the state of food and agriculture, 1974 · in addition to the usual review of the recent world food...

TRANSCRIPT

AF 99

r ?

FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS

SPECIAL CHAPTERS

In addition to the usual review of the recent world food and agriculture situation, eachissue of this report from 1957 has included one or more special studies of problems oflonger term interest. Special chapters in earlier issues have covered the following subjects:

Factors influencing the trend of food consumptionPostwar changes in some institutional factors affecting agriculture

Food and agricultural developments in Africa south of the SaharaThe growth of forest industries and their impact on the world's forests

Agricultural incomes and levels of living in countries at different stagesof economic development

Some general problems of agricultural development in less developedcountries in the light of postwar experience

Programing for agricultural development

Land reform and institutional changeAgricultural exetension, education and research in Africa, Asia and LatinAmerica

The role of forest industries in the attack on economic underdevelopmentThe livestock industry in less developed countries

Basic factors affecting the growth of productivity in agricultureFertilizer use: spearhead of agricultural development

Protein nutrition: needs and prospectsSynthetics and their effects on international trade

Agriculture and industrializationRice in the world food economy

Incentives and disincentives for farmers in developing countriesThe management of fishery resou. rces

Raising agricultural productivity in developing countries through techno-logical improvementImproved storage and its contribution to world food supplies

Agricultural marketing improvement programmes: some lessons fromrecent experienceModernization of institutions to promote development

Agriculture at the threshold of the Second Development Decade

Water pollution and its effects on living aquatic resources and fisheries

Education and training for developmentAccelerating agricultural research in the developing countries

Agricultural employment in developing countries

STATE OF FOOD AND AGRICULTURE 1974

WORLD REVIEW

REVIEW BY REGIONS

POPULATION, FOOD SUPPLY AND AGRICULTURAL DEVELOPMENT

FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONSRome, 1975

The statistical material in this publication hasbeen prepared from the information availableto FAO up to 1 November 1974

The designations employed and the presentationof the material in this publication do not implythe expression of any opinion whatsoever on thepart of the Food and Agriculture Organizatiotzof the United Nations concerning the legalstatus of any country, territory, city or area,or of its authorities, or concerning the delimi-tation of its frontiers or boundaries.

© FAO 1975

Printed in Italy

Foreword VII FISHERIES 33

1. World review

Production 1973

Production 1974The influence of weather and climate on food

production

AGRICULTURAL TRADE

Trade in 1973

Trade outlook for 1974/75

STOCKS OF AGRICULTURAL PRODUCTS

CONSUMER FOOD PRICES 222. Review by regions 51

DEVELOPMENT ASSISTANCE 23 WESTERN EUROPE 51

The flow of aidTerms of assistanceRepayment burdenThe World Bank Group and the financing

of agricultureRegional development banks and new sources

of aidFood aid

AGRICULTURAL PRODUCTION REQUISITES . . . . 28

NORTH AMERICA

CONTENTS

Production and trade 33

Policies and other issues 35

Outlook 36

57

The energy crisis 28

Fertilizers 30 Agricultural prices and farm incomes 57

Pesticides 32 Problems, policies and programmes 58

27 Production and trade 38

11Forest policies 41

UNITED NATIONS CONFERENCES AND SPECIAL16 SESSION 43

16 World Food Conference 43

18 Sixth Special Session of the United NationsGeneral Assembly 46

World Population Conference 4720 Conference on the Law of the Sea 48

23 Agricultural policies and problems 51

24 Prices 1974/75 5325

25 EASTERN EUROPE AND THE U.S S R 54

25 Investment and current inputs 54

27 Farm incomes, prices and policies 55

Plans and policies 56

AGRICULTURAL PRODUCTION 2

FORESTRY 38

OCEANIA

Agricultural prices and farm incomesProblems, policies and programmes

LATIN AMERICA

Development plans and policiesIntegrated rural developmentRegional economic integration

FAR EAST

Development plans and policiesTechnological innovation and its policy im-

plicationsRegional economic cooperation

China 80

Japan 81

NEAR EAST 82

Development plans and policies 82Country perspective studies 84

Development plans and policiesRegional economic integration

3. Population, food supply and agriculturaldevelopment

65

POPULATION AND FOOD SUPPLY 93

Food production 93Production resources 96Rural institutions and services 98Development assistance 100

