeevika Weerahewa, Sarath S. Kodithuwakku and Rifana

Buhary investigate the different characteristics of exporting and non-exporting firms in two

key industries using a rice data set from a recent (2011) World Bank “Enterprise Survey” of over 800 firms. The researchers chose econometric techniques and a modelling approach

that avoids the common problem of “selection bias” in studies of this type. They show that

several firm-level characteristics, in particular size and geographical location, as well as the

managers’ perceptions regarding the overall business environment, influence whether firms

become exporters or not. Indeed, a few large exporters, many with foreign linkages,

account for the bulk of exports. The results of this study raise several issues that merit

future investigation in more detail, including the reasons for different managerial

perceptions regarding the business climate. The overall impression conveyed by the results

of this analysis is that Sri Lanka faces formidable challenges if it were to succeed infostering a broad based export culture among the small and medium sized firms who

comprise the majority.

The final essay, “Evaluation of business association membership on small and

medium enterprises’ growth performance: Evidence from enterprise survey of Cambodia” is

by Vathana Roth. It addresses issues relating to the major policy challenge of how to assist

small and medium enterprises operating in a developing country setting of imperfect factor

and information markets, and how to overcome scale and market access constraints. It

examines factors that impact on performance among small and medium firms, with a focuson whether business associations can contribute to increasing their competitiveness and

overall performance. The study uses data from the 2007 World Bank Enterprise Surveys of

Cambodia to examine the impact of belonging to a business association on Small and

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 19/215

xvii

Medium Enterprises (SMEs) from four sectors – manufacturing, tourism, trade, and others.

The analytical approach involved propensity score matching (PSM) as well as PSM with

ordinary least squares (OLS) regression. The study finds that firms belonging to business

associations tend to have higher turnover and production, and tend to spend more on

production and other related costs. However, it did not find membership to have anysignificant impact on firms’ labour productivity and labour cost per worker. This may be due

to business associations in Cambodia having limited capacity to enhance productivity of

members through provision of appropriate services. In any case, the results ought to be

treated with some caution, not only because of data limitations but also as participation in

such associations is a relatively new experience for many firms.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 20/215

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 21/215

1

I. Structural transformation and trade policy:Case of Nepal

By Paras Kharel

Introduction

High and sustained economic growth entails structural transformation. This involves

the shift of productive factors from low-productivity and low-wage activities to

high-productivity and high-wage activities. The aim is to move the output structure into

higher-productivity activities, and production of more complex and sophisticated products.

In the past, structural transformation was generally seen as a consequence of growth anddevelopment. However, recent advance in literature has produced powerful analysis

methods for appreciating the role of structural transformation in inducing growth and

development. It also provides evidence that product potential varies in effecting structural

transformation. In particular, what a country exports now influences the type of goods it will

export in future, thus influencing its future economic growth rate. In this context, the

literature suggests that governments may have a more direct and important role to play,

particularly in economies with low economic complexity.

These findings are particularly relevant for Nepal. Asa least developed economystarting to rebuild its economy after a period of political conflict, it is now attempting to

embark on a sustainable economic development path. The country has formulated

a range of policies, including Trade Policy 2009 and Nepal Trade Integration Strategy

(NTIS) 2010, for active government intervention in stimulating export growth and

industrialization. It has also selected products to be given high-priority status for

government support. This paper analyses the nature and extent of structural change in the

Nepali economy by studying trends, patterns and composition of productivity growth. It also

assesses Nepal’s export performance, including the sophistication and diversification of its

exports, and the extent government high-priority products have in assisting Nepal’sstructural transformation and future growth.

