thomas winfield november 5, 2016 - files.meetup.comfiles.meetup.com/18528044/multifamily investing...

TRANSCRIPT

Multifamily Investing for Newbies

Thomas WinfieldNovember 5, 2016

• This is not a solicitation, endorsement or offer

•Nothing in this presentation is meant to be Legal, Tax or Financial advice• Consult your Lawyer for legal advice• Consult your Tax Advisor for Tax advice• Consult your Financial Advisor for Financial advice

Our Philosophy

• Buy and Hold (2-5 Years)

• Risk Appropriate Investments• Rigorous Due Diligence

• Appropriate Leverage

• Data/Metrics Driven vs. Hype Driven

Topics

•Market Analysis

•Property Analysis/Due Diligence

• Finance

• Exit Strategy

• The Plan and the Team

Market Analysis

Criteria for Selecting a Market

• Population Growth• Primarily from Net Migration• States With Large and Growing Populations

• Workforce• Income Growth• Educated Workforce

• Gross Domestic Product (GDP)/GSP• Diversified Economic Base• Good Debt Rating

• RE Cycle Phase• Real Estate Prices Not Volatile

Virtuous Circle for Economic Growth

Population Growth

Talented Workforce

Increase in Job OpeningsIncome Growth

A Growing Population and Talented Workforce Creates a Demand for Real Estate

The Population of the South and West is Increasing Faster Than the Northeast and Midwest

Howdy Y’all

Follow the People

States with higher net migration are best for real estate investors

The Real Estate Cycle Tracks the Economic Cycle

• Cycle has Peaks and Troughs

• Next Peak is Generally Higher than Past Peaks

• Goal is to Survive one Cycle

• Focus on the Trend Line

I Believe the Market Is Going to Fluctuate– J. P. Morgan

Recovery Phase

Expansion Phase

Recession Phase

Contraction Phase

Above Long Term Average Occupancy

Below Long Term Average Occupancy

Rents are Increasing Rents are Decreasing

Buy Here

Sell Here

In What Phase of the RE Cycle is Your Market

States With Best Long Term Prospect for Buy and Hold Multifamily Investors

South

• North Carolina

• South Carolina

• Florida

Western

• Colorado

• Utah

• California

• Nevada

• Washington

• Oregon

• Georgia

• Texas

Property Analysis and Due Diligence

Due Diligence - Definition1. An investigation or audit of a potential investment. Due diligence serves to confirm all material facts in regards to a sale.

2. Generally, due diligence refers to the care a reasonable person should take before entering into an agreement or a transaction with another party.

Types of Due Diligence

• Sub Market

• Financial

• Physical

• Legal

Time

Market Due Diligence Should Proceed all Other Due Diligence

Important Metrics

• Cash on Cash Return

• Cap Rate

• Vacancy Rate

• Expense as a % of Income

• Median Income

• Median Rents

Long Beach Sub Markets Price Per Unit

Long Beach Market Median Price is $200K Per Unit

Long Beach Sub Market Price Per Square Foot

Long Beach Market Median Price is $275 Per Square Foot

Rents and Vacancies

Financial Due Diligence-Valuation

• Appraisal/Broker Opinion of Value

• Metrics• Price Per Unit

• Price Per Square Foot

• Vacancy Rate

• Property Sales History

These values should be compared to the Market/submarket norms

Financial Due Diligence-Income• Income Statement

• Rents

• Other Income

• Rent Rolls (Past 3 years)• Review All Leases

• Tenant Background

• Obtain Tenant Estoppel Certificates

Financial Due Diligence- Expenses

• Property Tax

• Insurance Policy

• Security Deposits

• Utility Deposits

• Loan Documents (if assuming loan)

• Utility Bills

• Existing Contracts (Property Managers, Maintenance, etc.)

Legal Due Diligence• Seller Listing Agreement

• What’s Included in the Sale• What are the conditions of the

purchase

• Purchase Agreement (RIPA)• What are you Offering• What are the conditions of the

purchase

• Seller Disclosures• Title

• Who Owns Property• How is Title Held

• Deed• Covenants, Conditions & Restrictions

(CC&Rs)• Ownership Rights

• Litigation History• Liens

• Recorded• Unrecorded

Legal Due Diligence-Governing Bodies

• Zoning

• Rent Ordinances• Rent Control

• Number of Occupants

• Etc.

• Building Permits

• Easements

Is this Property Suitable for it’s Intended Use?