World trade in food 100

vi

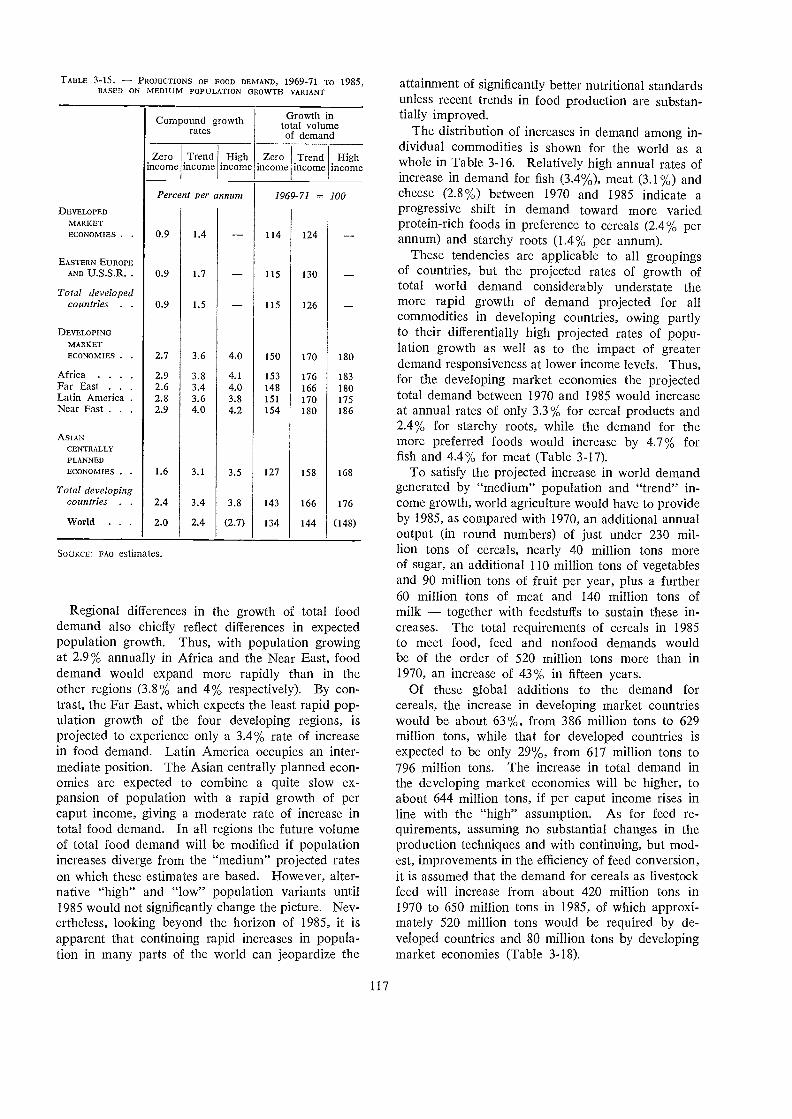

Food demand projections 116

Extrapolated food production trends 119

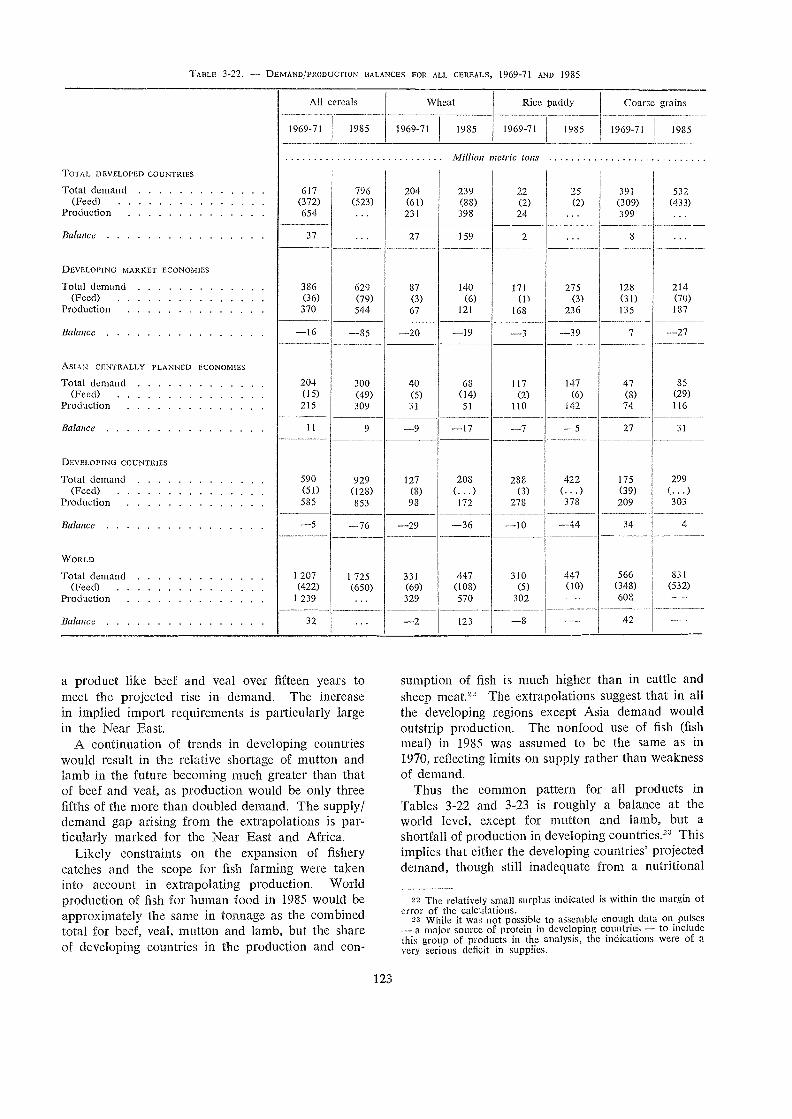

The demand/production balance 121

Supplementary needs to meet nutritionalstandards 124

Production fluctuations 125

Outlook for rural poverty 126

Methodological note 127

MAJOR POLICY IMPLICATIONS 136

ANNEX TO CHAPTER 3 139

AFRICA 88 POSSIBILITIES FOR INCREASING PRODUCTION ... 130

DIMENSIONS AND CAUSES OF HUNGER AND MAL- BIBLIOGRAPHY TO CHAPTER 3 154

NUTRITION 103

Assessment of undernutrition and malnutri-tion 103 Annex tables 155

63 Food availability 104

Distribution of food by income and social63 group 106

63 Other indicators of the incidence of food defi-ciency 107

The decline in breast-feeding 109

Other nutritional deficiencies 110

Causes of inadequate nutrition 110

65

69

72 THE DEMAND FOR FOOD I I 1

Patterns of food expenditure73 Food in family expenditure 111

Other factors influencing long-term food73 demand 114

7679 THE FOOD PROBLEM OF THE FUTURE 116

88 Agricultural inputs 130

90 Water and land resources 132

Livestock 132

Fisheries 134

Post-harvest losses 135

Incentives and services 13593 Mobilizing the rural population 136

FOREWORD

As I reminded the World Food Conference when I addressed it on 5 November, it is 110Walmost thirty years since John Boyd-Orr, the first Director-General of FAO, evoked the ideaof "a great world food scheme, which will bring freedom from want of food to all men."Yet the governments of the day were unable to rise to this challenge, so that now, a wholegeneration later, the world food problem ig still unsolved and is worsening, and there aremore people in want of food than at any time since then.

For the third consecutive year the world food and agricultural situation must be viewedwith grave concern. During 122uch of 1974 there were high hopes that this year would bringthe bountiful harvests so badly needed for the world to beghz to emerge from the food crisisthat started with the widespread bad weather and poor crops of 1972. Although there was asubstantial recovery in production in 1973, very large harvests were needed in 1974 if a begin-ning was to be made in returning to any reasonable degree of security in world food supplies.

It is llOW clear that these hopes were not realized in 1974. In many countries the expan-sion ill acreage and other special efforts ¡nade to increase production were defeated by theweather. Any easing of the world food situation has thus been put offfor at least another year.

Although bad weather was much less widespread in 1974 than in 1972, it affected produc-tion with particular severity in two vitally important regions of the world: North America,the largest food exporter, and the Far East, where the majority of the world's malnourishedpeople are to be found. The final outcome of the cereal crops in son2e parts of the Far Eastis still unknown, but it is already certain that in both of these regions there has been a dropin cereal production and in total food and agricultural production.

World cereal production thus declined in 1974 for the second time in three years. FAO'searly estimates indicate a fall of between 40 and 50 million tons. The gravity of this largedrop in production, superimposed on the already precarious situation, is readily apparentwhen it is recalled that an increase of more than 20 million tons of cereals is needed merelyto keep ul»vith the annual growth of population at present average consuinption levels. It is/IOW likely that the total carry-over stocks of cereals (outside China and the U.S.S.R., forwhich there is as yet no information) will full below 100 million tons by mid-1975. This wouldbe less than half their 1970 volume and only 11 % of world consumption, as compared withthe 17-18 % estimated by FAO to be the minimum required for world food security.

Any increase in total world food and agricultural production in 1974 is likely to have beenvery small. If 1974 production does turn out to have matched the 1973 kvel, this will mainlybe the result of the unusually large upsurge in livestock slaughterings, especially, in westernEurope, and will thus bring no relief to the countries where food shortages are most critical.What is more, the big increase in livestocic production reflects very serious difficulties in thissector and has benefited neither producers nor consumers.

Side by side with the continued general shortage of food, especially of staple cereals, thesituation is critical for several of the main inputs essential for food production. The sYliortageand high price of chemical fertilizers show no sign of abating .for some time to come. Someimportant pesticides are running short, and this niay soon become a serious problem. Anumber of developing countries face shortages of fuel and power for irrigation pumping andother essential agricultural purposes.

In the face of these dual shortages of food and the means of producing it, there is anobvious need for urgent, immediate action if widespread starvation is to be avoided.

First, it is necessary to ensure an equitable distribution of the exportable food suppliesthat are available until next year's harvests begin to come in, with special attention to needsof the most seriously affected countries, some of which cannot be fully known until later. To

this end, I have been engaged in special consultations with the main exporting and importingcountries.

vii

Second, in order to obtain the biggest possible harvests in 1975, it is necessary to securea balanced distribution of the scarce means of production as well. Here FAO's InternationalFertilizer Supply Scheme is of particular importance.

Third, in the case of both food and inputs, it is 770i sufficient to earmark supplies. Manydeveloping countries are very hard hit by the huge increases that have occurred in the pricesof the food, fertilizers, fuel and many other essential items they have to import, and they facevery serious balance-of-payments difficulties. Even if the necessary supplies can be set aside,these countries will ¡leed substantial financial assistance in order to pay for them. An impor-tant instrument in this regard is the United Nations Emergency Operation, with ivhich FAOis cooperating actively.

I have dwelt at some length on the immediate aspects of the food crisis and the measuresneeded to cleat with them. These are extremely serious and are the main subjects of the firsttwo chapters of this issue of The state of food and agriculture. However, the longer iel'117dimensions of the world food problem must not be neglected. Two or three years of goodweather and good harvests are 1701V 1170S1 urgently needed; but it would be tragic if, oncethey are achieved, the world should again lapse hito complacency about its longer term foodproblems.

When the World Food Conference met in Romefrom 5 to 16 November 1974, it was underthe shadow of a firther worsening in the immediate situation becctuse qf the disappointingperformance of food production during the year. However, the inain objective of the Con-ference was to tackle the longstanding, underlying ills in the world's food and agriculturalsector, and to agree on the necessary action to ensure that such short-term crises can 17eVeroccur again. It focused mainly on the medium-term period of the next ten years or so.

The main decisions of the World Food Conference are sunitnarized in Chapter 1 qf thiseport. The Conference achieved a very encouraging degree of consensus OH the nature and

dimensions of the world food problem and on the national and international action neededto overcome it. It called for the establishment of a munber of neiv bodies that could have adecisive role in mounting the necessary concerted action. It resolved that all governmentsshould "accept the goal that within a decade no child will go to bed hungry, that no familywill fear for its next day's bread, and that no human being's fieture and capacities will bestunted by malnutrition." Much will depend 017 how speedily the world's governments matchthese impressive goals with the action that they agree is necessary.

There is also a further time dimension to the 3vorld food problem. In looking inainlyat the next ten years or so, the World Food Conference was concerned with a period duringwhich the rate of population growth is virtually predetermined. Its task was therefore toconsider the measures needed to meet an already inevitable growth of population. Lookingfarther ahead, however, the rate of population growth is far from inevitable. According tothe United Nations population projections, the world's population in the year 2000 could heanywhere between 5 900 million and 7 200 nfillion. This huge difference of 1 300 millionwould greatly affect the magnitude ,of the friture challenge to the world's food and agriculturalsector. Provided that the action agreed to by the World Food Conference is begun in2-mediately, it should be possible to meet the expected increase in the demand for food up to 1985and for some years beyond that date; but the action that has to be taken will need to be plannedas a crash programme. It is therefore essential to take parallel action 770W to ensure thatiii the more distant future the rate of population growth and thus the increctse in the demandfor food are substantially reduced.

In these circumstances it is particularly appropriate that Chapter 3 of The state of foodand agriculture is this year devoted to a study of population, food supply and agriculturaldevelopment. This study was prepared with financial support from the United Nations Fundfor Population Activities. Its findings have afready formed the basis of part of FAO's docu-mentary contribution to the World Food Conference and to the preceding World PopulationConference, held from 19 to 30 August in Bucharest. The link between these two inzportantUnited Nations conferences is seljlevident. They in turn are linked with a series of importantmeetings, including the Conference 077 Human Environment, the Sixth Special Session of theUnited Nations General Assembly, and the forthcoming conferences on the role of 1VOMC17,human settlemenm, and water, all of which concern different aspects of the interlocking setof problems with which the world is now confronted. For, as FAO has always stressed, the

food problem is not a problem of agriculture alone, but part of the whole complex problemof economic and social developnient and improving the quality of life.

