the role of self-help groups in community … role of self-help groups in community development...

TRANSCRIPT

The Role of Self-Help Groups in Community

Development

Evidence from a Field Experiment in Rural India

Raj Desai and Shareen Joshi

Georgetown University

May 2010

Abstract

This paper explores the impact of participation in self-help groups (SHGs) on the well-being of women and their

communities. A randomized-control-trial framework is used to evaluate the impact of SHGs in 32 villages of

Dungarpur district of Rajasthan. These results suggest that in the first two years of their operation, SHGs had direct

and positive impacts on women’s savings, employment, participation in household decisions and participation in

local government. They also have ―spillover‖ effects on women who do not participate in the SHG but reside in the

same village that the SHGs operate. The post-program impacts are not attributable to pre-program differences in the

villages or the types of women who participated. The results confirm that SHGs can be a powerful instrument of

development policy. Moreover, placing women at the center of development policy can have far-reaching impact.

1

1. Introduction

In recent years, self-help groups (SHGs) and other types of community-based

organizations have been increasingly regarded as important instruments of development policy

(World Bank, 2002; Bardhan, 2002; Chen, Jhabwala, Kanbur and Richards, 2006).1 SHGs can be

broadly characterized as membership-based organizations whose members provide each other

with mutual support and attempt to achieve collective objectives using, in part, their own

contributions. One of the main distinguishing characteristics of these groups is the strong

emphasis on building social cohesion. This enables members to overcome social, economic, and

political differences and develop the collective strength to promote their collective interests

(Chen, Jhabwala, Kanbur and Richards, 2006).

Scholars and practitioners in the field of development have been attracted to SHGs for

two main reasons. First, the expansion of freedoms and creation of opportunities in marginalized

populations has intrinsic value and is one of the primary ―ends‖ of development (Sen, 2000).

Second, these groups are increasingly regarded as an important ―means‖ through which many

other development goals can be attained. Evidence from case-studies across the world suggests

that they achieve this by linking marginalized individuals to the state and to markets, lowering

risk, dissipate information barriers and/or increasing accountability (World Bank, 2002).2 Such

evidence however, is rarely based on scientific evaluations. Evidence based on randomized and

scientific evaluations of SHGs or even other community-based institutions are quite rare. Efforts

to measure impact are typically constrained by the non-random placement of programs, the non-

random assignment of individuals to groups and wide variations in the methods employed by

these organizations (Rao and Mansuri, 2004).

The SHG movement has been particularly strong in India. Official figures from India’s

National Bank for Agricultural and Rural Development (NABARD) – likely an underestimate of

the true number of self-help groups in India – suggest that at least 90 million Indian households

are currently organized into 6 million self-help groups (NABARD, 2010). Indian SHGs are

typically established by facilitating agencies that include NGOs, the Indian government, formal

sector banks (including private banks) and federations of SHGs themselves (Basu and

1The World Bank defines Community-based Development (CBD) and Community-driven Development (CDD) as a

process of development in which communities and community-groups have direct control over key project

decisions, including management and investment of funds (Chapter 9, World Bank, 2002). 2 This is a summary of Chapter 9 entitled ―of the World Bank’s Poverty Reduction Strategy Paper Sourcebook.

2

Srivastava, 2005; Bhatia, 2007; NABARD, 2010). These groups have not only helped groups

with organization, but also with the supported SHGs by the introduction of innovative financial

instruments, investment opportunities and the provision of education and training (Basu and

Srivastava, 2006; Chen et al, 2006; Nair, 2005). 3

The precise impact of such initiatives however, remains poorly understood. In one of the

few examples of rigorous evaluations, Deininger and Liu (2009) study the impact of a large-scale

intervention in the Southern state of Andhra Pradesh. Unbanked villagers were organized into

SHGs. Second-tier institutions were also created at the village-level to aid groups with credit,

insurance and interactions with the private-sector and were given ―seed‖ capital to aid them in

these efforts. While the program was not randomly placed, the authors use methods such as

propensity score matching to compare participants and non-participants and find that 2.5 years of

exposure to the program was associated with improvements in consumption, nutritional intake,

and asset accumulation. While this paper makes an important contribution in understanding the

impact of such groups, it is not clear that the results can be generalized to the rest of India, where

the SHG-movement has a much shorter history and levels of participation are significantly

lower.4 Moreover, the paper evaluates only one type of SHG out of many possible models. More

studies are required, of other types of groups and in other states of India (Bhatia, 2007).

This paper extends the literature on the effectiveness of SHGs by evaluating an SHG

program in the Dungarpur district of the North-Western state of Rajasthan. The state has levels

of SHG prevalence that are one-quarter of those seen in Andhra Pradesh or for that matter most

of Southern India.5 The evaluation is conducted in partnership with the Self-Employed Women’s

Association (SEWA) of India, a woman-focused NGO that aims provides over 1 million poor

women with improved opportunities for saving, investment, employment, education and life-

3 A famous example of this is the case of this is the SHG-bank Linkage Program, which attempts to provide formal-

sector credit and financing services to informal groups, particularly in rural areas. Launched in 1992 by the National

Bank for Agriculture and Rural Development, this program supported micro-finance institutions through training

and capacity building, grant assistance, equity/capital support and the provision of 100% refinance for loans that

supported microfinance activities (NABARD, 2010). The 1992 pilot envisaged linking of just 500 SHGs to banks.

By the end of March 1994, 620 SHGs had been linked to banks. The success of the pilot led to its transformation

into the SHG bank linkage program and in less than one decade this became one of the biggest micro-finance

projects in the world. Over 10% of credit to rural areas of India is now channeled through this program. 4 Andhra Pradesh accounts for 26.2 per cent of the total SHGs and 38.1 per cent of the total loans disbursed in India

as a whole (Bhatia, 2007). 5 While Rajasthan has the highest prevalence of SHGs in the Northern states of India, it accounts for only 4.4 per

cent of the SHGs and just 2.1 per cent of the total loans disbursed (Bhatia, 2007).

3

skills training. SEWA used its deep understanding of contextual conditions in this region to

design suitable SHGs. It organized 450 randomly selected women into a total of 32 village-based

SHGs since 2007. We examine the impact of this effort using a comprehensive randomized-

controlled trial (RCT) which identifies clear treatment and control groups and compares them

before the intervention and then two years later.

Our results confirm that participation in the carefully designed and implemented SHG

program had private as well as social returns. Participating women saved more, were more likely

to have bank accounts and were more likely to participate in the management of their savings.

They were also more knowledgeable about credit opportunities and more likely to take loans.

They are also more likely to have a greater say in household decisions regarding children’s

education and health. Participating women were more likely to take advantage of key

government programs and know which authorities to report grievances about government

services such as water/sanitation, roads, electricity supply and educational and health services.

There is also evidence that some of these benefits spilled over into the greater village

community. Women who resided in the same village as the SHG, including those who did not

participate in the SHGs, experienced an increase in decision-making authority within the

household.

These results have some major policy implications. First, the results confirm that when

SHG programs are implemented well, with careful consideration of contextual factors, they can

promote collective action in marginalized communities be valuable instruments of development

policy. Second, the results confirm that placing women at the center of development policy can

have far-reaching impact. This result is now well-established for investments in education and

health (Schultz, 1995; 2001a, 2001b; Buvinic and King, 2007). We show that other types of

investments – such as the opportunity to form networks and take collective action – can also

have positive effects on women as well as their broader communities.

2. Background and Data

Dungarpur is located close to the Southern border of the state of Rajasthan in North India.

The total population of Dungarpur is approximately 1.1 million and its population density is one

of the highest of Rajasthan’s rural areas, at 284 people per square-kilometer (Census of India,

4

2001). The population is largely composed of scheduled caste and scheduled tribes.6 The rural

population has traditionally relied on three major sources of subsistence: gathering from the local

forests, animal husbandry and seasonal agriculture. Growing levels of deforestation in recent

years however, have prompted many to turn to settled agriculture. The proportion of the

population engaged in agriculture (cultivators and agricultural laborers) stands at about 76 per

cent (Census of India, 2001). Levels of poverty however, remain high and per-capita income

remains low. In 2004-05 the per capita income of Dungarpur stood at Rs. 12,474 (approximately

$312) compared to state average of Rs. 16,800 (approximately, $420) (Government of India,

2009). 21 percent of the population is estimated to live below the rural poverty line (Government

of India, 2009).

