time and attendance audit for six months … · time and attendance audit for six months ended...

TRANSCRIPT

TIME AND ATTENDANCE AUDIT FOR SIX MONTHS ENDED December 31, 2010

Executive Office Finance

College and Career Readiness Departmental Support

Innovations

INTERNAL AUDIT REPORT

Audit Control Number: TA 2-10 December 1, 2011

Issued: December 15, 2011

LOUISIANA DEPARTMENT OF EDUCATION BUREAU OF INTERNAL AUDIT

Baton Rouge, LA

NOTICE

STATE OF LOUISIANA

DEPARTMENT OF EDUCATION POST OFFICE BOX 94064 / BATON ROUGE, LOUISIANA 70804-9064

Toll Free #: 1-877-453-2721 http://www.doe.state.la.us

December 15, 2011 Board of Elementary and Secondary Education Mrs. Ollie Tyler, Acting Superintendent of Education Louisiana Department of Education The Bureau of Internal Audit (BIA) completed a semiannual audit of the State Department of Education’s (SDE) time and attendance records for the period ended December 31, 2010 as part of our ongoing responsibilities. The scope of this project included the following:

Reviewing SDE automated time and attendance procedures, Reviewing Department of State Civil Service payroll rules and procedures, Examining fixed time entry sheets and supporting documentation, Examining fixed time entry reports, and Testing all active employees in each unit of the selected SDE offices.

Our objectives included determining if:

time and attendance records are maintained timely and properly, overtime, leave, and prior period adjustments are properly administered and recorded, restricted appointment, student, and hourly employees are reported and paid properly, management has complied with requirements of Office of Management and Budget Circular A-87, terminations and resignations are properly and timely recorded, and management is properly reviewing time and attendance documents.

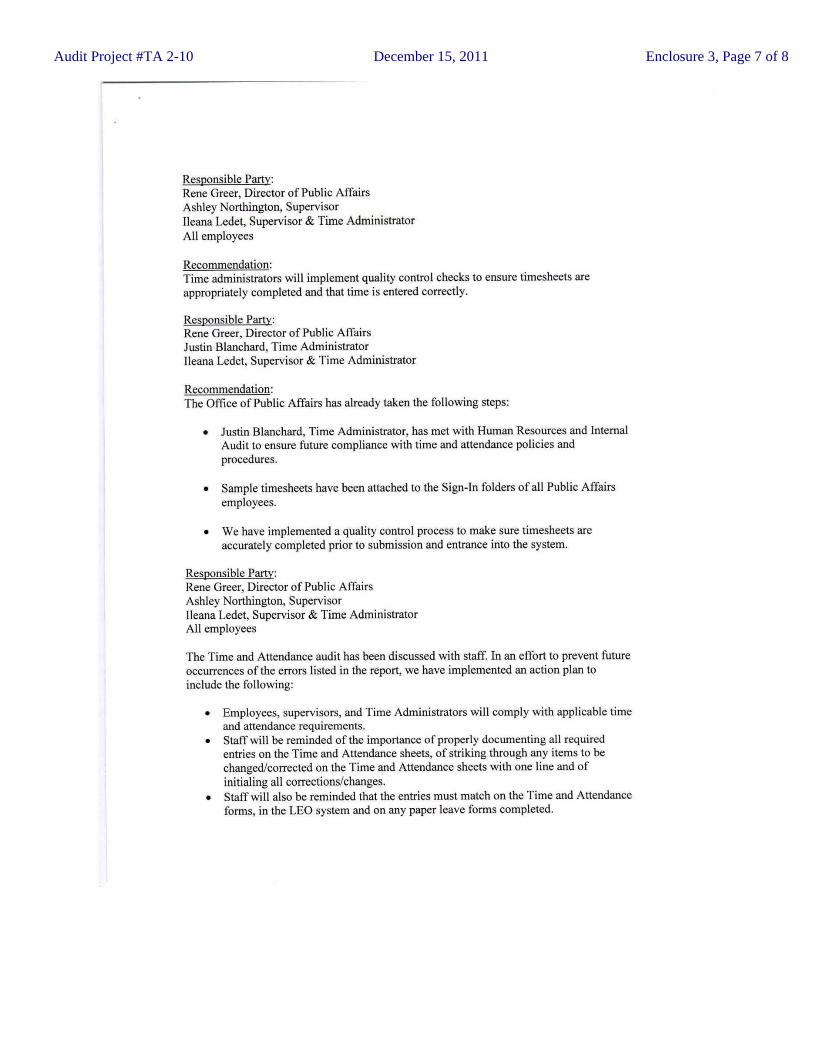

The attached report contains conclusions regarding overall performance of the Offices, as well as specific observations noted within each Office. Management’s responses and action plans to address the observations are included in Enclosures contained herein. The nature of these observations indicates the need for management to establish and preserve certain internal controls to ensure time and attendance records are maintained properly on a daily basis and in accordance with state and federal laws and regulations. In addition, management must ensure employees, supervisors, and timekeepers are following all procedures outlined in the Employees’ Policies and Procedures related to payroll time and attendance.

Respectfully submitted, Dudley J. Garidel, Jr. Director of Internal Audit

DJGJr/nrl Distribution:

Board of Elementary and Secondary Education (11) Ollie Tyler, Acting Superintendent Sharon Southall, Executive Management Officer Beth Scioneaux, Finance Rayne Martin, Innovations

Leslie Jewel, Appropriation Control, Division Director Debbie Schum, College and Career Readiness Catherine Pozniak, Executive Director, BESE Office of the State Inspector General

Office of the Legislative Auditor

“An Equal Opportunity Employer”

TABLE OF CONTENTS EXECUTIVE SUMMARY .......................................................................................... 1 AUDIT RESULTS & RECOMMENDATIONS (with Management’s Response) ............. 2 SPECIAL REVIEW OF RE-ORGANINZATIONAL UNIT/INNOVAITONS ......... 20 AUDIT SCOPE AND OBJECTIVES.......................................................................... 21 MANAGEMENT’S FORMAL RESPONSE ............................... ENCLOSURES 1 - 8

Audit Project #TA 2-10 December 15, 2011 Page 1

EXECUTIVE SUMMARY

Time and attendance audits are conducted semiannually as of June 30 and December 31. For each semiannual period, time and attendance procedures for one-half of the State Department of Education (SDE) Offices are examined to provide coverage to the entire SDE annually. This particular audit, therefore, included the following offices:

Executive Office Finance College and Career Readiness Departmental Support Innovations

Each employee and supervisor within each office was tested individually against forty (40) criteria based on federal and state laws and regulations, as well as SDE policies and procedures. In addition, timekeepers were tested for compliance with job responsibilities including safeguarding time records and accurate data entry. The following is a summary of unit scores within each office:

Office Exemplary Satisfactory Needs

Improvement Unsatisfactory

Executive office 0% 100% 0% 0%

Finance 0% 100% 0% 0%

College and Career Readiness 25% 75% 0% 0%

Innovations 20% 80% 0% 0%

Departmental Support 30% 70% 0% 0%

Overall, the following were areas of concern noted during the audit:

Payroll documentation does not present a clear, easily understandable record of all hours worked and leave taken by staff.

