the university athletic association, inc. financial ... · the university athletic association,...

TRANSCRIPT

THE UNIVERSITY ATHLETIC ASSOCIATION, INC.

FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. JUNE 30, 2014 AND 2013 TABLE OF CONTENTS

Page(s)

Independent Auditors’ Report 1 – 2 Required Supplementary Information

Management’s Discussion and Analysis 3 – 16 Basic Financial Statements

Statements of Net Position 17 Statements of Revenues, Expenses, and Changes in Net Position 18 Statements of Cash Flows 19 – 20 Notes to Financial Statements 21 – 38

Report on Internal Control over Financial Reporting and on

Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing

Standards 39 – 40

- 1 -

INDEPENDENT AUDITORS’ REPORT

The Audit Committee, The University Athletic Association, Inc.:

Report on the Financial Statements:

We have audited the accompanying financial statements of The University Athletic Association, Inc. (the Association), a direct support organization and component unit (for accounting purposes only) of the University of Florida, as of and for the years ended June 30, 2014 and 2013, and the related notes to the financial statements, which collectively comprise the Association’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

The Association’s management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

- 2 -

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Association as of June 30, 2014 and 2013, and the changes in financial position and cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 3 through 16 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated September 3, 2014, on our consideration of the Association’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Association’s internal control over financial reporting and compliance.

Gainesville, Florida September 3, 2014

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013

- 3 -

Introduction

The University Athletic Association, Inc. (the Association), a not-for-profit corporation, is a direct support organization of the University of Florida (UF). The Association exists to advance UF’s teaching, research and service missions through the intercollegiate athletics program.

The Association’s strategic purpose focuses on providing a championship experience with integrity on and off the field for student-athletes and the Gator Nation. The Association’s vision is to be the model collegiate athletics program, combining excellence and integrity in academics, athletics, and fan engagement to elevate the UF brand. The Association recognizes its responsibility to UF to operate the Association in an efficient manner using sound business principles within an ethical decision making process.

The tremendous success of the athletic program can be attributed to many factors: outstanding coaches and support staff, extremely talented student-athletes, a great academic institution, a strong recruiting base, university support, supportive alumni and friends, and a commitment to each sport. The Association’s financial strength is also a key component in its success and is a major factor in maintaining or surpassing its current level of achievement in all the Association’s endeavors.

Overview of the Financial Statements and Financial Analysis

The Association is pleased to present its financial statements for the fiscal years ended June 30, 2014 and 2013. This discussion and analysis is a narrative explanation of the Association’s financial condition and operating activities for these years. The overview presented below highlights the significant financial activities that occurred during the past two years and describes changes in financial activity from the prior year. Please read this overview in conjunction with the comparative summaries of net position and revenues, expenses and changes in net position and the Association’s financial statements which begin on Page 17.

Using these Financial Statements

This report consists of a series of financial statements, prepared in accordance with the Governmental Accounting Standards Board (GASB) Statement No. 34, Basic Financial Statements and Management’s

Discussion and Analysis – for State and Local Governments and Statement No. 35, Basic Financial

Statements – and Management’s Discussion and Analysis – for Colleges and Universities.

There are three financial statements presented: the Statements of Net Position; the Statements of Revenues, Expenses and Changes in Net Position; and the Statements of Cash Flows.

The Association’s net position is one indicator of the improvement or erosion of its financial health when considered with non-financial facts such as the overall academic and athletic success of the intercollegiate athletic program and the condition of its facilities, and is a key indicator of the overall health of the Association and its programs. This success is evidenced by:

� Two NCAA titles highlighted Florida’s national team finishes in the 2013-2014 season. Florida moved from third to a tie for first on the final rotation, giving the Gators their second consecutive NCAA gymnastics team held in Birmingham last April. Softball swept through the Women’s College World Series with a 5-0 record, outscoring opponents 32-6 in Oklahoma City to claim the

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 4 -

program’s first title. Six other programs contributed NCAA top-three finishes. Men’s outdoor track & field was second while five Gator teams recorded third-place finishes in NCAA action - men’s basketball, men’s swimming & diving, women’s tennis, men’s and women’s indoor track & field.

� In all, 12 teams registered top-10 finishes last season, which matches the third-highest total in school history. At least 10 Gator teams have turned in top-10 finishes in each of the last dozen seasons. The program’s record of 14 top-10 finishes came in 2009-2010.

� Florida took second overall in the 2013-2014 Learfield Sports Directors’ Cup standings for the third-straight year. The finish matches Florida’s highest ever in the annual all-sports rankings and marks Florida’s sixth consecutive top-four finish in the rankings. The national all-sports competition award is presented annually by the National Association of Collegiate Directors of Athletics (NACDA), Learfield Sports and USA Today. The finish marks Florida’s 31st consecutive finish among the nation’s top-10 programs. Florida is the only school to finish in the top 10 in national all-sports rankings every year since 1983-1984.

� Florida’s runner-up finish in the Director’s Cup standings was the highest by any school in the Southeastern Conference (SEC).

� Six Gator teams won conference titles in 2013-2014, including a league-high five in Southeastern Conference action. Florida won SEC titles in baseball, men’s basketball, soccer, men’s swimming & diving and women’s indoor track & field. The Gators now own 57 titles since the 2004-2005 academic year, the most by any conference school during the 10-year span. The Gators’ newest program won its fourth consecutive American Lacrosse Conference title.

� The University of Florida swept the 2013-2014 Halifax Media Group's Southeastern Conference All-Sports titles – the 14th time the Gator program has taken the three titles. The overall SEC All-Sports title is the 24th for Florida, while the Gator program also earned its 21st women's and 18th men’s.

� Florida was also successful away from the athletic arena in 2013-2014, as the Gators earned 184 SEC Academic Honor Roll accolades. The SEC annually selects an Academic Honor Roll for each team that honors student-athletes who have posted cumulative 3.0 grade-point averages for the previous academic year. When Florida’s selections for the SEC First-Year Academic Honor Roll are added, a total of 240 Gators earned recognition by the league in 2013-2014 for their work in the classroom. Additionally, three UF student-athletes were named Capital One Academic All-Americans in 2013-2014.

� In an era when the NCAA estimates that 70 percent of Division I schools are losing money on intercollegiate athletics, the University Athletic Association has contributed more than $79.7 million since 1990 to help fund University of Florida academic endeavors. This includes $4.3 contributed to UF in 2013-14.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 5 -

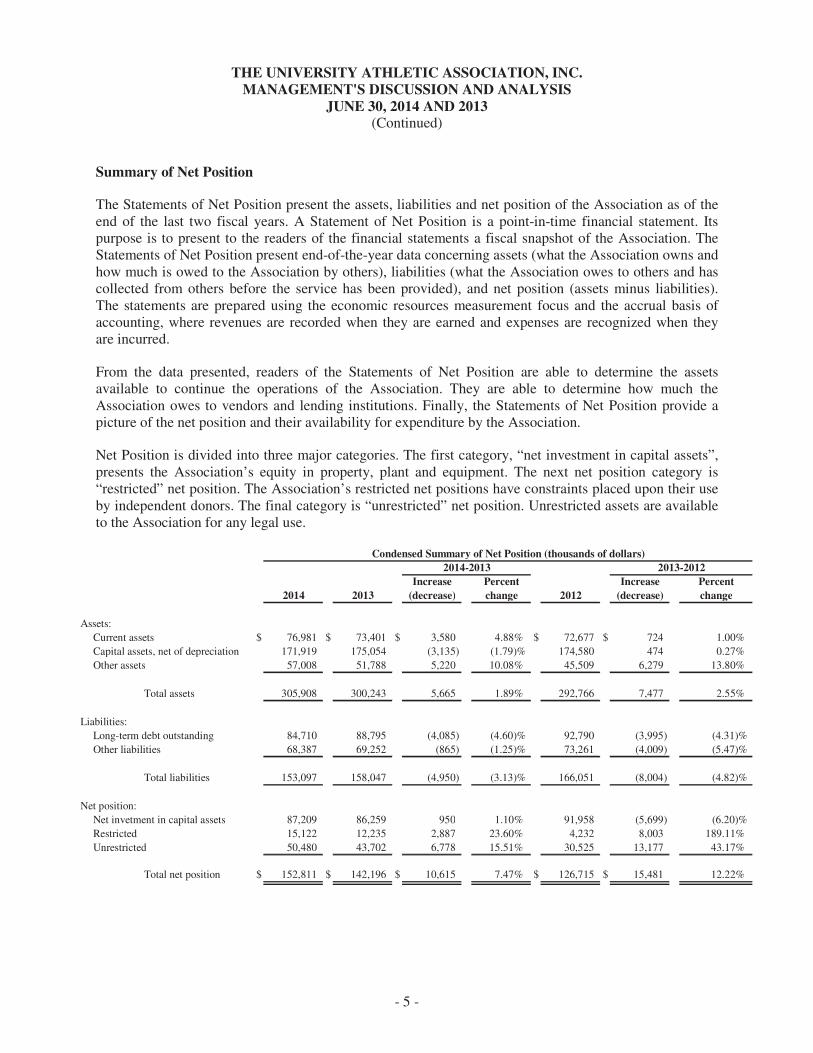

Summary of Net Position

The Statements of Net Position present the assets, liabilities and net position of the Association as of the end of the last two fiscal years. A Statement of Net Position is a point-in-time financial statement. Its purpose is to present to the readers of the financial statements a fiscal snapshot of the Association. The Statements of Net Position present end-of-the-year data concerning assets (what the Association owns and how much is owed to the Association by others), liabilities (what the Association owes to others and has collected from others before the service has been provided), and net position (assets minus liabilities). The statements are prepared using the economic resources measurement focus and the accrual basis of accounting, where revenues are recorded when they are earned and expenses are recognized when they are incurred.