Dungarpur’s gender profile has some interesting contrasts. It is one of the only districts of

Rajasthan, perhaps even North-West India, where the female-male sex-ratio is relatively close to

the biologically ―normal‖, at 1,019 women for every 1,000 men. Yet the total fertility rate (TFR)

and infant mortality rate (IMR) however, are higher than the Indian and the Rajasthan average, at

4 and 112 respectively (Census of India, 2001). The female labor-force participation rate of

Dungarpur is almost double the Indian average, at 44.7 per cent (Census of India, 2001).7 Yet

more than half of all female-workers report that they are ―marginal workers‖, one of the poorest

paid in rural India.

Overall human development in Dungarpur remains one of the weakest in the state of

Rajasthan, which is already one of the lowest in India (Government of India, 2009). With the

overall literacy of 48 per cent in 2001 (up from 19 per cent in 1981 and 31 per cent in 1991)

Dungarpur still continued to be at the bottom in the ranking of districts with respect to its

educational indicators. Only half as many women are literate than men: male and female literacy

rates, stand at 66 and 31 per cent, respectively (Census of India, 2001). The district is also third

from the bottom on indicators of health and income (Government of India, 2009).

In 2004, the Indian Planning Commission included Dungarpur in its ―Backward Districts

Initiative‖ which aimed to address the problems of low agricultural productivity, unemployment,

and to fill critical gaps in physical and social infrastructure through the efforts of both the central

6 65 percent of Dungarpur’s population belongs to the ST group, with the highest concentration in the South of the

district. The dominant tribe here is that of the Bhils. This tribe’s occupancy in the Aravalli range (one of the oldest

mountain ranges in the world) is said to date back to 4000 BC (Government of India, 2009). 7 A higher female labor-force participation rate than average is typical of India’s tribal regions.

5

and state-level government interventions.89

Part of the district’s development strategy was to

invite into its borders an NGO with an excellent history of working in neighboring state of

Gujarat, the Self-Employed Women’s Association (SEWA). The organization has a membership

of over 1 million women in 7 states of India. The members are largely poor and self-employed

female workers who seek economic, social, and professional self-reliance. Members are provided

technical training, are connected with marketing organizations and larger businesses, and are

enabled to purchase agricultural inputs collectively at lower prices. SEWA largely accomplishes

these goals with the formation of SHGs that help women improve access to credit, increase

savings, and provide for community-based social services such as health and childcare for their

members. SEWA also intends to support participants in SHGs as well as the broader village

community in becoming active in village affairs, standing for local elections, and taking action to

address social or community issues (abuse of women, the dowry system, educational quality, and

maternal health). These self-help groups can also serve as intermediaries for the poor, enabling

them to enter more effective cooperative agreements with larger corporations (domestic and

multinational) as potential business partners.

SEWA began a rollout of its rural integrated development pilot project in Dungarpur

district in late 2007. All villages on the census listing for the Dungarpur district were stratified

according to average female literacy rate, total number of households, and average household

size. From these strata, 32 villages were randomly selected for the SEWA pilot, 48 villages

selected as ―control‖ villages (80 villages in total) for the evaluation. A group of 500 women in

the SEWA villages were randomly invited to participate in SEWA’s SHG program. 442 of these

women accepted the offer and went on to participate in the SHG program. The ―treatment‖ given

to SEWA members in the two subsequent years included the following:

Formation of SHGs that consisted of groups of 10—20 women with an elected leader.

Each member is required to save money on a regular basis and the collected saving

money is given as loan to members on a rotating basis (usually once a month). The entire

transaction is transparent and properly audited.

8 The identification of backward districts within a State has been made on the basis of an index of backwardness

comprising three parameters with equal weights to each: (i) value of output per agricultural worker; (ii) agriculture

wage rate; and (iii) percentage of SC/ST population of the districts. 9 A sum of Rs. 15.00 crore per year (approximately $3 million) will be provided to each of the districts for a period

of three years i.e. a total of Rs. 45.00 crore (approximately $9 million) per district.

6

The Membership Education program: This is the most basic and introductory program of

SEWA that is intended to create a sense of unity and direction, and an understanding of

collective action among SEWA members.

Training and Capacity Building: This program aims to build capacity of the SHG leaders

(through reflection meetings, exposure trips, lateral learning), and build capacity by

developing skills such as management of the group, maintaining accounts, writing reports

etc.

A baseline survey was carried out by the Wolfensohn Center for Development at the Brookings

Institution in November and December of 2007 shortly before women were organized into the

SHGs. Two years later, in late 2009, the same research team conducted a follow-up study.

Following RCT methodology, the survey was designed compare the participants in SEWA’s

programs with a control group consisting of women who are not participating in SEWA’s

programs, both in the targeted villages as well as in villages that are not part of the SEWA pilot.

The new sample thus contained three separate groups of women:

Treatment Sample: All 442 women who were scheduled to participate in SEWA’s programs

in the 32 SEWA-pilot villages in the Dungarpur district;

Control Sample A: An additional sample of between 358 women in these same villages who

are not participants in SEWA’s program;

Control Sample B: An additional sample of approximately 802 female-households in 48

other villages that are not part of the SEWA-Dungarpur pilot. These villages are drawn from

the same census frame from which pilot villages are selected, and these villages may have

other SHGs (besides SEWA) operating.

The baseline survey together with the endline survey thus formed a pooled cross-section

that could be used to evaluate the program. The survey collected data on income, savings, labor

force participation, agricultural operations and credit arrangements. The survey also focused on

political-economic issues such as whether SHG membership changes the relationship of SEWA

members with local government officials and whether membership in SEWA increases political

awareness and participation by SEWA members in the village. In the rest of this paper, we use

the terms ―treatment group‖, ―SEWA members‖, ―participation in SHGs‖ and ―participation in

SEWA SHGs‖ interchangeably to refer to the treated sample.

7

4. Analysis and Results

We seek to explore the impact of the treatment program on the treated individuals and

villages in which treated individuals resided. We are interested in five areas of impact:

1. Saving and Financial Decision Making: One of the primary benefits of participation in a

SHG is the opportunity to save regularly, access formal savings institutions and participate in

the management of these savings. We would thus expect treated individuals to be more likely

to report that they save regularly, be more likely to have their own bank accounts and make

deposits into these accounts. We define dummy variables accordingly – saving regularly and

owning a bank account and making deposits into these accounts.

2. Access to credit: A corollary of participation in SHGs is an improvement in a woman’s

access to credit. Since the project is perhaps too early in its implementation to directly

improve women’s access to credit, we examine whether participation in an SHG leads to

greater awareness of credit opportunities by defining a simple dummy variable that takes

value 1 if a woman knows of any programs in the local area that give loans to women so they

can start or expand a business of their own, and 0 otherwise. We also examine actual credit

obtained by examining a dummy variable that takes value 1 if a woman has taken a loan in

the preceding five years and 0 otherwise.

3. Employment: While SHGs were not directly provided with employment opportunities during

the time-frame under consideration here, one of SEWAs foremost goals is to improve

women’s employment prospects as well as the wages that they are paid. We explore just

three simple employment measures – whether or not a woman is employed, whether or not

she is self-employed, and whether or not she participates in the NREG program.10

4. Decision-making within the household: Improvement in access to economic opportunity can

influence a woman’s bargaining position within the household (Schultz, 2001a). We do not

have data on spending patterns that allow us to test whether women gained more control over

resources, but women were asked about their participation in key household decisions: their

ability to make a Final say in matters of keeping children in school, medical decisions and

10

The Mahatma Gandhi National Rural Employment Guarantee (NREG) Scheme is an Indian job guarantee scheme,

enacted by legislation on August, 2005. The scheme provides a legal guarantee for one hundred days of employment

in every financial year to adult members of any rural household willing to do public work-related unskilled manual

work at the statutory minimum wage (http://nrega.nic.in/).

8

family-planning. We define dummy variables that take value 1 if the woman participates in

these decisions and 0 if she does not participate at all.

5. Participation in local government: As mentioned earlier, SEWA supported SHGs are

intended to promote participation in the broader village community, participation in local

elections, and take action to address social or community issues. While two years is perhaps

too short of a time-frame to expect many of these outcomes, we would at the least expect

women to know about their local political institutions such as the Gram Panchayat and would

also expect them to have better knowledge of where to report certain types of grievances.11

We explore women’s knowledge of where to report five types of grievances:

water/sanitation, road conditions, electricity supply, education services and health services.

These are well-known as the key areas where service delivery in rural India has seen

significant failures and mismanagement.

