the uk's eu referendum: brexit - what...

TRANSCRIPT

Investment Research

www.danskebank.com/CI

22 February 2016

Morten Helt Senior Analyst [email protected], + 45 45 12 85 18

The UK’s EU Referendum: Brexit - what if?

Mikael Olai Milhøj Analyst [email protected], + 45 45 12 69 08

Important disclosures and certifications are contained from page 35 of this report

2 www.danskebank.com/CI

Summary

• An EU-UK deal has been reached.

• The UK’s EU in/out referendum is set to be held in June (23 June).

• Our main scenario is that the UK remains in the EU.

• However, opinion polls indicate it is a close race and we would not rule out the possibility of the UK voting to leave the EU.

• A ‘Brexit’ could have a large impact on both the UK and the EU but we are in uncharted territory. To a large extent, it depends on the future relationship between the EU and UK in the case of a Brexit.

• Given the significant uncertainty surrounding the EU referendum, we see risks skewed on the upside for EUR/GBP going into election day. We expect volatility to remain high and believe EUR/GBP is likely to be very sensitive to newsflow, changes in polls and so on.

• We forecast EUR/GBP at 0.80 in 3M, lower in 6-12M on relative rates, growth and no Brexit. In our view, EUR-based clients should maintain a high short-term FX hedge ratio on GBP risks.

3 www.danskebank.com/CI

DEAL

4 www.danskebank.com/CI

Referendum held on 23 June

• Prime Minister David Cameron has announced that the EU in/out referendum is due to be held on 23 June 2016.

• (This has not been formally approved by parliament but we believe this is only a formality.)

• Voters will be asked: ‘Should the United Kingdom remain a member of the

European Union or leave the European Union?’

• Cameron has stated that cabinet members are free to campaign for each side but that he recommends the UK remains in the EU.

• Although the majority of politicians are in favour of staying in the EU, a fair number of Conservative and Labour members are in favour of leaving. UKIP is the most prominent advocator of leaving the EU.

• Scotland, Wales and Northern Ireland are generally more EU positive than England.

• A ‘leave’ win could trigger another Scottish independency referendum.

5 www.danskebank.com/CI

Deal summary

• The deal will be ’a legally binding and irreversible decision’ by all 28 leaders.

• The deal does not include any changes to the EU treaty, mostly changes to ’EU secondary legislation’.

• The deal is ’fully compatible with the Treaties’.

• The arrangements ’will become effective on the date that the government

of the United Kingdom informs the Secretary-General of the Council that

the United Kingdom has decided to remain a member of the European

Union’.

6 www.danskebank.com/CI

Deal summary

• Child benefits

− Child benefits for children living abroad are being indexed to the cost of living in the country (however, minimum equivalent to the level of benefits in the home country).

− This applies only to new claims made by EU workers until 1 January 2020.

− No intention to extend the system to ‘other types of exportable benefits, such as old-age pensions’.

• Migrant welfare payments

− ‘Safeguard mechanism that responds to situations of inflow of workers from other Member States of an exceptional magnitude over an extended period of time’.

− Limit the access to in-work benefits for immigrants ‘for a total period of up to four years from the commencement of employment’.

− Gradually increasing access to benefits over the four years.

− This safeguard mechanism ‘would have a limited duration [...] of seven years’, i.e. this emergency brake would be in effect until 2023.

• Limits on free movement

− No automatic free movement rights to nationals of a country outside the EU that marries an EU national.

− Excludes people believed to be a security risk.

European Council conclusions, 18-19 February 2016: http://www.consilium.europa.eu/en/meetings/european-council/2016/02/EUCO-

Conclusions_pdf/

7 www.danskebank.com/CI

Deal summary

• Euro area

− Not obliged to adopt the euro.

− The UK does not need to participate in bailouts. ‘Emergency and crisis measures designed to safeguard the financial stability of the euro area will not entail budgetary responsibility for Member States whose currency is not the euro’.

− ‘Measures the purpose of which is to further deepen economic and monetary union will be voluntary for Member States whose currency is not the euro....’