Scratch-outs/corrections are not initialed by the employee.

Leave slips are not electronically/manually submitted and approved for leave taken.

Timesheets do not match leave slip information reported on payroll reports.

Management using incorrect timesheets to record time and attendance.

Management not signing and dating timesheets for employees.

Inconsistencies of payroll documentation and card readers for building.

Audit Project #TA 2-10 December 15, 2011 Page 2

AUDIT RESULTS

Executive Office The Office of the Deputy Superintendent is under the direction of Sharon Southall, Executive Management Officer, for time and attendance purposes and administration and consisted of a total of 34 employees tested over two (2) pay periods.

Pay Period Units included in this audit: Supervisor(s)

August 23, 2010 – September 5, 2010

Deputy Undersecretary Ollie Tyler Governmental Affairs Paul Pastorek

Legal Joan Hunt

James Hrdlicka

Public Affairs Rene Greer Ileana Ledet Ollie Tyler

October 18, 2010 – October 31, 2010

Deputy Undersecretary Ollie Tyler Governmental Affairs Paul Pastorek Legal Joan Hunt

Jim Hrdlicka Public Affairs Rene Greer

Ileana Ledet Ollie Tyler

The following observations were noted during testing:

Deputy Undersecretary

2 instances of timekeepers not insuring all information is correct on employee timesheet (Supervisor – Ollie Tyler)

1 instance of timesheet not maintained on a daily basis. (Supervisor – Ollie Tyler)

1 instance payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken. (Supervisor – Ollie Tyler)

5 instances of incomplete timesheet. (Supervisor – Ollie Tyler)

Governmental Affairs

16 instances of timekeepers not insuring all information is correct on employee timesheet (Supervisor – Paul Pastorek)

10 instances of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken. (Supervisor – Paul Pastorek)

17 instances of student coding not documented on timesheet. (Supervisor – Paul Pastorek)

Audit Project #TA 2-10 December 15, 2011 Page 3

Public Affairs

2 instances of employee corrections not corrected properly. (Supervisor – Rene Greer)

10 instances of timesheets default costing not being filled out on timesheet. (Supervisor – Rene Greer)

5 instances of incomplete timesheet. (Supervisor – Rene Greer)

2 instances payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken. (Supervisor – Rene Greer)

1 instance of overtime not accurately recorded on time sheet. (Supervisor – Rene Greer)

1 instance of timesheets not maintained on a daily basis. (Supervisor – Rene Greer) Legal Services

2 instances of employee corrections not corrected properly. (Supervisor – Joan Hunt)

1 instance of employee not having prior approval for Leave without Pay. (Supervisor – James Hrdlicka)

1 instance of payroll documentation not matching payroll reports for Overtime. (Supervisor – James Hrdlicka)

1 instance of management payroll records not completed within the 30 days allotted for completion. (Supervisor – James Hrdlicka)

Audit Risks & Impact: The observations noted above increase risk for the SDE in the following manner if not addressed and corrected by management:

Incorrect pay to employees

Unauthorized overtime and/or leave

Noncompliance with Civil Service Payroll Rules and Regulations and other existing labor laws

Recommendation:

The Bureau of Internal Audit recommends management correct timesheets, leave slips, and associated backup documentation where appropriate; compile and implement a management action plan addressing each of the observations to prevent and detect future reoccurrences; and ensure all supervisors and staff comply with federal and state laws and regulations, as well as SDE policies and procedures Management Response:

Management concurs with observations and will implement corrections immediately.

Audit Project #TA 2-10 December 15, 2011 Page 4 Finance The Finance is under the direction of Beth Scioneaux, Deputy Superintendent for Management and Finance and consists of a total of 81 employees tested over two (2) pay periods.

Pay Period Units included in this audit: Supervisor(s)

August 23, 2010 – September 5, 2010

Appropriation Control Chief Educational Finance Human Resources

Leslie Jewell Mark Ott

Jane Sledge Patti Wallace

Beth Scioneaux Carlos Dickerson

Toni Gordon Priscilla Williams

Tracy Garcia Charlotte Stevens Marelle Houghton

Isabelle Olivier Nakia Jason

KimbraLamonte Mary Calivier Laura Lapeza

Rashaunda Matthews Paula Matherne Michele Staggs

Ruth Aron Monita Reed

October 18, 2010 – October 31, 2010

Appropriation Control Chief Educational Finance Human Resources

Leslie Jewell Mark Ott

Jane Sledge Patti Wallace

Carlos Dickerson Toni Gordon

Priscilla Williams Tracy Garcia

Beth Scioneaux Charlotte Stevens Marelle Houghton

Isabelle Olivier Nakia Jason

KimbraLamonte Mary Calivier Laura Lapeza

Rashaunda Matthews Paula Matherne Michele Staggs Beth Scioneaux

Ruth Aron Monita Reed

Audit Project #TA 2-10 December 15, 2011 Page 5 The following observations were noted, during testing:

Management and Finance

3 instances of timekeepers not insuring all information is correct on employee timesheet

45 instances of improperly correcting errors on timesheets

Management does not concur

Additional comments: Management response states Human Resources Timesheet Quick Tips Guide does not require, recommend, or even suggest corrections may only be made by drawing one line through the error; however Human Resources Timesheet Quick Tips Guide, on the employee intranet, states, as of November 8, 2011, in the Do’s and Don’ts section: “DON’T scratch thru an error but line thru and initial.”

In addition the Bureau of Internal Audit has given trainings along with Human Resources in which the information for making a correction on timesheet was given and this Quick Tips reference Guide was cited as being a source for compliance to making these corrections.

3 instances of employee not completing timesheets.

68 instances of timesheets default costing not being filled out on timesheet.

Management does not concur

Additional comments: Managements states uniformity as the basis for the response, however; due to inconsistencies noted in testing in which most employees fill out default costing while other do not. Bureau of Internal Audit recommends consistency within a division completing timesheets.

17 instances of timesheet not maintained on a daily basis.

Management does not concur

Additional comments: Managements states uniformity as the basis for the response; however, due to inconsistencies noted in testing in which most employees fill out default costing while others do not, the division is not consistent in completing timesheets. Bureau of Internal Audit recommends consistency within a division completing timesheets.

