the webinar will start shortlyapi.ning.com/files/iufm5vldqwlmakaqszuf7xwy3dtxhmwhxulhzvl… ·...

TRANSCRIPT

Welcome to: What works for smallholders and agribusiness?

The Webinar will start shortly

Jessica Graf Hugh Scott Caroline Ashley

Join the discussion on Twitter #Smallholdersuccess

What works for smallholders and agribusiness?

Speakers: Jessica Graf: Network Partner, Hystra Hugh Scott: Director, African Enterprise Challenge Fund

Webinar Structure: Quiz & Insights on 5 topics Questions and discussion

Join the discussion on Twitter #Smallholdersuccess Type your questions in ‘chat’ anytime

2

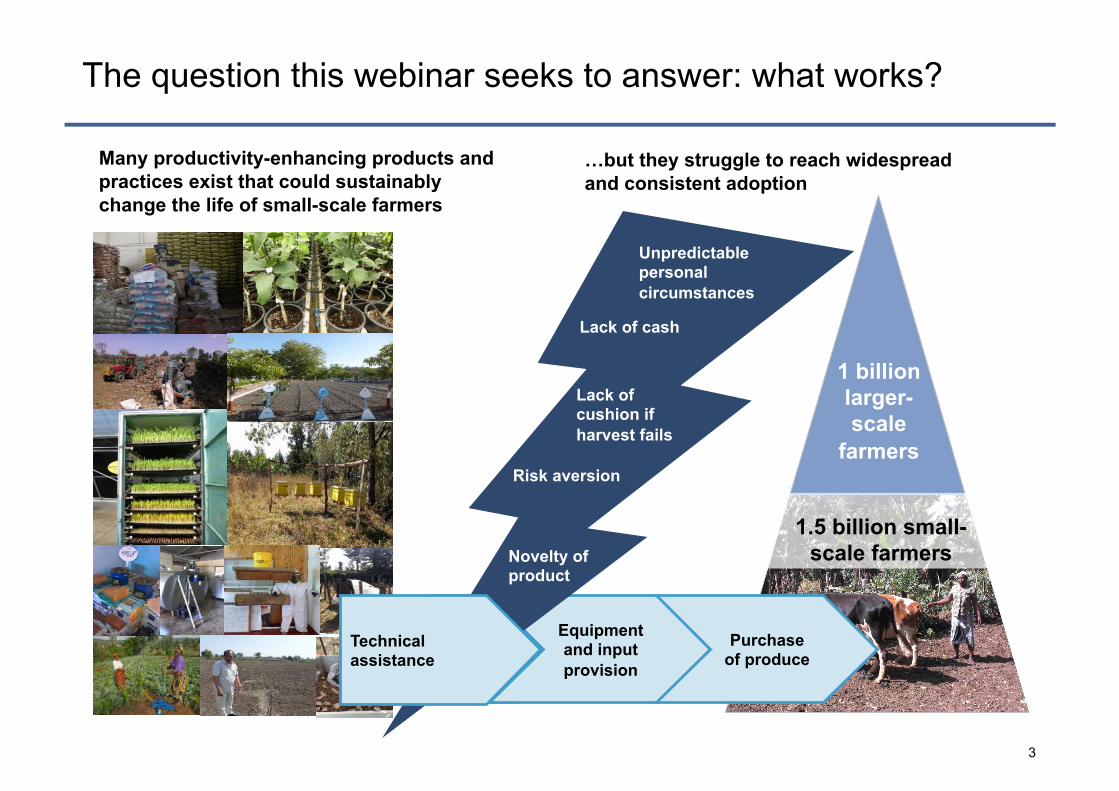

The question this webinar seeks to answer: what works?

1 billion larger-scale

farmers

1.5 billion small-scale farmers

Equipment and input provision

Purchase of produce

Novelty of product

Unpredictable personal circumstances

Lack of cushion if harvest fails

Risk aversion

Lack of cash

Technical assistance

3

Many productivity-enhancing products and practices exist that could sustainably change the life of small-scale farmers

…but they struggle to reach widespread and consistent adoption

∂∂∂∂

∂∂

Empresa de Comerciali-zação Agricola (ECA)

4

Analysed 15 pioneer organizations working in 15+ commodities with 2 million small-scale farmers

