the time value of money chapter 9. chapter 9 - outline time value of money perpetuity future value...

TRANSCRIPT

The Time Valueof Money

Chapter 9

Chapter 9 - OutlineTime Value of MoneyPerpetuityFuture Value and Present ValueEffective Annual Rate (EAR)Annuity

Time Value of MoneyThe basic idea behind the concept of time value

of money is:– $1 received today is worth more than $1 in the

future OR – $1 received in the future is worth less than $1

today

Why?– because interest can be earned on the money

The connecting piece or link between present (today) and future is the interest rate

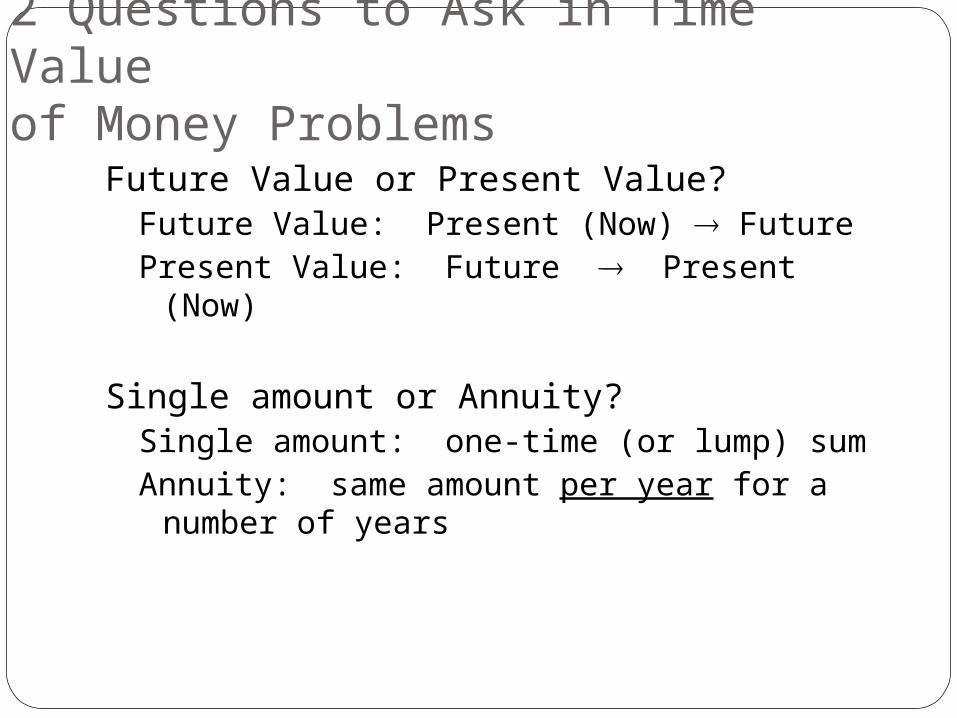

2 Questions to Ask in Time Value of Money Problems

Future Value or Present Value?Future Value: Present (Now) FuturePresent Value: Future Present (Now)

Single amount or Annuity?Single amount: one-time (or lump) sumAnnuity: same amount per year for a number

of years

Perpetuity: Constant Payment Forever

PV = PMT/iThis is the present value

of receiving a constant payment forever.

C

r

EXAMPLE:

• Suppose you wish to endow a chair at your old university. The aim is to provide $100,000 forever and the interest rate is 10%.

$100,000 PV = = $1,000,000 .10

A donation of $1,000,000 will provide an annual income of .10 x $1,000,000 = $100,000 forever.

