this document is being provided for the exclusive use of ... during a aug. 15 and 16 board meeting,...

TRANSCRIPT

1 2 3 4 5 6 7 8 9 10 11 12 13 14

BRIEF Leveraged Finance 10.07.13

www.bloombergbriefs.com

News, aNaLysis aNd CommeNtary

Ohio Highway Patrol Allocates to Loans in Yield Huntby DaviD Holley

The State of Ohio’s Highway Patrol Retirement System allocated $22 million in as-sets to senior secured loans in august as it seeks higher yield.

The retirement system for troopers and communications personnel employed by the highway patrol approved a $22 million allocation to Credit Suisse’s senior secured loan product during a aug. 15 and 16 board meeting, said Mark Atkeson, the executive direc-tor. The Columbus, ohio-based system terminated a $22 million allocation to Western Asset Management’s high yield fund, he said.

“in today’s environment, fixed income is not giving the yield it once did,” atkeson said in a telephone interview oct. 3. “We’re trying to find things within the asset classification to try to get better yields. We think by making some of these changes we’ll accomplish that.”

The system also approved a $25 million investment in JPMorgan’s strategic income opportunities fund, atkeson said. The system has no further plans for allocation changes in fixed income, he said.

The retirement system had $717.9 million in assets as of Dec. 31, 2012, which earned a gross return of 11.9 percent, according to its annual report. Fixed income accounted for $162.1 million of the total assets.

a new private equity firm to manage $5 million to $15 million will be selected on Dec. 19, according to a request for proposals. Finalists are being interviewed in November. The

0

1

2

3

4

5

6

7

8

9

10

1/1 2/1 3/1 4/1 5/1 6/1 7/1 8/1 9/1

$bn

Daily Average

Daily HY Trade

Source: Trace, Bloomberg LP NTMBHV Index <GO>

FIRST QUARTER THIRD QUARTER SECOND QUARTER

May 15: $9.7bn traded, most since Feb. 2012

BLOOmBerg BArOmeter Lisa abramowicz

Daily junk-bond trading averaged $4.87 billion in the third quarter, 18.1 percent less than volumes in the first half of the year and the biggest drop-off since the credit crisis five years ago, according to data from Trace. investment-grade trading is down 13.6 percent during the same period.

WeeK AHeAD

COMMitMentS due for Learfield, Gentiva, Harvey Gulf and Syncreon loans. (See Page 8.)

nGL eneRGY Set to price $400m 8NC3 this week.

neiMAn MARCuS oct. 7: bank meeting, $2.95bn lbo loans

ALLiAnt teCHSYSteMS oct. 8: bank meeting, $1.9bn M&a loans

SYnCReOn oct. 8: investor call, $225m 8NC3 Sr Notes

SiRiuS xM RAdiO oct. 10: investor meeting

INSIDe

LeveL 3 COMMuniCAtiOnS CFo Sunit Patel says the company may not refinance $2.6 billion of loans and $640 million of bonds next year. Page 2

AAR CORP CFo John Fortson plans to repay debt with rising free cash flow. Page 3

RbC The bank is on pace to join the ranks of the 10 largest underwriters of high-yield debt in the U.S. for the first time. Page 6

Q&A Jim Cassel of Cassel Salpeter, on lower-mid market M&a, financing. Page 7

euRO HiGH-YieLd RetuRnS best, worst performing sectors. Page 14

QUOte OF tHe WeeK

I compare Royal to a race car driver who never finishes in the winner’s circle, but finishes every race and never crashes.

— Peter Routledge, analyst at National Bank Financial, referring to

RBC’s high-yield underwriting. (See Page 6.)

“”

trading in Junk bonds declines Most Since 2008

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 2

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Continued from page 1

Market News

system is looking for a firm that is raising a fund of at least $100 million, been operating for at least five years and invests in strategies including buyout, venture capital and “op-portunistic” strategies.

a representative from the system’s investment consultant, Hartland, did not return a request for additional comment.

Level 3 Holds Loan refinance, Awaits Positive Cash FlowLevel 3 Communications may choose not to refinance $2.6 billion of loans and $640

million of bonds that can be called at cheaper rates in 2014 after it saved $23 million by refinancing this year, said CFo Sunit Patel.

it can call $1.796 billion of loans due 2020 and $815 million of loans due 2019 at par in February, Patel said. level 3 will save $9 million when the rate on a $1.2 billion tranche of the loans is cut by 25 basis points to 300 basis points over libor oct. 4, after a similar refinancing that saved it $14 million earlier this year.

While level can refinance again when the soft call expires in Feburary, “i don’t know that we will,” Patel said. “The savings would have to be pretty compelling to do that.”

its $815 million of loans due 2019 traded at 100.125, according to prices compiled by bloomberg. The $596.96 million in loans due 2020, which are being combined with the $1.2 billion of loans after oct. 4, traded at 100.06 cents.

level 3 has $640 million in 10 percent notes due 2018 that can be called at 105 cents on the dollar starting Feb. 2014. The notes traded at 107.5 Sept. 30, according to Trace.

“Those certainly would be the logical ones given that our bonds are trading at 7 percent or so currently,” Patel said about potential refinancing. “it’s still far enough away that it’s tough for me to prognosticate other than there’s certainly money to be saved.”

level 3 may become cash flow positive in 2014 for the first time since 2009, according to analyst estimates compiled by bloomberg. “We’ve guided to cash-flow even,” Patel said. “it’s not surprising that research analysts have us at cash flow positive next year.”

increased ebitda should come from cost savings on interest expenses and limited capital expenditure, as well as revenue growth from increasing demand in the company’s enterprise business in latin america, Patel said.

“The leverage is going to keep coming down because of ebitda growth,” Patel said. “let’s make sure we generate cash first and then we can decide what to do with it.”

once cash flow turns positive, Patel said he will decide whether to refinance or repay debt.The company’s $604 million in 11.875 percent notes due 2019 can be called at 105.94

in Feb. 2015, bloomberg data show. The notes traded at 115.75 cents oct. 2.The company cut 25 basis points off the $595.6 million loan aug. 16 and from the $815

million loan aug. 12. both pay 300 basis points over libor.— David Holley

ON tHe mOVe ■ Citi named tyrone thomas as

head of loan sales in North amer-ica as issuance of the debt has in-creased 84 percent this year. Thomas reports to ish McLaughlin, U.S. head of flow credit sales.

■ RbS hired former nomura execu-tive Kieran Higgins as head of fixed-income trading for europe, the Middle east and africa. The 41-year-old reports to Michael Lyublinsky, head of global trading, and Peter nielsen, co-head of the markets unit. Higgins last year left Nomura, where he was co-head of fixed income in europe.

■ institutional Financial Markets is cutting 20 percent of its workforce as the investment firm consolidates its PrinceRidge and Jvb Financial units into a single broker-dealer. PrinceRidge and Jvb will operate under the Jvb Financial brand once it receives regulatory approval. That would mean the end of PrinceRidge, which was started by two ubS bank-ers in 2009.

■ J.C. Penney named david Jordan vP of financial planning.