− Non-euro member states ‘will not create obstacles to but facilitate such further deepening while this process will, conversely, respect the rights and competences of the non-participating Member States’.

− A non-euro member state can demand decisions made by euro area countries be discussed at the EU council. The member state does not have a veto right in the matter though.

• City of London

− The Bank of England is responsible for the supervision of national banks and markets.

− However, ‘this is without prejudice to the development of the single rulebook...’.

European Council conclusions, 18-19 February 2016: http://www.consilium.europa.eu/en/meetings/european-council/2016/02/EUCO-

Conclusions_pdf/

8 www.danskebank.com/CI

Deal summary

• Sovereignty:

− The UK ‘is not committed to further political integration into the European Union’. ‘...this will be incorporated into the Treaties at the time of their next revision.’

− ‘Ever closer union’ does not apply to the UK. This will also be incorporated into the Treaties at the time of their next revision.

• 'Red card‘

− Of the national parliaments, 55% can block legislation (temporarily).

• Competitiveness

− ‘Fully implement and strengthen the internal market.’

− ‘Regulatory simplification and burden reduction.’ ‘Doing more to reduce the overall burden of EU regulation’.

− ‘Conclude ambitious bilateral trade and investment agreements with third countries.’ ‘Work must be advanced in negotiations with the US, Japan and key partners in Latin America and in the Asia-Pacific region.’

European Council conclusions, 18-19 February 2016: http://www.consilium.europa.eu/en/meetings/european-council/2016/02/EUCO-

Conclusions_pdf/

9 www.danskebank.com/CI

THE VOTERS

10 www.danskebank.com/CI

British voters increasingly split on EU membership

• The size of the ‘leave’ camp has been growing and it seems like a very close race.

• The opinion polls indicate that we cannot rule out a ’Brexit’.

• It is important to note that there is still a large group of undecided voters, who could alter the picture in coming months.

• Opinion polls before the deal showed that many voters want to stay in the EU on renegotiated terms.

• The question, which coming opinion polls may answer, is whether the UK voters are satisfied with the EU-UK deal.

Source: ICM, YouGov, Bloomberg

UK's EU membership

(%)

Current

terms

Renegotiated

terms

Remain in the EU 41 50 Leave the EU 41 23 Undecided 18 27

Renegotiated terms' = 'substantial changes'

0%

10%

20%

30%

40%

50%

60%

70%

Jul/2015 Sep/2015 Nov/2015 Jan/2016

Remain in the EU

Leave EU

Undecided

Source: https://en.wikipedia.org/wiki/Opinion_polling_for_the_United_

Kingdom_European_Union_membership_referendum

11 www.danskebank.com/CI

Most voters are worried about immigration and ‘benefit

tourism’

• In particular, the question is whether UK voters are satisfied with the deal on immigration and welfare benefits to the EU.

• Immigration, welfare benefits and more power to the national parliament are the most important issues according to a YouGov survey.

• Participants were asked to choose the three most important issues.

Source: YouGov, December 2015

12 www.danskebank.com/CI

Prominent Conservatives campaign to leave the EU

• Around 150 Conservative MPs are expected to campaign for the UK to leave the EU.

• Six cabinet members have announced they are campaigning for the UK to leave the EU. The most prominent is Michael Gove, the Justice Secretary.

• On Sunday, the Mayor of London Boris Johnson announced that he too will campaign for the UK to leave the EU. Boris Johnson is a very popular figure in the UK and is one of the favourites to succeed David Cameron as the leader of the Conservative Party.

• Boris Johnson’s announcement is seen as a significant blow to the ‘remain’ side.

Source: YouGov, October 2015: https://yougov.co.uk/news/2015/11/16/why-uk-might-end-voting-brexit/

13 www.danskebank.com/CI

WHAT IF?

14 www.danskebank.com/CI

’Brexit’ uncertainties by far analysts’ biggest concern

• Growth in the UK has slowed but the upturn remains on track, in our view.

• We still expect growth slightly above trend in coming years, driven mainly by domestic demand.

