to our unitholders, - ag growth international · to our unitholders, ... we must keep the market...

TRANSCRIPT

To Our Unitholders, On behalf of the management, employees and the board of trustees of Ag Growth Income Fund, we are pleased to present our financial results for the third quarter ended September 30, 2008. The third quarter of 2008 was the strongest ever for the Fund. We achieved revenues of $60.0 million (2007- $40.7 million) an increase of almost 50% over the prior year. Our EBITDA*, adjusting for foreign exchange gains or losses, increased 31% over 2007 to $15.1 million (2007 - $11.5 million). What a difference a couple of months can make. Equity markets have been hit with a major liquidation that has impacted equities around the world. In particular, commodities have experienced a major sell off as investors fear global recession. Agricultural commodities have not escaped this carnage. Corn is trading below $4.00 per bushel and soybeans have settled below $10.00 per bushel. This is substantially below levels of a few months ago when corn approached $8.00 and soybeans traded in the mid teens as a result of an overreaction to the possible effect of spring floods in the U.S. Midwest. Although this has unnerved many investors, we must keep the market fundamentals in perspective. For almost ten years after the 1997 Asian crisis corn traded in a tight range between $2.00 and $2.50 per bushel. Soybeans traded in the $6.00 range and wheat in the $3.00-$4.00 range. Corn at $4.00, soybeans at $9.00 and wheat at $5.50 represents a pullback from recent highs but remains well above levels at which producers have historically operated profitably. At the writing of this report, harvest was still being completed in the northern regions of the U.S. Midwest that were negatively impacted by flooding at the beginning of the year. This year’s harvest will have one of the latest completion dates of the last 20 years. Although the USDA’s recently announced 2008 corn crop estimate of 12.02 billion bushels represents a substantial decline from last year’s corn harvest of over 13 billion bushels, the 2008 estimate still represents the second largest corn crop in US history. Even with two successive large crops, grain carryovers are anticipated to be at or near multi-decade lows. Recent economic developments have given cause to reassess the state of our segment of the agricultural sector. The characteristics of our equipment give us confidence regarding the sustainability of our growth. Small ticket equipment, the demand for which is primarily driven by grain volumes, has a distinct advantage over larger items such as tractors, combines and tillage equipment in times of lower commodity prices. When asked about the outlook for auger sales in 2009, one of our largest distributors replied “We are in the sweet spot of equipment manufacturers”. We couldn’t have said it better ourselves. This has proven itself through past pullbacks in agricultural markets and we believe this will again be the case. In addition, farmers have the most conservative balance sheets they have had in the last ten years with debt representing less than 10% of total assets. Despite the credit crunch that is affecting many industries, we feel it will have a much more tempered effect on domestic agricultural producers than many other sectors.

1

We are, however, anticipating a pull back in our larger commercial equipment as the tightening of credit will have a more pronounced short term impact on larger capital projects for grain handlers. This equipment represents approximately 20% of our historic revenue base. We hope to offset much of this decline through our recent efforts in expanding our overseas markets. I have recently spent time traveling with our marketing team in emerging markets such as Russia, Kazakhstan, Ukraine and Brazil, in an attempt to assess the potential size of these markets. The large scale of farms that exist or are being assembled are conducive to the adoption of our type of equipment. These countries have corporate farming operations that are of individual scale that dwarf the size and scope of North American farming operations. More importantly, recognition of the benefits of and payback from preserving the quality of the grain through on-farm storage and aeration is greatly increasing. These emerging market nations as a rule only have on farm storage capacity representing 10% of annual grain production. This compares to over 80% capacity in Canada and approximately 70% in the U.S. Despite tightening in the availability of credit in these markets, we believe that substantial growth opportunities exist as they accelerate their efforts to maximize the value they receive for their grain. Our broad catalogue of grain handling, storage and conditioning products have positioned us well to have a strong competitive advantage when entering these exciting new markets. We are aggressively building the business plan to establish these international markets as the new long term growth driver for our business. This has been a transition year for the Fund. Aggressive product line acquisitions in 2007 have created opportunities but have also caused a few digestion problems in 2008. We are diligently working through these challenges. The product line acquisitions have positioned the company to begin reaping the rewards of our expanded catalogue in 2009. In particular, the introduction of grain bins through the Twister acquisition and commercial handling equipment through the Hi Roller and Union Iron acquisitions have positioned us well to enter overseas markets. Our biggest hurdle, the capacity expansion at Westfield, our largest division, finally is delivering the benefits that we promised the market at the outset of the project. Our ship rate in the second half of the year is exceeding last years run rate by 68%. We believe we are now beginning to see market share gains in this expanding market as we are ahead of our competitors in capacity expansion. We anticipate another strong year from Westfield, which is still our flagship division. As we complete the third quarter, we have finally eliminated backlogs at Westfield that were locked in at older price levels that did not compensate for the dramatic run up in steel prices earlier this year. We are still hampered by backlogs at Twister and Edwards where pricing does not yet reflect the higher input costs, but we expect to be benefiting from increased prices by the end of the year. In the last month the fear of recession has

2

seen softening in steel prices. We will be burdened for a period of time with higher priced steel inventory, but expect to realize the benefit from lower input costs in 2009. The recent dramatic drop in the Canadian dollar has allowed us to lock in currency hedges at lower rates than in the last couple of years. We will be negatively impacted by the repricing of our US dollar denominated debt if the currency remains at current levels, but given that the majority of our sales are also US dollar denominated we expect this negative impact will be more than offset by margin expansion in 2009. The equity and debt market as well as concerns over the sustainability of the agricultural cycle has hurt our trust unit price. Given the strength of our balance sheet and our low debt levels relative to cash flow we requested and received approval to begin a unit buyback. Our normal course issuer bid commenced in late October. Overall, despite the concerns of some regarding the end of the agricultural cycle, we will continue to build for a solid growth year until we see evidence to the contrary. We have been in this industry for many years and have been correct more often than not with respect to the interpretation of the macro economic situation. We again intend to trust our instincts in these uncertain times. The world is having increasing difficulty keeping supply tracking with demand growth. What is becoming apparent as we have expanded our sights outside of North America is that there is enough land to feed the world. The answer to the supply demand equation is reducing the extensive loss of crop in developing nations as a result of archaic storage, handling and conditioning practices. We are convinced of this but more importantly producers and governments in these markets are finally recognizing this too. Our job is to capitalize on the opportunity!! We thank all of our customers, suppliers, employees and investors who have supported us to date. If you agree with our vision and commit to our plan in the long term we believe you all will be rewarded. Yours Truly, Rob Stenson Chief Executive Officer Ag Growth Income Fund * See “non-GAAP measures” in the Management’s Discussion and Analysis.

3

AG GROWTH INCOME FUND MANAGEMENT’S DISCUSSION AND ANALYSIS NOVEMBER 13, 2008 This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with the audited consolidated financial statements and accompanying notes of Ag Growth Income Fund (the “Fund”) for the year ended December 31, 2007 and the unaudited interim consolidated financial statements of the Fund for the three and nine month periods ended September 30, 2008. Results are reported in Canadian dollars unless otherwise stated and have been prepared in accordance with Canadian generally accepted accounting principles. Throughout this Management's Discussion and Analysis references are made to "EBITDA", “gross margin”, "standardized distributable cash", “adjusted distributable cash” and "payout ratio". A description of these measures and their limitations are discussed below under "Non-GAAP Measures". See also "Risks and Uncertainties" and "Forward-Looking Statements" below. FORWARD-LOOKING STATEMENTS This Management’s Discussion and Analysis contains forward-looking statements that reflect our expectations regarding the future growth, results of operations, performance, business prospects, and opportunities of the Fund. Forward-looking statements may contain such words as “anticipate”, “believe”, “continue”, “could”, “expects”, “intend”, “plans”, “will” or similar expressions suggesting future conditions or events. Such forward-looking statements reflect our current beliefs and are based on information currently available to us. Forward-looking statements involve significant risks and uncertainties. A number of factors could cause actual results to differ materially from results discussed in the forward-looking statements, including changes in national and local business conditions, crop yields, crop conditions, seasonality, industry cyclicality, volatility of production costs, commodity prices, foreign exchange rates, and competition. These risks and uncertainties are described under “Risks and Uncertainties” and in our Annual Information Form. Although the forward-looking statements contained in this MD&A are based on what we believe to be reasonable assumptions, we cannot assure readers that actual results will be consistent with these forward-looking statements and we undertake no obligation to update such statements except as expressly required by law. OVERVIEW OF THE FUND The Fund is an unincorporated, open-ended, limited purpose trust established under the laws of the Province of Ontario. The Fund holds indirectly all of the securities of Ag Growth Industries Inc. (“Ag Growth”), which conducts business in the grain handling, storage, and conditioning market. The following units of the Fund (“Trust units”) were issued and outstanding and participated pro rata in distributions during the periods indicated:

4

# Trust units

# Class B units (1)

# Total units

December 31, 2006 11,088,915 136,085 11,225,000 October 2, 2007 equity financing 1,730,000 0 1,730,000

December 31, 2007 and September 30, 2008 12,818,915 136,085 12,955,000 Units purchased under normal course issuer bid (172,100) 0 (172,100)

November 13, 2008 12,646,815 136,085 12,782,900 (1) The previous owners of Ag Growth were issued Class B exchangeable limited partnership units (“Class B units”) of AGX Holdings Limited Partnership (“AGHLP”), a wholly owned subsidiary of the Fund. The Class B units are exchangeable for Trust units of the Fund at the option of the holder on a one-for-one basis at any time. The Trust units of the Fund and the Class B units of AGHLP participate pro rata in distributions. The Fund has issued one Special Voting Unit for each Class B unit outstanding. The Special Voting Units are not entitled to any interest or share in the Fund, or in any distribution from the Fund, but are entitled to vote on matters related to the Fund. On October 22, 2008, the Fund commenced a normal course issuer bid for up to 1,262,090 Trust units, representing 10% of the Fund’s public float. The normal course issuer bid will terminate on October 21, 2009 unless terminated earlier by the Fund. Units purchased under the normal course issuer bid will be cancelled. Trust units are purchased at market price and in accordance with Toronto Stock Exchange (“TSX”) requirements. The Fund has granted 220,000 unit awards under its unit award incentive plan approved by unitholders in May 2007. The unit awards remain outstanding at September 30, 2008 and November 13, 2008 and, subject to vesting and payment of the exercise price, are each exercisable for one Trust unit. The Fund’s Trust units trade on the Toronto Stock Exchange under the symbol AFN.UN. RATE OF FOREIGN EXCHANGE Impact on U.S. dollar denominated sales and expenses The appreciation of the Canadian dollar is a significant factor when comparing results for the three and nine month periods ended September 30, 2008 to the same periods in 2007. The Fund’s average rate of exchange per U.S. dollar for the three and nine months ended September 30, 2008 was $1.03 and $1.01, respectively, compared to $1.06 and $1.11 for the same periods in 2007. A stronger Canadian dollar will result in lower sales and lower expenses as transactions denominated in U.S. dollars are translated to Canadian dollars at a lower rate. As the Fund’s sales denominated in U.S. dollars greatly exceed its expenses denominated in that currency, a stronger Canadian dollar negatively impacts operating results of the Fund. The Fund’s average rate of exchange for the fourth quarter of 2007 was $0.99, and for the quarters ended March 31, 2008 and June 30, 2008 was $0.99 and $1.01, respectively. The Canadian dollar has recently weakened and unless it recovers to these levels, in future quarters the impact of foreign exchange will benefit the Fund’s operating results when comparing to prior periods.

5

Impact on gain (loss) on foreign exchange The Fund’s gain (loss) on foreign exchange on the income statement is comprised of gains or losses on foreign exchange hedging contracts as well as the impact of translating U.S. dollar denominated assets and liabilities, including U.S. dollar denominated long-term debt, into Canadian dollars using the foreign exchange rate in effect at the end of the reporting period. As the Canadian dollar strengthened throughout 2007, the Fund recorded large gains when translating its U.S. dollar denominated debt into Canadian dollars. The opposite was true in the third quarter of 2008, as the Canadian dollar weakened and the Fund recorded an unrealized loss on its U.S. dollar denominated debt. Largely due to the impact of U.S. dollar denominated debt, for the three and nine months ended September 30, 2008, the Fund has recorded a loss on foreign exchange of $1.2 million and $1.5 million, respectively, compared to gains of $1.1 million and $2.3 million for the same periods in 2007. The Canadian dollar has weakened significantly to date in the fourth quarter of 2008. Accordingly, unless the Canadian dollar recovers before the end of the Fund’s fiscal year, the Fund anticipates it will record a large unrealized loss on its U.S. dollar denominated long-term debt in the fourth quarter of 2008. OPERATING RESULTS (thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Sales $60,012 $40,762 $151,100 $103,808 Cost of goods sold 38,134 23,492 97,330 61,743

Gross margin 21,878 17,270 53,770 42,065

General, administrative and other (1) 6,884 5,261 20,387 14,659 Long-term incentive plan 150 157 700 471 Unit award incentive plan (220) 397 637 686 Loss (gain) on foreign exchange 1,242 (1,117) 1,537 (2,254) Amortization 2,063 1,572 6,106 3,905 Interest expense 772 855 2,002 2,141

Earnings before tax 10,987 10,145 22,401 22,457 Current income taxes 1,094 1,109 2,899 1,412 Future income taxes 140 60 400 11,353

Net earnings for the period $9,753 $8,976 $19,102 $9,692 EBITDA * $13,822 $12,572 $30,508 $28,503 EBITDA before loss (gain) on FX $15,064 $11,455 $32,045 $26,249 Net earnings per unit $0.75 $0.80 $1.47 $0.86 * See “non-GAAP Measures”. (1) Comprised of selling, general and administrative expenses, professional fees, research and development, capital taxes and other expense (income).

6

ASSETS AND LIABILITIES (thousands of dollars)

September 30 2008

September 30 2007

Total assets $230,888 $183,462 Total liabilities $84,495 $74,734 Distributions Declared The table below summarizes the distributions declared for Trust units of the Fund and for Class B units of AGHLP. The Fund’s distribution policy is described in the “Distributions” section of this MD&A. DISTRIBUTIONS (thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Trust units $6,153 $4,657 $16,921 $13,972 Class B units 65 57 180 171

Total distributions $6,218 $4,714 $17,101 $14,143 Acquisitions The inclusion of the assets, liabilities and operating results of the following acquisitions significantly impacts comparisons to 2007: Effective May 31, 2007, the Fund acquired substantially all of the operating assets of Twister Pipe Ltd. (“Twister”), a manufacturer of grain storage bins, aeration equipment, and bin unload systems. Subsequent to the acquisition the assets, liabilities and operations of Twister were integrated with the Fund’s Edwards division. Effective November 19, 2007, the Fund acquired 100% of the outstanding shares of Union Iron Inc. (“Union Iron”) and the shares and assets of certain related companies of Union Iron, a manufacturer of material handling and storage equipment. Effective January 15, 2008, the Fund acquired substantially all of the assets of Applegate Steel Inc. (“Applegate”), a manufacturer of livestock equipment. Overall Performance Strong demand for portable grain handling and aeration equipment and a significant increase in production at the Westfield division has resulted in a substantial increase in sales compared to 2007. The table below summarizes consolidated sales as well as sales at core divisions (defined as those divisions reporting full three and nine month results in both 2007 and 2008):

7

SALES (in thousands)

Three Months Ended Nine Months Ended Core Consolidated Core Consolidated

September 30, 2008 $44,787 $60,012 $118,655 $151,100 September 30, 2007 $38, 126 $40,762 $100,213 $103,808 Increase $6,661 $19,250 $18,442 $47,292 Percentage increase 17% 47% 18% 46% Gross margin (see “non-GAAP measures”) as a percentage of sales for the three and nine month periods ended September 30, 2008 was 36.5% (2007 – 42.4%) and 35.6% (2007 – 40.5%), respectively. Previously disclosed gross margin issues at Westfield have been resolved. Compared to 2007, gross margin was negatively impacted by integration issues at the Edwards/Twister division, increases in input costs, particularly raw steel, and a stronger Canadian dollar. The Fund has announced several sales price increases to offset the increase in input costs, however the impact of these price increases for the periods ended September 30, 2008 has been limited as the Fund honoured old pricing on its backorder. Management initiatives to enhance gross margin percentages have been largely successful, as gross margin excluding Edwards/Twister was 41.5% and 40.1% in the three and nine months periods ended September 30, 2008, and excluding both Edwards/Twister and the impact of foreign exchange, was 42.2% and 41.9%. The Fund has enhanced management depth and made organizational changes at Edwards/Twister, and expects gross margin improvements over the next several quarters to result from enhanced labour productivity, the realization of previously announced price increases, and the continuation of higher sales volume. EBITDA for the three and nine month periods ended September 30, 2008 was $13.8 million (2007 - $12.6 million) and $30.5 million (2007 - $28.5 million), respectively. The increase in EBITDA was due primarily to a significant increase in sales and gross margin at Westfield, strong results at Hi Roller, offset by the gross margin pressures discussed above and a significant decrease in the gain on foreign exchange. As a percentage of sales, EBITDA for the three and nine months ended September 30, 2008 was 23% and 20%, respectively (2007 – 31% and 27%). As discussed under “Foreign Exchange” the Fund has recorded losses in 2008 on its U.S. dollar denominated debt. Excluding the gain (loss) on foreign exchange, which encompasses the impact of translating U.S. denominated debt into Canadian dollars, EBITDA in the three and nine month periods ended September 30, 2008 was $15.1 million (2007 - $11.5 million) and $32.0 million (2007 - $26.2 million), respectively. Sales Sales for the three months ended September 30, 2008 were $60.0 million, including $15.2 million at divisions acquired in 2007 and 2008. Excluding the impact of acquisitions, sales in the third quarter of 2008 were $44.8 million, compared to $38.1 million in 2007. The increase of $6.7 million or 17% over 2007 is largely due to the following:

