to learn more, visit myafmbenefits - my...

TRANSCRIPT

To Learn More, visit MyAFMBenefits.com

To Learn More, visit MyAFMBenefits.com 2

Introduction ..................................................................... 3

Enrollment Process ........................................................... 4 Open Enrollment Instructions .......................................... 5

Changes for the Year ........................................................ 6 MyAFMBenefits.com ......................................................... 7

Medical Plan .................................................................... 8-10 HelpCard .......................................................................... 11-13

Dental Plan ....................................................................... 14 Vision Plan ....................................................................... 15

Supplemental Plans .......................................................... 16

Accident Plan .................................................................... 17 Critical Illness Plan .......................................................... 18

Term Life, Optional Life, Dependent Life Plans ................. 19-20 Disability Coverage Plans ................................................. 21

Legal Notices .................................................................... 22-25 Affordable Care Act Update .............................................. 26

Important Phone Numbers ............................................... 27 Rates ............................................................................... 28-31

Every reasonable effort has been made for the information provided in this booklet to be accurate. It is intended to

provide the employees with Arnold’s Fabricating & Machine an overview of the coverages offered. It is in no way a

guarantee or offer of coverage. Each carrier has the ability to underwrite based on its contract with Arnold’s

Fabricating & Machine or its employees. Each carrier’s contract, underwriting, and policies will supersede this

document. Please be aware that each carrier may have exclusions or limitations and you must consult your summary

plan description and/or policies for details.

Look for the Different Colors at the top of each page to Designate the Section you are Viewing

TA

BLE O

F C

ON

TEN

TS

To Learn More, visit MyAFMBenefits.com 3

Your Arnold’s Fabricating & Machine Benefits Package

Arnold’s Fabricating & Machine takes pride in providing our employees with a competitive, affordable benefit package. Employees enjoy favorable purchasing power due to negotiated discounts as well as a company contribution towards your healthcare coverage. In addition, our Cafeteria Plan allows our employees to pay for certain benefit plans with pre-tax dollars.

All of our benefit programs are designed to work cohesively to protect you and your family from catastrophic losses. Keeping our annual healthcare increases year-over-year to a minimum takes a joint effort. We depend on our employees to become educated healthcare consumers and to spend your health care dollars wisely. Visit your primary care physician annually and take advantage of the ‘no cost to you’ preventive screenings included in all of our medical plan option. When medical tests or surgical procedures are recommended, use Blue Cross Blue Shield of Tennessee’s on-line quality and cost comparison tools. This will reduce your out-of-pocket expenses and help manage the cost to the plan.

Full-time benefit eligible employees have an annual opportunity to review your benefit option selections and make any changes in your plan selections. During this annual open enrollment period you can have a one-on-one meeting with an Enrollment Counselor to discuss your personal benefit needs for the upcoming new plan year (8/1/15-7/31/16). If you’re confused about putting together a benefit package, this personalized meeting can be a valuable resource for you. You will need to complete your enrollment in the system on your own or with a benefit counselor for 2015-2016 plan elections.

Your Benefit Options…

• Medical Plan - Covers you and your family for routine, wellness & catastrophic care.

• HRA– Employer Reimbursement of Deductible Charges

• HelpCard - Access to doctors by phone 24 hours a day, 7 days a week

• Dental Plan - Plan covers routine annual cleanings & x-rays at no cost to you.

• Vision Plan - Save money on eye examinations & materials

• Critical Illness Plan - Coverage for Heart Attack, Stroke, Cancer and more.

• Accident Plan - Coverage for Hospital bills, Emergency room and more!

• Term Life Insurance - For you & your dependents

• Disability Coverage - To protect your paycheck.

When Does My Coverage Begin as a Full Time Employee?

All Employees—1st of the month following 60 days of employment

To Learn More, visit MyAFMBenefits.com 4

ADDING DEPENDENTS If you are adding dependents to the medical, dental or vision plans for the first time during this open

enrollment you must present the following verification documentation to your Human Resources Department

immediately following your enrollment. If proper documentation is not provided by your effective date of

coverage under the plan, these newly added dependents will not be enrolled for coverage during the new

plan year unless you experience a change in family status or other specific change event.

Dependent Required Documentation

Spouse Marriage License & first page of your most recent joint tax return. (financials should be blackened out)

Natural Children Birth Certificate

Step-Children Birth Certificate and Marriage License showing both parent’s names

Dependent Child(ren): Legal guardian, adoption or foster

Birth Certificate, Final Court Order of legal guardian-ship with judge’s signature and/or final adoption de-

cree with judge’s signature

ENROLLMENT PROCESS

ENROLLMENT SESSIONS

Why is it important to meet with an enrollment counselor during open enrollment?

• To review and verify your current and upcoming elections and payroll deductions.

Has your life changed in the last year? How has it changed? It is important to

take a look at your selections and adjust them accordingly to fit your needs and

that of your family.

• To see how much Arnold’s Fabricating and Machine is contributing to your

benefits package. Arnold’s values you as an employee and invests many dollars

towards your benefits. Benefits are a substantial part of your overall

compensation package.

• To update your beneficiaries. While beneficiary changes can be made outside of

open enrollment, open enrollment is a good time to reflect on changes that you

may have had throughout the year and determine if you need to make a change.

• Confirm that your contact information is correct and up-to-date.

• Enrollment Counselors can help provide you with a better understanding of your

benefits and options.

To Learn More, visit MyAFMBenefits.com 5

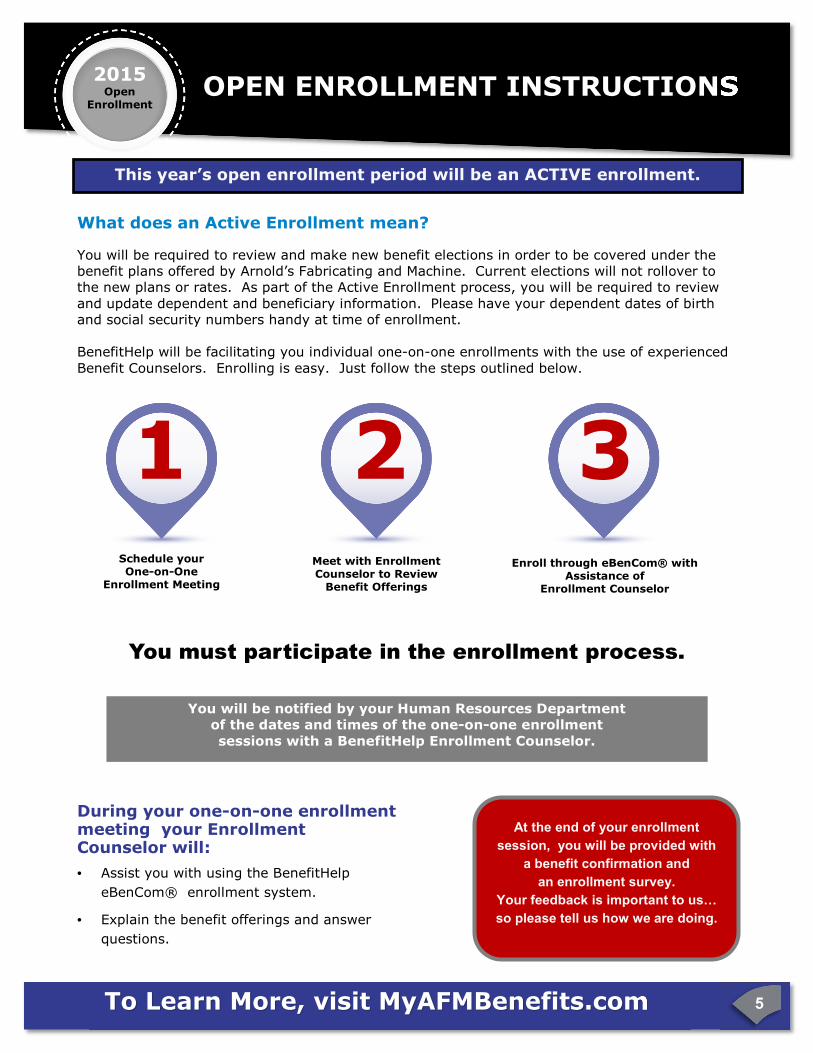

What does an Active Enrollment mean?

You will be required to review and make new benefit elections in order to be covered under the benefit plans offered by Arnold’s Fabricating and Machine. Current elections will not rollover to the new plans or rates. As part of the Active Enrollment process, you will be required to review

and update dependent and beneficiary information. Please have your dependent dates of birth and social security numbers handy at time of enrollment. BenefitHelp will be facilitating you individual one-on-one enrollments with the use of experienced

Benefit Counselors. Enrolling is easy. Just follow the steps outlined below.

During your one-on-one enrollment meeting your Enrollment Counselor will:

• Assist you with using the BenefitHelp

eBenCom® enrollment system.

