the whitlock company what health care reform means for your business

Post on 22-Dec-2015

213 views

TRANSCRIPT

The Whitlock Company

WHAT HEALTH CARE REFORM MEANS FOR YOUR BUSINESS

The Whitlock Company

Definitive Healthcare Update

Overview• Small employer tax credit• W-2 changes• Changes to HSA’s• 1099 changes• Medicare payroll tax• Medicare tax on net investment income• Employer required health insurance coverage

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDITEffective 1/1/2010

Incentive for small businesses to provide their employees with group health insurance coverage

Businesses with 10 or less full-time-equivalent (FTE) employees– Average annual earnings less than $25,000 a year– Maximum credit of 35% of health insurance costs

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDITEffective 1/1/2010

Credit phase-out

Companies with FTEs between 11 and 25 workers– average annual wages of up to $50,000 – eligible for partial credits

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDIT (cont.)Effective 1/1/2010

TAX EXEMPT EMPLOYERS-Same criteria for FTEs and annual wages-Reduced credit rate of 25% -More guidance to be issued on how to claim the credit

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDITEffective 1/1/2010• Employer must pay at least 50% of health insurance

premiums• Credit

– Offsets Income tax liability only– Can NOT offset employment taxes (941, etc.)– Will flow through for partnerships and S Corporations to

shareholders– Non-refundable – Reduces insurance tax expense deduction

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDITEffective 1/1/2010• Employer meets the FTE test as long as FTEs are less

than 25 (total employees may be more than 25 considering part time individuals)

• Owner-types are excluded from FTE count:– Owners– Partners/members – > 2% shareholders – Owner’s family or household members

The Whitlock Company

Definitive Healthcare Update

SMALL BUSINESS TAX CREDIT (cont.)Effective 1/1/2010

Calculation of creditDetermine Full Time Equivalents (FTEs)1. Calculate total hours worked per employee2. Divide by 2080 to determine FTEs

Determine Average Wages3. Calculate total FICA wages paid to all employees4. Divide by FTEs

The Whitlock Company

Definitive Healthcare Update

EXAMPLE #1 (Full credit)

Facts:# of Employees Annual

Hours/Employee Total Hours Limited to 2,080/employee

5 2,080 10,400 10,400

3 1,040 3,120 3,120

1 2,300 2,300 2,080

9 15,820 15,600

The Whitlock Company

Definitive Healthcare Update

EXAMPLE #1 Answer Calculation:

Total Hours 15,600Full-Time Hours (divided by) 2,080FTE 7.50FTE Rounded Down 7

The Whitlock Company

Definitive Healthcare Update

EXAMPLE #1 AnswerFacts:

Total Wages 150,000FTE 7

Calculation:Total Wages 150,000FTE (divided by) 7Avg Wages 21,429Avg Wages (Rounded Down to nearest 1000) $21,000

The Whitlock Company

Definitive Healthcare Update

EXAMPLE #1 AnswerFTE 7Average Annual Wages 21,000Health Care Premiums – Employer Paid 40,000

Calculation:Health Care Premiums 40,000Allowable Credit Percentage 35%Credit $14,000

The Whitlock Company

Definitive Healthcare Update

EXAMPLE #2 (Partial Credit)

Facts:FTE 12Average Annual Wages 30,000Health Care Premiums – Employer Paid 40,000

The Whitlock Company

Definitive Healthcare UpdateEXAMPLE #2 (Partial Credit)

Credit Calculation:40,000 * 35% = 14,000Credit Reduction for FTE greater than 10:14,000*((12-10)/15) = 1,866Credit Reduction for Average Wages greater than $25,00014,000*((30,000 – 25,000)/25,000) = 2,800Total Credit Reduction:1,866 + 2,800 4,666Total 2010 Tax Credit:14,000 – 4,666 = $9,334

The Whitlock Company

Definitive Healthcare Update

REPORTING HEALTH CARE BENEFITS ON W2sEffective in 2011, reporting in January 2012• Employers responsible for reporting the value of the health care benefits they provide to employees on their 2011 W2