The AECF’s has a large portfolio of agribusiness and related projects

Adapta(on7% 48 Inputsupply

21 Outgrower

46 Agro-processing

7 Distribu6onandmarke6ng

4 Financialservices

6 Informa0on

132 Agribusiness+related

$100m+ net benefit to 1.1m smallholders

Agribusiness 122

Information 6

Financial services

20

Renewable energy

30

Adaptation 30

2014

And now for the Quiz…

We want to hear from you too! Click on the link in the chat box >>>>

1. CAN BUSINESSES MAKE MONEY BY WORKING WITH SMALL FARMERS (as sellers or buyers)?

2. WHAT IS THE SINGLE BIGGEST LEVER TO INCREASE THE PROFITABILITY OF FARMERS?

3. WHY SOME PROJECTS STRUGGLE TO REACH HIGH PENETRATION?

4. HOW MUCH DO ORGANIZATIONS SPEND ON TRAINING FARMERS (as % of product bought from or input provider’s sales to farmers)?

5. WHAT ARE EFFECTIVE STRATEGIES TO DEAL WITH “DEFAULTERS”?

6

QUESTION 1: CAN BUSINESSES MAKE MONEY BY WORKING WITH SMALL FARMERS (as sellers or buyers)

a. No

b. Yes, but in a limited fashion

c. Yes, and often in significant ways

7

Seller 3

Seller 2

Seller 1 3.3x

4x

The organizations working with small farmers also derive significant benefits

24%

20%

11%

2.5%

5%

2%

2.5%

Buyer 6

Buyer 5

Buyer 4

Buyer 3

Buyer 2

Buyer 1 Premium on selling price**

Better quality of produce***

Logistical gains

Additional net margins for buyers of produce* (as % of sales)

Increase in number of small-scale farmer clients for sellers of inputs/equipment

*On top of margins made at the processing plant or dairy hub level ** Premium on price of product sold (e.g. market premium fetched by the Kenya Tea Development Agency factories on Mombasa auction) 8

*** Better quality of produce collected from farmers, yielding higher returns in processing (e.g. JAIN onions have higher solid content)