Physical Due Diligence• Location

• Class/Age• A (0-15)• B (15-30)• C (30-45)

• Building Inspection Report • Roofing• Plumbing• Electrical• HVAC• Mold Inspection Report

• Capital Improvement History

• Deferred Maintenance

• Environmental Reports

• Engineering Report

• Lead Paint

Physical Due Diligence

Financing

Why Borrow Money-The Power of Leverage

Non-Leveraged

• $10,000 to Invest

• 5% Interest

• Amount Returned ($10,000*.05)=$500

• Return 5%

Leveraged Investment

• $10,000 to Invest

• 80% Loan to Value (20% Down)

• 5% Interest

• Purchase Power = $10,000/.2 = $50,000

• Amount Returned ($50,000*.05) = $2,500

• Return 25%

Time is on your Side

• Starting Early is Most Effective

• Appropriate Use of Leverage Accelerates the Effect of Compounding

Where Does Real Estate Financing Come From

• Savings• Seller Financing• Conventional Loans• Commercial Loans• Hard Money• Private Money• Portfolio Lenders• FHA/HUD Programs• Home Equity Loans and Lines of

Credit• Self-directed IRAs

• Development Loan, Construction Loan

• 1031 Exchange• Partnerships• REITS• Crowdfunding• Syndications

Sources of Funds -Direct Lenders

• Credit Unions

• Savings and Loans

• Banks

• Portfolio--loans are funded by a bank or other institutionalized lender which does not securitize or sell their loans into capital markets.

• Terms may be more flexible than a securitized loan and it is typically serviced by the lender.

• Securitized loans are pooled and sold on the secondary market.

Sources of Funds -Private Lenders

• Your Rich Uncle

• High Net Worth Individuals

• Someone’s IRA

• Crowdfunding

• Sellers

Mortgage Brokers Can Help You Find Money

• An intermediary who brings mortgage borrowers and mortgage lenders together.

• A mortgage broker collects an origination fee and/or a yield spread premium from the lender as compensation for its services.

Borrower Mortgage Broker

Lender # 1

Lender # N

.

.

.

.

.Loan Application

Borrower’s Liability

• Recourse Loan-A type of loan that allows a lender to seek financial damages if the borrower fails to pay the liability, and if the value of the underlying asset is not enough to cover it. A recourse loan allows the lender to go after the debtor's assets that were not used as loan collateral in case of default.

• Non-Recourse Loan-A type of loan that is secured by collateral, which is usually property. If the borrower defaults, the issuer can seize the collateral, but cannot seek out the borrower for any further compensation, even if the collateral does not cover the full value of the defaulted amount unless there is fraud involved

Important Metrics for Lenders

• Net operating income: The annual income, minus expenses that a property generates from its operations

• Debt service coverage: Measure of NOI relative to debt payment obligations

• Loan-to-value (LTV) ratio: A measure of the loan amount relative to the value of the property

NOI and Cash Flow

• Net operating income: The annual income, minus expenses that a property generates from its operations

NOI = Income - Expenses

• Cash Flow: The cash flow (before tax) is the net result of gross income minus expenses and debt service.

Cash Flow = NOI – Debt Service

Cash Flow

Debt Service

Higher Debt Service = Lower Cash Flow

Debt Service Coverage Ratio

• The DSCR or debt service coverage ratio is the relationship of a property's annual net operating income (NOI) to its annual mortgage debt service (principal and interest payments).

DSCR= NOI/Annual Debt Service

NOI = $225,000ADS = $115,000

DSCR = $225,000/$115,000 = 1.9

Loan to Value (LTV)

• Loan-to-value (LTV) ratio: A measure of the loan amount relative to the value of the property

LTV=(Amount of Loan)/(Value of Property)

Property value = $735,000Amount of Loan = $588,000

LTV=$588,000/$735,000=80%

The Anatomy of a Conventional Loan

• Treatment of Income (Rental vs. earned)

• Entry Cost/Issues

• Terms

• APR

• Interest Rate (Fixed vs. Adjustable)