■ Schaeffler replaced Juergen Geissinger as Ceo to shift strategy after plans to combine with car-component maker Continental failed. CFo Klaus Rosenfeld will assume Geissinger’s role on an interim basis, Schaeffler is the third-largest issuer of junk bonds in europe year-to-date.

bloomberg brief Leveraged Finance Contributing Analysts newsletter business

Manger

Nick [email protected]+212-617-6975

To subscribe via the Bloomberg Terminal type BRIEF <GO> or on the web at www.bloombergbriefs.com. To contact the editors: [email protected]© 2013 Bloomberg LP. All rights reserved.This newsletter and its contents may not be forwarded or redistrib-uted without the prior consent of Bloomberg. Please contact our re-prints and permissions group listed above for more information.

bloomberg brief executive editor

Ted Merz [email protected] +1-212-617-2309

Michael Luongo Himanshu Bakshi

Afrim Zeka Paul BandongAdvertising

Jeff [email protected]+1-203-550-2446bloomberg

news Managing editor

Robert Burgess [email protected] +1-212-617-2945

Spencer Cutter Daniel Covello

Michael Acciani Lara Deke Reprints & Permissions

Lori Husted [email protected] 717-505-9701Leveraged

Finance editorJames Crombie [email protected] 212-617-3590

Maureen Gallagher Aselya Kerimkulova

Michael Kovacs

Reporter David Holley [email protected] 212-617-1311

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 3

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Continued from page 2

Market News

AAr to repay Debt With excess Cash, eyes ConvertibleAAR, the aviation repair company with a $74.8 million convertible note due March 2014,

will repay debt with free cash flow that reached the highest level ever.The 1.625 percent convertible note “has a maturity that is sort of staring us in the face,’’

John Fortson, the company’s CFo and treasurer, said in an oct. 1 telephone interview. “Priority number one for us is continuing to pay down debt.’’

aaR has a history of buying back convertible bonds in the open market, said Fortson, who joined aaR in June from bAML, where he was an investment banking MD.

Total debt fell to $702.2 million as of aug. 31 from $787.6 million a year earlier, accord-ing to regulatory filings. That is the biggest decline among junk-rated peers with more than $2 billion in revenue, according to data compiled by bloomberg. Free cash flow of $125.3 million for the fiscal year ended May 31 was a record for the company.

aaR cut debt by $91 million in fiscal 2013 by retiring 1.75 percent convertibles, david Storch, chairman and Ceo said in a July 25 earnings call.

Debt could rise again if the company made a large acquisition, which it would fund with borrowings, Fortson said. New issuance of debt would be event-driven, he said. The company aims to reduce leverage to 2-2.5 times from 3.62 times as of aug. 31, bloom-berg data show.

The company has $39.2 million outstanding on a revolver due 2015 that pays 325 basis points over libor, as well as $137.8 million outstanding in letters of credit and on a revolver due 2018 that pays 175 basis points over libor, bloomberg data show.

its $35 million unsecured term loan due 2017 pays 250 basis points more than libor.— David Holley

DeAL WAtCH ■ Samson investment, an oil and

gas producer owned by a group led by KKR, canceled plans to seek a lower rate on a $1 billion covenant-light loan. it was seeking to cut the interest on the debt due Sept. 2018 to 4 percentage points over libor with a 1 percent minimum, from 4.75 percentage points with a 1.25 percent floor. Credit Suisse was arrang-ing. The loan was quoted oct. 1 at 100.063 cents on the dollar down from 101.5 cents on July 22. S&P cut the company to b from b+ on Sept. 24, stating oil and gas exploration “production next year is likely to be lower than we initially contemplated, resulting in debt to ebitda leverage of more than 4.5 times at least through the end of 2014.”

Cortland is SSAE 16 SOC I Type II certified.

Investment Servicing

With Cortland’s complete infrastructure solution for CLO managers and leveraged loan professionals, adding operational leverage to your organization is like catching fish in a barrel. Contact us at:

Instant loan infrastructure, just add water.And by “water”, we mean Cortland.

Lora Peloquin [email protected]

www.cortlandglobal.comTim Houghton, [email protected]

Fund Administration Leveraged Loan Services SBA Loan Services Securitization Services Escrow Administration

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 4

1 2 3 4 5 6 7 8 9 10 11 12 13 14

VerBAtIm

What high-yield issuers are saying at confer-ences and on investor calls about their debt. Comments have been edited and condensed.

■ Parker drilling: “We’ve got to strength-en the balance sheet. our debt load is too high, we need to address that. and while we’re doing all of this, we got to make sure that we’re still developing paths for growth to be able to grow the business go-ing forward. We’re committed to reducing our debt leverage. We know it’s too high. at the end of Q2, our debt-to-cap was sitting at 52 percent. our net debt was 47 percent. our plan is to call $100 million of the 9-1/8 percent notes that we have when they come due in april of next year, that will take our leverage down under 50 percent. it’ll be in that sort of 47 percent range after we can do that. i think that by the end of this year we’ll be sitting with a debt to ebitda that’s at or slightly below three times. looking forward to end of 2014, i would expect our debt to ebitda to be closer in the two times range. So we’re committed to addressing our capital structure. again, these 9-1/8 percent notes become callable in april of next year. That gives us a path to debt reduction, and so it’s going to be a question as we look forward and we look at the cash that we expect to generate, a question of balanc-ing debt reduction and growth.”

— Christopher Weber, CFO, at the Johnson Rice Energy Conference Sept. 30

■ Regal entertainment: “We want to make sure we stay in that 3 to 4 times net debt-to-ebitda range. Fortunately, throughout our history we’ve mostly been able to finance acquisitions with cash on the balance sheet. So those have been generally helpful to our leverage profile. and for us to get outside that range, quite frankly, it would have to be a real sweet-heart transaction and we would have to have a very clear path to get back inside that range pretty quickly. our two tranches of debt still out there that have relatively high coupons, 8.625 percent for the opCo and then some 9.25 percent notes that still exist at the HoldCo. We took a small chunk of the 9.125 percent out earlier this year kind of as a hedge against rising rates between now and the call dates,

■ Sirius xM Radio: “effectively as the ebitda grows, we expect to maintain about 3.5 times leverage. if we do do that, look at your model, everybody else’s model, you’d come to the conclusion that we’re probably going to be a net issuer of about $1 billion a year of debt.”

— David Frear, CFO, at the Deutsche Bank Leveraged Finance Conference Oct. 2

■ Scientific Gaming: “i’m excited to be able to have largely pre-payable debt structure going forward, which i think given the cash flow characteristics of this merger that we’ll be able to take advantage of.”

— Jeff Lipkin, CFO, at the Deutsche Bank Leveraged Finance Conference Oct. 2

■ Crown Castle international: “The question was just as we issue debt in the future, post ReiT conversion will there be any changes in the way we think about our structure, where we would issue indebtedness and the short answer is, no. ... Certainly we’re mindful of implications potentially to our HoldCo ratings as we use various levels of secured or structured indebtedness. The agencies have differ-ing views of structured versus unsecured indebtedness. … Some of them — one of them — doesn’t care at all where it is. They just look at it as total leverage and one of them does push a finer point on that. So i think it’s going to be a balance over time. The midpoint of our targeted level of lever-age, the four times to six turns, it would ap-pear that in the neighborhood of five turns of debt to ebitda probably gets us there with at least one and hopefully multiple rat-ing agencies on an investment grade credit rating at the holding company. Today we’re at about six times.”

— Jay Brown, CFO and treasurer, said during the Deutsche Bank Leveraged

Finance Conference Oct. 2

■ Frontier Communications: “We did a large debt offering earlier this year and we did a whole bunch of liability management transactions and we really cleared the path for our debt for the next many years, so we don’t have to be in the market until at least 2017, 2018.”

— Robert Starr, treasurer, at the Deutsche Bank Leveraged Finance Conference Oct. 2

which are mid next year. obviously, we’ll continue to watch the rate. and right now it seems like maybe it makes sense to bide our time until the call date when we can maybe do that a little bit more effectively and manage our interest costs a little bit better. … We’ll definitely look to manage that interest cost going forward.”

— David Ownby, CFO, at the Deutsche Bank Leveraged Finance Conference Oct. 1

■ town Sports international: “our exist-ing credit facility was initially launched in May of 2011. So our facility, we’re about two and a half years ... into our facility. and given that we’re approaching the an-niversary of the amendment of November of last year, our pre-payment penalty of 1 percent will go away, i believe, on Novem-ber 14 or thereabouts. So as we speak, we’re actively working with the Deutsche bank team to see what opportunities we might have out there now, as we get closer to this expiration of the penalty box, to see what we can do at some critical areas to reduce our borrowing cost to per-haps extend the term, so we can refresh the term, reset the runway so we could start off with a five-year revolver, perhaps a seven-year term loan. but we would also try to reduce some of the covenants and go after the restricted basket to try to expand the restricted basket.”

