tm annette k. mcclave health scientist, epidemiology branch michael a. tynan public health analyst,...

Post on 21-Dec-2015

217 views

TRANSCRIPT

TM

Annette K. McClaveHealth Scientist, Epidemiology Branch

Michael A. TynanPublic Health Analyst, Policy Unit

CDC, Office on Smoking and Health

Smokeless Tax Policies Differences in Taxes on Cigarettes and Smokeless Tobacco

5th National Summit on Smokeless & Spit TobaccoSeptember 21, 2009

TM

Health Consequences of Smokeless Tobacco Use

Smokeless tobacco use can lead to nicotine addiction and other serious health consequences– Oral, pancreatic cancer

– Possible acute cardiovascular effects (e.g. Heart Rate, Blood Pressure)

– Adverse Pregnancy Outcomes

– Periodontal Disease

– May lead to cigarette smoking, delay quitting

• Adolescents who use smokeless tobacco are more likely to become cigarette smokers

TM

Smokeless Tobacco Use in the U.S.

More than 8.1 million Americans aged 12 or older (3.2%) are current smokeless tobacco users

Smokeless use has not declined since 2002

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2002 2003 2004 2005 2006 2007

Past month use of smokeless tobacco among persons age 12 and older in the U.S. – 2002 to 2007

Source: SAMHSA, National Survey on Drug Use and Health (2002-2007)

TM

Excise Taxes as a Policy Tool

Excise tax increases are a policy intervention recommended to reduce tobacco consumption by raising the price of tobacco products

– Surgeon General

– Institute of Medicine

– Community Guide

– World Health Organization

TM

Review from 2000 SGR

Economic studies tend to focus on the impact of cigarette taxes on consumption– 10% increase in price reduces use by 4%

Very little research exists on the impact tax increases may have on smokeless tobacco use

However, the existing research (though limited) shows higher smokeless tobacco prices are associated with lower smokeless tobacco use

Source: Reducing Tobacco Use: A Report of The Surgeon General (2000)

TM

Tax Imbalance

Historically, cigarette taxes have increased at a greater rate than smokeless taxes– Price of cigarettes rise more rapidly than

smokeless

This imbalance may also impact smokeless– Previous results show an imbalance in cigarette

and smokeless tax increases potentially results in higher smokeless tobacco use

If cigarette taxes continue to increase disproportionately, the gap between cigarette and smokeless prices will potentially increase

Source: Reducing Tobacco Use: A Report of The Surgeon General (2000)

TM

Indentifying Tax Imbalances

We reviewed state excise tax data available from Center for Disease Control and Prevention (CDC) and National Cancer Institute (NCI) legislative databases– CDC’s State Tobacco Activities Tracking and

Evaluation (STATE) System

– NCI’s State Cancer Legislative Database (SCLD) Program

Through Library of Congress research, we reviewed recent legislation to update the history of Federal excise tax increases contained in 2000 Surgeon General’s Report

TM

19171901

History of Federal Excise Tax Imbalance

Cigarette Excise

Tax Enactment

Sources: Reducing Tobacco Use: A Report of The Surgeon General (2000); Children’s Health Insurance Program Reauthorization Act of 2009.

1864 2009

2002

2000

1865

1866

1867

1868 1875

1883

1897

1898 1910 1919

1940

1942

1951

1983

1991

1993

TM

19171901

History of Federal Excise Tax Imbalance

Cigarette Excise

Tax Enactment

Smokeless Excise

Tax Enactment

Sources: Reducing Tobacco Use: A Report of The Surgeon General (2000); Children’s Health Insurance Program Reauthorization Act of 2009.

