topics for cfo’s current tax topics roger poulin, principal proposed fasb lease accounting changes...

TRANSCRIPT

TOPICS FOR CFO’S

Current Tax Topics Roger Poulin, Principal

Proposed FASB Lease Accounting ChangesNick Ireland, Senior Manager

Recap on New Allowance DisclosuresMatt Prunier, Manager

�

2

�

�

Current IRS Audit Issues

3

�

�

IRS Audit Issues

• Deducting OREO Carrying Costs

• There have been a growing number of examinations in which the IRS has sought the capitalization of OREO carrying costs

• The IRS argument is based upon an assertion that the OREO property is “inventory” acquired for resale and, consequently, §263A requires all carrying costs to be capitalized to the basis of the individual properties (which would permit them to be deducted upon disposal of the applicable properties)

• The IRS position appears to be coordinated

4

�

�

IRS Audit Issues (continued)

• Deducting OREO Carrying Costs• The taxpayer argument in support of deducting these costs

as they are incurred is based upon an assertion that the OREO properties are not, in fact, “inventory”

• Instead, the properties are acquired in the ordinary course of the loan relationship in order to mitigate the potential loss on the worthless debt obligation, not to be sold at a profit

• Such an argument would support the deduction of the OREO carrying costs as an ordinary and necessary business deduction under §162

5

�

�

Cease Accrual of Interest

• Cease accrual when determined to be uncollectible– When charge-off occurs

– There exists no reasonable expectation at the time of accrual that the items of income will be collected (Rev. Rul. 80-361 also see Rev. Rul. 2007-32)

– For example, where it can be demonstrated that the borrower was insolvent at the time the right to accrue the interest arose

6

�

�

Bad Debt Rules for Financial Institutions

• For banks under IRC Sec. 581:– Partial bad debt

– Bad debt conformity election (Reg. 1.166-2(d)(3))

– Rev. Rul. 2007-32

– Safe harbor method of nonaccrual interest (Rev. Proc. 2007-33)

• General rules apply in absence of these special elections (Reg. 1.166-2(a))– Based on all “pertinent evidence”

– Legal action not required

– Bankruptcy generally indication of worthlessness

7

�

�

Bad Debt Conformity (Reg. §1.166-2(d)(3))

• Presumption that a charge-off for regulatory purposes is correct

• Loan must be classified as a loss asset for regulatory purposes

• Provides IRS audit protection of charge-offs

• Must obtain determination letter from federal regulator (see Rev. Proc. 92-84)

8

�

�

Bad Debt Conformity (Reg. §1.166-2(d)(3)) (continued)

• Election made bank-by-bank

• Treated as an adoption or change in method of accounting– For new banks – automatic change (as opposed to

manual) for first election

– Cut-off approach, so no Sec. 481(a) adjustment

9

�

�

Revenue Ruling 2007-32 – Non-accrual Interest

• Deals with accrued but uncollected interest when the bank has made conformity election under Reg. §1.166-2(d)(3)

• Extends conformity election to nonaccrual interest• Holds that without a conformity election:

– Accrued but unpaid interest must be recognized for tax purposes, even when loan is charged-off, when some expectation of payment

– Remedy is bad debt deduction for accrued but unpaid interest in year of charge-off

– Subsequent payment goes to interest first

10

�

�

Fixed Asset Depreciation

• The 50% bonus depreciation provisions have been extended for qualified property placed in service before 1/1/2013

• However, the bonus depreciation amount is increased to 100% for qualified property acquired after 9/8/2010 and placed in service before 1/1/2012

• Guidance is provided in Revenue Procedure 2011-26

11

�

�

Fixed Asset Depreciation (continued)

• Qualified property for both provisions generally includes all depreciable fixed assets and software, but does not include buildings and their structural components

• However, certain leasehold improvements made to the interior of a leased building may qualify if the building is more than three years old

• Bonus depreciation only applies to new property (not used), but §179 applies to both new and used property

• Cost segregation opportunities abound for construction projects, especially those placed into service in 2011 and 2012

12

�

�

Maine Tax Credits

13

�

�

Maine – Bonus Depreciation / Credit

Bonus Depreciation - Maine Capital Investment Credit• For tax years beginning in 2011 and 2012, Maine will allow a credit equal to 10%

of federal bonus depreciation claimed by businesses for new property placed in service in this State

• Credit is nonrefundable, but unused amounts may be carried forward for 20 years

• The bonus depreciation upon which the credit is based must be added-back for Maine purposes (except for composite filings addressed later)

• Credit is subject to recapture if the property is not used in Maine for 12 months after being placed in service.