The Whitlock Company

Definitive Healthcare Update

REPORTING HEALTH CARE BENEFITS ON W2sEffective in 2011, reporting in January 2012

• Reporting requirement does not make the amount taxable to the employee

The Whitlock Company

Definitive Healthcare Update

REPORTING HEALTH CARE BENEFITS ON W2sEffective in 2011, reporting in January 2012• Update payroll systems effective 1/1/2011 for

reporting purposes (discuss with software vendor if applicable)

• Where do you get the values for the W2?– Health insurance company for fully insured plans– Third party administrators for self-funded plans

The Whitlock Company

Definitive Healthcare Update

REPORTING HEALTH CARE BENEFITS ON W2s

• Health plans that are NOT included on W2:– Flexible spending amounts– Specified illness or disease, (i.e. cancer)– Disability insurance– Workers’ compensation

The Whitlock Company

Definitive Healthcare Update

REPORTING HEALTH CARE BENEFITS ON W2s

Possible W2’s for Non-Employees?This issue will be spelled out in later regulations• Retirees• COBRA participants

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTINGEffective at 1/1/2012 for January 2013 1099 reporting• New requirement considered as a “pay for” to

provide other tax cuts • Joint Committee on Taxation estimates it will raise

$17 to $19 billion in additional revenue• Will effect every business at this point unless

legislation is changed

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTINGEffective at 1/1/2012 for January 2013 1099 reporting

PRIOR LAW• Payments in excess of $600• Payments to corporations were exempt from

reporting requirement• Generally issued for services (i.e. contract labor),

rent, interest

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTINGEffective at 1/1/2012 for January 2013 1099 reporting

NEW LAW• Payments in excess of $600• No corporate exemption (All vendors to receive

1099s)• Payments for ALL goods, services, and property to

be reported

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTING Effective at 1/1/2012 for January 2013 reporting

Could dramatically increase accounting and reporting costs to all businesses. START PLANNING NOW

Example: Small business owner selling collision parts speaking to Senate leaders “I am going to go from preparing four 1099 forms to somewhere over 200.”