• Explain the benefit offerings and answer

questions.

You must participate in the enrollment process.

Schedule your One-on-One

Enrollment Meeting

1 Meet with Enrollment Counselor to Review

Benefit Offerings

2 Enroll through eBenCom® with

Assistance of Enrollment Counselor

3

At the end of your enrollment

session, you will be provided with

a benefit confirmation and

an enrollment survey.

Your feedback is important to us� so please tell us how we are doing.

OPEN ENROLLMENT INSTRUCTIONS 2015

Open Enrollment

This year’s open enrollment period will be an ACTIVE enrollment.

You will be notified by your Human Resources Department of the dates and times of the one-on-one enrollment

sessions with a BenefitHelp Enrollment Counselor.

To Learn More, visit MyAFMBenefits.com 6

CHANGES FOR THE YEAR

Benefit Plan Changes Effective August 1, 2015

Your medical coverage will remain with BCBS of Tennessee however, you will

experience an increase in the deductible and maximum out-of-pocket

effective August 1, 2015. You will also be required to contribute toward the

cost of coverage. You must either select or waive coverage during this

open enrollment. Your HRA will remain the same amount.

All employees enrolled in medical will receive the HelpCard at no additional

cost. The HelpCard provides you with access to a physician 24 hours/day

by phone or internet, without any out-of-pocket cost.

Need Help with Enrollment? Contact BenefitHelp at 888-663-1285 option #2

or email [email protected] for assistance.

1

2

3

4 Allstate Benefits will replacing AFLAC as the supplemental coverage

provider. Allstate Benefits was selected for their enhanced benefits and

competitive pricing. You may purchase Accident, Critical Illness (with or

without cancer coverage) and Short Term Disability coverage with NO un-

derwriting questions. AFLAC premiums will no longer be payroll deducted

as of August 1, 2015.

Vision coverage through BCBS of Tennessee is being added to your benefit

package. This company provided benefit allows you access to examinations

and materials at a fixed co-payment. You may purchase coverage for your

family members for a nominal cost.

5 You now have the option to purchase additional term life insurance

coverage for yourself and your family members. Coverage will be offered

by BCBS of Tennessee.

To Learn More, visit MyAFMBenefits.com 7

Have you ever had trouble locating information about your benefits?

What about trying to remember how

to find a participating doctor or dentist?

Problem Solved!

It’s All Online...

One place to go, just an internet

connection away.

Watch Videos About

Your Benefits.

Get Important

Phone Numbers &

Carrier

Information.

Search for a

Doctor or Dentist.

Print Important

Documents &

Forms.

MyAFMBenefits.com

To Learn More, visit MyAFMBenefits.com 8

It’s up to you to take advantage of everything your health plan offers. You will have the lowest out-of-pocket expense when you use doctors and facilities that participate in the Blue Cross Blue

Shield of Tennessee provider network. It is your responsibility to determine if the provider is in network.

Terms and Definitions Deductible This is the amount of money you pay for health services before your medical Insurance begins paying. For some services you have to pay the deductible before the plan pays. Your deductible starts over each January 1st.

Copay This is the amount of money that you pay each time a particular service is utilized.

Coinsurance This is the rate that you will essentially be splitting the cost of your healthcare with your insurance provider. For instance, if your health plan has an 80/20 coinsurance rate, your insurance plan pays for 80% of your eligible medical expenses and you’re responsible for the remaining 20%.

Out-of-pocket Coinsurance Maximum This is the most you will have to pay under your medical plan each year. Includes deductible & coinsurance. This protects you from the financial drain of high medical expenses. Copays do count towards your out-of-pocket maximum and still apply after you meet your maximum.

In-Network / Out-of-Network If your medical plan has “in and out” coverage, this means you can see any provider you wish. However, if you choose to see a provider that is not on the approved in-network list, you will pay a greater share of the

cost. Determining whether or not a provider is in-network is your responsibility. Please check with the pro-vider to see if he or she is in the network. before services are rendered, preferably when making the appointment.

To locate a provider or to review the policy

details, please visit: www.MyAFMBenefits.com

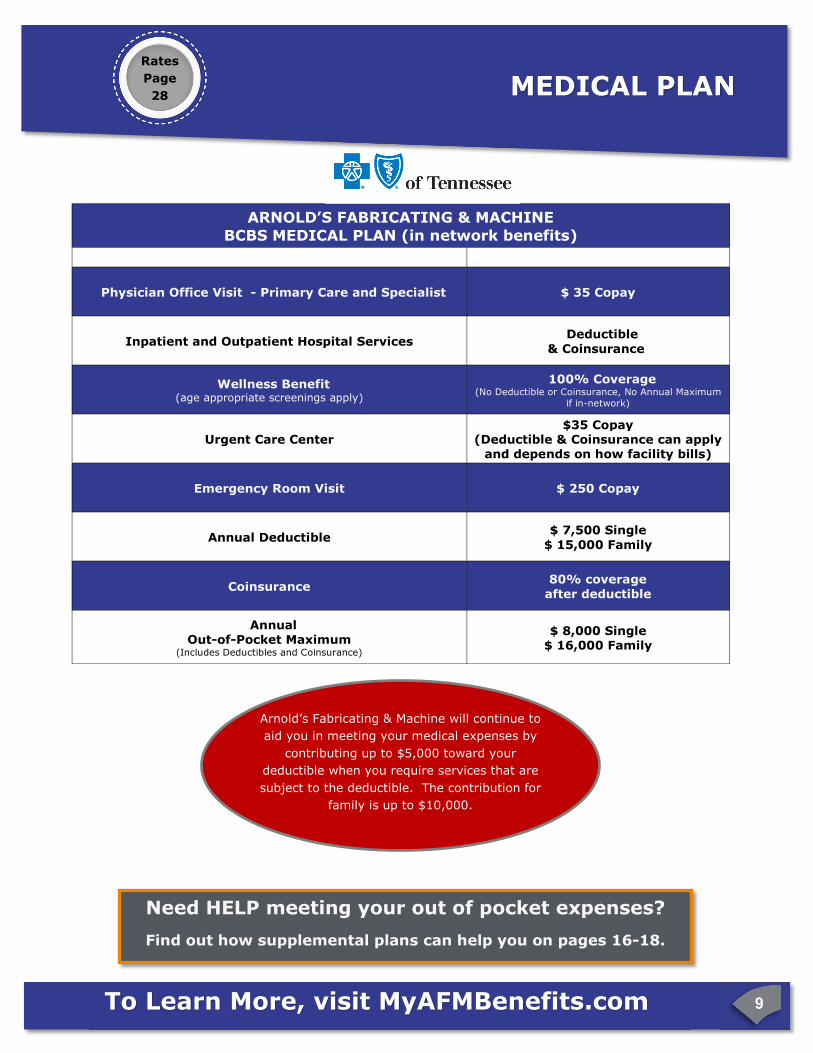

MEDICAL OVERVIEW

To Learn More, visit MyAFMBenefits.com 9

ARNOLD’S FABRICATING & MACHINE

BCBS MEDICAL PLAN (in network benefits)

Physician Office Visit - Primary Care and Specialist $ 35 Copay

Inpatient and Outpatient Hospital Services Deductible

& Coinsurance

Wellness Benefit (age appropriate screenings apply)

100% Coverage (No Deductible or Coinsurance, No Annual Maximum

if in-network)

Urgent Care Center $35 Copay

(Deductible & Coinsurance can apply and depends on how facility bills)

Emergency Room Visit $ 250 Copay

Annual Deductible $ 7,500 Single

$ 15,000 Family

Coinsurance 80% coverage

after deductible

Annual Out-of-Pocket Maximum

(Includes Deductibles and Coinsurance)

$ 8,000 Single $ 16,000 Family

MEDICAL PLAN Rates

Page

28

Need HELP meeting your out of pocket expenses?

Find out how supplemental plans can help you on pages 16-18.

Arnold’s Fabricating & Machine will continue to

aid you in meeting your medical expenses by

contributing up to $5,000 toward your

deductible when you require services that are

subject to the deductible. The contribution for

family is up to $10,000.

To Learn More, visit MyAFMBenefits.com 10

Drugs on the Blue Cross Blue Shield Drug List/Formulary are grouped by ‘tiers.’ A number of factors are considered when classifying drugs into tiers, including, but not limited to: the absolute

cost of the drug; the cost of the drug relative to other drugs in the same therapeutic class; the availability of over-the-counter alternatives; and other clinical and cost-effectiveness factors.

To View the BCBS Drug List, visit www.MyAFMBenefits.com

RETAIL PHARMACY

31 Day Supply

Copay Plan

Generic $ 10

Preferred $ 35

Non-Preferred

$ 50

MAIL ORDER

PHARMACY

90 Day Supply

Copay Plan

Generic $ 30

Preferred $105

Non-Preferred

$150

PRESCRIPTION DRUG COVERAGE

To Learn More, visit MyAFMBenefits.com 11

MYHELPCARD

HIGHLIGHTS

• 24/7/365 access to a doctor online or by phone at

NO cost to you!