Descriptive Statistics

Establishment of a causal relationship between the SEWA program implemented in late

2007 and the observed outcomes in 2009 requires an analysis of the pre-program differences

between treatment and control villages. If for example, the two areas differ in characteristics that

are associated with improvements in socio-economic well-being before or after the program was

established in 2007, estimates of the SEWA program could be biased. Our first objective

therefore, is to compare some basic outcomes in the treatment villages as well as the two sets of

control villages before the SEWA programs were introduced. This information is presented in

Table 1.12

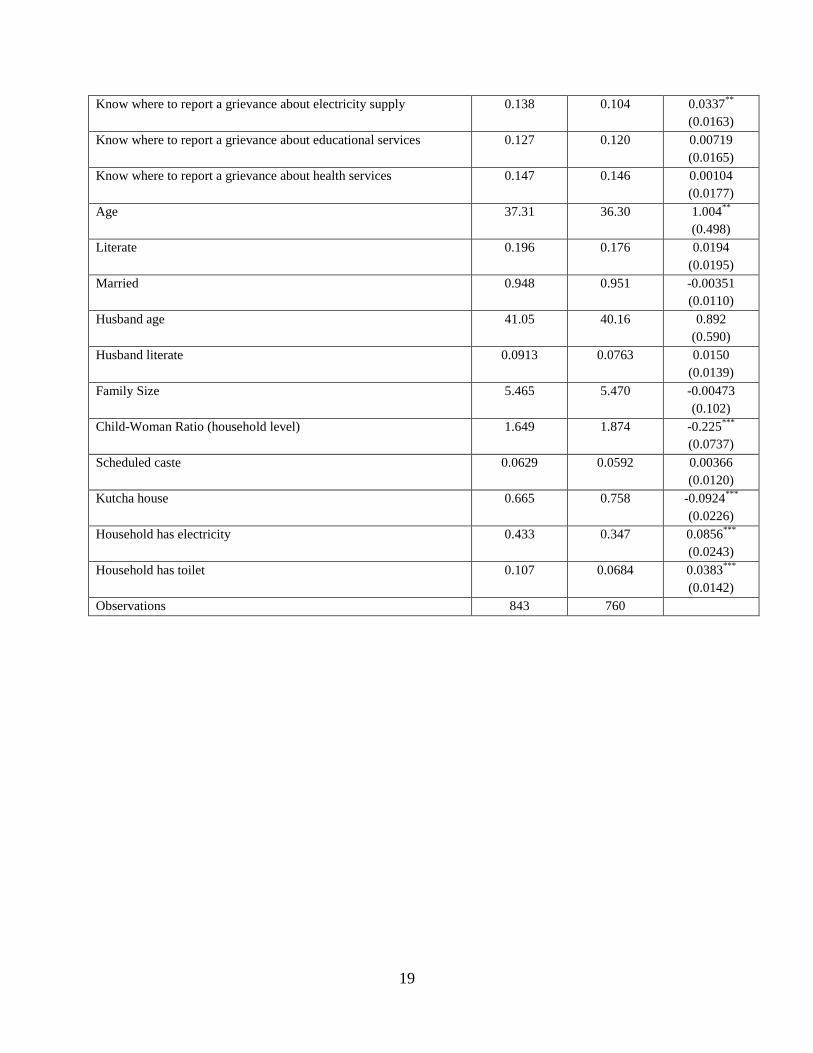

The estimates indicate that the villages do not systematically differ with respect to any

of the outcomes that of interest to us in this paper. There is no evidence that the treatment

villages had more SHGs prior to the arrival of SEWA. There is also no systematic difference in

11

The Gram Panchayat is the local governing body of a village or small town in India. It is the foundation of India’s

system of grass-roots governance. It is generally composed of 7 to 31 members and performs functions such as the

resolution of local disputes, the implementation of development schemes for the village, the establishment of

primary health centers and primary schools, arrangements for clean drinking water, drainage, construction and repair

of roads, development of SEWA Memberall-scale industries and opening of cooperative societies.

The Gram Sabha is composed of all men and women in the village who are above 18 years of age. Meetings of the

Gram Sabha are usually convened several times a year. In Rajasthan they are typically held twice a year. The agenda

typically includes the annual budget, the development schemes for the village, and where necessary, individual

difficulties or grievances of the people of a village. The Gram Sabha plays a critical role in holding government

institutions, particularly local Panchayat members, accountable. 12

Note that the two sets of controls villages are included as one major group because there was no SEWA presence

to distinguish them in 2007.

9

women’s schooling, labor-force participation or involvement in SHGs prior to the program.

There is however, evidence that SEWA villages have better infrastructure than non-SEWA

villages, with a greater proportion of households reporting electricity, toilets and use of pucca

building materials. SEWA villages also appear to have more women who already know about

where to report two particular types of grievances (water and electricity). This could be driven by

a difference in the types of services (or delivery systems) in the two types of villages. It could

also be driven by the quality of local governance. We address this issue by including village-

level fixed effects in all the regressions performed in the analysis, controlling for socio-economic

status by including controls for the variables where we observe the differences, and finally,

considering a broad set of dependent variables for each category of outcomes.

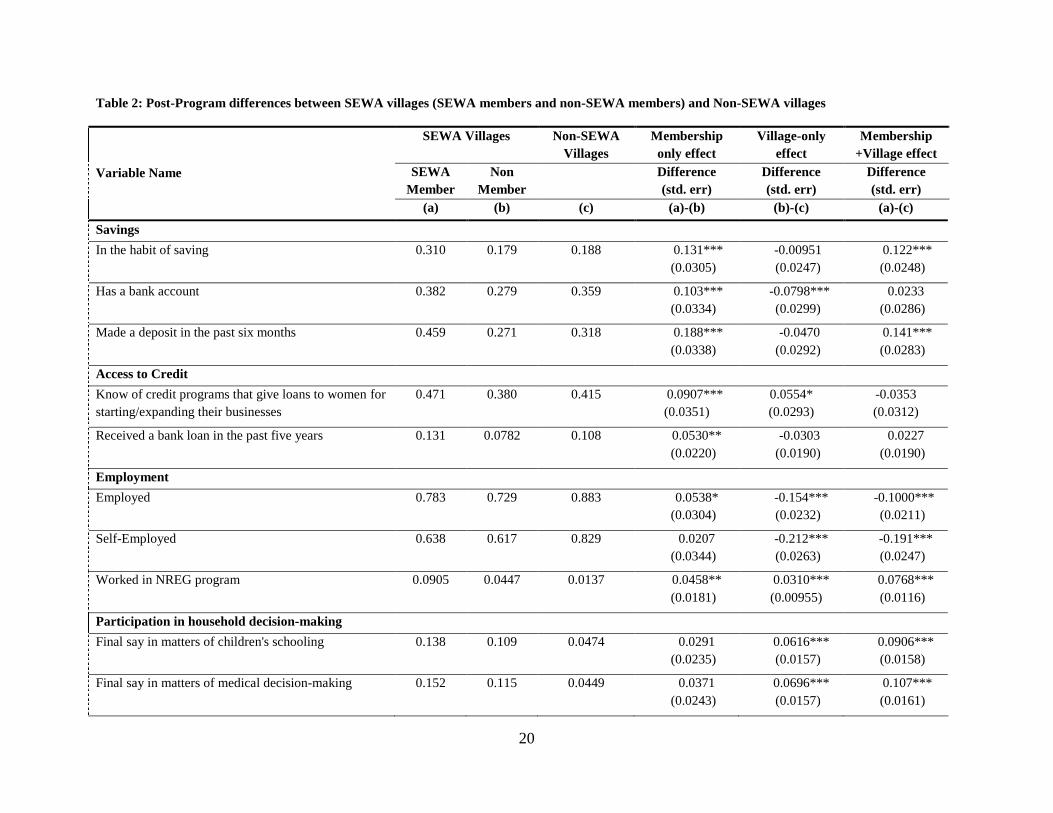

The second step of our analysis involves the simple tabulation of differences between the

three groups of households after the intervention was conducted. We define three groups of

households – (a) SHG members in villages in which SEWA was active; (b) Non-SHG members

in villages in which SEWA was active; and (c) Non-SEWA villages. The means of various

outcome variables are presented in Table 2. The difference between (a) and (b) provides the

unconditional average impact of SEWA membership for households who reside in SEWA

villages. We call this the ―SHG membership effect‖. It captures a household’s private benefits

from participation in a SHG by comparing these housesholds with other households in the same

village who did not participate in the SHG. The results in Table 2 suggest that the private returns

associated with SEWA membership are most significant for financial outcomes such as the

tendency to save, make deposit into bank accounts and manage savings. There is also a

beneficial effect of membership on employment and participation in the Indian government’s

National Rural Employment Guarantee (NREG) program. There is little-to-no effect on

participation in local government institutions but a large and significant effect on knowledge of

how to address grievances about water/sanitation, road conditions, electricity, educational

services and health services.