Section 179 – Conforms to federal in 2011 •Beginning in 2011, Maine will follow federal law regarding Sec. 179 depreciation. The maximum deduction for 2011 will be $500,000

14

�

�

Maine – Seed Capital Credit

Seed Capital Credit•Program administered by the Finance Authority of Maine (FAME)

•Investments made prior to 1/1/2012 - a tax credit certificate may be issued by FAME in an amount not more than 40% of the cash actually invested in an eligible Maine business in any calendar year, or in an amount not more than 60% of the cash actually invested in any one calendar year in an eligible Maine business located in a high-unemployment area, as determined by FAME

•For investments made or after January 1, 2012, a tax credit certificate may be issued to an investor other than a private venture capital fund in an amount not more than 60% of the amount of cash actually invested in an eligible Maine business in any calendar year

15

�

�

Maine – Seed Capital Credit (continued)

Eligible Business•Must be located in Maine

•It must be a manufacturer: must provide a product or service that is sold or rendered, or is projected to be sold or rendered, predominantly outside of the State; must be engaged in the development or application of advanced technologies; must be certified as a visual media production company Program administered by FAME

•Must have annual gross sales of $3MM or less

•The operation of the business must be the full-time professional activity of the principal owner

16

�

�

Maine – Seed Capital Credit (continued)

Eligible Investments/Investors•Aggregate investment eligible for tax credits may not be more than $5MM for any one business as of the date of issuance of a tax credit certificate

•Investment for which any individual is applying for a tax credit certificate may not be > $500K in any one business (can be invested over 3 consecutive calendar years). (This does not limit other investment by any applicant for which no tax credit certificate is being sought.)

•The principal owner / principal owner's spouse are not eligible for a credit

•A tax credit certificate may not be issued to a parent, brother, sister or child of a principal owner

•Investors qualifying for the credit must each own < 1/2 of the business

•The investment must be at risk for 5 years

•Specific rules apply for investments through private venture capital funds

17

�

�

Maine – Seed Capital Credit (continued)

Utilization of Credits•Credit calculated / approved by FAME – shown on Certificate issued•Must be used 25% per year•Amount used cannot exceed 50% of tax liability before the credit•Carry forward of 15 years•Investments made through private venture capital funds after 1/1/2012 may be eligible for refundable credits. (Specific rules apply. Credit to be calculated by FAME.)

18

�

�

Maine – Pine Tree Development Zone

PTDZ Income Tax Credit Basics•Tier 1 business location (other than Cumberland or York Counties) – 100% credit in years 1 – 5; 50% credit in years 6 – 10

•Tier 2 location – 100% credit in years 1 – 5

•Credit is calculated by computing an apportionment percentage – PTDZ payroll & property of business activity / total payroll & property of business activity – multiplied by tax = credit. (Also compute credit against ME minimum tax)

•When calculating percentage attributable to PTDZ activity from a PTE, make sure to include the shareholder’s PTDZ eligible wages in the PTDZ income allocable to him/her

•No carry forward

19

�

�

Maine – Rehab. Of Historic Properties

Tax Credit•Applies to qualified expenditures made from 1/1/2008 – 12/31/2023

•Credit equal to 25% of the taxpayer's certified qualified rehabilitation expenditures for which a tax credit is claimed under Section 47 of the Code for a certified historic structure located in ME (a copy of Part 3 of the Historic Preservation Certification Application signed by the Nat’l. Park Service and federal form 3468 must be attached); or

•25% of the certified qualified rehabilitation expenditures of a taxpayer who incurs not less than $50,000 and up to $250,000 in certified qualified rehabilitation expenditures in the rehabilitation of a certified historic structure located in ME and who does not claim a credit under the Code, Section 47 (a copy of Part 3 of the small project rehab certification application signed by the ME Historic Preservation Commission must be attached.)

