topic 4 audit planning including analytical procedures

TRANSCRIPT

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 1/28

1

TOPIC 4

AUDIT PLANNING

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 2/28

2

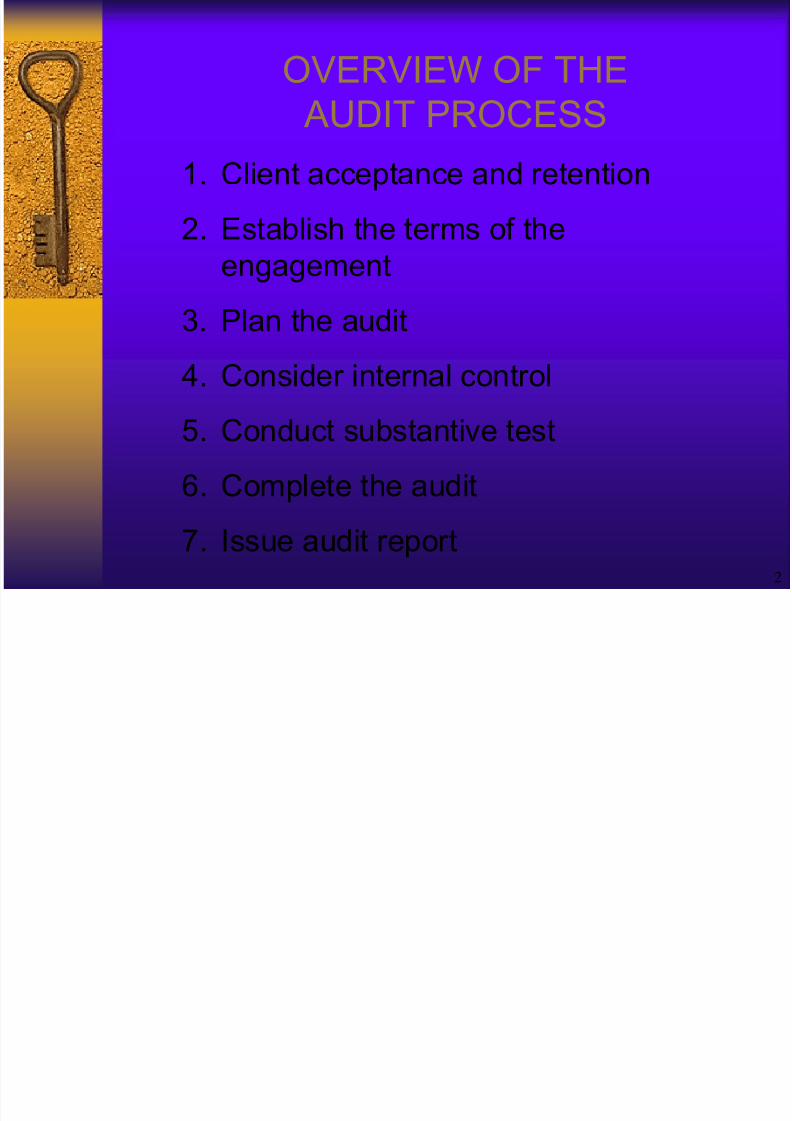

OVERVIEW OF THE

AUDIT PROCESS

1. Client acceptance and retention

2. Establish the terms of the

engagement3. Plan the audit

4. Consider internal control

5. Conduct substantive test

6. Complete the audit

7. Issue audit report

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 3/28

3

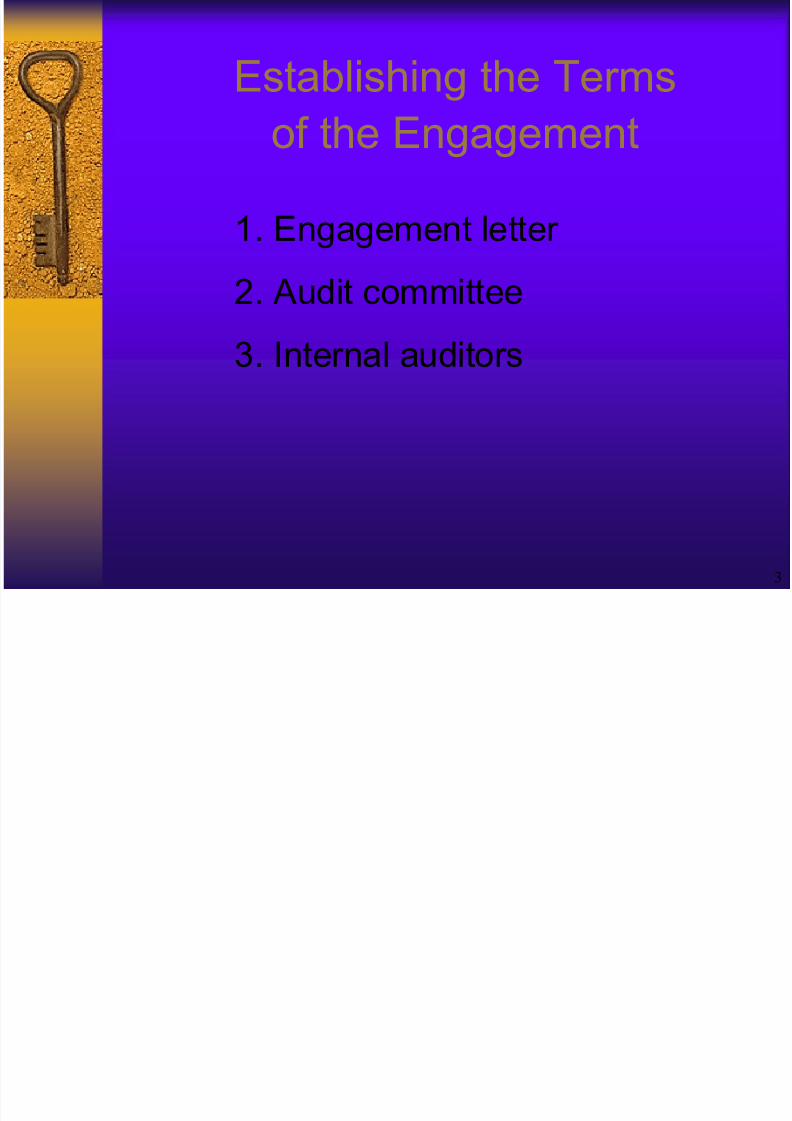

Establishing the Terms

of the Engagement

1. Engagement letter

2. Audit committee

3. Internal auditors

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 4/28

