the strategic use of corporate cash holdings in collective

TRANSCRIPT

The strategic use of corporate cash holdings in collective bargaining with labor unions*

* We thank an anonymous referee, Amr Addas, Tom Bates, Edith Ginglinger, Jarrad Harford, David Haushalter, Jean Helwege, Marcin Kacperczyk, Kathy Kahle, Kai Li, Sattar Mansi, Josh Rosett, Bill Schwert, Husayn Shahrur, Janet Smith, Mike Stegemoller, Marc Weidenmier, and seminar participants at the University of Arizona, the 2007 Northern Finance Association Conference, and the 2008 French Finance Association conference for helpful suggestions. Hernan Ortiz-Molina acknowledges the financial support provided by the Social Sciences and Humanities Research Council of Canada. We are grateful to Barry Hirsch for providing us with his firm-level estimates of collective bargaining coverage. Tyler Brough and Aseem Vyas provided excellent research assistance.

Sandy Klasa Eller College of Management

University of Arizona Tucson, AZ 85721

520.621.8761 [email protected]

William F. Maxwell

Eller College of Management University of Arizona

Tucson, AZ 85721 520.621.1716

Hernan Ortiz-Molina Sauder School of Business

University of British Columbia Vancouver, BC V6T 1Z2

604.822.6095 [email protected]

July 2008

Abstract

We provide evidence that firms in more unionized industries strategically hold less cash to gain bargaining advantages over labor unions and shelter corporate income from their demands. Specifically, we show that corporate cash holdings are negatively related with unionization. We also find that this relation is stronger for firms that are likely to place a higher value on gaining a bargaining advantage over unions and weaker for those firms in which lower cash holdings provide less credible evidence that a firm is unable to concede to union demands. Additionally, we document that for unionized firms increases in cash holdings raise the probability of a strike. Finally, we show that unionization decreases the market value of a dollar of cash holdings. Overall, our findings indicate that firms trade-off the benefits of corporate cash holdings with the costs resulting from a weaker bargaining position with labor. JEL Classifications: G31; G32 Key Words: cash holdings; corporate liquidity policy; labor unions

The strategic use of corporate cash holdings in collective bargaining with labor unions

Abstract: We provide evidence that firms in more unionized industries strategically hold less cash to gain

bargaining advantages over labor unions and shelter corporate income from their demands. Specifically,

we show that corporate cash holdings are negatively related with unionization. We also find that this

relation is stronger for firms that are likely to place a higher value on gaining a bargaining advantage over

unions and weaker for those firms in which lower cash holdings provide less credible evidence that a

firm is unable to concede to union demands. Additionally, we document that for unionized firms

increases in cash holdings raise the probability of a strike. Finally, we show that unionization decreases

the market value of a dollar of cash holdings. Overall, our findings indicate that firms trade-off the

benefits of corporate cash holdings with the costs resulting from a weaker bargaining position with labor.

1. Introduction

Firms often take strategic actions to improve their bargaining position with input suppliers. For

instance, horizontal mergers can be used to improve the buying power of the merged firm vis-à-vis

suppliers of input goods (e.g., Robinson (1933), Snyder (1996), and Shahrur (2005)). Firms also strive to

improve their bargaining position against labor, since labor costs usually represent a large fraction of a

firm’s total costs. Bronars and Deere (1991) show that firms can strategically use financial leverage to

shelter income from labor unions’ demands. Further, DeAngelo and DeAngelo (1991) find that unionized

firms manage their earnings downward prior to labor negotiations. They contend that this allows managers

to gain concessions from unions by creating the perception that the firm’s competitive viability is

threatened by current economic conditions.

In this paper, we investigate whether firms’ cash holding policies are affected by strategic

considerations that arise in the bargaining between the firm and its unionized workers. We hypothesize

that lower reported cash holdings improve firms’ bargaining positions against unions. By implementing a

policy of holding less liquid assets in the presence of a union, a firm can make a more credible case that

the risk of liquidity shortages threatens its competitive viability, a situation that would be exacerbated by

granting additional concessions to the union. Thus, we predict that firms facing stronger unions

strategically hold smaller cash reserves to improve their bargaining position and shelter corporate income

from union demands. Also, we predict that because a larger cash balance weakens a firm’s bargaining

position and allows unionized workers to capture a larger fraction of firm profits, the contribution of cash

holdings to firm value is lower in firms that face a strong union.

The anecdotal evidence suggests that corporate cash holdings indeed play an important role in

collective bargaining with unions. For instance, in 2006 General Motors was faced with a strike by workers

at Delphi, the auto-parts supplier which it owns. The Economist reported that because Delphi’s workers

knew that General Motors had a cash balance of approximately 20 billion dollars “they hope the threat of

a strike will prompt GM’s management to dip into its cash reserves to compensate them for accepting

2

lower pay and benefits.”1 Similarly, at the end of 1995 the United Auto Workers pointed out that Chrysler

was sitting on a cash balance of 7.5 billion dollars and demanded that it was time “the company repay its

73,000 hourly and salaried workers for the concessions they made to help keep the automaker afloat

through the 1980s.”2 Finally, in 2005 Delta was able to use its falling cash balances to trigger a provision in

the contract with its pilots’ union which would allow Delta to seek pay cuts from the pilots.3

In our empirical tests we use a firm’s industry unionization rate, defined as the percentage of workers

in the firm’s industry that belong to a union, as our primary proxy for whether the firm is likely to bargain

with a powerful union that represents a large fraction of the firm’s workers. Over the 1983-2005 period we

find strong support for the hypothesis that firms facing more powerful unions strategically hold smaller

cash reserves to improve their bargaining position and shelter income from unions’ demands. Specifically,

we document that firm-level cash holdings are negatively associated with industry unionization rates and

also show that changes in cash holdings are negatively related with changes in unionization rates. Further,

in industry-level analyses we find that average industry cash holdings are negatively associated with

industry unionization. These results hold after controlling for profitability, the ease with which firms can

access external capital markets, growth opportunities, leverage, capital intensity, import penetration levels,

whether a firm recently had an initial public offering, and a number of other control variables.

For a smaller sample for which we have estimates of firm-level unionization rates, we confirm the

finding of a negative association between cash holdings and unionization. We also study the effect of

unionization on cash holdings using two industry case studies. These case studies provide further evidence

that unionized firms hold less cash than do their non-unionized rivals, and additionally show that firms

reduce their cash holdings after they become unionized.

To better understand the nature of the negative relation between unionization and corporate cash

holdings, we examine how this relation is affected by the importance that firms are likely to attach to

1 See, “Last Tango In Detroit,” The Economist, April 8, 2006. 2 See Nichole M. Christian, “UAW Gets Tough With Cash-Rich Chrysler,” The Wall Street Journal, January 11, 1996. 3 See Evan Perez, “Delta Tells Pilots Union It May Seek Concessions as Cash Dwindles,” The Wall Street Journal, August 22, 2005.

3

gaining a bargaining advantage over unions. If this relation is driven by firms that face strong unions

strategically maintaining low cash balances to improve their bargaining position, then it should be more

pronounced when a strong bargaining position against unions is more valuable. Prior work indicates that

labor demands are larger in more concentrated industries due to a higher persistence of economic profits,

and that unions capture a greater proportion of the available economic rents in these industries (e.g.,

Salinger (1984) and Karier (1985)). Also, extant work shows that in states that have right-to-work laws,

which prohibit unions from making membership or payment of union dues a condition of employment,

union bargaining power is reduced (e.g., Ellwood and Fine (1987) and Holmes (1998)). As well, the

importance of gaining a bargaining advantage against unions and minimizing labor costs should be greatest

for firms in industries in which labor costs represent a large fraction of total costs. Consistent with

expectations, we find that the negative effect of industry unionization rates on cash holdings is more

pronounced for firms in more concentrated industries, for firms principally located in states with no right-

to-work laws, and for firms in industries in which labor costs represent a larger fraction of total costs.

To further determine if the negative relation between cash holdings and industry unionization rates is

the result of collective bargaining issues, we examine the effects of factors that impact the bargaining

advantage provided by a small cash balance. If this negative relation arises because firms that face strong

unions hold less cash to gain a bargaining advantage, then this relation should be less pronounced for

firms in which smaller cash reserves are less credible evidence that the firm cannot concede to unions’

demands. DeAngelo and DeAngelo (1991) show that dividend cuts enable firms to obtain concessions

from unions by convincing rank-and-file union members that shareholders themselves are forced to make

sacrifices to alleviate the firm’s financial difficulties. Along the same lines, if a firm is a dividend-paying

firm that disburses free cash flows to shareholders, it can less credibly use a small cash balance to induce

the union to accept a labor contract favorable to the firm. Likewise, a small cash balance provides less of a

bargaining advantage for firms that can easily raise external capital to alleviate cash shortfalls. Also, firms

that are closer to financial distress can more credibly argue that because of their low cash reserves they are

unable to provide concessions to unions. Consistent with these ideas, we find that the negative relation

4

between cash holdings and unionization rates is less pronounced for dividend-paying firms and for firms

with higher bond ratings. We also show that this negative association is more pronounced for firms that

that face greater bankruptcy risk, such as those that are less profitable, have lower Altman-Z scores, or

have higher debt levels.