Audit Project #TA 2-10 December 15, 2011 Page 6

Management and Finance cont’d

1 instance of employee not recording coding on timesheet. (Supervisor – Charlotte Stevens)

Management does not concur

Additional comments: Managements states due to the employee working on a Sunday, coding was not necessary: however, the type of coding is essential due to determining paid overtime or compensatory time being awarded. Timesheets clearly state amount of overtime and type. Bureau of Internal Audit recommends consistency within a division in completing timesheets.

1 instance of employee with improper coding. ( Supervisor –Leslie Jewell)

Management does not concur

Additional comments: Management states the supervisor, employee, and time administrator understood the picture of all hours worked; however, coding should be readily apparent to anyone who reviews the timesheets which was not the case in instance because there was no coding on the timesheet.

1 instance of employee not submitting timesheet. (Supervisor – Michelle Staggs)

1 instance of employee not signing and dating at the end of pay period. (Supervisor – Michelle Staggs)

Audit Risks & Impact:

The observations noted above increase risk for the SDE in the following manner if not addressed and corrected by management:

Civil liability and penalties for noncompliance with the FLSA

Questioned costs - Federal grants

Incorrect charge of leave to employee

Incorrect pay to employees

Noncompliance with Civil Service Payroll Rules and Regulations and other existing labor laws

Recommendation:

The Bureau of Internal Audit recommends management correct timesheets, leave slips, and associated backup documentation where appropriate; compile and implement a management action plan addressing each of the observations to prevent and detect future reoccurrences; and ensure all supervisors and staff comply with federal and state laws and regulations, as well as SDE policies and procedures

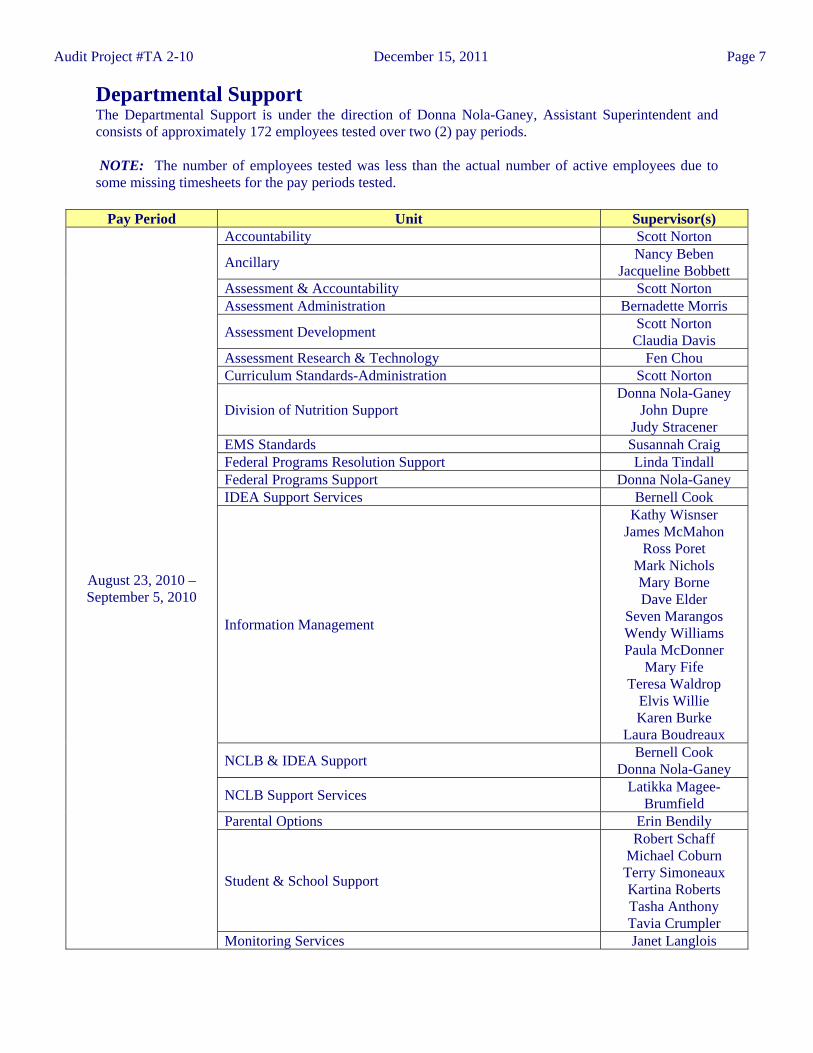

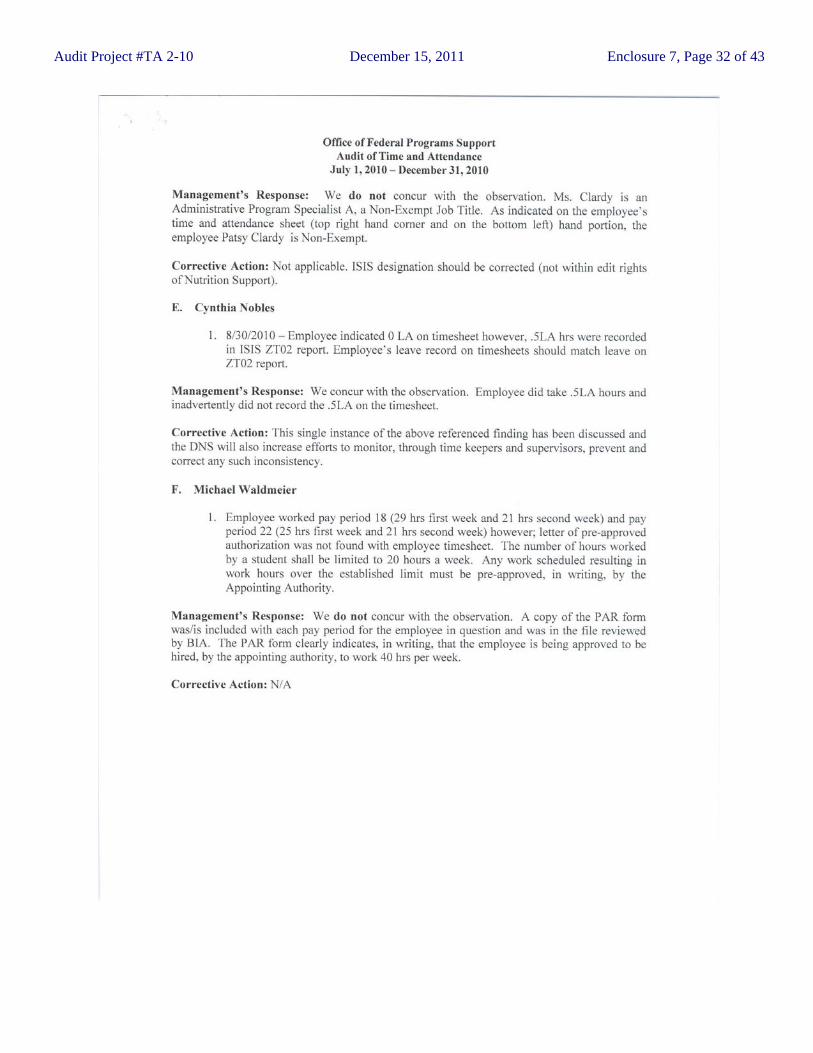

Audit Project #TA 2-10 December 15, 2011 Page 7 Departmental Support The Departmental Support is under the direction of Donna Nola-Ganey, Assistant Superintendent and consists of approximately 172 employees tested over two (2) pay periods. NOTE: The number of employees tested was less than the actual number of active employees due to some missing timesheets for the pay periods tested.

