the robustness of empirical models for unemployment. a ...folk.uio.no/rnymoen/victoriamain.pdf ·...

TRANSCRIPT

The robustness of empirical models for unemployment.

A review of Nickell, Nunziata, and Ochel (2005).

Victoria Sparrman Department of Economics, University of Oslo.

Very Preliminary, please do not cite

November 17, 2008

Abstract

A number of recent papers have tried to explain the evolution of unemployment

in the OECD area, based on an equilibrium unemployment framework. One of

the most influential is Nickell et al. (2005). They find that institutions explains

most of the variation in unemployment for 20 OECD countries from 1960 to 1995.

However, the importance of Nickell et al. (2005) has also spurred a lively debate,

and several papers have criticized their findings. This paper re-asses the findings

of Nickell et al. (2005), benefitting from nine additional years of data. A dynamic

simulation of unemployment by using the model in Nickell et al. (2005), I find a

clear tendency that the model underpredicts the change in unemployment. The

dynamic simulation of unemployment illustrates that actual unemployment rate is

higher than simulated by the empirical model for 13 countries. The unemployment

rate is substantially lower than simulated for 4 countries. Furthermore, I evaluate

the empirical model by implementing some of the critiques into the original model

of Nickell et al. (2005).

1

1 Introduction

The theory for equilibrium unemployment is determined by the behavior of the wage and

price setters in an imperfect market. The price setters are firms sets prices in a non

competitive environment dependent on the development of nominal wages. This is the

price curve, i.e. a relationship between real wage and unemployment. The wage setters

decides on nominal wages given the price level. This is another relationship between

wage and employment. The intersection between the two curves determines the level of

equilibrium unemployment.

A number of recent papers have tried to explain the evolution of unemployment in the

OECD area, based on an equilibrium unemployment framework. One of the most influen-

tial is Nickell et al. (2005). They find that the development in labor market institutions

can account for 55 percent of the increase in European unemployment for the period 1960

to 1995. The effect of institutions to unemployment is equal for all countries in the panel.

The panel consists of 20 OECD-countries.

There are several reasons to re-asses the paper by Nickell et al. (2005). First, the

results are strong, explaining the bulk of variation in unemployment by variation in insti-

tutions.. It is impressive to achieve homogenous results of institutions for all the countries

in the panel. Secondly, the strand of research focussing on the link between labour market

institutions and unemployment has been very influential. Nickell et al. (2005) is a major,

recent contribution to this strand, spurring a lively debate and receiving 267 references in

Google Scholar. The recommendations of international organizations like OECD for how

countries should organize the economies efficiently are heavily influenced by this strand.

Thus, the results of strand of research have been interpreted as a recommendation to

countries for how they should change their institutions in order to avoid or reduce unem-

ployment. The institutions that affects unemployment negatively are benefit replacement

ratio, employment protection, union density and taxes should be reduced to achieve lower

unemployment rate.

This paper evaluates the results in Nickell et al. (2005) over the extended sample 1995

to 2004. A dynamic simulation of the model for unemployment with the original estimated

coefficients illustrates how well the model simulate actual unemployment out of sample.

The actual unemployment rate is higher than simulated by the empirical model for 13

2

countries. The unemployment rate is substantially lower than simulated for 5 countries.

The difference between simulation and actual unemployment rate for the period 1995 to

2004 motivates a closer look at the specified model in Nickell et al. (2005).

How trustworthy are the results in Nickell et al. (2005)? Previous critiques of Nickell

et al. (2005) include authors like Baker, Dean, Glyn, Andrew, Howell, David, Schmitt,

and John (b), Baker, Dean, Glyn, Andrew, Howell, David, Schmitt, and John (a), Howell,

Baker, Glyn, and Schmitt (2007) and also by Bassanini and Duval (2006). The time series

used in Nickell et al. (2005) are discussed by Kenworthy (2001) and Belot and van Ours

(2004). The problem is however, that it is difficult to determine the effect of the critique

to the original result. The problem arises because neither the time period, the method

or the time series for the variables rarely is the same between papers. This illustrates the

overall or broader critique of empirical approaches in the labor market: That it is difficult

or impossible to compare new results with other papers. How can one evaluate the model,

when the critique is not comparable to the original results? Or, to put it another way,

even if there are several weaknesses of the original model how much will the critique affect

the model?

In this paper, the effect of the extended time period and the revised data can be

compared to the benchmark model. By replicating the model on old and revised data,

varying the time period and include new indexes for the same variables, the sensitivity of

the results will be discovered.

The first step of the paper is to replicate the original result in table 5 in Nickell

et al. (2005). The replicated result is quite similar to the original results and is used as a

comparison for the rest of the paper. The correspondence between the results also ensures

that the same method is used throughout the paper. The second step is to extend the

time period and collect the variables in data set 2. The model in Nickell et al. (2005) is

estimated on data set 2. The results deviates from the former. There are two possible

explanations: revision of data or time extension. The explanations are investigated in

step three. The last step is to evaluate the indicators for the institutions. New indexes

for the same variables are collected in data set 3. These three data sets can be used to

test the sensitivity of the model in Nickell et al. (2005): replication, revision of time series,

extended time period and new indexes.

3

The estimation results of the model on the three data sets illustrate that the model is

not too robust to small changes in the data set. This leads to an evaluation of the model

in Nickell et al. (2005) in section 3.5. For instance, three countries have not stationary

error terms. The effect of non stationary error terms on the estimated coefficients and

the dynamic simulation are evaluated. Is it possible to use another estimation method to

achieve more robust estimates of the institutions (Arelleano Bond).

Outline of the paper, the simulation of model 5 in Nickell et al. (2005) on the extended

time period is presented in section 2. This section also presents the empirical model in

Nickell et al. (2005) and some related literature. The empirical investigation of the model

in Nickell et al. (2005) is discussed in section 3. In section 4 are some previous critiques by

authors like Baker et al. (b), Baker et al. (a), Howell et al. (2007) and Bassanini and Duval

(2006) discussed. Further, the critique of the chosen indexes for institutions, Kenworthy

(2001) and Belot and van Ours (2004). Section 5 concludes and Appendix 6 describes the

construction of the data.

2 Possible explanations to the development in unem-

ployment since 1995

This paper re-asses the findings of Nickell et al. (2005), benefitting from nine additional

years of data. The dynamic simulation of unemployment rate by using the model in

Nickell et al. (2005) over the period 1995 to 2004 is presented in section 2.1.

The empirical model in Nickell et al. (2005) is based on an equilibrium unemployment

framework. The model in Nickell et al. (2005) is presented in section 2.2 and the three

main theories to equilibrium unemployment are briefly presented in section 2.3.

2.1 Explanatory power of the model for unemployment in Nick-

ell et al. (2005) on the extended time period

This section explore wether the explanation to the development in unemployment for 1960

to 1995, as given in Nickell et al. (2005), hold for the latter period 1995 to 2004.

The empirical model in Nickell et al. (2005) is founded on a theoretical framework that

4

the long rung equilibrium unemployment is determined by the intersection between the

wage and the price curve. The relationship is further described in section 2.3. Equilibrium

unemployment will increase with factors that increases the wage pressure for instance

strong union power or a high tax level. These variables will be referred to as institutional

variables. Further, actual unemployment rate may deviate from the equilibrium rate if

the economy is exposed to shocks. Example of shock is unexpected change in labour

demand or productivity.

New data have become available since Nickell et al. (2005) presented their work. The

institutional variables are available in Nickell (2006), i.e. the authors home page. Data are

available up to 2003. Unemployment rate and shocks are referred to as macro variables.

The macro variables are collected at OECD (2007) and are available up to 2007. The

variables are only used up to 2004 in the empirical investigation due to the limitation

of the institutional variables. See appendix 6 for details. The extended time series are

collected in a data base and is in what follows denoted as data set 2.

To simulate unemployment for the period 1995 to 2004 the coefficients in table 5 in

Nickell et al. (2005) are replicated. The data set used in the replication is denoted as

data set 1. The replicated result is reported in table 1. The estimated coefficients are all

within the original 90 percent intervals. The replicated coefficients are used to simulate

unemployment rate out of sample, i.e. on the extended time period 1995 to 2005. The

extended data set is denoted as data set 2.

The static simulation method simulates unemployment one year ahead out of sample.

This means that we use all available information up to last period, t− 1, to simulate the

unemployment rate today, t. The new simulated value for unemployment rate is related

to the E(U |X, β̂), where X is a vector that contains all explanatory variables and β̂) is a

vector with all the estimated coefficients in equation (1).

Figure 1 presents actual unemployment rate and the simulated unemployment rate.

The model simulates well for Denmark, Finland, France, Germany, Ireland, Netherlands,

Spain, Sweden and Switzerland. For some countries the simulated unemployment rate is

higher that actual unemployment rate. This is the case for Denmark, Finland, Ireland,

Netherlands, Sweden and Switzerland. For the rest of the countries is the simulated

unemployment rate lower than actual unemployment rate.