A niain feature of Chapter 3 of this report is FAO's new appraisal of the extent of hungerand malnutrition in the ivorld. It is 1701V estimated that the awesome number of at least460 million of our fellow human beings are suffering from severe malnutrition. What

viii

worse, this estimate is based on the peak level of per caput food supplies before the situationbegan lo deteriorate so seriously in 1972; since then, the number of severely malnourishedpeople must have greatly increased. .Hany die at an early age from a combination of mal-nutrition ancl other related causes without being recorded as deaths by starvation. There isrecent evidence in a number of developing countries of an ominous increase in death ¡'ates, towhich there is little doubt the worsening of the nutritional situation has contributed significantly.

The challenge to the world's governments and to the international community could not beclearer. I. was acknowledged by all at the World Food Conference. Time efforts to meet thechallenge will be watched anxiously in the coming months. There is no time to lose if theseefforts are not to be too late to save the situation.

A.H. BOERMADirector-General

ix

The following symbols are used in statistical tables:

none or negligible

not available1971/72 signifies a crop, marketing or fiscal year

running from one calendar year to the next; 1971-72signifies the average for two calendar years.

Figures in statistical tables may not add up be-cause of rounding. Percent changes from one yearto another have been calculated from unroundedfigures. Unless otherwise indicated, the metric sys-tem is used throughout.

Production index numbers '

The indices of agricultural production are calcu-lated by applying regional weights, based on 1961-65farm price relationships, to the production figures,which are adjusted to allow for quantities used forfeed and seed. The indices for food products excludetobacco, inedible oilseeds, animal and vegetable fibres,and rubber. They are on a calendar year basis andare therefore not comparable with the indices for cropyears published in the 1966 and prior issues of thisreport.

For fishery production, quantities are weighted bythe average unit values of fishermen's landings in1961-65. For forest production, roundwood produc-tion is weighted by 1961-65 prices.

Trade index numbers 2

In calculating trade index numbers of agriculturalproduction for the present issue, both commodityand country coverages include all the commoditiesand countries shown in the 1973 issue of the FAOTrade yearbook.

All the different indices are calculated indepen-dently for the value, volume and unit value of exportsand of imports.

1 For full details, including a list of weights, see FAO, Productionyearbook 1973, Rome, 1974.

2 For full details see FAO, Trade yearbook 1973, Rome, 1974.

EXPLANATORY NOTE

xi

Value indices represent the current values of ex-ports (f.o.b.) and imports (c.i.f.), all expressed in U.S.dollars. If some countries report imports valued atf.o.b., these are adjusted to approximate c.i.f. values.This method of estimation shows an error wheneverthe trend of insurance and freight diverges from thecommodity unit values at export level.

Volume and unit value indices represent thechanges in the price-weighted sum of quantities andof the quantity-weighted values of products tradedbetween countries. The weights are respectively theprice and quantity averages of 1961-65, which is thebase reference period used for all the index numberseries currently computed by FAO. The Laspeyresformulas were used in the construction of the indexnumbers.

Regional coverage

The regional grouping used in this publicationfollows the recently adopted "FAo country classifi-cation for statistical purposes." The coverage ofthe groupings is in most cases self-explanatory. Itshould be noted, however, that in line with the deci-sion to divide countries into three broad economiccategories (developed market economies, developingmarket economies, and centrally planned economies)japan, Israel and South Africa have been removedfrom Far East, Near East and Africa respectivelyand are presented under "Developed market econ-omies." For this reason, tables for the three regionsare not always comparable with those shown inearlier issues.

The trade index numbers of a country group arebased on the total trade of each country includedin the group irrespective of destination, and in con-sequence generally do not represent the net tradeof the group.

Among other regions, it should be noted thatwestern Europe is defined as including Yugoslavia,and the Near East as extending from Cyprus andTurkey in the northwest to Afghanistan in the east,and including from the African continent Egypt, theLibyan Arab Republic and the Sudan.

HIGHLIGHTS

World agricultural production is likely to have increased little in 1974 compared with1973, when there had been a good recovery from the poor 1972 results. Performance inboth developed and developing regions in 1974 was discouraging.

Per caput food production in the developing countries as a whole in 1974 remainedlower than in 1970, in Africa and the Far East very substantially so.

Cereal production fell sharply in several regions in 1974, especially in the Far East,North America, and the U.S.S.R. Drought was again a principal cause. Livestock productionexpanded, especially in western Europe, but this sector faces serious problems.

Total cereal stocks in all countries (excluding China and the U.S.S.R.) have droppedbelow minimum levels for world food security.

The world fisheries catch again failed to expand in 1973.

World roundwood production increased in 1973 at a higher rate than in recent years.

The value of world trade in agricultural, fishery and forest products in 1973 increasedabout 26% in real terms. This large rise came from exceptional prices as trade volumeonly increased by 6%.

Sharply rising food prices have been a major factor in high rates of inflation since1973 in most countries.

Population, food supply and agricultural development are examined in Chapter 3.Malnutrition affects around 460 million people, a conservative estimate. It is stronglycorrelated with poverty. The world food situation will remain perilous until a much higher,sustained rate of increase in food production is attained in the developing countries.

xii

World agricultural production, particularly of ce-reals, made a good recovery in 1973 from the poorresults of the previous year, when the present foodcrisis began. Fishery production increased by about5% and forest production by some 3%. The totaloutput of agriculture, fishery and forest commoditiesrose by 4% (Table 1-1). Conditions in 1973 were

TABLE I-1. - INDICES OF WORLD PRODUCTION OF AGRICULTURAL,FISHERY AND FOREST PRODUCTS

Ciater 1. WORLD REVIEW

NOTE: For details of the methodology and coverage of these in-dices, sec the explanatory note on page xi.

Preliminary. 2 Percent changes from one year to anotherhave been calculated from unrounded figures. 3 ExcludingChina.

generally good, especially in the U.S.S.R. and in theFar East, in contrast to the widespread bad weatherof 1972. Most countries made special efforts to in-crease food production, and any remaining restric-tions on output were removed. However, with aworld population growth of 2%, per caput food pro-duction increased only slightly, and the gap in levelsof food production per caput between rich and poorcountries continued to widen. Many countries, par-ticularly in Africa and the Far East, were still pro-ducing less food per caput in 1973 than in the base

period, 1961-65 (100). The rise in food produc-tion in 1973, although substantial, did not preventfurther depletion of cereal stocks in the main ex-porting countries, particularly those of North Amer-ica; nor did it halt the steady rise in consumer foodprices. Moreover, agriculture was afflicted with widerproblems, including the energy crisis, inflation, mone-tary problems, a slowing down in the economic per-formance of major industrial countries and a gen-eral atmosphere of uncertainty.

In 1973, for the first time in many years, worldfood supplies depended precariously on the outcomeof the current season and therefore to a large extenton the weather. Again in 1974, with cereal stocksbelow safe levels, the situation remained unchangedor worsened. Even if the weather had been optimumfor agriculture throughout the world in 1974, it wouldnot have been possible to take full advantage of itbecause of the shortage and high prices of fertilizers.It is now clear that the weather was far from optimumfor agricultural production in 1974. Although therewere large harvests in most parts of Africa, Europe,Latin America and the Near East, earlier optimisticforecasts in North America and the U.S.S.R. wereprogressively scaled down. In the Far East, wherethe final results are not yet known, the monsoon waslate and erratic, causing damaging droughts andfloods in many areas.

Total world food and agriculture production in1974 thus appears to have only increased slightly,if at all. Any increase resulted mainly from anexpansion in livestock production, especially in west-ern Europe, reflecting serious problems in this sector.Cereal production fell sharply in several regions in1974, especially in the Far East and North America.The harvest in the U.S.S.R. was below the exceptionalone of 1973, but it is reported to have been its secondlargest ever.

Current stocks are so depleted that grain suppliesfor 1975/76 will depend entirely on the outcomeof 1975 harvests. While many governments areencouraging all-out expansion of production, theresponse of farmers may again be restricted by high

1969 1970 1971 1972 1973 1

Change1972to

1973 2

1961-65 average 100 Per-cent

TOTAL PRODUCTION 117 120 124 124 129 -I 4

Agriculture . . 117 120 124 124 129 +4Fishery 3 . . . . 130 135 136 134 141 +5Forestry 112 114 116 117 120 +3

POPULATION . . 112 114 117 119 121 +2

PER CAPLJT TOTALPRODUCTION . . 104 105 106 104 106 +2

Agriculture . . . 104 105 107 104 107 +2Fishery 3 . . . 116 118 116 113 116 +3Forestry . . . 99 100 100 99 99 +1

production costs and shortages of fertilizers and otherinputs. Individual farmers in many regions have alsobeen increasingly affected by inflation and by thecost/price squeeze in the livestock sector. There hasbeen no easing of the fertilizer shortage, but pricesmay be reaching a peak as demand is discouraged bytheir present very- high level. Some important pes-ticides will also be in short supply during 1975. Theweather, of course, is an unknown factor. On theother hand, the world demand for foodgrains willprobably continue to increase, while the short-termoutlook for animal feedstuffs is very uncertain inview of the state of the livestock industry.