•Credit increased to 30% for a certified affordable housing project

•Total credit limited to $5MM

•Credit fully refundable equally over 4 years

20

�

�

Maine – New Markets Capital Investment Program

Tax Credit•Modeled after Federal NMTC program

•Administered by FAME

•Maine credit of up to 39% to investors in qualified community development entities – investments on or after 1/1/2012

•Credit taken over 7 years – 0% in years 1 and 2, 7% year 3, 8% years 4 through 7

•Taxpayers may elect to make the credit refundable, or carry forward for up to 20 years

•Recapture rules apply

•Awaiting guidance from MRS and FAME

21

�

�

Maine – Credits Summary

22

�

�

Questions

23

�

�

Proposed FASB Lease Accounting Changes

24

�

�

Does it make sense that an airline’s balance sheet doesn’t show airplanes?

25

�

�

FASB/IASB Convergence Project

• FASB and IASB are jointly working on several new standards. Why?– The Boards’ desire to improve existing U.S. GAAP and

IFRS– To reduce the “gap” between U.S. GAAP and IFRS to

allow for less pain if U.S. does move to IFRS in the future• Lease accounting is one of four remaining major areas in

which FASB and the IASB are trying to reach convergence in standards.

• A separate but related project to the SEC’s potential adoption of IFRS.

26

�

�

Exposure Draft - Leases

• Original Exposure Draft was issued in August 2010.

• Original target date was June 2011.

• Hundreds of comment letters and significant outreach

• The Boards have punted issuance several times as the topic has been debated at just about every meeting since

27

�

�

Exposure Draft – Leases (continued)

• The key redeliberations topics relate to:– Scopes (leases of inventory or of internal use software)– Definition and measurement– Accounting for modifications/extinguishments, subleases, and

leasehold improvements – Presentation and disclosure– Transition and effective date

• The revised exposure draft is expected to be released in second half of 2012.

• We’ll just have to stay tuned.

28

�

�

Fundamental Proposals

• Lessees will record all leases on their balance sheet –similar to how lease accounting is currently done for capital leases– Liability will be recorded for lease obligations– Asset will be recorded for right-to-use asset, which will be amortized– Interest expense will be recorded relating to the obligations using the

effective interest method– There will be some shortcuts allowed for short term leases– New disclosures

29

�

�

Comparison at a Glance

• Current GAAP – Operating– Balance Sheet n/a– Income Statement Rent expense

• Current GAAP – Capital– Balance Sheet Asset and liability– Income Statement Depreciation and interest expense

• Proposed – All leases– Balance Sheet Right-to-use asset and liability– Income Statement Amortization and interest expense