PV =

Valuing perpetuities

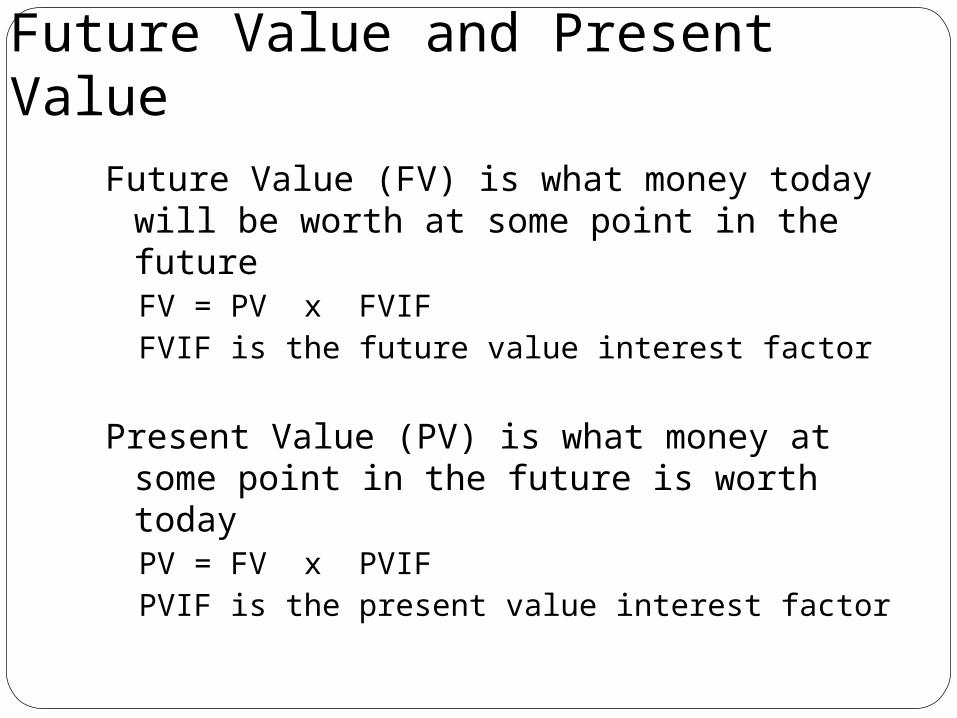

Future Value and Present ValueFuture Value (FV) is what money today will

be worth at some point in the futureFV = PV x FVIFFVIF is the future value interest factor

Present Value (PV) is what money at some point in the future is worth todayPV = FV x PVIFPVIF is the present value interest factor

Future Value of a Lump Sum

FV = PV * (1+i)n

Why is this formula correct?

This is the amount that will be accumulated by investing a given amount today for n periods at a given interest rate.

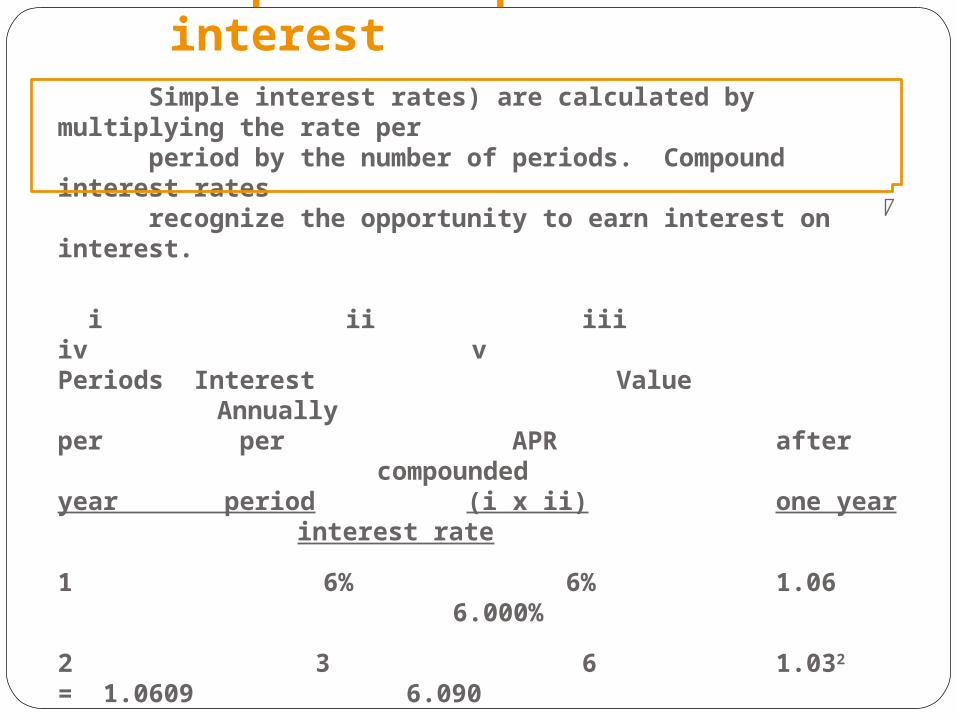

Simple & compound interest

Simple interest rates) are calculated by multiplying the rate per period by the number of periods. Compound interest rates recognize the opportunity to earn interest on interest.

