the supply chain executive’s role in managing rising pharmacy expense · the supply chain...

TRANSCRIPT

THE SUPPLY CHAIN EXECUTIVE’S ROLE IN

MANAGING RISING PHARMACY EXPENSE

Marv Feldman, MS, RPh

Pharmacy Executive, Retired

OBJECTIVES

Overview the current trends in pharmacy supply expense with a focus on

the health-system environment (acute care and ambulatory clinics)

Discuss many of the contributing factors for this change including drug

pricing, medication utilization and availability of new products

Present the strategies being used to manage pharmacy supply cost

including the associated impediments to full implementation

Provide suggestions for the Supply Chain Executive to position their expertise

in helping to control overall pharmacy supply expense increase

LET’S START BY GETTING TO KNOW YOU…

How many of you work in a health-care provider setting and at an

executive level in supply chain leadership?

How many of you work in the health-care supplier industry and

have some interest in the changing pharmaceutical field?

How many of you are now (have been) close to the pharmacy

leadership in a hospital or health-system?

Who has actively participated in organized cost management?

Who here has the complete solution to rising drug expense?

Hospital formularies are open and getting more lax

Closing an “open formulary” will save significant dollars

Prescriptive patterns cannot be changed (“black box”)

Clinicians don’t pay attention to supply cost

The most costly product always works better

There is always an alternative product

We spend more for drugs when our census rises

We spend more for drugs…so we can save more in drugs

CEO MISCONCEPTIONS ABOUT COST MANAGEMENT

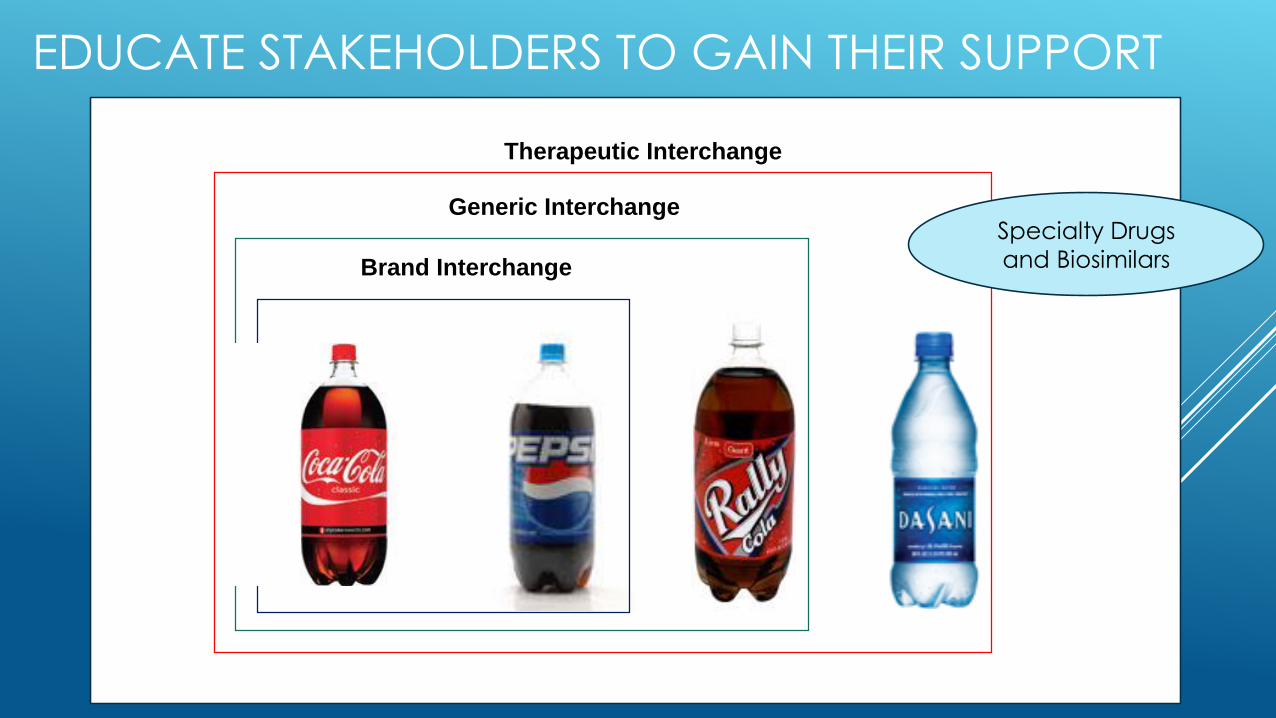

Brand Interchange

Generic Interchange

Therapeutic Interchange

EDUCATE STAKEHOLDERS TO GAIN THEIR SUPPORT

Specialty Drugs

and Biosimilars

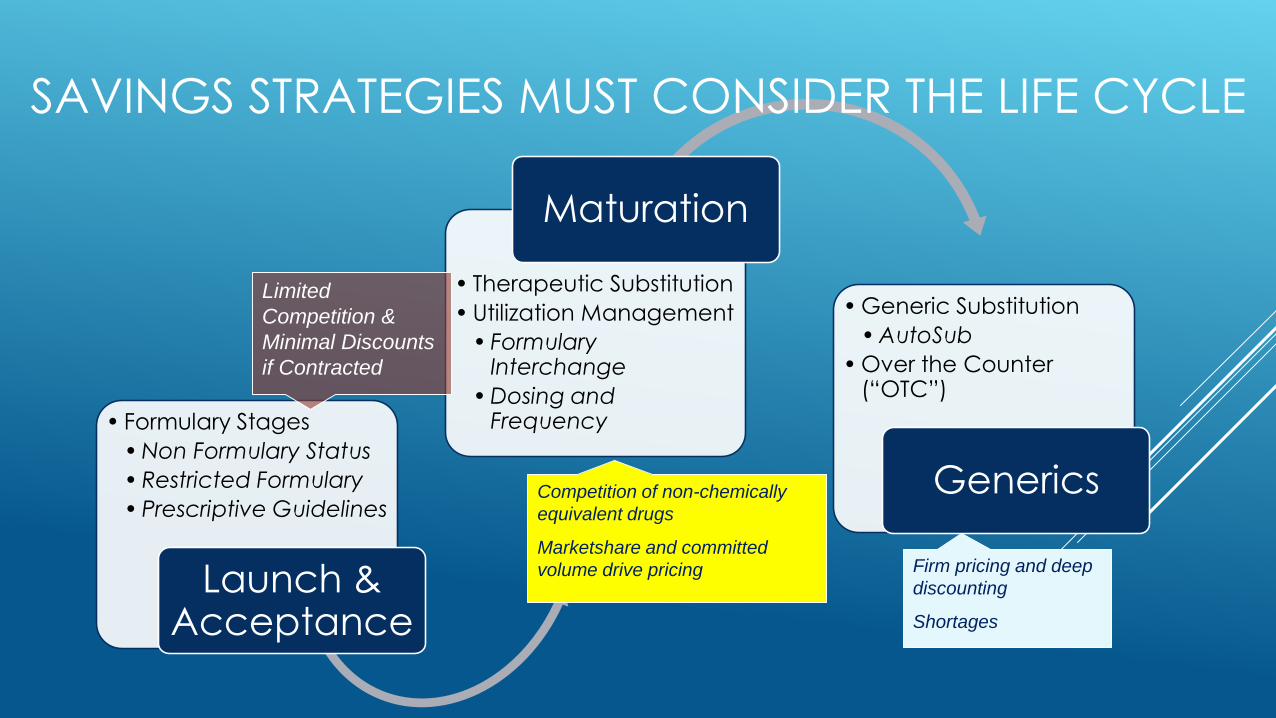

• Formulary Stages

• Non Formulary Status

• Restricted Formulary

• Prescriptive Guidelines

Launch & Acceptance

• Therapeutic Substitution

• Utilization Management

• Formulary Interchange

• Dosing and Frequency

Maturation

• Generic Substitution

• AutoSub

• Over the Counter (“OTC”)

Generics

Limited

Competition &

Minimal Discounts

if Contracted

Competition of non-chemically

equivalent drugs

Marketshare and committed

volume drive pricing Firm pricing and deep

discounting

Shortages

SAVINGS STRATEGIES MUST CONSIDER THE LIFE CYCLE

CAN UNDERSTANDING DRUG COST BE THIS SIMPLE?