5

If the explanation to unemployment is given in Nickell et al. (2005), i.e. that insti-

tutions and shocks explains most of the unemployment over time and between countries,

the model should simulate actual unemployment well on data set 2. From the above

discussion the model simulates quite well. The conclusion is therefore that the model,

as specified in Nickell (2006), in general simulates well but if anything simulates lower

unemployment rate than is observed in the data after 1995.

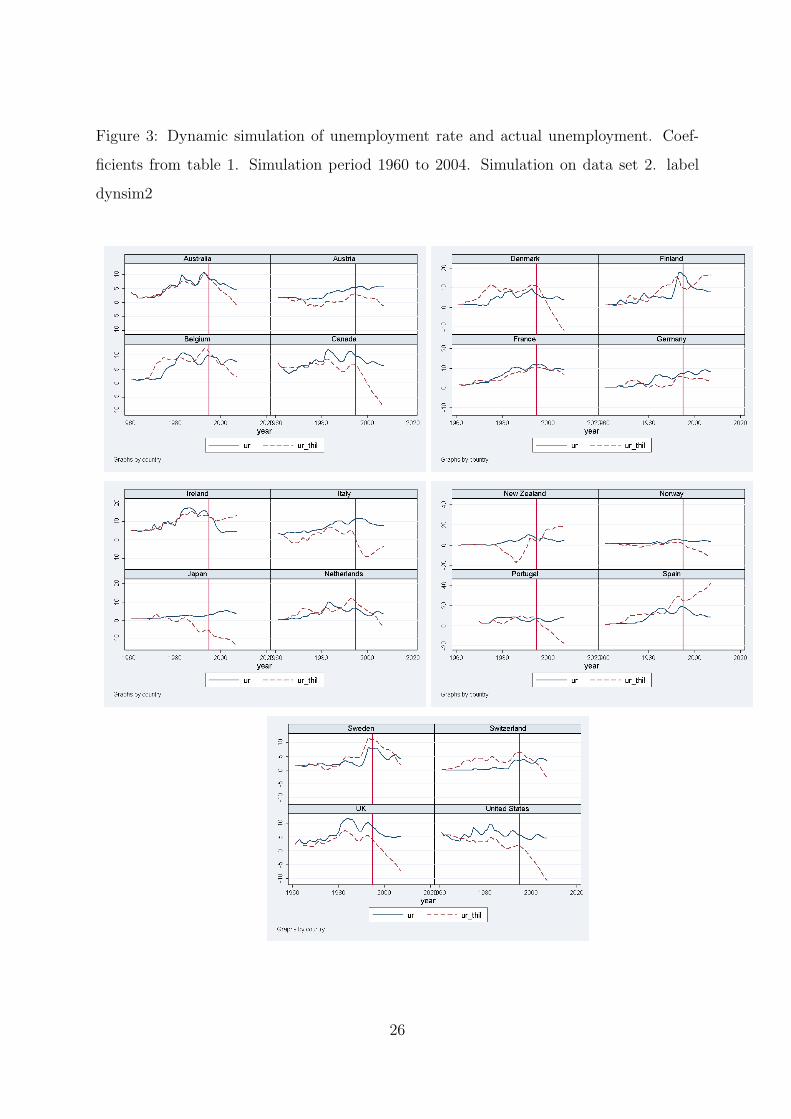

The explanatory power of the model in Nickell et al. (2005) can be evaluated by a

dynamic simulation over the period 1995 to 2004. The dynamic simulation with estimated

coefficients from data set 1 over the extended time period is illustrated in figure 3. The

simulation of the extended time period only is illustrated in figure 4.

The difference between the simulated and the actual value of unemployment rate can

be caused by the development in the institutions or by shocks. To exclude the effect

of shocks to the results, shocks are set to zero after 1995. The graphs are presented in

figure 2. In general the simulated unemployment rate is lower than actual unemployment

for most countries. Spain is the only country where the simulated unemployment is

higher than actual unemployment. For Denmark, Netherland and Switzerland the model

simulates even lower unemployment rate compared to the situation with shocks, which

means that the shocks contributes positive to the simulated unemployment.

The dynamic simulation with zero shocks is presented in figure 5.

The dynamic simulation with constant institutions is presented in figure 18.

The mismatch between actual and simulated unemployment rate for the period 1995

to 2004 implies a further investigation of the specified model in Nickell et al. (2005). The

model is presented in the next section 2.2.

2.2 A brief description of the empirical investigation in Nickell

et al. (2005)

This section take a closer look at the empirical investigation in Nickell et al. (2005). The

paper by Nickell et al. (2005) is one of the leading empirical papers in supporting the

theory of equilibrium unemployment on panel data. The model is estimated over the

period 1960 to 1995.

The empirical specification of unemployment in Nickell et al. (2005) include explana-

6

tory variables that explains equilibrium unemployment and factors that makes actual

unemployment to deviate from equilibrium unemployment.

Equilibrium unemployment between countries varies due to different levels of insti-

tutions. The institutions included in the model are indexes for employment protection,

benefit replacement ratio, benefit duration, union density, taxes and coordination. The

empirical investigation also includes some interaction terms among these institutions.

The theory predict that the unemployment rate can deviate from the long run equilib-

rium rate over the business cycle. The regression in Nickell et al. (2005) include variables

that account for these short term deviations, referred to as shocks. Shocks are determined

by unexpected changes in labour demand, productivity, terms of trade, money demand

and real interest rate.

The variables and data are explained in detail in Appendix 6.

The model estimated in table 5 in Nickell et al. (2005) is given by equation (1).

Uit = θUi,t−1 + β1eplit + β2BRRit + β3bdit ∗ BRRit + β4D.udnetit + β5coit

+β6coit ∗ udnetit + β7TWit + β8coit ∗ TWit + α1ldsit + α2Dprod hpit

+α3TTSit + α4D2.MSit + α5RIRLit + γ1t + γ2i + γ3iTt + uit (1)

(maybe explain variables epl is employment protection and so on)

The coefficients in equation (1) are estimated by using data for 20 OECD countries over

the period 1960 to 1995. The result is in line with the equilibrium theory of unemployment,

se table 1.

The empirical result supports the theory. The long run level of unemployment rate

in all OECD countries is due to the development of institutions, i.e. higher level of taxes

and unemployment benefits increases unemployment. Unemployment level decreases with

higher level of coordination in wage setting. Deviations from the equilibrium rate are

explained by shocks like for instance unexpected changes in labour demand, productivity

or terms of trade.

The estimated result imply that if everything else is equal the lagged dependent vari-

able will reduce unemployment by a factor θ = 0.86 this period in all countries. Further,

if benefit duration increases by 1 unit this period, unemployment will increase by 0.47

7

percentage points. This is however, only the immediate effect of benefit duration since

the explanatory variables also will have an effect on unemployment trough the lagged

dependent variable. The total increase in unemployment by 1 unit increase in benefit

duration is calculated by the estimated coefficient of the explanatory variable divided by

one minus the estimated coefficient of the lagged dependent variable, i.e. 0.47/(1 − θ).

This is the long run effect of an initial increase of 1 unit increase in benefit duration. If

for instance benefit duration increases by 0.3 from its mean level 0.4, unemployment will

increase by around one percent. The change is equal to one standard deviation in the

time series for benefit duration.

There are several ways to evaluate an empirical model. Nickell et al. (2005) chose

to show the results of a dynamic simulation of the unemployment rate together with

the actual unemployment rate over the estimation period. Figure 1 in Nickell et al.

(2005) reveals that the model explains the data well. According to Nickell et al. (2005)

the dynamic simulation is a more revealing measure of fit than a country specific R2

since the coefficient of the lagged dependent variable is large. They also argue that the

difference between the dynamic simulation with variation in institutions and with no

variation in institutions reveals that institutions can explain a large part of the increase

in unemployment in Europe.

2.3 Theory of equilibrium unemployment

This section describes the theory for equilibrium unemployment and how it relates to the

Neo-classical view of the labour market. Nickell et al. (2005) gives substantial empirical

support to equilibrium theory of unemployment.

The Neo-classical framework for the labour market determines prices and outputs

through supply and demand for labour. Workers maximize utility which is dependent on

consumption and leisure given real wages. This result in the supply function. Firms on the

other hand maximize profits with respect to wages, this results in the demand for labour.

The theory assumes rational expectations and complete information. The theory implies

that the unemployed workers have determined not to work, since the outside option is

better.

Layard, Nickell, and Jackman (1991) is a book, which has become the standard refer-

8

ence for how to model the labor market. They argue convincingly that the Neo-classical

framework is unsuitable when developing models for the labor market. The imperfections

in the labor market are of such importance that every theory for unemployment has to

put the imperfections in center.

The theory for equilibrium unemployment is determined by the behavior of the wage

and price setters in an imperfect market. The price setters are firms sets prices in a non

competitive environment dependent on the development of nominal wages. This is the

price curve, i.e. a relationship between real wage and unemployment. The wage setters

decides on nominal wages given the price level. This is another relationship between wage

and employment.