The rest of the paper is organized as follows. Section 2 reviews the literature on

structural transformation, including recent methodological advances. Section 3 discusses

Nepal’s economic and export performance. Section 4 discusses sectoral productivity

growth and whether structural change has been growth-enhancing or growth-reducing in

Nepal over a recent decadal period. Section 5 reviews Nepal’s trade policy, plans and

strategies, with focus on products identified for export promotion. Section 6 discusses the

methods and data used for analysing the nature, pattern and prospects of structural

transformation from the export dimension. Section 7 analyses the evolution of Nepal’s

export basket in terms of export sophistication and diversification. It also assesses the

prospects for structural transformation offered by products identified/targeted by Trade

Policy 2009 and NTIS 2010. Section 8 concludes.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 22/215

2

A. Review of literature on structural transformation

High and sustained economic growth entails structural transformation – a shift of

productive factors from low-productivity and low-wage activities to high-productivity

and high-wage activities. This is such that the output structure progressively shifts intohigher-productivity activities, including increased production of more complex and

sophisticated products. Countries should be able to produce not just more of the same

products, but also new ones. Also, the products chosen for specialization will have different

consequences for development.

Founders of development economics emphasize the importance of industrialization

for the externalities it generates, leading to accelerated growth (Rosenstein-Rodan, 1943;

Hirschman, 1958; Kaldor, 1967). Experiences of industrialized economies, as well as those

of the newly industrialized East Asia, suggests the importance of structural transformation

(see, for example, Chang, 2002). However, lacking formal models, mainstream economic

theory has made little use of these ideas (Hidalgo and Hausmann, 2008:5).

Dominant neo-classical trade and growth theories state that the type of products

a country produces and exports have little or no bearing on long-term growth and

development. The Heckscher-Ohlin model suggests that, in an open economy, countries

specialize on the production of goods that intensively use the productive factors that they

are endowed with, such as physical capital, labour, land, human capital, infrastructure and

institutions. The specialization pattern changes with the accumulation speed of specific

factors. Therefore, controlling for initial factor endowments, the particular productsa country produces and exports do not matter for its future economic performance

(including export).

Similarly, the Ricardian model argues that technological differences across

countries determine comparative advantage. Also two other dominant theories – the

varieties model of Romer (1990), and the quality ladders model of Aghion and Howitt

(1992) and Grossman and Helpman (1991) – explain productivity differences as “assume

a degree of homogeneity across products that eliminates the possibility to capture the

impact of initial specialization” (Hausmann and Klinger, 2007:1). New trade theory(Helpman and Krugman, 1985; Krugman, 1979) explains intra-industry specialization

(which Ricardian and Hecksher-Ohlin models cannot) through economies of scale and

product differentiation. The so-called “new-new” trade theory – the Melitz model (Melitz,

2003) – takes into account heterogeneity among firms, explaining which firms would find it

advantageous to export and which firms would sell only in the domestic market. However,

neither explains the path-dependent process of specialization. Thus, dominant mainstream

economic theories does not consider the structure of the product space (the universe of

goods and services that a country may produce) to be important for future growth, ignoring

the path-dependent nature of growth and development.

Recent advances in the literature challenge this view with more explicit recognition

of externalities and path dependence. Hausmann et al. (2006) finds that countries that

export goods associated with higher productivity levels grew more rapidly, even after

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 23/215

3

controlling for initial income per head, human capital levels, and time-invariant country

characteristics. This is through measures of the productivity or income potential of

a product (PRODY and EXPY). Their findings also reveal that countries with initial high

levels of export sophistication subsequently experienced higher growth in exports.

Hausmann et al. (2006) argues that “countries become what they produce”. This appeals tothe mechanism of “cost discovery” (Hausmann and Rodrik, 2003), under which the range of

goods that an economy ends up producing and exporting is determined not just by the

usual fundamentals, but also by the number of entrepreneurs who can be stimulated to

discover the cost of production in modern sectors of the economy. Such cost discovery

generates considerable positive externalities for other entrepreneurs.

Hausmann and Klinger (2006, 2007) show that changes in the revealed

comparative advantage of nations are governed by the pattern of relatedness of products at

the global level. As countries change their export mix, there is a strong tendency to move

towards “related goods” (goods that are, somewhat, more sophisticated but fairly similar),

rather than to goods that are farther away. They introduced an outcome-based measure of

relatedness, called proximity, between pairs of products using cross-country export data.

Formally, the proximity between products i and j is the minimum of the pair-wise conditional

probabilities of a country exporting a good, given that it exports another. Their findings

show that the pattern of relatedness of products is only very partially explained by similarity

in broad factor or technological intensity classifications, as in Leamer (1984) or Lall (2000).