• Fast treatment—Teladoc doctors respond within 24 minutes,

on average

• Talk to a Teladoc doctor from anywhere: at home, work,

or while traveling

• Save money by avoiding expensive urgent care or ER visits

• Teladoc treats conditions like:

DISCLAIMERS: ©Teladoc, Inc. All rights reserved. Teladoc and the Teladoc logo are registered trademarks of Teladoc, Inc. and may not

be used without written permission. Teladoc does not replace the primary care physician. Teladoc does not guarantee that a prescription

will be written. Teladoc operates subject to state regulations and may not be available in certain states. Teladoc does not prescribe DEA

controlled substances, non-therapeutic drugs and certain other drugs which may be harmful because of their potential for abuse. Teladoc

physicians reserve the right to deny care for potential misuse of services. Teladoc phone consultations are available 24 hours, 7 days a

week while video consultations are available during the hours of 7am to 9pm, 7 days a week.

As an added benefit, Arnold’s Fabricating & Machine is providing

the HelpCard to all employees who enroll in the medical plan.

This benefit will provide you with some assistance with the cost

of receiving healthcare and is available at no cost to you. A

description of services follows.

• Cold and flu

• Bronchitis

• Respiratory infection

• Sinus problems

• Vomiting

• Diarrhea

• Allergies

• Urinary Tract Infection

• Poison Ivy

• Pink eye

HELPCARD

To Learn More, visit MyAFMBenefits.com 12

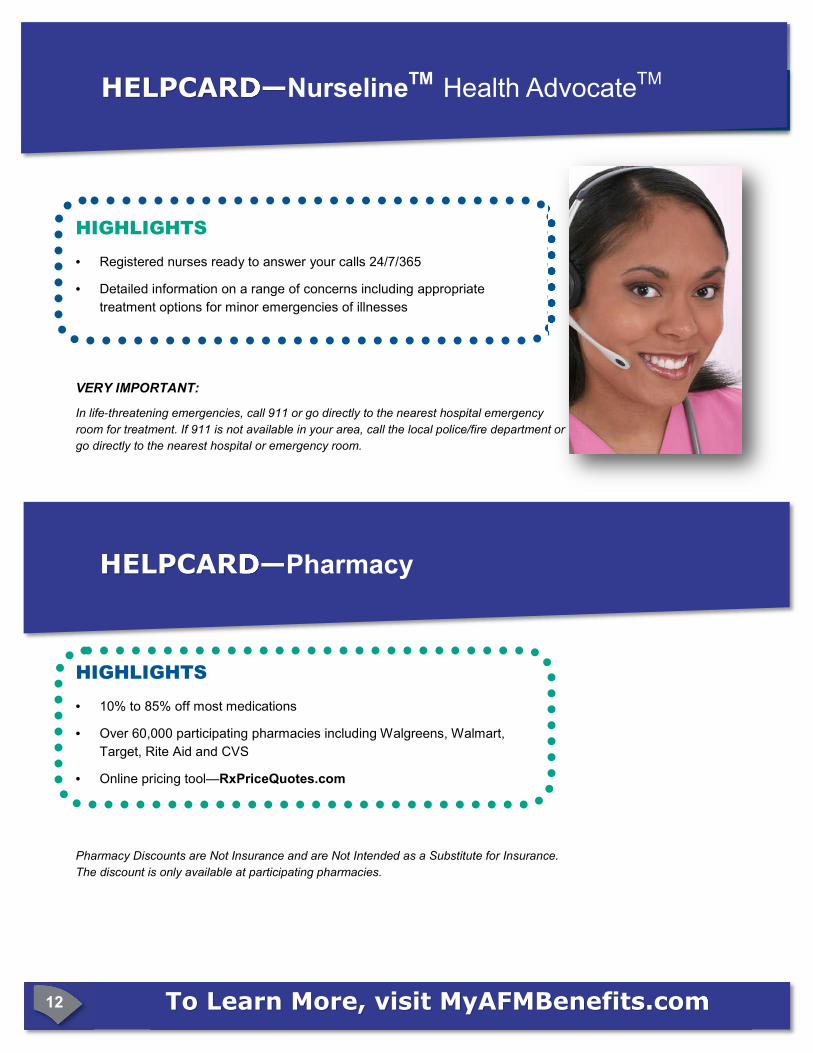

HIGHLIGHTS

• 10% to 85% off most medications

• Over 60,000 participating pharmacies including Walgreens, Walmart, Target, Rite Aid and CVS

• Online pricing tool—RxPriceQuotes.com

Pharmacy Discounts are Not Insurance and are Not Intended as a Substitute for Insurance. The discount is only available at participating pharmacies.

HIGHLIGHTS

• Registered nurses ready to answer your calls 24/7/365

• Detailed information on a range of concerns including appropriate treatment options for minor emergencies of illnesses

MYHELPCARD

VERY IMPORTANT:

In life-threatening emergencies, call 911 or go directly to the nearest hospital emergency

room for treatment. If 911 is not available in your area, call the local police/fire department or

go directly to the nearest hospital or emergency room.

HELPCARD—NurselineTM Health Advocate

TM

HELPCARD—Pharmacy

To Learn More, visit MyAFMBenefits.com 13

MYHELPCARD

HIGHLIGHTS

• Negotiation can result in 25% to 50% savings.

• Easy-to-read, personal Savings Result Statement, summarizing outcome and payment terms.

• Provider sign-off on payment terms and conditions.

Health Advocate does not replace health insurance coverage, provide medical care or

recommend treatment.

HIGHLIGHTS

Call Medical Health Advisor to:

• Find your way through the healthcare and insur-

ance systems

• Find doctors, hospitals and other providers

• Make appointments with providers

• Find “best in class” medical institutions for a

serious illness or injury

• Get unbiased health information to make

informed medical decisions

• Find and research current treatment options for a

medical issue

• Use our Health Cost Estimator—a pre-service

pricing decision support tool

• Resolve insurance claims and billing issues

• Explain test, treatment and medications

• Get second opinions for peace of mind

• Address eldercare and related healthcare issues

• Get help with Medicare and other government insurance programs

• Make arrangements for in-home services after

discharge from a hospital

HELPCARD—Medical Bill SaverTM

HELPCARD— Medical Health Advisor

Health AdvocateTM

To Learn More, visit MyAFMBenefits.com 14

Arnold’s Fabricating offers dental protection through

Blue Cross Blue Shield of Tennessee.

With BCBS you can receive care from any dentist. However, BCBS has contracts with a large network of dentists who have agreed not to charge more than a specified amount for

particular services. If you use one of these network dentists, you won’t have to worry about being charged for additional amounts above the allowable amount covered by the plan.

Coverage A

Oral exams, X-Ray, Cleanings, Brush Biopsy, Topical fluoride,

Space maintainers, Sealants 100% Coverage

Coverage B

Basic Restorative Services (fillings, emergency treatment for the relief of

pain) Basic and Major Endodontics (pulpotomy, pulpal therapy, root canal

treatment), Basic and Major Periodontics ( non-surgical periodontics,

periodontal scaling and root planning, full mouth debridement, gingivectomy,

gingivoplaty, osseous surgery and bone and tissue grafting) and Basic and

Major Oral Surgery (non-surgical or simple extractions, surgical extractions

including removal of impacted teeth and wisdom teeth)

80% Coverage

Coverage C

Major Restorative (single tooth restorations, including crowns, inlays and

onlays and veneers), Implants and Prosthodontics (fixed bridges, removal

dentures, crown and bridge services including core buildups, post and core,

re-cementation and repair).