i ii iii iv vPeriods Interest Value Annuallyper per APR after compoundedyear period (i x ii) one year interest rate

1 6% 6% 1.06 6.000%

2 3 6 1.032 = 1.0609 6.090

4 1.5 6 1.0154 = 1.06136 6.136

12 .5 6 1.00512 = 1.06168 6.168

52 .1154 6 1.00115452 = 1.06180 6.180

365 .0164 6 1.000164365 = 1.06183 6.183

Effective Annual Rate (EAR) or Yield (EAY)

EAR or EAY = (1+inom/m)m-1This is used to calculate the compounded

yearly rate. It considers interest being earned on interest.

Adjusting for Non-Annual Compounding

Interest is often compounded quarterly, monthly, or semiannually in the real world

Since the time value of money tables and calculators often assume annual compounding, an adjustment must be made in those cases:– the number of years is multiplied by the

number of compounding periods– the annual interest rate is divided by the

number of compounding periods

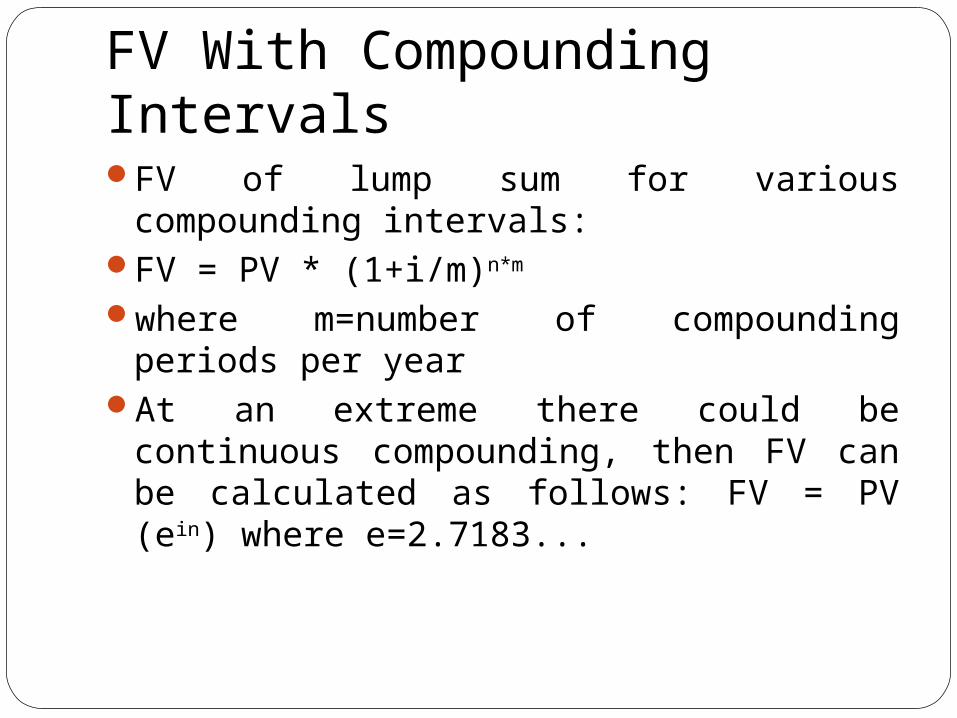

FV With Compounding IntervalsFV of lump sum for various compounding

intervals:FV = PV * (1+i/m)n*m

where m=number of compounding periods per year

At an extreme there could be continuous compounding, then FV can be calculated as follows: FV = PV (ein) where e=2.7183...