Additionally, we find some evidence of a small decrease in the cash holdings of unionized firms the

year prior to labor contract expirations. While this is additional evidence that unionized firms manage their

cash holdings downward to gain bargaining advantages over labor, this finding also suggests that these

firms obtain bargaining advantages over unions primarily by holding less cash at all times rather than

managing cash levels downward prior to negotiations.

Next, we investigate whether increases in cash holdings weaken a firm’s bargaining position.

Specifically, since unions are more likely to seek concessions when they perceive that a firm is more able

to concede to their demands, we examine whether increases in cash holdings are associated with the

likelihood of strikes. Consistent with higher cash holdings weakening firms’ bargaining positions, we find

that recent increases in cash holdings raise the probability of a strike.

Finally, we examine whether the contribution of cash holdings to firm value is lower in firms facing a

stronger union. We predict that this should be the case because a large cash balance is costly for a firm

that faces a strong union as it weakens the firm’s bargaining position and allows labor to capture a larger

fraction of firm profits. Using the Faulkender and Wang (2006) methodology to determine the market

value of a firm’ cash holdings, we find consistent with expectations that the value of a dollar of corporate

cash reserves is lower in more unionized industries.

Our study makes two main contributions. First, we provide evidence that firms facing stronger

unions strategically maintain low cash balances to gain bargaining advantages over organized labor. In

doing so, we add to the literature on how strategic considerations that arise in the bargaining between

firms and unions affect corporate decisions (e.g., DeAngelo and DeAngelo (1991), Bronars and Deere

(1991), and D’Souza, Jacob, and Ramesh (2001)). More broadly, our study contributes to the literature on

how firms’ financial decisions are affected by the strategic interaction between firms and input suppliers

5

(e.g., Robinson (1933), Snyder (1996), Fee and Thomas (2004), Shahrur (2005), and Kale and Shahrur

(2007)).

Second, our study sheds additional light on what determines corporate cash holdings and the

contribution of cash holdings to firm value. In particular, we provide new evidence on the costs associated

with holding more liquid assets. Prior work, such as Jensen (1986), Harford (1999), and Harford, Mansi,

and Maxwell (2008) generally focuses on the agency costs that arise in firms in which CEOs use excess

cash holdings to invest in negative net-present-value projects. Pinkowitz, Stulz, and Williamson (2006) and

Dittmar and Mahrt-Smith (2007) show that in such firms these costs significantly reduce the value of a

dollar of cash holdings. Our analysis identifies another important cost of large cash reserves: they weaken

firms’ positions in collective bargaining with unions, and thus allow labor to capture a larger portion of

profits. Given that Kim, Mauer, and Sherman (1998), Opler, Pinkowitz, Stulz, and Williamson (1999), and

Mikkelson and Partch (2003) show that larger corporate cash holdings benefit firms by providing them

with the ability to fully invest in their growth prospects, our results suggest that unionized firms trade-off

these benefits with the costs resulting from a less favorable bargaining position with organized labor.

The remainder of the paper is organized as follows. Section 2 reviews prior work, develops

hypotheses, and discusses our empirical approach to measure union bargaining power. Section 3 describes

our sample and variables. Section 4 presents our empirical findings. Finally, Section 5 concludes.

2. Related literature, hypothesis development, and empirical approach

2.1. Bargaining betweens firms and unions: Theory

Most strategic models on collective bargaining between firms and unions consider a general two-party

situation (bilateral monopoly) in which a union tries to maximize the utility of its members, while the firm

attempts to maximize its value. The desire of a particular party to concede or hold out depends on

objective factors, such as the state of product demand and capital-labor substitution, and on subjective

factors, such as the assessment of the bargaining strategy of the other party. The wide variety of existing

models differ in their views of labor unions’ objectives, the information sets of each of the parties,

6

whether firms and unions negotiate over wages, employment, or both, whether the bargaining is static or

dynamic, and on how disagreements are resolved in practice. For example, in traditional static models,

such as those in Leontief (1946) and McDonald and Solow (1981) unions have control over wages but

firms choose employment levels. Earle and Pencavel (1990) model the bargaining over hours of work and

both Clark (1990) and Johnson (1990) model the bargaining over work rules. Other models rely on the

Nash (1950) bargaining solution where each party receives its payoff in case of disagreement plus a

fraction of the joint surplus that is increasing in the party’s bargaining power. Sequential bargaining models

based on Rubinstein (1982) incorporate the cost of delays in reaching agreements. For instance, in war of

attrition models (e.g., Fundenberg and Tirole (1986)) a party’s ability to endure strikes endows it with a

strong bargaining position.

Since the failure to agree on a settlement prior to a contract’s expiration is costly to the firm (loss of

profits) and workers (loss of wages), most collective bargaining models embed a tendency for the parties

to come to an agreement in time to avert a strike. Moreover, regardless of specific modeling details, in

these models a party’s ability to increase its share of the firm’s surplus is directly related to its bargaining

power. We hypothesize that firms can strategically use their cash holdings to increase their bargaining

power vis-à-vis the union, and thus obtain a larger share of firm surplus.

2.2. Bargaining betweens firms and unions: Empirical evidence

Prior empirical work shows that unionized firms place important emphasis on increasing their

bargaining power with unions. For instance, DeAngelo and DeAngelo (1991) provide evidence from the

restructuring of the steel industry during the 1980s showing that to gain concessions from unions firms

often try to make the case that the firm’s competitive viability is threatened by current economic

conditions. Their findings suggest that prior to negotiations with unions firms manage their earnings

downward in order to help their case for union concessions. Specifically, they show that unionized firms

report lower net income during negotiation than non-negotiation years. This difference is driven by

managers using their discretion to report one-time special charges during negotiation years. D’Souza,

7

Jacob, and Ramesh (2001) also report findings indicating that firms engage in earnings management to

gain bargaining advantages with unions. They document that prior to reducing retirement benefits

unionized firms are likely to adopt new accounting standards that allow them to reduce current net

income. Finally, DeAngelo and DeAngelo (1991) also find that during negotiations with unions

stakeholders other than union members agree to make sacrifices to bolster managerial requests for labor

concessions. For instance, they show that dividend reductions and cuts to managerial compensation are

more likely to occur during negotiations.

Bronars and Deere (1991), Hanka (1998), and Matsa (2006) suggest that firms can also improve their

bargaining power with unions by issuing more debt. By committing itself to repaying a larger portion of

future cash flows to creditors the firm puts a ceiling on the revenues that labor can extract from the firm

without driving it into bankruptcy. Consistent with these propositions, Bronars and Deere (1991) and

Matsa (2006) show that more unionized firms hold more debt than do less unionized firms. Also, Hanka

(1998) reports that higher debt results in decreased labor costs.

2.3. Corporate cash holdings

Because firms presumably choose their cash holding policies by trading-off benefits and costs of

holding cash reserves, recent research focuses on identifying these benefits and costs. Corporate cash

holdings are beneficial to firms because they reduce underinvestment problems in firms with high external

financing costs and large growth opportunity sets (e.g., Kim, Mauer, and Sherman (1998), Opler,

Pinkowitz, Stulz, and Williamson (1999), and Mikkelson and Partch (2003)). Supporting this view,

Faulkender and Wang (2006) document that the contribution of cash holdings to firm value is larger in

more financially constrained firms. Also, Harford, Mikkelson, and Partch (2003) show that a large cash

balance enables firms to continue investing in their growth opportunities both during and immediately

after an industry downturn. Further, Haushalter, Klasa, and Maxwell (2007) find that the ability to fully

invest in growth opportunities provided by cash holdings enables firms to compete more successfully in

the product markets.

8

On the other hand, large cash reserves can also be costly to the firm. In addition to the lower return

earned by cash holdings relative to other investments of the same risk, in firms with important agency

problems large cash holdings can allow managers to invest in value-decreasing projects (e.g., Jensen (1986),

Harford (1999), and Harford, Mansi, and Maxwell (2008)). Consistent with the idea that in such firms cash

holdings are costly, Pinkowitz, Stulz, and Williamson (2006) and Dittmar and Mahrt-Smith (2007) show

that market participants value a dollar of cash holdings less highly when a firm has more severe agency

problems.

2.4. Hypothesis development

Our main hypothesis is that firms’ cash holding policies are determined, at least in part, by strategic

considerations that arise in the collective bargaining between firms and unionized workers. In particular,

we argue that a policy of holding less liquid assets improves firms’ bargaining positions against labor

unions, and that firms choose their cash holding policies taking this into account. Our intuition is simple.

By holding small cash reserves, a firm can make a more credible case that the risk of liquidity shortages

threatens its competitive viability, a situation that would be exacerbated by granting additional concessions

to unionized workers. As a result, a policy of holding smaller cash reserves is beneficial to the firm because

it allows it to moderate the demands of its labor force. Thus, our first hypothesis is:

Hypothesis 1. Firms facing unions with greater bargaining power strategically hold smaller cash reserves to improve their bargaining position and shelter corporate income from union demands.

Our main hypothesis also suggests the following three sub-hypotheses.