50% Coverage

Plan Deductible and Maximums

Deductible ( Up to 3 per family) $50

Benefit Maximum $1,500

DENTAL PLAN Rates

Page

28

To Learn More, visit MyAFMBenefits.com 15

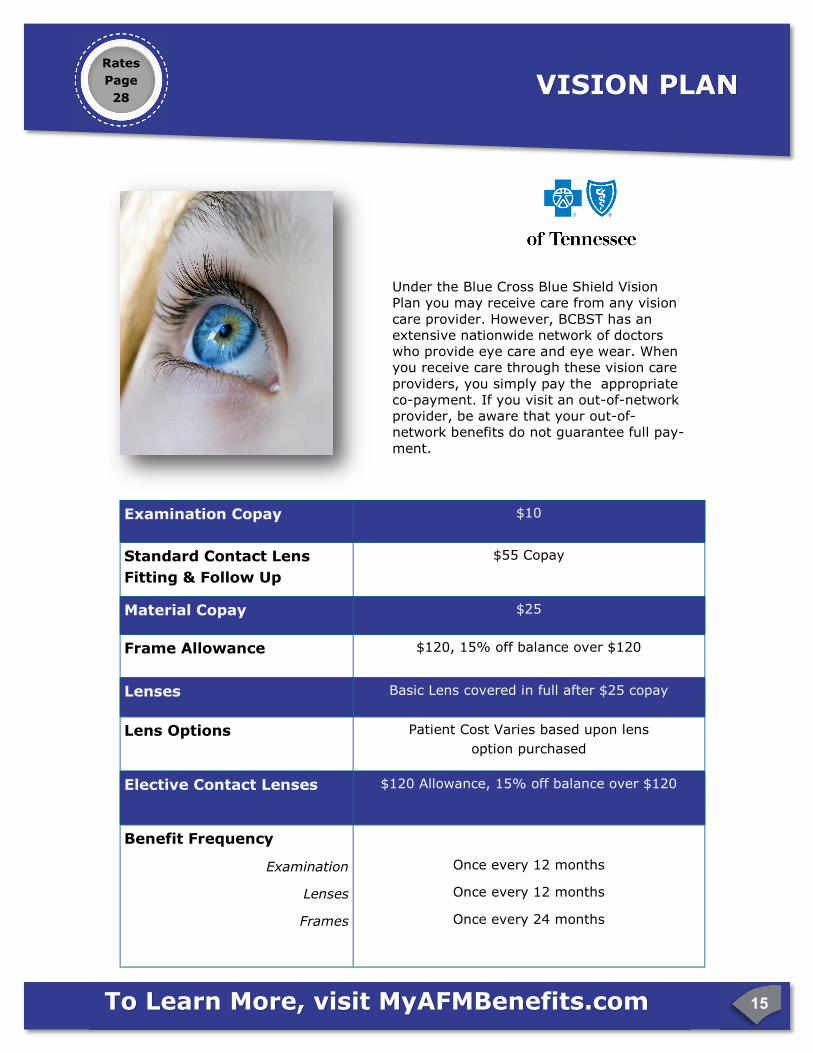

Under the Blue Cross Blue Shield Vision Plan you may receive care from any vision

care provider. However, BCBST has an extensive nationwide network of doctors who provide eye care and eye wear. When you receive care through these vision care

providers, you simply pay the appropriate co-payment. If you visit an out-of-network provider, be aware that your out-of-network benefits do not guarantee full pay-

ment.

VISION PLAN Rates

Page

28

Examination Copay $10

Material Copay $25

Frame Allowance $120, 15% off balance over $120

Lenses Basic Lens covered in full after $25 copay

Elective Contact Lenses $120 Allowance, 15% off balance over $120

Benefit Frequency

Examination

Lenses

Frames

Once every 12 months

Once every 12 months

Once every 24 months

Standard Contact Lens

Fitting & Follow Up

$55 Copay

Lens Options Patient Cost Varies based upon lens

option purchased

To Learn More, visit MyAFMBenefits.com 16

What exactly are Supplemental Benefits and how can they benefit you?

Basically, Supplemental Benefits can help protect your health and savings.

What would happen to you if you had a medical catastrophe that you could not afford?

When this happens, enormous bills and expenses can add up fast.

If you were in the hospital for a few weeks or more, would you have enough money to cover your other expenses that your insurance would not? You may not be able to earn a living which could be devastating. How would you be able to support yourself or your family? The cost of financial misfortune can escalate fast. In fact, recent research shows that medical bills contributed to over 60% of all bankruptcies.

But what can you do now to help prevent a crisis? One way is through supplemental benefit plans. Supplemental benefits provide cash directly to you to use as you need it. The amount of cash you would receive and how it is paid out depends on the specific

supplemental plan or policy you select. Only you can decide if a supplemental plan is right for you. Some things to consider when deciding if you need supplemental coverage are your health risk factors, your savings, and how much coverage you can afford. Let’s take a look at some of the plans available to you.

HOW TO FILE CLAIMS GO TO PAGE 29

How much does it cost?

The per day cost is less than you think...

Accident Critical Illness Plan

Less than a Bottle of Water

Less than a Cup of Coffee

SUPPLEMENTAL PLANS

To Learn More, visit MyAFMBenefits.com 17

What is the need?

Accidents can happen anytime, anywhere and can often lead to medical care. Accident coverage

provides cash beneifts to help cover out-of-pocket medical costs and other incidental expenses.

Even if you already have life and disability, accident coverage is a complementary plan because

the benefits do not overlap.

What are the key features?

• A schedule of benefits based upon your injury and treat-

ments.

• Benefits are paid directly to you.

• You can take it with you if you change jobs.

• Coverage is available for you, your spouse and your family.

What plans are available?

• Select a low or high option plan based upon your family’s

need.

Concerned about hospital bills? Plans Available from $0.41 / Day

In a year, more

than 1 in 5 children go

the Emergency Room.

National Center for Health Statistics

Health, United States 2007

How it Works?

Melissa elected during

her open enrollment

period an Accident

Plan. Some time later,

she took a nasty spill.

Melissa incurred

expenses for services

provided to treat her

injuries. The plan paid

the following:

What a different an

accident plan can

make when life

takes a tumble!

With Accident Coverage:$1,925

Addi�onal dollars to pay for copay, deduc�ble

and other expenses

Without Accident Coverage: $0

When individual hospital confinement coverage is applied for during the enrollment process, each applicant will be asked to attest (acknowledge) that they are currently covered by health insurance that qualifies

as minimum essential coverage as defined by federal law.

ACCIDENT PLAN

Rates

Page

29

To Learn More, visit MyAFMBenefits.com 18

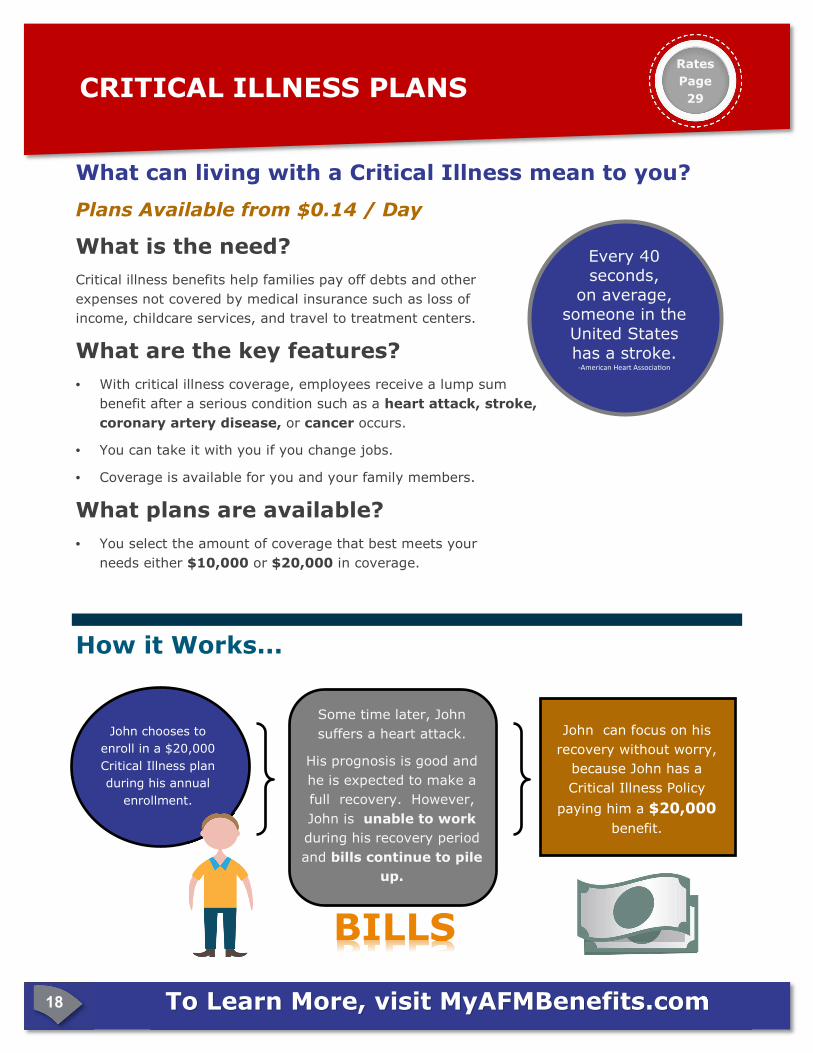

How it Works...

What can living with a Critical Illness mean to you?

Plans Available from $0.14 / Day

What is the need?

Critical illness benefits help families pay off debts and other

expenses not covered by medical insurance such as loss of

income, childcare services, and travel to treatment centers.

What are the key features?

• With critical illness coverage, employees receive a lump sum

benefit after a serious condition such as a heart attack, stroke,

coronary artery disease, or cancer occurs.

• You can take it with you if you change jobs.

