tlip5035a presentation 8

TRANSCRIPT

PRESENTATION 8:RISK MANAGEMENT AND CONTINGENCY PLANNING

PRESENTATION 8 OUTLINE

The following areas are covered in this presentation:

• Risk Management

• Contingency Plans

• Revenue Loss

• Cost of Goods

• Expenses

• Cash Flow

RISK MANAGEMENT

• Identification, analysis and evaluation of risk – used to arrive at a

contingency plan

• Risk can be simply defined as, in the financial planning context,

“loss”

• In reality loss will include loss of profit, loss of income, loss of

funding, loss of market share, loss of contract, loss of key

personnel, loss of reputation or loss of life. None of these are

good.

Establish areas most at risk

Identify risk or probability of risk occurring in these areas

Analyse the risk and its consequences

CONTINGENCY PLANS

• If things start going wrong or the organisation suffers a “negative

event” there should be a contingency plan in place

• Contingency plans can be looked at as the risk controls

• In the financial planning and budgetary context, contingency plans

are grouped into areas that cover negative impacts on revenue,

costs of goods and/or services sold, expenses and cash flows

• In order to identify the risk, you must ask two questions:

1. What can happen? 2. How will it happen?

CONTINGENCY PLANS

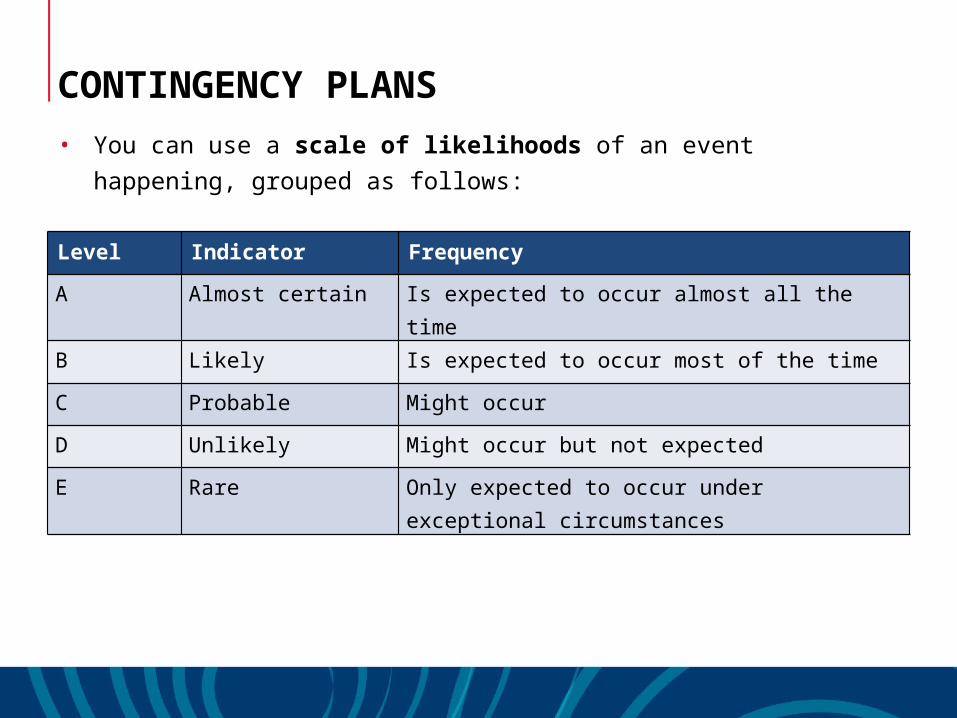

• You can use a scale of likelihoods of an event happening,

grouped as follows:

Level Indicator Frequency

A Almost certain Is expected to occur almost all the time

B Likely Is expected to occur most of the time

C Probable Might occur

D Unlikely Might occur but not expected

E Rare Only expected to occur under exceptional circumstances

CONTINGENCY PLANS

• Together with a qualitative measure of consequence:

Level Indicator (examples)