From the data presented, readers of the Statements of Net Position are able to determine the assets available to continue the operations of the Association. They are able to determine how much the Association owes to vendors and lending institutions. Finally, the Statements of Net Position provide a picture of the net position and their availability for expenditure by the Association.

Net Position is divided into three major categories. The first category, “net investment in capital assets”, presents the Association’s equity in property, plant and equipment. The next net position category is “restricted” net position. The Association’s restricted net positions have constraints placed upon their use by independent donors. The final category is “unrestricted” net position. Unrestricted assets are available to the Association for any legal use.

Increase Percent Increase Percent

2014 2013 (decrease) change 2012 (decrease) change

Assets:

Current assets $ 76,981 $ 73,401 $ 3,580 4.88% $ 72,677 $ 724 1.00%

Capital assets, net of depreciation 171,919 175,054 (3,135) (1.79)% 174,580 474 0.27%

Other assets 57,008 51,788 5,220 10.08% 45,509 6,279 13.80%

Total assets 305,908 300,243 5,665 1.89% 292,766 7,477 2.55%

Liabilities:

Long-term debt outstanding 84,710 88,795 (4,085) (4.60)% 92,790 (3,995) (4.31)%

Other liabilities 68,387 69,252 (865) (1.25)% 73,261 (4,009) (5.47)%

Total liabilities 153,097 158,047 (4,950) (3.13)% 166,051 (8,004) (4.82)%

Net position:

Net invetment in capital assets 87,209 86,259 950 1.10% 91,958 (5,699) (6.20)%

Restricted 15,122 12,235 2,887 23.60% 4,232 8,003 189.11%

Unrestricted 50,480 43,702 6,778 15.51% 30,525 13,177 43.17%

Total net position $ 152,811 $ 142,196 $ 10,615 7.47% $ 126,715 $ 15,481 12.22%

Condensed Summary of Net Position (thousands of dollars)

2014-2013 2013-2012

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 6 -

Highlights

� The Association’s total assets increased by $5.7 million and $7.5 million in 2014 and 2013, respectively. The fluctuation in total assets between 2013 and 2012 was primarily due to fluctuations in the market value of investments. In 2014, the increase was also due to increases in the market value of investments and accounts receivable.

� Current assets increased in 2014 by $3.5 million due to a $2.8 million decrease in cash and cash equivalents, a $0.5 million increase in short-term investments and a $5.8 million increase in accounts receivable.

� Capital assets, net of depreciation decreased in 2014 by $3.1 million due to depreciation expense exceeding asset additions.

� In 2014, other assets increased by $5.2 million due to an increase in the amount due from Gator Boosters and increased in 2013 by $6.3 million due to fluctuations in the value of long term investments.

� Long-term debt outstanding decreased by $4.1 million and $4.0 million in 2014 and 2013, respectively, due to loan repayments.

� Other liabilities decreased by $4.0 million in 2013 due to a $3.0 million decrease in advanced football ticket sales and deferred Gator Booster contributions related to the 2013 and future football seasons, a $0.1 million decrease in deferred royalties, a $0.7 million decrease in accounts payable and accrued expenses, an increase of $0.1 million in accrued compensated absences and a decrease of $0.1 million in contracts payable.

� Total net position increased by $10.6 million and by $15.5 million in 2014 and 2013, respectively. Unrestricted net position increased by $6.8 million in 2014 and $13.2 million in 2013.

� In 2013, net position invested in capital assets, net of related debt decreased by $5.7 million due to payments of $4.0 million on long-term debt, purchases of $12.7 million in capital assets, spending of $10.2 million in construction trust funds, disposal of $3.3 million in capital assets and the expensing of $8.9 million in depreciation.

� Restricted net position increased by $2.9 million in 2014 and $8.0 million in 2013 primarily due to receipt of contributions related to future projects in the Stephen C. O’Connell Center & the Farrier Hall Academic Center.

Summary of Revenues, Expenses and Changes in Net Position

The Statements of Revenues, Expenses and Changes in Net Position present the revenues and expenses incurred during each year. Revenues and expenses are reported as operating and nonoperating. In general, operating revenues are received for providing goods and services to the Association’s various customers and constituencies. Operating expenses are those expenses paid to acquire or produce goods and services provided in return for the operating revenues, and to carry out the mission of the Association. The utilization of long-lived assets, referred to as capital assets, is reflected in the financial statements as depreciation, which amortizes, and reduces net income, by the cost of an asset over its expected useful life.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 7 -

Nonoperating revenues are revenues received for which goods or services are not provided. Investment income and other revenues, such as sales taxes retained and state appropriations, which are not payment for services are classified as nonoperating revenues.

Nonoperating expenses include interest on capital asset related debt and contributions to the University of Florida (UF) and the University of Florida Foundation (UFF). Contributions to UF include unrestricted gifts for the academic mission of the University, contributions for designated purposes and costs contributed by the Association for UF projects. Contributions to the UFF are transfers by the Association to the athletic scholarship endowment.

Capital contributions are considered neither operating nor nonoperating and are reported after “Income before contributions.”

Changes in total net position as presented on the Statements of Net Position are based on the activity presented in the Statements of Revenues, Expenses and Changes in Net Position. The purpose of the Statements of Revenues, Expenses and Changes in Net Position is to present the operating and nonoperating revenues received by the Association and the operating and nonoperating expenses paid by the Association, and any other revenues, expenses, gains and losses received or spent by the Association.

Condensed Summary of Revenues, Expenses and

Changes in Net Position (thousands of dollars)

Increase Percent Increase Percent

2014 2013 (decrease) change 2012 (decrease) change

Operating revenues:

Football $ 67,384 $ 71,293 $ (3,909) (5.48)% $ 70,664 $ 629 0.89%

Other sports 10,781 10,179 602 5.91% 10,528 (349) (3.31)%

Royalties and sponsorships 18,769 18,785 (16) (0.09)% 17,767 1,018 5.73%

Auxiliaries, camps and other 10,001 10,043 (42) (0.42)% 12,053 (2,010) (16.68)%

Total operating revenues 106,935 110,300 (3,365) (3.05)% 111,012 (712) (0.64)%

Nonoperating revenues 11,926 7,908 4,018 50.81% 1,270 6,638 522.68%

Total revenues 118,861 118,208 653 0.55% 112,282 5,926 5.28%

Operating expenses:

Team expenses 43,605 43,857 (252) (0.57)% 40,393 3,464 8.58%

Scholarships and support services 25,087 24,071 1,016 4.22% 23,652 419 1.77%

General and administrative 25,965 24,341 1,624 6.67% 24,503 (162) (0.66)%

Auxiliaries, camps and depreciation 12,460 12,072 388 3.21% 13,565 (1,493) (11.01)%

Total operating expenses 107,117 104,341 2,776 2.66% 102,113 2,228 2.18%

Nonoperating expenses:

Interest on capital related debt 2,035 2,088 (53) (2.54)% 2,434 (346) (14.22)%

Contributions to University of Florida

and UF Foundation 4,345 7,596 (3,251) (42.80)% 6,457 1,139 17.64%

Total nonoperating expenses 6,380 9,684 (3,304) (34.12)% 8,891 793 8.92%

Total expenses 113,497 114,025 (528) (0.46)% 111,004 3,021 2.72%

Capital contributions from Gator

Boosters and others 5,252 11,298 (6,046) (53.51)% 7,985 3,313 41.49%

Increase (decrease) in net position 10,616 15,481 (4,865) (31.43)% 9,263 6,218 67.13%

Net position, beginning of year 142,196 126,715 15,481 12.22% 117,452 9,263 7.89%

Net position, end of year $ 152,812 $ 142,196 $ 10,616 7.47% $ 126,715 $ 15,481 12.22%

2014-2013 2013-2012

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 8 -

Highlights

� Football revenues decreased in 2014 by $3.9 million primarily due to a reduction in the number of home games in the 2013 season.

� Royalties and sponsorships increased by $1.0 million in 2013 due to a reporting change as a result of outsourcing the sportshop operations previously reported as an Auxiliary.

� Auxiliary, camps and other revenue decreased by $2.0 million in 2013 due to the outsourcing of the sportshop operation.

� Nonoperating revenue increased by $4.0 million in 2014 and $6.6 million in 2013 due to investment performance fluctuations.

� In 2013, operating expenses increased by $2.2 million due to the following: Team expenses increased by $3.5 million primarily due to increases in football bowl expenses and opponent guarantees and other sports post season travel and related expenses. Scholarships and supports services increased by $0.4 million primarily due to an increase in scholarship costs. General and administrative expenses decreased by $0.2 million primarily due to a decrease in capital asset disposals. Auxiliaries, camps and depreciation expenses decreased by $1.5 million primarily due to a $1.3 million decrease in sportshop expenses, a $0.6 million decrease in camp expenses and a $0.4 million increase in depreciation.

� Operating expenses for 2014 increased by $2.8 million primarily due to a $1.0 million increase in scholarships and support services and a $1.6 million increase in general and administrative expenses. Most of this increase was due to a budgeted salary increase. Additionally, marketing expenses increased due to new branding initiatives, ticket office expenses increased due to a new consulting contract related to ticket sales services and termination settlements increased due to the retirement of a long time coach.

� Contributions to the University of Florida and to the University of Florida Foundation decreased by $3.3 million in 2014 and increased by $1.1 million in 2013. Contributions to the University of Florida include unrestricted gifts for the academic mission of the University, contributions for designated purposes and costs incurred by the Association for UF projects. See Note 9 in the Notes to the Financial Statements for further details on the Association’s contributions to the University of Florida. Contributions to the University of Florida Foundation consisted of transfers by the Association to the Athletic Endowment Fund from profits from the Gator Walk brick program. See Note 10 in the Notes to the Financial Statements for further details on the Association’s contributions to the University of Florida Foundation.