• Coverage is available for you and your family members.

What plans are available?

• You select the amount of coverage that best meets your

needs either $10,000 or $20,000 in coverage.

Every 40 seconds,

on average, someone in the

United States

has a stroke. -American Heart Associa�on

CRITICAL ILLNESS PLANS

John chooses to

enroll in a $20,000

Critical Illness plan

during his annual

enrollment.

Some time later, John

suffers a heart attack.

His prognosis is good and

he is expected to make a

full recovery. However,

John is unable to work

during his recovery period

and bills continue to pile

up.

BILLS

John can focus on his

recovery without worry,

because John has a

Critical Illness Policy

paying him a $20,000

benefit.

Rates

Page

29

To Learn More, visit MyAFMBenefits.com 19

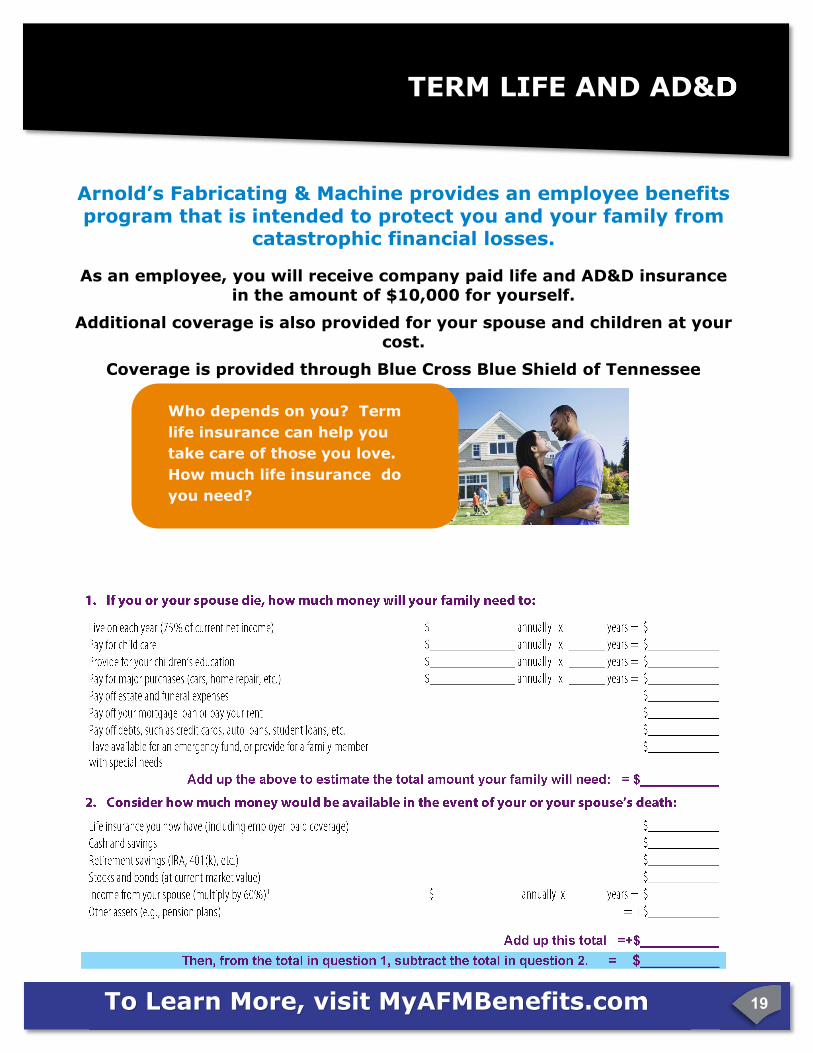

Arnold’s Fabricating & Machine provides an employee benefits program that is intended to protect you and your family from

catastrophic financial losses.

As an employee, you will receive company paid life and AD&D insurance in the amount of $10,000 for yourself.

Additional coverage is also provided for your spouse and children at your cost.

Coverage is provided through Blue Cross Blue Shield of Tennessee

Who depends on you? Term

life insurance can help you

take care of those you love.

How much life insurance do

you need?

TERM LIFE AND AD&D TERM LIFE AND AD&D

To Learn More, visit MyAFMBenefits.com 20

You have the opportunity to purchase additional life coverage for yourself and your dependents at your expense.

How Much Coverage Can You Buy?

Employee: You may purchase additional term life insurance in $10,000 increments to a

maximum of $300,000.

Spouse: You may purchase term life insurance for your spouse in increments of $10,000 to a maximum

benefit of $300,000. You must have coverage for yourself under the optional term life plan to have

coverage for your spouse.

Child/Children: Life insurance coverage is available for your dependent children between the ages of 6

months and 26 years. You may purchase a coverage amount of either $5,000 or $10,000. Children under the age of 6 months can be covered up to $1,000. You must have coverage on yourself to purchase coverage on your children.

Guaranteed Issue: Guaranteed issue means that you are guaranteed coverage without having to

answer any health questions or provide evidence of good health.

Employee: Guaranteed issue up to $80,000 up to age 70

Guaranteed Issue for your Spouse is $30,000 and $10,000 for your children.

Evidence of Insurability: If you did not elect additional life insurance when you were initially eligible or you are requesting amounts over the Guarantee Issue amount, you will be required to answer health questions on an Evidence of Insurability form. USAble Life must approve all new applications (following initial eligibility) and coverage amounts above the guarantee issue amount. If you are newly eligible and you elect an amount over Guar-antee Issue, you will be covered at the guarantee issue amount until a determination is made by USAble Life at which point your coverage will increase to the requested amount or will remain at the guarantee is-

sue amount (if denied). In either case, you may receive a request for additional information, if you fail to provide the additional information your application may be denied or in the event of a newly eligible employee you will only be covered for the guarantee issue amount.

Reductions in Insurance: By the time you or your spouse reach age 65, chances are that your children will be grown and your mortgage paid.

At age 65, providing you are still employed, your coverage will decrease to 65% of the benefit amount.

It will decrease to 50%. Coverage will terminate upon retirement.

OPTIONAL TERM LIFE Rates

Page

30

To Learn More, visit MyAFMBenefits.com 21

SHORT TERM DISABILITY

Coverage available from $ 0.81 per

week per $100 of benefit.

Rates

Page

30

GroupvoluntarydisabilityAllstate Benefits (AB) Group Voluntary Disability coverage provides a monthly cash benefit when you suffer a sickness or off -

the-job injury that leaves you totally disabled or par�ally disabled.

You can’t predict if or when you will become disabled in your life�me. But you can plan for a disability by having coverage in

place to help provide an income should you become disabled due to a sickness or injury and are unable to work. Our coverage

can help provide a monthly income when it is needed most.

Disability benefits can offer peace of mind when a disability occurs. Below is an example of how benefits might be paid.*

Meetingyourneeds

Our coverage offers support during a period of

unexpected sickness or an off -the-job injury.

Choose a guaranteed issue**

maximum monthly

benefit ranging from $400 - $5,000, up to 60%***

of income

A benefits representa�ve may help you determine

the following:

Maximum Monthly Benefit: varies

Maximum Benefit Period: 3-6 months

Elimina�on Periods:

Accident: 7-14 days

Sickness: 7-14 days

Premium: varies

Benefits start the first day a<er the elimina�on (wai�ng)

period, when you are totally disabled and cannot work

Yourbene�itcoverage

Termsandconditionsforeachbene�itvary.Pleasereviewyourcoverage

carefully.

Total Disability - Pays for total disability that begins while ac�vely at work.

Monthly benefit starts a<er the wai�ng period. Benefits con�nue while

totally disabled up to the maximum benefit period.

Par�al Disability - Pays 50% of the monthly benefit when par�ally disabled

immediately a<er at least one month of total disability. Payments con�nue

while par�ally disabled for up to 3 months, but not beyond the maximum

benefit period.

Concurrent Disability - Pays one monthly benefit even if you are disa-

bled due to more than one cause. Being disabled due to more than one

cause will not extend the �me benefits are paid.

Recurrent Disability - Pays when disabled from the same or related cause

within 6 months without a new wai�ng period or maximum benefit period.

Pregnancy - Pays for pregnancy if total disability first begins a<er your cov-

erage has been in force for at least 9 months.

Organ Donor - Pays when disabled from dona�ng an organ to another.

Waiver of Premium - Pays your premium a<er monthly disability benefits are

payable for 30 days in a row, for as long as monthly benefits are payable.

Jane chooses $3,000 in disability coverage. 8 months later she

suffers a disabling injury, is air li�ed to the local hospital

emergency room, hospitalized (3 days), and is disabled for 6

months. 1

Jane and John

are offered

group

disability by

their

employer

John declines coverage. 6 months later he suffers a disabling

back injury, is rushed to the hospital by ambulance, treated,

hospitalized (2 days), and is disabled for 4 months.