Pay Period Unit Supervisor(s)

August 23, 2010 – September 5, 2010

Accountability Scott Norton

Ancillary Nancy Beben

Jacqueline Bobbett Assessment & Accountability Scott Norton Assessment Administration Bernadette Morris

Assessment Development Scott Norton

Claudia Davis Assessment Research & Technology Fen Chou Curriculum Standards-Administration Scott Norton

Division of Nutrition Support Donna Nola-Ganey

John Dupre Judy Stracener

EMS Standards Susannah Craig Federal Programs Resolution Support Linda Tindall Federal Programs Support Donna Nola-Ganey IDEA Support Services Bernell Cook

Information Management

Kathy Wisnser James McMahon

Ross Poret Mark Nichols Mary Borne Dave Elder

Seven Marangos Wendy Williams Paula McDonner

Mary Fife Teresa Waldrop

Elvis Willie Karen Burke

Laura Boudreaux

NCLB & IDEA Support Bernell Cook

Donna Nola-Ganey

NCLB Support Services Latikka Magee-

Brumfield Parental Options Erin Bendily

Student & School Support

Robert Schaff Michael Coburn Terry Simoneaux Kartina Roberts Tasha Anthony Tavia Crumpler

Monitoring Services Janet Langlois

Audit Project #TA 2-10 December 15, 2011 Page 8

Pay Period Unit Supervisor(s) Ellen Spears

Planning & Reporting Services Evelyn Johnson Standards, Assessment & Accountability Scott Norton

October 18, 2010 – October 31, 2010

Accountability Scott Norton

Ancillary Nancy Beben

Jacqueline Bobbett Assessment & Accountability Scott Norton Assessment Administration Bernadette Morris

Assessment Development Scott Norton

Claudia Davis Assessment Research & Technology Fen Chou Curriculum Standards-Administration Scott Norton

Division of Nutrition Support

Donna Nola-Ganey John Dupre

Judy Stracener EMS Standards Susannah Craig Federal Programs Resolution Support Linda Tindall Federal Programs Support Donna Nola-Ganey IDEA Support Services Bernell Cook

Information Management

Kathy Wisnser James McMahon

Ross Poret Mark Nichols Mary Borne Dave Elder

Seven Marangos Wendy Williams Paula McDonner

Mary Fife Teresa Waldrop

Elvis Willie Karen Burke

Laura Boudreaux

NCLB & IDEA Support Bernell Cook

Donna Nola-Ganey

NCLB Support Services Latikka Magee-

Brumfield Parental Options Erin Bendily

Student & School Support

Robert Schaff Michael Coburn Terry Simoneaux Kartina Roberts Tasha Anthony Tavia Crumpler

Monitoring Services Janet Langlois Ellen Spears

Planning & Reporting Services Evelyn Johnson Standards, Assessment & Accountability Scott Norton

Audit Project #TA 2-10 December 15, 2011 Page 9 In addition, the following observations were noted during testing:

Accountability

1 instance of employee corrections not corrected properly (Supervisor – Scott Norton)

1 instance of timesheets default costing not filled out on timesheet (Supervisor – Scott Norton)

Ancillary Resources

2 instances of corrections not being initialed by employee (Supervisor – Jacqueline Bobbett)

1 instance of timesheet not maintained on a daily basis (Supervisor – Jacqueline Bobbett) Assessment & Accountability

1 instance of employee corrections not corrected properly(Supervisor – Scott Norton)

2 instances of timekeepers not insuring all information is correct on employee timesheet (Supervisor – Scott Norton)

2 instances of students working more than the 20 hrs allotted without prior written approval by appointing authority. (Supervisor – Scott Norton)

1 instance of timesheet not maintained on a daily basis (Supervisor – Scott Norton)

Assessment Administration

5 instances of corrections not initialed by employee (Supervisor – Bernadette Morris)

1 instance of proper supervisory approval not noted for Leave without Pay. (Supervisor – Bernadette Morris)

Assessment Development

3 instances of corrections not being initialed by employee (Supervisor – Scott Norton)

1 instance of timesheet and ZT02 report inconsistent. (Supervisor – Scott Norton)

2 instances of timesheets default costing not being filled out on timesheet (Supervisor – Scott Norton)

Additional comments: Managements states uniformity as the basis for the response; however, due to inconsistencies noted in testing in which most employees fill out default costing while others do not, the division is not consistent in completing timesheets. Bureau of Internal Audit recommends consistency within a division completing timesheets.

1 instance of proper supervisory approval not noted for Leave without Pay. (Supervisor – Claudia Davis)

1 instance of incorrect recording of timesheet. (Supervisor - Claudia Davis) Assessment Research & Technology

3 instances of corrections not initialed by employee (Supervisor – Fen Chou)

Audit Project #TA 2-10 December 15, 2011 Page 10

2 instances of timesheet and ZT02 report inconsistent. (Supervisor – Fen Chou)

1 instance of Non-exempt employee not signing out for lunch. (Supervisor – Fen Chou)

Management does not concur

Additional comments: Management states compensatory time is not owed to this employee due to the fact employee was relieved of duties during his/her lunch break and had neglected to sign out. Fair Labor Standards Act (FLSA) regulations state: Non-exempt employees must sign in upon arrival, departure and in/out from lunch each day. Due to employee not signing in/out for lunch it is undetermined whether employee is owed compensatory time according to the rule and regulations set forth within FLSA.