The difference between (b) and (c) provides the unconditional average impact of having

SHGs in the village for households who did not directly participate in these groups. We call this

the ―village spillover effect‖ since it focuses entirely on non-members and provides an estimate

of the village-level ―spillovers‖ of SHGs. The evidence on these village-spillover effects is

mixed. For non-members, the presence of SHGs in the village has little effect on savings

10

behaviors, or the likelihood of receiving a loan. But there is a positive effect on the knowledge

of receiving a loan, a modest effect on participation in the NREG program and a modest effect

on participation in local political institutions. There is a significant positive impact on

participation in household decision-making and the knowledge of where to report grievances

regarding water/sanitation, electricity and health services. Non-SHG members in treated villages

were more likely to report a greater say in matters of children’s education, medical decision-

making and the use of family-planning. Some types of outcomes however, were actually weaker

than in the control villages. Compared to villages where there was no program at all, non-SHG

members in treated villages were less likely to manage their savings themselves or with their

spouses. They were also less likely to be employed, self-employed or cultivate their own land.

This however could be driven by the fact that women who were highly motivated to save,

participate in the labor-force and participate in local governance in fact participated in the SHG

program, which was not offered in the control villages.

The table also presents the difference between (a) and (c), which is the combined effect

of SHG membership and residence in a SEWA village. This is a measure of the private as well as

the social returns from participating in SHGs compared to villages which receives no treatment

at all. This overall effect is presented in the final column of Table 2. Note that the overall effect

is simply a combination of the two above-described effects. We turn now to a more rigorous

evaluation of these differences.

Regression Results

Simple aggregate estimates of the program’s effect on households can be derived from a

regression of the following form:

Yhvt = β0 + β1 SEWA Memberh + β2 SEWA Villagev + β4X + μv + ejt

h=1,2,…, 1602 for households, v = 1, 2, ..., 38, for villages, t=2007, 2009

where Yhvt is the outcome of interest for household h in village v in time period t, SEWAMember

takes value 1 if the woman interviewed in h is a member of SEWA, SEWA Village takes value 1

if the village is a village in which SEWA is present, X is a vector of control variables, μv is a

village-specific fixed-effect and ejt is the error. We use this specification primarily because it

11

captures both types of randomized interventions – selection of SEWA villages and selection of

SHG members within villages – with simplicity. Control variables include measures of a

woman’s age, literacy, marital status, husband’s age and literacy, family size, the child-woman

ratio (dependency ratio for a woman), a dummy for belonging to a scheduled-caste, a dummy for

home-ownership, a dummy for a kutcha (lack of solid) housing structure and a dummy for the

presence of a toilet. We exclude measures of income and assets out of concerns of endogeneity.

We also include a dummy variable that takes value 1 if the household was in the endline survey

and 0 in the baseline survey. Results are discussed below. We group them based on the type of

outcome that is being considered.

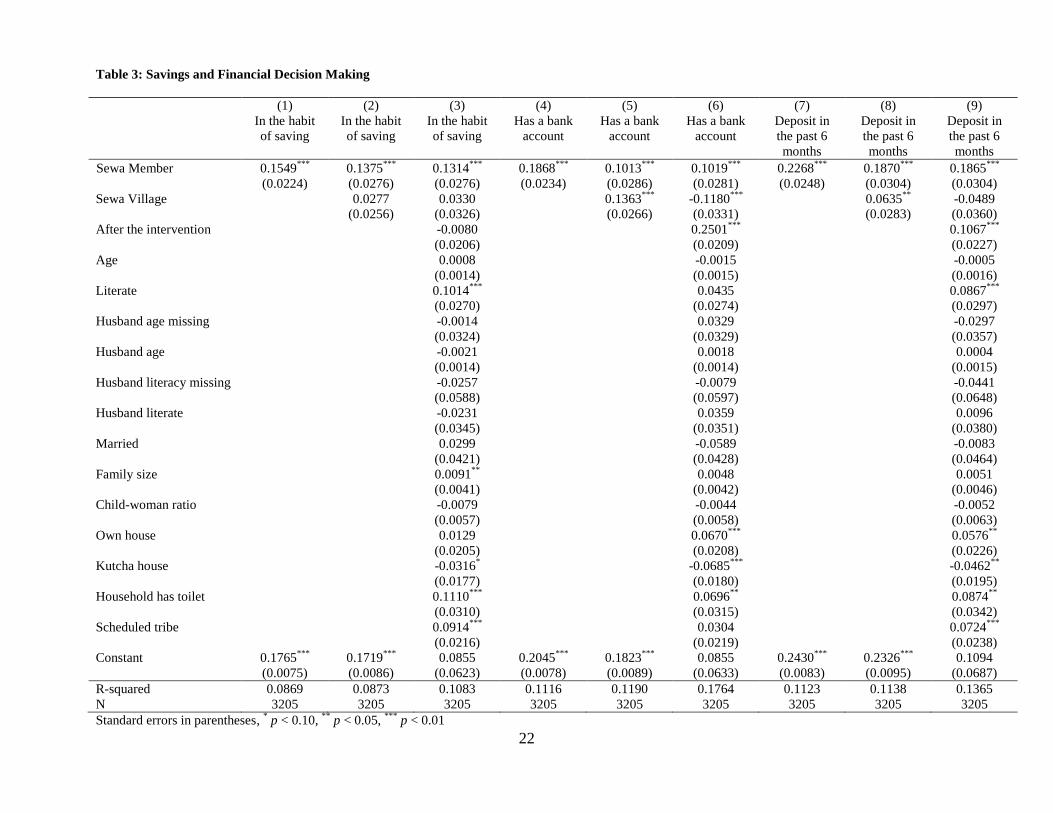

Saving and Financial Decision-Making (Error! Reference source not found.): The

positive and significant coefficient of the SEWA Member dummy, in both the regressions with

controls and those without, suggests that relative to non-members, SEWA members are 13

percent more likely save, 10 percent more likely to have bank accounts and 19 percent more

likely to make deposits into their accounts within the six months preceding the survey. All these

estimates are statistically significant at the 1% level. The broader effects of the program at the

village level – as measured by the variable SEWA Village – are also positive and statistically

significant for ownership of bank accounts and deposits into the bank accounts. In the regression

for the variable ―Deposit in the past 6 months‖, the coefficient for SEWA Village, is however

about one-third the magnitude that of SEWA Member. We interpret this as evidence that while

non-participants in SEWA villages may gain access to the means to save, and they are even more

likely than SEWA members to open bank accounts, but their actual savings do not increase as

significantly as the SEWA members. These benefits are restricted to members of the SHG

groups.

Access to Credit (Error! Reference source not found.): We have already shown (Table 1)

that prior to the entrance of SEWA, women in the treatment and control villages did not differ in

any statistically significant way with respect to their knowledge and access to credit. The results

in Error! Reference source not found. however, suggest that the treatment had significant effects.

Regression results further confirm that SEWA members were about 8 percent more likely to

know of their opportunities for credit in the local area and 6 percent more likely to have been

recipients of a bank loan, and this effect is statistically significant at the 1% level. There is no

12

broad village-level effect. Women who resided in SEWA villages but did not participate in the

program received no statistically significant benefit in terms of either knowledge or the receipts

of loans. We infer from this that access to credit remains concentrated among women who are

members of these groups and the knowledge of credit opportunities does not easily diffuse

beyond the group.

Employment (Table 5): Participation in SEWA’s SHGs does not seem to have any

positive effect on the likelihood of members reporting that they are employed or self-employed.

In results not shown here, we also find no evidence that members are more likely to cultivate

their own farms. The village-level spillover effect with respect to these employment measures is

puzzlingly negative and statistically significant.13

It is interesting to observe that SEWA

membership is associated with a 4 percent greater likelihood of being employed by the

government-led NREG scheme, even though overall employment in the scheme declined

between 2007 and 2009. This may suggest that SHG members are more aware of employment

opportunities offered through this program, and are better able to benefit from government

services.14

The village-level effect of this program is not statistically significant. Interestingly,

female literacy is associated with neither increased employment nor with an increased effect at

the level of the individual or the village. This is possibly driven by the fact that job-opportunities

for women in this area are limited to unskilled labor and the returns to literacy are quite low in

the labor market.