World production of cereals in 1974/75 will proba-

Agricultural production

Production 19731

Both world food and agricultural production areestimated to have increased in 1973 by 4% in totaland by 2% per caput (see Table 1-2), a good recoveryfrom the 1972 setback. Food production rose by 5%in the developed regions and by 4% in the developingregions; it fell by 4% in two regions, Africa andthe Near East. The most serious situation arose inAfrica, where per caput food production in 1973 wassome 7% below that of 1961-65, mainly because ofdrought, not only in the Sahelian zone, but also inother countries of west Africa and in east and south-ern Africa. The 1973 drop in the Near East fol-lowed a year in which there was an exceptionallylarge increase, but not all of the 1972 increase waslost, so production was still higher than in 1971.

The best result in the developing regions was inthe Far East (up 8 to 9% for both food and agri-cultural production), where favourable monsoon con-ditions led to excellent paddy crops. In Latin Amer-ica, food production rose by 3%, which contrastsfavourably with the near-stagnancy of the two pre-vious years.

There was a 5% gain in China, where the recordgrain harvest of slightly more than 250 million tonshelped to overcome the setback caused by droughtin 1972.

The best result in the developed regions was shownby eastern Europe and the U.S.S.R., where both foodand agricultural production increased by 10%, amajor factor being the record U.S.S.R. grain harvest

1. See also Food and agricultural production in 1973, by regionsand countries, in rno, Monthly Bulletin of Agricultural Economicsand Statistics, 23, March 1974.

2

bly be below requirements for the third successiveyear. There are virtually no reserves left in export-ing countries, and despite the efforts to expand pro-duction in 1974, stocks cannot be replenished until1976, at the earliest. There is no assurance .that thedeveloping countries will be able to finance their in-creased food import bills. Food aid has already fallensharply, and unless aid budgets are increased tooffset inflated costs, its volume will shrink evenfurther. The world food situation will remain perilouS'.until a much higher and sustained rate of increasein food production is attained in the developingcountries and cereal stocks are rebuilt to saferlevels.

of 222 million tons, one third larger than in 1972.Also Oceania, with gains of 3% in agricultural

production and 10% in food production, made anexcellent recovery from the drought-stricken level ofthe previous year. Harvests were generally good toexcellent in western Europe and North America, andproduction increased by 3% and 2% respectively.

The marked improvement in world food produc-tion in 1973 as compared with the very difficultsituation in 1972 is further indicated in Table 1-3,which shows comparative results for ninety-sevendeveloping countries in 1972 and 1973, using 1961-65as the base period (100). Table 1-3 shows thatforty-seven of the countries included produced lessfood per caput in 1972 than in the base period, andthat per caput output in fifteen countries was downby more than 15% and in four others by more than10%. The combined populations of those countrieswhere food production per caput was lower than in1961-65 about 1 200 million represent some46% of the total population covered. Two maingroups of countries were involved: in the Indiansubcontinent and in west and central Africa. Onthe brighter side of the 1972 situation, as many asthirty-eight countries were producing at least 5%more food per caput than in 1961-65, seventeen ofthese as much as 15% and more. The change for thebetter in the world food situation in 1973 is indicatedby the sharp fall, from about 1 200 million to 470million, in the total populations of countries whereper caput food production was still below 1961-65;the proportion of population affected thus droppedfrom about 46% to 17%. The number of countrieswith per caput production levels below the 1961-65average fell slightly, the worst-affected area becom-ing concentrated largely in west, central and southern

TABLE 1-2. INDICES OF WORLD AND REGIONAL FOOD AND AGRICULTURAL PRODUCTION

Total

3

1 Preliminary. 2 Including countries in other regions not specified.

Africa. Conditions in the Far East improved sig- growing areas. The U.S.S.R. had a record crop ofnificantly, particularly in such heavily populated 110 million tons, about 30% larger than the disas-countries as India, Indonesia and the Philippines. trous 1972 crop. Production was also substantially

higher in the United States, encouraged by changesin government policy, as well as in Canada; it almost

PRODUCTION OF MAIN COMMODITIES 2 doubled in Australia. However, output fell in manydeveloping countries, including Argentina, Brazil,

World wheat production in 1973 reached a new India and several Near East countries, as well as inrecord, estimated at 377 million tons, with crop north Africa, and in the developing countries as aconditions good to excellent in the most important group. The gains were thus concentrated in the

U.S.S.R. and the developed exporting countries, whiletotal production in wheat-importing countries declined

2 For a more detailed review of the commodity situation, sccFAO Commodity review and outlook 1973-1974, Rome, 1974. slightly. Shipments to developing countries in 1973/

1973 I 1969 1970

Per caput

1971 1972 1973 1

Change1972

to1973

Food production

1961-65 aI'eragr 100 Per-cent 1961-65 averagc 100 Per-

cent

DEVELOPED MARKET ECONOMIES2 116 116 123 122 125 -I- 2 109 108 113 112 113 +2Western Europc 115 117 121 121 124 -I- 3 109 111 114 113 115 +2North America 115 113 124 122 125 +2 107 104 113 110 1 I I +1Oceania 121 121 127 127 139 +10 108 107 109 107 115 +8

EASTERN EUROPE AND TUE U.S.S.R. 125 132 134 134 148 +10 117 123 124 123 135 +9Total developed countries 119 121 127 126 132 + 5 111 112 117 115 120 +4

DEVELOPING MARKET ECONOMIES2 119 124 125 125 129 + 3 102 103 101 99 99 +1

Latin America 120 125 125 128 131 4- 3 101 102 100 99 99 oFar East 118 124 124 120 130 + 9 102 104 102 96 101 +6Near East 122 125 127 139 134 4 104 103 102 108 101 6Africa 117 119 122 124 119 102 101 101 99 93 7ASIAN CENTRALLY PLANNED ECONOMIES 116 122 125 123 129 +5 104 107 108 105 108 +3

Total developing countries 118 123 125 124 129 +4 103 104 104 101 102 +1

World 118 122 126 125 131 +4 105 106 108 105 108 +2

Agricultural production

DEVELOPED MARKET ECONOMIFS2 113 113 120 120 122 +2 106 105 110 109 110 + I

Western Europe 114 117 121 120 123 +3 109 110 113 112 114 +2North America 110 109 119 118 120 +2 103 100 108 106 107 +1Oceania 119 121 123 123 127 -I- 3 107 106 107 104 105 +1

EASTERN EUROPE AND THE U.S.S.R. 124 131 134 134 147 +10 117 123 124 123 134 +9

Total developed countries 116 119 124 124 130 -I- 5 109 111 115 114 118 +4

DEVELOPING MARKET ECONOMIES 2 119 123 124 124 128 + 3 I 102 102 101 99 99 o

Latin America 119 122 122 125 128 + 2 100 101 98 97 97 1Far East 118 123 124 120 130 + 8 102 104 102 96 101 +6Near East 122 124 128 139 133 4 104 103 102 108 100 7Africa 117 119 122 124 119 4 102 101 100 99 93 7ASIAN CENTRALLY PLANNED ECONOMIES 116 122 126 124 129 5 104 108 109 105 108 +3

Total developing countries 118 122 124 124 129 +4 103 104 103 101 102 +1

World 117 120 124 124 129 +4 104 105 107 104 107 +2

TABLE 1-3. FOOD l'RODUCTION PER CA PUT IN DEVELOPINGCOUNTRIES, 1972 AND 1973 (1961-65 AVERAGE = MO)

SOURCE: Annex table 2.

1974 rose by almost 30%, and larger amounts alsowent to China and eastern Europe, despite the factthat 1973 production had actually increased in theseareas.

World production of coarse grains increased toapproximately 675 million tons in 1973, 7% abovethe previous season and almost 4% above the recordlevel of 1971. The increase was due mainly to thelarge crop in the U.S.S.R., as output in the rest ofthe world rose by only 2%. Some increase in pro-duction occurred in most areas, but not in Africa,the Near East and eastern Europe. All grains con-tributed to the increase in world production. Barleyrecorded the largest rise in both absolute and relativeterms, almost exclusively owing to the record cropin the U.S.S.R.; in most other regions output de-creased or remained relatively stable. World pro-duction of maize resumed its upward trend followingrecovery in Argentina and larger crops in westernEurope, the United States and the U.S.S.R. Therewere larger crops of sorghum and millet in Argentina,India, the United States and to a lesser extent theU.S.S.R. Recovery in oats and rye production wasmainly a result of larger harvests in the U.S.S.R.

The 1973 world paddy crop (most of which wasavailable for consumption and trade in 1974) is esti-mated at 321 million tons, 4% above the previousrecord of 309 million tons (1971) and well above thelow 1972 crop of 294 million tons. There were biggercrops in most countries, although the recovery wasmost marked in the developing countries of the FarEast, where the 1972 setback had been more serious.The larger harvests were due not only to betterweather conditions, especially in the Far East, but

4

also to the response of farmers to sharply higherprices and other incentives.