1 Severe or catastrophic (bankruptcy, forced closure)

2 Significant (major financial loss, key personnel loss)

3 Moderate (failure of major supplier, fire)

4 Minor (business downturn, bad publicity)

5 Negligible (price rises in fixed costs)

CONTINGENCY PLANS

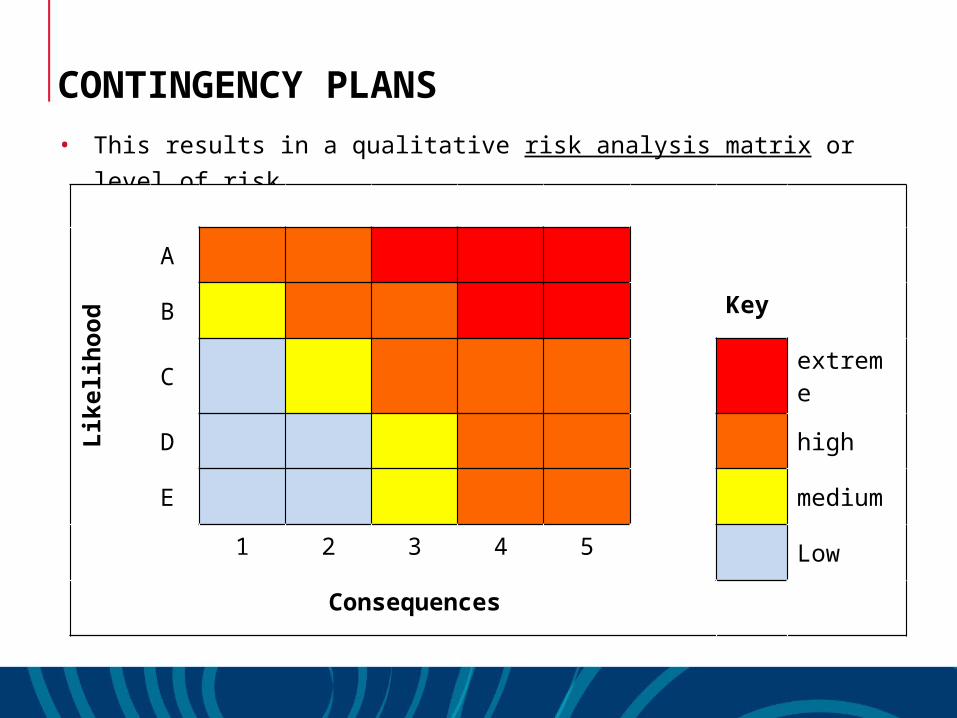

• This results in a qualitative risk analysis matrix or level of risk

Likelihood

A

B Key

C extreme

D high

E medium

1 2 3 4 5 Low

Consequences

CONTINGENCY PLANS

• In terms of a budget context the levels of risk may manifest

themselves in the following examples:

Extreme risk: closure of the business or bankruptcy or be an

accident resulting in death of staff or members of the public

High risk: big downturn in business, financial loss or loss of

key staff

Medium risk: financial loss, adverse publicity, and loss of a major contract or failure of a major creditor. These are all

recoverable events; the extreme risk events and high-risk events are not certain to be recoverable

Low-level risk: increase in interest rates or other overhead

expenses that were not budgeted for

CONTINGENCY PLANS

• Risk assessments are best done as a group with participation

sought from as many as possible. This greatly assists in identifying

risks no one else had thought of

• Keep in mind that what has been assessed as a low risk event with

negligible consequences within one organisation may well have

significant impacts on another

• Some events cannot be easily allowed for within contingency

plans and it is these unforeseen events that risk management

should be attempting to target

CONTINGENCY PLANS

• There are various options for treating risk and after evaluation of

the options, the best response should be selected. The options

are:

AvoidEither don’t go ahead with the activity of operation or change

some of the circumstances. Have another look and reassess.

AcceptSome organisations might choose to accept the risk

because the alternatives are worse or the benefits outweigh

the possible problems.

ControlControl involves instigating some form of risk control to reduce the adverse outcomes. This may be something like staff training or

extra supervision.