This suggests that the relevant determinants are much more product-specific. Countries

that specialize in a dense part of the product space (where there are a lot of products in

close proximity to one another) find it easier to change their revealed comparative

advantage than countries that specialize in more disconnected products.

In general, rich (poor) countries tend to specialize in dense (sparse) parts of the

product space, although there is significant variation in this relationship. Controlling for the

level of income, countries like China, India, Indonesia, Turkey and Poland, specialize in

a very dense part of the product space, while countries that specialize in natural resources

(particularly oil) have export baskets in disconnected parts of the space (Hausmann and

Klinger, 2007:16). Hausmann and Klinger (2007) find that the speed at which countries can

transform their productive structure and upgrade their exports depends on having a path of nearby goods that are of increasingly higher value. In their model, they argue that the

assets and capabilities2 needed to produce one good are imperfect substitutes for those

needed to produce another good. However, this degree of asset specificity varies,

determining product interrelatedness. As a result, the process of structural transformation

tends to favour nearby goods in the product space, making the pattern of structural

transformation path-dependent.

2 The model focuses on human capital but is applicable to other specific non-tradable assets like

knowledge, labour training requirements, infrastructure needs, property rights, regulatory requirements or other

public goods (Hausmann and Klinger (2006, 2007).

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 24/215

4

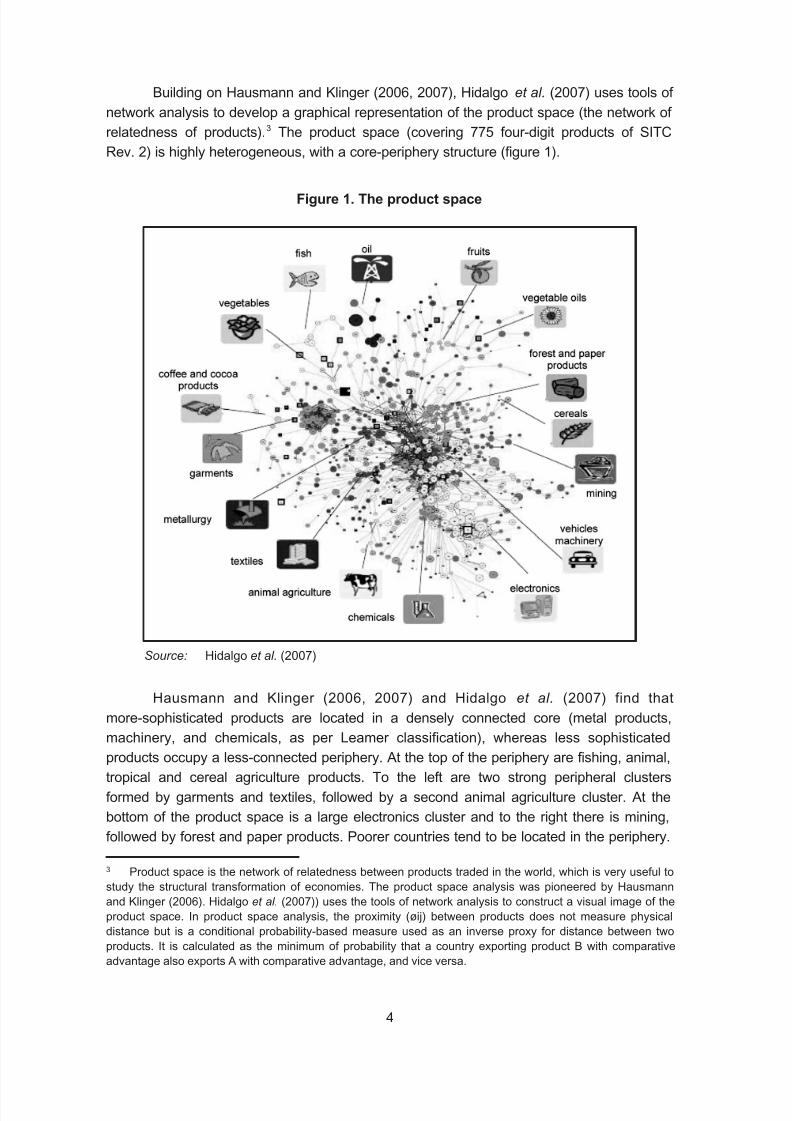

Building on Hausmann and Klinger (2006, 2007), Hidalgo et al. (2007) uses tools of

network analysis to develop a graphical representation of the product space (the network of

relatedness of products).3 The product space (covering 775 four-digit products of SITC