� Capital contributions are major gifts designated by the donors for facility construction, renovations and equipment purchases. The amount will fluctuate from year to year based on giving schedules. In 2014, capital contributions totaled $5.3 million and included $2.6 million for the renovation of the Stephen C. O’Connell Center, $1.0 million for the “Gateway of Champions” football front door project, $0.5 million for renovation of the Carse swim dive facility, $0.4 million for the lacrosse stadium and $0.8 million for various other projects.

� In 2013, capital contributions totaled $11.0 million and included $7.6 million for the renovation of the Stephen C. O’Connell Center, $1.3 million for the “Gateway of Champions” football front door project, $0.9 million for renovation of the Carse swim dive facility, $0.4 million for the lacrosse stadium and $0.8 million for various other projects.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 9 -

Football60%

Men's Basketball8%

Other Sports1%

Auxiliaries1%

Camps1%

Royalties and Sponsorships16%

Other6%

Nonoperating Revenues7%

Revenue 2012-2013

Football57%

Men's Basketball8%

Other Sports1%

Auxiliaries1%

Camps1%

Royalties and Sponsorshps16%

Other6%

Nonoperating Revenues10%

Revenue 2013-2014

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 10 -

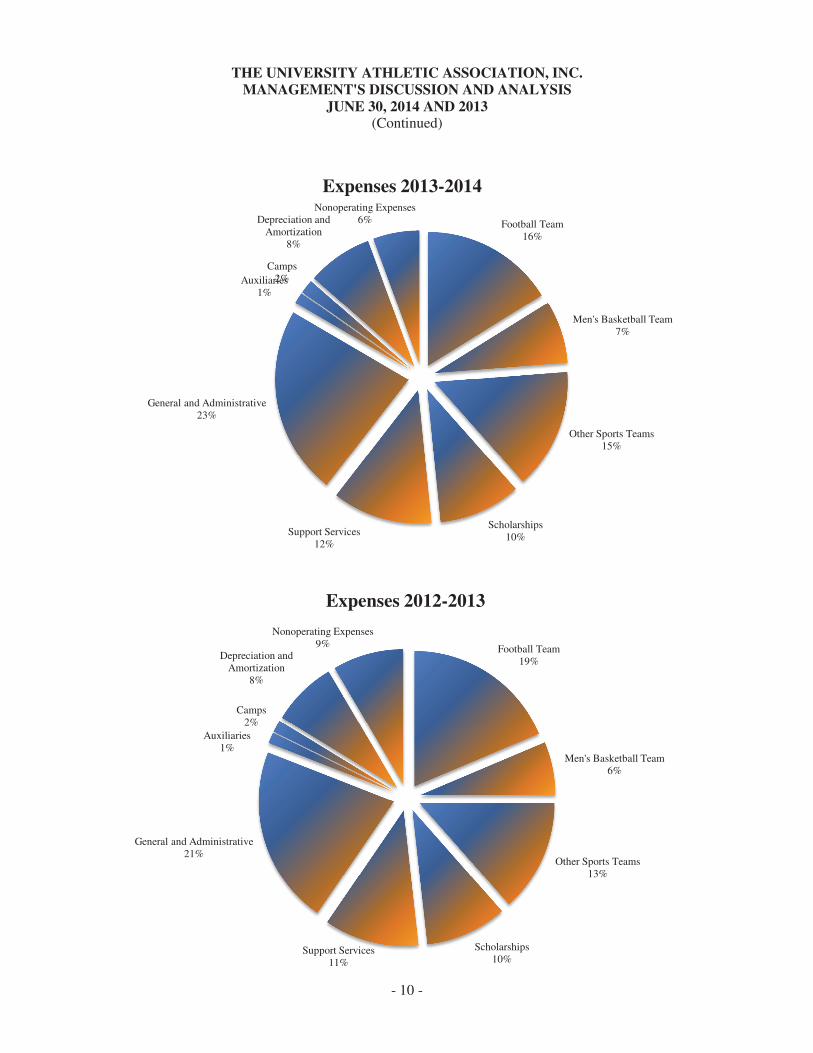

Football Team19%

Men's Basketball Team6%

Other Sports Teams13%

Scholarships10%

Support Services11%

General and Administrative21%

Auxiliaries1%

Camps2%

Depreciation and Amortization

8%

Nonoperating Expenses9%

Expenses 2012-2013

Football Team16%

Men's Basketball Team7%

Other Sports Teams15%

Scholarships10%

Support Services12%

General and Administrative23%

Auxiliaries1%

Camps2%

Depreciation and Amortization

8%

Nonoperating Expenses6%

Expenses 2013-2014

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 11 -

��

����������

����������

����������

����������

����������

���������

���������

����������

����������

���� ��� ��� ���� ���� ���� ���� ���� ���� ����

Annual Contributions to UF

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 12 -

Statement of Cash Flows

The final statements presented include Statements of Cash Flows. The primary purpose of the Statements of Cash Flows is to provide relevant information about the Association’s cash receipts and cash payments during the years shown. The statements classify cash receipts and cash payments as they result from operating, noncapital financing, capital and related financing, or investing activities. The first section, cash flows from operating activities, presents the cash effects of transactions and other events that enter into the determination of the Association’s operating income. The second section, cash flows from noncapital financing activities, shows the cash received and spent for nonoperating, noninvesting, and noncapital financing purposes and includes contributions to and from the University of Florida, the University of Florida Foundation and the State of Florida. The next section, cash flows from capital and related financing activities, provides information about cash used for the acquisition and construction of capital and related items and cash received from contributions specifically designated for capital purposes. The fourth section, cash flows from investing activities, details the purchases, proceeds and income received from investing activities. The final section reconciles the net cash provided (used) by operating activities to the operating income reflected on the Statements of Revenues, Expenses, and Changes in Net Position.

Increase Percent Increase Percent2014 2013 (decrease) change 2012 (decrease) change

Cash flows from:

Operating activities $ 3,670 $ 3,669 $ 1 0.03% $ 18,632 $ (14,963) (80.31)%

Noncapital financing activities (3,974) (4,134) 160 3.87% (4,531) 397 8.76%

Capital & related financing activities (6,782) (4,442) (2,340) (52.68)% (2,181) (2,261) (103.67)%

Investing activities 4,301 10,899 (6,598) (60.54)% (10,623) 21,522 202.60%

Net change in cash and cash equivalents (2,785) 5,992 (8,777) (146.48)% 1,297 4,695 361.99%

Cash and cash equivalents, beginning of year 10,766 4,774 5,992 125.51% 3,477 1,297 37.30%

Cash and cash equivalents, end of year $ 7,981 $ 10,766 $ (2,785) (25.87)% $ 4,774 $ 5,992 125.51%

Condensed Summary of Cash Flows (thousands of dollars)2014-2013 2013-2012

Highlights

� Cash provided by operating activities decreased by $15.0 million in 2013 due to decreased cash contributions from Gator Boosters of $7.8 million, decreased cash receipts from ticket holders of $6.0 million, increased cash receipts from the Southeastern Conference of $0.5 million, increased cash receipts from rights, royalties and sponsors of $1.7 million, increased other cash receipts of $0.2 million, increased cash used for payments to suppliers of $3.3 million and for scholarships of $0.5 million and decreased cash used for payments to employees of $0.2 million.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 13 -

� Cash used in capital and related financing activities increased in 2014 by $2.3 million due to a $6.9 million decrease in the purchase of capital assets, a $6.0 million decrease in capital contributions from Gator Boosters and a $3.2 million decrease in the proceeds from the sale of capital assets. In 2013, cash used in capital and related financing activities decreased by $2.3 million due to a $6.5 million decrease in the purchase of capital assets, a $15.0 million reduction in the proceeds from the issuance of long-term debt, a $3.3 million increase in capital contributions from Gator Boosters, a $0.3 million increase in cash used for the payment of bond principal and interest and a $3.2 million increase in the proceeds from the sale of capital assets.

� Cash used in investing activities increased by $6.6 million in 2014 due to a $39.5 million reduction in cash payments for the purchase of investment securities and a $46.1 million reduction in cash proceeds from the sale and maturities of investment. In 2013, cash provided by in investing activities increased by $21.5 million due to a $24.0 million reduction in cash payments for the purchase of investment securities, a $2.3 million reduction in cash proceeds from the sale and maturities of investment securities and a $0.2 million reduction in cash received from interest and dividends.