• ’Brexit’ is the main risk factor for the UK economy. Higher uncertainty until the referendum may hurt the recovery.

• The upcoming EU in/out referendum raises the issue that firms may be reluctant to invest as the future economic environment for British firms is uncertain.

• The majority of analysts agree that ‘Brexit’ is the biggest threat to the UK economy.

Source: Bloomberg, Danske Bank Markets

8%

9%

9%

9%

9%

56%

Biggest economic threat

Asset bubbles/current account deficit Other

Weak global growth

UK fiscal policy

Deterioration in UK household spending Brexit

Source: Bloomberg, Danske Bank Markets

15 www.danskebank.com/CI

Brexit timeline after a ‘leave’ vote

The full process could take several years

Note: Two years of negotiations can be extended (unanimous agreement)

EU laws still apply in the UK during the withdrawal

negotiations

Source: Danske Bank Markets

Referendum

bill passed by

Parliament

Negotiations

between UK

and EU

UK’s EU in/out

referendum to

be held on 23

June

In the event of Brexit, the

UK government has 2

years to negotiate the

terms of withdrawal cf.

Article 50 of the EU

Treaty

UK formally

exits EU

Further

negotiations to

define

relationship

(Swiss model or

FTA approach)

Autumn

2015 23 June

2016

c. 23

June

2018

? 20

February

2016

Deal

Election

campaign

16 www.danskebank.com/CI

Macroeconomic consequences

• It is very difficult to estimate what would happen if the UK votes to leave the EU.

• Standard economic models for the UK are not useful as they are based on the UK being an EU member state.

• To a large extent it depends on the future relationship between the EU and the UK.

• If many partial agreements are reached, the negative impact could be minor. If no agreements can be made, the negative impact could be major.

• It is worth noting that countries such as Norway and Switzerland do well without being EU member states. However, both countries have made agreements with the EU.

• There are also many negative political consequences as the UK is one of the largest and most important countries/economies in the EU.

• Overall, we judge that ’Brexit’ is a lose-lose game for both the UK and the EU.

Difficult to estimate impact on the UK economy

as there are so many uncertainties in the case of

‘Brexit’

Source: Bank of England, http://www.bankofengland.co.uk/publications/

Documents/speeches/2015/euboe211015.pdf

17 www.danskebank.com/CI

Transmission channels set to lower growth

• Could hit the UK manufacturing sector (restricted/limited access to the single market if no agreements are made).

• Could hit the UK financial sector (restricted/limited/no access to the single market if no agreements are made).

• Could hit UK firms if access to European labour supply is limited.

• Could lower foreign direct investment in the UK.

18 www.danskebank.com/CI

Different UK sectors would likely be affected very differently

Source: Open Europe: 'What if…? The consequences, challenges & opportunities facing Britain outside EU, 2015

19 www.danskebank.com/CI

Brexit scenarios

• As no member state has ever left the union (except Greenland, which left the EU in 1985), it is difficult to tell how the withdrawal negotiations would turn out.

• It is likely the negotiations would be difficult due to different interests and priorities.

• Norway and Switzerland are two examples of European countries that are not EU member states.

• The negotiations before the new EU-UK deal show that this may be easier said than done.

• Also, the EU has to show that it is not free to leave the union.

Source: Danske Bank Markets

Full single market

access Influence over EU

regulations No contributions

to EU budget

Political appeal Verdict

Swiss-style bilateral

accords ÷ ÷ ÷ + Possible but may not be attractive to the EU (cherry picking)

FTA

(free trade

agreement) ÷ ÷ + + Possible but depends on the deal

Norwegian style EEA

agreement + ÷ ÷ ÷ Does not address problems with the EU

Possible Brexit scenarios(pros and cons)

20 www.danskebank.com/CI

What about the UK’s financial centre?

• Large trade services surplus. Financial services account for a large share.

• The UK is the largest financial centre in the EU.

• One major concern in the UK has been the ever-growing financial regulation coming from the EU.

• If the UK leaves the EU, the UK can regulate its financial services industry on its own but with the risk that the importance of the City of London will decline.