The Whitlock Company

Definitive Healthcare Update

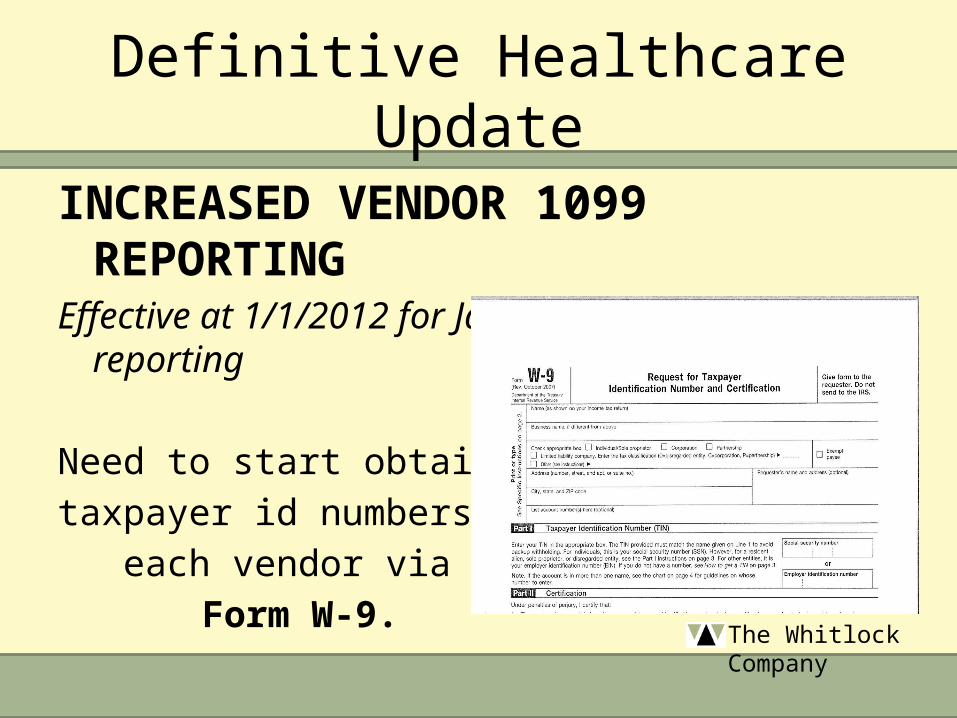

INCREASED VENDOR 1099 REPORTINGEffective at 1/1/2012 for January 2013 1099 reporting

Need to start obtaining taxpayer id numbers for each vendor via

Form W-9.

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTINGEffective at 1/1/2012 for January 2013 1099 reporting

This process would need to be completed by 1/1/2012 in order for accounting software to capture data.

Back-up withholding may be required for any vendor not supplying their federal ID number before payment is made to that vendor.

The Whitlock Company

Definitive Healthcare Update

INCREASED VENDOR 1099 REPORTING

PROPOSED LEGISATION Fully Repeal

ORExempt Companies with fewer than 25 employees and

Companies with more than 25 employees raise reporting amount from $600 to $5,000

Credit card purchases to be exempt

The Whitlock Company

Definitive Healthcare Update

OVER THE COUNTER MEDICATIONSEffective beginning 1/1/2011• Ban on OTC medication reimbursed from:– Flexible spending accounts (FSAs) through a cafeteria plan– Health reimbursement arrangements (HRA)– Health savings accounts (HSA)

Unless the physician formally prescribes the OTC medications

The Whitlock Company

Definitive Healthcare Update

HEALTH SAVINGS ACCOUNTSEffective beginning 1/1/2011

• Penalties increase to 20%– for non- medical distributions from • Archer MSAs (medical savings accounts) • HSAs (health savings accounts)

The Whitlock Company

Definitive Healthcare Update

MEDICARE PAYROLL TAXEffective in 2013• New tax 0.9% wages – Not matched by employer– 401K (deferred comp) are EXEMPT*– In addition to 1.45% Medicare tax w/hldg

• Employer must:– Withhold on wages over $200,000 for an employee

The Whitlock Company

Definitive Healthcare UpdateMEDICARE PAYROLL TAXEffective in 2013

• Wage threshold amounts :– $200K for single– $250K for married filing jointly– $125K for married filing separately

• Individuals must:– Compute 0.9% tax on aggregate wages on Form 1040– Any balance due, pay with 1040– Consider higher estimated tax payments

The Whitlock Company

Definitive Healthcare Update

MEDICARE PAYROLL TAX

EXAMPLE:Jack has $200k W-2 from XYZ CorporationSally, his wife, has $210k W-2 from ABC Corporation

XYZ withholds no 0.9% tax: $200,000 – 200,000 = no excess, no tax

ABC withholds 0.9% tax:($210,000 – 200,000) = $10,000 excess x .9% = $90 medicare tax withheld

cont…

The Whitlock Company

Definitive Healthcare Update

EXAMPLE: cont…1040 – Married filing jointlyCompute their additional tax:

Jack’s W-2 $200,000Sally’s W-2 210,000Total wages 410,000Threshold for MFJ 250,000 Taxable portion 160,000

x _ 0.9%Total tax 1,440

Less (Sally’s withholding) - 90Balance due 04/15 $ 1,350

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON “NET INVESTMENT INCOME”

Effective in 2013• 3.8% Medicare tax in ADDITION to all other Medicare

taxes• Tax is based on “net investment income” for

- individuals- estates- trusts

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON “NET INVESTMENT INCOME”Effective in 2013

What is “Net Investment Income”?• Interest income• Dividend income• Annuity income• Royalty income• Rent income• Net gains (ordinary and capital) sale of property• Passive investment income • Commodity trading

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON “NET INVESTMENT INCOME”Effective in 2013