���������

���������

��������

��

������

�������

�������

�������

���� ����

������

���������������

��������

������

��������

��������

������

�������

��������

Net Cash Flow Activities

���������

����������

���������

!��������

����������

"����� # $� ���%

!��������

����������

&��������

����������

�������� ����

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 14 -

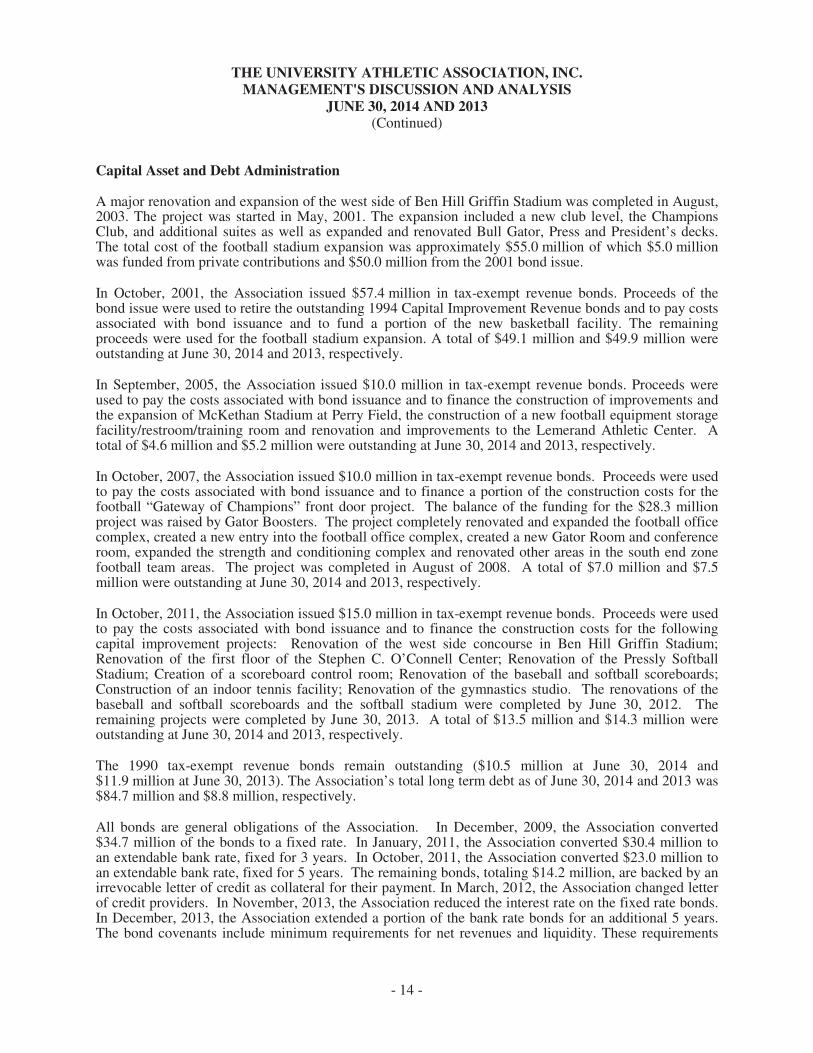

Capital Asset and Debt Administration

A major renovation and expansion of the west side of Ben Hill Griffin Stadium was completed in August, 2003. The project was started in May, 2001. The expansion included a new club level, the Champions Club, and additional suites as well as expanded and renovated Bull Gator, Press and President’s decks. The total cost of the football stadium expansion was approximately $55.0 million of which $5.0 million was funded from private contributions and $50.0 million from the 2001 bond issue.

In October, 2001, the Association issued $57.4 million in tax-exempt revenue bonds. Proceeds of the bond issue were used to retire the outstanding 1994 Capital Improvement Revenue bonds and to pay costs associated with bond issuance and to fund a portion of the new basketball facility. The remaining proceeds were used for the football stadium expansion. A total of $49.1 million and $49.9 million were outstanding at June 30, 2014 and 2013, respectively.

In September, 2005, the Association issued $10.0 million in tax-exempt revenue bonds. Proceeds were used to pay the costs associated with bond issuance and to finance the construction of improvements and the expansion of McKethan Stadium at Perry Field, the construction of a new football equipment storage facility/restroom/training room and renovation and improvements to the Lemerand Athletic Center. A total of $4.6 million and $5.2 million were outstanding at June 30, 2014 and 2013, respectively.

In October, 2007, the Association issued $10.0 million in tax-exempt revenue bonds. Proceeds were used to pay the costs associated with bond issuance and to finance a portion of the construction costs for the football “Gateway of Champions” front door project. The balance of the funding for the $28.3 million project was raised by Gator Boosters. The project completely renovated and expanded the football office complex, created a new entry into the football office complex, created a new Gator Room and conference room, expanded the strength and conditioning complex and renovated other areas in the south end zone football team areas. The project was completed in August of 2008. A total of $7.0 million and $7.5 million were outstanding at June 30, 2014 and 2013, respectively.

In October, 2011, the Association issued $15.0 million in tax-exempt revenue bonds. Proceeds were used to pay the costs associated with bond issuance and to finance the construction costs for the following capital improvement projects: Renovation of the west side concourse in Ben Hill Griffin Stadium; Renovation of the first floor of the Stephen C. O’Connell Center; Renovation of the Pressly Softball Stadium; Creation of a scoreboard control room; Renovation of the baseball and softball scoreboards; Construction of an indoor tennis facility; Renovation of the gymnastics studio. The renovations of the baseball and softball scoreboards and the softball stadium were completed by June 30, 2012. The remaining projects were completed by June 30, 2013. A total of $13.5 million and $14.3 million were outstanding at June 30, 2014 and 2013, respectively.

The 1990 tax-exempt revenue bonds remain outstanding ($10.5 million at June 30, 2014 and $11.9 million at June 30, 2013). The Association’s total long term debt as of June 30, 2014 and 2013 was $84.7 million and $8.8 million, respectively.

All bonds are general obligations of the Association. In December, 2009, the Association converted $34.7 million of the bonds to a fixed rate. In January, 2011, the Association converted $30.4 million to an extendable bank rate, fixed for 3 years. In October, 2011, the Association converted $23.0 million to an extendable bank rate, fixed for 5 years. The remaining bonds, totaling $14.2 million, are backed by an irrevocable letter of credit as collateral for their payment. In March, 2012, the Association changed letter of credit providers. In November, 2013, the Association reduced the interest rate on the fixed rate bonds. In December, 2013, the Association extended a portion of the bank rate bonds for an additional 5 years. The bond covenants include minimum requirements for net revenues and liquidity. These requirements

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 15 -

were met in 2014 and 2013. For additional information on Capital Assets and Long Term Obligations, see Notes 5 and 6 in the Notes to the Financial Statements.

The Association has made a significant commitment to buildings and improvements. Since 2005 over $128 million dollars has been spent on capital assets. The funding for these projects has come from operating funds, private capital contributions and tax exempt revenue bonds.

'������ "�����

"�����()�����

�����������

��*

+��% &��)����

�����������

�*

��������� !)�%�

���������

��*

Annual Capitalized Projects - 2005-2014Total of $127,889,722

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014 AND 2013 (Continued)

- 16 -

Economic Outlook

Although the U.S. economy continues its lackluster recovery, the Association remains in good financial condition as a result of a supportive fan base and the success of the Gator Booster Organization. Through the recession, the Association’s Increase in Net Position has continued to have steady growth year after year. This has been accomplished by keeping expenses to minimum and maximizing opportunities to increase revenue through ticket sales, the multi-media rights, Southeastern Conference revenues and major gift fund raising. The Association will continue to be challenged to maintain this growth, while still providing significant support to the University and a first class experience for the student athletes. For 2014-2015, the Association is again projecting minimal increases in both revenue and expense, along with continued focus on major gifts and scholarship endowment fund raising to ensure the future financial success of the Association.

Contacting Management

This financial narrative is designed to provide the reader with a general overview of the University Athletic Association, Inc.’s finances and to show the Association’s accountability for the money it receives. If you have questions about this report or need additional financial information, contact the Association’s Business Office at Ben Hill Griffin Stadium, Gainesville, Florida:

The University Athletic Association, Inc. Attn: Assistant Athletics Director/Controller PO Box 14485 Gainesville, FL 32604-2485 (352) 375-4683

��

����������

�����������

�����������

�����������

�����������

���� ��� ��� ���� ���� ���� ���� ���� ���� ����

���������

!)�%�

+��% &��)����

'������

"�����

"�����()�����

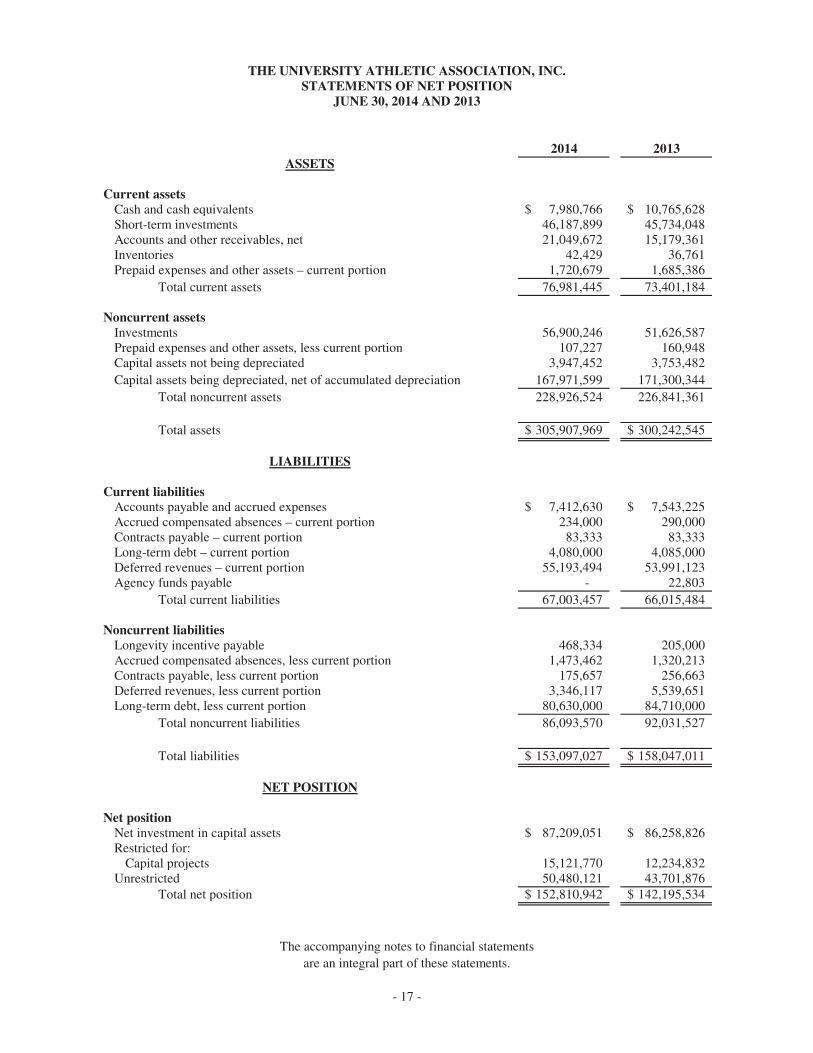

2014 2013

Current assetsCash and cash equivalents 7,980,766$ 10,765,628$ Short-term investments 46,187,899 45,734,048 Accounts and other receivables, net 21,049,672 15,179,361 Inventories 42,429 36,761 Prepaid expenses and other assets – current portion 1,720,679 1,685,386