• Fees

• Points

• Exit Cost/Issues

• Balloon Payment

• Prepayment Penalties

• Underwriting

How do Lenders Reduce Their Risk

• FHA and other Government Guarantors

• Securitizing

• Higher Down Payments

• Shorter Payback periods

• Higher Debt Service Coverage Ratios

• Seasoned Income

• Longer Investment Experience

• Recourse Loans

Example Properties

Owner Occupied 3 Units Purchased With FHA 3.5% Down

Address 1521 Junipero

City Long Beach

Zip 90804

No. Units 3

Year Built 1947

Building Size 2253

Lot Size 6393

Property Description

Asking Price $599,900

Price/Unit $199,967

Price/Sq Ft $266

Down Payment $20,997

Closing Cost $17,997

Loan Fees $8,684

Rehab Cost $9,000

Total Cost $56,677

Loan Amount $578,904

Annual Debt Service -$32,172

Owner Occupied

Economics of Deal Owner Occupied

GROSS SCHEDULED INCOME $28,600

Less: Vacancy & Cr. Losses $1,430

EFFECTIVE RENTAL INCOME $27,170

GROSS OPERATING INCOME $27,170

TOTAL OPERATING EXPENSES $15,719

NET OPERATING INCOME $11,451

Less: Annual Debt Service $32,172

CASH FLOW BEFORE TAXES -$20,721

Rent from Former Apartment $18,000

Effective Cash Flow -$2,721

Cash Flow Calculations

Year 1 Year 2 Year 3 Year 4 Year 5

Cash Flow Before Taxes -$20,721 -$20,005 -$15,458 -$14,698 -$13,916

Effective Cash Flow -$2,721 -$2,005 $2,542 $3,302 $4,084

Five Units Commercial Loan 30% Down

Address 1189 W. Spring St.

City Riverside

Zip 92507

No. Units 5

Year Built 1950

Building Size 3400

Lot Size 9148

Property Description

Asking Price $500,000

Price/Unit $100,000

Price/Sq Ft $147

Down Payment $150,000

Closing Cost $15,000

Loan Fees $7,000

Rehab Cost $15,000

Total Cost $187,000

Loan Amount $350,000

Annual Debt Service -$21,281

Five Units

Economics of Five Units

Year 1 Year 2 Year 3 Year 4 Year 5

Cash Flow Before Taxes $7,647 $10,309 $11,257 $12,233 $13,238

GROSS SCHEDULED INCOME $43,500

Less: Vacancy & Cr. Losses $2,175

EFFECTIVE RENTAL INCOME $41,325

GROSS OPERATING INCOME $41,325

TOTAL OPERATING EXPENSES $12,398

NET OPERATING INCOME $28,928

Less: Annual Debt Service $21,281

CASH FLOW BEFORE TAXES $7,647

Cash Flow Calculations

Mortgage Broker

Hayden Harper

Single-Family Loans

• 1 – 4 unit properties

• Owner-occupied, second home, vacation rental, rental property

• Qualified off of housing ratios / debt-to-income ratios.

• Including FHA, VA, jumbo, conventional and portfolio programs.

