the south african sugar industry and potential expansion...

TRANSCRIPT

THE SOUTH AFRICAN SUGAR INDUSTRY

AND POTENTIAL EXPANSION OF ITS

PRODUCT CHAIN

MPUMALANGA

KWAZULU-NATALFREE STATE

EASTERN

CAPE

Malelane

Pongola

Umfolozi

Felixton

Amatikulu

Darnall

Gledhow

Maidstone

Sezela

Umzimkulu

Komati

UCL Company

Noodsburg

Eston

SUGAR MILLS

RAIN FED AREAS

IRRIGATED AREAS

Industry structure - representation

13 LOCAL GROWER

COUNCILS

Tongaat Hulett Sugar Ltd 4 Mills)Illovo Sugar Ltd (4 Mills)

TSB Sugar RSA Ltd (3 Mills)UCL Company Ltd (1 Mill)

Umfolozi Sugar Mill (Pty) Ltd (1 Mill)Gledhow Sugar Company (Pty) Ltd

(1 Mill)

SA SUGAR ASSOCIATION

COUNCIL

GROWERS MILLERS

SA CANE GROWERS’

ASSOCIATION

SA SUGAR MILLERS’

ASSOCIATION LTD

South African Sugar Industry

an important contributor to the SA economy

Total average industry income R12 billion p.a

Gross Domestic Product 0.84% of SA GDP

Export earnings R2.5 billion p.a

Annual Cane Production 20 million tons

Average value of sugarcane production +/- R7.7 billion p.a.

Area under cane ~ 371 662 ha

Contribution to SA’s total agricultural

output

6%

Dependent rural livelihoods Approx. 1 million people

Direct job opportunities 79 000 (11% of agri employment)

Indirect employment 350 000

Production and exports statistics

• The global sugar industry has almost 120 producers, including the

individual EU member states.

• In its 2013 Yearbook the International Sugar Organisation (ISO)

ranked South Africa as the 18th largest sugar producer globally.

• South Africa further ranked as the 11th largest exporter globally.

• The industry is more than 150 years old.

World sugar market – major producers 2011

0 5 10 15 20 25 30 35 40

Peru

Vietnam

Cuba

RSA

Egypt

Columbia

Guatemala

Turkey

Indonesia

Ukraine

Phillipines

Australia

Pakistan

Russia

Mexico

USA

Thailand

China

EU

India

Brazil

Million Tonnes

South Africa

1,981,186 Tonnes

* South Africa dropped places from 16 in 2010 to 18 in 2011 due to drought.

World sugar market – major exporters 2011

* South Africa dropped places from 9 in 2010 to 11 in 2011 due to drought.

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Serbia

Azerbaijan

U.S.A.

Ghana

South Africa

Nicaragua

Zambia

EU

Mexico

Guatemala

UAE

Australia

India

Thailand

Brazil

South Africa

265,887 Tonnes

Million Tonnes

Journey for shared growth and sustainability

Improved

productivitySustainable sugarcane

agriculture

Increased revenueLimiting Imports

Diversification

Premium market access

SACU policy harmony

Stable regulatory

environmentTariff Protection

Internal industry

processes for cost

reduction

Holistic and specialised approach to the complex

challenges faced by the sugar industry

Skills training (Shukela Training

Centre)

Research (SASRI)

Land reform and rural development

Terminal

GROWER

DEVELOPMENT

FUNDING

FACILITY

Industry support

Grower Development Account

Invested over R206 million for the development

of black growers in the industry

Sugar Industry Trust fund for Education:

Established in 1965, assisted over 10 000

students from rural and urban communities with

bursaries, various interventions at a school level

such as maths and science.

Supplementary Payment Fund (SPF):

SPF initiated in 2005/06, with approximately

R240 million distributed to growers to date.

BOOST INCOME OF

SMALL SCALE

GROWERS

DELIVERING < 5 000

TONS CANE PER

SEASON

Decline in production

Decline in

area under

cane and

cane yields

~10%

reduction

over the past

10 years

Decline in number of growers

Decline in

number of

growers

50%

reduction in

small scale

grower

numbers

Land reform status

• Most progressive

commodity terms of

land transfers.