5 x

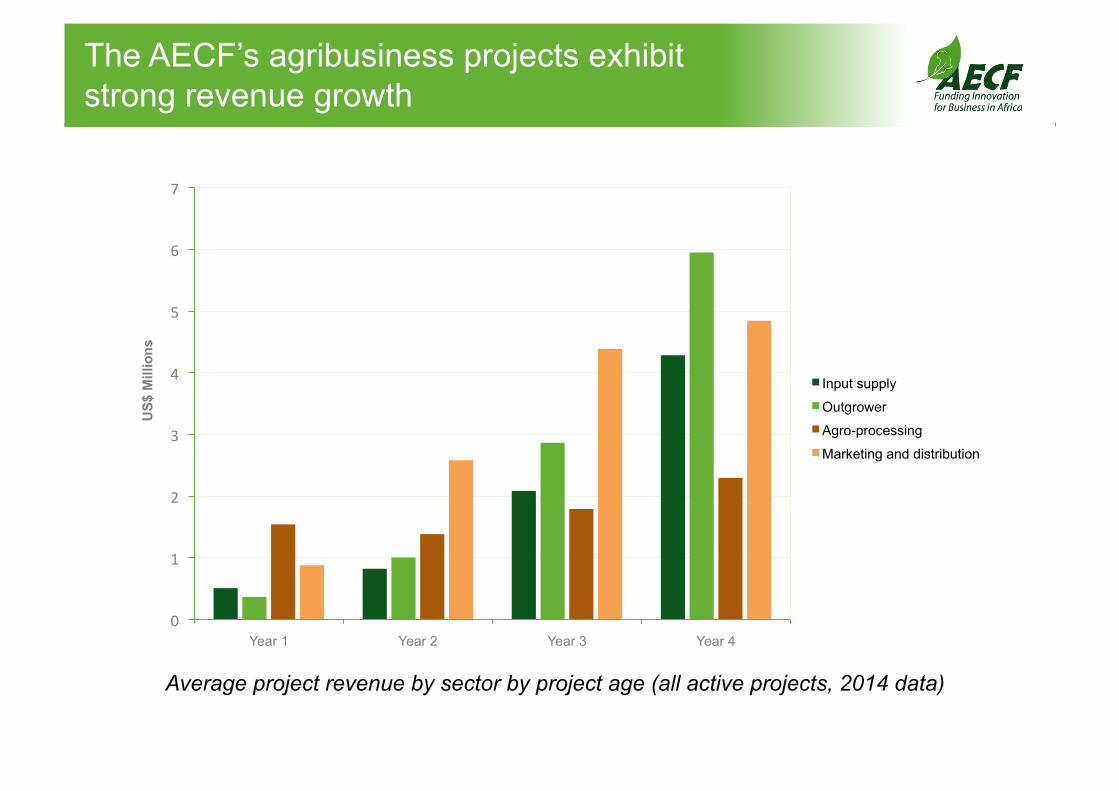

The AECF’s agribusiness projects exhibit strong revenue growth

Average project revenue by sector by project age (all active projects, 2014 data)

0

1

2

3

4

5

6

7

Year 1 Year 2 Year 3 Year 4

US$

Mill

ions

Input supply

Outgrower

Agro-processing

Marketing and distribution

QUESTION 2: WHAT IS THE SINGLE BIGGEST LEVER TO INCREASE THE PROFITABILITY OF FARMERS?

a. Training on better agricultural practices

b. Provision of a new technology

c. Higher selling prices (from certification or value chain

disintermediation)

d. Savings (e.g. on inputs purchase)