Rev. 2) is highly heterogeneous, with a core-periphery structure (figure 1).

Figure 1. The product space

Source: Hidalgo et al. (2007)

3 Product space is the network of relatedness between products traded in the world, which is very useful to

study the structural transformation of economies. The product space analysis was pioneered by Hausmannand Klinger (2006). Hidalgo et al. (2007)) uses the tools of network analysis to construct a visual image of the

product space. In product space analysis, the proximity (øij) between products does not measure physical

distance but is a conditional probability-based measure used as an inverse proxy for distance between two

products. It is calculated as the minimum of probability that a country exporting product B with comparative

advantage also exports A with comparative advantage, and vice versa.

Hausmann and Klinger (2006, 2007) and Hidalgo et al. (2007) find that

more-sophisticated products are located in a densely connected core (metal products,

machinery, and chemicals, as per Leamer classification), whereas less sophisticated

products occupy a less-connected periphery. At the top of the periphery are fishing, animal,

tropical and cereal agriculture products. To the left are two strong peripheral clusters

formed by garments and textiles, followed by a second animal agriculture cluster. At the

bottom of the product space is a large electronics cluster and to the right there is mining,

followed by forest and paper products. Poorer countries tend to be located in the periphery.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 25/215

5

The empirical findings indicate that countries move through the product space by

developing goods close to those they currently produce, and that many countries will meet

considerable difficulty in reaching the core. An important implication of these findings is that

even with similar levels of production and export sophistication, countries face different

prospects for structural transformation. This would depend on the proximity of moresophisticated products to their respective current productive capacities (proxied by the

products that a country exports with revealed comparative advantage).

Felipe et al. (2010a) develops an “Index of Opportunities” (IoO) for 130 countries

based on their capabilities to undergo structural transformation. The four dimensions of IoO

are related to the characteristics of a country’s export basket: sophistication, diversification,

standardness, and possibilities to export other products with comparative advantage. The

rationale behind IoO is that in the long run a country’s income is determined by the

sophistication and variety of products it makes and exports, reflecting its capabilities. In the

IoO rankings, Nepal ranks 33rd among 96 non-high income countries, putting it in the

second quintile. Among the four South Asian countries (for which data is available), Nepal’s

capabilities to undergo structural transformation are better than Bangladesh, Pakistan and

Sri Lanka and second only to India.

Felipe et al. (2010b) argues that becoming a rich country requires the ability to

produce and export goods that embody certain characteristics. In classifying 779 exported

goods (SITC Rev. 2, 4-digit), two dimensions are accorded – sophistication (measured by

PRODY) and connectivity to other products (measured by PATH). As a result, 352 “good”

products and 427 “bad” products are identified.

Researchers then categorized 154 countries into four groups according to these two

characteristics, with Nepal being among the “low core” 75 countries in the “low product”

trap. This group also includes Pakistan, Sri Lanka and Bangladesh from South Asia. The

share of core products in the number of products Nepal exports with comparative

advantage is 18.8 per cent. The exports of the countries in this group are concentrated in

products with low sophistication and little or average linkages with other products. Felipe

et al. (2010b) suggests that to escape this situation, these countries need to implement

policies that would help them accumulate the capabilities needed to manufacture andexport more sophisticated and better connected products. This would involve human capital

acquiring skills, technology and knowledge; a higher drive to diversify and to increase

sophistication by embracing a realistic industrial vision; and improvement in organizational

abilities e.g. firm-level organization (Felipe et al., 2010b: p. 30).