—Dan Gallagher, CFO, at the Deutsche Bank Leveraged Finance Conference Oct. 1

Our plan is to call $100 million

of the 9-1/8 percent notes that we have

when they come due in April of next year.

— Parker Drilling CFO Christopher Weber‘‘

‘‘

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 5

1 2 3 4 5 6 7 8 9 10 11 12 13 14

0

5

10

15

20

25

2012 2013

Mar

ket S

hare

(%)

Source: Barclays

High

Low

Hedge Fund Share of u.S. High-Yield Rises 5 Percentage Points

Hedge Funds expand Bets With most Junk Bond market Share Since 2008Hedge funds have amassed the greatest

share of the $1.2 trillion U.S. junk-bond market since the credit crisis, raising concern bets with borrowed cash will ac-celerate losses when the Federal Reserve stops printing record amounts of money.

The funds hold as much as 23 percent of outstanding dollar-denominated high-yield bonds, from as much as 18 percent last year and the highest since 2008, ac-cording to barclays. Credit hedge funds have boosted assets by 89 percent since 2008, outpacing the 66 percent growth of the junk market, data from Hedge Fund Research and bAML indexes show.

Funds that use leverage may threaten the financial system in a broader selloff, the U.S. Treasury Dept.’s office of Finan-cial Research wrote in a report gauging risks from investment firms that have bal-looned. Sophisticated investors including hedge funds were among the first to exit as the market started to fracture in 2008, according to the Sept. 30 study.

“any time leverage is involved it’ll exacerbate swings in the market,” said Marc Gross, a money manager at RS investments who oversees $3.5 billion. if a mass exodus is triggered, “they’ll all be selling and they’ll be selling with leverage.”

The baMl U.S. High yield index plunged 2.6 percent in June, more than stocks and Treasuries, after the Fed said it could start slowing its $85 billion of monthly asset purchases if the economy showed sustained improvement. in the four years before then, the debt posted average an-nual returns of 16.1 percent.

even as funds that use borrowed money grab a bigger proportion of the market, leverage in the system is less than it was leading up to the crisis as banks boost debt-to-equity ratios. Credit hedge funds are also, on average, using less leverage, according to barclays’s bradley Rogoff.

Hedge funds may, in some cases, be acting as buffers against price swings fueled by redemptions from mutual and exchange-traded funds, helping to fill a void left by banks that have reduced hold-ings of riskier assets in the face of new regulations, according to Gross.

“in theory, having a more diverse group of investors is a good thing and en-hances liquidity because there’s more of a chance that one group is buying as one group is selling,” said Martin Fridson, Ceo of Fridsonvision. “but it’s hard to make the case that it’s going to help stabilize the markets when bonds start to really sell off.”

Hedge funds’ share of the speculative-grade bond market has grown 5 per-centage points from last year to include as much as $290 billion of junk bonds, barclays strategists led by Jeffrey Meli and bradley Rogoff wrote in a Sept. 26 report. The 17-23 percent of the market that hedge funds own this year compares with 12-18 percent in both 2012 and 2011, according to barclays data that doesn’t go back further than those years.

in the past year, the proportion of junk notes outstanding owned by U.S. mutual funds and eTFs fell about 9 percent, or $21 billion, to a maximum of $240 billion, the analysts said. assets owned by high-yield closed-end funds, which also typi-cally buy with borrowed money to boost returns, doubled to about $14 billion this year, the barclays strategists said.

Credit hedge funds have received $113.3 billion of deposits since 2009 and boosted assets under management to $648.3 bil-lion as of June 30, according to data from HFR. That contrasts with the two years ended Dec. 31, 2009, when investors yanked $86.65 billion from the funds.

When investment managers crowd into similar assets at the same time, espe-cially those that aren’t frequently traded, the behavior may “create adverse market impacts if financial shocks trigger a rever-sal of the herding behavior,” the Treasury said in its report last week. at the same time, fund managers who are able to buy securities trading “significantly below their intrinsic values” could help stabilize price declines, according to the study.

When investors pull money for illogical reasons, “it’s as if we’re sitting at a poker table and a drunk businessman walks into the casino and sits at our table,” said Steve Kuhn, whose Pine River Fixed income Fund was the second-best performing hedge fund last year. “That’s a good day for you, when people are mak-ing decisions for less than logical reasons, and you can sit there and calmly try to decide what true value is.”

CreDIt mArKet WAtCH Lisa abramowicz

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 6

1 2 3 4 5 6 7 8 9 10 11 12 13 14

0

5

10

15

20

250

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Deal Volume ($bn, Left Axis)

Market Share (%, Left Axis)

League Table Rank (Right Axis)

Source: Bloomberg LP LEAG44 <GO>

U.S. High-Yield Bonds, Year to Oct. 1

RbC u.S. Junk bond deal volume Jumped 21% Year-on-Year

Canada’s rBC Poised to Crack top 10 of U.S. Junk-Bond Arrangers After Hiring SpreeRoyal bank of Canada is on pace to

join the ranks of the 10 largest underwrit-ers of high-yield debt in the U.S. for the first time as the largest Canadian lender seeks profits abroad with issuance slow-ing at home.

RbC Capital Markets ranks 10th among arrangers of speculative-grade bonds at the end of the third quarter after luring bankers from firms including deutsche bank and Credit Suisse. The Toronto-based firm has never been a top-10 underwriter for non-investment-grade debt in the U.S. on any given year, according to data compiled by bloomberg.

“i compare Royal to a race car driver who never finishes in the winner’s circle, but finishes every race and never crash-es,” Peter Routledge, an analyst at na-tional bank Financial. “you can’t say he doesn’t take risk if he’s running around the track at 200 miles an hour, but he doesn’t crash and earns a decent paycheck. That’s Royal.”

RbC is focusing on the U.S. junk-bond market, which is more than 300 times larger than its domestic counterpart, as booming sales contrast with a slowdown in Canada. Record stimulus from the Fed is filtering into the balance sheets of the most indebted U.S. borrowers, while in Canada commodity-dependent issuers are suffering from a plunge in resource prices as asia curbs consumption.

While RbC expects total sales of junk bonds in the U.S. market to surpass last year’s record $353 billion, on Sept. 4 it cut its annual forecast for Canadian issuance to as little as C$4 billion ($3.9 billion) from about C$6 billion. The firm boosted the headcount in its U.S. credit team by 15 percent in the past two years, hiring almost 20 people, including 10 sales staff and eight traders. last month neil Yaris, who has held jobs at Credit Suisse and bAML, joined as co-head of high-yield debt trading.

RbC’s long-standing goal to be a Top 10 investment bank in the U.S. contrasts with retrenchment in other areas of banking. The company sold its unprofitable U.S. lender RbC bank to PnC in March 2012,

ending an unsuccessful decade-long foray into U.S. retail banking.

in Canada, RbC slipped to the third spot among underwriters of high-yield debt, from No. 1 in 2012. Still, the firm has led arrangers of investment-grade company bonds in Canada for at least 14 years.

a bAML index of U.S. junk bonds has returned 3.8 percent in 2013, compared with a 2.5 percent loss on investment-grade bonds. in Canada, high-yield bonds gained 3.3 percent this year to Sept. 30.

RbC arranged high-yield debt sales for companies including Sprint, Sirius xM Radio and Ancestry.com in the third quarter, according to data compiled by bloomberg.

Sanchez energy, an oil explorer and producer based in Houston, hired RbC with Credit Suisse to manage its first junk bond in June, which it increased last month to a total $600 million.