Total world output of pulses increased by about4% in 1973, largely because of a sharp rise of 2 mil-lion tons (25%) in eastern Europe and the U.S.S.R.Output continued its downward trend in India, theworld's largest producer.

Expansion of world meat production came to ahall in 1973 after a slowdown in 1972. Red meatoutput in the developed countries actually declined,with production falling sharply in North America andremaining virtually unchanged elsewhere. Small gainswere reported in eastern Europe and the U.S.S.R.,and a substantial expansion took place in Latin Amer-ica, which accounted for the moderately higher totalproduction of the developing countries in 1973. Poul-try meat production continued to rise, although therate of increase in 1973 was probably one of thelowest in the past two decades. There was a slightreduction in North America. World egg productionmaintained its steady upward trend. World pigmeatproduction remained practically unchanged in 1973.Output fell by about 6% in North America, while forthe third consecutive year it showed no significantincrease in western Europe. Faced with an increasingcost/price squeeze and growing uncertainty aboutmarket conditions, many producers have apparentlyabandoned plans to expand output. World sheepnumbers continued to decline. The major reductionsoccurred in Oceania, where adverse weather resultedin lower lambing rates and slaughterings remainedhigh even some time after the marked rise in woolprices. The slow downward trend in numbers con-tinued in the United States and in most western Euro-pean countries, exceptions being France, the FederalRepublic of Germany and the United Kingdom. Thedecline in flocks led to a further drop in world muttonand lamb production, and the wool clip also declinedmarginally.

World milk production again increased slightly, butat roughly half the rate of 1972. There was signifi-cant expansion in eastern Europe and the U.S.S.R.,but output fell in Japan, North America and Oceania.There was only a marginal gain in western Europe.Both cow numbers and fodder production increasedin eastern Europe and the U.S.S.R., in contrast toconditions in most other developed regions, wherefeed conditions were unfavourable. In addition todrought in some areas, particularly severe in NewZealand, prices of concentrate feeds reached unprece-dented levels. Both cow numbers and milk yieldswere down in North America and New Zealand,although yields improved in Australia. In westernEurope lower milk yields offset an increase in cownumbers.

Although world sugar production in 1973/74 isestimated to llave reached a record total of about

Index offood production

per caput

1972 1973

Numberof

countries

Popu-lation(X)

Numberof

countries

Popo-lation(%)

84 and below . . 15 6.1 18 5.135-89 4 2.6 9 5.3)0-94 13 5.1 12 4.3)5-99 15 32.0 6 2.6

47 45.8 45 17.3

100-104 . . . . 12 6.0 19 37.4105-109 . . . . 14 37.1 9 34.8110-114 . . . . 7 7.2 12 9.0115 and above . 17 3.9 12 1.5

50 54.2 52 82.7

97 100.0 97 100.0

80 million tons, raw sugar equivalent, demand waseven greater, and world market prices more thandoubled between September 1973 and April 1974.World stocks were insufficient to ensure the continuityof supplies, especially after the beginning of 1974.The decline in stocks was widespread in both import-ing and exporting countries. Beet sugar productionis estimated to have reached nearly 32 million tonsraw sugar equivalent, about 3% more than in thePast two seasons. There was a substantial improve-ment in production in the U.S.S.R., mainly becauseof better weather conditions and yields. In westernEurope output did not fully recover to the recordlevel achieved with good weather in 1971/72, despitefurther expansions in the total area under beet.Production in the United States fell sharply and wasthe lowest for several years, owing to poor weatherat planting time and competition from grains andsoybeans. Output in eastern Europe was slightlydown. Cane sugar production in 1973/74 increasedby 6%, raising its share in total world sugar produc-tion to 60% as compared with 57% in the late 1960s.The increase came from developing countries, withproduction down in both Australia and South Africa.The largest increase, of about 1 million tons, camefrom Brazil; Cuba had another recovery and therewere record crops in Argentina, Colombia and Peru.The secular decline in output of some of the Carib-bean islands was reinforced by drought, notably inPuerto Rico, Barbados, Trinidad and Guadeloupe. Inthe Far East there was further recovery in India, andthe expansion in Indonesia and Thailand is expectedto continue. The upward trend of production in theAfrican and Near East regions continued, with recordcrops in Mauritius and Egypt.

Output of citrus fruit is estimated to have fallenslightly in 1973/74, after five years of uninterruptedgrowth. There were smaller harvests of oranges andtangerines in most main producing areas in the north-ern hemisphere, especially in the Mediterranean zoneand the United States. Exceptions are Italy andEgypt, where output rose by 5% and 10% respec-tively. Production of oranges and tangerines formarketing during the summer of 1973, consisting ofthe harvest in the southern hemisphere and the Va-lencia Late crop in California, fell by about 5%,mainly because of reductions in Australia and Brazil.Lemon supplies were also slightly down in 1973/74,as a 20% fall in United States production was notquite offset by an excellent Italian crop. World pro-duction of grapefruit was less, owing to poorer cropsin Israel and the United States. In Cyprus and SouthAfrica production was at the 1972/73 levels, whileoutput continued to expand in Argentina.

World output of oils and fats decreased in 1973for the first time in ten years. Production fell 0.6million tons below the previous year's record of

5

46.7 'pillion tons, and the drop was in sharp contrastlo the average long-term increase of some 1 1 milliontons annually. Production remained practically un-changed in developed countries but fell elsewhere.The fall by 3% in exports of oils and fats from de-veloping countries led to a resumption, after a re-versal in 1972, of the long-term decline in the relativeimportance of these countries in world trade. Amongthe soft oils the largest absolute drop in output wasin groundnut oil, primarily because the Indian cropwas drastically cut by drought, which also affectedproduction in west Africa. An increase in worldoutput of soybean oil largely offset the lower outputof groundnut oil, mostly reflecting increased produc-tion in Brazil and the United States. Both produc-tion and trade of cottonseed oil expanded, mainly onaccount of developments in the United States, andthere was a significant increase in exports of rapeseedoil despite a smaller world production. Sunflower-seed oil output and trade are estimated to have fallenslightly. For the fourth consecutive year there wasa smaller crop in the U.S.S.R., the world's largestproducer and exporter, owing to unfavourableweather. World output of olive oil was slightly down.Sharply lower production in Italy led to high imports,mainly from Spain, to maintain consumption levels.World exports of palm oil continued to expand,largely because of another expansion of output inMalaysia. Fish oil production, still drastically af-fected by low catches of anchoveta off South Amer-ica, fell below the already reduced level of 1972.

The 1973/74 world coffee crop was about 15%lower than in 1972/73, mainly because of frost inBrazil and drought in Africa. Total carryover inproducing countries was again sharply reduced, aftertending to stabilize in the last two crop years. Thefinal official estimate for Brazil places the crop at855 000 tons, as compared with 1.4 million tons in1972/73. The most serious losses were in the Stateof Paraná, but production was also down in SaoPaulo and other states. The African drought reducedcrops in many countries, including the arabica cropsof Ethiopia and Kenya and the robusta crops ofCameroon and Ivory Coast; the latter's outputmay be 40% lower. Colombia, on the other hand,is expected to have a record crop for the second yearrunning, owing to good weather and the high yieldsbeing obtained from the recent and increasing plant-ings of Caturra varieties. Elsewhere in Latin Amer-ica production was generally lower, notably in Mexicoand El Salvador. Output in the main Far Easternproducers, India, Indonesia and the Philippines, isagain at a high level.

Cocoa bean production in 1973/74, at some 1.4million tons, was close to the previous season's levelbut about 10% down from 1971/72. The 1973/74crops in the main west African producing countries

were again badly affected by drought, and the worldsupply situation continued very tight in spite ofrecord production in Latin America. The very dryweather in west Africa came during the period ofpod development, and most crops were thereforeabnormally late. Decreases in the Ghana and Nigeriacrops were only partially offset by better results inCameroon and Ivory Coast, where the 1973/74crops (at some 210 000 tons) were the second largeston record despite the dry weather. The good LatinAmerican results are primarily due to increased out-put in Brazil, where there was a record Bahia maincrop and a recovery in the tempordo crop from thedrought-affected 1972/73 level. A return to morenormal weather conditions could result in improvedworld output next season, but the problem of thelonger-term potential is one of increasing urgency.

World tea production reached another record in1973, but the 2% increase over 1972 was less thanexpected. Production recovered sharply in Bangla-desh (up 16%), and in India a good northern croplargely accounted for a 3% increase. Output wasunchanged in Indonesia but fell sharply in Sri Lanka.Kenya had an 8% increase compared to less than3% for Africa. Production fell sharply in Argentina,discouraged by higher costs and adverse weather.