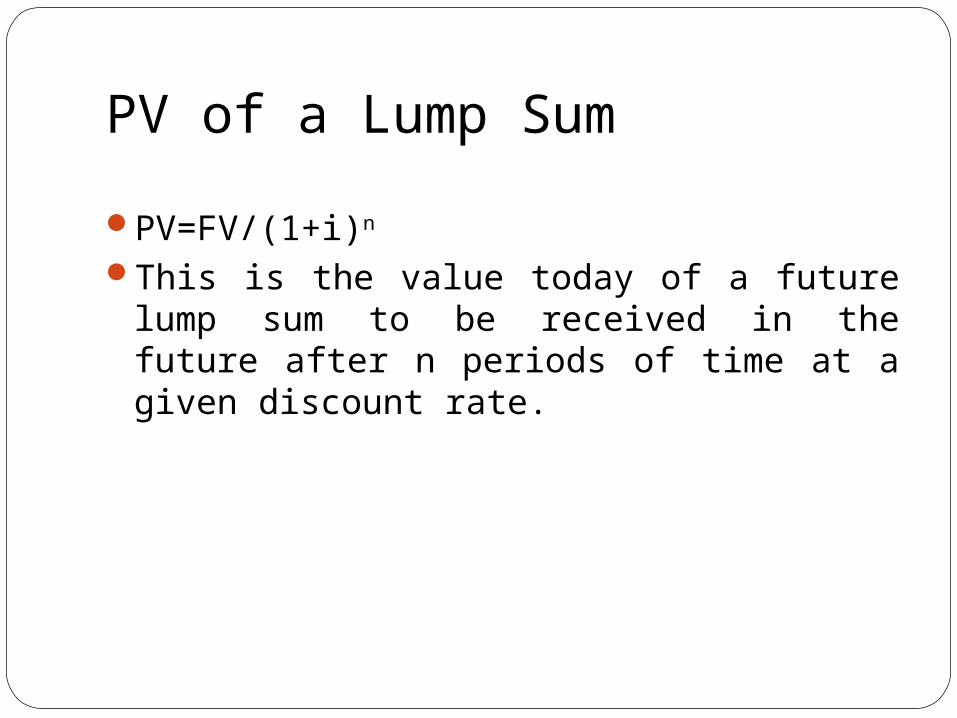

PV of a Lump Sum

PV=FV/(1+i)n

This is the value today of a future lump sum to be received in the future after n periods of time at a given discount rate.

Present valuesexample: saving for a new computer

Suppose: - you need $3000 next year to buy a computer - the interest rate = 8% per yearHow much do you need to set aside now?

3000PV of $3000 = = 3000 x .926 = $2777.77 1.08 1- year discount factor

By end of 1 year $2777.77 grows to $2777.77 x 1.08 = $3000

Suppose you can postpone purchase until Year 2.

3000PV = = 3000 x .857 = $2572.02 1.082

2-year discount factor

PV With Compounding IntervalsPV of a lump sum for various compounding

intervals is calculated as:PV=FV/(1+i/m)n*m

where m=number of compounding periods per year

At an extreme there could be continuous discounting, then PV=FV/(ein) where e=2.7183...

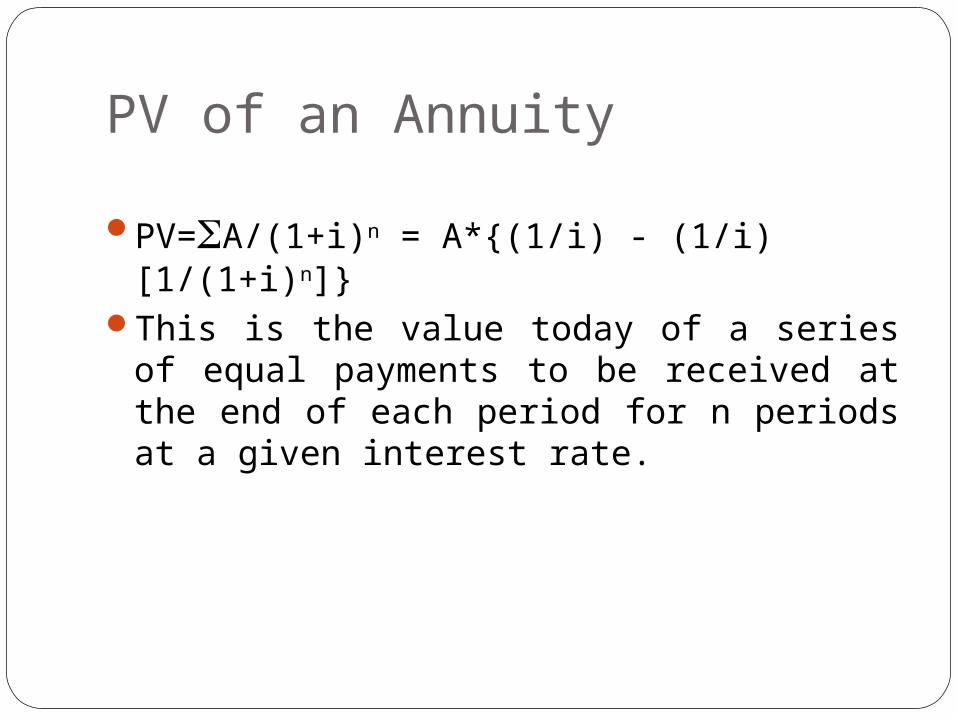

PV of an Annuity

PV=A/(1+i)n = A*{(1/i) - (1/i) [1/(1+i)n]}This is the value today of a series of equal

payments to be received at the end of each period for n periods at a given interest rate.