• Looking at Switzerland, which also has a large financial services industry, firms have only limited access to the EU market, as they need to establish a subsidiary inside the EEA to sell their services.

Source: ONS, OECD, ECB

UK:

23.2 %

Germany:

15.7 %

France:

12,5 %

Italy:

12.4 %

Nether-

lands

6.8 %

Spain:

5.7 %

Rest of EU:

23.8 %

Share of EU financial services activity - gross value added

GBP bn Exports Imports Net exports

US 50 23 27EU 81 64 17Rest of the world 87 43 45

Trade in services

Source: ONS, OECD, ECB

21 www.danskebank.com/CI

However, not a given it is positive for the EU to lose City of

London either

• The UK could choose to compensate increasing costs on the financial institutions by lowering costs elsewhere (e.g. through taxation).

• There could be some pressure from financial institutions on the EU to strike a deal. Not straightforward (or cost free) to move the financial centre to, for example, Frankfurt.

• (Remember that half the world’s largest financial firms have their European headquarters in the UK.)

• Financial centres in Asia and US are growing – ’Brexit’ could accelerate this trend. The EU is very focused on financial regulation, so this could be a problem for the EU.

• Some financial centres in the EU may benefit from Brexit but businesses and households in the EU would be likely to face increased costs for financial services.

22 www.danskebank.com/CI

• Many foreign direct investments in the UK come from the EU.

• The financial sector accounts for a large share of inward FDIs (45%).

• It could hurt the UK economy if investors think that the return on investments in the UK has fallen.

• However, investment decisions depend on things other than EU membership.

The EU is the UK’s biggest investment partner

Source: ONS, OECD

Foreign direct

investments

GBP bn 2014 2013

EU 496 458

US 253 216

Rest 286 236

Total 1,034 910

FDI in the UK by source

GBP bn 2014 2013

EU 404 407

US 240 226

Rest 371 391

Total 1,015 1,025

UK FDI overseas by destination

Out

In

Source: ONS, OECD

Source: ONS, OECD

Source: ONS, OECD

23 www.danskebank.com/CI

Immigration another issue that needs to be addressed

• There would also be hard negotiations on migration. There are many UK citizens living abroad and many EU citizens living in the UK. This is an issue that needs to be addressed.

• Politically, the UK wants to limit immigration and welfare benefits to immigrants.

• Economically, the UK benefits from its access to the European labour force. This could drag down long-term growth perspectives if firms experience a shortage of skilled workers.

UK 55,375

Non UK citisens 8,277

- EU 3,025

- outside EU 5,252

Population in the UK by country of birth, 1000'

Total 4,917

- Europe 1,352

- EU 1,280

People born in the UK living overseas, 1000'