Curriculum Standards

1 instance of timesheets default costing not filled out on timesheet (Supervisor – Scott Norton)

Elementary/Middle/Secondary Standards

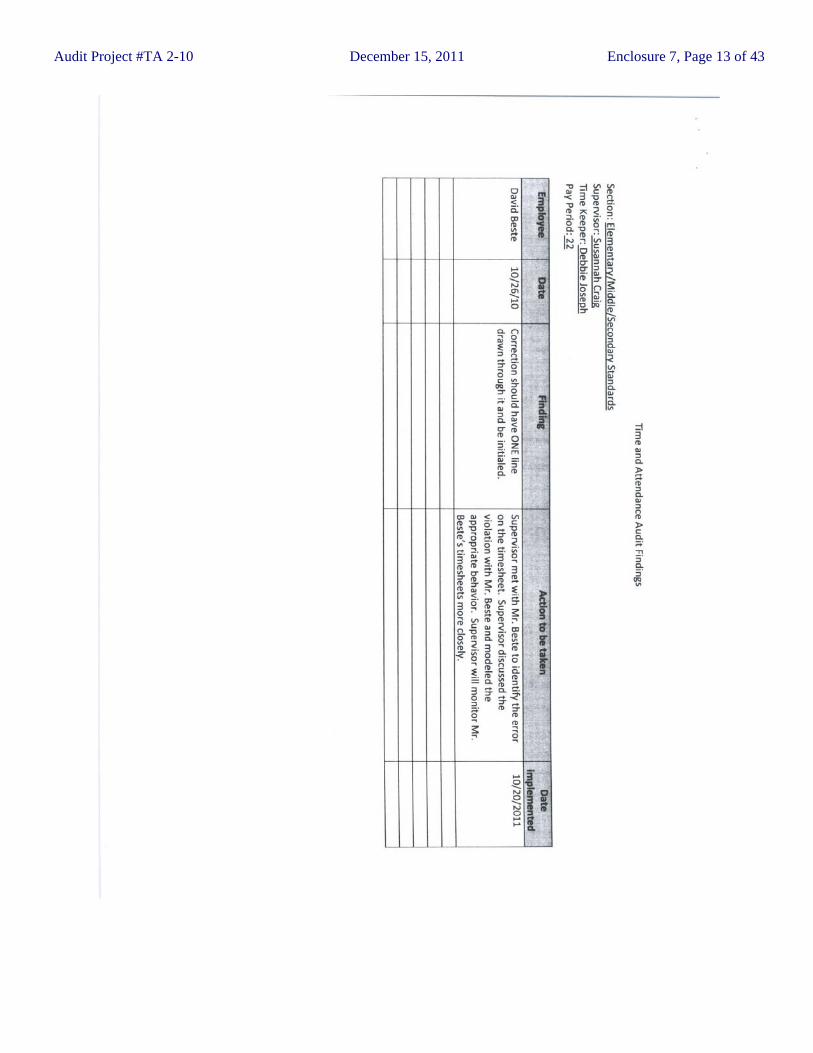

1 instance of employee corrections not corrected properly(Supervisor – Susannah Craig) Division of Nutrition Support

Division using unapproved timesheets for all employees. (Supervisor – John Dupre)

Management does not concur

Additional comments: Management states emails from Human Resources as approval for using this timesheet. Bureau of Internal Audit review of email indicates email does not give approval for this timesheet to be used but, rather the Human Resource Director liked it and would have used it in lieu of, than the current one in use by LDOE employees. EP 3.2 states clearly: the same standard timesheet will be used by all employees, except those exempt from completing timesheets, whether the employee has A-87 reporting requirements or not.

8 instances of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken. (Supervisor – Judy Stracener)

Management does not concur

Additional comments: Management stated they will take corrective action to assist in clarifying timesheets. Bureau of Internal Audit believes due to unauthorized timesheets being used in this division, the coding was unclear. EP 3.2 states: the same standard timesheet will be used by all employees, except those exempt from completing timesheets, whether the employee has A-87 reporting requirements or not.

Audit Project #TA 2-10 December 15, 2011 Page 11

Division of Nutrition Support cont’d

1 instance of timesheet and ZT02 report inconsistencies. (Supervisor – Judy Stracener)

2 instances of student working more than 20 hours without prior written approval by Appointing Authority. (Supervisor – John Dupre)

Management does not concur

Additional comments: Management states Position Action Request form as approval. EP 7.10. However, this was not included with the requested supporting documentation for the six month audit; therefore, the BIA was not able to review the documentation during the audit.

Federal Programs

1 instance of employee corrections not corrected properly. (Supervisor – Donna Nola-Ganey)

Federal Programs Resolution Support

1 instance of employee corrections not corrected properly. (Supervisor – Linda Tindall)

1 instance of timesheet and ZT02 report inconsistencies. (Supervisor – Linda Tindall) IDEA Support Services

1 instance of employee corrections not corrected properly. (Supervisor – Bernell Cook) Information Management

42 instances of employee corrections not corrected properly. (Supervisors –James Wilson. Elvis Willie, Rajeswari Mani, Mary Fife, Teresa Waldrop, Steven Maragos, James McMahon, Paula McDonner, Wendy Williams, Dave Elder, Ross Poret, Mary Borne, Laura Boudreaux)

7 instances of timesheets not maintained on a daily basis (Supervisor – Laura Boudreaux, Dave Elder, Mary Fife, James McMahon, Kathy Wisner, Ross Poret)

5 instances of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken.

1 instance of employee corrections not corrected properly. (Supervisors – Mary Fife, James McMahon, Teresa Waldrop)

1 instance of employee’s signature and date not recorded at the end of the pay period (Supervisor – Mary Fife)

1 instance of overtime hours not accurately recorded on timesheet (Supervisor- Elvis Willis)

13 instances of default costing not filled out on timesheet (Supervisor – Elvis Willis, Mary Fife, James McMahon, Ross Poret, Laura Boudreaux, Mark Nichols, Dave Elder, )

2 instances of timesheet and ZT02 report inconsistencies (Supervisor - Mary Fife, Kathy Wisner)

Audit Project #TA 2-10 December 15, 2011 Page 12

Information Management cont’d

1 instance of original management signature and date was not on timesheet (Supervisor – Karen Burke)

1 instance of student working more than 20 hours without prior written approval by Appointing Authority (Supervisor - Wendy Williams)

NCLB &IDEA Support

1 instance of timesheets not maintained on a daily basis (Supervisor – Bernell Cook)

1 instance of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken. (Supervisor – Bernell Cook)

1 instance employee’ scheduled hours not documented on timesheet (Supervisor – Walter Atterberry, Valerie Triggs, Janet Langlois)

2 instances of default costing not filled out on timesheet (Supervisor – Donna Nola- Ganey, Bernell Cook)

NCLB Support Services

1 instance of default costing not filled out on timesheet not being maintained on a daily basis (Supervisor – Latikka Magee-Brumfield)

Parental Options

1 instance of timesheets not maintained on a daily basis (Supervisor – Erin Bendily)

1 instance of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken (Supervisor- Erin Bendily)

1 instance of employee corrections not corrected properly (Supervisor – Erin Bendily)

Management does not concur

Additional comments: Management response states due to the time being identifiable they do not concur with this finding; however, Human Resources Timesheet Quick Tips Guide, on the employee intranet, states, as of November 8, 2011, in the Do’s and Don’ts section: “DON’T scratch thru an error but line thru and initial.”