In addi�on to her medical coverage our disability insurance

provided Jane the following:

Total Disability Monthly Benefit-$3,000

John does not have disability coverage. His medical cover-

age will pay for a por�on of his hospital expenses, but his

monthly expenses while out of work will be paid out of his

own pocket.

**You must apply during your initial enrollment period to be

eligible. If enrolling after your

will be required.

***May be less depending on state.

Legal Notices 22

Premium Assistance Under Medicaid and the Children’s Health Insurance Program (CHIP)

If you or your children are eligible for Medicaid or CHIP and you are eligible for health coverage from your employer,

your State may have a premium assistance program that can help pay for coverage. These States use funds from their

Medicaid or CHIP programs to help people who are eligible for these programs, but also have access to health insur-

ance through their employer. If you or your children are not eligible for Medicaid or CHIP, you will not be eligible for

these premium assistance programs.

If you or your dependents are already enrolled in Medicaid or CHIP and you live in a State listed below, you can contact

your State Medicaid or CHIP office to find out if premium assistance is available.

If you or your dependents are NOT currently enrolled in Medicaid or CHIP, and you think you or any of your depend-

ents might be eligible for either of these programs, you can contact your State Medicaid or CHIP office or dial 1-877-

KIDS NOW or www.insurekidsnow.gov to find out how to apply. If you qualify, you can ask the State if it has a pro-

gram that might help you pay the premiums for an employer-sponsored plan.

Once it is determined that you or your dependents are eligible for premium assistance under Medicaid or CHIP, as well

as eligible under your employer plan, your employer must permit you to enroll in your employer plan if you are not

already enrolled. This is called a “special enrollment” opportunity, and you must request coverage within 60 days of

being determined eligible for premium assistance. If you have ques�ons about enrolling in your employer plan, you

can contact the Department of Labor electronically at www.askebsa.dol.gov or by calling toll-free 1-866-444-EBSA

(3272).

You may be eligible for assistance paying your employer health plan premiums. The following is current as of

July 31, 2014. You should contact your State for further informa<on on eligibility –

TENNESSEE—Medicaid

Website: hAps://www.tn.gov/tenncare/

Phone: 1-855-259-0701

For more informa<on on special enrollment rights, you can contact either:

US Department of Labor

Employee Benefits Security Administra<on

www.dol.gov/ebsa

1-866-444-EBSA (3272)

Legal Notices 23

** Continuation Coverage Rights Under COBRA**

Initial Notification Introduction You are receiving this notice because you may have recently become covered under a group health plan (the Plan). This notice contains important information about your right to COBRA continuation coverage, which is a temporary extension of coverage under the Plan. This notice generally explains COBRA continuation cov-erage, when it may become available to you and your family, and what you need to do to protect the right to receive it. The right to COBRA continuation coverage was created by a federal law, the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA). COBRA continuation coverage can become available to you when you would otherwise lose your group health coverage. It can also become available to other members of your family who are covered under the Plan when they would otherwise lose their group health coverage. For ad-ditional information about your rights and obligations under the Plan and under federal law, you should review the Plan’s Summary Plan Description or contact the Plan Administrator. What is COBRA Continuation Coverage? COBRA continuation coverage is a continuation of Plan coverage when coverage would otherwise end be-cause of a life event known as a “qualifying event.” Specific qualifying events are listed later in this notice. After a qualifying event, COBRA continuation coverage must be offered to each person who is a “qualified beneficiary.” You, your spouse, and your dependent children could become qualified beneficiaries if cover-age under the Plan is lost because of the qualifying event. Under the Plan, qualified beneficiaries who elect COBRA continuation coverage must pay for COBRA continuation coverage. If you are an employee, you will become a qualified beneficiary if you lose your coverage under the Plan be-cause either one of the following qualifying events happens:

• Your hours of employment are reduced, or • Your employment ends for any reason other than your gross misconduct. If you are the spouse of an employee, you will become a qualified beneficiary if you lose your coverage under the Plan because any of the following qualifying events happens:

• Your spouse dies; • Your spouse’s hours of employment are reduced; • Your spouse’s employment ends for any reason other than his or her gross misconduct; • Your spouse becomes entitled to Medicare benefits (under Part A, Part B, or both); or • You become divorced or legally separated from your spouse. Your dependent children will become qualified beneficiaries if they lose coverage under the Plan because any of the following qualifying events happens: The parent-employee dies; • The parent-employee’s hours of employment are reduced; • The parent-employee’s employment ends for any reason other than his or her gross misconduct; • The parent-employee becomes entitled to Medicare benefits (Part A, Part B, or both); • The parents become divorced or legally separated; or • The child stops being eligible for coverage under the plan as a “dependent child.”

Legal Notices 24

When is COBRA Coverage Available?

The Plan will offer COBRA continuation coverage to qualified beneficiaries only after the Plan Administra-tor has been notified that a qualifying event has occurred. When the qualifying event is the end of em-ployment or reduction of hours of employment, death of the employee, or the employee becoming entitled to Medicare benefits (under Part A, Part B, or both), the employer must notify the Plan Administrator of the qualifying event.

You Must Give Notice of Some Qualifying Events For the other qualifying events (divorce or legal separation of the employee and spouse or a de-pendent child’s losing eligibility for coverage as a dependent child), you must notify the Plan Ad-ministrator within 60 days after the qualifying event occurs. You must provide this notice to: Hu-man Resources , Life Care Partners, LLC. 6320 Venture Drive, Suite 205, Bradenton, FL 34202. You will be required to present certified documentation to make the change. How is COBRA Coverage Provided?

Once the Plan Administrator receives notice that a qualifying event has occurred, COBRA continuation coverage will be offered to each of the qualified beneficiaries. Each qualified beneficiary will have an in-dependent right to elect COBRA continuation coverage. Covered employees may elect COBRA continu-ation coverage on behalf of their spouses, and parents may elect COBRA continuation coverage on be-half of their children. COBRA continuation coverage is a temporary continuation of coverage. When the qualifying event is the death of the employee, the employee's becoming entitled to Medicare benefits (under Part A, Part B, or both), your divorce or legal separation, or a dependent child's losing eligibility as a dependent child, CO-BRA continuation coverage lasts for up to a total of 36 months. When the qualifying event is the end of employment or reduction of the employee's hours of employment, and the employee became entitled to Medicare benefits less than 18 months before the qualifying event, COBRA continuation coverage for qualified beneficiaries other than the employee lasts until 36 months after the date of Medicare entitle-ment. For example, if a covered employee becomes entitled to Medicare 8 months before the date on which his employment terminates, COBRA continuation coverage for his spouse and children can last up to 36 months after the date of Medicare entitlement, which is equal to 28 months after the date of the qualifying event (36 months minus 8 months). Otherwise, when the qualifying event is the end of employ-ment or reduction of the employee’s hours of employment, COBRA continuation coverage generally lasts for only up to a total of 18 months. There are two ways in which this 18-month period of COBRA continu-ation coverage can be extended.

Disability extension of 18-month period of continuation coverage If you or anyone in your family covered under the Plan is determined by the Social Security Administration to be disabled and you notify the Plan Administrator in a timely fashion, you and your entire family may be entitled to receive up to an additional 11 months of COBRA continuation coverage, for a total maximum of 29 months. The disability would have to have started at some time before the 60th day of COBRA contin-uation coverage and must last at least until the end of the 18-month period of continuation coverage.

Legal Notices 25

Second qualifying event extension of 18-month period of continuation coverage If your family experiences another qualifying event while receiving 18 months of COBRA continuation coverage, the spouse and dependent children in your family can get up to 18 additional months of CO-BRA continuation coverage, for a maximum of 36 months, if notice of the second qualifying event is properly given to the Plan. This extension may be available to the spouse and any dependent children receiving continuation coverage if the employee or former employee dies, becomes entitled to Medi-care benefits (under Part A, Part B, or both), or gets divorced or legally separated, or if the dependent child stops being eligible under the Plan as a dependent child, but only if the event would have caused the spouse or dependent child to lose coverage under the Plan had the first qualifying event not oc-curred. If You Have Questions about COBRA Questions concerning your Plan or your COBRA continuation coverage rights should be addressed to the contact or contacts identified below. For more information about your rights under ERISA, includ-ing COBRA, the Health Insurance Portability and Accountability Act (HIPAA), and other laws affecting group health plans, contact the nearest Regional or District Office of the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) in your area or visit the EBSA website at www.dol.gov/ebsa

Keep Your Plan Informed of Address Changes

In order to protect your family’s rights, you should keep the Plan Administrator informed of any changes

in the addresses of family members. You should also keep a copy, for your records, of any notices you

send to the Plan Administrator.

Arnold’s Fabricating and Machine

Attn: Human Resources

3333 Reynoldsburg Rd

Camden, TN 38320

731-584-3601

To Learn More, visit MyAFMBenefits.com 26

Please note: The medical plan offered by Arnold’s Fabricating & Machine does in fact provide minimum essential coverage and is deemed to be affordable using the IRS federal poverty line safe harbor definition.