Asset Year of payment PV

1 2 . . t t+1 . .

Perpetuity (first payment year 1)

Perpetuity (first payment year t + 1)

Annuity from year 1 to year t (1+r)

1t)

Cr(-

Cr

(1+r))rC 1

( t

Cr

An annuity is equal to the difference between two perpetuities

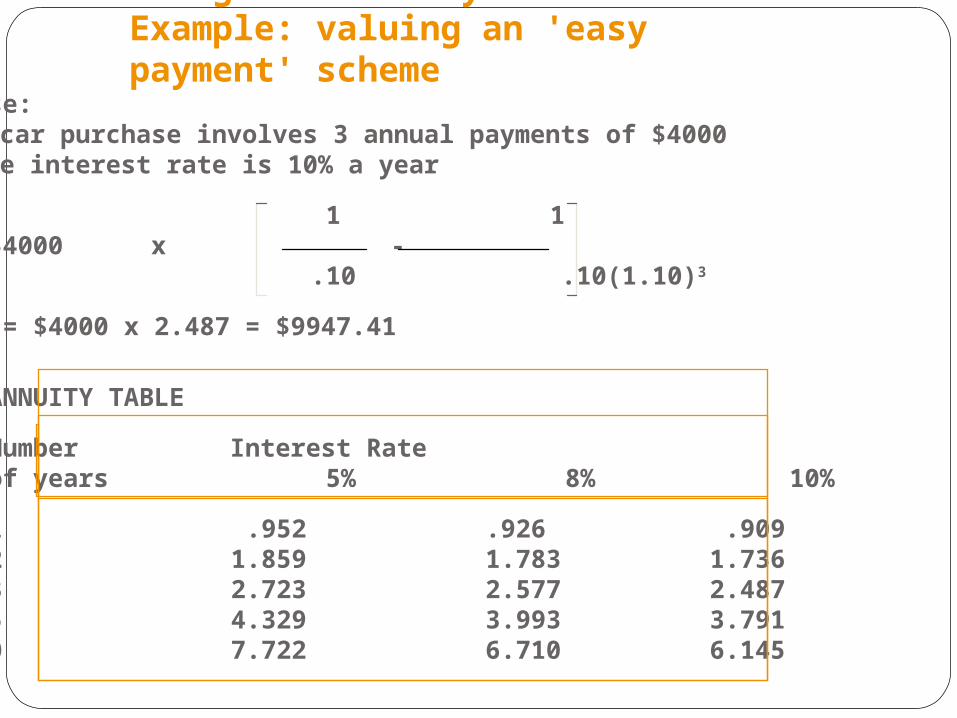

Using the annuity formulaExample: valuing an 'easy payment' scheme

Suppose: a car purchase involves 3 annual payments of $4000 the interest rate is 10% a year

1 1PV = $4000 x - .10 .10(1.10)3

= $4000 x 2.487 = $9947.41

ANNUITY TABLE

Number Interest Rate of years 5% 8% 10%

1 .952 .926 .909 2 1.859 1.783 1.736 3 2.723 2.577 2.487 5 4.329 3.993 3.791 10 7.722 6.710 6.145

FV of an Annuity

FV=A* (1+i)n = A*{[(1+i)n -1]/i} This is the accumulated value of equal

payments for n years at a given interest rate.