• Sales of grain handling equipment in the North American market, in particular Westfield augers and Batco conveyors, increased significantly (30% over the prior year) due to exceptional farm level demand.

8

• Sales at Hi Roller in the three month period decreased $2.1 million from the third quarter of 2007. Hi Roller sales in the third quarter of 2007 were exceptional due to a sizeable ethanol industry component.

• Total international sales for the quarter were $3.6 million (2007 - $1.9 million). The increase is largely due to the development of new markets in Russia and Kazakhstan.

• Sales were negatively impacted by foreign exchange. Had the average exchange rates experienced in 2007 been in effect in 2008, all other factors remaining constant, sales excluding acquisitions would have increased an additional $0.7 million.

Sales for the nine months ended September 30, 2008 were $151.1 million, including $32.4 million at divisions acquired in 2007 and 2008. Excluding the impact of these acquisitions, sales in the nine month period were $118.7 million, compared to $100.2 million in 2007. The increase of $18.5 million or 18% over 2007 is largely due to the following:

• Sales of grain handling equipment in the North American market, in particular Westfield augers and Batco conveyors, increased significantly (24% over the prior year) due to exceptional farm level demand.

• Sales at Hi Roller for the nine month period increased $0.1 million compared to 2007 as an increase in sales to its traditional customer base and growth in overseas markets more than offset the decrease in sales to the ethanol industry.

• Total international sales were $11.6 million (2007 - $4.3 million). The increase is largely due to the development of new markets in Russia and Kazakhstan.

• Sales were negatively impacted by foreign exchange. Had the average exchange rates experienced in 2007 been in effect in 2008, all other factors remaining constant, sales excluding acquisitions would have increased an additional $8.5 million.

Foreign Exchange Sales and expenses denominated in a foreign currency are recorded each month at the rate of exchange in effect on the closing business day of the previous month. For the three and nine months ended September 30, 2008, sales denominated in U.S. dollars accounted for 78% and 76% of total sales respectively (2007 - 74% and 73%) and U.S. dollar denominated expenses equated to 34% and 36% of sales for the periods then ended (2007 – 25% and 28%). As sales denominated in U.S. dollars significantly exceed purchases denominated in that currency, the Fund’s operating results are negatively impacted by a strengthening Canadian dollar. The Fund’s average rate of exchange for the three and nine months ended September 30, 2008 was $1.03 and $1.01 respectively, compared to $1.06 and $1.11 in 2007. Ag Growth has entered into a series of hedging arrangements to partially mitigate the potential effect of fluctuating exchange rates. Realized gains or losses on foreign currency hedging instruments have been included, along with the gain or loss on the translation of U.S. dollar monetary items, in operating expenses as a gain or loss on foreign exchange. Gross Margin Gross margin as a percentage of sales for the three and nine months ended September 30, 2008 was 36.5% and 35.6%, respectively, compared to 42.4% and 40.5% in 2007. The decrease in gross margin percentages compared to 2007 was largely due to the following:

• The inclusion of Twister negatively impacted gross margin percentages due primarily to set-up and integration issues. Excluding the Edwards/Twister division, gross margin for

9

the three and nine months ended September 30, 2008 was 41.5% and 40.1% respectively. The Fund has enhanced management depth and made organizational changes at Edwards/Twister, and expects gross margin improvements over the next several quarters to result from enhanced labour productivity, the realization of previously announced price increases, and the continuation of higher sales volume.

• The comparison to 2007 was negatively impacted by foreign exchange. Excluding the impact of the Edwards/Twister division and the stronger Canadian dollar, gross margin as a percentage of sales for the three and nine months ended September 30, 2008 would have been 42.0% and 41.9% respectively.

• Although Westfield’s previously disclosed gross margin issues were resolved with the completion of the capacity improvement initiative in March 2008, the project negatively impacted first quarter gross margin percentages prior to its completion.

• Gross margin was negatively impacted by increases in the price of steel. The Fund has implemented a number of price increases to address rising input costs, however these price increases are generally not applied to its back order and accordingly there is a lag effect between the date of a price increase announcement and the full realization by the Fund of the higher sales price. The lag effect most materially affected Westfield and Edwards/Twister. The Fund expects the benefit of all price increases to fully impact the first quarter of 2009.

• The Fund’s sales mix has changed substantially with the acquisitions of Twister, Union Iron, and Applegate. These are inherently lower margin businesses and their inclusion in the Fund’s consolidated results will lower the consolidated gross margin percentage. Divisions that were acquired in 2007 and 2008 accounted for 25% and 21% of total sales in the three and nine months ended September 30, 2008.

Expenses For the three months ended September 30, 2008, selling, general and administrative expenses were $6.6 million or 11% of sales. Excluding acquisitions, selling, general and administrative expenses were $5.3 million or 12% of sales (2007 - $4.8 million or 13% of sales). The increase of $0.5 million over 2007 is primarily due to the following:

• Salary expense increased $0.2 million due largely to personnel additions to facilitate growth and acquisition integration, wage adjustments, and a number of smaller items.

• Sales and marketing expense increased $0.2 million due largely to the development of an international sales group and investment in offshore territory development.

• A number of miscellaneous items accounted for the remaining change. For the nine months ended September 30, 2008, selling, general and administrative expenses were $19.3 million or 13% of sales. Excluding acquisitions, selling, general and administrative expenses were $15.8 million or 13% of sales (2007 - $13.4 million or 13% of sales). The increase of $2.4 million over 2007 is primarily due to the following:

• Commission expense payable to third parties increased $0.5 million largely due to increased sales at Westfield and Hi Roller’s customer mix.

• Salary expense increased $0.5 million due largely to personnel additions to facilitate growth and acquisition integration, wage adjustments, and a number of smaller items.

• Sales and marketing expense increased $0.5 million due largely to the development of an international sales group and investment in offshore territory development.

• Repairs and maintenance increased $0.3 million due to a number of small items at Westfield and Edwards.

• A number of miscellaneous items accounted for the remaining change.

10

Variances compared to the three and nine months ended September 30, 2007 were also recorded in the following:

• The Fund adopted a unit award incentive plan in May 2007. Calculation of the expense is

based on the trading price of the Trust units at the balance sheet date and the vesting provisions of the plan. For the three months ended September 30, 2008, the fund recorded a recovery of $0.2 million (2007 – expense of $0.4 million) and for the nine months then ended recorded an expense of $0.6 million (2007 – $0.7 million).

• In 2007 the Fund adopted an amended long-term incentive plan (“LTIP”) that provides for annual awards based on distributable cash generated. The awards are expensed over the term of the participant’s vesting period and as a result the expense in 2008 includes a component related to the fiscal 2007 award as well as a component related to the current fiscal year. For the three and nine months ended September 30, 2008, the Fund recorded an expense related to the LTIP of $0.2 million and $0.7 million respectively (2007 - $0.2 million and $0.5 million).

• For the three and nine months ended September 30, 2008 the Fund recorded a loss on foreign exchange of $1.2 million and $1.5 million respectively (2007 – gains of $1.1 million and $2.3 million). As discussed under “foreign exchange”, the gain (loss) on foreign exchange has been significantly impacted by measuring U.S. dollar liabilities at current exchange rates.