Source: ONS, UN

Source: ONS, UN

Source: ONS, UN Source: ONS, UN

24 www.danskebank.com/CI

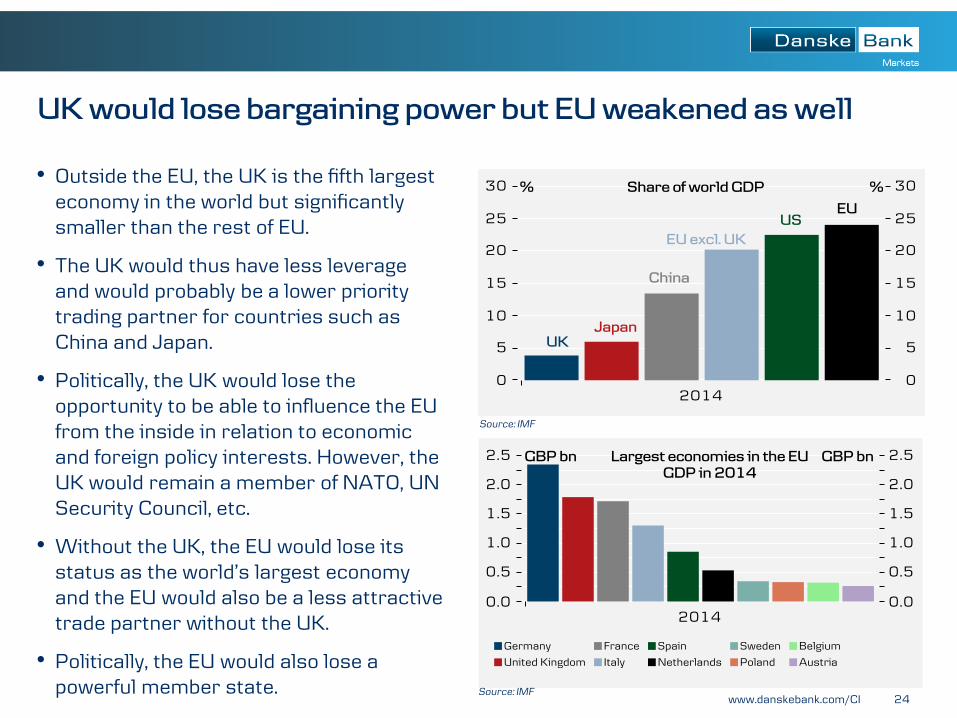

• Outside the EU, the UK is the fifth largest economy in the world but significantly smaller than the rest of EU.

• The UK would thus have less leverage and would probably be a lower priority trading partner for countries such as China and Japan.

• Politically, the UK would lose the opportunity to be able to influence the EU from the inside in relation to economic and foreign policy interests. However, the UK would remain a member of NATO, UN Security Council, etc.

• Without the UK, the EU would lose its status as the world’s largest economy and the EU would also be a less attractive trade partner without the UK.

• Politically, the EU would also lose a powerful member state.

UK would lose bargaining power but EU weakened as well

Source: IMF

Source: IMF

25 www.danskebank.com/CI

Brexit is a lose-lose game

Brexit is a lose-lose game

-6.4 -5.6

-2.2 -0.5 -0.4 -0.1

0.0 0.1 0.1 0.1 0.2 0.3 0.3 0.4 0.4 0.4 0.5 0.6

1.1 1.1 1.2 1.2

1.5 2.0

2.5 2.6 2.6

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4

Ireland

Malta

Luxembourg

Estonia

Bulgaria

Cyprus

Denmark

Finland

Slovenia

Croatia

Sweden

Netherlands

France

Italy

Romania

Greece

Latvia

Austria

Germany

Spain

Poland

Portugal

Hungary

Czech Republic

Belgium

Lithuania

Slovakia

% of GDP

Trade surplus with the UK in % of GDP 2014

-20,000 -10,000 0 10,000 20,000

Poland Hungary

Greece Romania Portugal

Czech Republic Bulgaria

Lithuania Spain

Slovakia Latvia

Slovenia Estonia

Malta Croatia Cyprus

Luxembourg Ireland Finland

Denmark Austria

Belgium Sweden

Italy Netherlands

UK France

Germany

Operating budgetary balance 2014 (EURm)

Deficit Surplus

Member States’ operating budgetary balances are calculated based on data on the allocation of EU expenditure by Member State and on Member States’ contributions to the EU budget

Source: EU, Eurostat Source: EU, Eurostat

26 www.danskebank.com/CI

Also bad for growth in other European countries

• As mentioned, we think a ‘Brexit’ would be a lose-lose game.

• Analysis finds that growth would be hit in other EU countries as well.

• To what extent depends on future relationships.

• Isolation of the UK hits economies more than a ‘soft exit’ would.

Source: Bertelsmann Stiftung, 'Brexit – potential economic consequences if

the UK exits the EU',May 2015

27 www.danskebank.com/CI

OUTLOOK FOR GBP

28 www.danskebank.com/CI

UK’s current account deficit is main risk factor for sterling

• The main risk for sterling is associated with the UK’s large current account deficit and its negative net international investment position (NIIP).

• As a deficit country, the UK relies on foreign investment and funding to finance its current account deficit.

• If it is no longer able to refinance its loans, or if investors no longer want to invest in the UK, it may have to run a current account surplus forcing domestic residents to spend less and/or would require a depreciation of the GBP.