Participation in Household Decision-Making (Error! Reference source not found.): Note

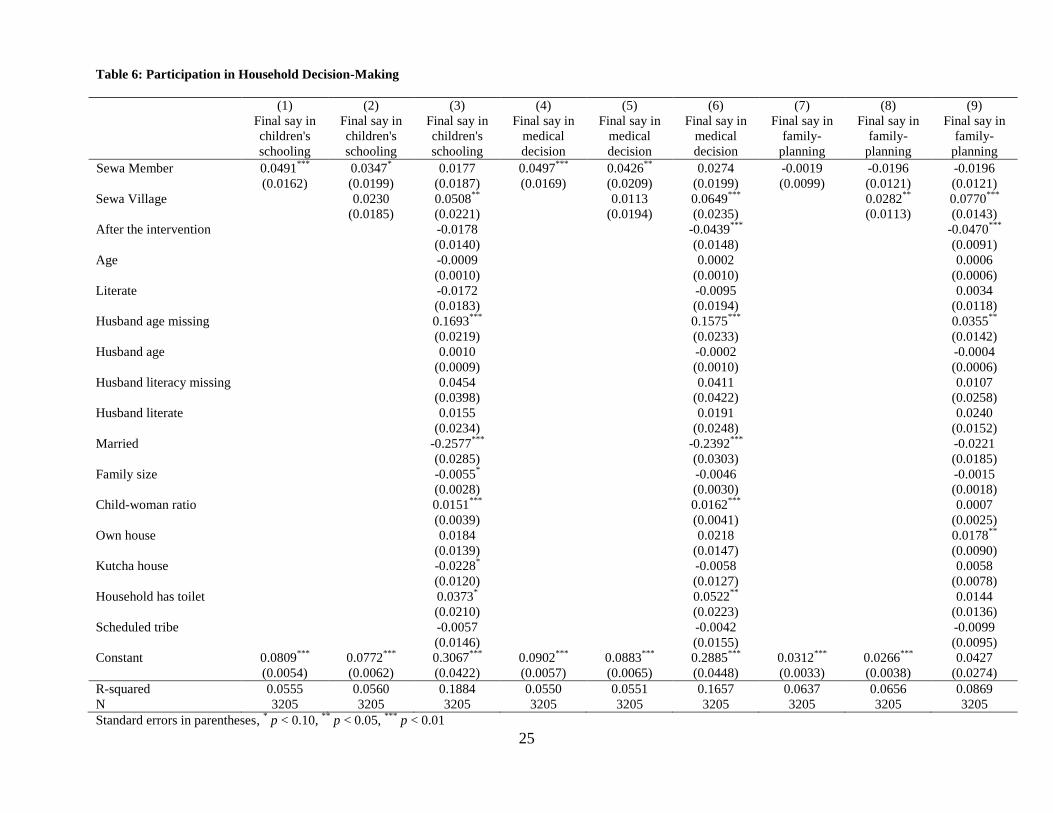

that that participation in SHGs is associated with increases in decision-making authority in two

of the three indicators, but the effect diminishes with the inclusion of control variables in even

those cases. Interestingly, we also observe a village-level effect that is positive and statistically

13

One possible explanation for this could have also been an increase in participation in SEWA’s vocational training

programs in the village. Individuals who were not invited to participate in SHGs may have been more inclined to

participate in these programs, resulting in a lowering of their labor supply. We explore this more carefully in future

work and in upcoming field visits. 14

An alternative explanation of the increased participation by SEWA participants in the NREG scheme is that there

is non-random placement of the NREG program and they are concentrated in the same villages as the SEWA

programs, perhaps as a result of better infrastructure in these villages. Our regressions include village-level fixed

effects and thus capture village-level characteristics that remained unchanged over time. If some SEWA villages

experienced improvements in infrastructure during the two years of the study, and were more likely to benefit from

government programs, the observed relationship may be upward biased and thus spurious. Our evidence suggests

that there was no deliberate effort by the government to prioritize implementation of NREG over SEWA villages. In

fact the program was implemented simultaneously in the entire district. In future work we plan to explore this more

carefully. For now we simply highlight the possibility that the presence of SHGs in SEWA villages may have led to

an improvement in the implementation of the same NREG scheme that was in place in all the districts villages.

13

significant for all three measures. The coefficient for the variable SEWA Village is positive and

statistically significant at the 1 percent level, indicating that women who reside in SEWA

villages were 5—8 percent more likely to participate in key household decisions regardless of

whether or not they participated in SHGS. One explanation of this finding is that the presence of

SHGs that are backed by a major NGO can increase the salience of issues such as female

empowerment in the community and trigger subtle changes in attitude. The coefficients of the

control variables illustrate that women’s literacy and socio-economic status has at best a weak

impact on these measures of well-being. Again, this is perhaps suggestive of the fact that SEWA

SHGs are structured to target women who are poor and are designed to be impactful in these

circumstances.

Participation in Local Government (Table 7 and Table 8): We begin by focusing on

women’s awareness of the most salient of the local government institutions in rural India: The

Gram Sabha and Gram Panchayat. We also examine the likelihood of their interaction with a

Panchayat member. Regression results are presented in Error! Reference source not found.. Note

that the coefficient for SEWA Member is positive and significant in the regression of knowledge

of the Gram Sabha. Women who are members of SEWA SHGs are about 10% more likely to

know about Gram Sabhas than non-members. There is however, no statistically discernible

impact of participation on knowledge of the Gram Panchayat (columns 4—6) or interaction with

its members (columns 7—9). The main reason for this could of course be that knowledge of the

Gram Panchayat was already very high (in excess of 70 percent) prior to the intervention.

Knowledge of the Gram Sabha, a much more recent institution, was a lot lower (around 30

percent in all the villages). It is also interesting to note that literate women are more likely to

know about both entities and are also more likely to interact with Panchayat members.

Interestingly, there is no village-level effect on knowledge of any of these indicators.

In another measure of women’s participation in local government, we explore women’s

knowledge of where to report five types of grievances: water/sanitation, road conditions,

electricity supply, education services and health services. We expect SEWA membership to have

direct as well as spillover effects. Indeed, the results confirm this. SEWA membership is

associated with a 6—15% increase in the likelihood of knowing where to report a grievance on

any of these matters, and the results are statistically significant in all cases. Table 8 presents

regressions on a measure that is defined as the sum of all five grievance measures. Results

14

confirm that SEWA membership has a positive and significant effect on women’s scores. There

is however, no evidence in this case of a broad village effect. The variable SEWA Village

remains statistically insignificant. This suggests that specific types of knowledge – such as

knowledge of credit or knowledge of where to report grievances – are likely concentrated within

SHGs and may take longer than the time-span of this study to diffuse into the community.

Overall the results suggest that participation in SHGs was associated with some

significant effects both at the level of participants, as well as the broader level of the village. The

effects we observe are much smaller than Deininger and Liu (2009), but we attribute this to the

fact that SHGs we study here were significantly different. Moreover, SHGs were far less

prevalent before the intervention and the area has lower levels of socio-economic development,

higher levels of gender inequality and worse indicators of governance than Southern India

(United Nations, 2000; 2010). SHGs in this environment may simply take longer to have impact.

6. Conclusion

This paper explores the impact of participation in SHGs on a variety of measures of

women’s well-being. With the help of the Self-Employed Women’s Association (SEWA) of

India, women in the Dugarpur district of Rajasthan were organized into SHGs in late 2007. Two

years later, participants were surveyed, along with women in two control groups, to examine the

impact of participation. Control groups included non-participants in the same village at the SHGs

as well as women in villages where there were no SHGs. Comparisons between these groups

suggest that SHGs had several effects. Participating women saved more, were more likely to

have bank accounts and were more likely to participate in the management of their savings. They

were also more knowledgeable about credit opportunities and more likely to take loans. They are

also more likely to have a greater say in household decisions, participate in government

programs and know which authorities to report grievances about government services such as

water/sanitation, roads, electricity supply and educational and health services. There is also

evidence that some of these benefits spilled over into the greater village community. Women

who resided in the same village as the SHG, including those who did not participate in the SHGs,

experienced an increase in decision-making authority within the household.

These results have two major policy implications. First, they confirm that SHGs – when

appropriately designed with a careful consideration of local conditions -- can indeed promote

collective action at the local level. Second, the results confirm that placing women at the center

15

of development policy has broad benefits. The opportunity to form groups and take collective

action is of course valuable in its own right, but it also has instrumental value in its tendency to

spill over into the community.