• Owner-Occupied Investor• 3.5% down 25% down

• 2 – 4 unit investment property O.K. Non-owner occupied

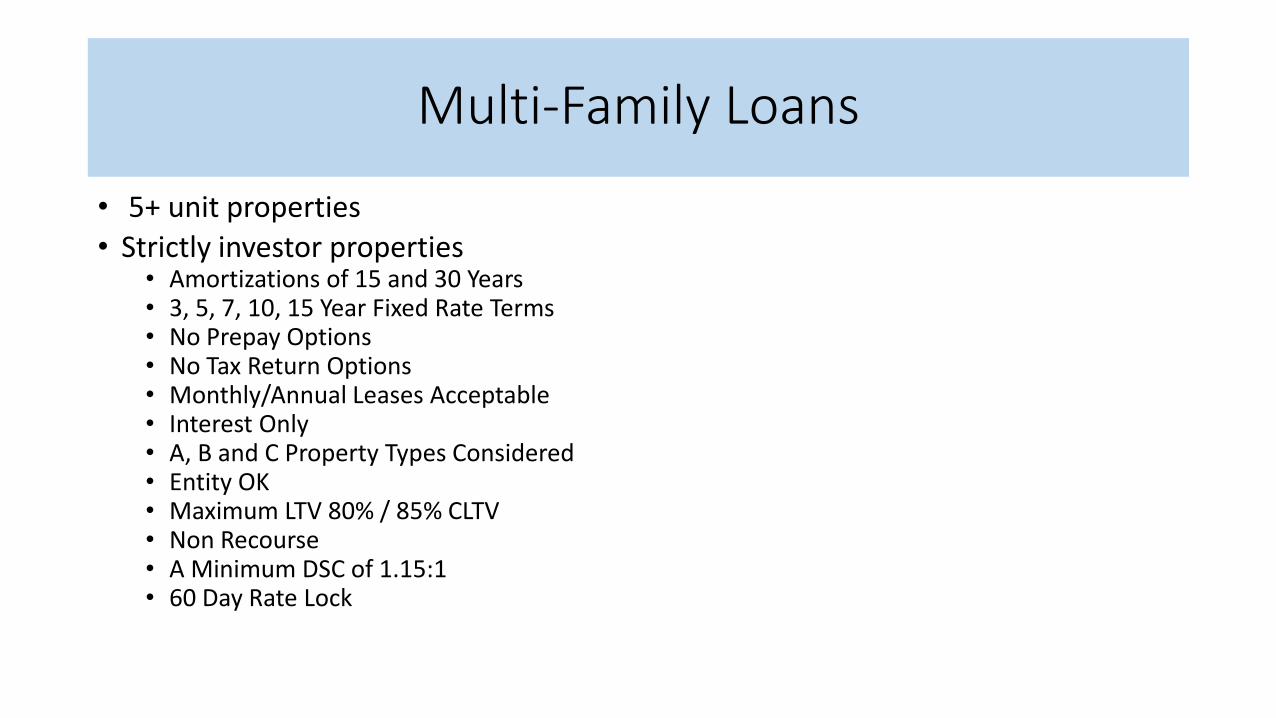

Multi-Family Loans

• 5+ unit properties

• Strictly investor properties• Amortizations of 15 and 30 Years• 3, 5, 7, 10, 15 Year Fixed Rate Terms• No Prepay Options• No Tax Return Options• Monthly/Annual Leases Acceptable• Interest Only• A, B and C Property Types Considered• Entity OK• Maximum LTV 80% / 85% CLTV• Non Recourse• A Minimum DSC of 1.15:1• 60 Day Rate Lock

Types of Loans – Fannie Mae / Freddie Mac• Conforming (Fannie/Freddie)

• Government-sponsored enterprises, give the ability to borrow more at lower interest rates than Private / Portfolio

• Maximum Conforming Loan amounts:• Loan Limits 1 – 4 units (Orange County / Los Angeles).

• 1-unit: $625,500• 2-unit: $800,775• 3-unit: $967,950• 4-unit: $1,202,925

• Loan Limits 1 – 4 units (San Bernardino / Riverside).• 1-unit: $417,000• 2-unit: $533,850• 3-unit: $645,300• 4-unit: $801,950

• Maximum investment transaction of 10; most banks will only allow up to 5 since this complicates underwriting.

Types of Loans - FHA

• FHA does not provide the loan itself, they insure banks against borrower defaults.

• Overseen by HUD – U.S. Department of Housing and Urban Development

• Provides a low down payment assistance. (3.5% down).

• Usually allows lower credit scores. (580 minimum).

• Upfront Mortgage Insurance Premium (UFMIP) – 1.75%; typically added to the loan amount, but borrower can bring amount to close and pay up front.

Example: $300,000 Loan with UFMIP = $305,250. UFMIP = (1.75% x $300,000 = $5,250)

Types of Loans – FHA (cont’d)• Annual Mortgage Insurance Premium (MIP) - .85% Annually.

• Must verify and document proposed rental income on 2-4 unit properties by obtaining an appraisal showing fair market rent in situations with limited or no history of rental income.

• FHA owner-occupied 3 – 4 unit investment. Monthly net rental income collected must be greater than - or equal to - monthly PITI. Conforming loan limitation still apply depending on county.

• Borrower must have three month’s PITI after closing on a purchase transactions. Unlike down payment, reserves cannot be derived from a gift.

• Net rental income = using the appraiser’s estimate of fair market rent from all the units, including the borrower's occupancy – the greater of the appraiser estimates for vacancies.

Debt To Income (DTI)

Formula: Total Recurring Debt / Gross Monthly Debt

• Fannie Mae / Freddie Mac: 45%

• Portfolio / Jumbo: 43%

• FHA: 56.99%

Residential Needs List

• Signed and Completed 1003 Loan Application

• Credit Authorization – Gives us the ability to pull credit

• Bank Statements (All Pages), verify assets

• W2’s or 1099’s

• 2015 – 2014 Personal Tax Returns (1040s) – Federal Only

• 2015 – 2014 Entity Tax Returns (1120, 1120S or 1065)• 1120 – Corporation

• 1120S – S-Corporation

• 1065 – Partnerships

• Insurance declaration and mortgage statements for all properties owned.