TransferThe process of spreading the risk

to other parties such as insurance

REVENUE LOSS• Revenue loss can be due to some of the following:

− Loss of big contract or failure to renew one

− Downturn in business due to competitors or increased competition

− Government action reducing subsidies or support

• Actions that might help will include:

− Increasing advertising

− Moving into new markets

− Reducing poorly selling items

− Opening up in new areas

• The particular circumstance for a company cannot be guessed so

specific action is best arrived at, as a group, specific to your company

COST OF GOODS

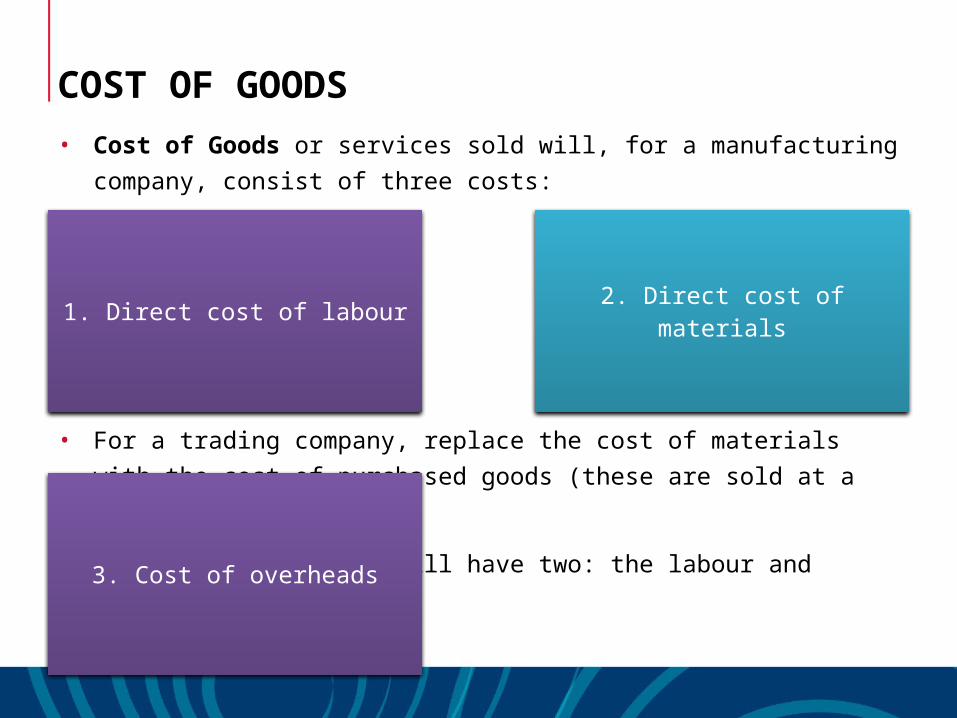

• Cost of Goods or services sold will, for a manufacturing

company, consist of three costs:

• For a trading company, replace the cost of materials with the cost

of purchased goods (these are sold at a profit)

• The service business will have two: the labour and overheads

1. Direct cost of labour 2. Direct cost of materials

3. Cost of overheads

COST OF GOODS

• Your possible contingency plans may include:

− Staff reductions

− Sourcing cheaper raw materials and purchases

− Adopting a just-in-time method of inventory purchase i.e.

purchase at the last minute before manufacture rather than

holding raw material inventory (and paying for it)

− Outsourcing some of your overheads

− Recycling

• Again, options are best arrived at in conjunction with staff and

relevant to your particular company

EXPENSES

Expenses in the budget will be administrative and include:

ElectricityFinancial costs (from the

bank for example, interest and charges)

Office expenses Bad debts

EXPENSES• Your contingency options may include:

− Bulk purchasing power and or gas or even switching over from

one to another or another supplier

− Bulk purchases of office supplies

− Efficiency programs

− Outsourcing services for accounting

− Human resources

− Some IT

• It is important to remember that the reason for an increase in

expenses may sometimes be due to a favourable upturn in business

activity and not necessarily due to errors in the expected budget

items

CASH FLOW

• Consists of the movement of cash both ways; that is, both into

and out of a business.

• To overcome shortfalls in cash flow required to operate the

business, short-term finance will be a viable contingency plan

• Any form of raising finance should be investigated, which can

result in a swift inflow of cash. Capital expenditure may need to be

postponed during a time of reduced cash flow.

• Contingency plans are activated due to a negative event as

described above. They form part of the risk controls to mitigate

any risk identified in a risk assessment. They need to be

formulated by a group and able to be acted on swiftly.