In addition the Bureau of Internal Audit has given trainings along with Human Resources in which the information for making a correction on timesheet was given and this Quick Tips reference Guide was cited as being a source for compliance to making these corrections.

Audit Project #TA 2-10 December 15, 2011 Page 13

Parental Options cont’d

2 instances of Non-exempt employee not signing out for lunch. (Supervisor – Erin Bendily)

Management does not concur

Additional comments: Management states compensatory time is not owed to this employee due to the fact that employee was relieved of duties during his/her lunch break and had neglected to sign out. Fair Labor Standards Act (FLSA) regulations as state: Non-exempt employees must sign in upon arrival, departure and in/out from lunch each day. Due to employee not signing in/out for lunch it is undetermined whether employee is owed compensatory time according to the rule and regulations set forth within FLSA.

1 instance of leave slip not submitted for leave taken (Supervisor - Erin Bendily)

1 instance of timesheet and ZT02 report inconsistencies (Supervisor - Erin Bendily)

2 instances of timekeepers not ensuring all information is correct on employee timesheet basis (Supervisor – Erin Bendily)

Student & /School Learning Support

5 instances of timesheets not maintained on a daily basis (Supervisor – Donna Nola- Ganey)

7 instances of employee corrections not corrected properly(Supervisor – Robert Schaff, Michael Coburn, Terri Simoneaux, Tasha Anthony, Tavia Crumpler)

2 instances of payroll documentation not presenting a clear, easily understandable record of all hours worked and leave taken (Supervisor - Robert Schaff)

2 instances of leave slip was not submitted for leave taken (Supervisor - Robert Schaff)

3 instances of default costing not filled out on timesheet (Supervisor – Robert Schaff, Kartina Roberts)

3 instances of timesheet and ZT02 report inconsistencies (Supervisor – Michael Coburn, Terri Simoneaux, Kartina Roberts)

Planning and Reporting Services

Pay period 22 timesheets were not available upon request.

Management does not concur

Additional comments: EP 3.2 states the Bureau of Internal Audit is responsible for conducting random and scheduled audits of time and attendance records for division/units. Records must be made available immediately upon request.

Audit Project #TA 2-10 December 15, 2011 Page 14 Audit Risks & Impact: The observations noted above increase risk for the SDE in the following manner if not addressed and corrected by management:

Civil liability and penalties for noncompliance with the FLSA

Unauthorized leave

Unauthorized overtime

Incorrect charge of leave to employee

Incorrect pay to employees

Noncompliance with Civil Service Payroll Rules and Regulations and other existing labor laws

Recommendation:

The Bureau of Internal Audit recommends management correct timesheets, leave slips, and associated backup documentation where appropriate; compile and implement a management action plan addressing each of the observations to prevent and detect future reoccurrences; and ensure all supervisors and staff comply with federal and state laws and regulations, as well as SDE policies and procedures

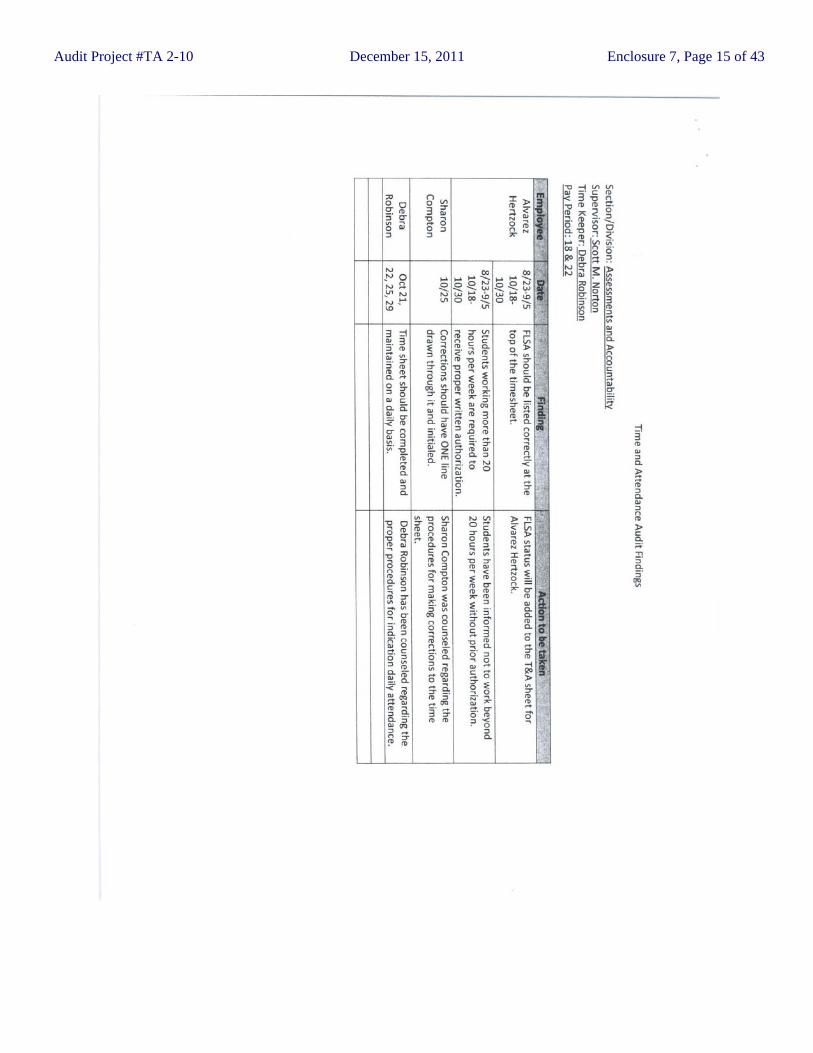

Audit Project #TA 2-10 December 15, 2011 Page 15 College and Career Readiness College and Career Readiness is under the direction of Debbie Shum, Superintendent, for time and attendance purposes and administration and consisted of a total of 33 employees tested over two (2) pay periods.