EBITDA and Net Earnings (see discussion of non-GAAP measures) EBITDA for the three and nine months ended September 30, 2008 was $13.8 million and $30.5 million, compared to $12.6 million and $28.5 million in 2007. The increases in EBITDA were largely the result of a significant increase in production and sales at the Westfield division that resulted from the completion of the Westfield capacity improvement initiative. EBITDA was negatively impacted by a lower consolidated gross margin percentage that resulted primarily from low margins at the Edwards/Twister division and the effect of a stronger Canadian dollar. As discussed under “Foreign Exchange” the Fund has recorded losses in 2008 on the translation of its U.S. denominated debt into Canadian dollars. Excluding the gain (loss) on foreign exchange, which includes the debt translation loss, EBITDA in the three and nine month periods ended September 30, 2008 was $15.1 million (2007 - $11.5 million) and $32.0 million (2007 - $26.2 million), respectively. The Fund’s credit facility includes operating lines of CAD $10.0 million and USD $2.0 million, and provides for long-term debt of up to USD $66.5 million. As at September 30, 2008, $5.9 million was drawn under the operating lines compared to a cash balance of $3.3 million at September 30, 2007. The Fund’s outstanding long-term debt is CAD $42.6 million (2007 - $48.9 million), comprised of term loans of USD $37.6 million and CAD $3.0 million. Interest rates on both facilities are based on performance calculations. For the three and nine months ended September 30, 2008, the Fund’s effective interest rate on its U.S dollar term debt was 6.5% and 6.9% respectively (2007 - 8.8% and 8.8%), and after consideration of the effect of the Fund’s interest rate swap was 6.2% and 6.1% (2007 – 6.3% in both periods). For the three and nine months ended September 30, 2007, the Fund’s effective interest rate on its Canadian dollar term debt was 4.9% in both periods. See “Financial Instruments”. Amortization for the three months ended September 30, 2008 was $2.1 million (2007 - $1.6 million) and included the amortization of capital assets of $1.3 million and the amortization of

11

intangible assets of $0.8 million. Amortization for the nine months ended September 30, 2008 was $6.1 million (2007 - $3.9 million) and included the amortization of capital assets of $3.9 million and the amortization of intangible assets of $2.2 million. Compared to 2007, amortization was most significantly impacted by the acquisitions of Twister, Union Iron and Applegate, and amortization of the new paint line at the Westfield facility. The Fund is a mutual fund trust for income tax purposes and therefore is not at this time subject to tax on income distributed to unitholders. The manufacturing business operations of the Fund’s divisions that are based in Canada are carried out within a limited partnership. Income from the limited partnership is not subject to tax but flows through to the holders of the partnership units, which includes the Fund. The Fund’s distributions are taxable in the hands of the unitholders. As a result of the Fund’s structure, a current tax provision is recorded only for the Fund’s subsidiary corporations, including its U.S. based divisions, and for the three and nine months ended September 30, 2008 the current tax provision was $1.1 million and $2.9 million respectively. For the three and nine months ended September 30, 2008 the Fund recorded a future tax expense of $0.1 million and $0.4 million respectively (2007 – $0.1 million and $11.4 million). The 2008 expense is related to the treatment of the Fund’s long-term incentive plan and unit award incentive plan, net of an expense derived primarily from the utilization of future tax assets. The 2007 expense included a charge related to new income trust tax legislation (see “Legislation Related to Income Trusts”). For the three and nine months ended September 30, 2008, the Fund recorded net earnings of $9.8 million and $19.1 million respectively (2007 – $9.0 million and $9.7 million) and earnings per basic and diluted unit of $0.75 and $1.47 (2007 – $0.80 and $0.86). Quarterly Financial Information (thousands of dollars):

2008

Sales Gain (Loss)

on FX Net Earnings

(Loss) Net Earnings

per Unit Q1 $35,138 $(586) $1,889 $0.14 Q2 55,950 291 7,460 0.58 Q3 60,012 (1,242) 9,753 0.75 Fiscal 2008 $151,100 $(1,537) $19,102 $1.47

2007

Sales

Gain (Loss) on FX

Net Earnings (Loss)

Net Earnings per Unit

Q1 $28,085 $ 59 $ 5,618 $0.50 Q2 34,960 1,078 (4,902) (0.44) Q3 40,762 1,117 8,976 0.80 Q4 26,563 1,864 2,674 0.20 Fiscal 2007 $130,370 $4,118 $ 12,366 $1.06

12

2006

Sales Gain (Loss)

on FX

Net Earnings Net Earnings

per Unit Q1 $19,704 $ 201 $ 4,116 $0.37 Q2 22,572 121 5,157 0.46 Q3 22,050 1,102 5,771 0.51 Q4 17,199 2,549 4,000 0.36 Fiscal 2006 $81,525 $3,973 $19,044 $1.70

Interim period revenues and earnings historically reflect some seasonality. The third quarter is typically the strongest primarily due to high in-season demand at the farm level. Adjusted distributable cash generated per unit will also typically be highest in the third quarter. Due to the seasonality of the Fund’s working capital movements, standardized distributable cash generated per unit will typically be highest in the fourth quarter. The following factors impact comparability between quarters in the table above:

• Sales, gain (loss) on foreign exchange, net earnings, and net earnings per unit are significantly impacted by the rate of exchange between the Canadian and U.S. dollars.

• The second quarter of 2007 includes a non-cash future tax accrual of $11.1 million related to the enactment of taxation laws related to income trusts for taxation years commencing January 1, 2011. The fourth quarter of 2007 includes a $1.6 million credit to future taxes to reflect a lower expected effective tax rate.

• Subsequent to January 15, 2008, results reflect the acquisition of Applegate. • Subsequent to November 19, 2007, results reflect the acquisition of Union Iron. • Subsequent to May 31, 2007, results reflect the acquisition of Twister. • Subsequent to December 31, 2006, results reflect the acquisition of Hi Roller.

CASH FLOW AND LIQUIDITY The table below reconciles net earnings to cash provided by (used in) operations for the three and nine months ended September 30, 2008 and 2007: (thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Net earnings for the period $9,753 $8,976 $19,102 $9,692 Add charges (deduct credits) to operations not requiring a current cash payment:

Amortization 2,063 1,572 6,106 3,905 Future income taxes 140 60 400 11,353 Translation gain on foreign exchange 1,730 (1,788) 2,832 (3,693) Non-cash interest expense 90 55 258 112 Long term incentive plan 150 0 700 0 Unit award incentive plan (220) 397 637 686 Loss (gain) on sale of property, plant & equipment

0 0 0 (40)

13,706 9,272 30,035 22,015

13

Net change in non-cash working capital balances related to operations:

Accounts receivable (1,549) 1,136 (22,427) (7,564) Inventory (2,941) 2,336 (10,573) 707 Prepaid expenses and other assets (402) 65 (861) (243) Accounts payable and accruals 787 345 4,103 506 Customer deposits (2,146) 280 (8,712) (4,223) Income taxes payable 758 265 1,186 (182)

(5,493) 4,427 (37,284) (10,999)