“There’s some that do more deals than others or are higher on the league tables, but it’s really the relationship focus and the delivery of the entire bank – and the manner in which it’s done – that drives us to really favor RbC,” said Michael Long,

Sanchez energy’s CFo.in april RbC hired former Credit Suisse

banker Steve Oplinger as head of U.S. high-yield and leveraged loan sales and trading. The company added John Rote, former head of baMl’s high-yield syndi-cate in New york, in May and Deutsche bank researcher Guy baron in June.

Royal bank’s return on equity for capital markets is at 14.3 percent for the first nine months of fiscal 2013, according to finan-cial statements. That compares with 13.5 percent in 2012 and 15.2 percent in 2011.

“They used the crisis and now the aftermath to selectively poach talent from competitors, and they’ve done that incre-mentally,” Routledge said. “if you look at the return-on-equity in capital markets, it’s held up well.”

“We’ve had a focus over the last two years of upgrading our talent, increasing our balance sheet selectively and increas-ing our resources in the overall credit business, especially in the U.S.,” said Mike Meyer, global head of credit at RbC Capital Markets. “a lot of our ranking has to do with people; we’ve made a number of strategic hires on our high-yield desk.”

HIgH-YIeLD BOND UNDerWrIter FOCUS Doug aLexanDer

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 7

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Q&A

Dividend recaps should continue among companies with between $10 million and $250 million of enterprise value as interest rates remain low, said Jim Cassel, co-founder of Cassel Salpeter & Co, a lower-middle market boutique investment bank that advises family-owned businesses and private equity firms on M&a and debt financing. Cassel spoke with bloomberg brief’s David Holley.

Q: What is your client base?A: Ninety percent of the M&a stuff is sellside. buyside is more where some-one is buying and they need an adviser. We work for some of the private equity firms. We do some restructuring work for financially troubled companies, not operationally troubled. We’ll raise money, we’ll raise equity.

Q: How many refinancings do you usually work on?A: We’ll do a couple a year. We’re a small shop. We get a half a dozen M&a deals.

Q: What is your outlook for lower mid-market M&A?A: There are a significant amount of sell-ers talking about selling mid- or late-2014. They think 2014 is going to be better than ’13. They want to get 2013 in the bag, so they can show to a buyer they put these numbers up, and maybe get a quarter or two in in 2014. assuming they’re right, things go up, then they can sell more on the growth side and get a better premium. Generally what i’m describing are family businesses rather than private equity.

Q: How are you involved in financing?A: We’ll do debt placements or we’ll find [mezzanine] money. Sometimes we do just debt placement.

Q: What terms of financing are you helping these firms get?A: We serve as financial advisers work-ing on project finance transactions. The size between equity and debt is in the $40 million range with the debt being about $27 million. The debt will be non-rated and issued pursuant to an econom-

Lower middle-market m&A expected to Pick Up; Cash ‘Not Being Lent Stupidly’

Recommended reading: GetAbstract for a short synopsis of business books

Favorite film: Goldfinger (1964)

If you could have another career, it would be: U.S. Senator

Favorite food: Ribs, black and white cookies

Favorite drink: Bombay Sapphire and tonic with lime

Favorite restaurant in the city you live (Miami): Joe’s Stone Crab

Favorite restaurant elsewhere: La Trattoria-Sporting Club in Monte Carlo

ic development authority. as a result of the Detroit bankruptcy and the concerns about Puerto Rico, rates have increased during the past six months from what might have been below 7 percent to more than 9 percent.

Q: What do you expect to happen with mezzanine borrowing rates?A: i expect mezzanine rates to start to move up in 2014. Rates have been low as a result of the vast amount of availability and the aggressiveness of mezz lenders to put money to work. We have seen all-in rates of 12 percent. These are historically low for this asset class. Having low interest rates and the need to put money to work have been a catalyst. as long-term rates start to increase, so will mezzanine rates.

Q: Why will rising interest rates impact mezzanine?A: late last year we worked on a mezza-nine deal. The term sheets we ended up with were 12 percent flat, nothing accrued above that and no equity. Today they’re up to 14 percent on a deal. Mezzanine will go up a little bit if rates go up.

Q: What is your outlook for mid-market dividend recaps?A: With everybody knowing that interest rates will rise but not exactly knowing when, good companies with growing and stable cash flows will continue to do leveraged recaps. For companies who have previously recapitalized, if cash flows have increased, they may do it again and take advantage of the low rates and availability of money.

Q: What is the cost of this for the com-panies you work with?A: you can get five-year term money, at 4 [percent] and change, it’s cheap money. if these guys can get their money back, they can kick it back to their partners. They’ve limited their downside and shifted the principal risk to the bank.

Q: What’s the value of a dividend recap versus a sale?A: a Pe firm, they’ve owned a portfolio company for 2-3 years, if they can do a dividend recap and get their money out, and they think there’s good upside in it, i think they’re happy to do it. i think there’s a big divide between quality assets and oK assets.

Q: What’s the divide?A: Quality assets with predictable, sustainable cash flows. There’s plenty of senior money out there for good deals. it’s not being lent stupidly yet. The pricing is getting pretty competitive. We’re not back to naked covenants, but they’re covenant-light.

Q: What’s your u.S. economic outlook?A: The next three months could be pivotal to the economy as the politicians play games with our fragile economy. if the debt ceiling is not increased, and the U.S. does not pay its debts when they come due, we could lose our financial status in the world as the reserve currency. The politicians are playing with fire. The uncertainty will create havoc if it continues.

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 8

1 2 3 4 5 6 7 8 9 10 11 12 13 14

LOANS

Source: Bloomberg LP LSRC <GO>

U.S. Institutional Loan Pipeline

BOrrOWer SPONSOr AmOUNt (m)

teNOr (YrS)

mArgIN (L+) rANK PrICe L FLOOr CALL

PrOteCt UOP LeADS COmmIt DAte

Hudson's Bay - $300 8.0 750-775 2L 99.0 - - m&a BamL/rBC 7-octLearfield Providence $215 7.0 425 1L 99.0 100 - LBo dB/Ge 8-octLearfield Providence $85 8.0 825 2L 98.5 100 - LBo dB/Ge 8-octGentiva - $200 5.0 400 1L 99.5 100 101 sC 6-mo m&a BarC/BamL 9-octGentiva - $655 6.0 450-475 1L 99.0 100 101 sC 6-mo m&a BarC/BamL 9-octHarvey Gulf Jordan $100 5.0 400 1L 99.5 100 - m&a BamL 9-octHarvey Gulf Jordan $250 7.0 450 1L 99-99.5 100 - m&a BamL 9-octCity Center - $1,700 7.0 400~ 1L 99.0 100 101 sC 6-mo refi BamL 9-octsyncreon Centerbridge $525 7.0 400-425 - 99.0 100 101 sC 6-mo m&a ms/Gs 10-octalliance Healthcare mts, oaktree $70 6.0 325 1L 99.0 100 101 sC to 6/14 refi Cs 10-octinsight Global ares $130 6.0 475 1L 99.0 125 - refi Cs 11-octProgressive solutions - $490 7.0 375-400 1L 99.0 100 101 sC 6-mo m&a Cs 15-octProgressive solutions - $160 8.0 775-800 2L 99.0 100 102/101/100 m&a Cs 15-octNeiman marcus ares, CPPiB $2,950 7.0 - 1L - - - LBo Cs 16-octUtility service - $185 7.0 475-500 1L 99.0 100 - m&a rBC/BNP/maCQ -amneal Pharma - $475 6.0 - 1L - - - div recap Ge/rBs -excelitas Veritas $620 7.0 - 1L - - - m&a UBs/Cs/mCs -excelitas Veritas $285 7.5 - 2L - - - m&a UBs/Cs/mCs -Huntsman - $1,150 7.0 300-325 1L 99.5 75 101 sC 6-mo - BamL -Penn National Gaming - $250 7.0 - - - - - refi JPm -seminole tribe - $395 4.0 - - - - 101 sC 6-mo - - -

LSTA 18th Annual Conference

October 17, 2013 Hilton Hotel - NYC

Analyzing the Future of the Loan Market

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 9

1 2 3 4 5 6 7 8 9 10 11 12 13 14

U.S. LeVerAgeD LOAN INDex retUrNS BY SeCtOr bLoomberg Data

The JPMorgan leveraged loan index was flat for the week ended oct. 3. a positive return in the metals & mining sector, which re-turned 43 basis points on the week, was countered by a 23 basis point loss in utilities. Despite the fact that the company avoided

default by making a scheduled coupon payment on its bonds oct. 1, energy Future Holdings term loans traded off, into the $67 area, on speculation that it will reach an agreement with creditors on a prepackaged bankruptcy restructuring within the next month.