Felipe et al. (2010c) argue that the key factor underlying China’s fast development

during the last 50 years is its “ability to master and accumulate new and more complex

capabilities”, citing the increase in diversification and sophistication of its export basket.

Furthermore, they say China’s accumulation of new capabilities is policy induced and not

the result of the market, beginning before economic liberalization started. Analysis of

China’s current export opportunity set shows that the country is “exceptionally well

positioned” to continue learning and gaining revealed comparative advantage in the export

of more sophisticated products.

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 26/215

6

Abdon and Felipe (2011) find that in contrast the majority of Sub-Saharan African

countries are trapped in the export of unsophisticated, highly-standard products that are

poorly connected in the product space. This makes the region’s process of structural

transformation particularly difficult. As the products that are “nearby” to those they already

export have the same characteristics, Abdon and Felipe (2011) conclude that shifting tothese products will do little to improve the region’s growth prospects. As a means for

jump-starting and sustaining growth, they recommend implementation of policies and

provision of public inputs that encourage the private sector to invest in new and more

sophisticated activities.

Hidalgo and Hausmann (2009) use the techniques of network science to develop

a method to characterize the structure of bipartite networks connecting countries to the

products they export. Labeled Method of Reflections, it creates measures to count the

relative number of capabilities present in a country without making any assumptions about

the nature of capabilities. This is done by iteratively combining information on diversity of

countries (number of products a country exports) and ubiquity of products (number of

countries that export a product) using trade data. The number of capabilities present in

a country forms the country’s economic complexity. The complexity measures developed

through the Method of Reflections do not include information on income.4 This method of

measuring complexity of product and economy addresses criticism of PRODY and EXPY

(measures using income information), which makes the tautological observation that rich

countries export rich country goods.

Hidalgo and Hausmann (2009) find that a) the complexity of a country’s economy iscorrelated with per capita income. Deviations from this relationship are predictive of future

growth, suggesting that countries tend to approach the level of income associated with the

available capability set. B) The level of complexity of a country’s economy predicts the type

of products that a country will be able to develop in the future. This suggests that the new

products that a country develops depend substantially on the capabilities already available

in that country. Hidalgo and Hausmann (2009) argue that changes in a country’s

productive structure can be understood as a combination of two processes a) that by which

“countries find new products as yet unexplored combinations of the capabilities they

already have”, and b) that by which “countries accumulate new capabilities and combinethem with other previously available capabilities to develop yet more products” (Hidalgo

and Hausmann, 2009:10575).

Ranking of products and countries according to the measures of complexity

(developed by Hidalgo and Hausmann (2009); Abdon et al. (2010)) finds that the most

complex products are in machinery, chemicals and metals, while the least complex

products are raw materials and commodities, wood, textiles, and agricultural products.

More so, the most complex economies in the world are Japan, Germany, and Sweden, and

the least complex, Cambodia, Papua New Guinea, and Nigeria; the major exporters of the

4 However, there is a strong correspondence between PRODY and EXPY with their network counterparts,

“suggesting that most of the information contained in PRODY and EXPY comes from the structure of the

network connecting countries to the products they export, rather than from income” [Hidalgo 2009: p. 7].

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 27/215

7

more complex products are the high-income countries, while the major exporters of the less

complex products are the low-income countries; and export shares of the more complex

products increase with income, while export shares of the less complex products decrease

with income. Among the South Asian economies with available data, Nepal is ranked 89 th

out of 124 countries in terms of economic complexity. This is higher than Bangladesh, SriLanka and Pakistan but below India. Despite this, Nepal’s export basket is positively

skewed towards less complex products.

Using the measures of complexity (diversification and ubiquity) developed in 2009,

Hausmann and Hidalgo, in 2010, construct a simple model that assumes that each product

requires a potentially large number of non-tradable inputs (capabilities). More so, that

a country can only make the products for which it has all the requisite capabilities. Within

the model, products differ in the number and specific nature of the capabilities they require,

while countries differ in the number and nature of capabilities they have. Therefore,

products that require more capabilities will be less ubiquitous, while countries that have

more capabilities will be more diversified. Mathematically, this proves that: i) the level of

diversification of a country increases on average with the number of capabilities it has;

ii) the ubiquity of a product decreases, on average, with the number of capabilities it

requires; iii) the average ubiquity of products exported by a country decreases with that

country’s level of diversification; iv) the average level of diversification of products exported

decreases with the ubiquity of that product.