Pay Period Units included in this audit: Supervisor(s)

August 23, 2010 – September 5, 2010

DOP – Special Ed East - West Executive Org Support Louisiana Virtual Schools

Dianna Keller Paul Theriot James Owens

Wendy Thibodeaux Nancy Hicks

Tiffanye Thomas

October 18, 2010 – October 31, 2010

DOP – Special Ed East - West Executive Org Support Louisiana Virtual Schools

Debbie Shum Paul Theriot James Owens

Wendy Thibodeaux Nancy Hicks

Tiffanye Thomas College and Career Readiness

12 instances of employee corrections not corrected properly (Supervisor – Debbie Shum, Dianna Keller, Paul Theriot, James Owens, Wendy Thibodeaux, Nancy Hicks, Alan Gauthreaux)

12 instances of payroll documentation not presenting a clear easily understandable record of all hours worked or leave taken. (Supervisors – Wendy Thibodeaux, Nancy Hicks, James Owens, Debbie Shum, Paul Theriot)

2 instances of timesheets not being maintained on a daily basis (Supervisor – Paul Theriot, Debbie Shum)

3 instances of timekeepers not insuring all information is correct on employee timesheet (Supervisor – Debbie Shum)

1 instance of leave slip and ZT02 report inconsistencies. (Supervisor – Debbie Shum)

1 instance of special leave supporting documentation not attached to time and attendance packet. (Supervisor – Debbie Shum)

1 instance of employee not having prior approval for Leave without Pay. (Supervisor – Debbie Shum)

Audit Project #TA 2-10 December 15, 2011 Page 16 Audit Risks & Impact: The observations noted above increase risk for the SDE in the following manner if not addressed and corrected by management:

Civil liability and penalties for noncompliance with the FLSA

Unauthorized leave

Incorrect charge of leave to employee

Incorrect pay to employees

Noncompliance with Civil Service Payroll Rules and Regulations and other existing labor laws

Recommendation:

The Bureau of Internal Audit recommends management correct timesheets, leave slips, and associated backup documentation where appropriate; compile and implement a management action plan addressing each of the observations to prevent and detect future reoccurrences; and ensure all supervisors and staff comply with federal and state laws and regulations, as well as SDE policies and procedures Management Response:

Management concurs with observations and will implement corrections immediately.

Audit Project #TA 2-10 December 15, 2011 Page 17 Innovations Innovations under the direction of Rayne Martin, Deputy Superintendent, for time and attendance purposes and administration and consisted of a total of 33 employees tested over two (2) pay periods.

Pay Period Units included in this audit: Supervisor(s)

August 23, 2010 – September 5, 2010

Certification, Preparation & Recruitment

Terry Rinaudo Andrew Vaughan

Ollie Tyler Elizabeth Shaw

Educator Support Patrice Saucier Elizabeth Shaw

Human Capital Elizabeth Shaw

Ollie Tyler

School Turnaround Stephanie Carlos Nicole Honore Patrick Weaver

TAP Patrice Saucier Shelia Talamo

October 18, 2010 – October 31, 2010

Certification, Preparation & Recruitment

Terry Rinaudo Andrew Vaughan

Ollie Tyler Elizabeth Shaw

Educator Support Patrice Saucier Elizabeth Shaw

Human Capital Elizabeth Shaw

Ollie Tyler

School Turnaround Stephanie Carlos Nicole Honore Patrick Weaver

TAP Patrice Saucier Shelia Talamo

Audit Project #TA 2-10 December 15, 2011 Page 18

Innovations

15 instances of employee corrections not corrected properly (Supervisor – Terry Rinaudo, Andrew Vaughan, Ollie Tyler, Patrice Saucier, Elizabeth Shaw, Rayne Martin, Nicole Honore)

Management does not concur

Additional comments: Additional comments: Management response states Human Resources Timesheet Quick Tips Guide does not require, recommend, or even suggest corrections may only be made by drawing one line through the error; however Human Resources Timesheet Quick Tips Guide, on the employee intranet, states, as of November 8, 2011, in the Do’s and Don’ts section: “DON’T scratch thru an error but line thru and initial.”

In addition the Bureau of Internal Audit has given trainings along with Human Resources in which the information for making a correction on timesheet was given and this Quick Tips reference Guide was cited as being a source for compliance to making these corrections.

4 instances of timesheets default costing not being filled out on timesheet. (Supervisor – Terry Rinaudo, Andrew Vaughan, Ollie Tyler, Patrice Saucier, Elizabeth Shaw, Rayne Martin, Nicole Honore)

Management does not concur

Additional comments: Managements states this creates an undue burden; however, our testing indicates a lack of consistencies in completing timesheets because most employees fill out default costing, while other does not. Bureau of Internal Audit recommends consistency within a division completing timesheets.

2 instances of timesheets not being maintained on a daily basis (Supervisor – Terry Rinaudo, Andrew Vaughan, Ollie Tyler, Patrice Saucier, Elizabeth Shaw, Rayne Martin, Nicole Honore)

Management does not concur

Additional comments: Employee handwriting was unidentifiable by audit staff. EP 3.2 states payroll documentation should present a clear, easily understandable record of all hours worked and leave taken by staff.

2 instances of timekeepers not insuring all information is correct on employee timesheet (Supervisor – Rayne Martin)

1 instance of overtime not preapproved by appointing authority. Supervisor – Rayne Martin)

2 instances of management not signing and dating timesheets. (Supervisor – Rayne Martin)

Audit Project #TA 2-10 December 15, 2011 Page 19 Audit Risks & Impact: The observations noted above increase risk for the SDE in the following manner if not addressed and corrected by management:

Civil liability and penalties for noncompliance with the FLSA

Unauthorized leave

Incorrect charge of leave to employee

Incorrect pay to employees

Noncompliance with Civil Service Payroll Rules and Regulations and other existing labor laws

Recommendation:

The Bureau of Internal Audit recommends management correct timesheets, leave slips, and associated backup documentation where appropriate; compile and implement a management action plan addressing each of the observations to prevent and detect future reoccurrences; and ensure all supervisors and staff comply with federal and state laws and regulations, as well as SDE policies and procedures

