theories and methods of the business cycle. part 1: dynamic stochastic general equilibrium models...

Post on 18-Dec-2015

213 views

TRANSCRIPT

Theories and Methods of the Business Cycle.Part 1: Dynamic Stochastic General Equilibrium ModelsIV. A New Neoclassical Synthesis?

Jean-Olivier HAIRAULT, Professeur à Paris I Panthéon-Sorbonne et à l’Ecole d’Economie de Paris (EEP)

1. Introduction

The RBC theory is at odds with the neoclassical synthesis

Real shocks vs. Monetary shocks

Optimal vs. Suboptimal fluctuations

RBC theory has not totally convinced that technology shocks can alone drive the business cycle. The internal mechanisms of the neoclassical growth model does not lead to fluctuations totally consistent with the stylized facts when calibration is seriously done.

The correlation between hours and labor productivity is too high

The response of output does not display a hump-shaped profile

How to reconcile theory with the numerous empirical works which show the non-neutrality of money (in particular in the VAR framework)? Gali [1989], Quarterly Journal of Economics

1. Introduction

Along the development of RBC theory in the 80’s, keynesianism was

looking for micro-foundations

How to get market failures when agents are assumed to optimize?

Imperfect information, imperfect competition, strategic behaviors,…New-

Keynesianism based on real and nominal rigidities. Ball and Romer [1990],

Review of Economic Studies

Non-walrasian features in the good market (monopolistic competition), the

labor market (search frictions), the credit market (adverse selection and

moral hazard)

Mainly theoretical works as new-keynesianism has to address the Lucas’

critique.

What a challenge to overcome RBC theory with their own methodology!

The 90’s was the decade during which a new neoclassical synthesis occurs:

intertemporal choices and strategic behaviors

2. Equilibrium unemployment

Employment volatility represents 70% of total hours

volatility

Hours indivisibility à la Hansen [1985]

Do efficiency wages better explain the relative volatility of

hours to labor productivity? Danthine and Donaldson

[1990], European Economic Review. Employment is not

volatile enough in their model

Efficiency wages are rigid in the sense they do not clear the

labor market, but they are elastic to technology shocks.

Fluctuations generated by the model are essentially the

same as those of the RBC canonical model.

2. Equilibrium unemployment

Equilibrium unemployment, Pissarides [1990], Equilibrium

unemployment theory, Basil Blackwell

Hirings take time as there is imperfect information in the

process of search: search unemployment

Search frictions could explain the persistence of

fluctuations

Merz [1995], Journal of Monetary Economics, Andolfatto

[1996], American Economic Review

2. Equilibrium unemployment

Hirings depend on vacancies (V) and unemployed people (U), but also the

search intensity (e) of these latter.

The participation rate is constant and exogenous.

The probability to have a job is:

The probability to contact a worker:

There are externalities in the search process

p depends positively on the number of vacancies (complementarity) and

negatively on the number of unemployed workers (congestion)

q depends negatively on the number of vacancies and positively on the

number of unemployed workers (congestion)

2. Equilibrium unemployment

The dynamics of employment depends on hirings (a

combination of unemploment and vacancy) and on firings

(a fixed proportion s of the employment stock)

2. Equilibrium unemployment

Representative household (risk-sharing due to the large

scale of the household)

First order conditions are the same as those in the

canonical RBC model, except there is no labor supply, no

partipation decision and hours are negociated between

households and firms (as wage)

2. Equilibrium unemployment

The production function is traditional and combines total

hours and capital.

Firm labor demand is no more static, as they invest in

vacancies. The firm program is now intertemporal.

Labor demand is now determined by the intertemporal

condition:

2. Equilibrium unemployment

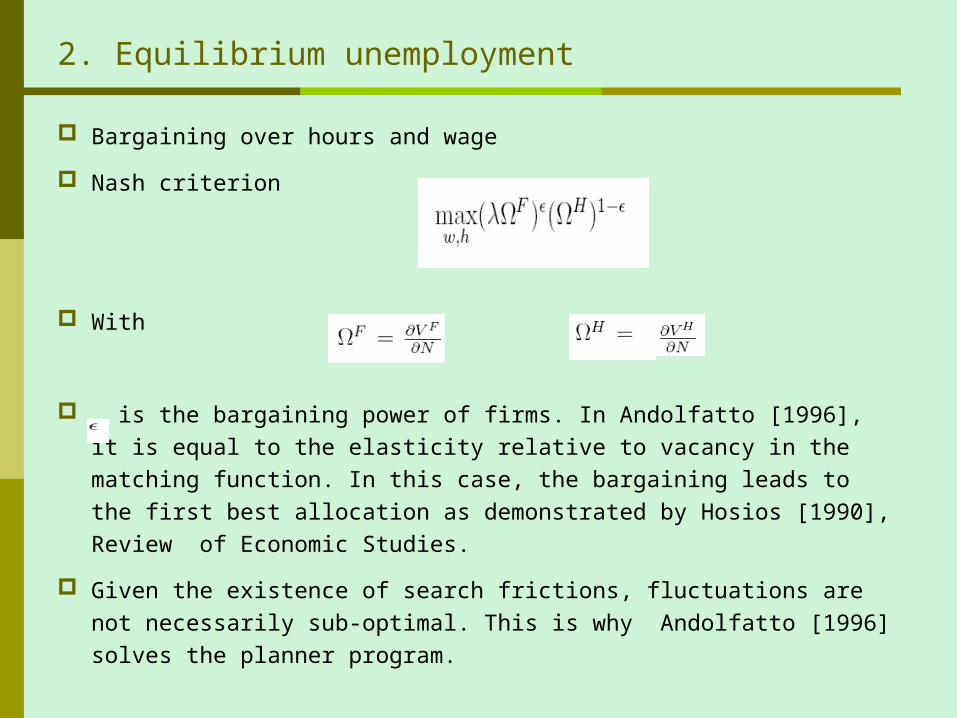

Bargaining over hours and wage

Nash criterion

With

is the bargaining power of firms. In Andolfatto [1996], it is equal to the elasticity relative to vacancy in the matching function. In this case, the bargaining leads to the first best allocation as demonstrated by Hosios [1990], Review of Economic Studies.

Given the existence of search frictions, fluctuations are not necessarily sub-optimal. This is why Andolfatto [1996] solves the planner program.

2. Equilibrium unemployment

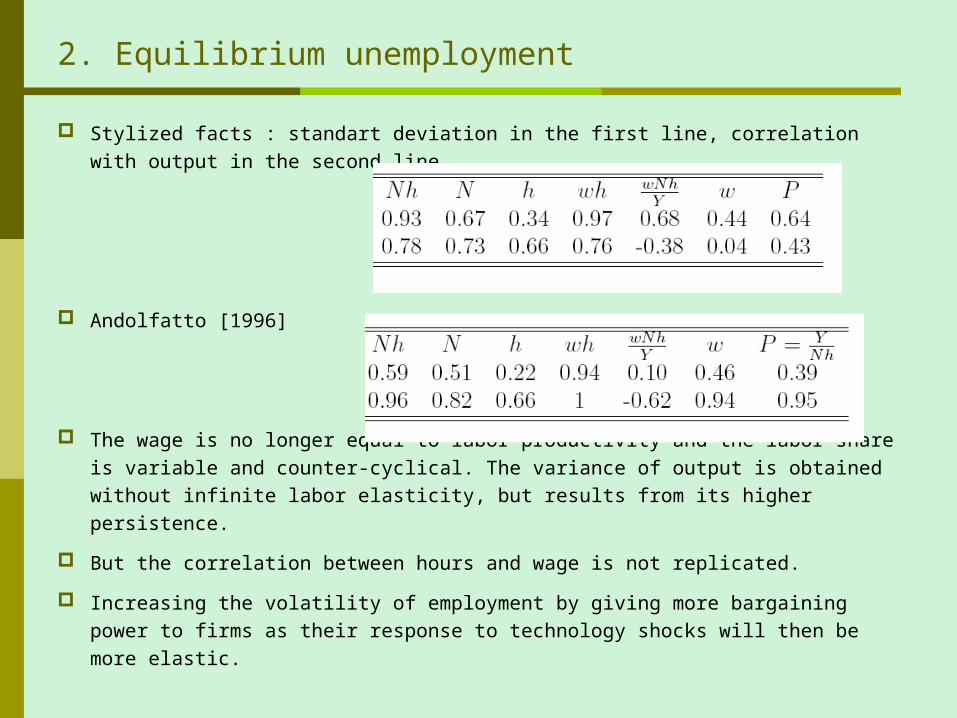

Stylized facts : standart deviation in the first line, correlation with output in the second line

Andolfatto [1996]

The wage is no longer equal to labor productivity and the labor share is variable and counter-cyclical. The variance of output is obtained without infinite labor elasticity, but results from its higher persistence.