The price and the wage curves are interpreted as a standard supply and demand for

labor. Firms increases prices as they employ more workers at a given wage when the

product function has decreasing return to labor. The workers on the other hand, given

the price level, demands higher wages when unemployment is low. This results in an

increasing supply function of labor in real wages.

The intersection between the two curves determines the equilibrium rate of unemploy-

ment. The level depends on factors that influence the price or the wage setting. For

instance the union bargain power, the level of taxes or coordination affect the supply

curve lies in a real wage and unemployment diagram. And hence yield in different levels

of unemployment.

This theory of wage and price setting where however only a macro economic framework

for unemployment. The book by Layard et al. (1991) also summarized the micro economic

foundation.

Today there exists three theories for unemployment that try to explain how frictions

affects the wage and price setting: collective bargain, efficiency wage and search models.

The theories are however not exclusively for each other.

3 Empirical investigation

The dynamic simulation of unemployment from 1995 to 2004 in chapter 2.1 motivates a

step by step investigation of the specified model in Nickell et al. (2005). In this section

9

the estimation method of Nickell et al. (2005) is kept constant, but the sample length and

the operational definition of the institutional variables vary.

The starting point is a replication of the empirical model in table 5 in Nickell et al.

(2005). The replication where successful and ensures that any difference in results later

in the paper are due to changes in definitions or sample length. The replication of the

model on data set 1 is discussed in section 3.1. The data set is taken from the authors

home page.

Since Nickell et al. (2005) published the paper the time series are revised and extended.

The extended time period is 1995 to 2004. The new time series for the whole period are

collected in data set 2. In section 3.2 is the former model in Nickell et al. (2005) estimated

on data set 2. The estimated coefficients deviates from the original results in Nickell et al.

(2005).

The further investigation of the model by reducing the time period in data set 2

is presented in section 3.3. In section 3.4 we look at the estimation results when new

and maybe better indexes are used. Finally section 3.5 takes a closer look at the model

specifications.

3.1 Replication of model 1 in table 5 in Nickell et al. (2005).

Data set 1

The result in Nickell et al. (2005) is replicated by using the same method and by using

the data set published at the first authors home page1. The data set is in what follows

denoted as data set 1. The replication also includes a calculation of the long term effects

of explanatory variables and a dynamic simulation. Dynamic simulation is according to

Nickell et al. (2005) the best way to illustrate that institutions have a large impact on

unemployment.

The replicated results are presented in Model A in table 1. As seen from the table,

all coefficients have the same sign as the coefficients in table 5 in Nickell et al. (2005).

Further, all coefficients are within the original 90 percent confidence intervals.

The small differences between the replicated coefficients and the original coefficients in

1The data for the institutional variables and method for estimation are presented at the authors home

page (http://cep.lse.ac.uk/papers).

10

Nickell et al. (2005) are illustrated in figure 7. The differences in the estimated coefficients

and the original results are probably due to differences in the data sets. The summarize

statistics of data set 1 according to table 1 in Nickell et al. (2005) shows that the time

series for unemployment are somewhat revised.

Further, the replication result show that both the total number of observations and the

average size of the observations in each group used in the estimations are different, se table

1. The average number of observations is 31.16 for each group in Nickell et al. (2005) but

29.95 in the replicated model. On the other hand the total number of observations only

differ by one single observation. The average number and the total number of observations

used in the estimation indicates that some of the observations in data set 1 are adjusted

before they were used in Nickell et al. (2005) estimated model.

The adjustments to the data set are not explained in detail in Nickell et al. (2005).

This can cause the estimated values to differ. Especially the value of the coefficient for

employment protection. This variable has an insignificant affect on unemployment both

in the paper Nickell et al. (2005) and in the replicated result based on data set 1. But a

low value of the t-statistic can imply that the estimated coefficient can change numerically

as a result of changes in the data set or estimation method.

Another cause to the difference in estimated coefficients could be due to the software.

In fact that two different versions of Stata have been used can result in different values

of the same model. This is most easily seen by considering the error term. The error

term is assumed to follow an autoregressive process. The coefficients on lagged error

terms are heteroscedastic, which means that they are country specific. The estimation

process requires some start values for these country specific coefficients in the iteration

process. These values are drawn randomly. Random values can obviously vary between

computers and between different versions of Stata. It is therefore necessary to describe the

initial values and the version of Stata, if the researcher wants their results to be exactly

replicable by others. Especially when the results are not robust in the first place, like the

employment protection coefficient.

That said, the replicated estimated coefficients on data set 1 in table 1 all have the same

sign as the coefficients in table 5 in Nickell et al. (2005), and all are within the original

90 percent confidence intervals, so for all practical purposes, the replication has been

11

successful. It is therefore possible to assume that the values of the replicated coefficients

can be used as a comparison for further investigation.

A standard dynamic simulation inserts the estimated coefficients and uses the observed

data for the exogenous variables to simulate the development in the endogenous variable.

Normally is the expected value of the error term 0 and is used in the simulation.

This is not the case for the error term in model 5 in Nickell et al. (2005). The error

term is expected to follow an autoregressive process with a country specific coefficient, ρi,

as previous mentioned. The expected value of the error term in Nickell et al. (2005) is

equal to the error term last period multiplied with ρi.

The values of the heteroscedastic coefficient for each country is specified in table 5 to-

gether with the coefficient of lagged unemployment. The predicted error term is calculated

by the difference between the simulated unemployment and the actual unemployment rate.

A dynamic simulation on data set 1 is presented in figure 10. The figure 10 illustrates

that the patterns are quite similar to the dynamic simulation in Nickell et al. (2005). The

method for the dynamic simulation is discussed further in section 3.5.

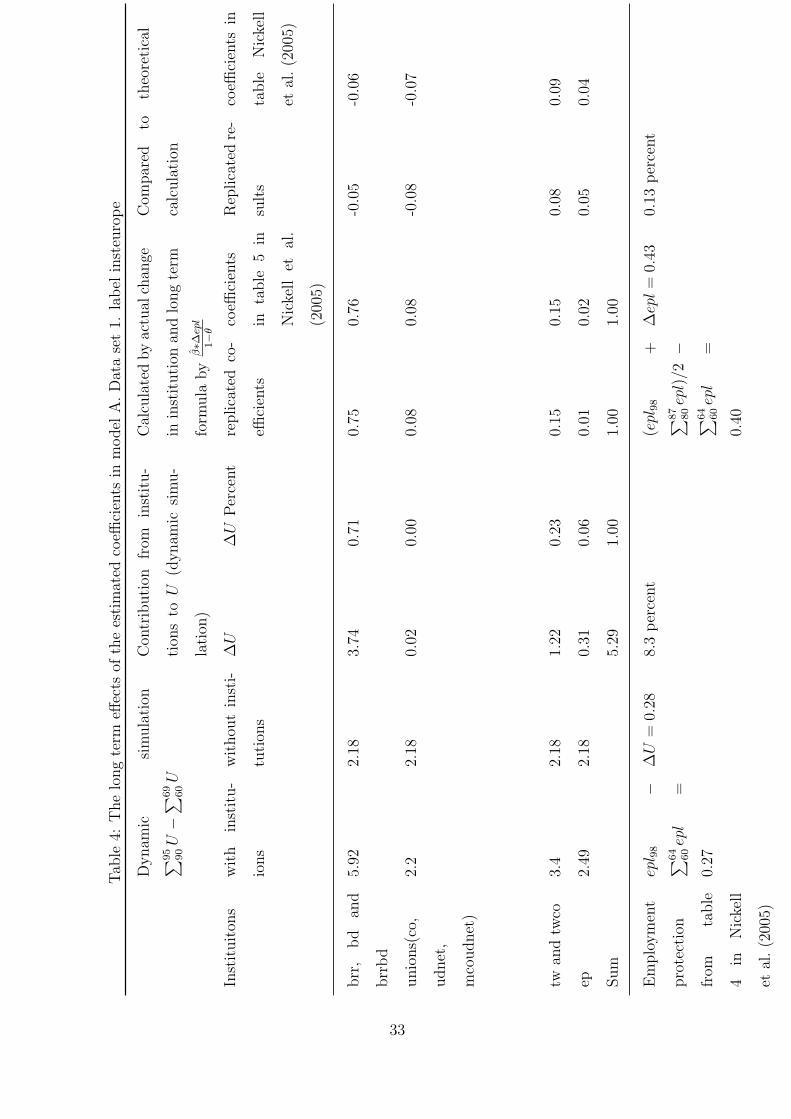

Nickell et al. (2005) claims that the variation in institutions accounts for 55 percent of

the increase in unemployment in Europe over the estimation period 1960 to 1995. The long

term effects of institutions are calculated in table 4. The table shows that our replication

implies that institutions accounts for 71 percent of the increase in unemployment in

Europe. This is consistent with the theoretical change, calculated by the long term effects

and actual change in data. (beregn ut i fra nick sine tabeller og koeff, lang tids effektene.)