4

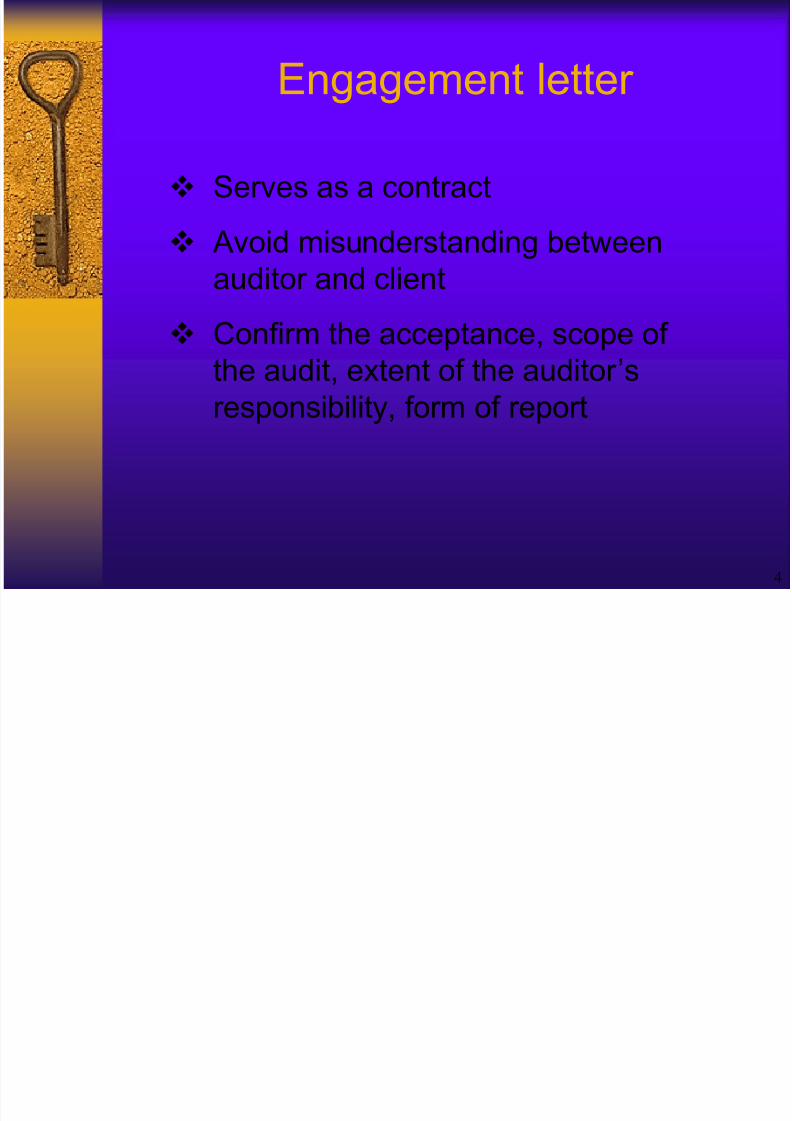

Engagement letter

Serves as a contract

Avoid misunderstanding between

auditor and client

Confirm the acceptance, scope of

the audit, extent of the auditor’s

responsibility, form of report

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 5/28

5

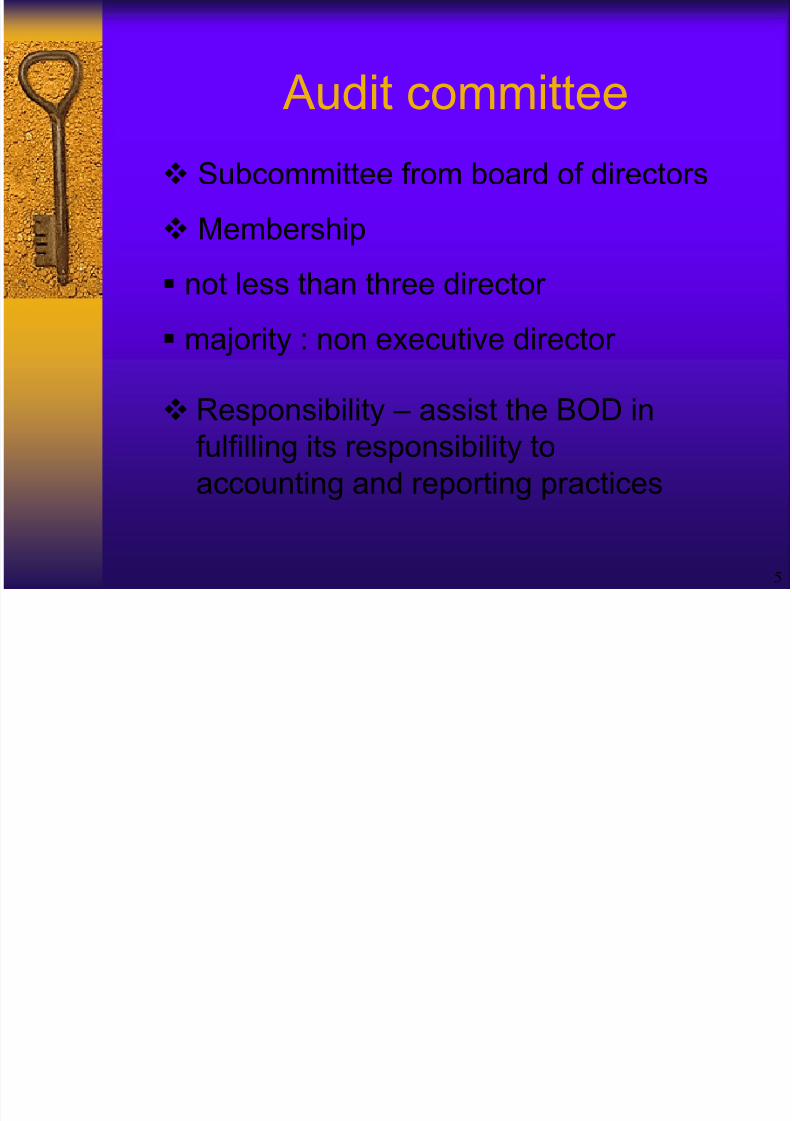

Audit committee

Subcommittee from board of directors

Membership

not less than three director

majority : non executive director

Responsibility – assist the BOD infulfilling its responsibility to

accounting and reporting practices

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 6/28

6

Audit committee cont’d

Typical functions and duties:

Recommend or consider thenomination of the external auditor

Consider and review with the

external auditors their audit plan

Review with the ext. auditor

- audited f/s and audit report

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 7/287

Audit committee cont’d

Before the engagement starts, the

audit committee should meet with the

external auditor to discuss: Auditors’ responsibility

Assistance to be given to the auditors

by the company’s officer

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 8/288

Internal auditors

ISA 610 Considering the Work of

Internal Auditor

External auditor should consider theactivities of int. auditing and their

effect on ext. audit procedures

External auditor should obtain

sufficient understanding of the int.