10

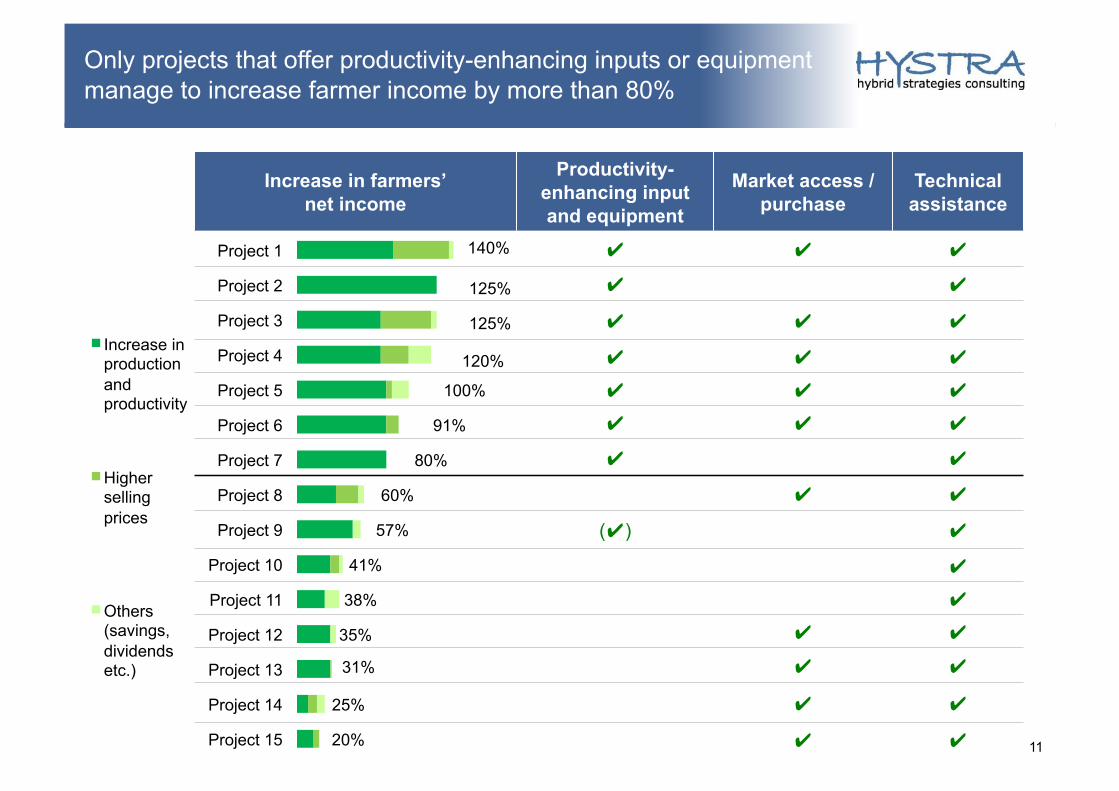

Increase in farmers’ net income

Productivity-enhancing input and equipment

Market access / purchase

Technical assistance

✔ ✔ ✔

✔ ✔

✔ ✔ ✔

✔ ✔ ✔

✔ ✔ ✔

✔ ✔ ✔

✔ ✔

✔ ✔

(✔) ✔

✔

✔

✔ ✔

✔ ✔

✔ ✔

✔ ✔ 20%

25%

31%

35%

38%

41%

57%

60%

80%

91%

100%

120%

125%

125%

Project 15

Project 14

Project 13

Project 12

Project 11

Project 10

Project 9

Project 8

Project 7

Project 6

Project 5

Project 4

Project 3

Project 2

Project 1

Increase in production and productivity

Higher selling prices

Others (savings, dividends etc.)

Only projects that offer productivity-enhancing inputs or equipment manage to increase farmer income by more than 80%

140%

11

The smallholder as a producer or a consumer

Extent of value chain integration

Input Supply

Agro-processing and marketing and distribution

Outgrower

Finance Information E.g. Shamba

Shape-up, 515k households $58 net benefit

Average net benefit ($/

farmer) per project

Average number of farmers benefitted per project (outreach)

5k 10k 15k 20k

$100

$200

QUESTION 3: WHY SOME PROJECTS STRUGGLE TO REACH HIGH PENETRATION?

a. Small farmers cannot afford to pay for expensive new

technologies/ inputs

b. Farmers believe that the gains they could make by

evolving their practices are not significant enough

c. Farmers are risk-averse yet not given any insurance/

guarantee against failure

d. Other

14

Penetration rate (%) Original net yearly income and net increase as a result of intervention

(US$)

Cost of intervention to farmers in %

of additional revenues

Yet, it is neither the prospect of important gains nor the limited need for upfront investments that drive penetration

90%

70%

70%

65%

60%

25%

20%

15%

15%

15%

1%

Project 1

Project 2

Project 3

Project 4

Project 5

Project 6

Project 7

Project 8

Project 9

Project 10

Project 11 800

480

2,500

228

14,714

1,350

491

659

38

2,500

274

1,000

120

2,000

130

20,600

1,350

589

208

48

500

164

40%

0%

12%

42%

29%

27%

60%

26%

40%

23%

40%

*In some projects implemented by buyers, farmers may side-sell part of their production to other buyers, leading to a greater actual original net yearly income and net increase than reported here

Penetration Ability to quit project easily Guarantee / insurance

✔ ✔

✔

✔

✔ ✔

(✔) ✔

✔ 1%

15%

15%

20%

25%

65%

70%

70%

90%

Project 9

Project 8

Project 7

Project 6

Project 5

Project 4

Project 3

Project 2

Project 1

16

Ability to easily quit drives penetration

QUESTION 4: HOW MUCH DO ORGANIZATIONS SPEND ON TRAINING FARMERS (as % of product bought from or input provider’s sales to farmers)?

a. More than 30%

b. Between 20 and 30%

c. Between 10 and 20%

d. Between 1 and 10%

17

Total yearly training cost* per farmer ($)

Number of training sessions per farmer

per month

Increase in productivity (% over previous situation)

2

0.5

2

2

2

0.2

0.2

2

4

Level and intensity of training provision do not correlate with farmers’ improved productivity

* Includes costs of deployment (e.g. transportation) and salaries of field staff (such as extension officers) spending a large part but not necessarily all of their time providing training and other technical support to farmers

50%

80%

80%

75%

20%

30%

15%

8%

35% Training + technology

Training only

9

19

20

20

50

67

125

150

570

Project 9

Project 8

Project 7

Project 6

Project 5

Project 4

Project 3

Project 2

Project 1

18

But when done well, training drives higher profits and incomes for both buyers and farmers

19

Providing technology and training

Providing only training

Additional net margin for buyers per $ spent in training

Additional farmer income per $ spent in training

$2

$2

$36

$11

$4

$- $2 $4 $6 $8 $10

Buyer 5

Buyer 4

Buyer 3

Buyer 2

Buyer 1

Premium on selling price

Better quality of produce

Logistical gains

$0,4

$4,4

$4,5 $4,5

$1,7

$8,2

QUESTION 5: WHAT ARE EFFECTIVE STRATEGIES TO DEAL WITH “DEFAULTERS”?

a. Offering more stable incomes

b. Increased transparency and convenience in transactions

c. Enforcing tough penalties

d. All of the above

20

Defaulters and side-selling

Kate Holt (KPMG IDAS)