The replication and the dynamic simulation on data set 1, imply that the values of

the replicated coefficients are slightly different from the estimated coefficients in Nickell

et al. (2005). But taking into consideration that all are within the original 90 percent

confidence intervals and the visual similarity in the dynamic simulation, the replication

of the results in Nickell et al. (2005) has been successful. The replicated results are used

as a comparison for further investigation when the data set is extended.

12

3.2 The model in table 5 in Nickell et al. (2005) is estimated on

data set 2

Nickell (2006) or the authors home page have data for institutional variables available up

to 2003. The macro variables from OECD (2007) are available up to 2007, although only

included to 2004. The extended time series are collected in a data base and is in what

follows denoted as data set 2. See appendix 6 for details.

The same procedure as in 3.1 for the replication, is now used to estimate the coefficients

on data set 2 over the period 1960 to 2004 for all 20 OECD countries. The results are

reported in this section.

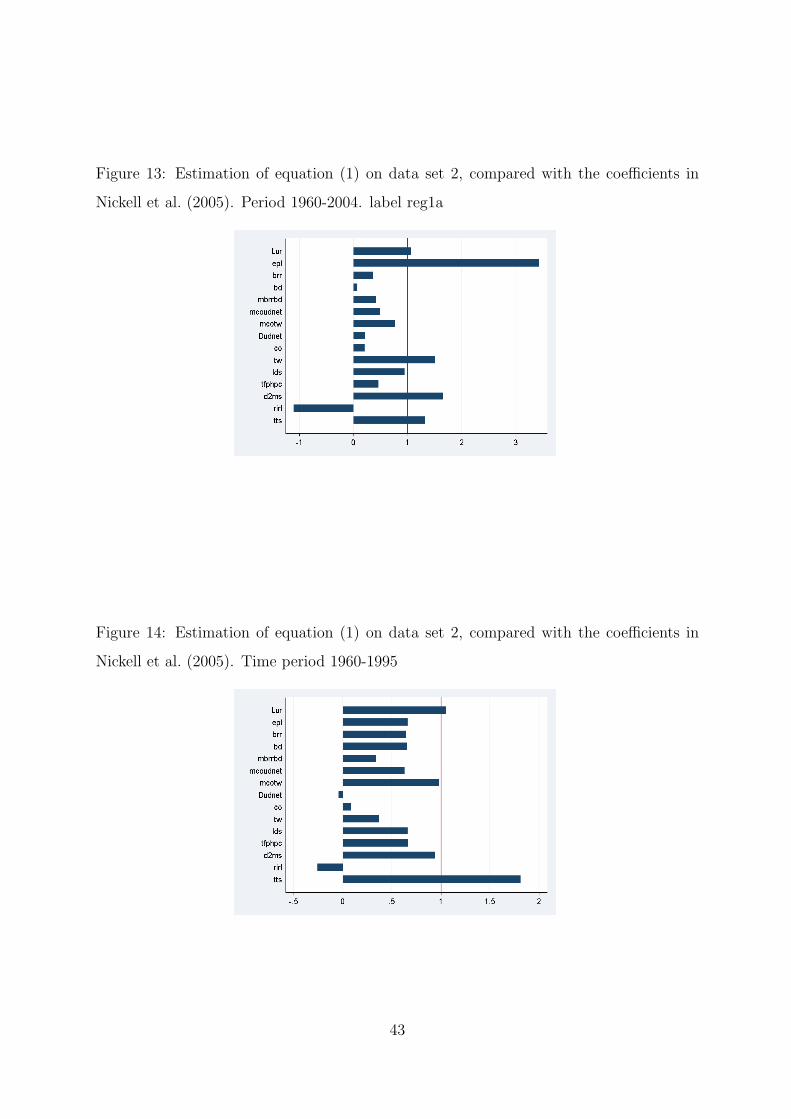

The estimation results are given in table 5. The results are very different from table 1

and therefore also the original results in Nickell et al. (2005). In general both the effects of

institutional variables and shocks on unemployment are reduced. Several variables are no

longer significant. Three of the coefficients have changed sign: employment protection,

monetary shock and real interest rate. The variables were not significant in the first

regression though. The difference to Nickell et al. (2005) is also presented graphically

in figure 13. As mentioned in the discussion of the replication in section 3.1, the effect

of explanatory variables can be less stable if they are insignificant. This can be one

explanation to why these coefficients change dramatically when the data set is extended.

Section 3.3 will take a closer look at the specification, to see if revision of the data sets

or time extension causes the differences.

Even if the values of the estimated coefficients on data set 2 are somewhat different, it

is interesting to look at the models static simulation of unemployment and the dynamic

simulation. This should result in a bad fit of unemployment, at least for the period 1960

to 1995, but it seems that the new coefficients simulates the new data set very well over

that period, se figure 17. This can be because the model is too flexible because of time

dummies and country specific trends, in the sense that the model can capture actual

unemployment with any values of the estimated coefficients of the institutional and shock

variables. Or it could be that unemployment is quite stable, so that when all information

is used up to t− 1 unemployment to simulate unemployment this period t is not to hard

since adjustment by considering actual unemployment is made every period.

It is therefore necessary to look into the dynamic simulation. The dynamic simulation

13

of the estimated coefficients from table 5 are given in figure 3 and 4. skriv ut!

3.3 How much of the change in 3.2 is due to revisions?

This section reduces the time period in data set 2 to check wether the change in the

coefficients discovered in section 3.2 only are due to revisions of the data. The second

section looks at the performance of the former coefficients from data set 1, by simulateing

the unemployment rate for the new time period 1995 to 2004.

3.3.1 Is the change due to shocks

The figure of the dynamic simulation for the period 1960 to 2004, with zero shocks after

1995 is presented in figure 5. skriv ut!

3.3.2 Reduced time period on data set 2

The time period is reduced to detect if the coefficients in section 3.2 is due to the revision

of data or to the time extension. The former model in Nickell et al. (2005) is estimated

on data set 2, but only over the former available time period from 1960 to 1995.

The estimation results for period 1960 to 1995 on data set 2 are listed in table 6.

Five of the variables, benefit duration, union density, coordination and taxes, no longer

significant effect unemployment. The effect of employment protection is reduced, the

coefficient is nearly zero and not significant. Real interest rate has changed sign, but is

not significant. The change in the estimated coefficients compared to the original results

in Nickell et al. (2005) is presented in figure 14. The change in the values of the coefficients

indicates that the former values of coefficients are not very robust even to small changes

in the data set, i.e. to the revisions of the time series.

It seems that some of the difference is due to the new updated time series, and some

of the difference is due to the extended time period.

3.4 Estimation of model 5 in Nickell et al. (2005) on data set 3

The results are presented in table 8 and 7.

14

3.5 The effect of the specification of the error term Nickell et al.

(2005). Data set 1.

Equation (1) contain: the lagged endogenous variable, several explanatory variables, the

error term and the time and country dummies. The goal of an econometric specification

like equation (1) is to extract some homogenous effects of the included variables. This

section take a closer look at the econometric specification.

3.5.1 Error term

In the model estimated on equation 1 the error term is assumed to be heteroscedastic and

autocorrelated. The assumptions are expressed by equation 2.

uit = ρiui,t−1 + εit (2)

where εit is white noise. ρi is estimated for every country i by a iteration process.

The choice of this process for the error term where justified by a rejection of the joint

hypothesis ρi = 0 for all i, i.e. countries in the panel.

The coefficient of the lagged error term is unknown and has to be jointly estimated

with the coefficients. Table 5 lists the estimated country specific autocorrelation ρi. The

table shows great variation in ρi from -1.28 up to 3.18.

The estimation method assumes that the process in equation (2) is stationary, i.e.

|ρ| < 1. As seen from table 5 this is not the case for Japan, New Zealand and Portugal.

This means that the effect of the error term to unemployment increases over time. New

Zealand has positive autocorrelation in the error term. This means that unemployment

will increase or decrease steadily over time. Japan and Portugal have negative autocor-

relation in the error term. This means that the error term in one period will increase

unemployment but decrease unemployment in the next period. The positive and the

negative effect of the error term to unemployment will increase over time.

What are the effect of non-stationarity on the coefficients on the estimation method?

The effects are illustrated by a dynamic simulation in the next section.

15

3.5.2 Dynamic simulation, equation (1) is rewritten

As described in Nickell et al. (2005) the included country dummies, time dummies, country

specific trends and the lagged dependent variable, ”...are to ensure that the estimated

coefficients are not distorted by omitted trended variables in each country or common

shocks.”.

This means that the estimated coefficients in table 1 expresses the influence of the

included variables on unemployment regardless of the country considered.

The above reasoning depends on that the specification of the model is true. Equation

(1) can be rewritten to illustrate the effect of the heterogenous lagged error term on the

included variables. This requires four steps. Start by making a simplification of equation

(1) as:

Uit = θUi,t−1 + βXit + αYit + γ1t + γ2i + γ3iTt + uit (3)

where X is a vector consisting of the institutional variables and the interaction terms

in equation (1). The vector β contains the coefficients corresponding to the institutional

variables and the interaction terms in vector X. The shocks are collected in vector Y

with the coefficients in α.