The model also implies that the return (in terms of diversification) to the

accumulation of new capabilities increases exponentially with the number of capabilitiesalready available in a country. This gives rise to the “quiescence trap” or a “trap of

economic stasis”, meaning countries with few capabilities will have negligible or no return to

the accumulation of more capabilities, while countries with many capabilities will experience

large returns to the accumulation of additional capabilities. The model opens up two options

to the quiescence trap – increase in the average complexity of products, or increase in the

total number of capabilities that exist in the world. The trap calls for solving the coordination

problem between the accumulation of additional capabilities and the demand for those

capabilities.

Particular within Hausmann and Hidalgo (2010)’s empirically validated model,

calibration suggests that the world exists in a regime with a strong quiescence trap. More

so, when this model is combined with the results of Hausmann and Klinger (2006, 2007)

and Hidalgo et al. (2007), a more refined insight into the process of structural

transformation is revealed. This is “the ability to add a product to the production set of

a country depends not only on how close a given product is to an already existing one, but

also on how many other capabilities are present in the country and used in other, potentially

more distant, products” (Hausmann and Hidalgo, 2010: p. 27).

Furthering economic complexity analysis, Hidalgo (2009) finds that during the

42-year period 1963-2005 (while the product space remains relatively stable) only a few

highly dynamic economies have been able to considerably transform their productive

structures. Products, such as vehicles and machinery, populated the more densely

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 28/215

8

connected part of the network, while oil and some of its derivate products are always

located in a weakly connected periphery of the network. This demonstrates that oil requires

specific capabilities that do not foster development, despite generating large revenues.

Agricultural products and raw materials are also consistently located in the periphery of the

space. The countries that have transformed their productive structures most dramaticallyare Brazil, Indonesia, Turkey, Malaysia, Thailand, Republic of Korea, Singapore and China.

They have followed different trajectories. While the economic complexity of Republic of

Korea, Singapore and China were relatively high at the beginning of the observation period,

Brazil, Indonesia and Turkey started from a primitive production structure. Hidalgo (2009)

argues that in complex economies good governance and institutions may be all that is

required to stimulate capability building and economic growth. In turn, governments of

countries with low economic complexity should actively help catalyze market activities and

solve coordination problems associated with attempts to accumulate capabilities.

Freire (2011) creates an index of productive capacity of an economy using a variant

of the Methods of Reflections. This shows that it is very difficult for countries to improve

their productive capacities when they start from lower levels. Focusing on the period

1984-2009, he also finds that while there has been convergence in productive capacity

among countries that were initially above the average (relative to the world), those that had

below average productive capacity two decades ago have lagged further behind. This

suggests increasing overall divergence. The countries that have transformed the most in

the 25-year period are China, India and the United Arab Emirates. In the Asia-Pacific

region, Turkey, the Republic of Korea and Thailand are among the top 10 countries which

increased their productive capacity in relation to the average in that period (Freire, 2011).

With the exception of Bangladesh, all other least developed countries (LDCs) in the region

have ended the period further away from the world’s average in 2009 when compared with

their position in 1984 (Freire, 2011). LDCs of the region have productive capacity way

below the world average. Nepal’s productivity capacity, relative to the world average in

2009, was only marginally worse than in 1984. It is greater than that of all Asia-Pacific

LDCs, except Bangladesh, but lower than that of the developing countries in South Asia,

namely India, Pakistan and Sri Lanka. Regionally, it is average for Latin America and the

Asia-Pacific.

Using methods developed by Freire (2011) in a related research, ESCAP (2011)

finds that the countries that export the greatest number of categories of products and those

which have more products at different prices within those categories tend to have higher

levels of GDP. Findings also show that diversifications within and between categories of

products are not mutually exclusive. Richer countries continue to diversify, with the

dominant form of diversification being the expansion of production of different varieties

within the same category, as product categories rise. With average diversification of

countries increasing, but product mix becoming more standard, countries that do not

diversify are likely to fall behind (ESCAP, 2011).