JPMorgan Leveraged institutional Loan index-Sector Returns and Characteristics october 3, 2013

SeCtOr JP mOrgANtICKer StW (BP) YtW (%)

tOtAL retUrN, % [1,2]

1 WeeK 1m 3m YtD Automotive JLLIAUTO 372.32 4.85 -0.03 0.44 1.60 3.59Broadcast JLLIBRDC 536.82 6.81 -0.06 0.61 2.42 9.38Cable/Satellit JLLICBLE 310.56 4.79 0.12 0.29 1.28 2.38Chemicals JLLICHEM 385.81 5.22 0.11 -0.02 1.19 2.46Consumer Prod. JLLIPROD 425.05 5.84 0.06 0.29 1.27 4.04Diverse Media JLLIDVMD 530.55 6.63 -0.13 -0.04 0.81 4.14Energy JLLIENER 509.13 6.45 0.05 0.39 1.50 3.97Financial JLLIFINL 465.05 6.10 -0.05 0.37 1.44 3.87Food & Bev JLLIFDBV 339.04 5.04 -0.01 0.27 1.11 3.13Gaming/Leisure JLLIGAME 405.49 5.69 -0.04 0.27 1.37 3.63Healthcare JLLIHLTH 391.41 5.24 0.00 0.19 1.35 3.09Housing JLLIHOUS 396.85 5.73 0.08 0.60 0.20 1.42Industrials JLLIINDU 384.95 5.41 0.06 0.26 1.20 2.87Metals/Mining JLLIMETL 450.28 5.85 0.43 0.68 1.09 2.92Paper & Pack JLLIPAPR 374.88 5.20 -0.01 0.25 1.22 2.91Retail JLLIRETL 416.89 5.62 -0.08 -0.07 1.04 2.96Services JLLISERV 473.97 6.14 -0.04 0.39 1.54 3.99Technology JLLITECH 421.68 5.77 -0.03 0.27 1.45 3.98Telecom JLLITLCM 382.53 5.49 0.09 0.47 1.71 3.49Transportation JLLITRAN 405.67 5.42 0.03 0.80 1.57 5.31Utility JLLIUTIL 1,197.94 13.35 -0.23 0.58 -0.20 3.71

1L Leveraged Loans JLLILLI 454.24 139.25 0 0.31 1.28 3.622L Leveraged Loans J2LILLI 929.11 10.9 0.04 0.91 2.40 8.03

Loan Only JLLILNOY 466.20 6.18 -0.01 0.33 1.32 4.09Loan & Bond JLLILNBD 446.86 5.91 0.00 0.29 1.25 3.34Libor Floor JLLILFLR 414.32 5.69 0.02 0.27 1.31 3.35No Libor Floor JLLINLFL 682.62 7.86 -0.13 0.51 1.13 4.32Cov-Lite JLLICOVL 383.51 5.48 0.02 0.17 1.22 2.94Not Cov-Lite JLLINCVL 502.13 6.37 -0.01 0.39 1.32 3.92Domestic JLLIUS 457.10 6.03 -0.02 0.30 1.25 3.61International JLLIINTL 421.02 5.73 0.19 0.37 1.65 3.76

BB JLLIBB 323.04 4.75 0.01 0.18 1.10 2.47Split BB JLLISBB 384.32 5.32 0.00 0.20 1.43 3.14B JLLIB 467.17 6.15 0.01 0.30 1.43 4.21Split B JLLISBCC 1,454.00 15.62 -0.26 1.35 0.86 5.62Not rated JLLINR 679.43 8.03 -0.05 0.62 1.36 5.91US LeveRaged Loan Index JLLILLI 454.24 139.25 0.00 0.31 1.28 3.62

Source: JPMorgan Leveraged Loan IndicesNotes: 1)Monthly and yTD performance data represents periods up to the current date. 2)Green / red color coding represents performance ranking of the top/bottom three sectors in the period. JLLI INDEX <GO>

— Spencer Cutter, Bloomberg Data Analyst

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 10

1 2 3 4 5 6 7 8 9 10 11 12 13 14

eUrOPeAN LOANS Luke reeve, bLoomberg Data anaLyst

Western europe Leveraged Loan Pipeline BOrrOWer SPONSOr AmOUNt

(m)teNOr (YrS)

mArgIN (L+) rANK L FLOOr UOP LeADS COmmIt

DAte

oBertHUr teCH advent intl Usd 371 6 − 1L 100 LBo/refin Gs/JP/LLo -

oBertHUr teCH advent intl eUr 165 6 − 1L − LBo/refin Gs/JP/LLo -

oBertHUr teCH advent intl eUr 88 5 − 1L − LBo/refin Gs/JP/LLo -

tUNstaLL GroUP Charterhouse GBP 20 6 450 1L − LBo/refin JP -

tUNstaLL GroUP Charterhouse GBP 40 6 450 1L − LBo/refin JP -

tUNstaLL GroUP Charterhouse GBP 90 7 500 1L − LBo/refin JP -

tUNstaLL GroUP Charterhouse eUr 240 7 475 1L − LBo/refin JP -

sCaNdLiNes 3i, allianz eUr 35 6 425 1L − LBo/refin/work Cap daN/dB/Gs/iNG/JP/miZ/sC/UBs -

sCaNdLiNes 3i, allianz eUr 265 6 425 1L − LBo/refin/work Cap daN/dB/Gs/iNG/JP/miZ/sC/UBs -

sCaNdLiNes 3i, allianz eUr 525 7 475 1L − LBo/refin/work Cap daN/dB/Gs/iNG/JP/miZ/sC/UBs -

sCaNdLiNes 3i, allianz eUr 50 6 425 1L − LBo/refin/work Cap daN/dB/Gs/iNG/JP/miZ/sC/UBs -

Source: Bloomberg LP LSRC <GO>

Western europe Leveraged Loans Signed Sept. 18 - Oct. 1BOrrOWer SPONSOr AmOUNt

(m)teNOr (YrS)

mArgIN (L+ rANK UOP LeADS SIgNeD

Card FaCtory Charterhouse GBP 165 5 500 1L recap/div Nom 10/1/2013

sK sPiCe sK Capital Usd 320 5 825 1L LBo/acq JeF 9/30/2013

sK sPiCe sK Capital Usd 40 5 500 1L LBo/acq JeF 9/30/2013

doUGLas advent intl eUr 450 6 450 1L LBo/acq/refin JP/UNi 9/30/2013

doUGLas advent intl eUr 200 5 425 1L LBo/acq/refin JP/UNi 9/30/2013

CHesaPeaKe Carlyle GBP 50 6 400 1L LBo Cs/Gs/UBs/BarC 9/26/2013

CHesaPeaKe Carlyle GBP 145 7 500 1L LBo Cs/Gs/UBs/BarC 9/26/2013

CHesaPeaKe Carlyle eUr 173 7 450 1L LBo Cs/Gs/UBs/BarC 9/26/2013

m7 Providence eUr 75 6 425 1L LBo/refin/div BNP/Ca/dB 9/18/2013

m7 Providence eUr 270 7 475 1L LBo/refin/div BNP/Ca/dB 9/18/2013

m7 Providence eUr 10 6 425 1L LBo/refin/div BNP/Ca/dB 9/18/2013

Source: Bloomberg LP

LEARN HOW TO USE BLOOMBERG FUNCTIONS <HELP>

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 11

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Ticker Coupon Maturity Last Price