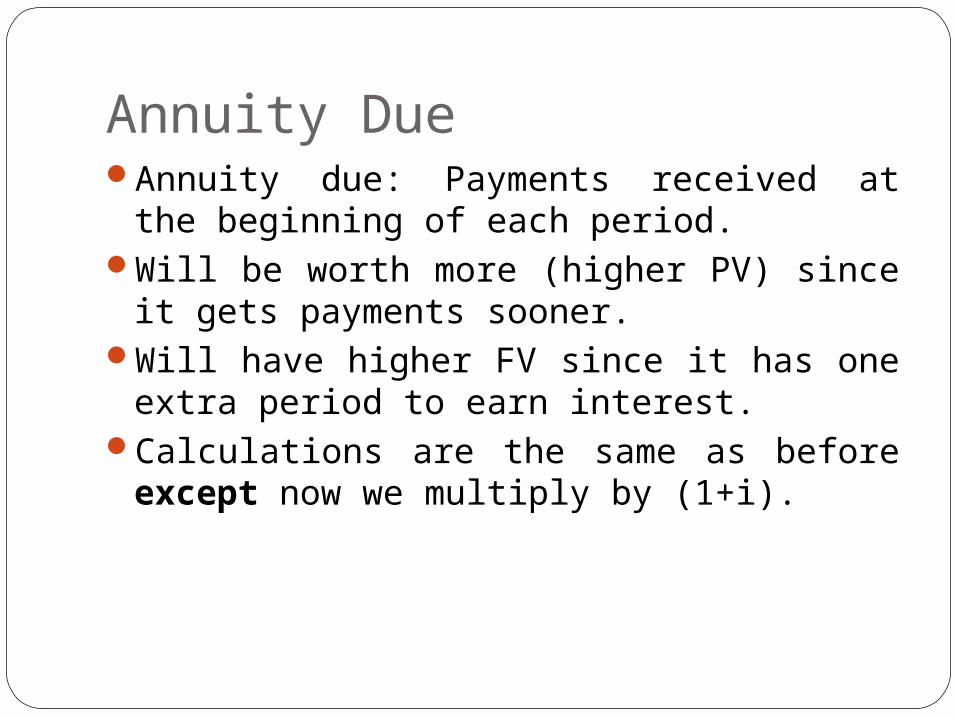

Annuity DueAnnuity due: Payments received at the

beginning of each period. Will be worth more (higher PV) since it gets

payments sooner.Will have higher FV since it has one extra

period to earn interest.Calculations are the same as before

except now we multiply by (1+i).

Solving for Annuity Payments (Present Value)

Recall thatPV=A*{(1/i) - (1/i) [1/(1+i)n]}, then

A=PV/{(1/i) - (1/i) [1/(1+i)n]}

A is the payment necessary for n years at given interest rate to amortize a present (loan) amount.

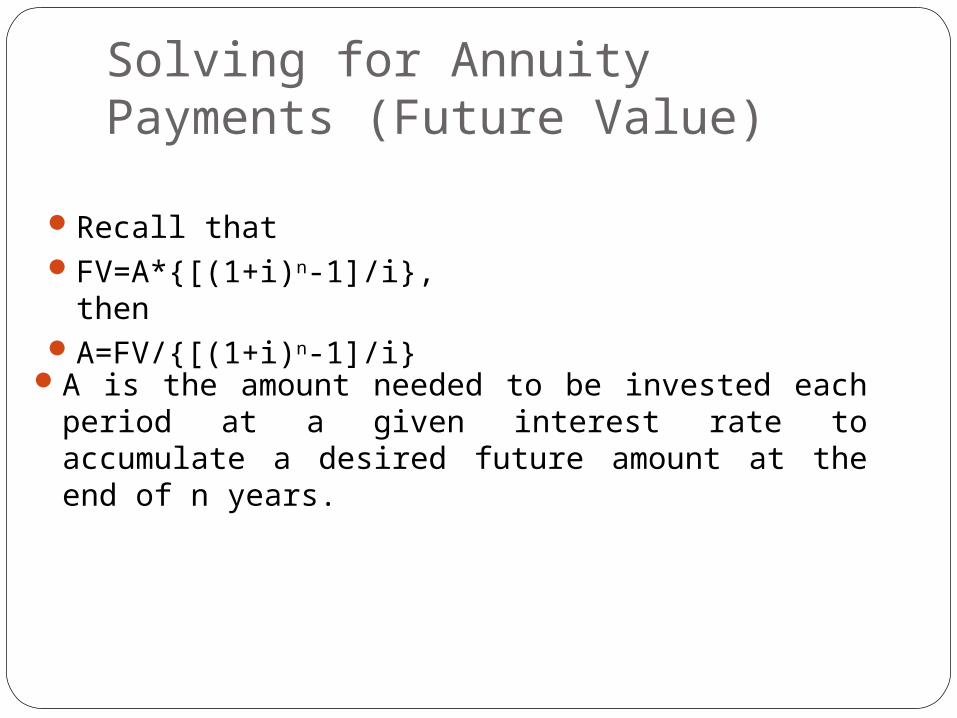

Solving for Annuity Payments (Future Value)

Recall thatFV=A*{[(1+i)n-1]/i}, thenA=FV/{[(1+i)n-1]/i}

A is the amount needed to be invested each period at a given interest rate to accumulate a desired future amount at the end of n years.