What is the Health Insurance Marketplace?

The Marketplace is designed to help you find health insurance that meets your needs and fits your budget. The Market-place at www.healthcare.gov offers "one-stop shopping" to find and compare private health insurance options. You may also be eligible for a new kind of tax credit that lowers your monthly premium right away.

Your Responsibility Under Health Care Reform

Individual Mandate. The law now requires that most individuals maintain health insurance coverage or otherwise pay a penalty. If you don’t have medical coverage in 2015, you’ll pay the higher of these two amounts1:

• 2% of your yearly household income. (Only the amount of income above the tax filing threshold, about $10,000 for an individual, is used to calculate the penalty.)

The maximum penalty is the national average premium for a bronze plan.

• $325 per person for the year ( $162.50 per child under 18 ). The maximum penalty per family using this method is $975. 1https://www.healthcare.gov/fees-exemptions/fee-for-not-being-covered/

As a result of some key parts of the health care law that took effect in 2014, there are now new ways to buy health

insurance: the Health Insurance Marketplace.

Can I Save Money on my Health Insurance Premiums

in the Marketplace?

You may qualify to save money and lower your monthly premium, but only if your employer does not offer coverage, or offers coverage that doesn't meet certain standards. The savings on your premium that you're eligible for depends on

your household income.

Does Employer Health Coverage Affect Eligibility for Premium Savings

though the Marketplace?

Yes. If you have an offer of health coverage from your employer that meets certain standards, you will not be eligible for a tax credit through the Marketplace and may wish to enroll in your employer's health plan. However, you may be eligi-ble for a tax credit that lowers your monthly premium, or a reduction in certain cost-sharing if your employer does not offer coverage to you at all or does not offer coverage that meets certain standards. If the cost of a plan from your em-ployer that would cover you (and not any other members of your family) is more than 9.5% of your household income for the year, or if the coverage your employer provides does not meet the "minimum value" standard set by the Afforda-ble Care Act, you may be eligible for a tax credit.1

Note: If you purchase a health plan through the Marketplace instead of accepting health coverage offered by your employer, then you may lose the employer

contribution (if any) to the employer-offered coverage. Also, this employer contribution -as well as your employee contribution to employer-offered coverage- is

often excluded from income for Federal and State income tax purposes. Your payments for coverage through the Marketplace are made on an after-tax basis. 1https://www.healthcare.gov/fees-exemptions/fee-for-not-being-covered/

AFFORDABLE CARE ACT UPDATE

To Learn More, visit MyAFMBenefits.com 27

Every reasonable effort has been made for the information provided in this booklet to be accurate. It is intended to

provide the employees with Arnold’s Fabricating & Machine an overview of the coverages offered. It is in no way a

guarantee or offer of coverage. Each carrier has the ability to underwrite based on its contract with Arnold’s

Fabricating & Machine or its employees. Each carrier’s contract, underwriting, and policies will supersede this

document. Please be aware that each carrier may have exclusions or limitations and you must consult your summary

plan description and/or policies for details.

BCBS OF TENNESSEE Customer Service……………….800-565-9140

HELPCARD Doctors by Phone ......................... ….800-847-3627

BCBS DENTAL Customer Service ..................... ….800-565-9140

BCBS VISION Customer Service ...................... ….877-342-0737

BCBS LIFE (to file a life claim) ......................... ...800-370-5856

ALLSTATE BENEFITS Customer Service ......... ...800-521-3535

WHO TO CONTACT

Need Help with Enrollment? Contact BenefitHelp Toll Free at 888-663-1285,

Option #2 or email [email protected] for

assistance.

IM

PO

RTA

NT P

HO

NE N

UM

BER

S

Who Do I Contact after Enrollment?

FOR CLAIMS OR BENEFITS QUESTIONS

BenefitHelp KKKKKKKKKKKKKK...888-663-1285, option #2

Rates 28

Med

ical

(p

g.

10

)

Medical Plan - Weekly Payroll Deduction

Who to Cover?

Medical Plan

Employee $ 9.51

Employee + 1 $ 121.17

Employee + 2 or more $ 214.49

Dental Plan - Weekly Payroll Deduction

Who to Cover?

Employee $ 0.00

Employee + 2 or more $ 12.30

Employee + 1 $ 5.70

Den

tal

(p

g.

13

)

Vision Plan - Weekly Payroll Deduction

Who to Cover?

Employee $ 0.00

Employee + 1 $ 1.16

Employee + 2 or more $ 2.55 Vis

ion

(p

g.

14

)

Review your worksheet prior to your enrollment

Pick the Plan that Best Meets Your Needs...

RATES

NEED HELP? Enrollment Counselors are available to answer questions and

assist you with your enrollment. Check with your Human

Resources Department to learn when your employee open enrollment meetings are scheduled.

Basic Life - Weekly Payroll Deduction

Who to Cover?

Employee $ 0.00

Employee + All Dependents $ .30 Lif

e (

pg

. 1

9)

Rates 29

Accid

en

t (p

g.

17

)

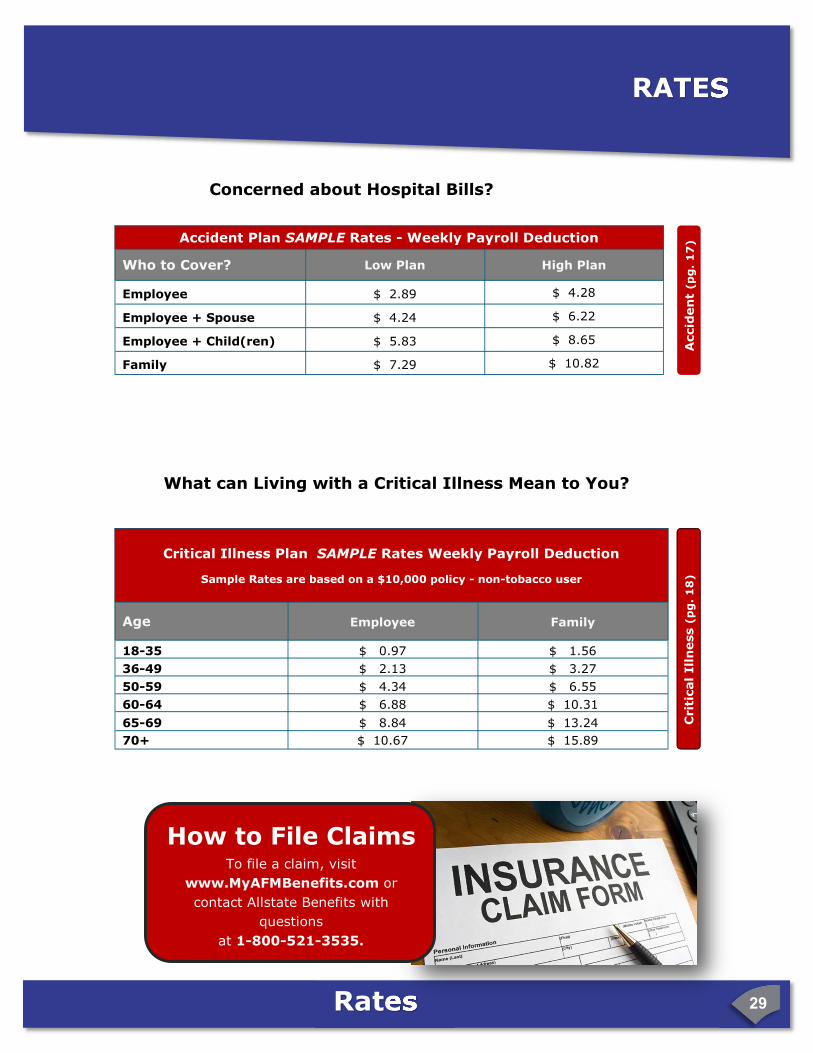

How to File Claims

To file a claim, visit

www.MyAFMBenefits.com or

contact Allstate Benefits with

questions

at 1-800-521-3535.

Concerned about Hospital Bills?

RATES

Critical Illness Plan SAMPLE Rates Weekly Payroll Deduction

Sample Rates are based on a $10,000 policy - non-tobacco user

Age Employee Family

18-35 $ 0.97 $ 1.56

36-49 $ 2.13 $ 3.27

50-59 $ 4.34 $ 6.55

60-64 $ 6.88 $ 10.31

65-69 $ 8.84 $ 13.24

70+ $ 10.67 $ 15.89

Crit

ical

Ill

ness (

pg

. 1

8)

What can Living with a Critical Illness Mean to You?