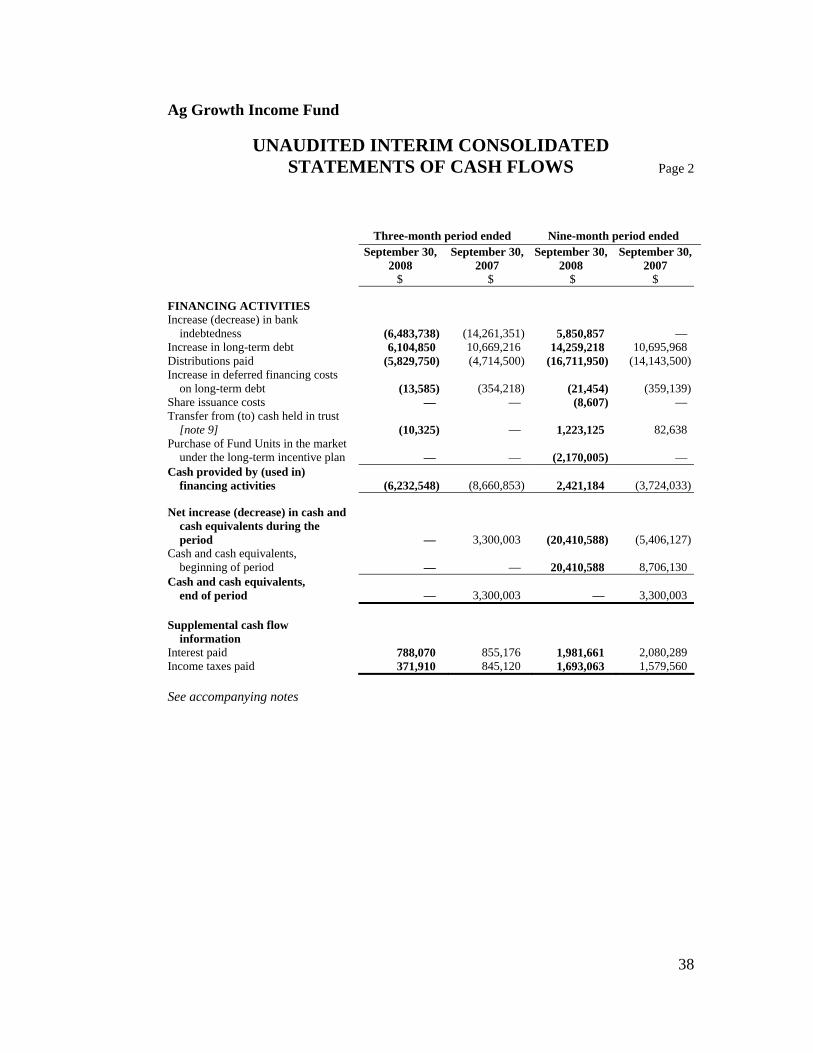

Cash provided by (used in) operations $8,213 $13,699 $(7,249) $11,016 For the three months ended September 30, 2008, cash provided by operations was $8.2 million (2007 - $13.7 million) and for the nine months then ended cash used in operations was $7.2 million (2007 – cash provided of $11.0 million). The increase in cash used in operations in 2008 is primarily due to changes in non-cash working capital. Increased demand resulted in a high level of customer deposits on hand at December 31, 2007, and accordingly a higher level of production and sales in 2008 related to cash received in 2007. Additional cash resources were required to support inventory levels in 2008 as an increase in purchasing resulted from increased production, higher input prices, and an increased investment in raw material to protect against rising input prices. An increase in period end accounts receivable resulted from higher sales. A number of smaller changes account for the remaining variance. Working Capital Interim period working capital requirements typically reflect the seasonality of the business. The Fund’s collections of accounts receivable are weighted towards the third and fourth quarters. This collection pattern, combined with seasonally high sales in the third quarter, result in accounts receivable levels increasing throughout the year and peaking in the third quarter. In order to ensure the Fund has adequate supply throughout its distribution network in advance of in-season demand, inventory levels must be gradually increased throughout the year. Accordingly, inventory levels typically increase in the first and second quarters and then begin to decline in the third or fourth quarter as sales levels exceed production. As a result of these working capital movements, historically, Ag Growth begins to draw on its operating lines in the first or second quarter. The operating line balance typically peaks in the second or third quarter and normally begins to decline later in the third quarter as collections of accounts receivable increase. Ag Growth has typically fully repaid its operating line balance by early in the fourth quarter. Operating results to date in 2008 have generally reflected these expectations, however, compared to prior years, additional cash resources were required to support inventory levels as an increase in purchasing resulted from increased production, higher input prices, and an increased investment in raw material to protect against rising input prices. Accordingly, the Fund’s consolidated inventory balance did not decrease in the third quarter as is typical, and largely due to the increased investment in inventory, the Fund’s cash balance at September 30, 2008 was below historical levels.

14

Capital Expenditures The Fund had maintenance capital expenditures of $0.5 million and $2.0 million for the three and nine months ended September 30, 2008 (2007 - $0.2 million and $1.2 million). Maintenance capital expenditures in 2008 relate primarily to purchases of a semi tractor unit and trailers and manufacturing equipment. The increase from 2007 is largely the result of the acquisitions of Twister, Union Iron and Applegate. Maintenance capital expenditures in a fiscal year are funded through cash from operations. Due to seasonality of the Fund’s cash flows, capital expenditures may be funded on a short-term basis through the Fund’s credit facilities (see “Capital Resources”). The Fund defines maintenance capital expenditures as cash outlays required to maintain plant and equipment at current operating capacity and efficiency levels. Non-maintenance capital expenditures encompass other investments including cash outlays required to increase operating capacity or improve operating efficiency. The following capital expenditures were classified as non-maintenance in the three and nine months ended September 30, 2008:

i. Westfield capacity improvement initiative - in addition to capacity enhancements, the initiative improved the quality and finish of the Westfield product through the implementation of a new paint system. The total expenditure prior to 2008 was $3.6 million. An additional $0.5 million was expended in 2008, including $0.2 million in the third quarter. The project is substantially complete and project costs were consistent with management expectations.

ii. Westfield facility in Winnipeg, Manitoba - to allow for capacity gains at Westfield’s primary facility in Rosenort, Manitoba, the Fund leased space and moved certain production to Winnipeg. In 2008 a total of $0.1 million was expended on manufacturing equipment at this facility. Additional non-maintenance capital expenditures are not anticipated to be material.

iii. Union City, Indiana facility – the facility was acquired to allow for a transfer of certain production from western Canada as well as to provide a more efficient facility for Applegate. Management anticipates expenditures of $3.0 million related to manufacturing equipment, paint line equipment and building enhancements. In 2008 the Fund expended $2.7 million on this project, including $1.3 million in the third quarter.

iv. Building and equipment related to the Twister acquisition - in 2008 the Fund expended $0.3 million related to site preparation and material handling equipment. In 2007 the Fund invested $1.6 million in building renovations and certain equipment not included in the purchase agreement.

v. Expansion of Batco manufacturing facility - to enhance capacity and improve productivity, Batco added approximately 6,000 square feet to its facility at a total projected cost of $0.7 million. Expenditures in 2008 totaled $0.3 million, bringing the project cost to date to $0.6 million. The project is complete and costs were consistent with management expectations.

vi. Acquisition of Hi Roller manufacturing facility - in February 2008 the Fund purchased the facility in Sioux Falls, South Dakota that it had previously leased. The total investment was $3.3 million.

vii. Westfield laser cutter – to allow for capacity gains and increased efficiency, Westfield purchased a second laser cutter for $0.6 million.

15

Cash Balance For the three and nine months ended September 30, 2008 the Fund’s cash balance decreased $nil and $20.4 million (2007 – increase of $3.3 million and decrease of $5.4 million). The variance from 2007 was largely the result of increased working capital requirements. CONTRACTUAL OBLIGATIONS (thousands of dollars) Total 2008 2009 2010 2011 2012 + Long-term debt 42,970 4 17 10,743 32,187 19 Operating leases 3,040 298 1,088 964 577 114

Total obligations 46,010 302 1,105 11,707 32,764 133

Long-term debt at September 30, 2008 includes non-amortizing term loans of $42.9 million (comprised of U.S. dollar debt of $37.6 million and CAD $3.0 million), which for financial reporting purposes are shown net of the related deferred financing costs of $0.3 million. The remaining long-term debt relates to GMAC financed vehicle loans. The operating leases relate primarily to vehicle, equipment, warehousing, and facility leases and were entered into in the normal course of business. DISTRIBUTIONS The Fund declared distributions to public unitholders of $6.1 million and $16.9 million for the three and nine months ended September 30, 2008 (2007 - $4.7 million and $14.0 million) and declared distributions to holders of Class B units of AGHLP of $0.1 million and $0.2 million (2007 - $0.1 million and $0.2 million) for the periods then ended. Total distributions declared to public unitholders have increased due to an increase in the number of outstanding units and an increase in the distribution rate. The Fund’s distribution level increased to $0.17 per unit effective August 2008, a $0.03 increase from $0.14 per unit, the distribution rate for all of 2007 and the first seven months of 2008. The Fund’s policy is to make monthly distributions to holders of both Trust units of the Fund and Class B units of AGHLP. The Fund's Declaration of Trust requires that it distribute all taxable income earned in its fiscal period ending December 31. It may be necessary for the Fund to estimate one or more special distributions to achieve this requirement. The Fund’s Board of Trustees reviews financial performance and other factors when assessing the Fund’s distribution levels. An adjustment to distribution levels may be made at such time as the Board determines an adjustment to be in the long-term best interest of the Fund and its unitholders. STANDARDIZED DISTRIBUTABLE CASH The Canadian Institute of Chartered Accountants (CICA) has issued an interpretive release providing guidance on standardized preparation and disclosure of distributable cash for income trusts. The CICA calculation of standardized distributable cash is based on cash flows from