5-Day Change Yield 5-Day

Volume

52W Range Avg 30D Price

Last PricePDVSA 9.75 05/17/35 75.760 2.510 13.151 115000BACR 0 08/29/49 57.750 2.250 N.A. 6000LONKIN 8.5 06/03/16 103.500 2.000 7.023 4000PDVSA 9 11/17/21 81.500 1.750 12.719 38000COGARD 7.25 04/04/21 100.150 1.650 7.218 8000GATSP 10 02/01/19 69.500 1.375 19.445 22000PDVSA 5.25 04/12/17 79.250 1.260 12.772 77000NAV 8.25 11/01/21 102.250 1.250 7.593 9000CCI 5.25 01/15/23 94.250 1.250 6.069 29000PDVSA 5.5 04/12/37 55.650 1.150 10.689 5000PDVSA 8.5 11/02/17 89.010 1.010 11.991 211000MPEL 8.5 12/01/20 110.500 1.000 6.028 4000MRFGBZ 8.375 05/09/18 92.250 1.000 10.547 12000S 7 08/15/20 103.000 1.000 6.449 24000ODHGPR 8.375 09/20/20 104.080 0.780 7.510 21000DISH 5.875 07/15/22 100.000 0.750 5.873 27000MGM 7.75 03/15/22 110.500 0.750 6.136 11000THC 4.5 04/01/21 95.375 0.750 5.256 20000PDVSA 5.375 04/12/27 57.390 0.740 11.741 20000REYNOL 8.25 02/15/21 101.875 0.625 7.811 17000

Ticker Coupon Maturity Last Price

5-Day Change Yield 5-Day

Vol

52W Range Avg 30D Price

Last PriceOGXPBZ 8.375 04/01/22 9.250 -4.470 93.477 19000JCP 5.65 06/01/20 70.000 -3.750 12.406 2000JCP 5.75 02/15/18 73.625 -3.125 14.052 18000OGXPBZ 8.5 06/01/18 9.000 -3.000 149.203 66000JCP 6.375 10/15/36 67.000 -2.000 10.090 2000FST 7.5 09/15/20 100.750 -1.500 7.314 35000JCP 7.4 04/01/37 67.750 -1.500 11.358 11000RBS 6.1 06/10/23 101.034 -0.930 5.956 28000ADROIJ 7.625 10/22/19 104.500 -0.750 6.343 4000ES 10.75 08/15/18 107.625 -0.750 7.537 14000AA 5.55 02/01/17 106.750 -0.637 3.376 3000PSD 6 09/01/21 108.933 -0.607 4.635 8000AMD 8.125 12/15/17 104.500 -0.500 5.362 4000TSO 5.375 10/01/22 95.500 -0.400 6.031 7000POST 7.375 02/15/22 105.375 -0.375 6.332 8000EVERRE 13 01/27/15 108.000 -0.300 6.465 8000LAMR 5 05/01/23 93.500 -0.250 5.899 3000KMI 7.75 01/15/32 101.750 -0.250 7.570 8000STZ 7.25 09/01/16 114.250 -0.250 2.145 5000BANBRA 9.25 10/31/49 106.750 -0.250 8.214 18000

BONDS

PdvSA, barclays, Lonkin See biggest Price Gains OGx 2022, J.C.Penney Fell Most Last Week

Source: Bloomberg LP TACT<GO> Source: Bloomberg LP TACT<GO>

BLOOMBERG BRIEF GROUP SUBSCRIPTIONSBloomberg newsletters are now available for group purchase at very affordable rates. Share with your team, firm or clients.

Contact us for more information:[email protected]

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 12

1 2 3 4 5 6 7 8 9 10 11 12 13 14

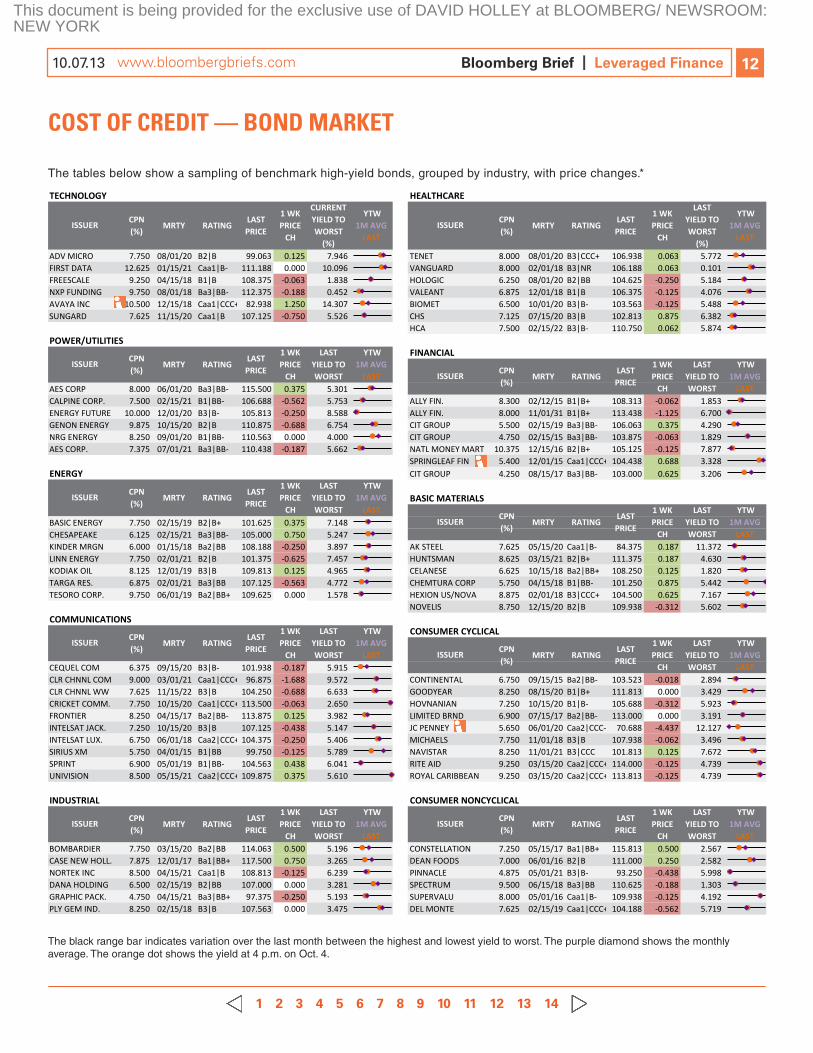

COSt OF CreDIt — BOND mArKet

The tables below show a sampling of benchmark high-yield bonds, grouped by industry, with price changes.*

The black range bar indicates variation over the last month between the highest and lowest yield to worst. The purple diamond shows the monthly average. The orange dot shows the yield at 4 p.m. on oct. 4.