30

�

�

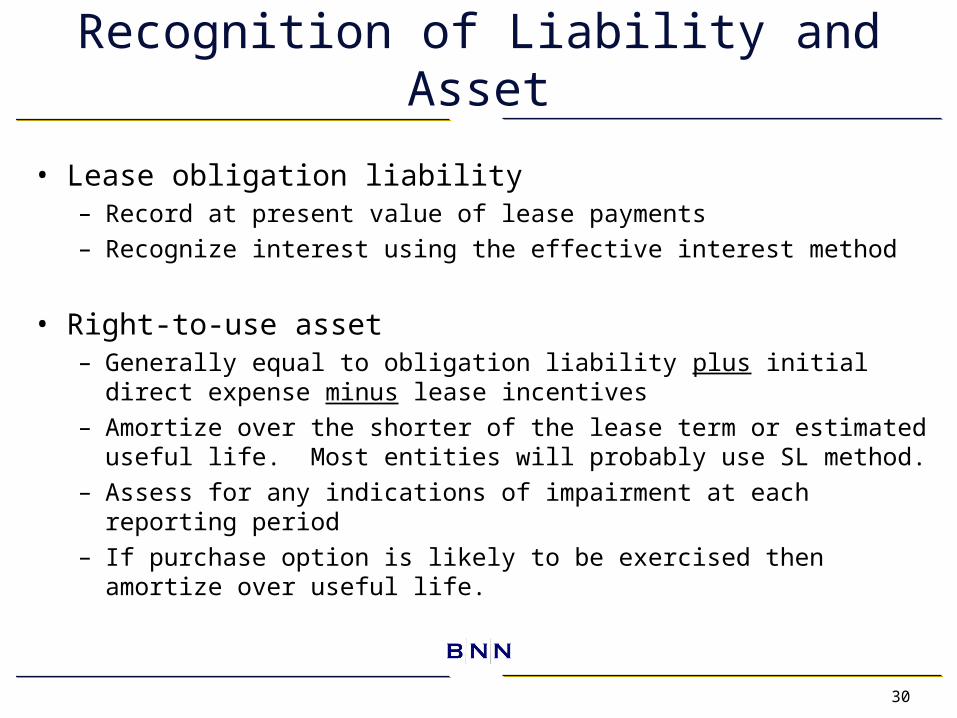

Recognition of Liability and Asset

• Lease obligation liability– Record at present value of lease payments– Recognize interest using the effective interest method

• Right-to-use asset– Generally equal to obligation liability plus initial direct expense minus

lease incentives– Amortize over the shorter of the lease term or estimated useful life.

Most entities will probably use SL method.– Assess for any indications of impairment at each reporting period– If purchase option is likely to be exercised then amortize over useful

life.

31

�

�

Present Value of Lease Payments

• Measure the present value using:– An ‘expected outcome’ technique– A discount rate at the lessee’s incremental borrowing rate

• Need to include the following in lease payments:– Estimated contingent rents payable– Estimated amounts payable under residual value guarantees– Estimated expected payments to lessor under nonrenewal optional

penalties– Exercise price of purchase option (only if lessee has significant

economic incentive to exercise the option)

32

�

�

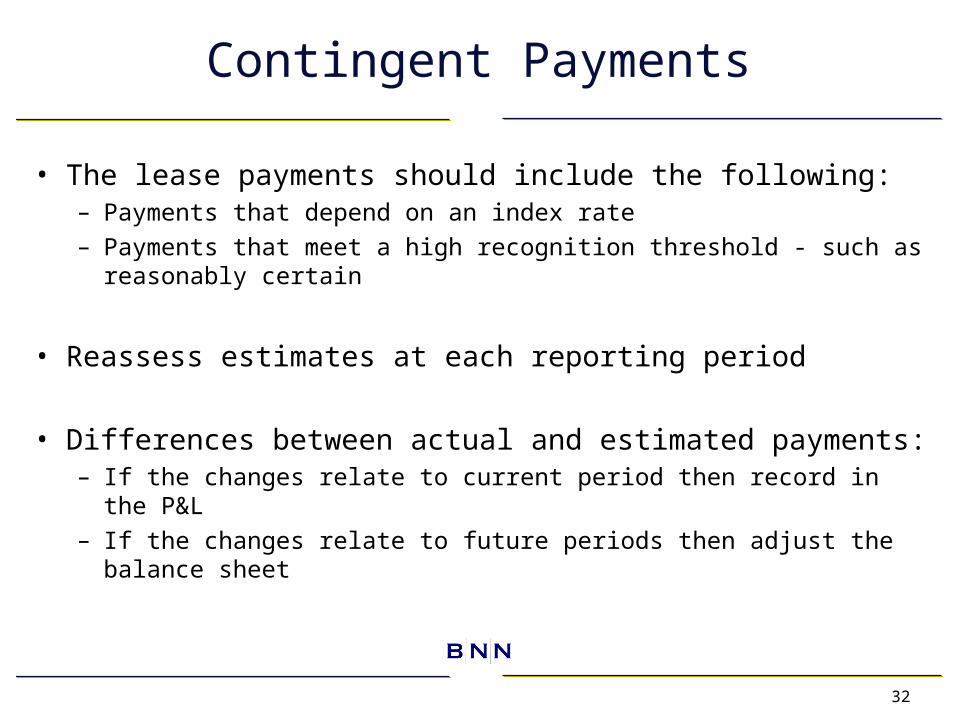

Contingent Payments

• The lease payments should include the following:– Payments that depend on an index rate– Payments that meet a high recognition threshold - such as

reasonably certain

• Reassess estimates at each reporting period

• Differences between actual and estimated payments:– If the changes relate to current period then record in the P&L– If the changes relate to future periods then adjust the balance sheet