UK’s significant current account deficit...

Source: Macrobond Financial, Danske Bank Markets

... and negative NIIP are risk factors for GBP

Source: Macrobond Financial, Danske Bank Markets

29 www.danskebank.com/CI

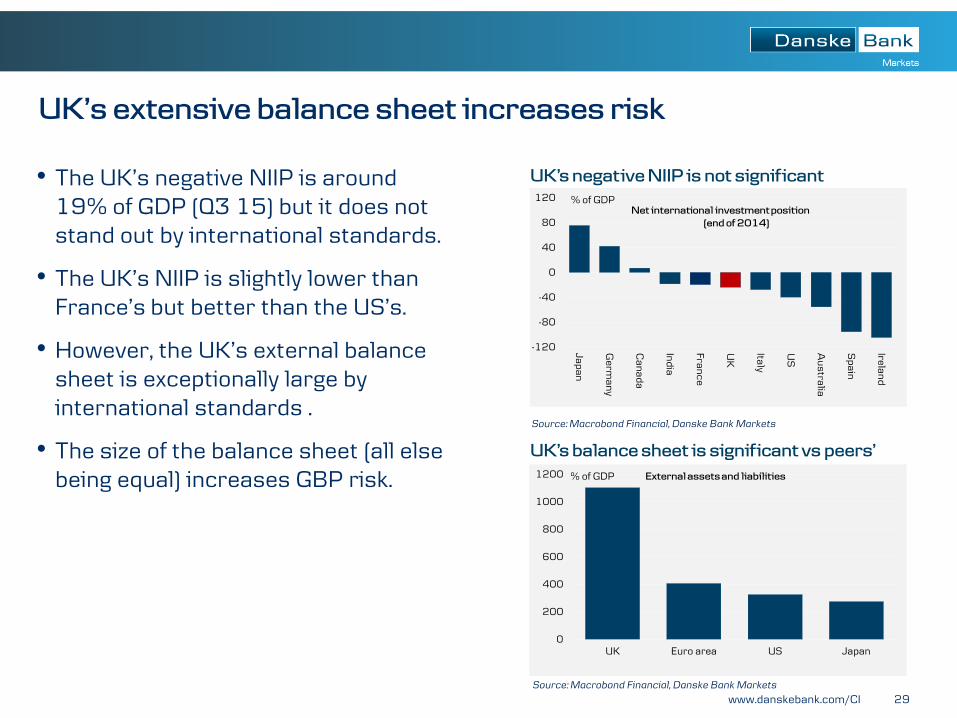

UK’s extensive balance sheet increases risk

• The UK’s negative NIIP is around 19% of GDP (Q3 15) but it does not stand out by international standards.

• The UK’s NIIP is slightly lower than France’s but better than the US’s.

• However, the UK’s external balance sheet is exceptionally large by international standards .

• The size of the balance sheet (all else being equal) increases GBP risk.

UK’s negative NIIP is not significant

Source: Macrobond Financial, Danske Bank Markets

UK’s balance sheet is significant vs peers’

Source: Macrobond Financial, Danske Bank Markets

-120

-80

-40

0

40

80

120

Jap

an

Germ

an

y

Ca

na

da

Ind

ia

Fran

ce

UK

Italy

US

Au

stralia

Sp

ain

Irelan

d

% of GDP Net international investment position

(end of 2014)