Notably, only four countries – Estonia, Latvia, Lithuania and Vietnam – have

succeeded in transforming themselves during 1984-2009. The group began with

productivity capacities similar to those of the LDCs, and then raised it to above the world

8/11/2019 Trade performance and competitiveness: Selected issues relevant for Asian developing economies

http://slidepdf.com/reader/full/trade-performance-and-competitiveness-selected-issues-relevant-for-asian-developing 29/215

9

average (ESCAP, 2011; Freire, 2011). The process of transformation was gradual, e.g. as

in Vietnam (ESCAP, 2011).

Based on the experiences of the countries that have transformed themselves,

ESCAP (2011) suggests a strategy for increasing productive capacities; this is made up of

three main processes for discovering, acquiring and spreading the productive capacities

required for developing economies to catch up. The first process is differentiation through

strategic product innovation, which is identification and production of products that are new

to the economy and more complex, facilitating further diversification. The second process is

through the selection of the business models of firms and farms that are successful in the

differentiation process. The third is the amplification of the successful business models and

the exploitation of the new market (ESCAP, 2011). These processes have to be repeated

continuously for the strategy to succeed (ibid.).

Regarding the first process, ESCAP (2011) finds that Asia-Pacific LDCs, onaverage, could product around 400 new products closely related to existing ones. However,

only 10-15 per cent of these would be both more complex and better connected to other

products. In the case of Nepal, there are around 514 products related to those already

exported, of which 58 (11 per cent), are more complex and better positioned for future

diversification. ESCAP (2011) suggests a pragmatic way to look for potential new products;

this is to emulate the production pattern of countries that have higher productive capacities,

even if they do not have higher per capita GDPs.

In the next section we review Nepal’s recent growth and export performance, usingsome of the product classifications developed in this paper.

