topic 5 share_based_payment_a132_march

TRANSCRIPT

1BKAF 3063 A132

INTRODUCTION

Share-based payment transaction

A transaction in which the entity

a) receives goods or services as consideration for equity instrument of the entity (including employee stock option), or

b) acquires goods or services by incurring liabilities to the supplier of those goods or services for amount that are based on the price of the entity’s shares.

BKAF 3063 A132

2

TYPES OF SHARE-BASED

PAYMENT

1. Equity-settled Share-based Payment

2. Cash-settled Share-based Payment

3. Cash or Equity Share-based Payment

BKAF 3063 A132

3

TYPES OF SHARE-BASED

PAYMENT…(a) Equity-settled share-based payment transactions

- the entity receives goods or services as consideration forequity instruments of the entity

(b) Cash-settled share-based payment transactions

- the entity acquires goods or services by incurringliabilities to the supplier of those goods or services foramounts that are based on the price of the entity’sshares or other equity instruments of the entity

(c)Cash or Equity share-based payment transactions

- Transactions in which the entity receives goods orservices and the terms of the arrangement provide eitherthe entity or the supplier of those goods or services witha choice of whether the entity settles the transactionin cash or by issuing equity instruments.

BKAF 3063 A132

4

RECOGNITION

An entity shall recognize the goods orservices received in a share-basedpayment transaction when it obtains thegoods or as the services are received.

The entity shall recognize a corresponding(Para 7)

increase in equity if the goods or serviceswere received in an equity-settled share-based payment transaction or

A liability if the goods or services wereacquired in a cash-settled share-basedpayment transaction

BKAF 3063 A132

5

EQUITY-SETTLED SHARE-BASED

PAYMENT TRANSACTIONS

MFRS 2 requires an entity to(a) Measure the goods or services received and the

corresponding increase in equity (para 10):

based on the fair value of the goods andservices received.

if the fair value cannot be measured reliably,refer to the fair value of the equity instrumentgranted.

(b) For the case such as option granted to employeesas their employment remuneration, an entity shouldmeasure the services received and the correspondingincrease in equity by referring to the fair value of theequity instrument on granting date.

BKAF 3063 A132

6

ILLUSTRATION 1

Example 1:

On 6 June 2013, X Bhd acquires a piece of land,which has been valued by professional valuer atRM50 million, by issuing 10 million of its ordinaryshares (par value of RM1.00).

In this case, MFRS 2 requires X Bhd to measure the transaction based on the fair value of land.

Solution:

Dr Land RM 50 million

Cr Share Capital RM10 million

Cr Share Premium RM 40 million

BKAF 3063 A132

7

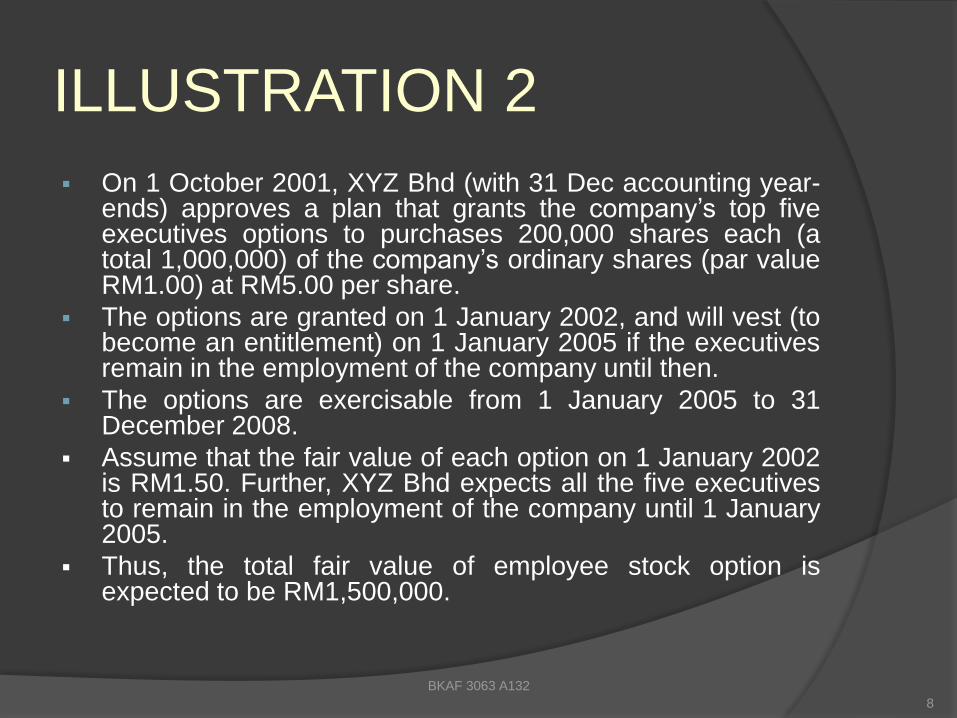

ILLUSTRATION 2

On 1 October 2001, XYZ Bhd (with 31 Dec accounting year-ends) approves a plan that grants the company’s top fiveexecutives options to purchases 200,000 shares each (atotal 1,000,000) of the company’s ordinary shares (par valueRM1.00) at RM5.00 per share.

The options are granted on 1 January 2002, and will vest (tobecome an entitlement) on 1 January 2005 if the executivesremain in the employment of the company until then.

The options are exercisable from 1 January 2005 to 31December 2008.

Assume that the fair value of each option on 1 January 2002is RM1.50. Further, XYZ Bhd expects all the five executivesto remain in the employment of the company until 1 January2005.

Thus, the total fair value of employee stock option isexpected to be RM1,500,000.

BKAF 3063 A132

8

ILLUSTRATION 2

(Continue)To record the stock option:

Paragraph 15: for the case of option granted in respect of the specified period of services to be completed, for example 3 years, the entity should account for increase in equity over the 3 year vesting-period.

1 Oct 2001 (No entry)

31 Dec 2002Dr Staff costs 500,000

Cr Capital reserve (RM1,500,000/3) 500,000

31 Dec 2003Dr Staff costs 500,000

Cr Capital reserve (RM1,500,000/3) 500,000

31 Dec 2004Dr Staff costs 500,000

Cr Capital reserve (RM1,500,000/3) 500,000

BKAF 3063 A132

9

ILLUSTRATION 2

(Continue)If on the grant date, the company expected two ofthe executives to leave the company before 1January 2005.Therefore only 3 executives to be ultimatelygranted the employee stock option.

BKAF 3063 A132

10

The fair valueof the employee stock option

=RM1.50x600,000

=RM900,000

The staff costs (for each 3 years)

=RM 900,000 / 3

=RM300,000 (instead of RM500,000)