Accident Plan SAMPLE Rates - Weekly Payroll Deduction

Who to Cover? Low Plan

Employee $ 2.89

Employee + Spouse $ 4.24

Employee + Child(ren) $ 5.83

Family $ 7.29

High Plan

$ 4.28

$ 6.22

$ 8.65

$ 10.82

Rates 30

Op

tion

al

Lif

e -

(p

g.

20

)

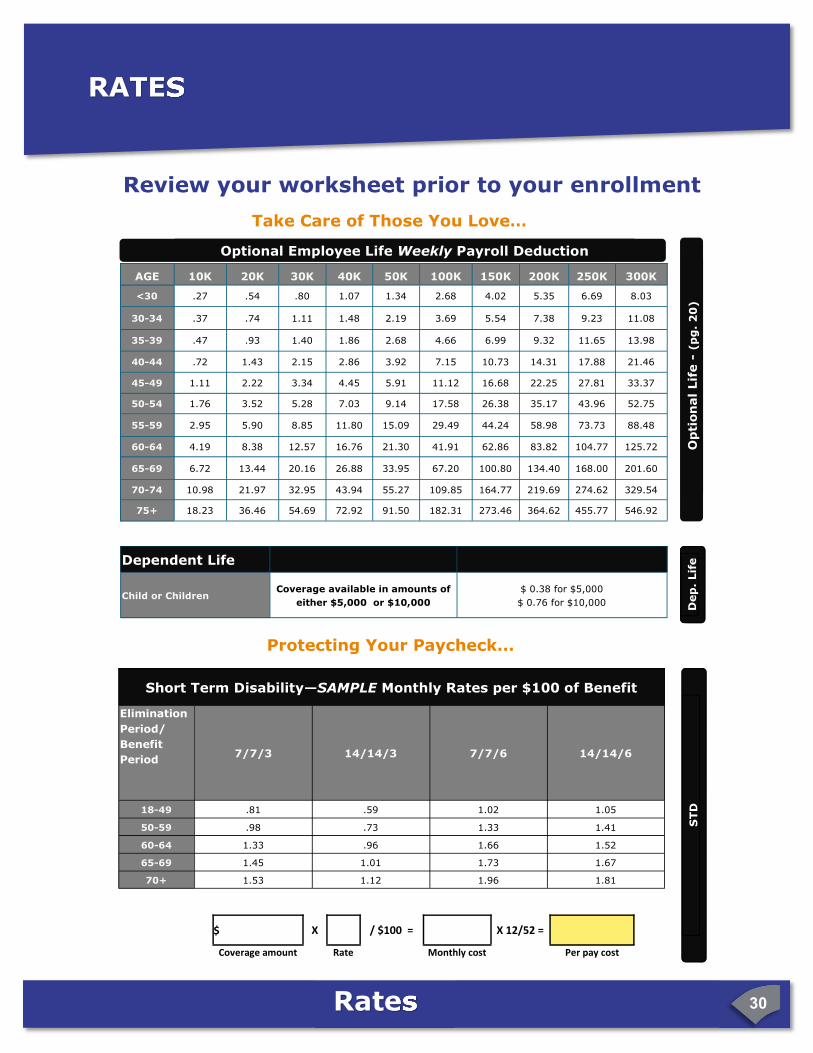

AGE 10K 20K 30K 40K 50K 100K 150K 200K 250K 300K

<30 .27 .54 .80 1.07 1.34 2.68 4.02 5.35 6.69 8.03

30-34 .37 .74 1.11 1.48 2.19 3.69 5.54 7.38 9.23 11.08

35-39 .47 .93 1.40 1.86 2.68 4.66 6.99 9.32 11.65 13.98

40-44 .72 1.43 2.15 2.86 3.92 7.15 10.73 14.31 17.88 21.46

45-49 1.11 2.22 3.34 4.45 5.91 11.12 16.68 22.25 27.81 33.37

50-54 1.76 3.52 5.28 7.03 9.14 17.58 26.38 35.17 43.96 52.75

55-59 2.95 5.90 8.85 11.80 15.09 29.49 44.24 58.98 73.73 88.48

60-64 4.19 8.38 12.57 16.76 21.30 41.91 62.86 83.82 104.77 125.72

65-69 6.72 13.44 20.16 26.88 33.95 67.20 100.80 134.40 168.00 201.60

70-74 10.98 21.97 32.95 43.94 55.27 109.85 164.77 219.69 274.62 329.54

75+ 18.23 36.46 54.69 72.92 91.50 182.31 273.46 364.62 455.77 546.92

Dependent Life

Child or Children Coverage available in amounts of

either $5,000 or $10,000

$ 0.38 for $5,000

$ 0.76 for $10,000 Dep

. Lif

e

Optional Employee Life Weekly Payroll Deduction

Review your worksheet prior to your enrollment

Take Care of Those You Love…

Elimination

Period/

Benefit

Period

7/7/3 14/14/3 7/7/6 14/14/6

18-49 .81 .59 1.02 1.05

Short Term Disability—SAMPLE Monthly Rates per $100 of Benefit

50-59 .98 .73 1.33 1.41

60-64 1.33 .96 1.66 1.52

65-69 1.45 1.01 1.73 1.67

70+ 1.53 1.12 1.96 1.81

Protecting Your Paycheck...

STD

RATES

$ X / $100 = X 12/52 =

Coverage amount Rate Monthly cost Per pay cost

Rates 31

NEED HELP? Enrollment Counselors are available to answer questions and assist you with your enrollment. Check with your

Human Resources Department to learn when your employee open enrollment meetings are scheduled.

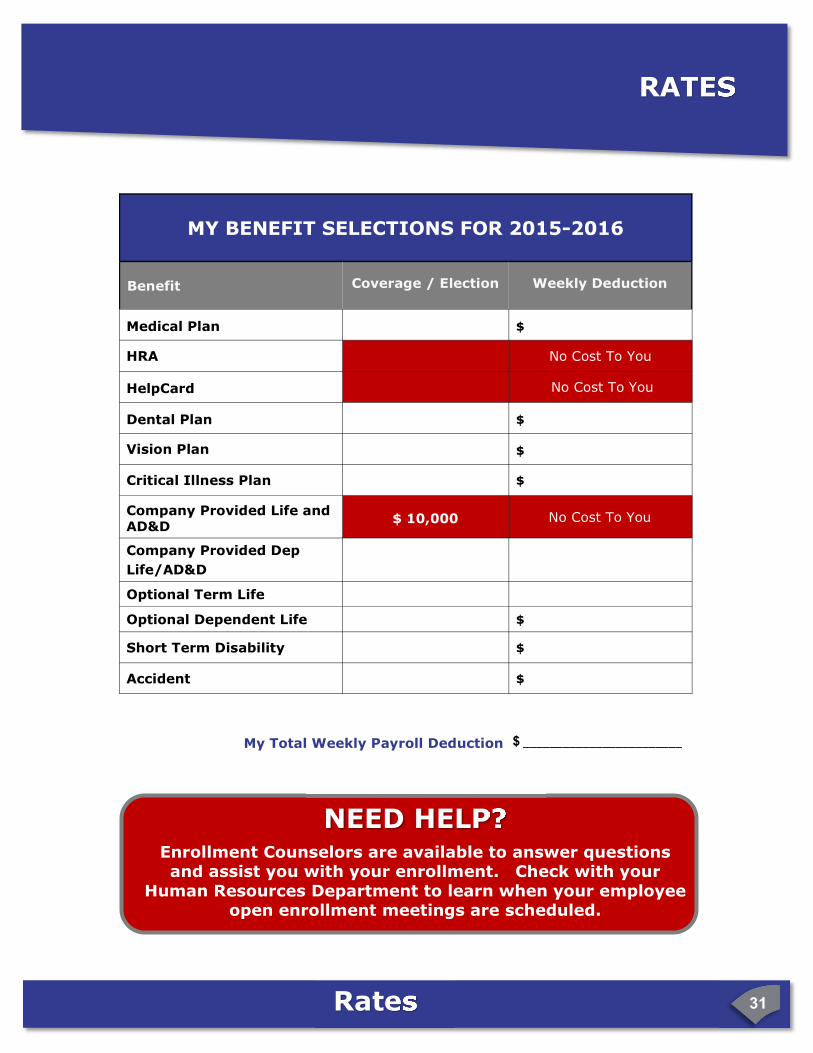

MY BENEFIT SELECTIONS FOR 2015-2016

Benefit Coverage / Election Weekly Deduction

Medical Plan $

HRA No Cost To You

HelpCard No Cost To You

Dental Plan $

Vision Plan $

Critical Illness Plan $

Company Provided Life and AD&D

$ 10,000 No Cost To You

Company Provided Dep

Life/AD&D

Optional Term Life

Optional Dependent Life $

Short Term Disability $

Accident $

My Total Weekly Payroll Deduction $ ________________________

RATES

V4-07062015

© BenefitHelp 2015

BenefitGuide Arnold’s Fabrica�ng & Machine v1

V5-08182015