PriceQuantity

UsedExtended ExpenseX

…probably not

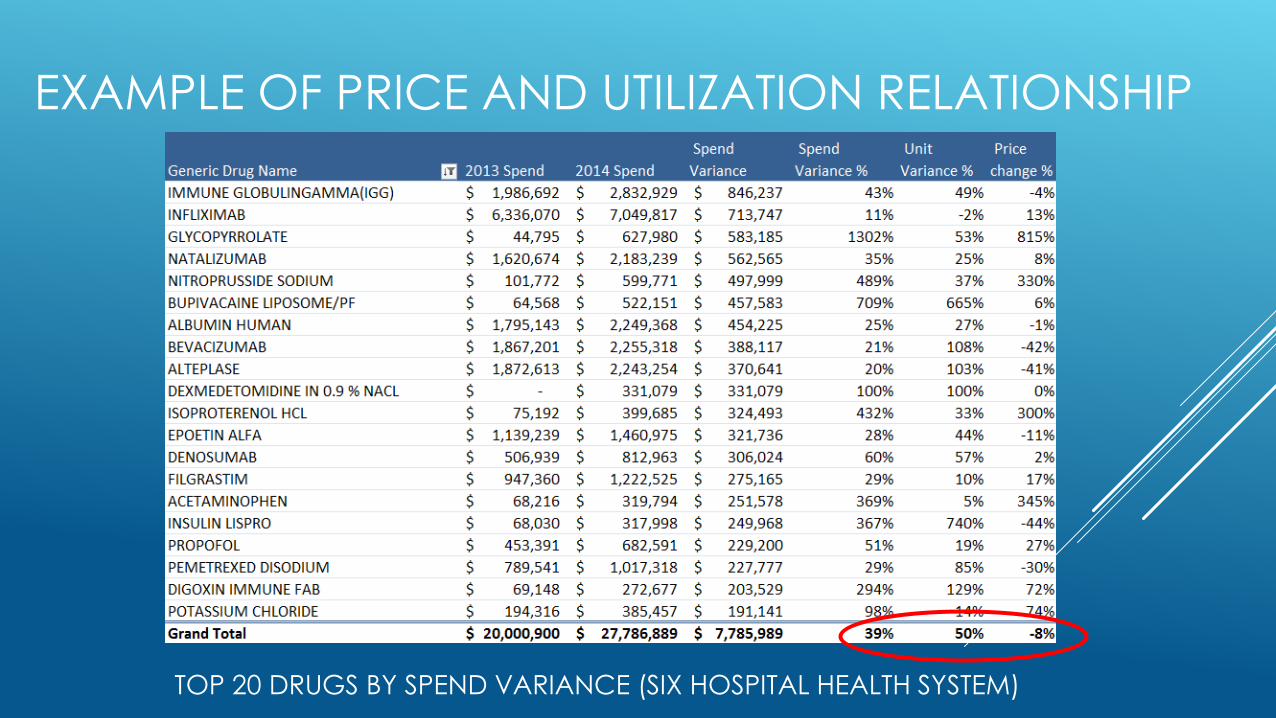

TOP 20 DRUGS BY SPEND VARIANCE (SIX HOSPITAL HEALTH SYSTEM)

EXAMPLE OF PRICE AND UTILIZATION RELATIONSHIP

Impacted by contracting (GPO, sole-source, aggregated, etc.)

Formulary considerations (preferred product, one-of-many)

Clinician preference (bias, unusual clinic/patient need)

Third party payers (restrictive and preferential coverage)

Access to specialty and limited distribution medications

Price

UNPRECEDENTED PRICE INCREASES >100% CY14/15CALCITONINSALMONSYNTHETIC VIAL MIACALCIN MIACALCIN 1255%

CEFAZOLIN SODIUM VIAL GENERIC CEFAZOLIN SODIUM 850%

MIDDRINE HCL MIDODRINE HCL 718%

HYDROCORTISONE CREAM PROCTOZONE-HC PROCTOZONE-HC 711%

AMIODARONE TABS PACERONE PACERONE 468%

ALLOPURINOL SODIUM VIAL ALOPRIM ALOPRIM 371%

PAPAVERINE HCL PAPAVERINE HCL 305%

CHLORPROMAZINE HCL TABLET CHLORPROMAZINE HCL 250%

FLUCYTOSINE GENERIC FLUCYTOSINE 248%

LEUPROLIDE ACETATE ELIGARD ELIGARD 214%

MITOMYCIN MITOMYCIN 200%

LIDOCAINE HCL SOLUTION LIDOCAINE HCL 153%

CEFEPIME HCL MAXIPIME MAXIPIME 151%

NYSTATIN NYSTOP NYSTOP 139%

TOLTERODINE TARTRATE DETROL LA DETROL LA 129%

PHYTONADIONE AMPUL VITAMIN K1 128%

NEOSTIGMINE METHYLSULFATE VIAL BLOXIVERZ BLOXIVERZ 127%

NALOXONE HCL SYRINGE NALOXONE HCL 120%

PHENOBARB/HYOSCY/ATROPINE/SCOP DONNATAL 112%

ALBENDAZOLE ALBENZA 105%

AMINOCAPROIC ACID VIAL AMINOCAPROIC ACID 100%

CEFTAROLINE FOSAMIL ACETATE TEFLARO 100%

FENOLDOPAM MESYLATE CORLOPAM CORLOPAM 100%

WHO WANTS TO LEARN MORE ABOUT THIS?