World tobacco production continued to increase,by some 2%, in 1973, but in contrast to the previousyear developing countries as a group did not sharein this increase. Production gains in western Europederived from a revival of output in Greece andcontinued increase in Yugoslavia. The tobacco cropin the U.S.S.R. made a good recovery, and Chinahad a record crop of nearly 1 million tons. Lowertotal output in the developing countries stemmedmainly from a sharp reduction in India and smallercrops in Cuba, the Republic of Korea, Pakistan,Rhodesia and Turkey. World output of light cigaretteleaf rose again in 1973, with notable increases influe-cured leaf in Canada, China, Japan and theUnited States. Burley production, however, was farbelow the 1972 record even if it was the secondhighest reached.

World production of cotton remained unchangedin 1973/74 after substantial increases in the previoustwo years. There was a shift in cultivation fromcotton to more remunerative crops in some areas,but this was balanced by high yields and the highquality of the fibre harvested. The United Statescrop was drastically reduced following extensiveflooding in the Delta region, while shifts away fromcotton led to lower production in western Europe,the Near and Far East, Mexico, Colombia and someAfrican countries. There were increases in theU.S.S.R., where production reached its third consec-utive record, and in China, where it staged a partialrecovery from last season's setback. Total output

6

in the developing countries was slightly below thehigh 1972 level.

Output of jute rose by about 10% over 1972/73.India liad an exceptionally large crop resulting froma combination of favourable weather and higheryields on its intensive cultivation schemes. Produc-tion rose by about 25% in Thailand. However,the crop in Bangladesh was about 9% smaller, as aresult of both floods and reduced sowings in favouror paddy cultivation because of the more favourablerice prices.

World production of sisal and henequen in 1973,still affected by the droughts of 1970-72 and thereduced replantings of the previous years, remainedat about the same low levels as in 1972. Althoughweather conditions in east Africa returned lo normalfor a large part of the year, output in Tanzaniadeclined slightly again; an increase of about 40% wasobtained in Kenya, largely from hedge sisal on smallfarms, and because of the new government policyencouraging resumption of output on estates whichhad gone out of production during the previouslow-price period. Production also continued torecover in Haiti, encouraged by better prices. Nochanges were reported from Brazil, now the majorworld sisal producer, or from Madagascar, Mozam-bique and other minor producing countries. Thedecline of more than 20% in Angola's output repre-sented a return to more normal levels after the largeincrease obtained in 1972 by heavy cutting-out ofold plantations. In Indonesia, production appearsto have eased completely in 1973. Mexican Ilene-quen declined marginally.

World output of natural rubber rose considerablyin 1973, as higher prices brought increased tappingin all producing countries. Demand was strong,partly as a result of uncertain supply conditions forsynthetic rubber. The increase in output from Ma-laysian smallholdings, where tapping was reduced in1972 because of low prices, was one third higher.Output in India and Thailand also rose substantially.Even in Indonesia, where the possibility of raisingproduction is limited because of the low rate ofreplanting over the last decade, and in Sri Lanka,where political difficulties have discouraged produc-tion, output increased as a result of excessive tapping,as well as of chemical stimulation in some areas.The increase in African production was largely dueto higher output in Nigeria.

After two years of reduced output, 1973 wine pro-duction expanded to record levels as a result of verylarge increases in most important produciug coun-tries. World output, estimated at 349 million hec-tolitres, was about 25% above the 1972 level, whenproduction was adversely influenced by weather.Output in western Europe was more than 30%greater, and the harvest was also excellent in quality.

In eastern Europe the harvest increased by about10%, with production higher in every country, par-ticularly in Hungary and Romania. The U.S.S.R.harvest was for the first time above 30 million hec-tolitres. Production rose by 15% in Algeria despitefurther reductions in planted arca. Good results wereobtained in Morocco and Tunisia. Wine productionin the United Sta tes was sharply up on the reduced1972 crop as a result of excellent weather duringspring and summer. In the southern hemispherethe crop harvested early in 1973 was aboutnormal.

Production 1974

FAO'S first tentative world and regional indices offood and agricultural production for 1974 reveal thatthe year failed to bring the very large harvests thatare so urgently needed for replenishment of stocksand reestablishment of a reasonable degree of securityin world food supplies. Thus, for the third year,the world continues to face a situation of shortage,uncertainty and crisis.

In 1973, and this should be emphasized, worldfood supplies depended precariously on the outcomeof the current season and therefore to a large extenton the weather. Fortunately the weather was gen-erally favourable in 1973, and there was a consid-erable increase in world food production, especiallycereals. But a very large part of this increase wasin eastern Europe and the U.S.S.R. (about 10%)and in the Far East (about 8%), so it did notlead to the necessary rebuilding of cereal stocks inthe main exporting countries, in particular those ofNorth America. These stocks were in fact stillfurther reduced by mid-I974, the end of the 1973/74crop season.

Therefore, again in 1974, world food supplies de-pended to an extreme degree on the current year'sproduction of cereals. There were however additionaldifficulties because of the shortage and high priceof fertilizers. While the difficult fertilizer situationbegan earlier because of cyclical conditions in theindustry, it was exacerbated by the increase in theprice of petroleum that began in October 1973 andreached a fourfold level by December 1973. Therise in petroleum prices caused shortages of fuel andpower for irrigation pumping in many countries.Thus, even if the weather had been optimum for agri-culture throughout the world in 1974, it would nothave been possible to take full advantage of it.

It became increasingly clear in the last few monthsof 1974 that the weather had been very far from theoptimum during the year. This particularly affectedthe production of cereals, the staple food of most ofthe world's poorest people. Cereal production fell

7

sharply in several regions in 1974, but especially inthe Far East and North America. The Far East isthe most heavily populated region in the world andalso the region where most of the world's malnour-ished people are concentrated. North America is theregion on which world food security must greatlydepend until the increase in food production can besufficiently stepped up elsewhere, particularly in theneedy, developing countries themselves.

World cereal production fell in 1974 for the secondtime in three years. In North America earlier opti-mistic expectations of record cereal harvests weregradually scaled down as a result of drought in theMidwest and early frost. Among the other developedregions, tbere were record wheat crops in westernEurope. But in the U.S.S.R. cereal crops fell furtherbelow the very high record levels of 1973 than wasearlier expected, and there was also a decline inOceania. In Africa, Latin America and the NearEast substantial gains were registered over the gen-erally poor results of 1973. In the crucial Far Eastregion, however, the monsoon was late and erratic,and although the fl-aal outcome is not yet known,cereal production appears to have been considerablybelow the high levels of 1973. The extent to whichthe fertilizer shortage contributed to the widespreadfailure of cereal harvests in 1974 cannot be deter-mined at present, since its effects have been largelymasked by those of the weather.

With the disappointing harvests of 1974, priceshave started to rise again (Table 1-4). United Statesexport prices for wheat and maize remain almostthree times higher than in mid-1972, and Thai riceprices, although continuing to fall slightly, almostfour times as high. These high prices, combined withthe limited availability of food aid, continue to ag-gravate the balance of payments problems of themany developing countries requiring large importsof cereals. The rapid inflation of retail food pricesalso continues to bring hardship to the poorer con-sumers, although nonfood items have recently takenthe lead in price increases in most countries.

The supplies of cereals available to the world forthe 1974/75 season should be sufficient to meet allessential requirements for human consumption. How-ever, the low level of these supplies makes theirorderly management and equitable distribution anurgent matter. If they are allocated purely by priceand cash purchase, many of the hardest-hit countrieswill be unable to obtain the imports they need. More-over, some of these needs are still not fully known.For example, in India, where the immediate situationis in the words of the Prime Minister "extremelydifficult," the outcome still depends largely on theresults of the winter crops, which will not be knownuntil March 1975. Thus it is necessary to earmarksome supplies now, while they are still available in

TABLE 1-4. - RECENT CHANGES IN EXPOR1 ERICES OF SELECTED AGRICULTURAL COMMODITIES

I March (first week). - 2 Three weeks. - 3 Thai rice, as well as rice from most other regions, was not quoted regularly on the worldmarket from the second week of March to November 1973; this average is estimated on the basis of the few quotations that are availableand is only indicative of the change that has taken place in prices.

the market, for emergency needs that may arise untilJuly to October 1975, when the next main crops inthe northern hemisphere are harvested. The Director-General of FAO has therefore urged that the maincereal-exporting countries should take concertedaction to set aside for emergency use a minimum of8 to 12 million tons of cereals, in addition to importsalready contracted for and quantities committed asfood aid, for the group of most severely affectedcountries. He has also called for special measures,such as deferred payments and other concessions, toassist the developing countries in paying for the im-ports they require and for a continuing monthlyreview of the cereals situation as a basis for con-sultations among the major exporting and consumingcountries. Other related contingency measures alreadyunder way include the United Nations EmergencyOperation and the International Fertilizer SupplyScheme, both of which are still short of re-sources.

The world food situation at mid-October 1974 musttherefore be viewed with considerable concern. Theavailable supplies must be carefully managed duringthe subsequent nine to twelve months. Lookingbeyond this critical period, the outcome of the 1975harvests will be decisive. The poor results of 1974have postponed the replenishment of stocks for atleast another year, and 1975 will be the successivethird year in which food supplies depend perilously

8

on current harvests. In addition to weather, fertilizersupplies will again be a crucial factor, underliningthe importance of the International Fertilizer Scheme.While the shortage of fertilizer has not eased, pricesmay be reaching a peak, demand being discouragedby their present very high level. Some importantpesticides will also be in short supply during 1975.The concern aroused by this fact is heightened by theconsideration that prospects for increasing productionin future years appear dim.