Hypothesis 1a. The negative relation between corporate cash holdings and the union’s bargaining power is stronger (weaker) for firms that attach more (less) importance to gaining a bargaining advantage over unions.

Hypothesis 1b. The negative relation between corporate cash holdings and the union’s bargaining power is stronger (weaker) for firms in which a small cash balance is likely to provide a larger (smaller) bargaining advantage.

Hypothesis 1c. Firms that experience increases in their cash holdings lose bargaining strength relative to unions and this raises the likelihood that a union decides to strike to obtain concessions from the firm.

9

Finally, previous work shows that the market value of firms’ cash holdings depends on the costs and

benefits of holding more liquid assets. Since large cash holdings are more costly for firms facing a strong

union because they weaken the firm’s bargaining position and allow labor to capture a larger fraction of

profits, this should be reflected in the market’s valuation of cash reserves. This leads to our second

hypothesis.

Hypothesis 2. The contribution of cash holdings to firm value is lower in firms that face stronger unions.

2.5. Empirical approach to measure union bargaining power

The labor economics literature typically uses unionization rates to measure union bargaining power.

The underlying logic is that a union’s bargaining power is increasing in the fraction of the firm’s workers

that are unionized, because unions’ actions in firms that have a large fraction of unionized workers carry

more important consequences for the firm. It is difficult to reliably collect firm-level unionization data

from the filings of publicly traded firms because such firms are not required to provide union membership

information about their workers. However, the Bureau of Labor Statistics collects detailed and accurate

industry-level data on union membership. As a result, previous studies on labor unions assume that

industry unionization rates are a reasonable proxy for the expected unionization rates of firms within an

industry and use them as a proxy for union bargaining power (e.g., Rosen (1969), Karier (1985), Connolly,

Hirsch, and Hirschey (1986), and Bronars and Deere (1991)). The empirical evidence supports the use of

industry unionization rates as a proxy for union bargaining power. For example, early work by Rosen

(1969) shows that in industries with higher unionization rates production workers earn higher salaries.

In our main tests we follow most of the previous literature and use industry unionization rates to

proxy for whether firms in a given industry are likely to bargain with a powerful union. An important

advantage of this approach is that it allows us to conduct a large-scale study of the effect of unionization

on corporate cash holdings. This gives us confidence about the general validity of the findings we

document across an important spectrum of firms and industries. Of course, the disadvantage of our

10

approach is that industry unionization rates may be a noisy proxy for firm-level unionization rates and this

may decrease the power of tests that use these rates.4

After using industry unionization rates to study the association between union bargaining power and

cash holdings, we conduct additional tests in which we refine our empirical measure of union bargaining

power. For this purpose, we supplement the use of industry unionization rates as a measure of union

bargaining power with the use of additional firm-level variables that affect this power. In particular, we

interact industry unionization rates with two sets of variables. The first set of variables proxies for the

importance that firms attach to obtaining a bargaining advantage over unions. The second set of variables

is designed to measure the extent to which having a small cash balance is likely to provide firms with a

bargaining advantage vis-à-vis unions.

Finally, for a small sample of observations we obtain firm-level estimates of unionization collected

from survey data and examine whether for this sample we find a similar association between unionization

and cash holdings as we do in our large-scale tests that use industry unionization rates. To further study

the effect of union bargaining power on corporate cash holdings, we also present evidence from two short

case studies in which we compare unionized firms with non-unionized firms within the same industry and

study a firm around the time when it first became unionized.5

3. Data

3.1. Sample

We study the population of Compustat firms that operate in the manufacturing sector (six-digit

North American Industry Classification System (NAICS) codes between 311111 and 339999) over the

1983-2005 period. Specifically, we have a sample of 34,042 firm-years during this period for which data on

industry unionization rates are available and there is no missing data for the main variables used in our

4 The evidence in Bronars and Deere (1991) and Matsa (2006) suggests using firm- or industry-level data in tests that examine how unionization affects firm-level corporate policy choices yields similar qualitative results. 5 We note that another approach to identify firms that bargain with a powerful union is to focus on one industry in which workers are represented by a powerful multi-employer bargaining group. For instance, DeAngelo and DeAngelo (1991) focus their analyses on U.S. steel firms in the 1980s that were represented by the United Steelworkers of America.

11

analyses. We focus on manufacturing firms because many of our tests require data on industry

concentration or industry cost structures which we obtain from the Census of Manufactures and Annual Survey

of Manufactures publications.

3.2. Industry unionization data

We obtain data on annual industry unionization rates for the 1983-2005 period from the Union

Membership and Coverage Database maintained by Barry Hirsch and David Macpherson, which is publicly

available at www.unionstats.com.6 This database reports industry unionization rates for 3-digit Census

Industry Classification (CIC) industries. These rates represent the percentage of total workers in a CIC

industry that are covered by unions in collecting bargaining agreements. Our unionization data span 77 3-

digit CIC industries in the manufacturing sector with CIC codes between 100 and 392. We are able to

determine which 4-digit SIC codes correspond to 3-digit CIC codes and hence are able to assign industry

unionization rates to our sample firms.

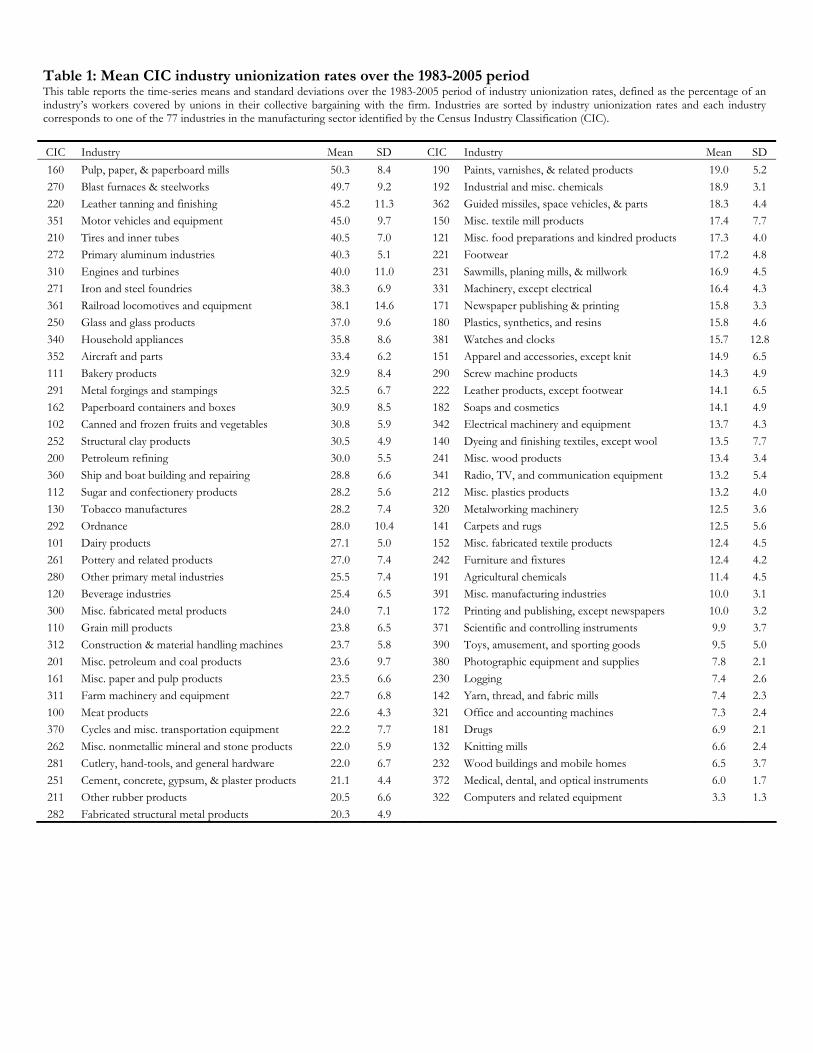

Table 1 provides a list of the 77 3-digit CIC manufacturing industries we study and the corresponding

means and standard deviations of the unionization rates within an industry over the 1983-2005 period.

The industries are sorted by unionization rates. The table shows that there is a large cross-sectional

variation in the unionization rates across industries. Pulp, paper, and paperboard mills, blast furnaces and

steelworks, leather tanning, motor vehicles, tires, primary aluminum, and engines and turbines are the

most unionized industries, with mean unionization rates above 40%. On the other hand, drugs, knitting

mills, wood buildings and mobile homes, medical, dental, and optical instruments, and computer and

related equipment are among the least unionized industries with mean unionization rates below 7%. The

standard deviations reported in the table show that there is also some time-series variation in unionization

rates. The times-series variation is similar across industries, as evidenced by the small differences across

industries in the standard deviation relative to the mean. To inspect the sources of the variation in industry

unionization rates more carefully, we run a regression of unionization rates on 3-digit CIC dummies and

6 See Hirsch and Macpherson (2003) for details on the construction of this unique and comprehensive dataset.

12

obtain an r-squared of 84 percent. This suggests that approximately 84 percent of the total variation in

industry unionization rates is cross-sectional variation while only 16 percent is time-series variation. Since

the cross-sectional variation is the primary source of independent variation in unionization rates, most of

our empirical tests rely on this variation to identify our coefficient estimates.