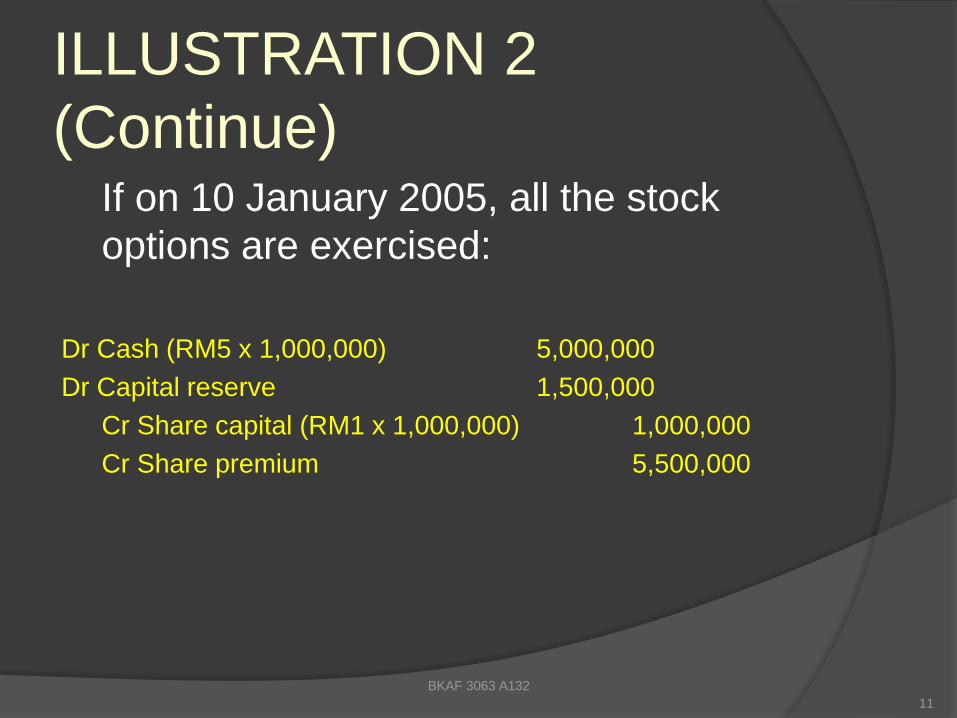

ILLUSTRATION 2

(Continue)If on 10 January 2005, all the stock

options are exercised:

Dr Cash (RM5 x 1,000,000) 5,000,000

Dr Capital reserve 1,500,000

Cr Share capital (RM1 x 1,000,000) 1,000,000

Cr Share premium 5,500,000

BKAF 3063 A132

11

Paragraph 19 - vesting

condition

Measurement of equity instrument

should be adjusted by including or be

based only on the number of equity

instruments that eventually vest

if the equity instrument granted do not vest

because of failure to satisfy a vesting

condition (e.g. employee failed to complete

the specified service period)

BKAF 3063 A132

12

ILLUSTRATION 3Refer to the case in the Illustration 2

On the grant date, XYZ Bhd expects all the fiveexecutives to remain in the employment of thecompany until 1 Jan 2005. However, in early 2004,one of the five executives unexpectedly left thecompany and his 200,000 share options areforfeited.

However, since RM1,000,000 of the cost has beencharged to years 2002 and 2003, only RM200,000(instead of RM500,000 as in Illustration 2) will becharged to 2004 income statement.

BKAF 3063 A132

13

Total fair value cost of the employee stock option

= RM1.50 x 800,000

= RM 1,200,000 ( instead of RM1,500,000)

ILLUSTRATION 3 (Continue)

1 October 2001

No entry

31 December 2002

Dr Staff cost (RM1,500,000/3) RM 500,000

Cr Capital reserve RM 500,000

31 December 2003

Dr Staff cost (RM1,500,000/3) RM 500,000

Cr Capital reserve RM 500,000

31 December 2004

Dr Staff cost (RM1,200k–RM1,000k) RM 200,000

Cr Capital reserve RM 200,000

BKAF 3063 A132

14

ILLUSTRATION 3

(Continue)If on 10 January 2005, all the 800,000 stock options are exercised:

Dr Cash (RM5 x 800,000) RM 4,000,000

Dr Capital reserve (RM1.50 x 800,000) RM 1,200,000

Cr Share capital RM 800,000

Cr Share premium RM 4,400,000

BKAF 3063 A132

15

Fair Value of Equity Instrument

Cannot be Estimated Reliably:

The entity should measure the services

received and the corresponding

increase in equity based on the intrinsic

value of the equity instrument granted.

(Para 24)

BKAF 3063 A132

16

Intrinsic Value = Market Price of the Entity’s Share – Option’s Exercise Price

ILLUSTRATION 4:

On 9 Jan 2006, PQR Bhd. announced a scheme whichgranted its 10 top executives a share option topurchase total of 50,000 units of company’s ordinaryshares (5,000 units each) at RM1.50.