16

operating activities, including the effects of changes in non-cash working capital, less total capital expenditures. Management believes that the standardized distributable cash calculation distorts the Fund’s distributable cash and payout ratios, as the Fund’s non-cash working capital fluctuates dramatically due to the seasonality of the Fund’s business and cash flow cycle. In addition the standardized distributable cash calculation does not contemplate the timing or source of funding for non-maintenance capital expenditures and as a result may not provide complete information with respect to distributable cash ultimately available for distribution. The table below calculates standardized distributable cash for the three and nine month periods ended September 30, 2008 and 2007. Standardized Distributable Cash (thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Cash provided by (used in) operations $8,213 $13,699 $(7,249) $11,016 Capital expenditures (2,026) (595) ( 9,869) (2,820)

Standardized distributable cash $6,187 $13,104 $(17,118) $8,196 Standardized distributable cash per unit $0.48 $1.17 $(1.32) $0.73 Distributions declared $0.48 $0.42 $1.32 $1.26 Standardized Distributable Cash (thousands of dollars)

12 Months Ended September 30, 2008

12 Months Ended September 30, 2007

Previous Twelve Months Standardized cash generated $5,454 $24,048 Distributions declared $1.74 $1.68 Standardized cash generated per unit $0.42 $2.14 Payout ratio – Standardized 413% 78% The decrease in standardized cash and the corresponding increase in payout ratio are primarily due to an increase in non-maintenance capital expenditures and the working capital movements described under “Cash Flow and Liquidity”. ADJUSTED DISTRIBUTABLE CASH Adjusted distributable cash, as defined under “non-GAAP measures”, is the equivalent of EBITDA less maintenance capital expenditures, cash interest expense, and current cash tax expense plus the non-cash charge related to unit award incentive plan. The objective of presenting this measure is to calculate the amount that is available for distribution to unitholders and exchangeable unitholders. The adjusted distributable cash definition excludes changes in working capital as they are necessary to drive organic growth and are expected to be financed by the

17

Fund’s operating facility (See “Capital Resources”). Adjusted distributable cash should not be construed as an alternative to cash flows from operating, investing, and financing activities as a measure of the Fund’s liquidity and cash flows. Adjusted distributable cash can be reconciled to cash provided by operating activities as follows: (in thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Cash provided by (used in) operating activities

$8,213 $13,699 $(7,249) $11,016

Change in non-cash working capital 5,493 (4,427) 37,284 10,999 Long term incentive plan (150) 0 (700) 0 Reversal of tax reserve 0 0 0 (500) Translation gain (loss) on FX (1,729) 1,788 (2,832) 3,693 Gain on sale of equipment 0 0 0 40 Net maintenance capital expenditures (483) (209) (1,969) (1,158)

Adjusted distributable cash (2) $11,344 $10,851 $24,534 $24,090 Weighted average units outstanding 12,955,000 11,225,000 12,955,000 11,225,000 Distributions declared per unit $0.48 $0.42 $1.32 $1.26 Distributable cash generated per unit (2) $0.88 $0.97 $1.89 $2.15 Payout ratio 55% 43% 70% 59%

(1) See “EBITDA and Net Earnings”. (2) See “non-GAAP Measures”.

The following table reconciles standardized distributable cash to adjusted distributable cash: (in thousands of dollars)

Three Months Ended September 30

Nine Months Ended September 30

2008 2007 2008 2007 Standardized distributable cash $6,187 $13,104 $(17,118) $8,196 Change in non-cash working capital 5,493 (4,427) 37,284 10,999 Reversal of tax reserve 0 0 0 (500) Long term incentive plan (150) 0 (700) 0 Translation gain (loss) on FX (1,729) 1,788 (2,832) 3,693 Gain on sale of equipment 0 0 0 40 Non-maintenance capital expenditures 1,543 386 7,900 1,662

Adjusted distributable cash $11,344 $10,851 $24,534 $24,090

18

The following table displays total adjusted distributable cash generated and total distributions declared since the inception of the Fund:

Adjusted Distributable Cash (in thousands of dollars)

Distributable Cash

Generated

Distributions Declared (1)

Payout Ratio

Period Ended December 31, 2004 $ 9,686 $ 9,109 94.0% Year Ended December 31, 2005 22,629 18,918 83.6% Year Ended December 31, 2006 21,979 18,858 85.8% Year Ended December 31, 2007 27,163 19,585 72.1% Nine Months Ended September 30, 2008 24,534 17,101 69.7%

Cumulative since inception $105,991 $83,571 78.8% (1) Distributions declared include special distributions of $1,328,940 in 2004 and $3,367,500 in 2005. Distributions declared for the three and nine months ended September 30, 2008 were $0.48 per unit and $1.32 per unit respectively (2007 - $0.42 per unit and $1.26 per unit). The distributions declared in the three and nine month periods ended September 30, 2008 represent a 47.7% and a 35.4% increase over the per unit distributions disclosed in the Fund’s 2004 prospectus. Distributions in a fiscal year are funded entirely through cash from operations. Due to seasonality distributions may be funded on a short-term basis by the Fund’s operating lines. The Fund's Declaration of Trust requires distribution of all taxable income earned in its fiscal periods ending December 31. Due to a number of tax deductions available to the Fund and its subsidiary entities, and to the acquisitions of its U.S. divisions, since inception the Fund has retained $22.4 million for internal purposes. The amounts retained have been used primarily to strengthen the Fund’s financial position, to fund certain strategic capital projects, to fund certain acquisition costs, and to allow for future strategic or expansionary capital expenditures. CAPITAL RESOURCES The Fund’s credit facility includes operating lines of CAD $10.0 million and USD $2.0 million, and provides for long-term debt of up to USD $66.5 million. As at September 30, 2008, $5.9 million was drawn under the operating lines compared to a cash balance of $3.3 million at September 30, 2007. The Fund’s outstanding long-term debt is CAD $42.6 million (2007 - $48.9 million), comprised of term loans of USD $37.6 million and CAD $3.0 million. Interest rates on both facilities are based on performance calculations. For the three and nine months ended September 30, 2008, the Fund’s effective interest rate on its U.S dollar term debt was 6.5% and 6.9% respectively (2007 - 8.8% and 8.8%), and after consideration of the effect of the Fund’s interest rate swap was 6.2% and 6.1% (2007 – 6.3% in both periods). For the three and nine months ended September 30, 2007, the Fund’s effective interest rate on its Canadian dollar term debt was 4.9% in both periods. See “Financial Instruments”. Under the terms of the credit facility agreement, the operating and term loan facilities will bear interest at prime plus 0.00%, 0.50%, or 1.00% per annum based on performance calculations. The loans mature August 31, 2009 and are extendible annually for an additional one-year term at the lender’s option. Under the terms of the credit facility agreement, if the bank elects to not extend

19

the operating and term loan facilities beyond the current August 31, 2009 maturity date, all amounts outstanding under the facilities become repayable in four equal quarterly instalments of principal, commencing November 30, 2010. CRITICAL ACCOUNTING ESTIMATES The preparation of financial statements in conformity with Canadian generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amount of revenues and expenses during the period. The Fund believes the accounting policies that are critical to its business relate to the use of estimates regarding the recoverability of accounts receivable and the valuation of inventory, intangibles, goodwill, and future income taxes. Due to the nature of Ag Growth’s business and the credit terms it provides to its customers, estimates and judgments are inherent in the on-going assessment of the recoverability of accounts receivable. In addition, assessments and judgments are inherent in the determination of the net realizable value of inventories and the fair value of goodwill and intangible assets. Goodwill and indefinite life intangible assets are tested for impairment at least annually. Future income taxes are calculated based on assumptions related to the future interpretation of tax legislation, future income tax rates, and future operating results, acquisitions and dispositions of assets and liabilities, and distribution policy. In the normal course of its operations, the Fund may become involved in various legal actions. The Fund maintains, and regularly updates on a case-by-case basis, provisions when the expected loss is both likely and can be reasonably estimated. While management has applied judgment based on assumptions believed to be reasonable in the circumstances, actual results can vary from these assumptions. It is possible that materially different results would be reported using different assumptions. FINANCIAL INSTRUMENTS Risk from foreign exchange arises as a result of variations in exchange rates between the Canadian and the U.S. dollar. The Fund has entered into foreign exchange contracts with a Canadian chartered bank to partially hedge its foreign currency exposure on anticipated U.S. dollar sales transactions and the collection of the related accounts receivable. As at September 30, 2008, the Fund had outstanding the following foreign exchange contracts:

Foreign Exchange Option Contracts Settlement Dates Face Amount

USD (000’s) Call Rate

CND Put Rate

CDN October - December 2008 $3,000 $1.0700 $1.2115 The Canadian dollar exceeded the put rate in October 2008 and, per the terms of the contracts, the November and December options that totalled USD $1.1 million were locked in at a rate of $1.07.