The close interconnection of cereals and livestockproduction remains a major element in the world foodsituation. In addition to any other possible policyimplications, more cereals will have to be used fordirect human consumption and less for meat pro-duction; the cost/price squeeze is already leading tothis result.

Despite the decline in cereal production in 1974,total world food and agricultural production appearslikely to have increased slightly (Table 1-5). Thedata available in mid-October, which are incompleteand highly tentative, indicate an increase of no morethan 1%. This increase has resulted in the mainfrom a sharp expansion in livestock production,especially in western Europe, and thus has not greatlybenefited the food supplies of the countries whereshortages are most critical.

In the developed countries as a whole, total foodproduction in 1974 is estimated at about the same

U.S. dollarslinetric ton U.S. centslpound1972: January 60 131 51 125 7.90 44.80

June 60 136 53 138 6.33 47.76December 104 186 69 174 9.15 55.12

1973: January 108 179 79 214 9.40 57.03June 106 1205 102 470 9.38 62.78December 199 521 113 254 11.85 65.11

1974: January 214 538 122 261 15.40 66.24February 220 575 131 271 21.10 70.77March 191 603 126 265 21.10 72.04April 162 630 114 235 21.60 72.89May 142 625 114 229 23.63June 156 596 117 228 23.51July 169 519 132 276 25.03August 167 521 146 320 31.10September 2 170 516 143 34.15

AVERAGE: 1971 62 129 58 126 4.50 44.661972 70 151 56 140 7.27 50.341973 139 1368 98 290 9.45 62.16

SugarWhen t

(U.S. No. 2Hard Winter,

Ordinary,f.o.b. Gulf)

Rice

(Thai whiterice 5%, f.o.b.

-Bangkok)

Maize

(Yellow No. 2,f.o.b. Gulf)

Soybeans

(U.S., c.i.f.Rotterdam)

(isn compositeprice, world

market, f.o.b.and stowedCaribbean

ports)

Coffee

(Leo compositeprice

New Yorkca-warchouse)

TABLE l-5. --- ANNUAL CHANGES IN WORLD AND REGIONALAGRICULTURAL PRODUCTION I

I While these figures refer to total agricultural production,changes in food production are likely in most cases to have beenof a similar order of magnitude; the slightly different figures forfood production in 1974 in North America and Oceania are notedseparately. 2 Preliminary. 3 Including Japan, Israel andSouth Africa. 4 Food production: 5 to 4%. 5 Foodproduction: +1 to +2%. 6 Excluding Japan. 7 ExcludingIsrael. -- s Excluding South Africa.

level as last year. A decline of 4 to 5% inNorth America and a possible slight fall in easternEurope and the U.S.S.R. have been roughly balancedby increases in western Europe and Oceania. In thedeveloping countries, for which the data are evenmore tentative, there appears to have been a slightrise in food production in 1974, but almost certainlyless than the population growth. In Latin Americathe increase of 3 to 4% would, if confirmed, bethe largest since 1969. There were large increasesin Africa and the Near East, the two regions wherefood production had declined in 1973. In the NearEast this recovery probably raised production abovethe very high record level of 1972, but in Africaproduction in 1974 was only 3 or 4% more thanin 1970. The serious drop in food production in theFar East in 1974, tentatively estimated at 2 to3%, and thus comparable to the 1972 decline, alsoimplies a level of production only 3 to 4% above1970. Food production in China probably increasedby 1 or 2% in 1974. Per caput food productionin the developing countries as a whole remains lower

9

Iban in 1970 in Africa and the Far East very!-iubstantially so.

PRODUCTION OF MAIN COMMODITIES

As cereals and livestock products have been themain determinants of the overall level of food andagricultural production in 1974, they will be discussedin more detail below. First, however, some othermain commodities must be mentioned.

Although total production of vegetable oils andoilseeds (in oil equivalent) is estimated to havedecreased by about 2% in 1974, there were sub-stantial variations in the production of certain. prod-ucts. Groundnut production rose by about 3%, witha large mercase in Africa (30%) and declines in LatinAmerica (16%) and the Far East (10%). Soybeanproduction dropped by 9%, with a fall of 19% in theUnited States, the world's major producer, and anincrease of 40% in Brazil; soybean prices have there-fore begun to rise again. Although fishing has beenresumed in the Peruvian anchoveta fishery, fishmealproduction remains sharply reduced and prices high.Thus the general shortage of other concentrates be-sides grains for livestock feeding continues.

World sugar production increased by about 2%in 1974 but fell by 21/2% in developed countries.Prices continued to rise steeply and by Septemberwere more than twice as high as in January 1974and more than four times as high as in January 1972.The 1974 cocoa output is estimated to be 5% higherthan in 1973.

Among the other main crops, coffee productionincreased by 16%. Brazil, where production recov-ered by about 50%, accounted for about 500 000 tonsof the 700 000-ton increase. Cotton production roseby about 1%, probably reaching a new high, anda record crop is reported in the U.S.S.R. A drop ofsome 20% in the production of jute and kenaf couldhave serious consequences for the export earningsof Bangladesh and India. The production of naturalrubber appears to have increased slightly to a newrecord level.

Preliminary estimates of world cereal productionindicate a decline of between 2 and 3% in 1974 fromthe previous year's record level (Table 1-6). Pro-duction fell particularly sharply in North America,Oceania, the U.S.S.R. and the Far East.

There is likely to have been only a moderatedecline in world wheat production in 1974 from the1973 record level, with a reduced but still largevolume of trade in the trading year 1974/75 (1 July-30 June) and little or no prospect of stock replenish-ment at the end of the season. The incentives pro-vided by higher prices, together with favourableweather in some regions, contributed to larger bar-

1961-63to

1971_73(an-

1970to

1971to

1972to

1973to

nual 1971 1972 1973 1974 2aver-age)

Percent

DEVELOPED MARKETECONOMIES 3 +2.1 +6 0 + 2 O

Western Europe . +2.1 +3 I + 3 +3 to +4North America . +2.0 +9 1 + 4-4 to 3Oceania +2.6 +2 0 -F 3 5+2 to +3Eastern Europe

the U.S.S R +1.6 +2 0 +10 5-1 to 0

Total develo pedcountries +2.6 +4 0 + 5 0

DEVELOPING MARKETECONOMIES +2.6 0 + 3 +1 to +2

Latin America +2.6 0 +2 + 2 +3 to +4Far East 6 +2.4 +I 3 + 8 3 to 2Near East 7 +3.3 +3 +8 4 +5 to +6Africa 5 +2.3 +2 +1 4 +4 to +5Asian centrally plan-

ned economies . +2.8 +3 --2 -I- 5 -i-1 to +2

Total developingcountries +2.6 +-", 0 + 4 +1 to +2

World +2.6 +3 0 + 4 0 to +1

TABLE 1-6. ANNUAL CHANGES IN WORLD AND REGIONAL CEREALAND LIVESTOCK PRODUCTION 1973 TO 1974 1

1 Preliminary. 2 Including Japan, Israel, South Africa. -3 Excluding Japan. Excluding Israel. 5 Excluding SouthAfrica.

vests in many importing countries; however, drought,rain and early frost restricted wheat production to48.5 million tons in the United States and 14.2 mil-lion tons in Canada, a total of about 15 million tonsless than earlier predictions for the North Americanharvest. The U.S.S.R. wheat crop is currently esti-mated at around 90 million to 95 million tons, down15 million to 20 million tons from the 1973 recordcrop. Excluding the U.S.S.R., total wheat produc-tion in 1974 was actually higher than in 1973, withrecord crops in both the United States and westernEurope. Total production in developing countriesincreased in 1974. Estimates issued by the Inter-national Wheat Council (twc) on 28 November 1974forecast exportable supplies for 1974/75 of between65.8 million and 69.1 million tons, compared withestimated imports of 65 million to 66.5 million tonsand actual imports of 62.1 million tons in 1973/74.Thus the global supply and demand situation forwheat remains very delicately balanced.

Production of coarse grains is estimated to haveincreased or at least remained at the 1973 level inall regions except North America, the major exporter,and the Far East, where production declined sub-stantially. United States maize production fell by18% from the 1973 record. On the basis of pres-ent production forecasts, total exportable suppliesof coarse grains will be much lower for 1974/75.More coarse grains are available for export in Ar-gentina, Australia, South Africa and Thailand, butthe increased supplies of these and some smallerexporting countries are far from sufficient to offset

10

the heavy decline in the United States, where exportsupplies are currently estimated at about 28 milliontons as compared with actual exports of almost40 million tons in 1973/74. This implies that ex-ports on the scale of 1973 can take place only byfurther reducing carryover stocks which were al-ready at minimum operating levels at the beginningof the season and with a substantial reductionin dom-stic feedgrain use in the United States.There are however many uncertainties connected withthe forecasting of export availabilities and import re-quirements for coarse grains in 1974/75. It is par-ticularly difficult to make a reliable forecast of thelikely demand for grains as animal feed, in bothexporting and importing countries, because of thesevere cost/price squeeze affecting the livestock in-dustry and the slowdown in economic activity in manydeveloped countries. Demand for coarse grains asfeed may also be reduced because the poor qualityof part of the wheat crop in some areas may necessi-tate its use for feed. Nevertheless, on the whole, itseems highly probable that the world supply anddemand situation for coarse grains will remain verytight in 1974/75.