0

200

400

600

800

1000

1200

UK Euro area US Japan

% of GDP External assets and liabilities

30 www.danskebank.com/CI

UK in a better position now compared with 2008

Balance sheet is much smaller than in 2008

Source: Macrobond Financial, Danske Bank Markets

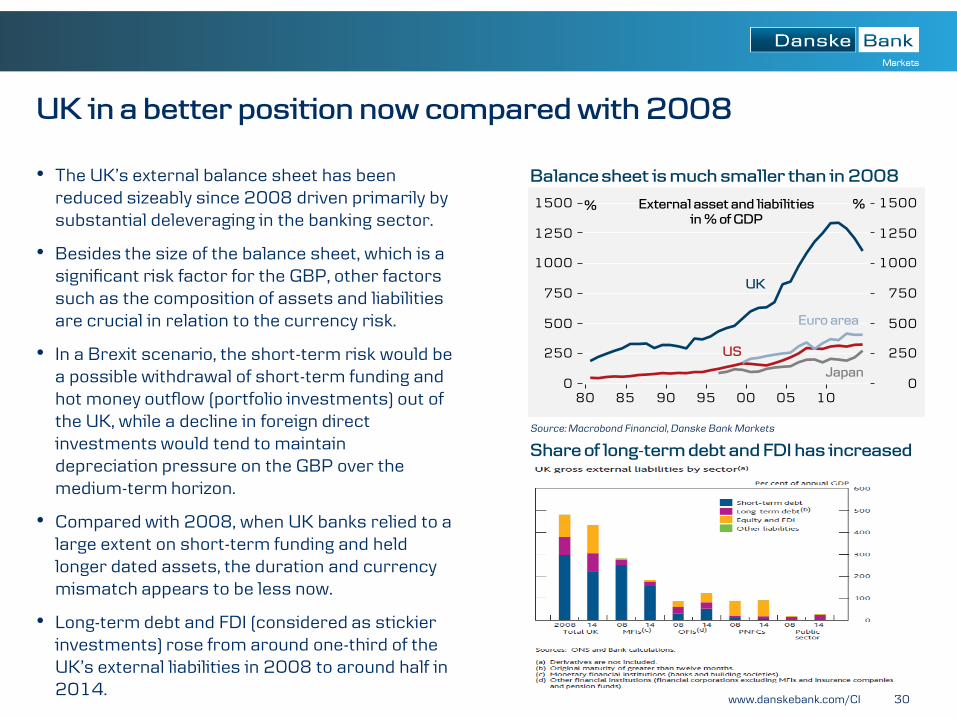

• The UK’s external balance sheet has been reduced sizeably since 2008 driven primarily by substantial deleveraging in the banking sector.

• Besides the size of the balance sheet, which is a significant risk factor for the GBP, other factors such as the composition of assets and liabilities are crucial in relation to the currency risk.

• In a Brexit scenario, the short-term risk would be a possible withdrawal of short-term funding and hot money outflow (portfolio investments) out of the UK, while a decline in foreign direct investments would tend to maintain depreciation pressure on the GBP over the medium-term horizon.

• Compared with 2008, when UK banks relied to a large extent on short-term funding and held longer dated assets, the duration and currency mismatch appears to be less now.

• Long-term debt and FDI (considered as stickier investments) rose from around one-third of the UK’s external liabilities in 2008 to around half in 2014.

Share of long-term debt and FDI has increased

31 www.danskebank.com/CI

Fundamentally EUR/GBP is not significant mispriced

- but GBP/USD is low

Danske Bank G10 PPP-model Danske Bank G10 MEVA-model

EUR/GBP trades slightly above medium- and long-term fair value.

According to MEVA models GBP/USD is significantly oversold. Our PPP model suggests around 1.60 is fair.

For details see FX Edge: Introducing the Danske G10 MEVA model (1 October 2015)

Source: Eviews, Macrobond Financial, Danske Bank Markets. Source:: Bloomberg, Macrobond Financial, Danske Bank Markets.

Source: Eviews, Macrobond Financial, Danske Bank Markets. Source:: Bloomberg, Macrobond Financial, Danske Bank Markets.

32 www.danskebank.com/CI

GBP has underperformed significantly since mid-November

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

GBP has been the worst performer among G10 over past 3

months

Relative rates alone cannot explain GBP depreciation

9.1%

3.7%

3.7%

3.0%

2.6%

1.7%

1.4%

1.2%

-3.0%

-6.9%

-10.0% -5.0% 0.0% 5.0% 10.0%

JPY

EUR

DKK

SEK

NZD

CHF

AUD

NOK

CAD

GBP

Spot changes (%) versus USD (since 16 Nov. 2015)

33 www.danskebank.com/CI

FX option market has priced in Brexit risk premium

GBP volatility is expensive

Overall

valuation

Implied vol.