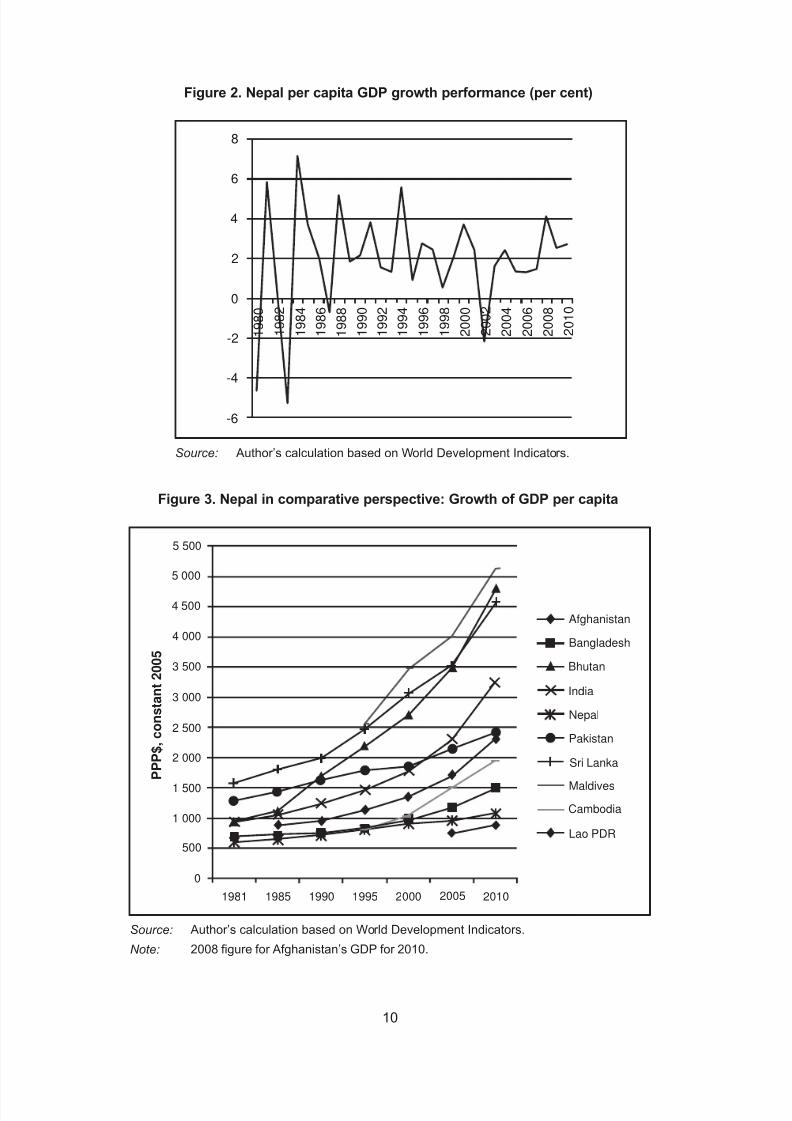

B. Nepal’s economic and export performance:A preliminary analysis

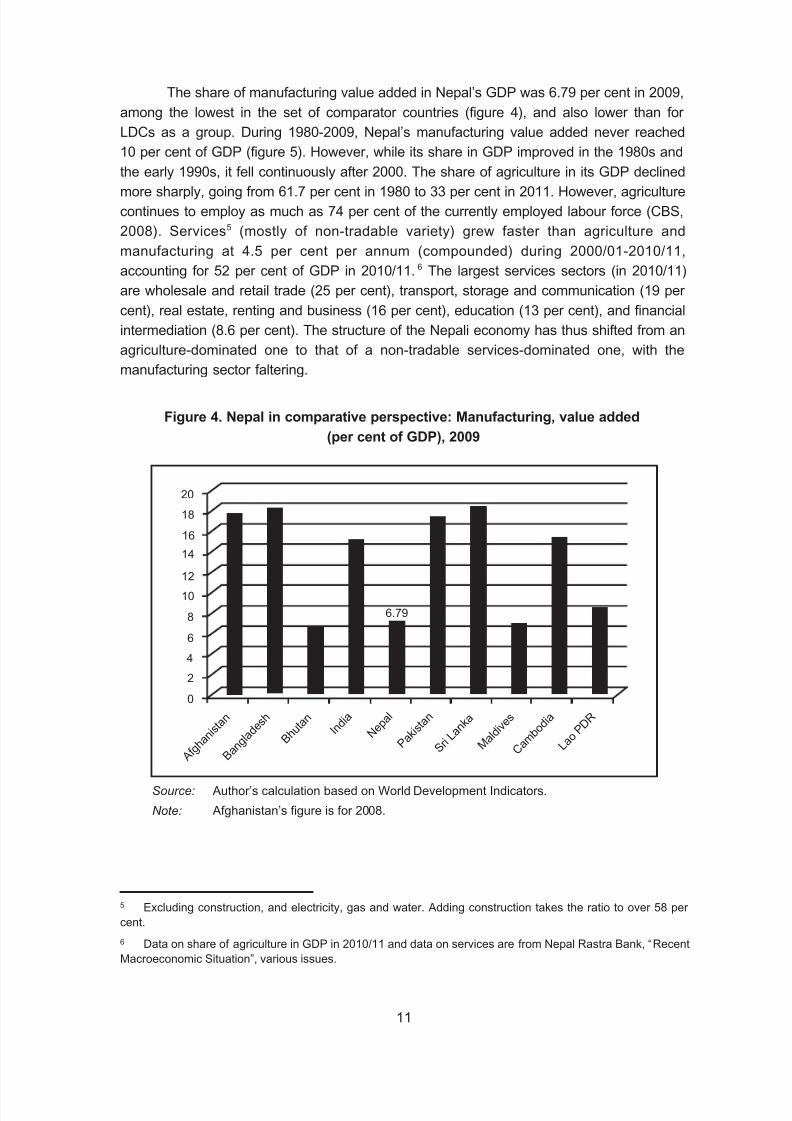

In the 30-year period 1980-2010, Nepal’s GDP per capita growth has been poor