NEJM

Selection of most appropriate therapy (right drug therapy-right patient)

Accurate and timely comparison of the “cost to treat” (source of truth)

Drug shortages may impact selection (more expense option)

Deployment of clinical pharmacists to influence “smart shopping”

Adherence to Formulary and prescribing guidelines (evidence based)

Quantity Used

Visible Savings

Invisible Savings

Drug A costs $45 per dose. The price drops by

$5 through a new contract. Utilization remains

constant. Annualized savings (based on 1,000

doses given) total $5,000.

Pharmacy target program educates

physicians to prescribe this drug once

daily instead of twice. Consumption

then drops to 500 doses annually with

no change in price. Annualized savings

of $22,500 without any change in price.

CHANGING PRESCRIPTIVE GUIDELINE GIVES SAVINGS

WHAT ADDITIONAL SITUATIONS IMPACT YOUR COST?

Expansion of your ambulatory care foot print (oncology practices, retail)

DESI (Drug Efficacy Study Implementation) review

Drug expiry and discard (Fact or Fiction?)

Value-based Pharmaceutical Contracting

Predatory Corporate pricing (Acthar, Isoproterenol, IV Acetaminophen)

Regulatory changes (Chapter 797 and 800; 503B Compounding; 340B)

Washington DC environment and changes in ACA?

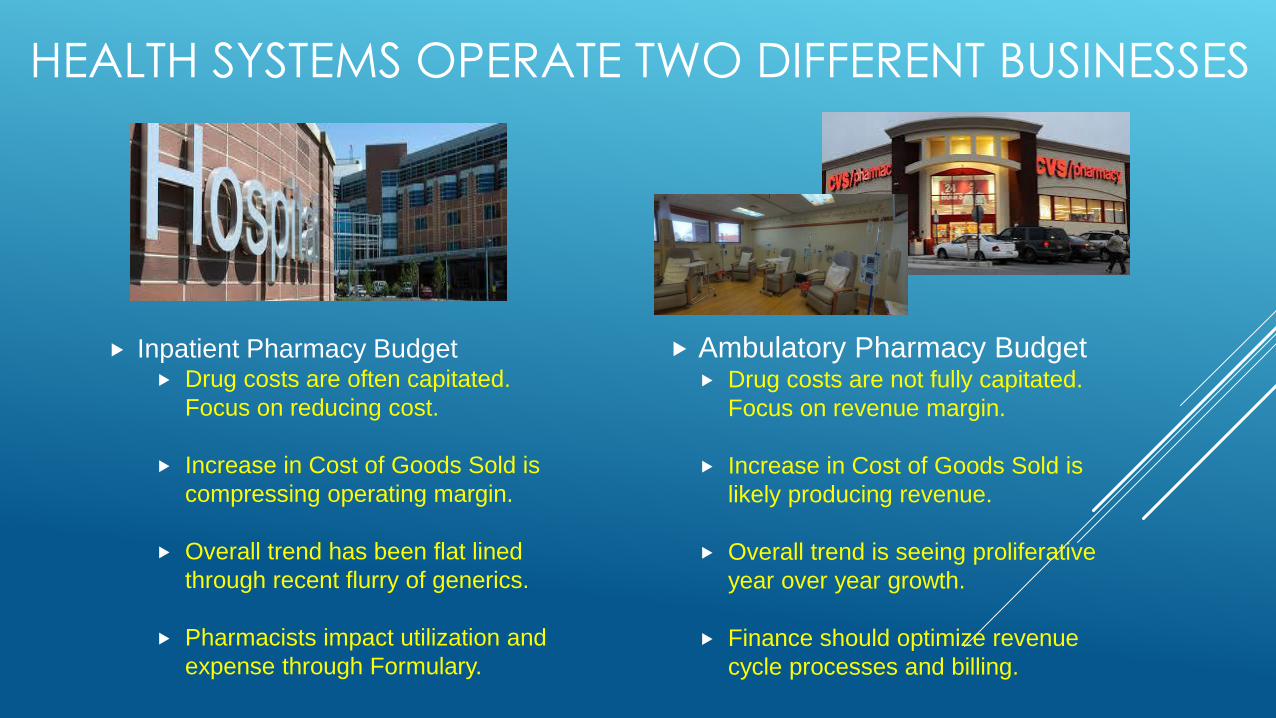

Inpatient Pharmacy Budget Drug costs are often capitated.

Focus on reducing cost.

Increase in Cost of Goods Sold is

compressing operating margin.

Overall trend has been flat lined

through recent flurry of generics.

Pharmacists impact utilization and

expense through Formulary.