20

Forward Foreign Exchange Contracts

Settlement Dates Face Amount USD (000’s)

Average Rate CDN

CAD Amount (000’s)

October - December 2008 $16,000 1.0268 $16,429 July – December 2009 $36,000 1.0387 $37,393 At September 30, 2008, the fair value of the foreign exchange contracts was a loss of $1,381,318. Subsequent to September 30, 2008 the Fund entered additional forward foreign exchange contracts with settlement dates as follows:

Forward Foreign Exchange Contracts Settlement Dates Face Amount

USD (000’s) Average Rate

CDN CAD Amount

(000’s) January - June 2009 $19,000 1.0893 $20,697 April – September 2010 $30,000 1.1741 $35,223 The Fund is subject to risks associated with fluctuating interest rates on its long-term debt. To manage this risk, as at September 30, 2008 the Fund had outstanding the following interest rate swap transactions with a Canadian chartered bank:

(i) Notional amount of USD $17.5 million, expires August 29, 2009, effective interest rate of 3.88%, resulting in interest charges to the Fund of 3.88% plus a variable rate based on performance calculations.

(ii) Notional amount of USD $2.5 million, expires August 29, 2009, effective interest rate of 3.88%, resulting in interest charges to the Fund of 3.88% plus a variable rate based on performance calculations.

(iii) Notional amount of USD $6.5 million, expires August 29, 2009, effective interest rate of 3.88%, resulting in interest charges to the Fund of 3.88% plus a variable rate based on performance calculations.

At September 30, 2008, the fair value of the interest rate swap contracts was a gain of $131,241. OUTLOOK Strong sales of portable grain handling and aeration equipment, which account for approximately two-thirds of the Fund’s total sales, have resulted in low inventory levels throughout the Fund’s distribution network. In addition, demand in the Fund’s segment of the agricultural space remains strong due to an increase in on-farm storage and successive large corn harvests. As a result, fourth quarter demand for portable grain handling and aeration equipment is expected to significantly exceed historical levels. Management anticipates that strong demand for portable grain handling and aeration equipment will continue into 2009. Consistent with prior years, demand in 2009, particularly in the second half, will be influenced by crop conditions. Demand for Hi Roller and Union Iron stationary grain handling equipment has historically been seasonally weighted towards the second and third quarters. Sales at Hi Roller remain strong but it is not expected that the fourth quarter of 2008 will match the prior year as the fourth quarter of

21

2007 was positively impacted by high levels of activity in the ethanol industry. Although demand in 2009 is contingent on a number of factors, including credit availability, management currently anticipates similar levels of activity compared to 2008. Demand for Twister storage products currently exceeds production capacity. Strong demand has resulted from positive market conditions in western Canada and the rapid development of overseas markets. As a result, Twister’s sales in the fourth quarter of 2008 and into 2009 are expected to exceed historical levels. The Fund anticipates gross margins on portable grain handling and aeration equipment will strengthen in the fourth quarter of 2008 and into 2009 as the impact of previously announced price increases, the benefit of which has been limited in the first nine months of 2008, more significantly impacts financial results. Gross margins on stationary grain handling equipment are expected to remain stable or slightly decrease as activity in this segment of the agricultural space returns to more historical levels. Gross margin on Twister product is expected to remain low over the next several quarters as management initiatives to improve manufacturing efficiency are not expected to significantly impact until the second half of 2009. In addition, the benefit of price increases at Twister in the short term will be largely offset by the impact of higher steel costs as Twister has large amounts of higher priced steel in inventory or on order. The inclusion of Twister, Union Iron and Applegate, which are inherently lower margin businesses, will reduce the consolidated gross margin percentage as compared to 2007. Gross margin percentages at all divisions are impacted by the price of steel and the rate of foreign exchange. Any softening in the price of steel will benefit gross margins, however there will be lag effect as the Fund works though higher priced steel existing in its inventory. This lag effect will be most pronounced at Twister. Any weakening of the Canadian dollar will result in improved gross margin percentages at all divisions compared to the prior year. The value of the Canadian dollar relative to its U.S. counterpart will continue to impact the financial results of the Fund. Any weakening of the Canadian dollar positively impacts sales and gross margin percentages compared to prior periods. In the fourth quarter of 2007, the Fund’s average rate of exchange was $0.99, and in the quarters ended March 31, 2008, June 30, 2008 and September 30, 2008 was $0.99, $1.01 and $1.03 respectively. The Canadian dollar weakened subsequent to September 30, 2008, and unless the rate of exchange returns to levels experienced in the first three quarters of 2008 the Fund expects a positive impact on sales and gross margins in the fourth quarter of 2008 and into 2009. The rate of foreign exchange impacts the gain or loss the Fund may realize on its foreign exchange hedging contracts. In addition, fluctuations in the rate of foreign exchange result in an accounting gain or loss when the Fund translates its U.S. dollar denominated debt into Canadian dollars at each balance sheet date. A weakening of the Canadian dollar, as has been experienced recently, may result in losses on the Fund’s foreign exchange contracts and on the translation of its U.S. dollar denominated debt. Unless the Canadian dollar appreciates significantly, the Fund expects to record a large unrealized loss on the translation of its U.S. dollar debt into Canadian dollars as at December 31, 2008. Management does not currently anticipate that recent developments in the credit markets will have a material adverse effect on the Fund. It is currently anticipated that the North American farmer will have sufficient access to capital to operate throughout this credit market. Management does expect that access to credit may negatively impact sales to commercial grain handling

22

facilities and to certain international markets. Management’s assessment is based on current conditions and may be subject to change if the credit environment deteriorates further. Overall, management expects strong demand for portable grain handling and aeration equipment to continue well into 2009. Strong demand coupled with increased capacity at Westfield and sales price increases at all divisions should allow the Fund to increase sales of portable grain handling and aeration equipment compared to prior periods. Gross margin on these products, which account for approximately two-thirds of the Fund’s total sales, are expected to increase due to previously announced sales price increases, moderating input costs and a weaker Canadian dollar. Demand for stationary grain handling equipment appears to be moderating slightly, however the financial impact on the consolidated results of the Fund is not expected to be significant. Demand for Twister product remains very strong, particularly internationally, and it is expected that margin improvements will be realized in the second half of 2009 due to improved efficiencies, sales price increases and decreasing input costs. LEGISLATION IMPOSING TAXATION ON INCOME TRUSTS In June 2007, the Government of Canada enacted legislation imposing additional income taxes upon publicly traded income trusts, including the Fund, effective January 1, 2011. Prior to June 2007, the Fund estimated the future income tax on certain temporary differences between amounts recorded on its balance sheet for book and tax purposes at a $nil effective tax rate. Upon enactment of the June 2007 legislation, the Fund estimated the effective tax rate to be 31.5% and as a result future income tax liabilities for the period increased by $11.1 million. On December 14, 2007, further legislation was enacted by the federal government to reduce the effective rate of tax on the Fund’s temporary differences from the previous rate of 31.5% to 29.5% in 2011 and 28.0% thereafter. As a result the Fund reduced its expected future income tax liability related to the legislation from $11.1 million to $9.5 million. Temporary differences reversing before 2011 will still give rise to $nil future income taxes. The amount and timing of reversals of temporary differences will depend on the Fund’s future operating results, acquisitions and dispositions of assets and liabilities, and distribution policy. A significant change in any of the preceding assumptions could materially affect the Fund’s estimate of the future tax liability.

Based on its assets and liabilities as at September 30, 2008, the Fund has estimated the amount of its temporary differences and the periods in which these differences will reverse. The Fund estimates that approximately $33.8 million net taxable temporary differences will reverse after January 1, 2011, resulting in a $10.6 million future income tax liability. The taxable temporary differences relate principally to the Fund’s intangible assets. Until 2011, the new legislation does not directly affect the Fund’s cash flow from operations. However, as enacted in its present form, the legislation will, all other things being equal, result in a reduction of cash available for distribution commencing in 2011. On July 14, 2008, the Department of Finance published proposed amendments to the Income Tax Act which are intended to facilitate the conversion of publicly traded income trusts, including the Fund, into corporate form on a tax deferred basis. The proposed amendments address many of the principal substantive and administrative issues that currently arise when structuring such a conversion. The Fund is considering these legislative changes and their possible impact on the Fund.