TECHNOLOGY HEALTHCARE

ADV MICRO 7.750 08/01/20 B2|B 99.063 0.125 7.946 TENET 8.000 08/01/20 B3|CCC+ 106.938 0.063 5.772FIRST DATA 12.625 01/15/21 Caa1|B- 111.188 0.000 10.096 VANGUARD 8.000 02/01/18 B3|NR 106.188 0.063 0.101FREESCALE 9.250 04/15/18 B1|B 108.375 -0.063 1.838 HOLOGIC 6.250 08/01/20 B2|BB 104.625 -0.250 5.184NXP FUNDING 9.750 08/01/18 Ba3|BB- 112.375 -0.188 0.452 VALEANT 6.875 12/01/18 B1|B 106.375 -0.125 4.076AVAYA INC 10.500 12/15/18 Caa1|CCC+ 82.938 1.250 14.307 BIOMET 6.500 10/01/20 B3|B- 103.563 -0.125 5.488SUNGARD 7.625 11/15/20 Caa1|B 107.125 -0.750 5.526 CHS 7.125 07/15/20 B3|B 102.813 0.875 6.382

HCA 7.500 02/15/22 B3|B- 110.750 0.062 5.874POWER/UTILITIES

FINANCIAL

AES CORP 8.000 06/01/20 Ba3|BB- 115.500 0.375 5.301CALPINE CORP. 7.500 02/15/21 B1|BB- 106.688 -0.562 5.753 ALLY FIN. 8.300 02/12/15 B1|B+ 108.313 -0.062 1.853ENERGY FUTURE 10.000 12/01/20 B3|B- 105.813 -0.250 8.588 ALLY FIN. 8.000 11/01/31 B1|B+ 113.438 -1.125 6.700GENON ENERGY 9.875 10/15/20 B2|B 110.875 -0.688 6.754 CIT GROUP 5.500 02/15/19 Ba3|BB- 106.063 0.375 4.290NRG ENERGY 8.250 09/01/20 B1|BB- 110.563 0.000 4.000 CIT GROUP 4.750 02/15/15 Ba3|BB- 103.875 -0.063 1.829AES CORP. 7.375 07/01/21 Ba3|BB- 110.438 -0.187 5.662 NATL MONEY MART 10.375 12/15/16 B2|B+ 105.125 -0.125 7.877

SPRINGLEAF FIN 5.400 12/01/15 Caa1|CCC+ 104.438 0.688 3.328ENERGY CIT GROUP 4.250 08/15/17 Ba3|BB- 103.000 0.625 3.206

BASIC MATERIALS

BASIC ENERGY 7.750 02/15/19 B2|B+ 101.625 0.375 7.148CHESAPEAKE 6.125 02/15/21 Ba3|BB- 105.000 0.750 5.247KINDER MRGN 6.000 01/15/18 Ba2|BB 108.188 -0.250 3.897 AK STEEL 7.625 05/15/20 Caa1|B- 84.375 0.187 11.372LINN ENERGY 7.750 02/01/21 B2|B 101.375 -0.625 7.457 HUNTSMAN 8.625 03/15/21 B2|B+ 111.375 0.187 4.630KODIAK OIL 8.125 12/01/19 B3|B 109.813 0.125 4.965 CELANESE 6.625 10/15/18 Ba2|BB+ 108.250 0.125 1.820TARGA RES. 6.875 02/01/21 Ba3|BB 107.125 -0.563 4.772 CHEMTURA CORP 5.750 04/15/18 B1|BB- 101.250 0.875 5.442TESORO CORP. 9.750 06/01/19 Ba2|BB+ 109.625 0.000 1.578 HEXION US/NOVA 8.875 02/01/18 B3|CCC+ 104.500 0.625 7.167

NOVELIS 8.750 12/15/20 B2|B 109.938 -0.312 5.602COMMUNICATIONS

CONSUMER CYCLICAL

CEQUEL COM 6.375 09/15/20 B3|B- 101.938 -0.187 5.915CLR CHNNL COM 9.000 03/01/21 Caa1|CCC+ 96.875 -1.688 9.572 CONTINENTAL 6.750 09/15/15 Ba2|BB- 103.523 -0.018 2.894CLR CHNNL WW 7.625 11/15/22 B3|B 104.250 -0.688 6.633 GOODYEAR 8.250 08/15/20 B1|B+ 111.813 0.000 3.429CRICKET COMM. 7.750 10/15/20 Caa1|CCC+ 113.500 -0.063 2.650 HOVNANIAN 7.250 10/15/20 B1|B- 105.688 -0.312 5.923FRONTIER 8.250 04/15/17 Ba2|BB- 113.875 0.125 3.982 LIMITED BRND 6.900 07/15/17 Ba2|BB- 113.000 0.000 3.191INTELSAT JACK. 7.250 10/15/20 B3|B 107.125 -0.438 5.147 JC PENNEY 5.650 06/01/20 Caa2|CCC- 70.688 -4.437 12.127INTELSAT LUX. 6.750 06/01/18 Caa2|CCC+ 104.375 -0.250 5.406 MICHAELS 7.750 11/01/18 B3|B 107.938 -0.062 3.496SIRIUS XM 5.750 04/01/15 B1|BB 99.750 -0.125 5.789 NAVISTAR 8.250 11/01/21 B3|CCC 101.813 0.125 7.672SPRINT 6.900 05/01/19 B1|BB- 104.563 0.438 6.041 RITE AID 9.250 03/15/20 Caa2|CCC+ 114.000 -0.125 4.739UNIVISION 8.500 05/15/21 Caa2|CCC+ 109.875 0.375 5.610 ROYAL CARIBBEAN 9.250 03/15/20 Caa2|CCC+ 113.813 -0.125 4.739

INDUSTRIAL CONSUMER NONCYCLICAL

BOMBARDIER 7.750 03/15/20 Ba2|BB 114.063 0.500 5.196 CONSTELLATION 7.250 05/15/17 Ba1|BB+ 115.813 0.500 2.567CASE NEW HOLL. 7.875 12/01/17 Ba1|BB+ 117.500 0.750 3.265 DEAN FOODS 7.000 06/01/16 B2|B 111.000 0.250 2.582NORTEK INC 8.500 04/15/21 Caa1|B 108.813 -0.125 6.239 PINNACLE 4.875 05/01/21 B3|B- 93.250 -0.438 5.998DANA HOLDING 6.500 02/15/19 B2|BB 107.000 0.000 3.281 SPECTRUM 9.500 06/15/18 Ba3|BB 110.625 -0.188 1.303GRAPHIC PACK. 4.750 04/15/21 Ba3|BB+ 97.375 -0.250 5.193 SUPERVALU 8.000 05/01/16 Caa1|B- 109.938 -0.125 4.192PLY GEM IND. 8.250 02/15/18 B3|B 107.563 0.000 3.475 DEL MONTE 7.625 02/15/19 Caa1|CCC+ 104.188 -0.562 5.719FLORIDA EAST RR 8.125 02/01/17 B3|B- 105.250 -0.188 4.036

YTW 1M AVG

LASTMRTY RATING

LAST PRICE

1 WK PRICE

CH

LAST YIELD TO WORST

LAST YIELD TO WORST

YTW 1M AVG

LAST

ISSUER CPN (%)

MRTY RATINGLAST PRICE

1 WK PRICE

CH

LAST YIELD TO WORST

CPN (%)

MRTY RATINGLAST PRICE

1 WK PRICE

CH

YTW 1M AVG

LAST

YTW 1M AVG

LAST

RATINGLAST PRICE

1 WK PRICE

CH

LAST YIELD TO WORST

(%)

YTW 1M AVG

LAST

RATINGLAST PRICE

1 WK PRICE

CH

LAST YIELD TO WORST

LAST YIELD TO WORST

YTW 1M AVG

LAST

ISSUER CPN (%)

LAST YIELD TO WORST

YTW 1M AVG

LAST

YTW 1M AVG

LAST

LAST YIELD TO WORST

CURRENT YIELD TO WORST

(%)

ISSUER CPN (%)

MRTY

ISSUER CPN (%)

MRTY

ISSUER

ISSUER CPN (%)

MRTY RATINGLAST PRICE

1 WK PRICE

CH

YTW 1M AVG

LAST

ISSUER CPN (%)

MRTY RATINGLAST PRICE

1 WK PRICE

CH

LAST YIELD TO WORST

YTW 1M AVG

LAST

ISSUER CPN (%)

MRTY RATINGLAST PRICE

1 WK PRICE

CH

1 WK PRICE

CH

1 WK PRICE

CH

ISSUER CPN (%)

MRTY RATINGLAST PRICE

ISSUER CPN (%)