• 74 624 hectares

transferred (22% of

freehold

commercial land

under sugar cane

production).

• Black ownership will

exceed 50% as the

pace of restitution

gains momentum.

Impact of the recapitalisation and development

programme

• Received R3 million: replanting,

ratoon management, irrigation

infrastructure for bananas.

• Resulted in a 61 % increase in

production.

• 9 permanent jobs and 70 seasonal

jobs created.

• Hosted her own youth day

programme in 2013 on her farm.

Impact of recapitalisation in the industry

Impact: tonnage delivered

Global market diversification

Impact of Import Tariff

Import Tariff

No limit to imports

Shrinkage of the industry

IMPACT

Sugarcane processing

Fibre (bagasse)

• Industry co-product used to produce electricityand steam - current fuel supply matched to ownenergy use

• Other products - animal feeds, paper, chemicals

Sugars

• 80% as sugar

• 20% as molasses

Sugars to ethanol

• Molasses as potable and industrial ethanol

• Fuel ethanol

Sugarcane – one of most efficient plants to convert sunlight into energy

15% fibre

15% sugar

Tops &

leaves

15% fibre

Renewable Energy Opportunities

• Cogenerated electricity

– Feedstock - bagasse & sugarcane brown leaves

– Brownfields cane supply – Brownfields cogeneration plant

• Biomass electricity

– Feedstock - sugarcane fibre brown leaves & other biomass fuels

– Brownfields cane supply – Greenfields biomass plant

• Biofuels

– Feedstock - sugar juice

– Greenfields cane supply – Greenfields ethanol distillery

– Brownfields cane supply - Greenfields back-end/stand alone ethanol distillery

Options premised on the principle that supply to existing domestic sugar market value

streams and ethanol distilleries remain

Harnessing the full value of the sugarcane talk

Renewable cogenerated electricity

Sugarcane HarvestingBagasse

Renewable Fuel

Processing at sugar

millElectricity

• Sugar industry can contribute to addressing current energy crisis

• Minimal capital investments, agreements and grid connections

secured sugar industry could export cumulatively 78 MWs to

national grid

• Projects span over 3 year period

Sugar Independent Power Producers

Technology and efficiency improvements, 2 to 7 times more

energy available ~ 712 MWs

Jobs and skills development

Vertical expansion –

increased intensity

of production

Horizontal

expansion – new

land under

production

Seasonal expansion

– length of season

from 36 to 40 weeks

Greencane

harvesting

Bioethanol

SugarcanePotable and

industrial ethanol

Fuel

Bioethanol

• Fastest implementation - export sugar could be diverted to fuel ethanol

• Industry would always supply local sugar market

• Most capital and cost efficient approach – also consistent with Brazilian practice is for

brownfields sugar ethanol production

• At least 2 to 3 large ethanol distilleries, capacity 125 000 m3/a with diversion of

50% of sugars to ethanol

• Investment > R3 billion rand and creation of > 4 500 jobs mainly in agriculture

Jobs estimated at full and expanded capacity

Job Creation

Sugar-electricity Bio-ethanol

Agriculture 19 147 15 369

Construction 6 935 5 243

Operations 416 466

Total 26 498 21 078

Full-Time Positions

• A full-time position constitutes employment for at least 12 person months.

• Creation of new jobs in agricultural and operations phases is attributable to expanded