Total current assets 76,981,445 73,401,184

Noncurrent assetsInvestments 56,900,246 51,626,587 Prepaid expenses and other assets, less current portion 107,227 160,948 Capital assets not being depreciated 3,947,452 3,753,482

Capital assets being depreciated, net of accumulated depreciation 167,971,599 171,300,344

Total noncurrent assets 228,926,524 226,841,361

Total assets 305,907,969$ 300,242,545$

Current liabilitiesAccounts payable and accrued expenses 7,412,630$ 7,543,225$ Accrued compensated absences – current portion 234,000 290,000 Contracts payable – current portion 83,333 83,333 Long-term debt – current portion 4,080,000 4,085,000 Deferred revenues – current portion 55,193,494 53,991,123 Agency funds payable - 22,803

Total current liabilities 67,003,457 66,015,484

Noncurrent liabilitiesLongevity incentive payable 468,334 205,000 Accrued compensated absences, less current portion 1,473,462 1,320,213 Contracts payable, less current portion 175,657 256,663 Deferred revenues, less current portion 3,346,117 5,539,651 Long-term debt, less current portion 80,630,000 84,710,000

Total noncurrent liabilities 86,093,570 92,031,527

Total liabilities 153,097,027$ 158,047,011$

Net positionNet investment in capital assets 87,209,051$ 86,258,826$ Restricted for:

Capital projects 15,121,770 12,234,832 Unrestricted 50,480,121 43,701,876

Total net position 152,810,942$ 142,195,534$

LIABILITIES

NET POSITION

THE UNIVERSITY ATHLETIC ASSOCIATION, INC.STATEMENTS OF NET POSITION

JUNE 30, 2014 AND 2013

ASSETS

The accompanying notes to financial statements

are an integral part of these statements.

- 17 -

2014 2013

Operating revenuesFootball 67,383,840$ 71,292,850$

Men’s basketball 9,978,197 9,393,073

Other sports 802,527 785,925

Auxiliaries 1,018,445 1,283,046

Camps 1,936,326 1,633,594

Royalties and sponsorships 18,768,621 18,785,043

Other 7,046,730 7,126,438

Total operating revenues 106,934,686 110,299,969

Operating expensesFootball team expenses 18,352,110 21,264,683

Men’s basketball team expenses 8,614,870 7,246,124

Other sports team expenses 16,637,783 15,346,179

Scholarships 11,315,976 11,144,842

Support services 13,770,659 12,925,922

General and administrative 25,965,091 24,341,225

Auxiliaries 1,529,465 1,493,752

Camps 1,945,653 1,675,423

Depreciation and amortization 8,985,548 8,902,820

Total operating expenses 107,117,155 104,340,970

Operating income (loss) (182,469) 5,958,999

Nonoperating revenues (expenses)Investment income (loss), net 10,055,552 5,936,340

Interest on capital asset related debt (2,034,440) (2,088,391)

Contributions to the University of Florida (4,305,881) (7,557,579)

Contributions to the University of Florida Foundation, Inc. (39,321) (38,022)

Other nonoperating revenues 1,870,307 1,971,142

Net nonoperating revenues (expenses) 5,546,217 (1,776,510)

Income before capital contributions 5,363,748 4,182,489

Capital contributions from Gator Boosters, Inc. and others 5,251,660 11,298,193

Increase in net position 10,615,408 15,480,682

Net position, beginning of year 142,195,534 126,714,852

Net position, end of year 152,810,942$ 142,195,534$

THE UNIVERSITY ATHLETIC ASSOCIATION, INC.STATEMENTS OF REVENUES, EXPENSES AND CHANGES IN NET POSITION

FOR THE YEARS ENDED JUNE 30, 2014 AND 2013

The accompanying notes to financial statements

are an integral part of these statements.

- 18 -

2014 2013

Cash flows from operating activitiesContributions from Gator Boosters, Inc. 28,430,297$ 26,848,610$

Receipts from ticket holders and others 30,820,650 28,701,685

Receipts from the Southeastern Conference and NCAA 20,259,843 22,467,081

Receipts from rights, royalties, and sponsors 18,295,149 18,903,272

Other receipts 611,495 760,303

Payments to suppliers and others (38,853,994) (40,660,450)

Payments to employees (44,569,509) (42,199,521)

Payments for scholarships (11,324,338) (11,151,922)

Net cash provided by operating activities 3,669,593 3,669,058

Cash flows from noncapital financing activitiesStatutory distributions for women's athletics from the

University of Florida and the State of Florida 1,870,307 1,971,142

Contributions to the University of Florida (5,805,881) (6,057,579)

Contributions to the University of Florida Foundation, Inc. (38,022) (47,225)

Net cash used in noncapital financing activities (3,973,596) (4,133,662)

Cash flows from capital and related financing activitiesPurchase of capital assets (5,853,446) (12,714,277)

Capital contributions from Gator Boosters, Inc. 5,251,660 11,298,193

Principal paid on bonds (4,085,000) (3,995,000)

Interest paid on bonds (2,100,781) (2,235,269)

Proceeds from sale of capital assets 5,275 3,203,909

Net cash used in capital and related financing activities (6,782,292) (4,442,444)

Cash flows from investing activitiesPurchases of investment securities (38,826,118) (78,291,495)

Proceeds from sale and maturities of investment securities 41,441,933 87,538,990

Interest and dividends received 1,685,618 1,651,425

Net cash provided by investing activities 4,301,433 10,898,920

Net increase (decrease) in cash and cash equivalents (2,784,862) 5,991,872

Cash and cash equivalents, beginning of year 10,765,628 4,773,756

Cash and cash equivalents, end of year 7,980,766$ 10,765,628$

THE UNIVERSITY ATHLETIC ASSOCIATION, INC.STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED JUNE 30, 2014 AND 2013

The accompanying notes to financial statements

are an integral part of these statements.

- 19 -

2014 2013

Reconciliation of operating income (loss) to net cash provided by operating activities

Operating income (loss) (182,469)$ 5,958,999$

Adjustments to reconcile operating income (loss) to

net cash provided by operating activities:

Depreciation and amortization 8,985,548 8,902,820

(Gain) loss on disposal of capital assets (2,602) 133,664

Changes in assets and liabilities:

Accounts and other receivables (5,843,113) (6,857,922)

Inventories (5,668) 662,480

Prepaid expenses and other assets 18,428 334,869

Accounts payable and accrued expenses 1,436,185 (2,138,000)

Accrued compensated absences 97,249 (60,349)

Longevity incentive payable 263,334 (5,695)

Contract payable (83,333) (83,334)

Deferred revenues (991,163) (3,136,262)

Agency funds payable (22,803) (42,212)

Net cash provided by operating activities 3,669,593$ 3,669,058$

THE UNIVERSITY ATHLETIC ASSOCIATION, INC.STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED JUNE 30, 2014 AND 2013(Continued)

The accompanying notes to financial statements

are an integral part of these statements.

- 20 -

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

- 21 -

(1) Summary of Significant Accounting Policies:

The following is a summary of the more significant accounting policies of The University Athletic Association, Inc. (the Association), which affect significant elements of the accompanying basic financial statements.

(a) Reporting entity––The Association is a not-for-profit entity organized in 1929 for the purpose of conducting various intercollegiate athletic programs for and on behalf of the University of Florida. The Association operates for the service and convenience of the University of Florida and is a direct support organization and component unit (for accounting purposes only) of the University of Florida.

(b) Measurement focus, basis of accounting, and financial statement presentation—The financial statements of the Association have been prepared using the economic resources measurement focus and the accrual basis of accounting. Accordingly, all assets and liabilities (whether current or noncurrent) are included on the Statement of Net Position. The Statement of Revenues, Expenses and Changes in Net Position presents increases (revenues) and decreases (expenses) in total net position. Under the accrual basis of accounting, revenues are recognized in the period in which they are earned while expenses are recognized in the period in which the liability is incurred.

The Association distinguishes operating revenues and expenses from nonoperating items. Operating revenues and expenses for the Association are those that result from the operation of the University of Florida’s intercollegiate athletic programs. It also includes all revenue and expenses not related to capital and related financing, noncapital financing, or investing activities. As required by GASB Statement No. 34, Basic Financial Statements – and Management's Discussion and Analysis – for State and Local Governments, capital contributions from Gator Boosters and others and contributions to the University of Florida and University of Florida Foundation, Inc. are not considered operating revenues or expenses and are reported after nonoperating revenues and expenses in the accompanying statements of revenues, expenses, and changes in net position.

(c) Cash and cash equivalents––Cash and cash equivalents include cash in banks and money market funds available for immediate use.

(d) Accounts receivable––Accounts receivable are stated at the amount management expects to collect from balances at year-end. Based on management's assessment of the credit history with organizations and individuals having outstanding balances and current relationships with them, it has concluded that realization losses on balances outstanding at year-end will be immaterial. The Association has no policy requiring collateral or other security to support its accounts receivable.

(e) Inventories––Inventories consist of items held for sale at the golf course pro shop and snack bar. Inventory items at the golf course pro shop are recorded at the lower of cost or market using the average cost method. All other inventory items are recorded at the lower of cost or market, as determined by using the first-in, first-out (FIFO) method.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(1) Summary of Significant Accounting Policies: (Continued)

- 22 -

(f) Capital assets––Capital assets purchased with an original cost of $1,000 or more are recorded at cost and depreciated utilizing the straight-line method over the estimated useful lives of assets (generally 5 years for permanent equipment and 10 to 15 years for capital improvements, except for improvements to buildings which range from 50 to 60 years). Interest incurred during the construction phase of capital assets is included as part of the capitalized value of assets constructed. Costs to maintain or repair these assets are expensed as incurred.