Second, equation 3 also holds for period t−1. This equation contains the lagged error

term, ui,t−1, see equation 4.

Ui,t−1 = θUi,t−2 + βXi,t−1 + αYi,t−1 + γ1t−1 + γ2i + γ3iTt−1 + ui,t−1 (4)

Third, reorganize and insert the expression for ui,t−1 in equation 2. This gives the

following expression in equation 5:

uit = ρi[Ui,t−1 − (θUi,t−2 + βXi,t−1 + αYi,t−1 + γ1t−1 + γ2i + γ3iTt−1)] + εit (5)

Finally insert 5 in equation 3. This gives

Uit = θUi,t−1 + βXit + αYit + γ1t + γ2i + γ3iTt

+ρi ∗ [Ui,t−1 − (θUi,t−2 + βXi,t−1 + αYi,t−1 + γ1t−1 + γ2i + γ3iTt−1)] + εit(6)

16

Equation 6 has a white noise error term, εit. The equation can be organized as follows

in equation 7:

Uit = (θ + ρi)Ui,t−1 − ρiθUi,t−2 + β(Xit − ρiXi,t−1) + α(Yit − ρiYi,t−1)

+(γ1t − ρiγ1t−1) + (1 − ρi)γ2i + (γ3iTt − ρiγ3iTt−1) + εit (7)

Equation 7 shows that the process for the error term effects the estimated coefficients

of both the lagged endogenous variable and the exogenous variables included in the model.

The the estimated coefficient of the lagged endogenous variable, θ in table 1, is heteroge-

nous if the coefficient is adjusted by the effect of the lagged heteroscedastic autocorrelated

error term, ρi.

A dynamic simulation by equation 7 will illustrate also how the process for the specified

error term affects unemployment. This is illustrated in figure 15 and 16. The dynamic

simulation of the countries in figure 15 illustrates a similar pattern as the previous figures

in figure 10. As can be seen from figure 16 unemployment in New Zealand decreases

rapidly. For Japan and Portugal are there an negative autocorrelation. This means that

unemployment one period will increase with the error term, and the next decrease with

the error term. The positive and negative effects will increase over time, this is typically

the case for Portugal as illustrated in figure 3.

The figures illustrates that the model is not stationary when the error term is consid-

ered. The non stationarity can also be calculated by the 2. order differential equation in

equation 7. If the values of the last three columns of table 5 are greater than zero, will

the 2. order differential equation 7 will be stable. As seen from the table Japan, New

Zealand and Portugal have values lower than zero and are consistent with the previous

findings. empirical strategy

3.6 Some different specifications of the model.

Nickell et al. (2005) argue that this specification of the error term is correct since they

can not reject that ρ = 0 under an LM test, where χ(1) = 77.3. This test is however not

reliable when you include the lagged endogenous variable.

Arelleano bond :

17

The estimated coefficients of equation (1) are not consistent since both the lagged en-

dogenous variable and country specific effects appears in the same equation. The specified

process, Psar1, means that every error term has an estimated parameter and that L.U r is

correlated with the error term. This is normally handled by a procedure called Arelleano

bond.

Transformation:

Multiply both sides by the factor (1 − L)Ut where L is the lagged operator. Estimate on

this model. But how to account for the lagged error term.

3.6.1 Error term and graphical plot, not ready, any point?

Should residuals be heteroscedastic and autocorrelated?

A graphical plot of the error term, can we exclude the assumptions or include Ui,t−2

in equation?

4 Previous critique of Nickell et al. (2005)

Summarize the main critique of empirical papers trying to explain unemployment by

Baker et al. (b), Baker et al. (a), Howell et al. (2007) and also by Bassanini and Duval

(2006). Especially are the two latter a critique of Nickell et al. (2005). How trustworthy

are the results of Nickell et al. (2005)? This section looks at the other critiques and

summarizes the main findings.

Main critique:

Baker et al. (a) chapter 3, discusses an early version of Nickell et al. (2005). They claim

that the time effect trough the lagged endogenous variable are far to high to be reasonable.

For instance they claim that unemployment would have been negative if institutions where

hold constant throughout the period. One could question this remark, due to the fact

that time effects are not significant. The level of time effects in the model of Nickell et al.

(2005) should therefore be interpreted with care.

Indexes in themselves:

The indexes used in Nickell et al. (2005) are employment protection, benefit replacement

ratio, benefit duration, union density, taxes and coordination. There are several objections

18

to these indexes.

First of all it can be argued that these indexes not necessarily operate only in one

direction. For instance a higher coordination level can imply lower wage claims if the

level is above a certain level, see for instance ?. This is the famous results of the hump

shaped wage claims in the level of coordination, where medium level of coordination

results in highest wage clams. The low and the high coordination levels results in low

wage claims. This is also related to union density, and the insider outsider theory of wage

setting. Wage setters that covers the whole economy will according to the theory care for

unemployment levels. On the other hand will unions that only are responsible, only care

for parts of the economy in wage setting, care less of unemployment levels and more of

wage growth.

Further, employment protection can lead to lower unemployment in recessions. This

will be the case if employment protection makes employers more cautiously in hiring

workers in both recessions and in high growth periods. If unemployment benefits causes

workers to take more risk because they are less risk averse (benefits ensures the downside),

this can result in less unemployment because workers are more spread and actually result

in higher productivity growth.

Taxes and unemployment could be questioned according to Baker et al. (a). They point

out the between country variation, for instance high tax and low unemployment rate in

Sweden and low tax and high unemployment in Spain, implies that the relationship is not

clear.

The last thing to remember is that the causality between the indexes and unemploy-

ment are not obvious. The causality argument is also supported by Baker et al. (a).

The above arguments are made to see that it is not obvious that all indexes included

in Nickell et al. (2005) should have the sign achieved from the estimation of equation (1)

as listed in table 1.

Indexes are collected every 2. or 5th year, used as annual observations:

Wrong source of indexes:

The time series used in Nickell et al. (2005) are previously discussed, see for instance

Kenworthy (2001), Belot and van Ours (2004) and Baker et al. (b). Summarize.

19

5 Concludes

References

Baker, Dean, Glyn, Andrew, Howell, R. David, Schmitt, and John. 3.. labor market

institutions and unemployment: Assessment of the cross-country evidence. Fighting

Unemployment , 72–119.

Baker, Dean, Glyn, Andrew, Howell, R. David, Schmitt, and John. 3.. labor market

institutions and unemployment: The failure of the empirical case for deregulation.

Center for Economic and Policy Research 1611 Connecticut Avenue, NW Suite 400

Washington, DC 20009 , 72–119.

Bassanini, A. and R. Duval (2006, June). Employment patterns in oecd countries: Re-

assessing the role of policies and institutions.

Belot, M. and J. C. van Ours (2004). Does the recent success of some oecd countries in

lowering their unemployment rates lie in the clever design of their labor market reforms?

Oxford Economic Papers 56 (4), 621+.

Howell, D., D. Baker, A. Glyn, and J. Schmitt (2007). Are protective labor market

institutions at the root of unemployment? a critical review of the evidence. Capitalism

and Society 2 (1), 1.

Kenworthy, L. (2001). Wage-setting measures: A survey and assessment. World poli-

tics 54 (1), 57–98.

Layard, R., S. Nickell, and R. Jackman (1991). Unemployment: Macroeconomic Perfor-

mance and the Labour Market. Oxford University Press, USA.

Nickell, S., L. Nunziata, and W. Ochel (2005). Unemployment in the oecd since the 1960s:

What do we know? The Economic Journal (115), 1–27.

Nickell, W. (2006, November). The cep-oecd institutions data set (1960-2004).

OECD (2007). Oecd. Oecd .

20

List of Figures

1 Actual and static simulation of unemployment rate. Coefficients for simu-

lated unemployment from table 1. Time period 1960 to 2004. label predict1 24

2 Actual and static simulated unemployment rate. Coefficients for simulated

unemployment from table 1. Shocks are zero after 1995. Time period 1995

to 2004. label predict2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

3 Dynamic simulation of unemployment rate and actual unemployment. Co-

efficients from table 1. Simulation period 1960 to 2004. Simulation on data

set 2. label dynsim2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4 Dynamic simulation of unemployment rate and actual unemployment. Co-

efficients from table 1. Simulation period 1995 to 2004. label dynsim3 . . . 27

5 Dynamic simulation of unemployment rate and actual unemployment. Co-

efficients from table 1. Shocks are set to zero after 1995. label dynsim4 . . 28

6 Dynamic simulation of unemployment rate and actual unemployment. Co-

efficients from table 1. Institutions are constant. label dynsim5 . . . . . . . 29

7 The replicated coefficients on data set 1 (model A in table 1) compared

with the coefficients in Nickell et al. (2005). label nick reg1a . . . . . . . . 38

8 Model B in table 1 relative to model A. Only the number of time dummies

differ. Data set 1. label nick reg1b . . . . . . . . . . . . . . . . . . . . . . 38

9 The country specific trend, time dummies and country specific effects.

Model A and data set 1 relative to the original results in Nickell et al.