Ambulatory Pharmacy Budget Drug costs are not fully capitated.

Focus on revenue margin.

Increase in Cost of Goods Sold is

likely producing revenue.

Overall trend is seeing proliferative

year over year growth.

Finance should optimize revenue

cycle processes and billing.

HEALTH SYSTEMS OPERATE TWO DIFFERENT BUSINESSES

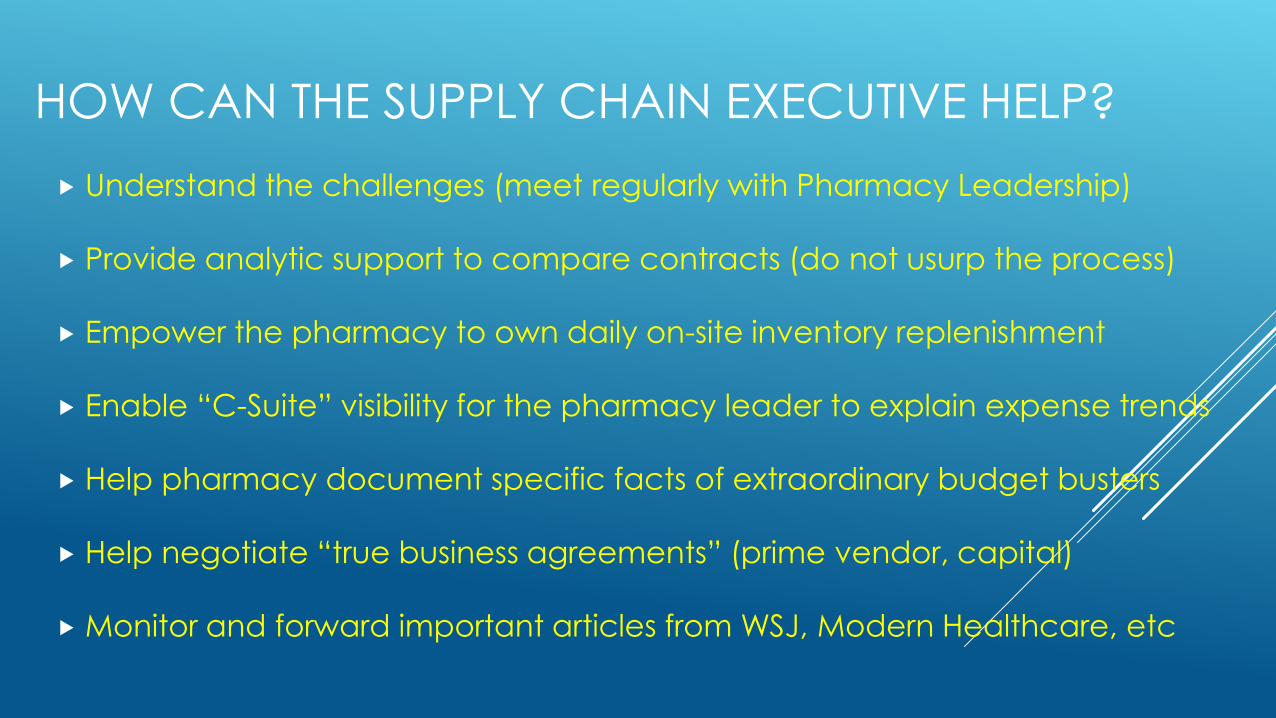

HOW CAN THE SUPPLY CHAIN EXECUTIVE HELP?

Understand the challenges (meet regularly with Pharmacy Leadership)

Provide analytic support to compare contracts (do not usurp the process)

Empower the pharmacy to own daily on-site inventory replenishment

Enable “C-Suite” visibility for the pharmacy leader to explain expense trends

Help pharmacy document specific facts of extraordinary budget busters

Help negotiate “true business agreements” (prime vendor, capital)

Monitor and forward important articles from WSJ, Modern Healthcare, etc

ASSUME YOUR PHARMACY LEADER WON’T SEE THESE

“What is driving up my health care costs?” (WSJ July 12, 2017)

“Novartis Defends Therapy’s Price” (WSJ August 31, 2017)

“Pfizer Files Antitrust Lawsuit Against J&J” (WSJ September 21, 2017)

“This State Is Taking On Drug Makers” (WSJ September 29, 2017)

“Abb Avie, Amgen Settle Humira Patent Fight” (WSJ September 29, 2017)

“Drug Prices Expected to Rise nearly 8% Next Year” (MH July 25, 2017)

“Providers Reduce Waste to Work Around Ballooning Drug Prices” (MH Sept 11, 2017)

QUESTIONS AND CONCLUDING THOUGHTS?