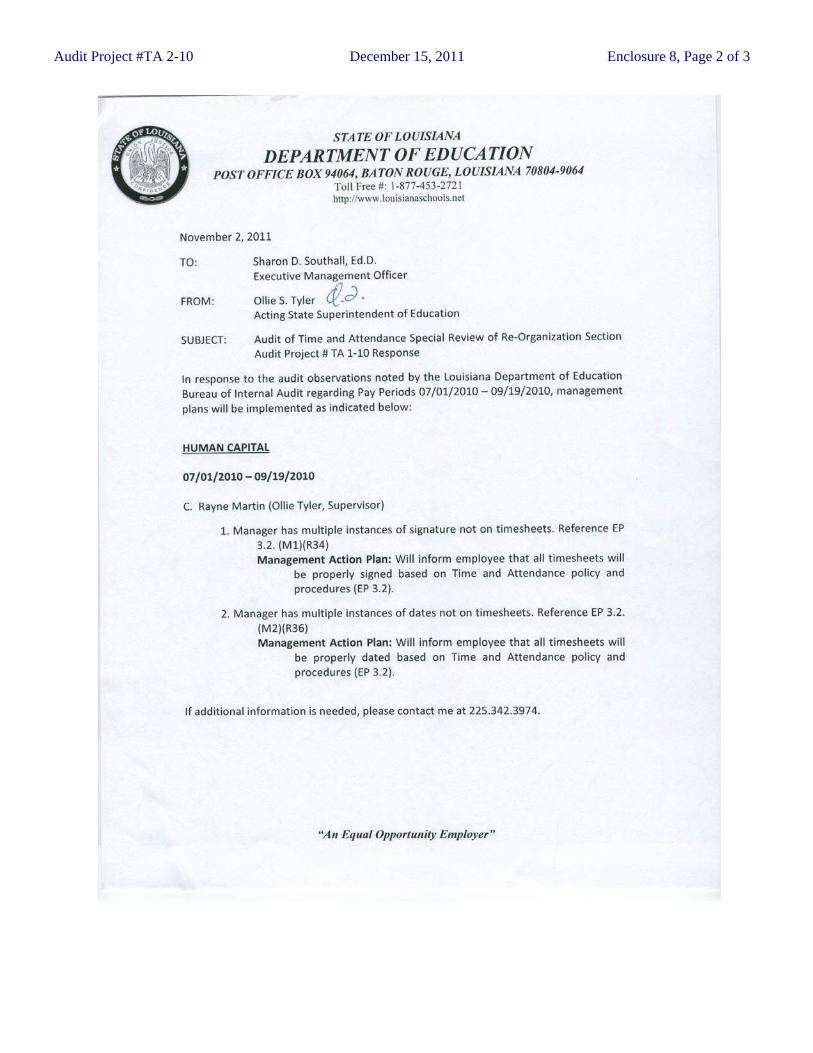

Audit Project #TA 2-10 December 15, 2011 Page 20 Special Review of Re-Organizational Unit / Innovations During the course of the regular semi-annual Time and Attendance audit, Bureau of Internal Audit noticed some inconsistencies that lead to further review of Human Capital. The inconsistencies were related to two employees and the supervisor. The dates reviewed were July 1, 2011 – September 19, 2011.

Molly Horstman 14 mostly consecutive instances of employee’s hours on the timesheet and

the cardholder scanner were inconsistent

Management does not concur

Additional comments: Management states the immediate supervisor gave work from home approval; however, on July 15, 2011 Bureau of Internal Audit contacted the immediate supervisor for supporting documentation related to employee’s work from home status and received a response back no one had approval to work from home. Furthermore, the immediate supervisor does not have the authority to give approval for this request. Approval can only be given by the Department of Education Superintendent, who had not been given this approval to anyone as of the dates in question.

1 instances of no activity on the cardholder transaction history report but

the employee claimed 4 hours of annual leave. Employee’s timesheet is not completed and maintained on a daily basis.

LaTanya Walker

19 mostly consecutive instances of employee’s hours on the timesheet and the cardholder scanner were inconsistent.

Management does not concur

Additional comments: Management states the immediate supervisor gave work from home approval; however, on July 15, 2011 Bureau of Internal Audit contacted the immediate supervisor for supporting documentation related to employee’s work from home status and received a response back no one had approval to work from home. Furthermore, the immediate supervisor does not have the authority to give approval for this request. Approval can only be given by the Department of Education Superintendent, who had not been given this approval to anyone as of the dates in question.

3 instances of the timesheet not being maintained on a daily basis. Employee has multiple instances of inconsistencies in irregular work

hours.

Audit Project #TA 2-10 December 15, 2011 Page 21

AUDIT SCOPE AND OBJECTIVES

Time and attendance audits are conducted semiannually as of June 30 and December 31. For each semiannual period time and attendance procedures for one-half of the State Department of Education (SDE) Offices are examined to provide coverage to the entire SDE annually. This particular audit included the following offices:

Office of the Deputy Superintendent Office of Educator Support Special School District

The scope of this project included the following:

Reviewing SDE automated time and attendance procedures, Reviewing Department of State Civil Service payroll rules and procedures, Examining fixed time entry sheets and supporting documentation, Examining fixed time entry reports, and Testing all active employees in each unit of the selected SDE offices.

Our objectives included determining if:

time and attendance records are maintained timely and properly, overtime, leave, and prior period adjustments are properly administered and recorded, restricted appointment, student, and hourly employees are reported and paid properly, management has complied with requirements of OMB Circular A-87, terminations and resignations are properly and timely recorded, and management is properly reviewing time and attendance documents

In order to accomplish our objectives each employee and supervisor within each office was tested individually against forty (40) criteria based on federal and state laws and regulations as well as SDE policies and procedures. In addition, timekeepers were tested for compliance with job responsibilities including safeguarding time records and accurate data entry.

The recommendations in this report represent, in our judgment, those most likely to bring about beneficial improvements to the administration of time and attendance in the offices audited. The varying nature of the recommendations, their implementation costs, and potential impact on operations of the SDE should be considered in reaching decisions on courses of action. Follow-up on management action plans will be conducted on a semiannual cyclical basis. Our audit was conducted in accordance with The Standards for the Professional Practice of Internal Auditing and the Code of Ethics issued by the Institute of Internal Auditors. By provisions of state law, this report is a public document, and it has been distributed to appropriate public officials.

Audit Project #TA 2-10 December 15, 2011 Page 22 We acknowledge with appreciation the courtesies extended to our representatives during the review.

_________________________ Dudley J. Garidel, Jr. Director of Internal Audit

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 1 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 2 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 3 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 4 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 5 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 1, Page 6 of 6

Audit Project #TA 2-10 December 15, 2011 Enclosure 2, page 1 of 1

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, page 1 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 2 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 3 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 4 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 5 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 6 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 7 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 3, Page 8 of 8

Audit Project #TA 2-10 December 15, 2011 Enclosure 4, page 1 of 2

Audit Project #TA 2-10 December 15, 2011 Enclosure 4, Page 2 of 2

Audit Project #TA 2-10 December 15, 2011 Enclosure 5, page 1 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 5, Page 2 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 5, Page 3 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 5, Page 4 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 6, page 1 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 6, Page 2 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 6, Page 3 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 6, Page 4 of 4

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 1 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 2 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 3 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 4 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 5 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 6 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 7 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 8 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 9 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 10 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 11 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 12 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 13 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 14 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 15 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 16 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 17 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 18 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 19 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 20 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 21 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 22 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 23 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 24 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 25 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 26 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 27 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 28 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 29 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 30 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 31 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 32 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 33 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 34 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 35 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 36 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 37 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 38 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 39 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 40 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 41 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 42 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 7, Page 43 of 43

Audit Project #TA 2-10 December 15, 2011 Enclosure 8, Page 1 of 3

Audit Project #TA 2-10 December 15, 2011 Enclosure 8, Page 2 of 3

Audit Project #TA 2-10 December 15, 2011 Enclosure 8, Page 3 of 3