(2005). label nick reg1aa . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

10 Dynamic simulation of the coefficients estimated on data set 1 over the

years 1960 to 1995. label dynsim1a . . . . . . . . . . . . . . . . . . . . . . 40

11 Dynamic simulation of the coefficients estimated on data set 1 over the

years 1960 to 1995. With and without variation in institutions. label

dynsim1b . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

12 Dynamic simulation of the coefficients estimated on data set 1 over the

years 1960 to 1995. Excluding variation in one by one institution. label

dynsim1c . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

21

13 Estimation of equation (1) on data set 2, compared with the coefficients in

Nickell et al. (2005). Period 1960-2004. label reg1a . . . . . . . . . . . . . 43

14 Estimation of equation (1) on data set 2, compared with the coefficients in

Nickell et al. (2005). Time period 1960-1995 . . . . . . . . . . . . . . . . . 43

15 The transformed equation 7. Model A in 1. Data set 1. label dynsim2a . . 45

16 The transformed equation 7. Model A in 1. Data set 1. label dynsim2b . . 46

17 Static simulation of model for unemployment in Nickell et al. (2005) over

the years 1960 to 2004. Estimated coefficients from table 5 are used in the

simulation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

18 Dynamic simulation and actual unemployment. Coefficients in table 5 over

the years 1960 to 2004. Simulation and estimation on data set 2. . . . . . . 48

19 Dynamic simulation with and without the effect of institutions to unem-

ployment. Coefficients in table 5 over the years 1960 to 2004. Simulation

and estimation on data set 2. . . . . . . . . . . . . . . . . . . . . . . . . . 49

20 Actual unemployment. Data set 2 over the years 1960 to 2007. label ur . . 54

List of Tables

1 Model 1 is the results in table 5 in Nickell et al. (2005). Model A is the

replication of model 1 on data set 1. Model B is the replication, but pools

the time dummies over the years 1966 and 1967 with the former periods

1960 to 1966. label t1emp . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

2 Model A, replication like Model A in table 1. Model B, the same explana-

tory variables as Model A, but pools ρ, i.e. no heteroscedastic lagged error

term. Model C, the same as Model B, but the lagged error term ρ, follows

a calc process. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3 The error term and stability restrictions. Data set 1. label stabrho . . . . . 32

4 The long term effects of the estimated coefficients in model A. Data set 1.

label insteurope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

5 Model A is a replication of model 1 given in table 5 in Nickell et al. (2005)

on data set 2. Time period 1960-2004. label t2emp . . . . . . . . . . . . . 34

22

6 Model 1 is a replication of model 1 given in table 5 in Nickell et al. (2005)

on data set 2. Time period 1960-1995. label t3emp . . . . . . . . . . . . . 35

7 Replication of model 1 given in table 5 in Nickell et al. (2005) on data set

3. Time period 1960 until 1995. label t5emp . . . . . . . . . . . . . . . . . 36

8 Replication of model 1 given in table 5 in Nickell et al. (2005) on data set

3. Time period 1960 until 2004. label t7emp . . . . . . . . . . . . . . . . . 37

9 Unemployment as Nickell et al. (2005) has presented the data, data set 2 . 50

10 Macrovariables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

11 Constructed variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

12 Institutional variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

23

Figure 1: Actual and static simulation of unemployment rate. Coefficients for simulated

unemployment from table 1. Time period 1960 to 2004. label predict1

24

Figure 2: Actual and static simulated unemployment rate. Coefficients for simulated

unemployment from table 1. Shocks are zero after 1995. Time period 1995 to 2004. label

predict2

25

Figure 3: Dynamic simulation of unemployment rate and actual unemployment. Coef-

ficients from table 1. Simulation period 1960 to 2004. Simulation on data set 2. label

dynsim2

26

Figure 4: Dynamic simulation of unemployment rate and actual unemployment. Coeffi-

cients from table 1. Simulation period 1995 to 2004. label dynsim3

27

Figure 5: Dynamic simulation of unemployment rate and actual unemployment. Coeffi-

cients from table 1. Shocks are set to zero after 1995. label dynsim4

28

Figure 6: Dynamic simulation of unemployment rate and actual unemployment. Coeffi-

cients from table 1. Institutions are constant. label dynsim5

29

Table 1: Model 1 is the results in table 5 in Nickell et al. (2005). Model A is the replication

of model 1 on data set 1. Model B is the replication, but pools the time dummies over

the years 1966 and 1967 with the former periods 1960 to 1966. label t1emp

Model 1 in table 5 in Nickell et al. (2005)

b t

L.ur 0.86 48.5

epl 0.15 0.9

brr 2.21 5.4

bd 0.47 2.5

brrbd 3.75. 4.0

codudnet -6.98 6.1

cotw -3.46 3.3

D.udnet 6.99 3.2

co -1.01 3.5

tw 1.51 1.7

lds -23.6 10.4

tfp -17.9 14.1

d2m 0.23 0.9

rirl 1.81 1.6

tts 5.82 3.3

obs 600

time periods

numb groups 20

min groups 12

max groups 33

avg groups 31.2

coef 85

est cov 20

est autocorr 20

log like -599.55

autocorr

Source:Nickell et al. (2005)

Model A Model B

b t b t

L.ur 0.86 47.61 0.86 47.51

ep 0.11 0.68 0.12 0.70

brr 2.33 5.61 2.32 5.61

bd 0.45 2.27 0.46 2.30

mbrrbd 3.72 3.75 3.75 3.78

mcoudnet -7.04 -6.14 -7.05 -6.14

mcotw -3.10 -2.98 -3.09 -2.97

D.udnet 6.55 3.16 6.55 3.16

co -0.90 -3.16 -0.89 -3.12

tw 1.54 1.77 1.53 1.76

lds -22.08 -10.19 -21.81 -10.11

tfphpc -17.29 -13.70 -17.28 -13.74

d2ms 0.23 0.98 0.24 1.02

rirl 2.22 1.93 2.20 1.91

tts 5.44 3.10 5.44 3.10

obs 599 599

time periods 33 33

numb groups 20 20

min groups 12 12

max groups 33 33

avg groups 29.95 29.95

coef 85 83

estimated cov 20 20

estimated autocorr 20 20

log likelihood -604.72 -598.52

estimated autocorr 43594 43409

Source: Data set 1

30

Table 2: Model A, replication like Model A in table 1. Model B, the same explanatory

variables as Model A, but pools ρ, i.e. no heteroscedastic lagged error term. Model C,

the same as Model B, but the lagged error term ρ, follows a calc process.