! Transparent seasonal price bands give:

• Extra margin to Margarita if price is high

• Extra cushion to farmers if price is low

" Increased visibility allows farmers to invest for the long-term

Smoothing income over price variations

Sustainability premium turned into

a savings plan

! Certification premium originally paid during planting season

! As season ends, income is low, but investments needs are high (inputs, labor, school fees)

! Farmers requested that the premium be paid in a lump sum at season’s end

" Farmers value support in smoothing out their annual cash flow

22

Offering minimum prices (hence predictable income) or payments smoothened over time helps reduce side-selling

250

460

Mechanical weighing Digital weighing

Kilo of cocoa delivered per farmer Percentage of registered farmers delivering cocoa

72%

86%

Without transport of harvest

With transport of harvest

+84%

+19%

23

Convenience and transparency also are effective incentives to reduce side-selling

Credibility of threats insured by the fact that Margarita can easily source elsewhere

$

Loyal farmer’s wife

Farmer engaging in side-selling

! Own end-of-year bonus (2% of annual sales)

! Share of bonus of disloyal farmers

! Exclusion from program for life

! Loss of bonus for entire period

Side-selling: 0% Churn: 5%

24

Credible penalties can also be effective at improving loyalty

A WEALTH OF EXPERIENCE AND FINDINGS…

25

AECF

Key findings on impact

! If your target is numbers of HH benefiting then fund input supply companies, information and TA providers, and financial service providers

! If your target is benefit per HH then focus on out-grower schemes with full engagement.

! Pareto rule applies – 80% of impact coming from 20% of projects – can we identify them ex ante?

! Livestock projects – dairy and poultry particularly – have a greater impact per HH than crop projects (on average…)

! Have patience – to see the real impact of agribusiness projects you need time

! Impact correlates almost directly with revenue (EBITDA relationship takes longer to show)

! Jobs is becoming the focus of funders – need to calculate this differently

! Huge opportunity to learn from the AECF’s portfolio – we must not waste this opportunity – the 2014 Impact Report is just a start (we hope..)

26

The AECF: Seven years, seven million people

AECF

Key findings and questions on process

! Use a “last hard number” approach to keep impact verification costs down (revenue is the best last hard number)

! Country and topic based competitions offer greater potential for systemic impact

! Continent wide competitions can identify and support the most innovative ideas

! Aim to start races rather than pick winners ! Disruptive innovation (triggered by technology and/or business model) is key

! Use of different financial products (grants, loans, guarantees, equity) or just grants with a stronger Connect?

! Matching funds and leverage – not the same thing – which matters?

! Competitions to solve particular challenges?

27

The AECF: 8 different funds; 20 competitions; US$244m; over 200 projects in 25 countries;

The AECF 2014 Impact Report

Our report present how the AECF’s portfolio of 160+ projects across Africa is having a significant impact on the lives of rural poor people by addressing some of the continent’s most urgent development challenges.

Impact Report: http://bit.ly/1QFZvpy

Review: bit.ly/AECFEdChoice

29

What other questions can you get answered in Hystra’s report?

# When entering a new area, which type of farmers invest into first?

# What player is best positioned to pay for farmers’ training in complex supply chains?

# How can ICT change the cost and impact game?

# To efficiently and effectively reach out to a large number of farmers, what is best: Working with farmers’ groups or through intermediaries?

# What proportion of projects have the farmers loyal and committed and why?

# What drives farmers to leave an intervention aiming at making them more productive?

# Do cooperatives actually manage to make farmers richer?

# What proportion of the fair trade premium arrives to farmers?

# How to develop long-term, win-win arrangements with farmers?

Full report available on www.hystra.com Contact: Jessica Graf, [email protected]

Review: bit.ly/HystraEdChoice

Thanks to our speakers for some evidence and answers…

Evidence of benefits to both farmers and business

What works for smallholders? ! productivity-increasing technology ! value chain integration

! Returns on training

! Strategies to increase adoption in the face of risk

! Strategies to reduce default

30

Discussion

Visit the webinar page for details and resources: http://bit.ly/Smallholder

Join the discussion on Twitter #Smallholdersuccess

Join the Practitioner Hub

InclusiveBusinessHub.org

Resources, insights and discussion on inclusive business

32