16

References

1. Alesina, Alberto and Eliana La Ferrara, 2000, "Participation in Heterogeneous

Communities," The Quarterly Journal of Economics, MIT Press, vol. 115(3), pages 847-

904, August.

2. Bardhan, Pranab, 2002, ―Decentralization of government and development‖, Journal of

Economic Perspectives, Vol 16, No. 4, pp. 185—205.

3. Basu, P. and P. Srivastava. 2005. "Scaling-up Microfinance for India's Rural Poor."

World Bank Policy Research Working Paper 3646. Washington, DC: World Bank.

4. Bhatia, Navin, 2007, ―Revisiting bank-linked Self Help Groups (SHGs) - A study of

Rajasthan State‖, Reserve Bank of India Occasional Papers Vol. 28, No. 2, Monsoon

2007.

5. Buvinic M. and E. King, 2007, ―Smart Economics‖, Finance and Development, Volume

44, Number 2,

6. Chen, Martha, Renana Jhabvala, Ravi Kanbur and Carol Richards, 2006, Membership

Based Organizations of the Poor: Concepts, Experience and Policy, Routledge

7. Deininger, K. and Y. Liu, 2009, "Economic and social impacts of self-help groups in

India," World Bank Policy Research Working Paper. Washington, DC: World Bank.

8. Garikipati, S., 2008, "The impact of lending to women on hosuehold vulnerability and

women's empowerment: Evidence from India," World Development forthcoming.

9. Government of India, 2009, District Human Development Report: Dungarpur, By

Government of Rajasthan and Institute of Development Studies, Jaipur

10. La Ferrara, Eliana, 2003, "Kin Groups and Reciprocity: A Model of Credit Transactions

in Ghana," American Economic Review, American Economic Association, vol. 93(5),

pages 1730—1751.

17

11. Mansuri , Ghazala and Vijayendra Rao, 2004, ―Community Based (and Driven)

Development: A Critical Review,‖ The World Bank Research Observer, vol. 19, no. 1,

pp. 1-39

12. Nair, A, 2005, "Sustainability of microfinance self help groups in India: would federating

help?" World Bank Policy Research Working Paper 3516. Washington, DC: World Bank.

13. Rao, Vijayendra, and Ana Maria Ibanez, 2005, ―The Social Impact of Social Funds In

Jamaica: A "Participatory Econometric" Analysis of Participation, Targeting, and

Collective Action in Community-Driven Development‖, Journal of Development Studies,

Vol. 41, Number 5, pp: 788-838.

14. Rao, Vijayendra, 2005, ―Symbolic Public Goods and the Coordination of Collective

Action: A Comparison of Local Development in India and Indonesia," Chapter 10 in

Pranab Bardhan and Isha Ray (edited) The Contested Commons: Conversations Between

Economists and Anthropologists, Blackwell Publishing Ltd, 2008

15. Schultz, T. Paul, 1995, Investments in Women’s Human Capital, University of Chicago

Press.

16. Schultz, T. Paul, 2001a, ―Women's Role in the Agricultural Household Bargaining and

Human Capital Investments‖ In: Agricultural and Resource Economics Handbook, Vol.

1.

17. Schultz, T. Paul, 2001b, Why Governments Should Invest More to Educate Girls, World

Development, 30(2): 207-225.

18. NABARD, 2010, The State of Microfinance in India, Available at: http://nabard.org/

(Accessed on April 5th

, 2010)

19. United Nations Development Program, 2000, Human Development in South Asia: The

Gender Question, Oxford University Press.

20. World Bank, 2002, A Sourcebook for Poverty Reduction Strategy Papers, Volumes 1 and

2, Edited by Jeni Klugman.

18

Table 1: Pre-program differences between SEWA Villages and Non-SEWA Villages

SEWA

Villages

Non-SEWA

Villages

Difference

(se)

Participation in any type of membership based-organization that

holds regular meetings

0.132 0.149 -0.0170

(0.0173)

In the habit of saving 0.163 0.191 -0.0283

(0.0190)

Has a bank account 0.123 0.101 0.0221

(0.0158)

Made a deposit in the past 6 months 0.210 0.193 0.0165

(0.0201)

Manage savings (either alone or with husband) 0.216 0.199 0.0172

(0.0203)

Know of credit programs that give loans to women for starting or

expanding their businesses

0.240

0.237 0.00278

(0.0213)

Received a bank loan in the past 5 years 0.0759 0.0921 -0.0162

(0.0138)

Employed 0.821 0.800 0.0209

(0.0196)

Self-Employed 0.700 0.714 -0.0146

(0.0228)

Cultivate own farm 0.714 0.696 0.0181

(0.0228)

Worked in NREG program 0.117 0.0776 0.0398***

(0.0149)

Final say in matters of children's schooling 0.0913 0.0868 0.00450

(0.0143)

Final say in matters of medical decision-making 0.0973 0.112 -0.0146

(0.0153)

Final say in matters of family-planning 0.0225 0.0553 -0.0327***

(0.00954)

Know of the Gram Sabha 0.399 0.405 -0.00669

(0.0245)

Ever attended Gram Sabha 0.0439 0.0368 0.00705

(0.00987)

Know about Gram Panchayat 0.706 0.703 0.00318

(0.0228)

Know a particular member of the Gram Panchayat 0.380 0.355 0.0243

(0.0241)

Interact with Gram Panchayat members 0.102 0.109 -0.00719

(0.0154)

Know where to report a grievance about water/sanitation 0.190 0.154 0.0359*

(0.0189)

Know where to report a grievance about road conditions 0.147 0.126 0.0208

(0.0172)

19

Know where to report a grievance about electricity supply 0.138 0.104 0.0337**

(0.0163)

Know where to report a grievance about educational services 0.127 0.120 0.00719

(0.0165)

Know where to report a grievance about health services 0.147 0.146 0.00104

(0.0177)

Age 37.31 36.30 1.004**

(0.498)

Literate 0.196 0.176 0.0194

(0.0195)

Married 0.948 0.951 -0.00351

(0.0110)

Husband age 41.05 40.16 0.892

(0.590)

Husband literate 0.0913 0.0763 0.0150

(0.0139)

Family Size 5.465 5.470 -0.00473

(0.102)

Child-Woman Ratio (household level) 1.649 1.874 -0.225***

(0.0737)

Scheduled caste 0.0629 0.0592 0.00366

(0.0120)

Kutcha house 0.665 0.758 -0.0924***

(0.0226)

Household has electricity 0.433 0.347 0.0856***

(0.0243)

Household has toilet 0.107 0.0684 0.0383***

(0.0142)

Observations 843 760

20

Table 2: Post-Program differences between SEWA villages (SEWA members and non-SEWA members) and Non-SEWA villages

Variable Name

SEWA Villages Non-SEWA

Villages

Membership

only effect

Village-only

effect

Membership

+Village effect

SEWA

Member

Non

Member

Difference

(std. err)

Difference

(std. err)

Difference

(std. err)

(a) (b) (c) (a)-(b) (b)-(c) (a)-(c)

Savings

In the habit of saving

0.310 0.179 0.188 0.131***

(0.0305)

-0.00951

(0.0247)

0.122***

(0.0248)

Has a bank account

0.382 0.279 0.359 0.103***

(0.0334)

-0.0798***

(0.0299)

0.0233

(0.0286)

Made a deposit in the past six months

0.459 0.271 0.318 0.188***

(0.0338)

-0.0470

(0.0292)

0.141***

(0.0283)

Access to Credit

Know of credit programs that give loans to women for

starting/expanding their businesses

0.471 0.380 0.415 0.0907***

(0.0351)

0.0554*

(0.0293)

-0.0353

(0.0312)

Received a bank loan in the past five years

0.131 0.0782 0.108 0.0530**

(0.0220)

-0.0303

(0.0190)

0.0227

(0.0190)

Employment

Employed

0.783 0.729 0.883 0.0538*

(0.0304)

-0.154***

(0.0232)

-0.1000***

(0.0211)

Self-Employed

0.638 0.617 0.829 0.0207

(0.0344)

-0.212***

(0.0263)

-0.191***

(0.0247)

Worked in NREG program

0.0905 0.0447 0.0137 0.0458**

(0.0181)

0.0310***

(0.00955)

0.0768***

(0.0116)

Participation in household decision-making

Final say in matters of children's schooling 0.138 0.109 0.0474 0.0291

(0.0235)

0.0616***

(0.0157)

0.0906***

(0.0158)