23

ACCOUNTING POLICY CHANGES Capital Disclosures and Financial Instruments – Presentation and Disclosure Effective January 1, 2008 the Fund has adopted the following accounting standards: The CICA issued three new accounting standards: section 1535, Capital Disclosures, section 3862, Financial Instruments – Disclosures, and section 3863, Financial Instruments – Presentation. These new standards were adopted on January 1, 2008. The required disclosure has been included in the notes to the unaudited financial statements. Section 1535 establishes disclosure requirements about an entity’s capital and how it is managed. The purpose is to enable users of the financial statements to evaluate the entity’s objectives, policies and processes for managing capital. Sections 3862 and 3863 replaced section 3861, Financial Instruments – Disclosure and Presentation, revising and enhancing its disclosure requirements, and carrying forward unchanged its presentation requirements. These new sections place increased emphasis on disclosures about the nature and extent of risks arising from financial instruments and how the entity manages those risks. Inventories The CICA issued section 3031, Inventories, which replaced section 3030, Inventories. This new standard was adopted on January 1, 2008. Section 3031 provides more extensive guidance on measurement, and expands disclosure requirements to increase transparency. The adoption of this standard has had no material impact on the Fund’s financial position or results of operations. NEW ACCOUNTING STANDARDS Goodwill and Intangible Assets As at January 1, 2009, the Fund will be required to adopt the CICA Handbook Section 3064, “Goodwill and Intangible Assets”, which will replace the existing Goodwill and Intangible Assets standard. The new standard revises the requirement for recognition, measurement, presentation and disclosure of intangible assets. The Fund is in the process of evaluating the impact of this new standard. International Financial Reporting Standards ("IFRS") On February 13, 2008, the AcSB confirmed that the use of IFRS will be required by January 1, 2011, with appropriate comparative data from the prior year. Under IFRS, the primary audience is capital markets and as a result, there is significantly more disclosure required, specifically for quarterly reporting. Further, while IFRS uses a conceptual framework similar to Canadian GAAP, there are significant differences in accounting policy that must be addressed.

24

The Fund is currently preparing its IFRS conversion plan and has initiated an assessment of the impact that the conversion may have on financial reporting, business processes, internal controls and information systems. The plan will be aimed in particular at identifying the differences between IFRS and the Fund’s current accounting policies, as well as assessing the impact of various accounting alternatives offered pursuant to IFRS. The financial impact of the transition to IFRS cannot be reasonably estimated at this time. DISCLOSURE CONTROLS AND PROCEDURES AND INTERNAL CONTROLS Disclosure controls and procedures are designed to provide reasonable assurance that all relevant information is gathered and reported to senior management, including the Fund’s Chief Executive Officer and Chief Financial Officer, on a timely basis so that appropriate decisions can be made regarding public disclosure. Management of the Fund is responsible for designing internal controls over financial reporting for the Fund as defined under Multilateral Instrument 52-109 issued by the Canadian Securities Administrators. Management has designed such internal controls over financial reporting, or caused them to be designed under their supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of the financial statements for external purposes in accordance with GAAP. On November 19, 2007 the Fund acquired Union Iron, Inc., and on January 15, 2008 the Fund acquired Applegate Steel Inc. Management has not fully completed its review of internal controls over financial reporting for the newly acquired operations. Management expects to have finalized the design and implementation of internal controls prior to completion of the current fiscal year. For the period covered by this MD&A, management has undertaken specific procedures to satisfy itself with respect to the accuracy and completeness of the acquired operation’s financial information. Management believes that Ag Growth’s existing internal controls over financial reporting, including Union Iron and Applegate, provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with GAAP. There have been no changes in the Fund’s internal controls over financial reporting that occurred in the three month period ended September 30, 2008, that have materially affected, or are reasonably likely to materially affect, the Fund’s internal controls over financial reporting. NON-GAAP MEASURES References to “EBITDA” are to earnings before interest, income taxes, depreciation, and amortization. Management believes that, in addition to net income or loss, EBITDA is a useful supplemental measure in evaluating the Fund’s performance. EBITDA is not a financial measure recognized by GAAP and does not have a standardized meaning prescribed by GAAP. Management cautions investors that EBITDA should not replace net income or loss as an indicator of performance, or cash flows from operating, investing, and financing activities as a measure of the Fund’s liquidity and cash flows. The Fund’s method of calculating EBITDA may differ from the methods used by other issuers. References to “gross margin” are to sales less cost of goods sold. Management believes that, in addition to net income or loss, gross margin provides a useful supplemental measure in evaluating

25

its performance. Gross margin is not a financial measure recognized by Canadian generally accepted accounting principles (“GAAP”) and does not have a standardized meaning prescribed by GAAP. Management cautions investors that gross margin should not replace net income or loss as an indicator of performance, or cash flows from operating, investing, and financing activities as a measure of the Fund’s liquidity and cash flows. The Fund’s method of calculating gross margin may differ from the methods used by other issuers. Standardized and adjusted distributable cash are non-GAAP measures generally used by Canadian income funds as an indicator of financial performance. The Fund defines standardized distributable cash as cash flow from operating activities less capital expenditures. The Fund defines adjusted distributable cash as cash flow from operating activities before the net change in non-cash working capital balances and before items not affecting cash other than items that impact amortization, interest expense, future taxes, or tax reserves, less maintenance capital expenditures (see “Capital Expenditures”). Standardized and adjusted distributable cash are not financial measures recognized by GAAP and do not have a standardized meaning prescribed by GAAP. The method of calculating the Fund’s standardized and adjusted distributable cash may differ from similar computations as reported by similar entities and, accordingly, may not be comparable to distributable cash as reported by such entities. Payout ratio is a non-GAAP measure used by Canadian income funds as an indicator of the amount of generated distributable cash that is distributed to the unitholders. The Fund defines payout ratio as total distributions expressed as a percentage of standardized and adjusted distributable cash. Payout ratio is not a financial measure recognized by GAAP and does not have a standardized meaning prescribed by GAAP. The method of calculating the Fund’s payout ratio may differ from similar computations as reported by similar entities and, accordingly, may not be comparable to payout ratio as reported by such entities. RISKS AND UNCERTAINTIES The risks and uncertainties described below are not the only risks and uncertainties we face. We believe that the risks mentioned are the principal risks relating to our operations. The Fund’s Annual Information Form contains a description of these and other risks that relate to the structure of the Fund. Additional risks and uncertainties not currently known to us or that we currently deem immaterial also may impair operations. If any of the following risks actually occur, our business, results of operations and financial condition, and the amount of cash available for distribution could suffer. Industry Cyclicality The performance of the agricultural industry is cyclical, and to the extent that the agricultural sector declines or experiences a downturn, this is likely to have a negative impact on the farm equipment and commercial grain handling industry, and the business of Ag Growth. The agricultural sector has recently been positively impacted by the expansion of the ethanol industry, and to the extent the ethanol industry declines or experiences a downturn, this is likely to have a negative impact on the farm equipment and commercial grain handling industry, and the business of Ag Growth. Seasonality of Business The seasonality of the demand for Ag Growth’s products results in lower cash flow in the first three quarters of each calendar year and may impact the ability of the Fund to make cash distributions to Unitholders, or the quantum of such distributions, if any. No assurance can be

26

given that the Fund’s credit facility will be sufficient to offset the seasonal variations in Ag Growth’s cash flow. Risk of Decreased Crop Yields Decreased crop yields due to poor weather conditions and other factors are a significant risk affecting Ag Growth. Both reduced crop volumes and the accompanying decline in farm incomes can negatively affect demand for grain handling equipment. Potential Volatility of Production Costs Various materials and components are purchased in connection with Ag Growth’s manufacturing process, some or all of which may be subject to wide price variation. Consistent with past and current practices within the industry, Ag Growth manages its exposure to material and component price volatility by planning and negotiating significant purchases on an annual basis, and passing through to customers, most, if not all, of the price volatility. There can be no assurance that industry dynamics will allow Ag Growth to continue to reduce its exposure to volatility of production costs by passing through price increases to its customers. Commodity Prices, International Trade and Political Uncertainty Prices of commodities are influenced by a variety of unpredictable factors that are beyond the control of Ag Growth, including weather, government (Canadian, United States and other) farm programs and policies, and changes in global demand or other economic factors. The world grain market is subject to numerous risks and uncertainties, including risks and uncertainties related to international trade and global political conditions.