But the correlation between hours and wage is not replicated.

Increasing the volatility of employment by giving more bargaining power to firms as their response to technology shocks will then be more elastic.

2. Equilibrium unemployment

Productivity cycle and Beveridge curve

Stylized facts

Model’s predictions: the productivity cycle is not replicated

contrary to the Beveridge curve

3. Perfect Insurance

Complete markets: perfect risk sharing

B is the amount of insurance whose price is tau.

1-alpha= s for employed workers; 1-alpha = 1-p for

unemployed workers

Two insurance schemes: profit =

The budgetary constraints:

3. Perfect Insurance

First-order conditions:

Risk-sharing condition

For s = n, u

These conditions imply that the capital choices are identical

whatever their employment status. For separable utility fonction,

consumptions are the same, and the unemployed workers are

better off. See Chéron and Langot [2002], Review of Economic

Dynamics for a case where their welfare is lower than that of

employed workers.

3. Perfect Insurance

Given these optimal choices, the budgetary constraints can

be rewritten as follows:

It can be noticed that:

The representative household program is then:

4. Monopolistic competition and nominal rigidities

Considering VAR studies (following the seminal article of Sims [1980], Econometrica), money supply shocks would impact the output. J. Gali [1992], Quarterly Journal of Economics, Bec and Hairault [1993], Annales d’Economie et Statistiques [1993]

Taking into account money supply shock in DSGE models implies to have money demand theoretical foundations: Why do we hold money ? Old issue in economics…

Money reduces transaction or search costs in the good market: Kiyotaki and Wright [1989], Journal of Political Economy

More tractable in DSGE models, cash-in-advance constraint can be added in the household program, Cooley and Hansen [1989], American Economic Review:

Without any nominal rigidities, this approach fails to generate a positive and strong response of output after a positive monetary (supply) shock. Only the inflation tax propagation mechanism which is a negative wealth effect: positive response of labour supply and output, but very weak effects.

4. Monopolistic competition and nominal rigidities

(Inflation tax +) nominal rigidities: prices are rigid due to

menu costs (New-Keynesian approach) (an alternative:

rigidity of the nominal wage due to the existence of wage

contracts)

This implies to consider imperfect competition in the good

market: monopolistic competition in the line of Blanchard

and Kiyotacki [1897], American Economic Review

Nominal rigidities + monopolistic competition in DSGE:

Hairault and Portier [1993], European Economic Review

4. Monopolistic competition and nominal rigidities

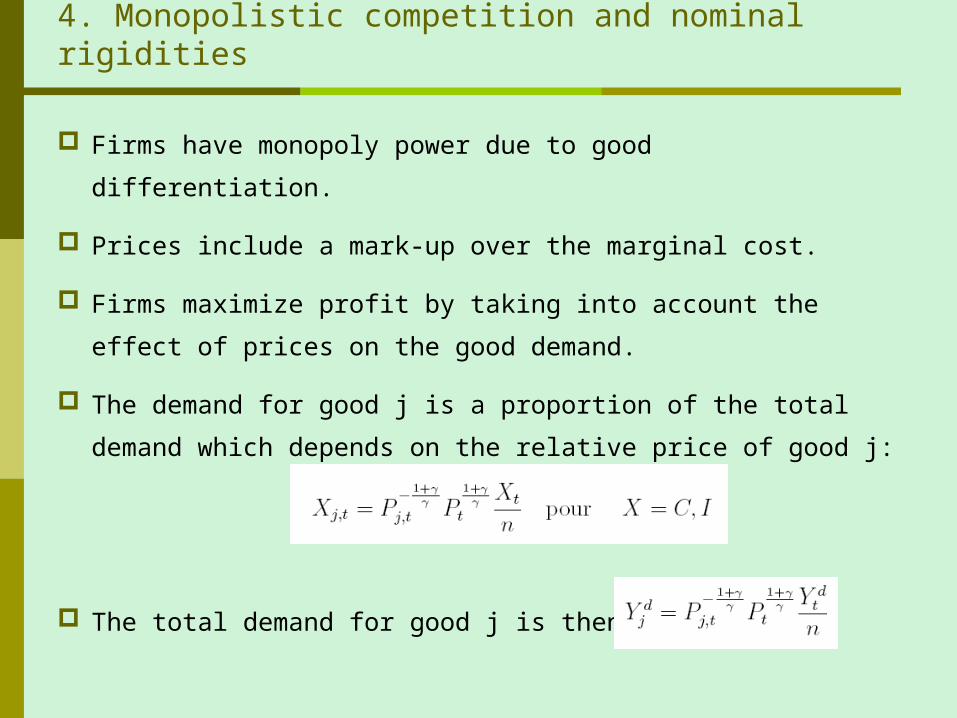

Firms have monopoly power due to good differentiation.