agricultural production

• Vertical expansion – increased intensity of production

• Horizontal expansion – new land under production

• Seasonal expansion – length of season from 36 to 40 weeks

• Greencane harvesting – labour intensive harvesting of cane without burning to

remove leaves and tops in order to provide brown-leaf for electricity production

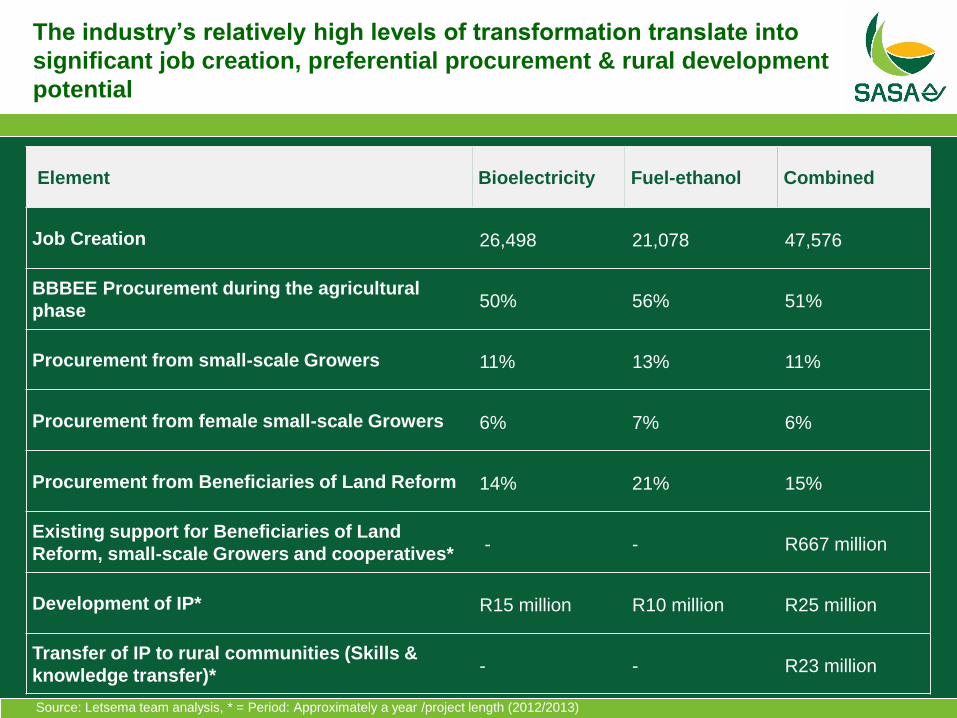

The industry’s relatively high levels of transformation translate into

significant job creation, preferential procurement & rural development

potential

Element Bioelectricity Fuel-ethanol Combined

Job Creation 26,498 21,078 47,576

BBBEE Procurement during the agricultural

phase50% 56% 51%

Procurement from small-scale Growers 11% 13% 11%

Procurement from female small-scale Growers 6% 7% 6%

Procurement from Beneficiaries of Land Reform 14% 21% 15%

Existing support for Beneficiaries of Land

Reform, small-scale Growers and cooperatives*- - R667 million

Development of IP* R15 million R10 million R25 million

Transfer of IP to rural communities (Skills &

knowledge transfer)*- - R23 million

Source: Letsema team analysis, * = Period: Approximately a year /project length (2012/2013)

Economic value add benefits from renewable

energy

Growth in sugarcane value chain for SA Inc.

> R20 billion

investment

> 40 000 jobs

Localisation &

industrialisation

Energy supply and

energy security

Extensive rural and agric dev.

Compliment IPPs

Renewable fuels

Build and expand socio

economic programmes – enterprise

dev.

Low carbon economic

growth

Principles of rural development

• Sustainable production models

• Production support

• Infrastructure development

• Enterprise Development

Sustainable sugar cane

development

• Youth Development

• Training and skills development

• Co-operatives support programme

People Development

Enterprise development

• Across cane production cycle

• contractors for planting

• ratoon management

• harvesting

• haulage

• Growth in supply chain services

• motor vehicle supply and

repair firms,

• fertilizer and chemicals

• engineering services

• fuel and lubricant outlets

Concluding points on energy

Biofuels

• Biofuels regulatory framework and the subsidy models are under

review by National Treasury

Renewable cogeneration from sugarcane fibre

• The release of the Request for Proposal for the national cogeneration

IPP programme which supports procurement of renewable

cogeneration from sugarcane fibre is imminent

SIYABONGA

THANK YOU

DANKIE