Final say in matters of medical decision-making 0.152 0.115 0.0449 0.0371

(0.0243)

0.0696***

(0.0157)

0.107***

(0.0161)

21

Final say in matters of family-planning

0.0317 0.0531 0.00623 -0.0214

(0.0141)

0.0468***

(0.00895)

0.0254***

(0.00723)

Participation in political institutions

Know of the Gram Sabha

0.403 0.318 0.274 0.0843**

(0.0341)

0.0441

(0.0288)

0.128***

(0.0274)

Know about Gram Panchayat

0.794 0.796 0.791 -0.00197

(0.0287)

0.00557

(0.0258)

0.00359

(0.0241)

Interact with member of the Gram Panchayat

0.120 0.0922 0.0948 0.0277

(0.0220)

-0.00258

(0.0186)

0.0251

(0.0181)

Know where to report a grievance about

water/sanitation

0.423 0.349 0.246 0.0739**

(0.0346)

0.104***

(0.0283)

0.177***

(0.0269)

Know where to report a grievance about road

conditions

0.310 0.221 0.253 0.0893**

(0.0314)

-0.0324

(0.0273)

0.0568**

(0.0264)

Know where to report a grievance about electricity

supply

0.477 0.385 0.273 0.0919***

(0.0352)

0.112***

(0.0292)

0.204***

(0.0276)

Know where to report a grievance about educational

services

0.222 0.137 0.147 0.0848***

(0.0274)

-0.0103

(0.0223)

0.0746***

(0.0224)

Know where to report a grievance about health

services

0.183 0.148 0.107 0.0352

(0.0266)

0.0408**

(0.0206)

0.0760***

(0.0201)

Number of observations 442 358 802

22

Table 3: Savings and Financial Decision Making

(1) (2) (3) (4) (5) (6) (7) (8) (9)

In the habit

of saving

In the habit

of saving

In the habit

of saving

Has a bank

account

Has a bank

account

Has a bank

account

Deposit in

the past 6

months

Deposit in

the past 6

months

Deposit in

the past 6

months

Sewa Member 0.1549***

(0.0224)

0.1375***

(0.0276)

0.1314***

(0.0276)

0.1868***

(0.0234)

0.1013***

(0.0286)

0.1019***

(0.0281)

0.2268***

(0.0248)

0.1870***

(0.0304)

0.1865***

(0.0304)

Sewa Village

0.0277

(0.0256)

0.0330

(0.0326)

0.1363***

(0.0266)

-0.1180***

(0.0331)

0.0635**

(0.0283)

-0.0489

(0.0360)

After the intervention

-0.0080

(0.0206)

0.2501***

(0.0209)

0.1067***

(0.0227)

Age

0.0008

(0.0014)

-0.0015

(0.0015)

-0.0005

(0.0016)

Literate

0.1014***

(0.0270)

0.0435

(0.0274)

0.0867***

(0.0297)

Husband age missing

-0.0014

(0.0324)

0.0329

(0.0329)

-0.0297

(0.0357)

Husband age

-0.0021

(0.0014)

0.0018

(0.0014)

0.0004

(0.0015)

Husband literacy missing

-0.0257

(0.0588)

-0.0079

(0.0597)

-0.0441

(0.0648)

Husband literate

-0.0231

(0.0345)

0.0359

(0.0351)

0.0096

(0.0380)

Married

0.0299

(0.0421)

-0.0589

(0.0428)

-0.0083

(0.0464)

Family size

0.0091**

(0.0041)

0.0048

(0.0042)

0.0051

(0.0046)

Child-woman ratio

-0.0079

(0.0057)

-0.0044

(0.0058)

-0.0052

(0.0063)

Own house

0.0129

(0.0205)

0.0670***

(0.0208)

0.0576**

(0.0226)

Kutcha house

-0.0316*

(0.0177)

-0.0685***

(0.0180)

-0.0462**

(0.0195)

Household has toilet

0.1110***

(0.0310)

0.0696**

(0.0315)

0.0874**

(0.0342)

Scheduled tribe

0.0914***

(0.0216)

0.0304

(0.0219)

0.0724***

(0.0238)

Constant 0.1765***

(0.0075)

0.1719***

(0.0086)

0.0855

(0.0623)

0.2045***

(0.0078)

0.1823***

(0.0089)

0.0855

(0.0633)

0.2430***

(0.0083)

0.2326***

(0.0095)

0.1094

(0.0687)

R-squared 0.0869 0.0873 0.1083 0.1116 0.1190 0.1764 0.1123 0.1138 0.1365

N 3205 3205 3205 3205 3205 3205 3205 3205 3205

Standard errors in parentheses, * p < 0.10,

** p < 0.05,

*** p < 0.01

23

Table 4: Access to credit

(1) (2) (3) (4) (5) (6)

Know of programs

that give loans to

women

Know of programs

that give loans to

women

Know of programs

that give loans to

women

Received a bank

loan in the past 5

years

Received a bank

loan in the past 5

years

Received a bank

loan in the past 5

years

Sewa Member 0.1991***

(0.0255)

0.0908***

(0.0313)

0.0755**

(0.0311)

0.0667***

(0.0166)

0.0581***

(0.0204)

0.0559***

(0.0206)

Sewa Village

0.1727***

(0.0291)

0.0182

(0.0367)

0.0137

(0.0190)

0.0097

(0.0243)

After the intervention

0.1531***

(0.0232)

0.0005

(0.0154)

Age

-0.0010

(0.0016)

0.0008

(0.0011)

Literate

0.1448***

(0.0303)

0.0211

(0.0201)

Husband age missing

-0.0312

(0.0364)

-0.0257

(0.0241)

Husband age

0.0001

(0.0016)

-0.0004

(0.0010)

Husband literacy missing

0.0152

(0.0661)

0.0002

(0.0438)

Husband literate

-0.0431

(0.0388)

0.0690***

(0.0257)

Married

-0.0236

(0.0474)

-0.0195

(0.0314)

Family size

0.0064

(0.0047)

0.0050

(0.0031)

Child-woman ratio

0.0061

(0.0065)

-0.0001

(0.0043)

Own house

0.0119

(0.0230)

0.0063

(0.0153)

Kutcha house

-0.0422**

(0.0199)

-0.0266**

(0.0132)

Household has toilet

0.0453

(0.0349)

-0.0074

(0.0232)

Scheduled tribe

0.0995***

(0.0243)

0.0099

(0.0161)

Constant 0.3030***

(0.0085)

0.2748***

(0.0097)

0.1728**

(0.0701)

0.0866***

(0.0055)

0.0843***

(0.0064)

0.0645

(0.0465)

R-squared 0.1503 0.1598 0.1901 0.0811 0.0813 0.0911

N 3205 3205 3205 3205 3205 3205

Standard errors in parentheses. * p < 0.10,

** p < 0.05,

*** p < 0.01

24

Table 5: Employment

(1) (2) (3) (4) (5) (6) (7) (8) (9)

Employed Employed Employed Self-

Employed

Self-

Employed

Self-

Employed

Worked in

NREG

program

Worked in

NREG

program

Worked in

NREG

program

Sewa Member -0.0271

(0.0216)

0.0433

(0.0265)

0.0310

(0.0264)

-0.0477*

(0.0249)

0.0102

(0.0306)

0.0089

(0.0305)

-0.0141

(0.0141)

0.0447***

(0.0172)

0.0429**

(0.0173)

Sewa Village

-0.1123***

(0.0247)

-0.1671***

(0.0312)

-0.0924***

(0.0285)

-0.1833***

(0.0361)

-0.0939***

(0.0160)

-0.0183

(0.0204)

After the intervention

0.0594***

(0.0197)

0.0916***

(0.0228)

-0.0738***

(0.0129)

Age

-0.0020

(0.0014)

-0.0040**

(0.0016)

-0.0001

(0.0009)

Literate

-0.0247

(0.0257)

-0.0438

(0.0298)

-0.0039

(0.0168)

Husband age missing

-0.0522*

(0.0309)

-0.0441

(0.0358)

0.0248

(0.0202)

Husband age

0.0023*

(0.0013)

0.0042***

(0.0015)

0.0008

(0.0009)

Husband literacy missing

0.0369

(0.0561)

-0.0256

(0.0650)

-0.0477

(0.0367)

Husband literate

-0.0345

(0.0329)

-0.0580

(0.0382)

-0.0075

(0.0216)

Married

-0.0045

(0.0402)

0.0682

(0.0466)

-0.0195

(0.0263)

Family size

0.0044

(0.0040)