Prices include a mark-up over the marginal cost.

Firms maximize profit by taking into account the effect of

prices on the good demand.

The demand for good j is a proportion of the total demand

which depends on the relative price of good j:

The total demand for good j is then:

4. Monopolistic competition and nominal rigidities

The nominal profit of firm j is:

Due to the presence of adjustment costs on prices, firm

choices are now intertemporal:

4. Monopolistic competition and nominal rigidities

The first-order conditions are :

Prices are not equalized to marginal costs:

4. Monopolistic competition and nominal rigidities

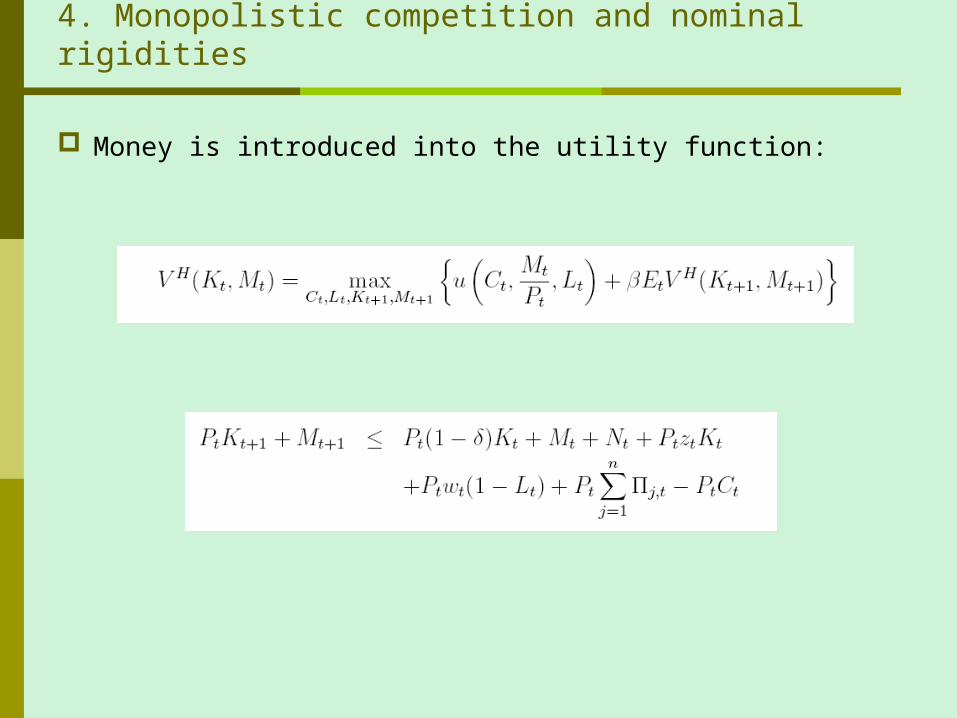

Money is introduced into the utility function:

4. Monopolistic competition and nominal rigidities

The first-order conditions are:

The money supply process is:

4. Monopolistic competition and nominal rigidities

The Solow Residual is no longer a pure measure of

technology. The factor elasticities are not consistently

measured by factor shares in total revenues due to the

existence of markups.

The naive SR is contamined by money supply shocks as

these latter make markups counter-cyclical in the business

cycle

After a money supply shock, firms want to increase prices

in order to leave unchanged their mark-up. As there exist

adjustment costs on prices, prices do not increase as much

as invariant mark-up would imply. Markups are weaker than

at the steady state.