3.3. Estimate of the fraction of an industry’s blue-collar workers that are unionized

From the division of Occupational Employment Statistics of the Bureau of Labor Statistics (BLS), we

obtained data for 3-digit SIC manufacturing industries (we converted NAICS codes to SIC codes after

2001) on the number of workers employed in approximately 800 different occupations. For each industry,

we examined the title of each occupation and following the definition used by the BLS we classified all

non-office occupations as blue-collar occupations. With the data available we are able to determine the

number of blue collar workers in each industry for 1989, 1992, 1995, and for each of the years 1997-2001.

We assume that the 1989, 1992, 1995, and 2001 estimates are valid for the 1983-1990, 1991-1993, 1994-

1996, and 2001-2005 periods, respectively. To estimate the number of unionized workers in a firm’s

industry, we multiply the number of workers in the firm’s 3-digit SIC industry by the fraction of the

workers in the firm’s 3-digit CIC industry that are unionized. Next, we estimate the fraction of the blue-

collar workers in a firm’s industry that are unionized by dividing the number of unionized workers by the

total number of blue-collar workers in the firm’s 3-digit SIC industry. This measure is admittedly coarse

given that 3-digit CIC and SIC industries are only roughly comparable, that it assumes than only blue-

collar workers belong to a union, and that due to data unavailability we are forced to fill in gaps in the data

for a number of years.

3.4. Firm-level unionization estimates

We obtained from Barry Hirsch firm-level unionization estimates constructed from survey data for a

small sample of observations for 1972, 1977, and 1987. The 1977 data and 1987 data were derived from

his 1987 survey of manufacturing firms and the 1972 data was collected in an independent 1972

Conference Board Survey. We refer the reader to Hirsch (1991) for details on this dataset.

13

3.5. Contract expirations

We obtain data on labor contract expiration dates from the BNA Labor Plus database maintained by

the Bureau of National Affairs. These data are compiled from 1993 onwards and are based on notices that

parties to a collective bargaining agreement, when up for renewal, are required to file with the Federal

Mediation & Conciliation Service.

3.6. Strike data

We also obtain data on strikes from the BNA Labor Plus database. This database has information on

strike beginning and ending dates as well as on the parties involved in strikes from 1990 onwards. The data

draws on published accounts in BNA publications, newspapers, government reports, and union

publications.

3.7. Industry concentration measures

We collect the Herfindahl-Hirschman Index of industry concentration from Census of Manufactures

publications, which were published as part of the 1982, 1987, 1992, 1997 and 2002 U.S. Censuses. We

note that the Census of Manufactures begins classifying industries with 6-digit NAICS codes in 1997. Prior to

this year industries were classified using 4-digit SIC codes. We assume that the 1982, 1987, 1992, 1997, and

2002 Herfindahl-Hirschman Index values are valid for the 1983-1984, 1985-1989, 1990-1994, 1995-1999,

and 2000-2005 periods. We use the Herfindahl-Hirschman Index values to create an indicator variable for

whether a firm has a high industry Herfindahl-Hirschman Index value, as defined by whether the index

value is greater than the sample median. Given that the Herfindahl-Hirschman index values for 6-digit

NAICS and 4-digit SIC industries are not comparable we create this indicator variable separately for the

1983-1994 and 1995-2005 sample periods.

14

3.8. Industry-level import penetration data

Following the international trade literature (e.g., Trefler (1996) and Bernard, Jensen, and Schott

(2006)), we construct an industry-level import penetration variable that is defined as the value of imports

divided by domestic absorption (value of shipments minus value of exports plus value of imports). This

variable is calculated at the 3-digit NAICS industry level for manufacturing industries over the 1983-2005

period. Data on the value of shipments for 3-digit NAICS manufacturing industries are obtained from the

U.S. Census Bureau. Data on imports and exports comes from two different sources. For the period 1983-

1991 we use data on the value of imports and exports which are available online from the Center for

International Data at the University of California, Davis, and described in Feenstra (1996). For the period

1992-2005 we use data on imports and exports available online from TradeStats Express, which is

maintained by the International Trade Administration of the U.S. Department of Commerce.

3.9. Industry-level data on total materials costs and labor costs

Information necessary to calculate the ratio of materials costs to labor costs in a firm’s industry is

gathered from the 1997 and 2001 Annual Survey of Manufactures publications which are published by the

U.S. Census. From these publications we collect data for 6-digit NAICS industries on total industry

materials costs and total payroll expenses. Like the Census of Manufactures publications, the Annual Survey of

Manufactures publications begin classifying industries with 6-digit NAICS codes in 1997. We assume that

the 1997 data on industry cost structures are valid for the 1995-1999 period and that those for 2001 are

valid for the 2000-2005 period.

3.10. Right-to-work legislation data

We obtain information regarding whether the state in which a firm has the majority of its operations

has right-to-work laws from the U.S. Department of Labor’s web page on state right-to-work laws. We

collect this information on an annual basis over our sample period. Right-to-work laws are statutes

currently enforced in twenty-two states, allowed under provisions of the Taft-Hartley Act, which prohibit

unions from making membership or payment of union dues or fees a condition of employment, either

15

before or after an employee is hired. To determine in which state a firm has the majority of its operations,

we use the Compustat variable ‘STATE’, which Compustat defines as the state in which the firm has most

of its operations. To decide on the state in which a firm has most of its operations, Compustat uses the

address that appears on firms’ annual reports, which can be different from the state of incorporation.

While most firms’ principal addresses may typically be in the state in which they have most of their

operations, the ‘STATE’ variable is clearly measured with noise. The noise in the data resulting from this

coding error may reduce the power of our tests based on the right-to-work law variable.

4. Empirical analysis

4.1. The relation between unionization and cash holdings

To test our hypothesis that firms facing stronger labor unions strategically choose a policy of holding

less cash, we first examine in univariate and multivariate analyses whether firms in more unionized

industries hold smaller cash reserves than do firms in less unionized industries.

4.1.1. Univariate findings

Table 2 reports summary statistics and results of univariate tests of the relation between industry

unionization and cash holdings. Cash holdings are defined as cash and short-term investments/book

assets. Panel A shows that over our sample period mean and median cash holdings are 0.205 and 0.106,

respectively. Panel B examines the univariate relation between industry unionization rates and cash

holdings. For this purpose, in each year we sort firms into quartiles according to their industry

unionization rates and report the mean and median for cash holdings in each quartile. Both the mean and

median values of cash holdings systematically decrease in each quartile from the first to the fourth

unionization quartiles. The differences in cash holdings between the bottom and top quartiles are striking

and economically significant. Mean and median cash holdings/book assets for firms with an industry

unionization rate in the first quartile are 0.314 and 0.235, respectively. In contrast, these statistics for the

fourth quartile are 0.082 and 0.035, respectively. Thus, the univariate results support the proposition that

firms in more unionized industries strategically maintain small cash reserves to gain bargaining advantages

16

over unions. However, since differences in industry unionization rates are likely to be associated with

differences in firm characteristics we next turn to our multivariate tests.

4.1.2. Multivariate evidence on the relation between industry unionization and cash holdings

Given the problems of heteroskedasticity and serial correlation, we adjust the standard errors in our

reported results. Specifically, in all the firm-level pooled cross-sectional tests the standard errors are

clustered at the firm-level. In regression models that use the Fama-MacBeth approach and in models that

use only industry-level variables we correct for serial-correlation with a lag of one. In models that use

time-series averages of firm-level variables we use White (1980) standard errors.

Table 3 provides the results of regressions of firms’ cash holdings on industry unionization rates and

control variables. Cash holdings are measured as the natural logarithm of cash and short-term investments

deflated by book assets less cash and short-term investments, as in Opler, Pinkowitz, Stulz, and

Williamson (1999). The main independent variable of interest is the unionization rate in a firm’s 3-digit

CIC industry. We control for other potential determinants of a firm’s cash holdings suggested by Opler,

Pinkowitz, Stulz, and Williamson (1999). Also, as in their paper, all right-hand-side variables that are

deflated by book assets are deflated by book assets net of cash so that the effect of cash is removed from

these variables.

To decrease the likelihood that an omitted variable that may impact both cash and unionization could

drive our results, we also control for four additional variables. Haushalter, Klasa, and Maxwell (2007) show

that firms in more concentrated industries hold greater cash reserves. The extant literature also shows that

unions in more concentrated industries are likely to have more bargaining power (e.g., Salinger (1984) and

Karier (1985)). Consequently, we control for industry concentration by including a dummy variable equal

to one if the firm’s industry Herfindahl-Hirschman index is greater than the median value for the entire

sample, and zero otherwise. Second, because unionization tends to be related with firms’ capital intensity

levels and the tangibility of a firm’s assets is a determinant of its cash holdings, we control for net

property, plant, and equipment/book assets. Third, global competition increases the need for firms to

17

carry cash for preventive purposes and also reduces union bargaining power. Thus, we include a firm’s

industry import penetration ratio as an additional control variable. Finally, Bates, Kahle, and Stulz (2007)

show that firms that have undergone an initial public offering during the last five years hold markedly

more cash than do other firms. Because industries with more firms that have recently gone public tend to

be younger industries in which unions may not have formed yet, this could result in industries that have

experienced significant recent IPO activity having both low industry unionization rates and a larger

number of firms with high cash holding levels. Consequently, we include in our regressions a dummy

variable for whether a firm had its IPO during the prior five years.