0.0056

(0.0046)

-0.0029

(0.0026)

Child-woman ratio

-0.0005

(0.0055)

-0.0083

(0.0064)

0.0121***

(0.0036)

Own house

0.0442**

(0.0195)

0.0432*

(0.0226)

0.0318**

(0.0128)

Kutcha house

0.0010

(0.0169)

-0.0058

(0.0196)

-0.0088

(0.0111)

Household has toilet

-0.1900***

(0.0296)

-0.1489***

(0.0343)

-0.0349*

(0.0194)

Scheduled tribe

0.0781***

(0.0206)

0.0460*

(0.0239)

0.0223*

(0.0135)

Constant 0.8197***

(0.0072)

0.8380***

(0.0082)

0.7174***

(0.0595)

0.7245***

(0.0083)

0.7396***

(0.0095)

0.5770***

(0.0689)

0.0722***

(0.0047)

0.0875***

(0.0054)

0.0548

(0.0389)

R-squared 0.1027 0.1086 0.1417 0.1148 0.1177 0.1460 0.1246 0.1342 0.1540

N 3205 3205 3205 3205 3205 3205 3205 3205 3205

Standard errors in parentheses, * p < 0.10,

** p < 0.05,

*** p < 0.01

25

Table 6: Participation in Household Decision-Making

(1) (2) (3) (4) (5) (6) (7) (8) (9)

Final say in

children's

schooling

Final say in

children's

schooling

Final say in

children's

schooling

Final say in

medical

decision

Final say in

medical

decision

Final say in

medical

decision

Final say in

family-

planning

Final say in

family-

planning

Final say in

family-

planning

Sewa Member 0.0491***

(0.0162)

0.0347*

(0.0199)

0.0177

(0.0187)

0.0497***

(0.0169)

0.0426**

(0.0209)

0.0274

(0.0199)

-0.0019

(0.0099)

-0.0196

(0.0121)

-0.0196

(0.0121)

Sewa Village

0.0230

(0.0185)

0.0508**

(0.0221)

0.0113

(0.0194)

0.0649***

(0.0235)

0.0282**

(0.0113)

0.0770***

(0.0143)

After the intervention

-0.0178

(0.0140)

-0.0439***

(0.0148)

-0.0470***

(0.0091)

Age

-0.0009

(0.0010)

0.0002

(0.0010)

0.0006

(0.0006)

Literate

-0.0172

(0.0183)

-0.0095

(0.0194)

0.0034

(0.0118)

Husband age missing

0.1693***

(0.0219)

0.1575***

(0.0233)

0.0355**

(0.0142)

Husband age

0.0010

(0.0009)

-0.0002

(0.0010)

-0.0004

(0.0006)

Husband literacy missing

0.0454

(0.0398)

0.0411

(0.0422)

0.0107

(0.0258)

Husband literate

0.0155

(0.0234)

0.0191

(0.0248)

0.0240

(0.0152)

Married

-0.2577***

(0.0285)

-0.2392***

(0.0303)

-0.0221

(0.0185)

Family size

-0.0055*

(0.0028)

-0.0046

(0.0030)

-0.0015

(0.0018)

Child-woman ratio

0.0151***

(0.0039)

0.0162***

(0.0041)

0.0007

(0.0025)

Own house

0.0184

(0.0139)

0.0218

(0.0147)

0.0178**

(0.0090)

Kutcha house

-0.0228*

(0.0120)

-0.0058

(0.0127)

0.0058

(0.0078)

Household has toilet

0.0373*

(0.0210)

0.0522**

(0.0223)

0.0144

(0.0136)

Scheduled tribe

-0.0057

(0.0146)

-0.0042

(0.0155)

-0.0099

(0.0095)

Constant 0.0809***

(0.0054)

0.0772***

(0.0062)

0.3067***

(0.0422)

0.0902***

(0.0057)

0.0883***

(0.0065)

0.2885***

(0.0448)

0.0312***

(0.0033)

0.0266***

(0.0038)

0.0427

(0.0274)

R-squared 0.0555 0.0560 0.1884 0.0550 0.0551 0.1657 0.0637 0.0656 0.0869

N 3205 3205 3205 3205 3205 3205 3205 3205 3205

Standard errors in parentheses, * p < 0.10,

** p < 0.05,

*** p < 0.01

26

Table 7: Participation in Local Governance

(1) (2) (3) (4) (5) (6) (7) (8) (9)

Know of the

Gram Sabha

Know of the

Gram Sabha

Know of the

Gram Sabha

Know of

Gram

Panchayat

Know about

Gram

Panchayat

Know about

Gram

Panchayat

Interact with

Panchayat

members

Interact with

Panchayat

members

Interact with

Panchayat

members

Sewa Member 0.0530**

(0.0270)

0.0942***

(0.0332)

0.0946***

(0.0328)

0.0492**

(0.0232)

-0.0126

(0.0285)

-0.0195

(0.0286)

0.0257

(0.0173)

0.0262

(0.0213)

0.0180

(0.0214)

Sewa Village

-0.0657**

(0.0308)

0.0521

(0.0388)

0.0986***

(0.0265)

0.0237

(0.0338)

-0.0008

(0.0198)

0.0275

(0.0252)

After the intervention

-0.1258***

(0.0245)

0.0711***

(0.0214)

-0.0268*

(0.0160)

Age

0.0008

(0.0017)

-0.0003

(0.0015)

0.0026**

(0.0011)

Literate

0.1789***

(0.0320)

0.0862***

(0.0279)

0.0752***

(0.0209)

Husband age missing

0.0062

(0.0385)

-0.0017

(0.0335)

0.0319

(0.0250)

Husband age

0.0011

(0.0017)

0.0019

(0.0014)

-0.0003

(0.0011)

Husband literacy

missing

0.0972

(0.0699)

0.0644

(0.0609)

-0.0184

(0.0455)

Husband literate

-0.0558

(0.0410)

0.0172

(0.0357)

0.0008

(0.0267)

Married

0.0701

(0.0501)

-0.0466

(0.0436)

0.0307

(0.0326)

Family size

0.0068

(0.0049)

0.0053

(0.0043)

-0.0037

(0.0032)

Child-woman ratio

0.0032

(0.0068)

0.0015

(0.0060)

0.0082*

(0.0044)

Own house

-0.0321

(0.0243)

-0.0268

(0.0212)

-0.0325**

(0.0158)

Kutcha house

-0.0980***

(0.0210)

-0.0548***

(0.0183)

-0.0321**

(0.0137)

Household has toilet

0.0445

(0.0369)

0.0037

(0.0321)

-0.0731***

(0.0240)

Scheduled tribe

-0.0251

(0.0257)

-0.0065

(0.0223)

0.0196

(0.0167)

Constant 0.3534***

(0.0090)

0.3641***

(0.0103)

0.2912***

(0.0741)

0.7417***

(0.0078)

0.7257***

(0.0089)

0.7019***

(0.0646)

0.0997***

(0.0058)

0.0999***

(0.0066)

0.0225

(0.0482)

R-squared 0.0908 0.0921 0.1331 0.1730 0.1767 0.1939 0.0714 0.0714 0.0858

N 3205 3205 3205 3205 3205 3205 3205 3205 3205

Standard errors in parentheses, * p < 0.10,

** p < 0.05,

*** p < 0.01

27

Table 8: Knowledge of whom to approach regarding grievances

(1) (2) (3)

Grievance Index Grievance Index Grievance Index

Sewa Member 0.1370***

0.0677***

0.0635***

(0.0168) (0.0206) (0.0203)

Sewa Village 0.1105***

0.0270

(0.0191) (0.0240)

After the intervention 0.0837***

(0.0151)

Age 0.0012

(0.0011)

Literate 0.0829***

(0.0198)

Husband age missing 0.0601**

(0.0238)

Husband age -0.0019*

(0.0010)

Husband literacy missing 0.0749*

(0.0431)

Husband literate 0.0207

(0.0253)

Married 0.0414

(0.0309)

Family size 0.0059*

(0.0030)

Child-woman ratio -0.0020

(0.0042)

Own house -0.0418***

(0.0150)

Kutcha house -0.0238*

(0.0130)

Household has toilet 0.1017***

(0.0228)

Scheduled tribe 0.0047

(0.0158)

Constant 0.1749***

0.1569***

0.1161**

(0.0056) (0.0064) (0.0458)

R-squared 0.1232 0.1325 0.1766

N 3205 3205 3205

Standard errors in parentheses, * p < 0.10,

** p < 0.05,

*** p < 0.01