33

�

�

Contingent Payments (continued)

• Many comment letters relate to disagreements with the Exposure Draft’s treatment of:– The “expected outcome approach” – Uncertainty of payments

• Subsequent deliberations decisions on contingent rents:– Eliminate “expected outcome approach” and use the “best estimate”

approach instead– Do not include contingent rent based on usage– Do include contingent rent based on index – Do include payments that meet a high recognition threshold

(reasonably certain)

34

�

�

Lease Term

• What is the appropriate lease term?– The longest possible term that is more-likely-than-not to occur

(>50%)– Consideration must be given to all relevant factors:

• History• Existence of renewal options and renewal rates• Termination penalties• Importance of underlying leased asset(s) to lessee’s operations• Significance of leasehold improvements

• Many comment letters relate to disagreements with the Exposure Draft’s definition of lease term:– Recognizing amounts that don’t meet the definition of a liability– It’s highly subjective – potential for manipulation

35

�

�

Short-term Leases

• Certain shortcuts will be allowed

• Short-term lease = maximum possible term, including any renewal options, of 12 months or less

• Exposure Draft says that lessees may elect to measure lease assets and liabilities on an undiscounted basis

• Subsequent deliberations decision – lessees may elect to treat an operating lease

– No right-of-use asset or lease liability recognized– Recognize payments on a SL basis

36

�

�

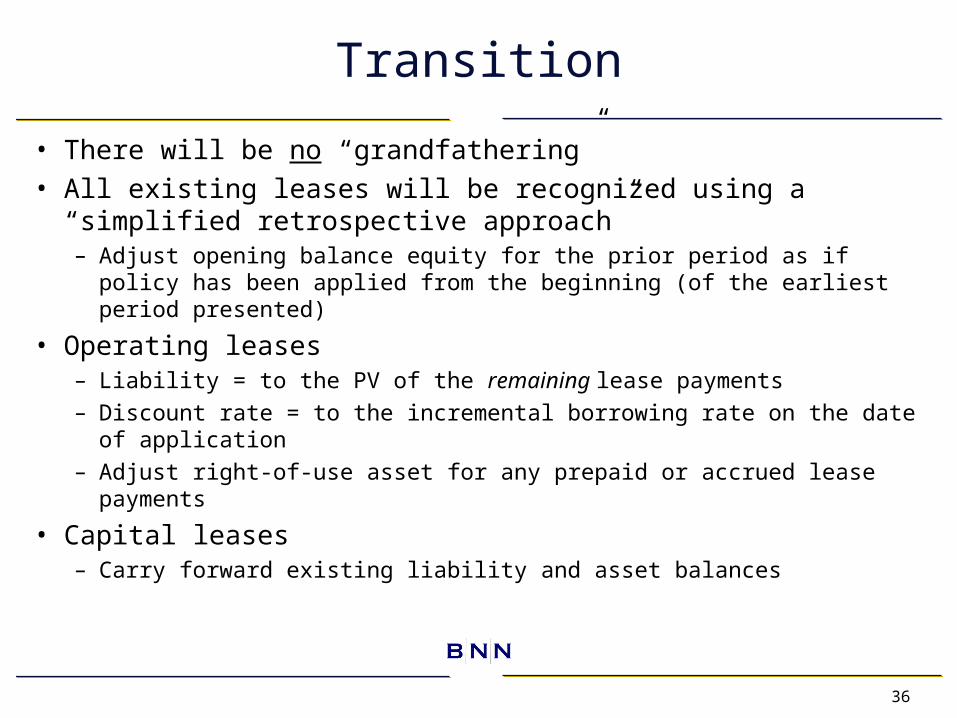

Transition

• There will be no “grandfathering”