The first model in Table 3 is a pooled regression, which includes year dummies to control for time-

specific factors. The second model is a Fama-MacBeth regression. The third model uses firm-specific

time-series means for each variable. The results from all three models show that there is a negative

relation between cash holdings and industry unionization rates. This relation is not only statistically

significant, but also economically significant. We multiply the standard deviation of the industry

unionization rate variable by the coefficient on this variable from the first model. Next, taking the anti-log

of the resulting value we find that a one-standard deviation increase in unionization leads to a 32.3%

decrease in a firm’s cash holdings. For comparison we calculate the impact on cash holdings of one-

standard deviation increases in operating income/book assets and total leverage as well as the impact of

having a bond rating that is investment grade. We find that these changes in firm characteristics would

lead to decreases in cash holdings of 43.6%, 17.2%, and 42.9%, respectively. Thus, the economic impact

of unionization on cash holdings seems comparable to that of several well known determinants of these

holdings. The majority of the coefficients on the control variables are statistically significant with the

expected signs, suggesting that the effect of industry unionization rates on cash holdings is not driven by

its correlation with other firm characteristics. For instance, this relation is not due to industry unionization

rates being correlated with firm leverage, investment opportunities, capital intensity, or import penetration.

Overall, the results for the first three models in Table 3 support the prediction that firms in more

unionized industries hold smaller cash reserves to improve their bargaining position with unions.

18

In the fourth model in Table 3 we run an industry-level regression of cash holdings on unionization

that gives each industry an equal weight in our analysis. For this regression, each year we convert all firm-

level variables into 3-digit CIC industry means. Year dummies are included in this regression model. This

specification allows us to address two issues, namely that industries with a greater number of firms receive

a larger weight in the first three models of Table 3 and that industry unionization rates may be a noisy

proxy for firm-level unionization. The results for this model continue to show a negative and statistically

significant relation between cash holdings and industry unionization rates.7,8

Finally, in the fifth model in Table 3 we examine whether the negative association between industry

unionization rates and cash holdings is robust to measuring a firm’s industry unionization rate as the

fraction of its industry blue-collar work force that is unionized. We investigate this issue because

unionized workers are largely blue-collar workers, and thus in some industries a lower industry

unionization rate may be due to a lower fraction of blue collar workers and not necessarily due to less

union bargaining power. As noted in Section 3.3 our measure for the fraction of the blue-collar workers in

an industry that are unionized is coarse. Nevertheless, the results for the fifth model in Table 3 show that

there is a statistically significant negative relation between firms’ cash holdings and our estimate of the

fraction of the blue-collar work force in a firm’s industry that is unionized.

A potential concern with the Table 3 results is that because unionization is measured at the industry

level it is possible that unobserved factors that are correlated with both industry unionization rates and

firm-level cash holdings could drive the negative association between these rates and firm-level cash

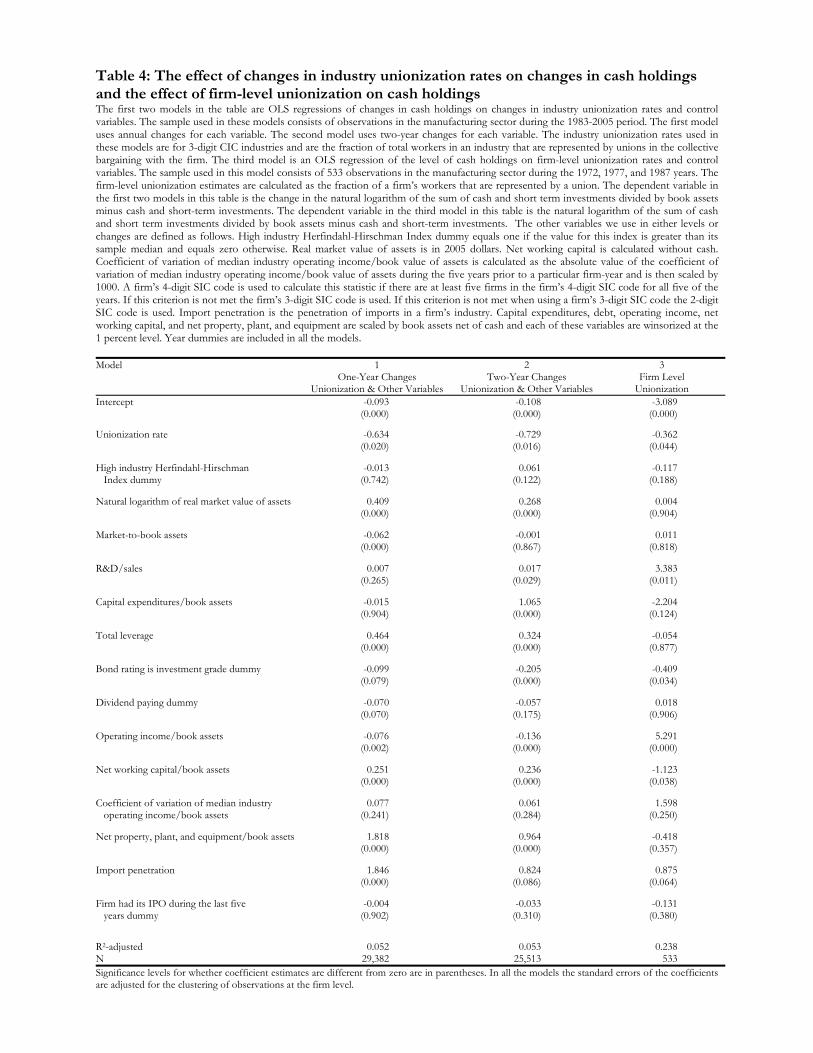

holdings. As noted previously, the time-series variation of industry unionization rates is limited. However,

in the first two models in Table 4 we attempt to exploit this variation be using differenced models. In the

first model all variables are converted into one-year changes. In the second model they are converted into

7 To further ensure that the negative association between cash holdings and industry unionization rates is not driven by differences in the number of firms across different industries, we also tried controlling in the first model in Table 3 for the number of firms per year in a firm’s 3-digit CIC industry. This does not affect our results. 8 Since the equal-weighted analysis ignores the relative importance of each industry in the manufacturing sector, we reran the industry-level model using weighted-least squares and weighting each industry-year observation by the inflation-adjusted assets of the industry. The negative association between cash holdings and industry unionization rates is also robust to using this specification.

19

two-year changes. The results for both models show that there is a negative association between changes

in industry unionization rates and changes in cash holdings. Thus, even after removing the effect of

potential unobserved factors correlated with industry unionization rates and cash holdings, we still find a

negative association between firm-level cash holdings and industry unionization rates. This is further

evidence that firms facing more powerful unions adopt a policy of holding smaller cash reserves.

In the third model of Table 4 we re-estimate our benchmark model using firm-level estimates of

unionization rates based on survey data. In these tests we restrict attention to the manufacturing sector

during the years 1972, 1977, and 1987 and to the small number of firms and industries for which this

survey data was compiled. We further impose the availability of data to construct the required control

variables.9 After imposing these data restrictions we are left with 533 observations. Consistent with the

results obtained using industry-level unionization rates, we find a negative association between

unionization and cash holdings. Further, this result is economically significant. We determine that a one-

standard deviation increase in unionization at the firm-level leads to a 10.1% decrease in a firm’s cash

holdings. Also, as in Table 2 in each year we divide the sample used for the tests with firm-level

unionization data into quartiles based on firm-level unionization and compare the mean and median values

for cash holdings between the different quartiles. We find that, as one moves from the lowest to the

highest unionization quartiles, each subsequent quartile has a lower mean and median value for cash

holdings. Overall, these results suggest that the industry-level unionization rates we use in our large-sample

analyses are a reasonable proxy for union bargaining power at the firm level and reduce the concern that

omitted variables correlated with industry unionization rates could spuriously drive our results.

Finally, we note that when interpreting the Table 3 and 4 results, it is important to consider the

possibility that the relation between cash holdings and industry unionization rates could run from cash

9 Information for the Herfindahl-Hirschmann index from the Census of Manufactures first became available in 1982. In our analysis using the firm level unionization estimates the High industry Herfindahl-Hirschmann Index dummy is created using data from the 1987 U.S. Census for 1987 and from the 1982 U.S. Census for 1972 and 1977. Also, because with the available data it is difficult to reliably calculate import penetration ratios for NAICS industries during the 1970s, import penetration ratios are calculated for 4-digit SIC industries.

20

holdings to these rates. However, we note that if this were the case one would expect that unions would

be more likely to form when cash holdings are larger and there are greater potential rents for unions to

capture. This would lead to a positive relation between cash holdings and industry unionization rates.

Given that we document a negative relation between cash holdings and industry unionization rates, it

seems unlikely that reverse causality could explain our results.