1W chg.

Realised vol.

Overall

valuation

Implied vol.

1W chg.

Realised vol.

Overall

valuation

Implied vol.

1W chg.

Realised vol.

Overall

valuation

Implied vol.

1W chg.

Realised vol.

EUR/USD Expensive 12.2% 9.6% Neutral 11.0% 10.2% Neutral 10.9% 10.3% Neutral 10.8% 11.8%

EUR/GBP Expensive 12.9% 12.0% Expensive 11.6% 10.8% Expensive 12.3% 10.3% Expensive 11.7% 10.3%

GBP/USD Expensive 11.3% 11.0% Expensive 10.6% 8.8% Expensive 12.0% 8.0% Expensive 11.5% 8.5%

Danske Bank Implied Volatility Valuation

Currency

pairs

1M 6M3M 12M

Source: Bloomberg, Danske Bank Markets

EUR/GBP 25 delta risk reversals

Source: Bloomberg, Macrobond Financial, Danske Bank Markets

Source: Bloomberg, Danske Bank Markets

Based on 1Y 25 delta risk reversals

GBP volatility has increased more than other majors

May 2010 election Scottish referendum May 2015 election

GBP puts have become expensive

2W 1M 3M 6M 12Y

1.6 1.5 1.9 2.9 2.9

EUR/GBP

Vol Adjust. Z-Score

1M Risk Reversal History

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15 Feb-16

3M Abs. RR 5Y Mean +/-2 Stdev

GBP volatility is calculated as the average of 3M EUR/GBP and GBP/USD at-the-

money volatility;

other G10 currency volatility is calculated as the average of 3M EUR/USD,

AUD/USD, USD/CAD, USD/JPY and NZD/USD volatility Source: Bloomberg, Danske Bank Markets

34 www.danskebank.com/CI

EUR/GBP outlook

Higher ahead of referendum due to uncertainty

• Given the high uncertainty surrounding the EU referendum, we see risks skewed to the upside for EUR/GBP ahead of 23 June.

• A substantial Brexit risk premium has already been priced in the FX option market, and further significant GBP selling pressure is not likely to be seen before we come closer to election day.

• However, volatility is likely to remain high and EUR/GBP is likely to be very sensitive to newsflow, changes in polls and so on.

Lower 6-12M on relative rates, growth and ‘no

Brexit’

• Longer term, the outlook for EUR/GBP very much depends on the outcome of the EU referendum.

• In our main scenario, we assume a status quo for the UK, meaning that people vote to remain in the EU. This implies that GBP should appreciate immediately after the referendum.

• Longer term, we project further EUR/GBP downside driven by relative growth and relative monetary policy. We target EUR/GBP at 0.74 in 6M (0.71) and 0.73 in 12M (0.75) but stress that these forecast are subject to significant digital risk.

Forecast: 0.78 (1M), 0.80 (3M), 0.74 (6M) and 0.73 (12M)

Source: Macrobond Financial, Danske Bank Markets

EUR/GBP 1M 3M 6M 12M

Forecast (pct'ile) 0.78 (52%) 0.80 (70%) 0.74 (26%) 0.73 (27%)

Fwd. / Consensus 0.78 / 0.76 0.78 / 0.75 0.78 / 0.74 0.79 / 0.72

50% confidence int. 0.76 / 0.80 0.75 / 0.81 0.74 / 0.82 0.72 / 0.83

75% confidence int. 0.75 / 0.81 0.73 / 0.83 0.71 / 0.86 0.69 / 0.88

k

0.65

0.70

0.75

0.80

0.85

0.90

Feb-15 May-15 Sep-15 Dec-15 Mar-16 Jul-16 Oct-16 Jan-17

EUR/GBP

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

35 www.danskebank.com/CI

Disclosures This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The authors of this research report are Mikael Olai Milhøj, Analyst, and Morten Helt, Senior Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’ rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including as sensitivity analysis of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

36 www.danskebank.com/CI

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to distribution in the United States This research reportwas created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.