The tight grain situation has recently caused theUnited States to halt certain shipments of grain tothe U.S.S.R. and Iran, and to introduce guidelinesfor export sales which are "intended to assure anadequate but not excessive flow of grain to traditionalcus':omers." The introduction of these guidelinesfollowed closely on the United States Department ofAgriculture's crop estimates, based on conditions asof 1 October, which showed that estimated totalwheat and maize production had dropped by I and6% respectively from the September estimates.

It is still too early for definite figures on the ricecrop harvested in the Far East at the end of the year.Some countries, including China, Indonesia, Japan,the Republic of Korea and Malaysia, liad or expectedgood harvests. In others, however, the monsoon,after a late start, seems to have departed early fromsome areas, and consequently the kharif crops (mainlyrice) in India may not exceed 60 million tons, com-pared with 67 million tons in 1973 and the targetof 69 million tons for 1974. On the basis of presentindications the world's paddy crop is likely to beabout 317 million tons, some 2% below 1973, andtherefore the supply and demand situation for ricein 1974/75 is likely to remain very difficult, withsharply depleted stocks (except in China) and acontinued increase in demand.

Livestock producers almost everywhere weatheredthe first year (1972/73) of the upsurge in grain pricesremarkably well thanks to buoyant meat markets.Beef and, to some extent, sheep producers foundthemselves benefiting from a worldwide shortage asgrowing demand from a more prosperous world econ-

Cereals Livestock

Percent

DEVELOPED MARKET ECONOMIES 2 4 to 3 +3 to +4Western Europe + 4 to + 5 +5 to +6North America 11 to 10 +1 to +2Oceania 6 to 5 +3 to +4Eastern Europe and the U.S.S.R 6,to 5 +3 to +4

Total developed countries . 5 to 4 +3 to +4

DEVELOPING MARKET ECONOMIES 0 to + 1 +1 to

Latin America + 9 to +10 1 to 0Far East3 6 to 5 +2 to +3Near East 4 +12 to +13 +2 to +3Africa 5 +15 to +16 1 to 0Asian centrally planned economies 0 to + 1 +2 to +3

Total developing countries . . O to + 1 +1 to +2

World 3 to 2 +3 to +4

only outstripped available supplies. This, in turn,encouraged the holding back of cattle to build upherds and increase production capacity -- - which fora time served only to make the shortage even worseand push prices still higher. It is true that most ofthe world's heel is produced off grass and is thereforerelatively independent of grain market developments;but expensive beef provoked an analogous rise in theprice ceiling on livestock products based almostwholly on grains and oilseeds (i.e., pigs, poultry andeggs). The producers concerned found they couldstill operate profitably despite the sharp rise in theprice of their biggest single input, feedgrains.

In 1973/74, however, the expansion in livestockproduction encouraged by the high prices ran aheadof demand, the growth of which had already beenreduced in many developed countries by high retailprices and consumer resistance in the face of fallingreal incomes. Livestock producers in developedcountries are now severely affected by the cost/pricesqueeze, and many developing and other countrieswhich depend on livestock exports are also facinggreat difficulties, while consumers have hardly bene-fited from these developments. The sudden changein demand has led in several countries to a sharpfall in producer prices and to various import re-strictions.

The expected 2 to 3% increase in world meatproduction in 1974 reflects both the record cattleinventories built up in 1973 and earlier in response

Annual fluctuations in production are a majorfeature of the world food situation. Often they tendto offset one another to some extent at the regionalor global level, but when, as in 1972, there are simul-taneous drops in production (or increases short ofthe trend rate) in a large number of major countriesand regions, the implications for the world food situ-ation are serious. Therefore, in assessing the longer-term trends in food production, it is necessary toexamine the annual fluctuations above and belowthese trends and to attempt to determine whetherthere has been any cyclical pattern in their magnitudeor frequency which has affected the longer-termtrends.

Variations in seasonal rainfall, temperature, andother climatic factors are generally the principalcauses of fluctuations in food production; but iso-lating their effects from those of other factors involvedis difficult, having been effected for only a few cropsin some developed countries. Fluctuations in pro-duction lead to changes in price, employment, income,

to high meat prices and the heavy slaughterings inwestern European countries (up 10 to 20% in mostof them) and in the United States from mid-yearonward as an immediate consequence of the droughtin the Midwest and the western ranges and theresulting high prices for maize, soybeans and otherfeeds. Beef consumption in nearly all major beef-importing countries failed to increase, as the de-cline in producer prices for cattle and calves wasnot reflected in consumer prices. From 16 July 1974import licences were suspended for all products cov-ered by the EEC beef regulations (with the exceptionof the GATT quotas for frozen beef) until the situationin the EEC markets improved, and imports from thirdcountries were stopped. Imports of beef into Japanwere temporarily suspended. In the United Statesthe weakening of demand from feedlots for replace-ment cattle is keeping feeder cattle prices low. Pig-meat and poultry prices have come under strongpressure in recent months in western Europe andNorth America owing to difficulties in finding outletsfor increased production. Sharp rises in costs anduncertainties about the future of the market in viewof consumer resistance to high prices will in thecoming months almost certainly discourage furtherexpansion in the production of beef and other meats.Stagnant demand and the building up of livestockherds, in addition to the substantial stocks of meatin cold storage, may prevent any improvement inlivestock prices until late in 1975.

The influence of weather and climate on food production

11

and demand, which in turn influence the course ofproduction, generally- accentuating the fluctuationscaused by the weather. Changes in price and otheragricultural policies can cause production to varysharply from the trend. Civil disturbances, hostilities,natural disasters unrelated to weather, and pests anddiseases (sometimes linked with weather) are othersignificant contributors.

Climatic variations over quite short periods arenow generally recognized. For example, in theSahelian zone of Africa, where from the 1920s to the1960s the rainy season extended well to the north,the seasonal rainfall for the past six years has beenfar below average. On the basis of recorded changesof this kind over the last few decades, the WorldMeteorological Organization (wmo) concludes thatthe main overall changes appear to be a trend towardcooler conditions in parts of the northern hemisphere(at least until the beginning of the 1970s) and morefrequent extreme weather conditions such as floods,droughts, and cold and warm spells in widely scat-

tered areas. Nevertheless, except for the coolingnoted in parts of the northern hemisphere, theredoes not appear to be any overall trend toward drier,wetter, colder, or warmer weather; rather, it seemsthat certain areas have become more subject todrought and flood and to temperature extremes.Although the basic causes of these changes are un-known, they are associated with changes in the atmo-spheric circulation in the northern hemisphere.

While such changes have, of course, substantiallyaffected fluctuations in food production in particularareas, there is no evidence that any of the globalclimatic trends have had any significant influence oneither their magnitude or frequency. According towmo, the numbers of countries where yields perhectare of wheat and rice fell in any year during theperiod 1962-72 are distributed at random, showing nounusual or significant trend. An FAo analysis givesno evidence of significant change in the distributionof the "instability indices" of total food productionin 125 countries between the periods 1952-62 and1962-72.3 Although neither of these analyses dealswith the effect of climate as a separate factor, theyindicate that all the factors affecting variability, suchas expanded or more effective irrigation, extension ofcultivation into marginal land, other positive andnegative effects of technological change, pest anddisease outbreaks, policy changes, hostilities, andearthquakes, as well as changes in the weather, tendedto balance one another at the global level during theperiods considered; it is even possible that the effectsof changes in the weather were offset by changes inother factors. In the future, however, the balancecould change, and it is therefore necessary to givegreater attention to studying the effects of weatheranomalies on agricultural production.

The instability indices calculated by FAO for totalfood production in individual countries for the period1952-72 range from less than 2 to 37. Because onecountry offsets another, the indices are smaller forbroad zones and regions. In the main regions theindices for cereal production (for which the index ishigher than that for food production as a whole)range from 4 in the Asian centrally planned econ-omies through 6 to 8 in most regions, to 10 in NorthAmerica, 13 in eastern Europe and the U.S.S.R., and42 in Oceania. The overall index for the developedcountries is 6, as compared with 3 in the developingcountries, reflecting the effect of changes in agri-cultural policies as well as climatic conditions.

The worldwide instability index for cereal pro-duction in 1952-72 is 4, indicating that normal fluc-tuations can be expected to lie within the limits of

3 The instability index is defined as the percentage standarddeviation of the annual change in production from the trend rate;e.g., an index of 4 means a fluctuation of 4% above or belowthe trend.

12

8%; in fact, the 1972 shortfall in crop productionlay within these fluctuation limits.