4.2. The determinants of the relation between industry unionization rates and cash holdings

4.2.1. The importance of gaining a bargaining advantage

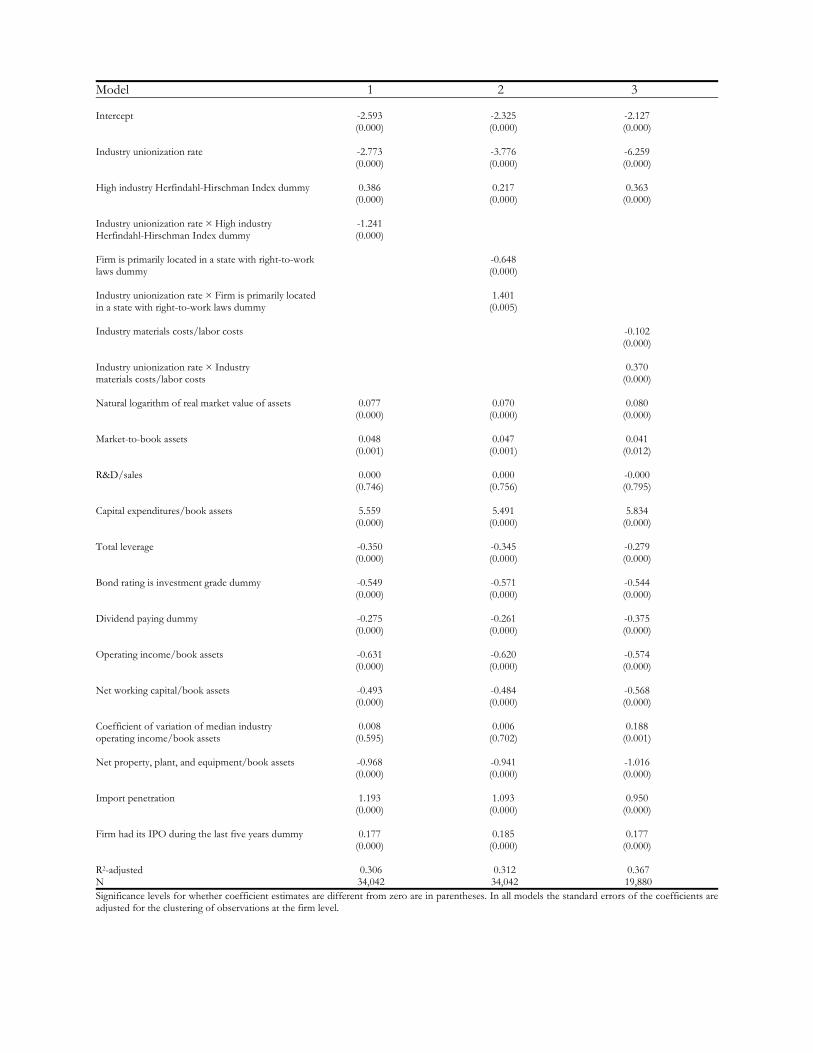

We now study how the negative relation between cash holdings and industry unionization rates

depends on the importance that firms are likely to attach to gaining a bargaining advantage over unions. If

this relation is driven by firms in more unionized industries strategically maintaining low cash balances to

improve their bargaining position, then this relation should be more pronounced when a strong bargaining

position against unions is more valuable to firms. We examine this issue in Table 5 using an empirical

model identical to that in column 1 of Table 3, but augmented to include an additional explanatory

variable and its interaction with a firm’s industry unionization rate. We consider three different factors that

affect the importance firms are likely to place on gaining a bargaining advantage relative to labor unions.

We first examine how industry concentration modifies the relation between cash holdings and

industry unionization rates. Economic theory predicts that the higher persistence of economic profits in

more concentrated industries lead to higher wage demands from workers. Furthermore, prior work shows

that unions indeed demand and capture a larger fraction of the available economic rents in more

concentrated industries (e.g., Salinger (1984) and Karier (1985)). As a result, firms in more concentrated

industries are more likely to place a higher value on having a strong bargaining position against unions

than would firms in less concentrated industries. The results for the first model in Table 5 show a

statistically significant and negative coefficient on the variable that interacts a firm’s industry unionization

rate with a dummy variable for whether the firm operates in a more concentrated industry (the Herfindahl-

Hirschman Index in the firm’s industry is above the value corresponding to the sample median). Thus, the

21

negative relation between cash holdings and industry unionization rates is more pronounced for firms in

more concentrated industries that are likely to attach a high value to improving their bargaining position

against unions.

Next, we investigate how the existence of right-to-work laws in the state in which a firm has most of

its operations affects the relation between cash holdings and industry unionization rates. Right-to-work

laws, which prohibit unions from making membership or payment of dues a condition of employment,

reduce unions’ bargaining power due to the resulting free-rider problem among union members (e.g.,

Ellwood and Fine (1987) and Holmes (1998)). The results for the second model in Table 5 show that there

is a significant positive coefficient on an interaction variable of a firm’ industry unionization rate with a

dummy variable for whether the state in which a firm has most of its operations has right-to-work laws.

This is consistent with the idea that when unions already have limited bargaining power due to the

existence of right-to-work laws, firms are less likely to attempt to improve their bargaining position with

unions by holding a small cash balance.10

It is also likely that gaining a bargaining advantage over unions to minimize labor costs is more

important for firms in industries in which labor costs represent a larger fraction of total costs. We

investigate this issue over the 1995-2005 period. To do so, we use data from 1997 and 2001 Annual Survey

of Manufactures publications to calculate the ratio of total materials costs to total payroll costs in a firm’s 6-

digit NAICS industry. In the third model in Table 5 we interact this ratio with a firm’s industry

unionization rate. The coefficient on this interaction variable is statistically significant and positive,

suggesting that when labor costs are a larger fraction of firms’ total costs the negative effect of

unionization on cash holdings is stronger.

10 As previously noted, since Compustat’s record of the state in which a firm is principally located may be sometimes inaccurate, the dummy variable for whether a firm is principally located in a state with right-to-work laws could be measured with error. This measurement error is likely to be larger for more diversified firms that have business segments located in different states. However, our evidence based on the right-to-work laws dummy variable is robust to excluding from the analysis firms in the highest diversification decile, quintile, quartile, or tercile, where diversification is measured inversely using the Hefindahl index of a firm’s sales across its different business segments.

22

To summarize, the Table 5 results show that the negative association between cash holdings and

industry unionization rates is more pronounced for firms in more concentrated industries, firms

principally located in states with no right-to-work legislation, and firms for which labor costs represent a

larger fraction of total costs. These results provide strong support to the proposition that the negative

relation between cash holdings and industry unionization rates is the result of attempts by firms facing

strong unions to gain bargaining advantages over their unionized workers.

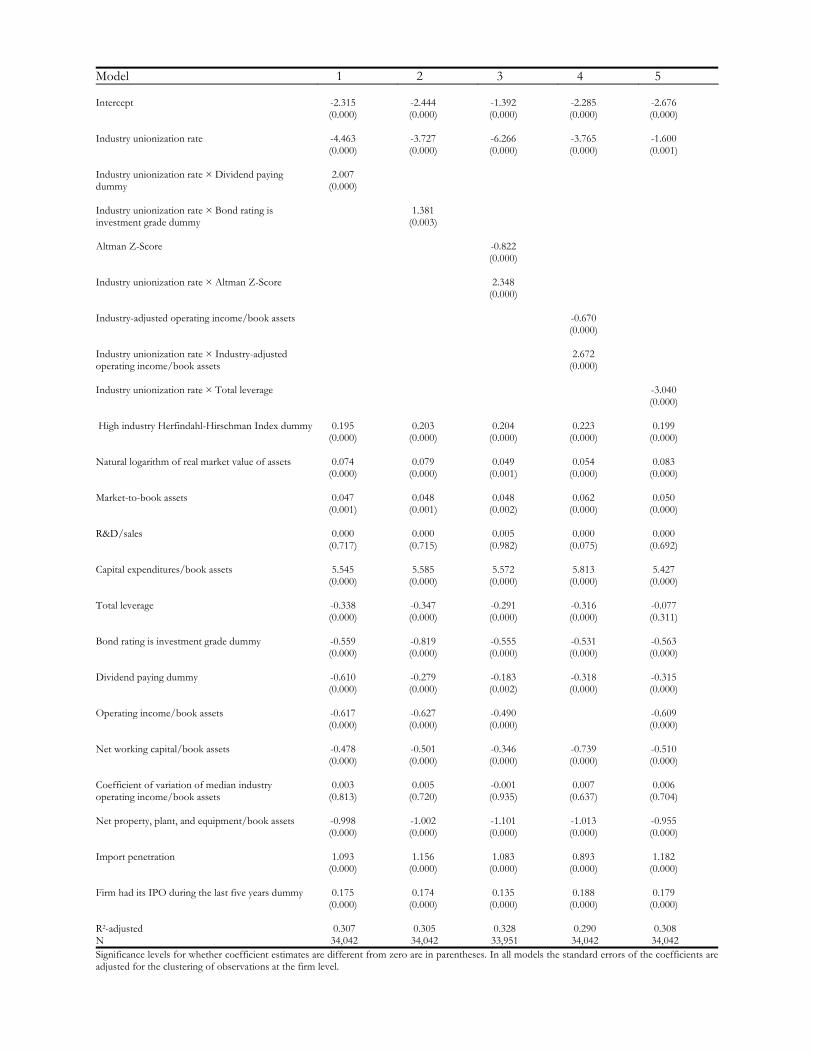

4.2.2. The bargaining advantage provided by a small cash balance

We also examine how variables that impact the bargaining advantage provided by a small cash balance

affect the negative relation between unionization and cash holdings. This allows us to further determine if

the negative relation between cash holdings and industry unionization rates is the result of collective

bargaining issues. We anticipate that if this relation arises because firms choose the level of their cash

reserves taking into account their effect on the bargaining with unions, then this relation should be weaker

in situations where lower cash reserves are less credible evidence that firms cannot concede to unions’

demands. Table 6 explores this issue using five models that are similar to the Table 5 models except that

different interaction variables are used.