(g) Agency funds––The Association acts as an agent for the control and distribution of cash from the sale of Gator Growl tickets for the University of Florida. Such amounts are not included in the statements of revenues, expenses and changes in net position.

(h) Accrued compensated absences––Eligible employees are entitled to vacation and sick leave with pay. Employees are not limited in the amount of annual and sick leave accrued during the fiscal year. For annual leave, however, only a maximum of 352 hours can be carried forward from one fiscal year to the next and only a maximum of 200 hours can be paid upon termination provided the employee has completed six months of continuous service. Any amounts accrued over the maximums convert to sick leave at the end of the year on an hour for hour basis. Effective January 2012, the sick leave payout for employees was eliminated except for employees separating employment for retirement reasons. Eligible employees must retire on or before June 30, 2016, and either be at least age 62 and have completed at least ten years of creditable service or have completed 30 years of creditable service. If these requirements are met, retirees will be paid out 1/4 of their sick leave balance up to a maximum of 480 hours. Vacation pay is expensed when earned by the employee up to the maximum payout. Sick leave payments are expensed when earned up to the maximum payout only for eligible employees.

(i) Deferred revenues––Current deferred revenue consist of advance sales of football, men’s and women’s basketball, volleyball gold and platinum card tickets, related football and men’s basketball contributions, and miscellaneous other unearned fees received. The deferred items are recognized as revenue when the related games are played and when the service is performed or event occurs for which miscellaneous fees were received.

Additionally, deferred revenues included in other liabilities consist of booster prepayments and advance sponsorship and royalty payments. The sponsorship and royalty amounts are recognized over the life of the agreements, while the booster prepayments will be recognized in the applicable sports season.

(j) Longevity incentive payable––These balances represent amounts due to various coaches as specified in their employment contracts. Such amounts are accrued based upon schedules included in the respective employment contracts. In some circumstances, the coach’s employment contract may require the Association to make specified deposits into an employee directed investment account until such time as the coach has reached the stay period specified in their contract. These investment balances would transfer to the coach at the end of the stay period and are included in investments or short term investments in the accompanying statements of net position. In other circumstances, the Association is obligated to pay certain amounts to the coach at the end of the stay period. The Association accrues for these amounts ratably over the contract period. No payments will be made to the coach until they have reached the stay period specified in their contract.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(1) Summary of Significant Accounting Policies: (Continued)

- 23 -

(k) Net position––Net position is classified and displayed in three components:

� Net investment in capital assets – consists of capital assets, net of accumulated depreciation, reduced by the outstanding balances of any debt that is attributable to those assets.

� Restricted – consists of assets that have constraints placed upon their use either by external donors or creditors or through laws, regulations or constraints imposed by law through constitutional provisions or enabling legislation, reduced by any liabilities to be paid from these assets. Restricted net position consists of capital contributions received for specific future capital projects and funds held by the bond trustee for payments on the bonds.

� Unrestricted – consists of net position that does not meet the definition of “restricted” or “net investment in capital assets.”

When both restricted and unrestricted net position is available for use, it is the Association’s policy to use restricted resources first, then unrestricted resources as they are needed.

(l) Sales taxes retained––In accordance with Chapter 1006, Section 71 of the Florida Statutes, the Association retains an amount equal to sales taxes collected from ticket sales to athletic events for use in the support of women’s athletic programs. Sales taxes retained totaled $1,485,845 and $1,586,680 for the years ended June 30, 2014 and 2013, respectively, and are included in nonoperating revenues in the statement of revenues, expenses, and changes in net position.

(m) Income taxes––The Association is generally exempt from Federal income taxes under the provisions of Section 501(c) (3) of the Internal Revenue Code. However, the Association is subject to income tax on unrelated business income. Deferred income taxes arise from temporary differences resulting from income and expense items reported for financial reporting and tax purposes in different periods. Deferred taxes are classified as current or noncurrent, depending on the classification of the assets and liabilities to which they relate. Deferred taxes arising from temporary differences that are not related to an asset or liability are classified as current or noncurrent depending on the periods in which the temporary differences are expected to reverse. The principal sources of temporary differences at June 30, 2014 and June 30, 2013, relate to differences in the timing of revenue recognition for financial reporting and tax purposes on certain sponsorship agreements.

The Association files tax returns in the U.S. federal jurisdiction and in the state of Florida. Management of the Association considers the likelihood of changes by taxing authorities in its filed income tax returns and recognizes a liability for or discloses potential significant changes that management believes are more likely than not to occur upon examination by tax authorities, including changes to the Association’s status as a not-for-profit entity. Management believes the Association met the requirements to maintain its tax-exempt status and has not identified any uncertain tax positions subject to the unrelated business income tax that require recognition or disclosure in the accompanying financial statements. The Association’s income tax returns for the past three years are subject to examination by tax authorities, and may change upon examination.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(1) Summary of Significant Accounting Policies: (Continued)

- 24 -

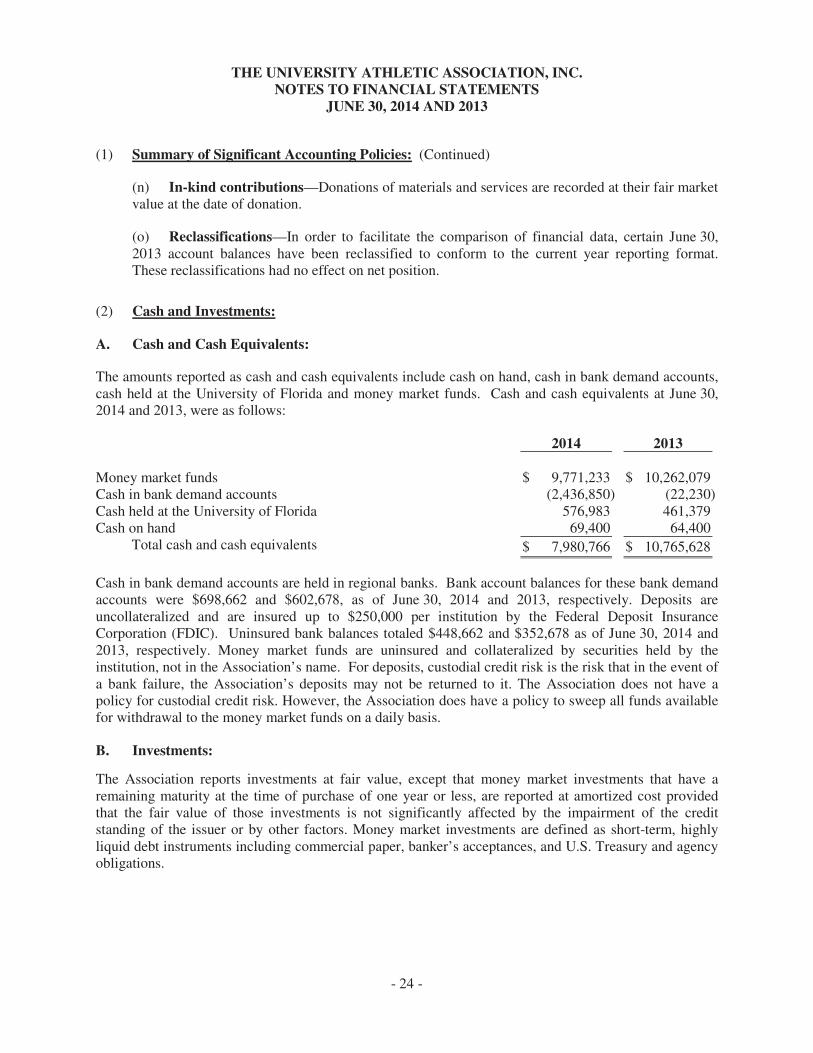

(n) In-kind contributions––Donations of materials and services are recorded at their fair market value at the date of donation.

(o) Reclassifications––In order to facilitate the comparison of financial data, certain June 30, 2013 account balances have been reclassified to conform to the current year reporting format. These reclassifications had no effect on net position.

(2) Cash and Investments:

A. Cash and Cash Equivalents:

The amounts reported as cash and cash equivalents include cash on hand, cash in bank demand accounts, cash held at the University of Florida and money market funds. Cash and cash equivalents at June 30, 2014 and 2013, were as follows:

2014 2013 Money market funds $ 9,771,233 $ 10,262,079 Cash in bank demand accounts (2,436,850) (22,230) Cash held at the University of Florida 576,983 461,379 Cash on hand 69,400 64,400

Total cash and cash equivalents $ 7,980,766 $ 10,765,628

Cash in bank demand accounts are held in regional banks. Bank account balances for these bank demand accounts were $698,662 and $602,678, as of June 30, 2014 and 2013, respectively. Deposits are uncollateralized and are insured up to $250,000 per institution by the Federal Deposit Insurance Corporation (FDIC). Uninsured bank balances totaled $448,662 and $352,678 as of June 30, 2014 and 2013, respectively. Money market funds are uninsured and collateralized by securities held by the institution, not in the Association’s name. For deposits, custodial credit risk is the risk that in the event of a bank failure, the Association’s deposits may not be returned to it. The Association does not have a policy for custodial credit risk. However, the Association does have a policy to sweep all funds available for withdrawal to the money market funds on a daily basis.