1864 2009

2009

2002

2002

2000

2000

1865

1866

1867

1868 1875

1883

1897

1898 1910 1919

1940

1942

1951

1983

1991

1993

1986

1991

1993

TM

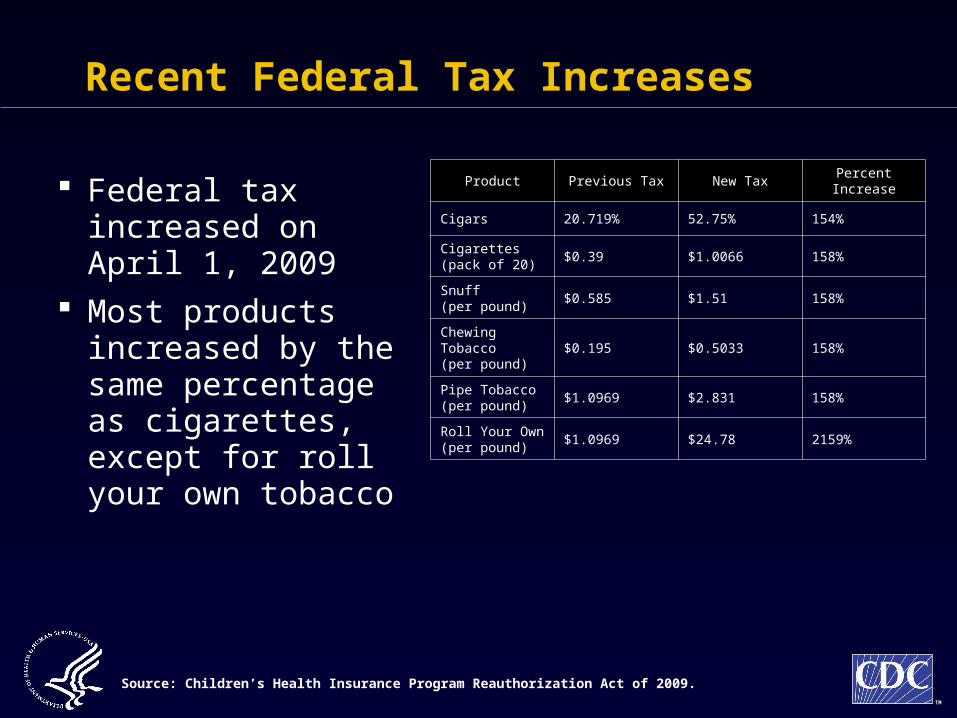

Recent Federal Tax Increases

Product Previous Tax New TaxPercentIncrease

Cigars 20.719% 52.75% 154%

Cigarettes (pack of 20)

$0.39 $1.0066 158%

Snuff(per pound)

$0.585 $1.51 158%

ChewingTobacco (per pound)

$0.195 $0.5033 158%

Pipe Tobacco(per pound)

$1.0969 $2.831 158%

Roll Your Own(per pound)

$1.0969 $24.78 2159%

Federal tax increased on April 1, 2009

Most products increased by the same percentage as cigarettes, except for roll your own tobacco

Source: Children’s Health Insurance Program Reauthorization Act of 2009.

TM

History of State Excise Tax Enactments

By 1949, 43 states had established a cigarette tax

By 1969 every state had a cigarette tax

By 1949, only 12 states had a smokeless tax

Half of smokeless taxes were established after 1980– 7 states established a

tax in last 10 years

– No smokeless tax in Pennsylvania

Took an average of 31 years after a state established a cigarette tax to establish a smokeless tax

State Cigarette Taxes State Smokeless Taxes

Sources: National Cancer Institute’s State Cancer Legislative Database Program; Centers for Disease Control and Prevention’s State Tobacco Activities Tracking and Evaluation System.

TM

State Excise Tax Increases 1995-2008

Between 1995 and 2008 there were 107 separate state cigarette excise tax increases

Between 1995 and 2008 there were only 24 state smokeless excise tax increases

State Cigarette Taxes State Smokeless Taxes

Source: Centers for Disease Control and Prevention’s State Tobacco Activities Tracking and Evaluation System.

TM

State Tax Increases in 2009

So far this year, 12 states have enacted tax increases on cigarettes

10 of these states have also increased the tax on smokeless products

4 other states have increased the smokeless tax without increasing the cigarette tax

State Cigarette Taxes State Smokeless Taxes

A promising start?

TM

AZ

WY

OR

ID

MT

UTNV

WA

CA

TX

AROK

ND

LA

KS

IANE

SD

CO

NM

MO

MN

TN

AL

KY

OH

MS

MI

IN

GA

FL

PA

ME

NY

WV VA

NC

SC

VT

CT

D.C.

RI

NJ

MD

DE

NHMA

IL

WI

AK

HI

Cigarette Tax Increased(n=2)

Smokeless Tax Increased(n=4)

No Change in Tobacco Taxes(n=35)

Both Cigarette and SmokelessTax Increased (n=10)

Note: DC is included among results for states.

2009 State Tobacco Excise Tax Increases

TM

Issues with Smokeless Excise Taxes

There is no uniform method to tax smokeless products– Federal smokeless tax is based on weight

– States smokeless taxes are based on:

• percentage of price (most common for smokeless)– sales price/purchase price

– wholesale price

– manufacturer sales, list or invoice price

• by weight (most common for snuff)

• percentage of product value or gross receipt of sales

Various methods in taxation complicate evaluation

Source: Centers for Disease Control and Prevention’s State Tobacco Activities Tracking and Evaluation System.

TM

Other Policy Gaps: Graphic Warning Labels By June 2010 new text

warnings will be required for smokeless

– comprise 30% of package

By September 2012, new graphic warnings required for cigarettes

– comprise the top 50% of the front and back of a pack

Graphics allowed, but not required for smokelessSource: Family Smoking Prevention and Tobacco Control Act of 2009

Image: Health Canada

TM

Annette K. McClave [email protected] Scientist, Epidemiology Branch

Michael A. [email protected] Health Analyst, Policy Unit

CDC, Office on Smoking and Health

Smokeless Tax Policies Differences in Taxes on Cigarettes and Smokeless Tobacco

The findings and conclusions in this presentation are those of the author and do not necessarily represent the official position of the Centers for Disease Control and Prevention.