Exemptions:• Sale of a personal residence • Gains on sale of business if “active participation”• Interest income on municipal bonds• IRA, qualified retirement plan distributions• Income subject to self-employment tax• Nonresident aliens

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON “NET INVESTMENT INCOME”

Effective in 2013

Tax computed on the lesser of:• An individual’s “net investment income”• OR the excess of the individual’s modified

adjusted gross income (AGI) over threshold amounts

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON “NET INVESTMENT INCOME”

Effective in 2013• Threshold amounts are the same as the 0.9%

Medicare payroll tax:• $200K for single • $250K for married filing jointly • $125K for married filing separately

The Whitlock Company

Definitive Healthcare Update

MEDICARE TAX ON NET INVESTMENT INCOMEEffective 2013

EXAMPLE:Sally is single:

ABC Corp W-2 $180,000XYZ Corp W-2 __ 50,000 Total wages 230,000Interest and dividend income 250,000Modified AGI $ 480,000

The Whitlock Company

Definitive Healthcare Update

MEDICARE NET INVESTMENT INCOME TAXEXAMPLE (cont.)

She will owe the lesser of: Net investment income of $250,000

x 3.8% $ 9,500

ORModified AGI $480,000

x__ 3.8% $ 18,240

The Whitlock Company

Definitive Healthcare UpdateMEDICARE NET INVESTMENT INCOME TAX COMBINED WITH PAYROLL TAX:

Sally owes $9,500 for NII Medicare Tax, plus the 0.9% Medicare payroll tax calculated below:

Total wages (180k + 50k) $ 230,000Less threshold for single - 200,000

30,000x 0.9%

Medicare payroll tax due $ 270Sally owes $9,770 for both.

The Whitlock Company

Definitive Healthcare Update

NEW LIMITS ON CAFETERIA PLANSEffective 1/1/2013New limits for health portion of FSA (cafeteria plans)

deferrals• OLD LAW:– No limit on election amount

• NEW LAW:– $2,500 limit per year– Amount indexed for inflation after 2013

The Whitlock Company

Definitive Healthcare Update

LARGE EMPLOYER MANDATEEffective 1/1/2014• To avoid health insurance excise taxes, large

employers must provide:– At least 50% of health insurance premium AND– At least 60% of the plan’s share of total allowed cost

of benefits of plan

– OR if the minimum essential coverage is unaffordable for the employee

The Whitlock Company

Definitive Healthcare Update

LARGE EMPLOYER MANDATEEffective 1/1/2014

Who is a Large Employer?Defined as a business employing:• average of at least 50 full-time employees• during the preceding calendar yearWhat is considered “full-time”?• Full-time means work at least 30 hours per week• All other employees counted on prorated basis

The Whitlock Company

Definitive Healthcare Update

LARGE EMPLOYER MANDATEEffective 1/1/2014

The Excise Taxes (penalty/fine):Excise tax of a maximum of $2,000 per employee, per year

• The first 30 employees don’t count in the penalty

$2,000 Excise tax amountx 1/12 Monthly portionx # of months not providing insur benefitx (Total employees – 30*) *reduction provided by Act= Total excise tax for that year

The Whitlock Company

LARGE EMPLOYER MANDATEEffective 1/1/2014

Additional $3,000 penalty for lower income employees if:

•Receive subsidies OR•Purchase insurance direct from insurance exchanges

Definitive Healthcare Update

The Whitlock Company

Definitive Healthcare Update

LARGE EMPLOYER MANDATEEffective 1/1/2014

Effect on “Small” Businesses: Most small businesses = fewer than 50 employees

Don’t HAVE to provide health insuranceBUT - there are the incentives:– tax credits – shopping the health insurance exchanges

The Whitlock Company

Definitive Healthcare Update

What to Do NowFinancially:• Consider whether to apply for tax credits• Analyze cost to offer insurance or not• Decide how to handle 1099’s• Owners need to consider personal tax effects

for tax planning in their future