B. Investments:

The Association reports investments at fair value, except that money market investments that have a remaining maturity at the time of purchase of one year or less, are reported at amortized cost provided that the fair value of those investments is not significantly affected by the impairment of the credit standing of the issuer or by other factors. Money market investments are defined as short-term, highly liquid debt instruments including commercial paper, banker’s acceptances, and U.S. Treasury and agency obligations.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(2) Cash and Investments: (Continued)

B. Investments: (Continued)

- 25 -

Short-term investments are comprised of mutual funds, employee directed investment accounts due to vest to the employee during the next year, and investment accounts with the State of Florida Division of Treasury and State Board of Administration and are reported at fair value. Short-term investments typically are funds accumulated from advance ticket sales and booster contributions and will be used to fund operations in the upcoming fiscal year. Other investments include mutual funds, commingled funds and commingled hedged strategies funds that are reported at fair value as determined by their net asset values at year-end. The classification of investments between short-term and long-term is based on management’s anticipated cash flow needs. However, the needs of the Association may require the sale or retention of investment balances which differ from the classifications reflected in the accompanying statements of net position.

The Association’s corporate investment policy divides the Association’s assets into two portfolios, the long-term portfolio and the short-term portfolio. The policy states that the short-term portfolio invests in cash and equivalents and the long-term portfolio invests in a diversified portfolio of commingled and/or mutual funds in the following classes: Domestic Large Cap Equity, Domestic Small Cap Equity, International Equity, Hedged Strategies and Fixed Income. The hedged strategies investment represents the Association’s interest in the Florida Hedged Strategies Fund, LLC, a limited liability company that is managed by the University of Florida Investment Corporation.

As of June 30, 2014 and 2013, the Association had the following investments:

2014 2013

Short-term Investments: External Investment Pools:

Florida State Treasury Special Purpose Investment Account $ 46,181,770 $ 45,727,929 Florida PRIME 6,129 6,119

Subtotal 46,187,899 45,734,048

Long-term Investments: Domestic equity mutual funds and commingled funds 25,993,046 24,300,168 International equity mutual funds 11,649,011 9,046,105 Fixed income mutual funds 6,171,693 6,614,197 Commingled hedged strategies 11,143,930 9,828,633 Limited liability company interests 1,942,566 1,837,484

Subtotal 56,900,246 51,626,587

Total investments $103,088,145 $ 97,360,635

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(2) Cash and Investments: (Continued)

B. Investments: (Continued)

- 26 -

Custodial Credit Risk—For an investment, custodial credit risk is the risk that, in the event of the failure of the counterparty, the Association will not be able to recover the value of its investments or collateral securities that are in the possession of an outside party. Investments are subject to custodial credit risk if the securities are uninsured, not registered in the Association’s name, and are held by the party that either sells to or buys for the Association. The Association does not have a policy regarding custodial credit risk.

At June 30, 2014 and 2013, most of the Association’s investments were invested in the State Treasury Special Purpose Investment Account (SPIA) and Local Government Surplus Trust Funds Investment Pool (Florida PRIME) and therefore, are not categorized as to custodial credit risk. The remaining investments listed above have custodial risk exposure.

At June 30, 2014 and 2013, the Association had $11,143,930 and $9,828,633, respectively, invested in commingled hedged strategies. These funds invest in various equities, debt instruments and derivatives in order to achieve the investment objectives of the fund. Redemptions of fund shares are limited to 50 percent of the previous month-end market value over a rolling three-month period.

Concentration of credit risk—At June 30, 2014 and 2013, more than five percent of the Association’s investments were held in the Florida Hedged Strategies Fund, LLC. Such concentrations are permitted by the Association’s investment policy.

Interest Rate Risk—Interest rate risk is the risk that changes in market interest rates will adversely affect the fair value of an investment. Generally, the longer the maturity of an investment, the greater the sensitivity of its fair value to changes in market interest rates. The Association does not have a policy for interest rate risk associated with its investments.

The Association’s investment in SPIA represents ownership of a share of the pool, not the underlying securities. This investment was not subject to custodial credit risk. The State Treasury has taken the position that participants in the pool should disclose information related to interest rate risk and credit risk. The SPIA carried a Standard and Poor’s credit rating of A+f, and had an effective duration of 2.57 years and 2.65 years at June 30, 2014 and 2013, respectively. The Association relies on policies developed by the State Treasury for managing interest rate risk or credit risk for this investment pool.

Florida PRIME is administered by State Board of Administration (SBA) pursuant to Section 218.405, of the Florida Statues and is a Securities and Exchange Commission Rule 2a-7 like external investment pool, similar to money market funds in which shares are owned in the fund rather than the actual underlying investments. This investment was not subject to custodial credit risk. The SBA has taken the position that participants in the pool should disclose information related to interest rate risk and credit risk. Florida PRIME carried a credit rating of AAAm by Standard and Poor’s and had a weighted average days to maturity (WAM) of 40 days at June 30, 2014 and 2013. The Association relies on policies developed by the State Board of Administration for managing interest rate risk or credit risk for this investment pool.

Disclosures for SPIA and Florida PRIME investment pools are included in the notes to the financial statements of the State of Florida’s Comprehensive Annual Financial Report.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(2) Cash and Investments: (Continued)

B. Investments: (Continued)

- 27 -

The Association’s long term investments include three investments in bond mutual funds, the PIMCO Total Return Fund Institutional Class (Total Return), PIMCO Unconstrained Bond Fund Institutional Class (Unconstrained Bond) and Templeton Global Bond Fund Advisor Class (Global Bond). The Total Return fund invests primarily in investment grade debt securities, but may invest up to 10% of its total assets in high yield securities rated B or higher by Moody’s or S&P or, if unrated, determined by PIMCO to be of comparable quality. The Total Return fund was unrated by Standard and Poor’s and had an effective duration of 5.7 and 5.8 years and an effective maturity of 8.4 and 6.5 years at June 30, 2014 and 2013, respectively. The Unconstrained Bond fund invests in a diversified portfolio of Fixed Income Instruments of varying maturities and is not constrained by management against an index. Fixed Income Instruments include bonds, debt securities and other similar instruments issued by various US and non-US public- or private-sector entities. The Unconstrained Bond fund was unrated by Standard and Poor’s and had an effective duration of 2.9 and 1.8 years and an effective maturity of 5.2 and 1.0 years at June 30, 2014 and 2013, respectively. The Global Bond fund seeks current income with capital appreciation and growth of income by investing predominately in bonds issued by governments and government agencies located around the world, including inflation-indexed securities. The Global Bond fund was unrated by Standard and Poor’s and had an average duration of 1.6 years at June 30, 2014 and 2013, and an average weighted maturity of 2.51 and 2.4 years at June 30, 2014 and 2013, respectively.

Additionally, the long term investments include a limited liability company investment that consists of an investment in the Crescent Senior Secured Loan Fund. This fund invests in a diversified portfolio consisting of direct or indirect interests in non-investment grade U.S. dollar denominated floating rate loans. The Crescent Senior Secured Loan Fund was unrated by Standard and Poor’s and had a weighted average life to final maturity of the assets in the portfolio of 5.5 and 5.4 years at June 30, 2014 and 2013, respectively.

Credit Risk—Credit risk relates to the risk that an issuer or other counterparty to an investment will not fulfill its obligations. The Association does not have a policy for credit risk associated with its investments.

(3) Accounts and Other Receivables:

Accounts and other receivables at June 30, 2014 and 2013, consist of the following:

2014 2013

Ticket accounts receivable $ 2,002,552 $ 2,322,968 Gator Boosters, Inc. 16,980,157 11,383,282 SEC and NCAA 254,373 6,537 Royalties and sponsorships 1,278,327 923,230 Other receivables 556,803 600,993

Total accounts and other receivables 21,072,212 15,237,010 Less allowance for doubtful accounts (22,540) (57,649)

Total accounts and other receivables, net $ 21,049,672 $ 15,179,361

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

- 28 -

(4) Accounts Payable and Accrued Expenses:

Accounts payable and accrued expenses consist of the following at June 30, 2014 and 2013:

2014 2013 Suppliers $ 1,972,076 $ 4,528,803 Salaries and benefits 3,740,923 2,362,369 Accrued interest 308,224 374,565 Gator Boosters, Inc. 1,339,111 219,987 Other 52,296 57,501

Total accounts payable and accrued expenses $ 7,412,630 $ 7,543,225

(5) Capital Assets:

Capital asset activity for the year ended June 30, 2014, was as follows:

Beginning Balance Additions Decreases

Ending Balance

Capital assets not being depreciated: Land and land improvements $ 2,430,236 $ - $ - $ 2,430,236 Construction in progress 1,323,246 4,044,971 (3,851,001) 1,517,216

Total capital assets not being depreciated 3,753,482 4,044,971 (3,851,001) 3,947,452

Capital assets being depreciated:

Buildings and improvements 6,075,303 211,520 - 6,286,823 Furniture and equipment 24,190,255 1,595,641 (447,743) 25,338,153 Leasehold improvements 218,236,630 3,852,315 - 222,088,945

Total capital assets being depreciated 248,502,188 5,659,476 (447,743) 253,713,921

Less accumulated depreciation for:

Buildings and improvements 3,312,957 236,265 - 3,549,222 Furniture and equipment 10,759,612 1,559,847 (445,070) 11,874,389

Leasehold improvements 63,129,275 7,189,436 - 70,318,711

Total accumulated depreciation 77,201,844 8,985,548 (445,070) 85,742,322

Total capital assets being depreciated,

net 171,300,344 (3,326,072) (2,673) 167,971,599

Capital assets, net $175,053,826 $ 718,899 $ (3,853,674) $171,919,051

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(5) Capital Assets: (Continued)

- 29 -

Capital asset activity for the year ended June 30, 2013, was as follows:

Beginning Balance Additions Decreases

Ending Balance

Capital assets not being depreciated:

Land and land improvements $ 2,430,236 $ - $ - $ 2,430,236 Construction in progress 6,850,839 8,696,912 (14,224,505) 1,323,246