Model A Model B Model C

b t b t b t

L.ur .8635487 47.60779 .7744939 32.08049 .7924479 33.6793

ep .1108613 .6767546 -.0127239 -.0582341 -.2027108 -.7113987

brr 2.327419 5.612366 2.198545 4.124974 2.339849 3.969217

bd .4511384 2.271153 .5226619 2.195521 .5441488 1.616523

mbrrbd 3.722513 3.75492 5.098122 4.159219 4.772874 3.387187

mcoudnet -7.036643 -6.137761 -5.707323 -4.072997 -4.861822 -3.028288

mcotw -3.098725 -2.978097 -3.689448 -2.859484 -2.550337 -1.704073

D.udnet 6.550333 3.15664 2.265205 1.287162 3.42791 1.73165

co -.9015665 -3.155782 -.6419443 -1.743556 -.6871283 -2.091191

tw 1.542205 1.774337 .6883075 .6362186 .789933 .6849612

lds -22.0755 -10.18768 -15.90552 -9.945486 -18.61467 -9.706006

tfphpc -17.28824 -13.70104 -15.97227 -12.78158 -18.55733 -12.61648

d2ms .2342279 .9827281 .3667688 2.31497 .46535 2.468598

rirl 2.224254 1.928584 1.62581 1.47075 1.532278 1.27637

tts 5.444384 3.097698 4.128078 2.683663 3.283862 2.032268

obs 599 599 599

time periods 33 33 33

numb groups 20 20 20

min groups 12 12 12

max groups 33 33 33

avg groups 29.95 29.95 29.95

coef 85 85 85

estimated cov 20 20 1

estimated autocorr 20 20 20

log likelihood -604.7176 -385.3741 -434.1662

estimated autocorr 43593.92 28811.02 20096.14

Source: Data set 1

31

Table 3: The error term and stability restrictions. Data set 1. label stabrho

Stability

Country rhoi a1 a2 real root if > 0 1 + a1 + a2 > 0 1 − a1 + a2 > 0 1 − a2 > 0

Australia 0.46 -1.33 0.40 0.04 0.07 2.72 0.60

Austria -0.15 -0.72 -0.13 0.26 0.16 1.59 1.13

Belgium -0.59 -0.27 -0.51 0.53 0.22 0.76 1.51

Canada -0.30 -0.56 -0.26 0.34 0.18 1.30 1.26

Denmark -0.48 -0.38 -0.42 0.45 0.20 0.96 1.42

Finland -0.97 0.11 -0.84 0.84 0.27 0.06 1.84

France 0.28 -1.14 0.24 0.09 0.10 2.38 0.76

Germany -0.39 -0.48 -0.33 0.39 0.19 1.14 1.33

Ireland -0.25 -0.61 -0.22 0.31 0.17 1.39 1.22

Italy -0.65 -0.22 -0.56 0.57 0.23 0.66 1.56

Japan -1.11 0.25 -0.96 0.97 0.29 -0.20 1.96

Netherlands -0.77 -0.09 -0.66 0.67 0.24 0.43 1.66

New Zealand 3.18 -4.04 2.73 1.35 -0.31 7.77 -1.73

Norway -0.53 -0.33 -0.46 0.49 0.21 0.87 1.46

Portugal -1.28 0.42 -1.10 1.15 0.32 -0.52 2.10

Spain -0.97 0.10 -0.83 0.83 0.27 0.07 1.83

Sweden -0.38 -0.48 -0.33 0.39 0.19 1.15 1.33

Switzerland -0.67 -0.19 -0.58 0.59 0.23 0.61 1.58

United Kingdom -0.41 -0.45 -0.35 0.40 0.19 1.10 1.35

United States -0.38 -0.48 -0.33 0.39 0.19 1.15 1.33

32

Tab

le4:

The

long

term

effec

tsof

the

esti

mat

edco

effici

ents

inm

odel

A.D

ata

set

1.la

bel

inst

euro

pe

Dynam

icsi

mula

tion

∑ 95 90U−

∑ 69 60U

Con

trib

uti

onfr

omin

stit

u-

tion

sto

U(d

ynam

icsi

mu-

lation

)

Cal

cula

ted

by

actu

alch

ange

inin

stit

uti

onan

dlo

ng

term

form

ula

by

β̂∗∆

epl

1−

θ

Com

par

edto

theo

reti

cal

calc

ula

tion

Inst

ituit

ons

wit

hin

stit

u-

ions

wit

hou

tin

sti-

tuti

ons

∆U

∆U

Per

cent

replica

ted

co-

effici

ents

coeffi

cien

ts

inta

ble

5in

Nic

kell

etal

.

(200

5)

Rep

lica

ted

re-

sult

s

coeffi

cien

tsin

table

Nic

kell

etal

.(2

005)

brr

,bd

and

brr

bd

5.92

2.18

3.74

0.71

0.75

0.76

-0.0

5-0

.06

unio

ns(

co,

udnet

,

mco

udnet

)

2.2

2.18

0.02

0.00

0.08

0.08

-0.0

8-0

.07

twan

dtw

co3.

42.

181.

220.

230.

150.

150.

080.

09

ep2.

492.

180.

310.

060.

010.

020.

050.

04

Sum

5.29

1.00

1.00

1.00

Em

plo

ym

ent

pro

tect

ion

from

table

4in

Nic

kell

etal

.(2

005)

epl 9

8−

∑ 64 60ep

l=

0.27

∆U

=0.

288.

3per

cent

(epl

98

+∑ 87 8

0ep

l)/2

−∑ 64 6

0ep

l=

0.40

∆ep

l=

0.43

0.13

per

cent

33

Table 5: Model A is a replication of model 1 given in table 5 in Nickell et al. (2005) on

data set 2. Time period 1960-2004. label t2emp

(1)

U r p

b t

L.U r p 0.91 67.91

epl nic1 ext 0.51 3.52

brr nic ext 0.80 2.89

bd nic ext 0.03 0.24

mbrrbd ext 1.55 2.51

mcodudnet ext -3.41 -4.86

mcodtw ext -2.64 -2.56

D.udnet vis nic1 ext 1.51 0.79

co nic ext -0.21 -0.99

tw nic1 ext 2.28 2.81

lds ext -22.24 -9.12

Dprod hp ext -8.21 -8.42

D2m ext 0.38 1.11

RIRL ext -2.00 -2.09

TTS ext 7.69 5.01

obs 873

time periods 45

numb groups 20

min groups 33

max groups 45

avg groups 43.65

coef 92

est cov 20

est autocorr 20

log like -889.92

autocorr 62110

34

Table 6: Model 1 is a replication of model 1 given in table 5 in Nickell et al. (2005) on

data set 2. Time period 1960-1995. label t3emp

(1)

U r p

b t

L.U r p 0.91 47.75

epl nic1 ext 0.10 0.41

brr nic ext 1.43 3.95

bd nic ext 0.31 1.67

mbrrbd ext 1.27 1.59

mcodudnet ext -4.39 -4.39

mcodtw ext -3.38 -2.46

D.udnet vis nic1 ext -0.30 -0.14

co nic ext -0.08 -0.28

tw nic1 ext 0.56 0.63

lds ext -15.62 -9.51

Dprod hp ext -11.87 -12.21

D2m ext 0.22 0.75

RIRL ext -0.46 -0.68

TTS ext 10.53 6.77

obs 633

time periods 33

numb groups 20

min groups 21

max groups 33

avg groups 31.65

coef 83

est cov 20

est autocorr 20

log like -652.85

autocorr 1332912

35

Table 7: Replication of model 1 given in table 5 in Nickell et al. (2005) on data set 3.

Time period 1960 until 1995. label t5emp

(1)

U r p

Coef. t

L.U r p 0.889 45.214

epl back p -0.428 -2.962

ibrr p 1.023 2.967

ibd p -0.107 -0.626

mibrrbd p 0.785 1.004

micodudnet p -2.833 -6.677

mcodtw p 0.011 1.856

D.iudnet bd p 0.701 0.431

icoord p 0.180 2.684

TW -0.002 -0.261

lds p -14.992 -8.665

Dprod hp p -11.210 -11.994

D2m p 0.105 0.372

RIRL p -0.802 -1.176

TTS p 9.846 6.218

obs 633.000

time periods 33.000

numb groups 20.000

min groups 21.000

max groups 33.000

avg groups 31.650

coef 83.000

est cov 20.000

est autocorr 20.000

log like -653.156

autocorr 1.25e+06

36

Table 8: Replication of model 1 given in table 5 in Nickell et al. (2005) on data set 3.

Time period 1960 until 2004. label t7emp

(1)

U r p

Coef. t

L.U r p 0.872 56.310

epl back p -0.234 -1.976

ibrr p 1.226 4.014

ibd p -0.038 -0.242

mibrrbd p 1.520 2.203

micodudnet p -2.444 -6.833

mcodtw p 0.009 1.736

D.iudnet bd p 1.681 1.146

icoord p 0.124 2.106

TW -0.004 -0.467

lds p -11.487 -8.696

Dprod hp p -10.931 -13.395

D2m p -0.358 -1.521

RIRL p -1.103 -1.855

TTS p 9.031 6.414

obs 755.000

time periods 45.000

numb groups 20.000

min groups 24.000

max groups 45.000

avg groups 37.750

coef 94.000

est cov 20.000

est autocorr 20.000

log like -755.769

autocorr 2.88e+06

37

Figure 7: The replicated coefficients on data set 1 (model A in table 1) compared with

the coefficients in Nickell et al. (2005). label nick reg1a

Figure 8: Model B in table 1 relative to model A. Only the number of time dummies

differ. Data set 1. label nick reg1b

38

Figure 9: The country specific trend, time dummies and country specific effects. Model

A and data set 1 relative to the original results in Nickell et al. (2005). label nick reg1aa

39

Figure 10: Dynamic simulation of the coefficients estimated on data set 1 over the years