audit activities to assist in planning

the audit

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 9/289

Internal auditors cont’d

External auditor must assess the

internal auditor’s competence and

objectivity

Competence – educational level and

professional experience

- Professional certification

Objectivity – organizational status,

scope of responsibility

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 10/2810

Categories of planning

1. Pre-engagement activities

2. Engagement-planning activities

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 11/2811

Pre-engagement activities

Client acceptance and retention

1. Evaluate prospective client

2. Evaluate whether to retain their

current client

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 12/2812

Engagement Planning Activities

Determine the audit staffing

requirements

Obtain knowledge of the client’s

business and industry

Consider going concern issue

Establish materiality,audit risk andassess inherent risk

Assess the possibility of errors,fraud

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 13/2813

Determine the audit staffing

requirements Engagement size and complexity

Level of risk

Requirement for special expert

Personnel availability

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 14/2814

Obtain knowledge of the client’s

business and industry

ISA 320 – “Knowledge of the Business”

Why ?

How to obtain info?

Impact to audit planning

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 15/2815

Consider going concern issue

The auditor’s report helps establishthe credibility of the financial

statements. However, the auditor’s

report is not a guarantee as to the

future viability of the entity.

When planning and performing audit

procedures & in evaluating the results

thereof, the auditor should consider

the appropriateness of the going

concern assumption underlying the

preparation of the financial statements.

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 16/2816

Going concern issue cont’d

Carry out additional audit procedures

Analyze and discuss cash flow, profit

and other relevant forecasts withmanagement.

Review events after period end for items

affecting the entity’s ability to continueas a going concern.

Analyze and discuss the entity’s latest

available interim financial statements.

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 17/2817

Establish materiality,audit risk

and assess inherent risk Materiality – if its omission or

misstatement could influence the

economic decision of users.

Audit risk - give inappropriate audit

opinion when the financial statements

are materially misstated

Inherent risk – risk that exist regardless

of internal control

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 18/2818

Assess the possibility of

errors,fraud Evaluate the risk of material

misstatement that may be caused

by fraud or error.

Reasonable assurance

Professional skepticism

Understand management vs

auditors’ responsibility

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 19/2819

Assess the possibility of

errors,fraud cont’d

Analytical procedures disclose

differences from expectations

Unreconciled differences exist a

control account and subsidiary

records.

Confirmation requests disclose

significant differences or a lower-

than-expected response rate

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 20/2820

Understand the Applicable

Laws & RegulationsISA 250

Legal provisions that determine the

form and content of the client’ f/s.

Laws and regulations that affect the

continuing operation

Non-compliance of which can result

in financial consequences such as

fines and litigations

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 21/2821

Identify Related Parties

MASB 8’ “Related Party Disclosures

Enterprises that control or are

controlled by the reporting enterprise

Enterprise that exercise significant

influence, or subject to significant

influence by the reporting enterprise Subsidiaries of enterprise that

exercise significant influence over

the reporting enterprise

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 22/28

22

Identify Related Parties cont’d

The auditor - perform audit proceduresto obtain sufficient appropriate audit

evidence :

(a) identification and disclosure bymanagement of related parties

(b) the effect of related party transactions

that are material to the fin. statements.

Management is responsible to identifyand disclose - related parties and

transactions with such parties.

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 23/28

23

Identify Related Parties cont’d

a) Disclosure requirement

- certain related party relationships and

transactions - IAS 24;

b) the existence of related parties or

related party transactions may affectthe financial statements.

Why auditor should aware ?

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 24/28

24

Identify Related Parties cont’d

c) the source of audit evidence affects

the auditor’s assessment of its

reliability.

d) a related party transaction may be

motivated by other than ordinary

business considerations.

Example : profit sharing or even fraud.

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 25/28

25

Identify Related Parties cont’d

Additional audit procedures to identify

related parties’ transactions:

Review the minutes of the BOD &executive for info. about material

transactions authorized.

Review conflict-of-interest statements.

Review accounting records – large,

unusual, non-recurring transactions or

balances

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 26/28

26

Conduct Preliminary

Analytical Procedures

ISA 520 – the analysis of significant

ratios and trends and the resulting

investigation of fluctuations and

relationship that are inconsistent with

other relevant info. or deviate from

predicted amounts

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 27/28

27

Conduct Preliminary

Analytical Procedures cont’d

Objectives:

To enhance auditor’s understanding

of the client’s biz, transactions, and

events.

To identify areas that are likely to

contain errors or potential risk.

7/30/2019 Topic 4 Audit Planning Including Analytical Procedures

http://slidepdf.com/reader/full/topic-4-audit-planning-including-analytical-procedures 28/28

Conduct Preliminary

Analytical Procedures cont’d

Compare current year financial info:

Prior period(s) data

Budgets, projection, and

forecast

Industry data

Non-financial info