Total capital assets not being depreciated 9,281,075 8,696,912 (14,224,505) 3,753,482

Capital assets being depreciated:

Buildings and improvements 6,075,303 - - 6,075,303 Furniture and equipment 30,121,001 4,017,366 (9,948,112) 24,190,255 Leasehold improvements 204,925,472 14,224,505 (913,347) 218,236,630

Total capital assets being depreciated 241,121,776 18,241,871 (10,861,459) 248,502,188

Less accumulated depreciation for:

Buildings and improvements 3,076,691 236,266 - 3,312,957 Furniture and equipment 15,723,816 1,730,297 (6,694,501) 10,759,612 Leasehold improvements 57,022,402 6,936,257 (829,384) 63,129,275

Total accumulated depreciation 75,822,909 8,902,820 (7,523,885) 77,201,844

Total capital assets being depreciated,

net 165,298,867 9,339,051 (3,337,574) 171,300,344

Capital assets, net $174,579,942 $ 18,035,963 $ (17,562,079) $175,053,826

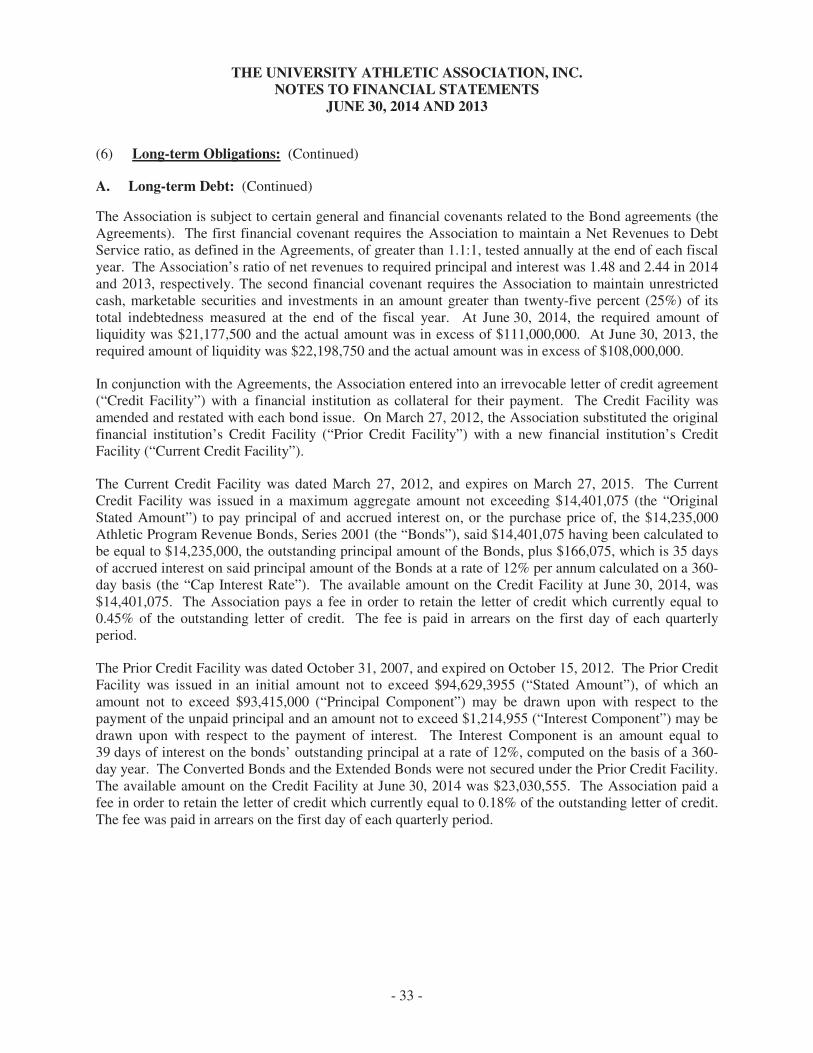

(6) Long-term Obligations:

The change in long-term obligations for the year ended June 30, 2014, was as follows:

Beginning Balance Additions Reductions

Ending Balance

Amounts Due Within One Year

Longevity incentive payable $ 205,000 $ 263,334 $ - $ 468,334 $ - Contracts payable 339,996 171,743 (252,749) 258,990 83,333 Accrued compensated absences 1,610,213 971,654 (874,405) 1,707,462 234,000 Deferred revenues 59,530,774 56,246,813 (57,237,976) 58,539,611 55,193,494 Long-term debt 88,795,000 8,165,000 (12,250,000) 84,710,000 4,080,000

Total long-term liabilities $150,480,983 $ 65,818,544 $ (70,615,130) $ 145,684,397 $ 59,590,827

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(6) Long-term Obligations: (Continued)

- 30 -

The change in long-term obligations for the year ended June 30, 2013, was as follows:

Beginning Balance Additions Reductions

Ending Balance

Amounts Due Within One Year

Longevity incentive payable $ 210,695 $ 215,695 $ (221,390) $ 205,000 $ - Contracts payable 423,001 171,064 (254,069) 339,996 83,333 Accrued compensated absences 1,670,562 753,052 (813,401) 1,610,213 290,000 Deferred revenues 62,667,036 55,039,772 (58,176,034) 59,530,774 53,991,123 Long-term debt 92,790,000 8,080,000 (12,075,000) 88,795,000 4,085,000

Total long-term liabilities $157,761,294 $ 64,259,583 $(71,539,894) $ 150,480,983 $ 58,449,456

A. Long-term Debt:

In February 1990, the Association issued $10,715,000 in tax-exempt variable rate revenue bonds. Proceeds of $10,559,000 were used to retire the outstanding 1982 and 1985 Stadium Revenue Bonds and pay accrued interest and costs associated with issuance. In December 1990, the Association issued an additional $17,300,000 in tax-exempt revenue bonds. Proceeds of the December 1990 issue were used to finance the construction cost of the North End Zone, and pay accrued interest and costs associated with issuance. Initially, the 1990 Bonds bore interest at the Daily Rate. The Daily Rate means that the interest rate is determined on each business day by the remarketing agent. The 1990 Series bond are scheduled to mature in the year 2020 and are secured by the gross revenues of the Association.

In August 1994, an additional $5,000,000 in tax-exempt variable rate revenue bonds was issued by the Association. Proceeds of the 1994 issuance were used to finance the construction of a volleyball practice gymnasium and to renovate the athletic field house. In October 2001, the Association issued $57,400,000 in tax-exempt variable rate revenue bonds. Proceeds of $4,688,193 were used to retire the outstanding 1994 Capital Improvement Revenue Bonds and pay costs associated with issuance. The remaining proceeds were used to finance the construction cost of the Basketball Practice Facility and the expansion of Ben Hill Griffin, Jr. Stadium. Construction of the Basketball Practice Facility was completed in 2002 and construction on the stadium was completed in 2004. The 2001 Series Athletic Program Revenue Bonds mature in the year 2031 and initially bore interest at the Multiannual Rate consisting of four tranches.

In September 2005, the Association issued $10,000,000 in tax-exempt variable rate revenue bonds. Proceeds were used to finance the construction of improvements and the expansion of McKethan Stadium at Perry Field, the construction of a new football equipment storage facility/restroom/training room and the renovation and improvements to the Lemerand Athletic Center (collectively, the “2005 Project”). Construction on the 2005 Project was completed in October, 2006. Initially, the 2005 Bonds bore interest at the Multiannual Rate.

THE UNIVERSITY ATHLETIC ASSOCIATION, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

(6) Long-term Obligations: (Continued)

A. Long-term Debt: (Continued)

- 31 -

Also in September 2005, the Association redeemed $800,000 of the Series 1990 Capital Improvement Revenue Bonds and converted all the remaining, outstanding 1990 Bonds ($19,600,000) to bear interest at the Multiannual Rate consisting of two tranches.

In October 2005, the Association converted a portion ($11,705,000) of the 2001 Bonds to the Daily Rate (as specified by the remarketing agent).

In October 2007, the Association issued $10,000,000 in tax-exempt variable rate revenue bonds. Proceeds were used to finance the acquisition, construction and equipping of capital improvements to Ben Hill Griffin Stadium (collectively, the “2007 Project”). Construction on the 2007 Project was completed in August, 2008. Initially, the 2007 Bonds bore interest at the Multiannual Rate.

In October 2008, the Association redeemed $2,400,000 of the Series 2005 Bonds and converted the remaining amount of the 2005 Bonds ($7,600,000) to the Weekly Rate (as specified by the remarketing agent). Additionally, the Association redeemed $710,000 of the Series 2001 Bonds and converted the remaining portion of that 2001 Bond traunch ($13,625,000) to the Weekly Rate.

In October 2009, the Association redeemed $4,000,000 of the Series 1990 Bonds and converted the remaining amount of the 1990 Bonds ($5,600,000) to the Weekly Rate (as specified by the remarketing agent). Additionally, the Association redeemed $790,000 of the Series 2001 Bonds and converted the remaining portion ($13,485,000) to the Weekly Rate and combined with the other 2001 Bonds into a Weekly Rate traunch ($27,110,000).

In December 2009, the Association converted the Weekly Rate traunch of the Series 1990 Bonds ($5,600,000), a portion of the Weekly Rate traunch of the Series 2001 Bonds ($22,130,000) and all of the Series 2005 Bonds ($7,000,000) to a Fixed Rate. The Converted Bonds bear an interest rate of 4.39%.

In October 2010, the Association converted $10,000,000 of the Series 1990 Bonds to the Weekly Rate (as specified by the remarketing agent). In January, 2011, the Association converted $10,000,000 of the Series 1990 Bonds and $15,950,000 of the Series 2001 Bonds (all the Weekly and Daily Rate traunches) to Extendable Bonds. The Extendable Bonds bear an interest rate of 1.95% until January 1, 2014.