DeAngelo and DeAngelo (1991) show that dividend cuts enable firms to obtain concessions from

unions by signaling that shareholders themselves are forced to make sacrifices to alleviate the firm’s

financial difficulties. We expect that because a dividend-paying firm disburses free cash flows to

shareholders, it can make a less credible case that a low cash balance indicates that it is unable to comply

with union demands. Consistent with this view, the first model in Table 6 shows a statistically significant

positive coefficient on the interaction between a firm’s industry unionization rate and a dummy variable

for whether the firm pays dividends. Thus, the negative relation between unionization rates and cash

holdings is weaker for dividend-paying firms.

Also, a small cash balance should provide less of a bargaining advantage for firms that can easily raise

external capital to alleviate cash shortfalls, such as those with high bond ratings. To examine whether

23

easier access to external capital diminishes the bargaining advantage provided by having a small cash

balance, in the second model in Table 6 we interact a firm’s industry unionization rate with a dummy

variable for whether the firm has an investment grade bond rating. We find a positive and statistically

significant coefficient on this interaction term, suggesting that firms with higher bond ratings rely less on

small cash balances to gain bargaining advantages over unions.

It is also likely that for firms that are closer to financial distress low cash reserves provide more

credible evidence that the firm is unable to comply with union demands. To examine this issue we first

interact a firm’s industry unionization rate with the firm’s Altman-Z score. A higher value for this measure

indicates that a firm faces less bankruptcy risk. The results for the third model in Table 6 show that the

coefficient on the interaction of a firm’s industry unionization rate with its Altman-Z score is significantly

positive. This suggests that a small cash balance provides more of a bargaining advantage for firms that are

closer to financial distress.

In the fourth model in Table 6 we proxy for whether a firm is likely to be financially distressed by

examining the firm’s industry-adjusted profitability, defined as operating income/book assets for the firm

minus the median value for this ratio in the firm’s 3-digit CIC industry. We find a significant positive

coefficient on the interaction of a firm’s industry-adjusted profitability with its industry unionization rate.

Given that firms with higher industry-adjusted profitability are less likely to be financially distressed this

finding indicates that the bargaining advantage provided by a small cash balance is lower for firms that are

further away from financial distress.

Finally, in the fifth model in Table 6 we use a firm’s leverage ratio as the proxy for whether the firm is

likely to be financially distressed. The coefficient on the interaction of a firm’s industry unionization rate

with it leverage ratio is significantly negative. This further indicates that firms that are more likely to be

financially distressed gain more of a bargaining advantage over unions by holding low cash reserves. This

result also suggests that low cash holdings and high debt levels are complementary mechanisms that allow

firms to gain bargaining advantages over unions. That is, it may be possible for firms to gain important

bargaining advantages over unions if they both reduce their cash holdings which provide a buffer against

24

future negative cash flow shocks and also issue debt to limit the firm’s future excess cash flow. To

determine the economic importance of debt on the relationship between unionization and cash holdings,

we examine how a one-standard deviation increase in debt impacts the effect of changes in unionization

on cash holdings. We find that as a result of such an increase in debt, a one-standard deviation increase in

unionization would lead to a 12.8% greater decrease in a firm’s cash holdings.

Overall, the Table 6 results show that the negative relation between unionization rates and cash

holdings is less (more) pronounced in situations where lower cash holdings are less (more) credible

evidence that the firm cannot concede to union demands. This additional evidence reinforces the idea that

the negative relation between cash holdings and industry unionization rates is driven by firms’ strategic

decisions in the context of their bargaining with unions.

4.2.3. Do unionized firms manage their cash holdings downward prior to negotiations?

Since DeAngelo and DeAngelo (1991) find that firms manage their earnings downward prior to labor

negotiations, we investigated whether unionized firms attempt to obtain bargaining advantages by

lowering their cash holdings prior to labor negotiations. For this purpose, we examined changes in firms’

cash holdings in the years surrounding collective bargaining negotiations that involved at least 1000

workers and were not preceded by other major negotiations during the previous two years.

Though not tabulated, for a sample of 96 contract-expiration events in the manufacturing sector from

1993-2005, we find that median annual changes in cash holdings/book assets are not significantly different

from zero in either of the two years preceding labor contract expirations. Since this result could be

contaminated by contemporaneous industry factors, we also examined median changes in industry-

adjusted cash holdings, where industry-adjusted cash holdings are defined as a firm’s cash holdings minus

the median cash holdings of firms in the same four-digit SIC industry. We find that in the year prior to

labor contract expirations unionized firms decrease their industry-adjusted cash holdings by about four-

25

tenths of a cent per dollar of assets.11,12 Although consistent with our principal hypothesis that unionized

firms manage their cash holdings downward to gain bargaining advantages over labor, this result is only

statistically significant at the 10 percent level. Taken together with the other results reported in Sections

4.1 and 4.2, this evidence suggests unionized firms obtain bargaining advantages over labor primarily by

holding smaller cash reserves at all times, rather than by managing cash levels downward prior to

negotiations.

4.3. Evidence from strikes

We also examine if increases in cash holdings lead to a greater likelihood that a union decides to

strike. If higher cash holdings convey to unions that a firm is more able to raise workers’ salaries and this

reduces the firm’s bargaining power, then we expect that increases in cash reserves will raise the

probability of a strike. To construct our strike sample, we start with the data from the BNA Labor Plus

database and require: (i) Firms to be manufacturing firms included in the Compustat database; (ii) Strikes

that involve at least 1000 workers; (iii) That we can calculate annual changes in cash holdings for years -2

to 0 relative to the fiscal year when a strike takes place. Our final sample of strikes has 59 observations

over the 1990-2006 period.

Panel A in Table 7 reports median annual changes in cash holdings, defined as cash and short-term

investments/book assets for years -2 to 0 relative to the fiscal year when a firm experiences a strike. Also,

this panel provides evidence on median changes in industry-adjusted cash holdings, where industry-

adjusted cash holdings are defined as a firm’s cash holdings minus the median value of cash holdings for

the other firms in the same 4-digit SIC code industry that do not contemporaneously experience a strike.

11 If firms manage their cash holdings downward prior to labor negotiations then it is possible that in the fiscal year subsequent to the year when a labor contract expires cash holdings significantly increase. We examined this issue but did not find that raw or industry-adjusted cash holdings significantly increase during this year. 12 The evidence in Bronars and Deere (1991) suggests that firms can use higher debt to improve their bargaining position against unions. We thus examined whether firms increase their raw or industry-adjusted debt levels prior to labor negotiations. However, we did not find any evidence that this is the case. This suggests that although firms can use both permanently higher debt levels and lower cash balances to improve their bargaining position, the strategic use of cash is potentially different from that of debt in that firms can more easily manage cash holdings prior to a negotiation.

26

We find that during the fiscal year prior to the year when a firm’s union goes on strike raw cash

holdings significantly increase by approximately three-tenths of a cent per dollar of assets. Also, during

this year cash holdings significantly increase relative to industry cash holdings by four-tenths of a cent per

dollar of assets. These results are consistent with increases in cash holdings resulting in a higher probability

that a union decides to strike, which suggests that increases in cash holdings weaken firms’ bargaining

positions relative to unions. We also document a small (one-tenth of a cent per dollar of assets), but

significant increase in raw cash holdings at the end of the fiscal year when a strike begins. However, it is

difficult to make inferences from this finding as a strike may lead to subsequent changes to a firm’s cash

holdings.13

Panel B in Table 7 reports evidence from two probit models that predict the likelihood that a firm

experiences a strike. In this analysis we match our sample firms that experience strikes with Compustat

firms that share the same primary 4-digit SIC code as a sample firm but do not experience a strike during

the same year. In the probit models the dependent variable takes a value of one if a firm experiences a

strike and takes a value of zero otherwise. The main independent variable of interest is the change in a

firm’s cash holdings during the previous fiscal year. We control for whether a firm is principally located in

a state with right-to-work laws, since if this is the case the union is likely to be weaker and less likely to go

on strike. We also control for other changes in the financial strength of the firm during the pre-strike year.