Tri-Merge Credit Report

• 3 credit repositories – score is based off the middle score• Equifax - 772

• Experian - 752

• Trans Union – 765

• Types of Credit• Revolving (Credit Cards).

• Installment (Leases).

• Mortgage.

35%

30%

15%

10%

10%

Credit Score Factors

Payment History

Debt Burden

Credit History

Types of Credit

Recent Searches

Exit Strategies

Investment Strategy

• Market and Sub Market Analysis

• Purchase• Under-Performing Properties

• High Growth Area

• Reposition• Resolve Property Issues

• Reduce Expenses

• Raise Income/Rents

• Refinance/Exchange • Minimize Taxes

• Based on Performance Metric (ROE, Cash Flow, IRR, Market Cycle)

• 1031 Exchange

• Installment Sale

• Sale

• Repeat

Owner Occupied Ten Year Performance

• 1031 Exchange Every Three Years

• $56,677 Investment Produced $609,047 Equity

Owner Occupied Cash Flow

Year 10 NOI =$65,000

Five Unit Ten Year Performance

• 1031 Exchange Every Three Years

• $187,000 Investment Produced $1,030,609 Equity

Five Unit Cash Flow

Year 10 NOI = $98,000

Make A Plan

• Cash Flow = Income – Expenses• Near term concern

• Increase Income

• Decrease Expenses

• Net Worth/Equity= Asset Value - Liabilities• Longer term Concerns

• Increase Asset Value

• Decrease Liabilities

Some Basic Financial Math

We go broke in the near term. - Unknown

In the long term, we’re all dead.- John Maynard Keynes

Elements of a Real Estate Investment Plan

Steps to Follow in Developing Your Plan

• Study History• Interest Rates/Financial Markets• Market Cycles• Demographic trends• Political Factors (Rent control, Zoning, etc.)

• Establish Criteria• Financial Returns (pick your metric)• Locations (All Real Estate is Local)• Condition• Holding periods/Exit Criteria

• Know your market(s)• Property Class• Cap Rates• Rent Rate• Demographics

• Locate Financing• Savings/Equity• Family• Friends• Partners• Lenders

• Establish Relationships with team• Lenders/Partners• Brokers• Inspectors/Contractors

• Find Property• Perform Due Diligence • Acquire

What to address in your Plan

• Why are you investing in Real Estate• Cash Flow• Appreciation• Tax Benefit• Leverage

• Time Horizon

• Success Metrics• Cap Rate• Return on Investment• Return On Equity• Internal Rate Return

• Use of Funds• Reserves• Expenses• Capital Improvements

• Source of investment funds• Personal Savings• Partnerships (My Brain, Your Money)• Conventional Financing• Seller Financing• Private Lenders• Cash Flow

• Exit Strategy• Sale• Exchange• Cash out Refi

“He who fails to plan is planning to fail" …Winston Churchill

You Need a Team

• Broker• Finding property• Market Analysis• Property Analysis• Broker Opinion of Value• Managing Transaction

• Attorney• Legal Due Diligence• Artificial Entities• Liabilities

• Accountant• Tax Implication• Financial Calculations• Financial Due Diligence

• Insurance Agent• Liability Coverage

• Property Manager• Expense management• Tenant Management

• Mortgage Broker/Lender• Finding Funds

• Contractor• Repairs• Remodeling• Physical Due Diligence

• Appraiser• Determine Market Value• Determine After Repair Value

(ARV)

• Network of fellow investors• Partners• Finding property

Success is where preparation and opportunity meet. (Bobby Unser)

Next Steps

• Determine Your Goals and Objectives• Why are you Investing

• What is your desired approach

• What is your time horizon

• What metrics will you use

• Select Your Market• Focus on Population Growth

• Focus on Diverse Sources of Income

• Build Your Team• Lenders and Brokers First

• Develop Property Analysis Model• Income• Expenses• Debt Service• Cash Flow

• Property Analysis• Select Three Locations

• Acquire Property

References

• What Every Real Estate Investor Needs to Know About Cash Flow … and 36 Other Key Financial Measures--- Frank Gallinelli

• Millionaire Real Estate Investor--- Gary Keller

• Apartment Building Investing--Michael Blank Podcast

• BiggerPockets Podcast: Real Estate Investing and Wealth Building• https://www.biggerpockets.com/

• US Bureau of Economic Analysis

• Bureau of Labor Statistic (bls.gov)

• Demographics• http://www.city-data.com/• US Census Bureau

• Crime Data• http://www.neighborhoodscout.com/