Solving for Rate of Return (i)For Lump Sum Case:

Since PV=FV/(1+i)n, then(1+i)n=FV/PV, and it follows that(1+i) = (FV/PV)1/n, and thereforei= (FV/PV)1/n-1

Solving for Rate of Return (i)Annuities:

In the annuity case, you could also solve for i using annuity relationship once you know the annuity.

You do not need a cash flow register.

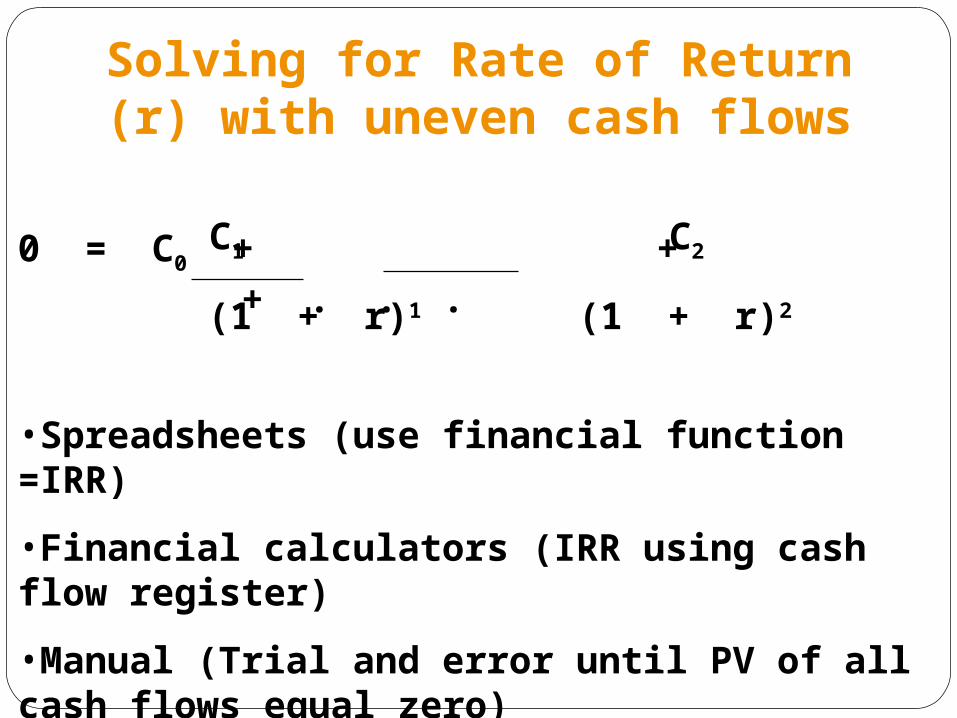

Solving for Rate of Return (r) with uneven cash flows

0 = C0 + + + . . .

•Spreadsheets (use financial function =IRR)

•Financial calculators (IRR using cash flow register)

•Manual (Trial and error until PV of all cash flows equal zero)

C1 C2

(1 + r)1 (1 + r)2

Solving for Number of Periods (n)

Since PV=FV/(1+i)n, then(1+i)n=FV/PV, and it follows thatnLN(1+i)=LN(FV/PV), and thereforen=LN(FV/PV)/LN(1+i)

Net Present Value in the General discounted cash flow formula

NPV = C0 + + + . . .

Note: It is today’s cost of capital that matters

C1 C2

(1 + r)1 (1 + r)2

Example

If C0 = -500, C1 = +400, C2 = +400

r1 = r2 = .12

NPV = -500 + +

= -500 + 400 (.893) + 400 (.794)

= -500 + 357.20 + 318.80 = +176

400 400

1.12 (1.12)2

Growing perpetuities

PV =

EXAMPLE:

Next year’s cash flow = $100

Constant expected growth rate = 10%, cost of capital = 15%

PV = = 2000

C

(r - g)

next year’s cash flow

cost of capital - growth rate

100

.15 - .10