• All existing leases will be recognized using a “simplified retrospective approach”– Adjust opening balance equity for the prior period as if policy has been

applied from the beginning (of the earliest period presented)

• Operating leases – Liability = to the PV of the remaining lease payments– Discount rate = to the incremental borrowing rate on the date of

application– Adjust right-of-use asset for any prepaid or accrued lease payments

• Capital leases – Carry forward existing liability and asset balances

37

�

�

Presentation

• Balance sheet– Present the liability on its own line– Present the right-to-use asset in with PP&E but separately from non-

leased assets

• Income statement– Present amortization and interest expense from other amortization

and interest expense (either in the P&L or footnotes)

• Cash Flows– Present lease payments as financing activities and show them

separately

38

�

�

What does this mean for you?

• Your Bank– Start addressing and analyzing now – The “grossing-up” of the balance sheet will negatively impact risk-

based capital ratios. – Differences between tax and book could result in DTA or DTLs– Adjustments for changes in estimates will result in increased balance

sheet volatility– Different expense profile – instead of having a SL of expense there

will be more expense recorded earlier and less later (due to interest on the unwinding of the liability)

39

�

�

What does this mean for you? (continued)

• Your Borrowers – Could have a detrimental impact on working capital ratios– Potentially could have significant impacts on covenant compliance -

both good and bad• Increased EBITDA

• Worsened financial statement ratios such as net worth ratio

– Increased balance sheet volatility

40

�

�

Questions

41

�

�

Recap of ASU No. 2010-20

New Allowance Disclosures

42

�

�

Who does this Effect?

• All entities, both public and nonpublic with financing receivables.

– For public entities, effective for periods ending on or after December 15, 2010

– For non-public entities, effective for periods ending on or after December 15, 2011

• Excludes

– Short-term trade accounts receivable

– Receivables measured at fair value / measured at the lower of cost or fair value.

43

�

�

What is the Purpose of the Update?

Quoted from the ASU:

“This Update is intended to provide additional information to assist financial statement users in assessing an entity’s credit risk exposures and evaluating the adequacy of its allowance for credit losses.”

What this means for you:

No new accounting requirements, rather a significant expansion of disclosure.

44

�

�

Main Provisions

Provide disclosures which allow the reader to evaluate:1.The nature of credit risk inherent in the entity’s portfolio of financing receivables

2.How that risk is analyzed and assessed in arriving at the allowance for credit losses

3.The changes and reasons for those changes in the allowance for credit losses

45

�

�

Amendments to Existing Disclosures

- A rollforward schedule of the allowance for credit losses on a portfolio segment basis

- For each portfolio segment the related recorded investment in financing receivables

- The nonaccrual status of financing receivables by portfolio segment

- Impaired financing receivables by portfolio segment

46

�

�

New Reporting Requirements

• Credit quality indicators of financing receivables by portfolio segment

• The aging of past due financing receivables by portfolio segment

• The nature and extent of troubled debt restructurings that occurred during the period by portfolio segment

• The nature and extent of financing receivables modified as troubled debt restructurings within the past 12 months that defaulted during the reporting period

• Significant purchases and sales of financing receivables during the reporting period by portfolio segment

47

�

�

Allowance Roll

Consumer Commercial Loans

Commercial Mortgage

Residential Un-allocated

Total

Beginning 2 8 6 4 1 21

Charge-offs - (2) (2) (1) - (5)

Recoveries - 1 1 - - 2

Provision (1) 4 5 1 1 10

Ending 1 11 10 4 2 28

Individually evaluated for impairment

- 2 4 1 - 7

Collectively evaluated for impairment

1 9 6 3 2 21

Loans Ending 100 1,100 1,000 400 - 2,600

Individually evaluated for impairment

- 400 500 100 - 1,000

Collectively evaluated for impairment

100 700 500 300 - 1,600

48

�

�

Past Due and Non Accrual

30+ 60+ 90+ Past Due

Current Total +90 Accrual

Consumer 10 10 - 20 80 100 -

Commercial loans 150 100 50 300 800 1,100

-

Commercial mortgages 200 50 50 300 700 1,000

-

Residential 35 5 10 50 350 400 10

Total 395 165 110 670 1,930 2,600

10

As of December 31, 2011, loans on nonaccrual status consisted of the following:

Commercial loans 50

Commercial mortgages 50

100

49

�

�

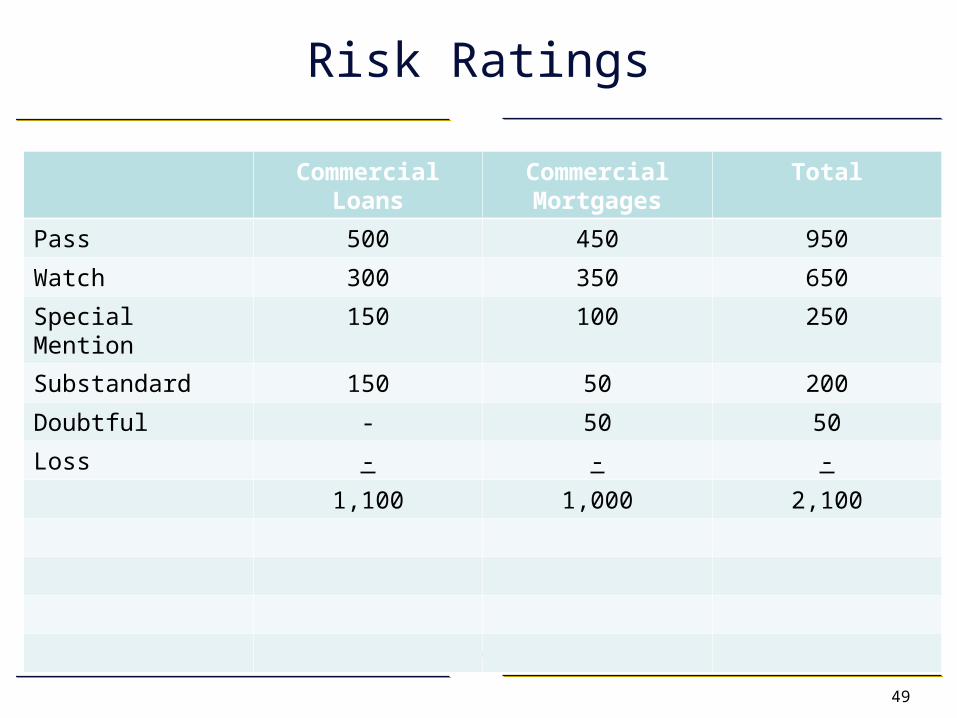

Risk Ratings

Commercial Loans

Commercial Mortgages

Total

Pass 500 450 950

Watch 300 350 650

Special Mention 150 100 250

Substandard 150 50 200

Doubtful - 50 50

Loss - - -

1,100 1,000 2,100

50

�

�

Performing Non Performing

Consumer Residential Total

Performing 100 400 500

Non-performing - - -

100 400 500

51

�

�

Recorded Investment

Unpaid Principal

Allowance Average Investment

With allowance:

Commercial loans 100 100 2 90

Commercial mortgages 50 50 4 50

Residential 10 10 1 15

With no allowance:

Commercial loans 300 320 - 290

Commercial mortgages 450 450 - 440

Residential 90 100 - 80

Total

Commercial loans 400 420 2 380

Commercial mortgages 500 500 4 490

Residential 100 110 1 95

Impaired Loans

52

�

�

Some Issues We Have Seen

• Negative provision for some categories• Consistency between the “buckets”• Negative, change, or size of unallocated• >90 days past due and still accruing• Recorded investment versus unpaid principal

balance• Data gathering

53

�

�

Questions

54

�

�

Contact Information

Baker Newman Noyes

280 Fore Street

Portland, ME 04101-4177

207-879-2100

Roger Poulin, CPA Nick Ireland, CPA Matt Prunier, CPA

Principal Senior Manager Manager

207-791-7123 207-791-7521 [email protected] [email protected] [email protected]

Visit our website at: www.bnncpa.com