As the company is a new start-up company, the marketvalue of the option was not available.

However, based on the net tangible asset, the fairvalue of the company’s ordinary shares was RM2.30each.

The par value of shares was RM1.00 each.

The option will be vest for the next 2 years (beginning1/1/2008 until 31/12/2009) should they remain in theemployment.

BKAF 3063 A132

17

ILLUSTRATION 4

(Continue)

Journal entries:

31 Dec. 2006 & 2007

Dr Remuneration Expenses (RM0.80 x 50k)/2 RM20,000

Cr Capital Reserve RM20,000

BKAF 3063 A132

18

Intrinsic value of the option = RM2.30-RM1.50

= RM0.80

ILLUSTRATION 4 (Continue)

Assume that the fair value of the company shares on 31 Dec 2008 would be RM2.60 each and options were exercised by 9 executives on 31 Dec 2008.

31 Dec 2008

Dr Remuneration Expenses (RM2.60- RM2.30) x 50k RM15,000

Cr Capital Reserve RM15,000

Dr Cash (RM1.50x45,000) RM67,500

Dr Capital Reserve (RM20k +RM20k+ RM15k) x 9/10 RM49,500

C r Ordinary Shares RM 45,000

Cr Share Premium RM 72,000

BKAF 3063 A132

19

ILLUSTRATION 4 (Continue)

If 5,000 options were exercised on 30 June

2009 (assuming no changes in fair value of

shares) :

30 June 2009

Dr Cash (RM1.50 x 5,000) RM 7,500

Dr Capital Reserve (RM55000- RM49500) RM 5,500

Cr Ordinary Shares RM 5,000

Cr Share Premium RM 8,000

BKAF 3063 A132

20

CASH-SETTLED SHARE-

BASED PAYMENT

TRANSACTIONS The settlement for the good or service by

an entity to be made in cash.

The amount of settlement is calculated

based on entity’s equity instrument.

Example:

When entity grants share appreciation rights to

their employee

Entitled to cash over the increase in the entity’s

equity instrument at a certain period of time.

BKAF 3063 A132 21

CASH-SETTLED SHARE-

BASED PAYMENT

TRANSACTIONS Entity shall measure goods or services

acquired and liability incurred at the fair

value of the liability

When the liability is settled,

The entity shall re-measure the fair value of

the liability at each reporting date of

settlement

Any changes in fair value shall recognized in

profit or loss for the period.(Para 30)

BKAF 3063 A132 22

ILLUSTRATION 5

On 1 January 2007, ABC Bhd. grants 8,000 share appreciationrights to each of its top 5 executives. With the condition thatthey remain employed in the next 2 years, it is estimated that100% of them will stay until 31 December 2008. The marketvalue of the company’s share and the fair value of shareappreciation rights are presented as follows :

On 31 Dec.2009, 100% of the rights exercised

BKAF 3063 A132

23

DATE MARKET VALUE OF COMPANY’S SHARE PER UNIT

FAIR VALUE OF COMPANY’S SHARE APPRECIATION RIGHTS PER UNIT

1 Jan. 2007 RM 3.00 RM 0.40

31 Dec.2007 RM 3.20 RM 0.50

31 Dec.2008 RM 3.50 RM 0.70

31 Dec.2009 RM 4.00 RM 0.80

SOLUTION

31 Dec.2007 RM RM

Dr Staff Remuneration expenses 10,000

Cr Liability ( RM0.50x8,000x5 )/2 10,000

31 Dec. 2008

Dr Staff Remuneration expenses 18,000

Cr Liability 18,000

( RM0.70x8,000x5 ) – 10,000

31 Dec.2009

Dr Liability 28,000

Staff Remuneration expenses 12,000

Cr Cash ( RM4.00- 3.00 ) x 40,000 40,000

BKAF 3063 A132

24

Cash or Equity share-based payment

(para 34)

Shared-Based Payment Transaction with Cash Alternative

The terms of the arrangement provide either theentity or the counterparty with the choice of whetherthe entity:(i) settles the transaction in cash or other assets(ii) by issuing equity instruments

The entity shall account that transaction(i) as a cash-settled share-based paymenttransaction if the entity has incurred a liability to settlein cash.(ii) as an equity-settled share-based payment

transaction if, and to the extent that, no suchliability has been incurred

BKAF 3063 A132 25

Arrangement Provides the

Counterparty With A Choice of

Settlement

An entity has granted the counterpartythe right to choose whether a share-based payment transaction is settled incash or by issuing equity instruments.