MRTY RATINGLAST PRICE

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 13

1 2 3 4 5 6 7 8 9 10 11 12 13 14

eUrOPeAN BONDS srobana ghosh, bLoomberg Data anaLyst

euromarket High-Yield bonds Priced Sept. 18-Oct. 3

ISSUer mAtUrItYISSUeD

rAtINgS LeAD (S)PrICe

YIeLD SPrDCUrreNCY AmOUNt(m) ISSUe LASt

CaLFraC 12/1/2020 Usd 150 B1e - ms/rBC 99.63 99.63 7.566 543

aVaNti 10/1/2019 Usd 370 Caa1 B BarC/JeF/UBs 100.00 101.81 9.594 786

mPt 10/1/2020 eUr 200 Ba1 BB BamL/BBV/dB/JPm/rBC 100.00 102.38 5.338 365

aBeNGoa 2/5/2018 eUr 250 B2e B Citi/ms 100.25 100.25 8.798 772

sPCm 1/15/2022 Usd 250 (P)Ba3 BB+ BamL/BNP 100.00 102.04 5.688 327

VeNeto BaNCa 1/18/2016 eUr 300 - BB dB/iNt/Nat/Nom - 99.85 4.330 365

HaPaG-LLoyd 10/1/2018 eUr 250 (P)Caa1 B- Citi/dB/JPm 100.00 103.57 6.896 553

LaFarGe 9/30/2020 eUr 750 Ba1 BB+ BBV/Bss/Com/HsBC/iNG/mit/Nat/rBs/UNi 99.55 102.48 4.330 264

soHo HoUse 10/1/2018 GBP 115 (P)Caa1 (P)B- imP 100.00 102.69 8.450 670

PHosPHorUs 4/1/2019 GBP 205 (P)Caa2 CCC+ Gs/LLo 99.00 99.46 10.138 826

Source: Bloomberg LP NIM<GO>

Goldman Rises, JPMorgan Falls in europe bond Ranking Jan. 1-Oct. 4

UNDerWrIter rANK rANK 1-Yr eArLIer

SHAre (%)

PrOCeeDS ($BN)) ISSUeS

deutsche Bank 1 1 8.3 9.00 77

Goldman sachs ▲ 2 3 8.3 8.99 64

JPmorgan ▼ 3 2 8.1 8.81 76

Citi 4 4 6.0 6.50 41

Credit suisse ▲ 5 12 5.8 6.34 53

BNP Paribas ▲ 6 7 5.7 6.23 55

morgan stanley ▼ 7 5 5.5 5.95 38

Barclays ▼ 8 6 4.9 5.30 50

HsBC ▲ 9 11 4.5 4.91 44

BamL ▼ 10 9 4.4 4.84 45

Source: Bloomberg LP LEAG <GO>

european High-Yield bond Pipeline

ISSUerAmOUNt

LeAD (S) ANNOUNCeDCUrreNCY (mm)

oBertHUr eUr 200 HsBC,Nat 10/2/2013

BioseV Usd 500 BNP,Bra,Citi 9/30/2013

NoKia eUr 500 - 9/6/2013

NoKia eUr 500 - 9/6/2013

NoKia eUr 500 - 9/6/2013

Laser CoFiNoGa eUr ─ BNP,HsBC,Nat 9/4/2013

NaKed wiNes GBP 3 - 9/2/2013

Source: Bloomberg LP PREL<GO>

HEDGE FUNDSNEWS, ANALYSIS, AND COMMENTARYBRIEF NEWSLETTERS FOR PROFESSIONALS, FROM PROFESSIONALS. BRIEF<GO> WWW.BLOOMBERGBRIEFS.COM

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK

10.07.13 www.bloombergbriefs.com Bloomberg Brief | Leveraged Finance 14

1 2 3 4 5 6 7 8 9 10 11 12 13 14

eUrO-DeNOmINAteD JUNK BOND tOtAL retUrNS BY SeCtOr bLoomberg Data

JPMORGAn euRO HiGH YieLd index-SeCtOR RetuRnS And CHARACteRiStiCS october 3, 2013

SeCtOr JP mOrgANtICKer StW (BP) YtW (%)

tOtAL retUrN, % [1,2]

1 WeeK 1m 3m YtD automotive CeUraUto 355.89 4.03 0.30 1.27 4.21 6.93Broadcast CeUrBrdC 543.00 5.55 0.11 1.43 4.31 8.93Cable/satellite CeUrCBLe 507.00 5.59 0.17 1.18 4.07 6.30Chemicals CeUrCHem 605.00 6.43 -0.03 0.86 3.87 13.49Consumer Prod. CeUrProd 718.00 7.64 0.34 2.57 6.17 5.62diverse media CeUrdVmd 795.00 8.59 0.21 2.53 4.42 -14.63energy CeUreNer 471.00 5.04 0.20 1.35 4.48 5.15Financial CeUrFiNL 473.00 5.50 1.11 1.91 5.23 8.76Food & Bev CeUrFdBV 452.49 4.98 0.31 1.01 5.33 9.60Gaming/Leisure CeUrGame 1,556.00 15.87 0.30 0.63 0.26 -3.37Healthcare CeUrHLtH 434.00 4.99 0.13 0.84 3.66 5.52Housing CeUrHoUs 328.00 3.81 0.26 0.96 2.70 4.14industrials CeUriNdU 469.08 5.38 0.41 2.24 5.22 8.66metals/mining CeUrmetL 425.00 4.82 0.25 1.97 5.16 4.53Paper & Pack CeUrPaPr 586.25 6.38 0.12 1.09 3.86 4.23retail CeUrretL 498.00 5.52 0.02 1.33 3.13 5.59services CeUrserV 594.00 6.39 0.37 1.61 6.02 10.52technology CeUrteCH 469.95 5.42 0.10 1.82 8.81 12.87telecom CeUrtLCm 504.96 5.50 0.69 2.74 6.04 9.81transportation CeUrtraN 670.00 7.19 0.27 1.96 7.56 11.83Utility CeUrUtiL 422.00 4.90 0.57 1.34 4.17 7.71

senior secured CeUrsNsC 638.00 6.84 0.28 1.82 5.19 7.35senior CeUrseNr 415.00 4.69 0.30 1.31 4.22 6.77senior sub CeUrsNsB 528.00 6.26 1.59 3.06 7.69 15.09Junior sub CeUrJrsB 567.00 5.96 -0.21 0.64 2.18 3.95

developed CeUrdm 493.00 5.48 0.40 1.61 4.76 7.26emerging CeUrem 665.00 7.15 0.17 1.54 4.24 7.96

BB CeUrBB 327.00 3.87 0.33 1.03 3.24 4.86B CeUrB 588.00 6.38 0.26 1.89 5.95 8.39CCC CeUrCCC 916.00 9.65 0.51 3.28 8.88 11.74euro High Yield CeUrHYI 501.00 5.56 0.39 1.61 4.73 7.31

Source: JPMorgan Bond Indices

Notes:1)Monthly and yTD performance data is as of last fully completed monthly period.2)Green / red color coding represents performance ranking of the top/bottom three sectors in the period.

The JPMorgan euro High-yield index rose for a fifth straight week, gaining 0.39 percent on a total return basis. The yield to worst lost 5 basis points to 5.56 percent. The top gainers were the financial and telecom sectors, with returns of 1.11 and 0.69 percent, respectively. Chemicals, the only industry to decline, lost

3 basis points. Junior subordinated debt remained the worst per-forming rank for a second week, with a 0.21 percent drop. Triple Cs outperformed single and double bs with 0.51, 0.26 and 0.33 percent returns, respectively.

— Aselya Kerimkulova, Benedict Metuh, Bloomberg Data Analysts

WHO GETS PAID BEFORE YOU DO?

This document is being provided for the exclusive use of DAVID HOLLEY at BLOOMBERG/ NEWSROOM:NEW YORK