These variables come from Tables 3-6 and are total leverage, operating income/book assets, net-working

capital/book assets, whether a firm has a bond rating that is investment grade, whether a firm pays

dividends, and the firm’s Altman-Z score. Finally, we control for firm size, and for the changes during the

pre-strike year in market-to-book assets, and industry cash flow risk.

The results for the first model show that after controlling for other effects there is still a significant

positive association between the prior year change in cash holdings and the likelihood that a firm

subsequently experiences a strike. A number of the control variables are also significantly associated with

13 For instance, costs resulting from the strike might cause cash holding levels to decrease. Alternatively, as a precautionary measure a firm could take actions to try and increase its cash reserves subsequent to a work stoppage.

27

the likelihood of a strike. Notably, the prior year change in operating income/book assets is positively

associated with the likelihood of a strike. This is supportive of the DeAngelo and DeAngelo (1991)

evidence that increases (decreases) in a firm’s profitability may weaken (improve) a firm’s bargaining

position relative to a union. Moreover, we find that if a firm’s bond rating improves to investment grade

during the prior year this increases the likelihood of a strike. This evidence further suggests that firms that

appear to be financially stronger have weaker bargaining positions vis-à-vis unions. Finally, in the second

model we control for the level of market-to-book assets and cash flow risk rather than the changes in

these variables. This does not affect the results documented in the first model.14

4.4. The impact of unionization on the contribution of cash holdings to firm value

Our results thus far suggest that large cash reserves are costly for firms in more unionized industries

because they weaken the firm’s bargaining position and permit unionized workers to capture a larger

fraction of the firm’s profits. It follows that the contribution of cash holdings to firm value should be

smaller in more unionized industries than in less unionized industries. We estimate how a change in cash

holdings leads to a change in the market value of a firm using the approach developed by Faulkender and

Wang (2006). For this purpose, we use a sample of 26,073 firm-year observations during the 1983-2005

period for which we are able to construct the variables required for the analysis.

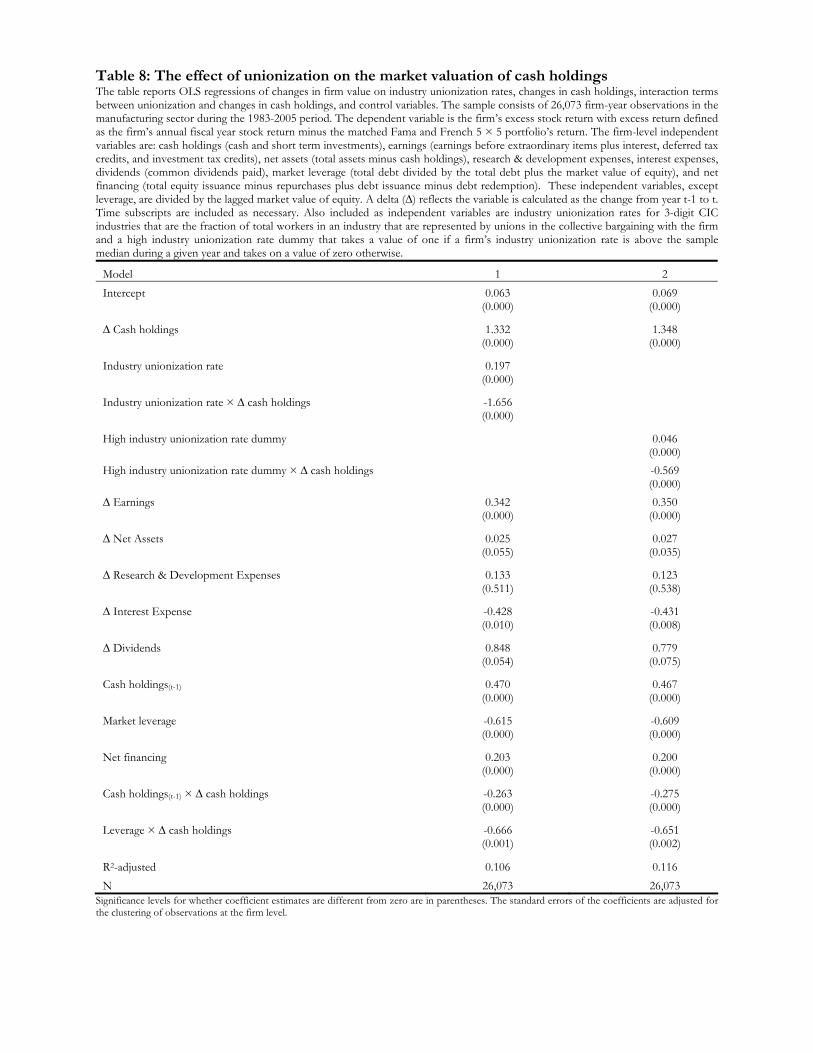

Table 8 provides the results of our analysis. Other than the unionization related variables the

dependent and independent variables are calculated exactly as in Faulkender and Wang (2006). The

dependent variable in both of the Table 8 models is a firm’s current fiscal year excess stock return, defined

as the firm’s annual stock return minus the firm’s matched Fama and French 5 × 5 portfolio return. The

independent variables in the first model in Table 8 are the change in current year cash holdings defined as

cash and short term investments, the firm’s industry unionization rate, the interaction of the firm’s

industry unionization rate with the change in current year cash holdings, the change in current year

14 It could also be expected that because higher cash holdings weakens firms’ bargaining positions with unions, higher cash holdings prior to a strike might lead to a longer strike. We examined this issue, but did not find that the change in cash holdings during the pre-strike year or the level of pre-strike year cash holdings are associated with the length of a strike.

28

earnings defined as earnings before extraordinary items plus interest, deferred tax credits, and investment

tax credits, the change in current year net assets defined as total book assets minus cash holdings, the

change in current year research and development expenses, the change in current year interest, the change

in current year common dividends paid, prior year cash holdings, current year market leverage, current

year net financing defined as total equity issuance minus repurchases plus debt issuance minus debt

redemption, the interaction of prior year cash holdings with the current year change in cash holdings, and

the interaction of current year market leverage with the current year change in cash holdings. Except for

market leverage and a firm’s industry unionization rate, all the independent variables are scaled by the

lagged market value of equity.

The results for the first model in Table 8 show that the coefficient on the change in current year cash

holdings is significant and positive, which indicates that the marginal value of an extra dollar of cash is

positive. Interestingly, we find that the coefficient on the interaction of a firm’s industry unionization rate

with the change in current year cash holdings is significantly negative. This indicates that the marginal

value of an extra dollar of cash is decreasing in a firm’s industry unionization rate and suggests that cash

holdings are less valuable in more unionized industries. Presumably, this occurs because in such industries

larger cash holdings make it more difficult for firms to gain concessions from unions. Consequently, in

these industries higher cash holdings lead to labor capturing a greater portion of firms’ profits and to a

reduction in shareholder value. The second model in Table 8, in which a firm’s industry unionization rate

is replaced with a dummy variable for whether in a given year the firm’s industry unionization rate is

greater than the sample median, provides further support for this proposition. We find a significant

negative coefficient on the interaction of the dummy variable for whether a firm has a high industry

unionization rate with the change in current year cash holdings.

We calculate the marginal value of a dollar of cash for the average firm in our sample using regression

coefficients from the first model of Table 8 and mean values of several independent variables. Specifically,

we use the coefficients on the interactions of prior year cash holdings with the change in current year cash

holdings, with current year market leverage, and with a firm’s industry unionization rate, as well as the

29

mean values of cash holdings as a percentage of market value of equity, market leverage, and industry

unionization of 16.9%, 22.6%, and 16.2%. We find that this marginal value is $0.87 (=1.332 + (-0.263 *

0.169) + (-0.666 * 0.226) + (-1.656 * 0.162)). This value is close to the marginal value of a dollar of cash

for the average firm in the Faulkender and Wang (2006) sample of $0.94.

Using a similar approach and focusing on the coefficients in the second model of Table 8, we

estimate the marginal value of a dollar of cash to be $1.15 for firm-years in which a firm’s industry

unionization rate is over the annual sample median and $0.59 for firm-years in which a firm’s industry

unionization rate is below the annual sample median. Thus, the negative effect of unionization on the

market value of a dollar of cash holdings is both statistically and economically significant.15

4.5. Robustness tests

We perform several robustness tests. First, a potential concern with our results is that they may be

affected by the increasing trend in cash holdings and decreasing trend in unionization rates during our

sample period.16 To alleviate this concern we run year-by-year cross-sectional regressions using the same

specification as in the first model in Table 3. We find a significant negative association between cash

holdings and industry unionization rates during each of the twenty-three years from 1983-2005. This

suggests that our results are not due to the aforementioned trends in unionization rates and cash holdings.

Moreover, it indicates that they are not driven by a particular subset of years or by industry-specific events,

such as major restructurings of particular industries.

Second, the negative relation between cash holdings and unionization could be driven by the

inclusion in our sample of firms from high-technology industries. This is because firms in such industries

simultaneously tend to have low unionization rates and to hold high cash balances as a result of their large

growth opportunity sets. To address this concern, we calculate mean values for R&D expenses/sales in