In this case, the entity has granted acompound financial instrument, whichincludes

A debt component

An equity component

BKAF 3063 A132

26

Arrangement Provides the

Counterparty With A Choice of

Settlement… cont

For transactions with parties other than

employees, the entity should:

a) measure the fair value of the goods or

services acquired

b) measure the fair value of the debt

component

The fair value of the equity component is

the difference between a) and b).

BKAF 3063 A132

27

Arrangement Provides the

Counterparty With A Choice of

Settlement… cont

• At the date of settlement,

If the conterparty demand settlement in

equity instruments, the entity should transfer

the liability to equity, as the consideration for

the equity instruments issued (para 39)

If the conterparty demand settlement in

cash, the entity should treat that payment

as full settlement of the liability. Any equity

component previously recognised shall

remain within equity. (para 40)

BKAF 3063 A132

28

Arrangement Provide The Entity With

A Choice of Settlement

Should determine whether it has a presentobligation to settle in cash and account for theshare-based payment transaction accordingly.

The entity has a present obligation to settle incash if Choice of settlement in equity instruments has no

commercial substances

Has a past practice or stated policy of settling incash

Generally settles in cash whenever the counterpartyasks for cash settlement.

BKAF 3063 A132

29

Arrangement Provide The Entity With

A Choice of Settlement… cont

If the entity has a present obligation to settle in cash, it shall account for the transaction in accordance with the requirements applying to cash-settled share-based payment transaction. [Para 30-33(para 42)]

If the entity has no such obligation exists, it shall account for the transaction in accordance with the requirements applying to equity-settled share-based payment transactions. [Para 10-29(para 43)]

BKAF 3063 A132

30

Disclosures

Paragraph 44: enables users of the financialstatements to understand the nature and extent ofshare-based payment arrangements that existedduring the period.

Paragraph 45 should disclose: Description of each type of share-based payment

arrangement that existed at any time during the period The number and weighted average exercise prices of

shares options The weighted average share price at the date of exercise

for share options exercised during the period The range of exercise prices and weighted average

remaining contractual life.

BKAF 3063 A132

31

Continue..

Paragraph 46: understand how the fair value of thegoods or services received or the fair value of theequity instruments granted.

Paragraph 47: measured indirectly the fair value ofgoods or services received as consideration for theequity instruments of the entity.

Paragraph 48: measured directly the fair value ofgoods or services received.

Paragraph 49: explain why the presumption need to berebutted.

BKAF 3063 A132

32

Continue…

Paragraph 50: disclose information

about the effect of share-based payment

transactions on the entity’s profit or loss

and on its financial position.

Paragraph 51: stated the minimum

disclosure

BKAF 3063 A132

33

Continue…

Para 51 - To give effect to the principle in paragraph 50, the entity shall disclose at least the following:

(a) the total expense recognised for the period arising from share-based payment transactions in which the goods or services received did not qualify for recognition as assets and hence were recognised immediately as an expense, including separate disclosure of that portion of the total expense that arises from transactions accounted for as equity-settled share-based payment transactions;

(b) for liabilities arising from share-based payment transactions:

i. the total carrying amount at the end of the period; and

ii. the total intrinsic value at the end of the period of liabilities for which the counterparty’s right to cash or other assets had vested by the end of the period (egvested share appreciation rights).

BKAF 3063 A132

34

BKAF 3063 A132

35