4. Monopolistic competition and nominal rigidities

Stylized facts

Model’s predictions

5. Financial imperfections

Limited participation and money supply shocks

Fuerst [1992], Journal of Monetary Economics, Christiano

and Eichenbaum [1992], American Economic Review

The nominal and real interest rates decline after a positive

monetary shock in empirical studies

5. Financial imperfections

The nominal and real interest rates decline after a positive

monetary shock since the supply of deposits is pre-

determined

Firms rent wages

R

Dd, Ds

5. Financial imperfections

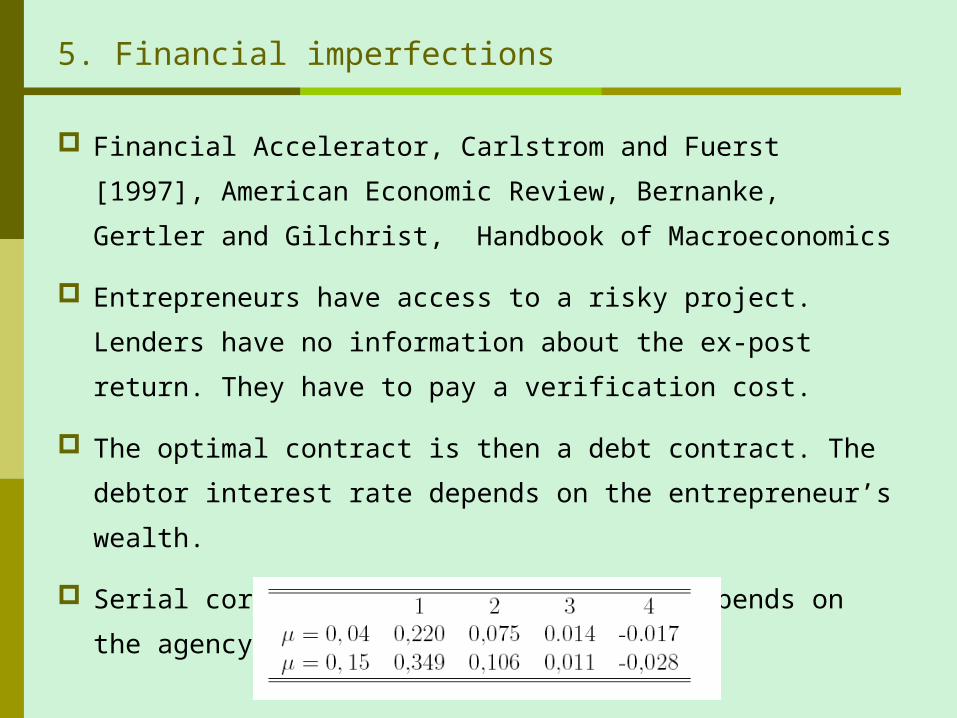

Financial Accelerator, Carlstrom and Fuerst [1997],

American Economic Review, Bernanke, Gertler and

Gilchrist, Handbook of Macroeconomics

Entrepreneurs have access to a risky project. Lenders have

no information about the ex-post return. They have to pay a

verification cost.

The optimal contract is then a debt contract. The debtor

interest rate depends on the entrepreneur’s wealth.

Serial correlation of output growth depends on the agency

costs:

6. Sunspot and fluctuations

Self-fulfilling propheties, Farmer and Guo [1994], Journal of

Economic Theory

Animal spirits at the heart of the business cycle

Extrinsic shocks vs. Shocks on fundamentals

Indeterminacy of the equilibrium: too many eigenvalues inferior to

1 (more than the number of pre-determined variables).

Sunspot equilibria can arise in this case.

This approach must be distinguished from news about the future

of some fundamentals, see Hairault, Langot and Portier [1997],

Journal of Economic, Dynamics and Control, Beaudry and Portier

[2006], American Economic Review

6. Sunspot and fluctuations

Final good is produced by using intermediated inputs

Production of these inputs under increasing return to scale

and monopolistic competition

The reduced form of the model is :

with

6. Sunspot and fluctuations

If the labor elasticity is small enough relative to a, ie the

labor demande curve is increasing with a slop superior to

that of the labor supply curve, the eigenvalues are strictly

inferior to one and sunspot equilibria exist

7. Business cycle costs

Stabilization of business cycle? What does it mean in the DSGE framework?

Welfare criterion must be considered, and not volatility criterion, especially the output volatility

Business cycle costs are very small in terms of stationary consumption; eliminating all fluctuations is equivalent in welfare units to 0.008% of the steady state consumption, Lucas [1987], Models of Business Cycles, Basil Blackwell.

This implies that the distorsions introduced by the stabilization policy must be very small too.

Harberger triangles could be much more important than Okun gaps, Greenwood and Huffman [1991], Journal of Monetary Economics.

« I argue in the end that, based on what we know now, it is unrealistic to hope for gains larger than a tenth of a percent from better countercyclical policy » Lucas [2003], American Economic Review

7. Business cycle costs

Reis [2007]

7. Business cycle costs

7. Business cycle costs

7. Business cycle costs

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles

8. Okun Gaps and Harberger triangles