1960 to 1995. label dynsim1a

40

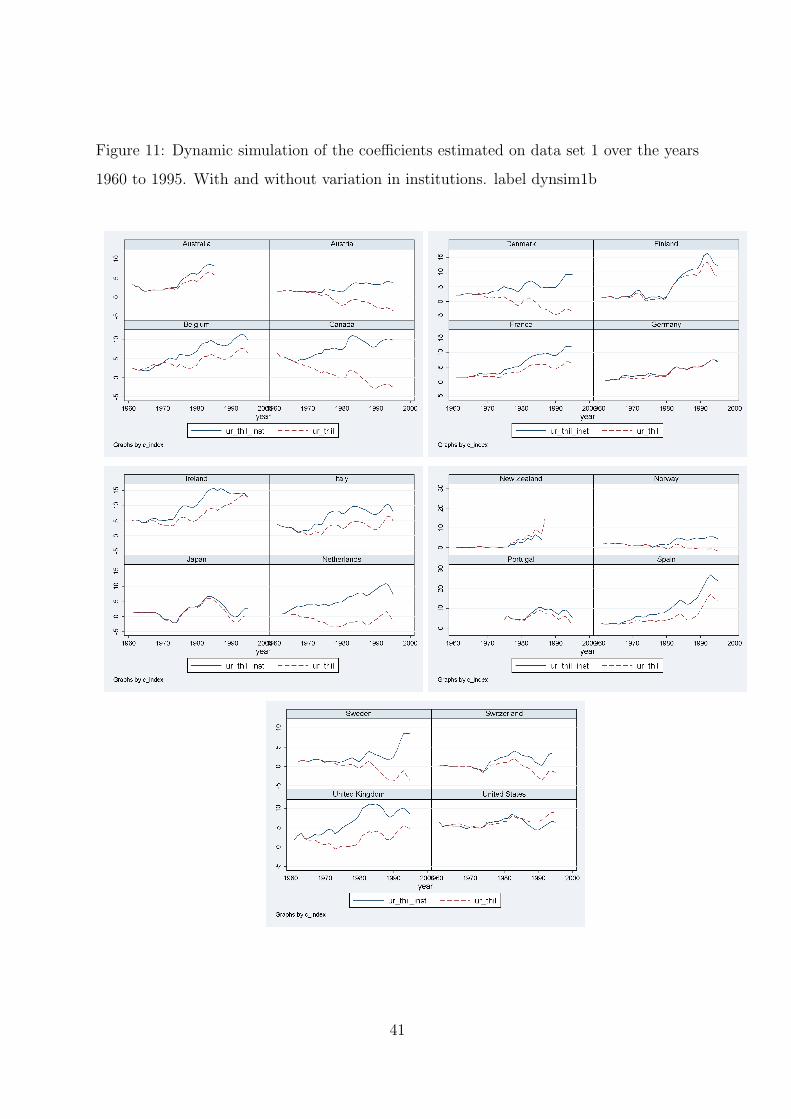

Figure 11: Dynamic simulation of the coefficients estimated on data set 1 over the years

1960 to 1995. With and without variation in institutions. label dynsim1b

41

Figure 12: Dynamic simulation of the coefficients estimated on data set 1 over the years

1960 to 1995. Excluding variation in one by one institution. label dynsim1c

42

Figure 13: Estimation of equation (1) on data set 2, compared with the coefficients in

Nickell et al. (2005). Period 1960-2004. label reg1a

Figure 14: Estimation of equation (1) on data set 2, compared with the coefficients in

Nickell et al. (2005). Time period 1960-1995

43

6 Background Data

44

Figure 15: The transformed equation 7. Model A in 1. Data set 1. label dynsim2a

45

Figure 16: The transformed equation 7. Model A in 1. Data set 1. label dynsim2b

46

Figure 17: Static simulation of model for unemployment in Nickell et al. (2005) over the

years 1960 to 2004. Estimated coefficients from table 5 are used in the simulation.

47

Figure 18: Dynamic simulation and actual unemployment. Coefficients in table 5 over

the years 1960 to 2004. Simulation and estimation on data set 2.

48

Figure 19: Dynamic simulation with and without the effect of institutions to unemploy-

ment. Coefficients in table 5 over the years 1960 to 2004. Simulation and estimation on

data set 2.

49

Tab

le9:

Unem

plo

ym

ent

asN

icke

llet

al.(2

005)

has

pre

sente

dth

edat

a,dat

ase

t2

countr

yY

r6064

Yr6

572

Yr7

379

Yr8

08

7Y

r8895

Yr9

6103

Yr1

04107

Aust

ralia

2.57

1.88

4.64

7.66

8.43

7.10

5.01

Aust

ria

1.87

1.50

1.32

3.11

4.67

5.30

5.82

Bel

gium

1.41

1.40

4.23

9.58

8.05

8.22

8.13

Can

ada

6.12

4.79

6.98

9.84

9.53

7.99

6.64

Den

mar

k1.

601.

233.

776.

687.

494.

984.

59

Fin

land

1.38

2.37

4.14

5.17

10.8

510

.93

8.21

Fra

nce

1.51

2.31

4.46

9.05

10.4

410

.44

9.63

Ger

man

y0.

460.

571.

835.

105.

927.

748.

72

Gre

ece

.3.

192.

086.

398.

3510

.94

10.2

5

Icel

and

.1.

571.

211.

483.

562.

942.

49

Irel

and

5.22

5.78

8.21

14.2

714

.90

6.65

4.38

Ital

y3.

484.

194.

877.

969.

9010

.27

7.82

Jap

an1.

311.

211.

832.

522.

464.

494.

16

Net

her

lands

0.56

1.08

3.20

7.50

6.00

3.85

4.36

New

Zea

land

0.11

0.37

0.74

3.95

8.14

6.00

4.20

Nor

way

1.95

1.55

1.74

2.44

5.13

3.82

4.20

Por

tuga

l.

3.11

5.63

8.23

5.48

5.34

7.49

Spai

n1.

812.

194.

2214

.51

15.0

012

.97

9.26

Sw

eden

1.65

2.01

1.99

2.75

4.62

5.72

5.07

Sw

itze

rlan

d0.

200.

000.

280.

612.

153.

283.

98

UK

3.08

3.49

4.81

10.4

48.

776.

005.

02

Unit

edSta

tes

5.82

4.51

6.51

7.75

6.16

4.95

5.00

Tot

al2.

222.

253.

586.

687.

556.

816.

11

Sour

ce:

Z:/

StH

/vic

/fra

Z/d

oes

tny

data

/vr0

8/R

eplic

N/t

emp1

.dta

50

Table 10: Macrovariables

Variable Time series, OECD definition

YC Gross Domestic Product (Market prices), Value

YQ V Gross Domestic Product (Market prices), Volume

Cp V Private Consumption, Volume

I V Total Fixed Investment (Excl Stockbuilding), Volume

Ig V Government Investment, Volume

NAWRU nawru

Ip V Private Fixed Investment (Excl Stockbuilding), Volume

Iph V Private investment in Housing 2, Volume

X V Exports Goods and Services, N.A. Basis, Volume

Pi d Import Price Goods and Services, Local Currency - deflator

Pgdp dm Deflator for GDP at Market Prices

CPI i Consumer Price Index

SUB Subsidies

TAXh Direct Taxes, Households

SSRG Social Security Contributions Received by Government

TAXind Indirect Taxes

IE Compensation of Employees

WAGE Wages and Salary

CRh Current Receipts Households

Cp Private Consumption, Household Account Basis

S r Saving Ratio

RW i Real Labour Cost

Wbus Wage Rate (Business Sector)

EPOP r Labour Force, Participation Ratio

L Labour Force, Total

N Total employment

U r Unemployment Rate

POP1564 Population, Total (15 and 64 years old, except USA, ESP, HUN, NZL, MEX see country’s notes)

M Money Stock

Is r Interest Rate, ShortTerm

Il r Interest Rate, LongTerm

MC V Imports of goods and services, value, local currency

Cg V Government consumption, volume

SBp V Stockbuilding private, volume

Source: OECD and others

51

Table 11: Constructed variables

Variable Constructed variables from time series data

t1 Employment tax rate

t2 Direct tax rate

t3 Indirect tax rate

TW Tax wedge

LABC Labour cost

infl Inflation rate

RIRL Real interest rate

prodhp Trade productivity

D2MS Acceleration in money supply

lds Labour demand shock

TTS Terms of trade shock

Dprod hp Deviations from labour productivity in the business sector

Average Hours Per Employee

Index of Relative Unit Labour Cost Manufacturing Sector, Common Currency

(Overall Competitiveness)

52

Table 12: Institutional variables

Variable Definition

BRR Average of brr66 and brr100. And brr66 is the average of r67a1-r67a4 and the same for brr100 OECD

brr67a1 Benefit replacement rate for workers with 66 percent of average earnings, first year, OECD (corresponds to brr66 in ? )

brr67a2 Benefit replacement rate for workers with 66 percent of average earnings, second and third year, OECD

brr67a4 Benefit replacement rate for workers with 66 percent of average earnings, fourth and fifth year, OECD

brr100a1 Benefit replacement rate for workers with average earnings, first year, OECD (corresponds to brr100 in ?)

brr100a2 Benefit replacement rate for workers with average earnings, second and third year, OECD

brr100a4 Benefit replacement rate for workers with average earnings, fourth and fifth year, OECD

bd66 Benefit duration for workers with 100 percent of average earnings, calculated

bd100 Benefit duration for workers with 66 percent of average earnings, calculated

iudnet Union density, OECD, interpolated

udnet nic1 Union density, Nickell (2006).

icentr Centralization, OECD, interpolated

cov Coverage, OECD

epl 1 Average employment protection (average of epl i and epl t), OECD table

epl 2 Average employment protection (average of epl i and epl t and epl c), OECD table

epl i Overall strictness of protection against (individual) dismissals, OECD table

epl c Overall strictness of regulation on collective dismissals, OECD table

epl t Overall strictness of regulation on temporary employment, OECD table

epl Overall employment protection, time series version from OECD

eplr Regular employment protection, time series version from OECD

eplt Temporary employment protection, time series version from OECD

ERTOT bo Average employment protection (sum of EP, FT and TWA), Belot and Ours

EP bo Protection open ended contracts, Belot and Ours

FT bo Protection fixed term contracts, Belot and Ours

TWA bo Protection temporary work agencies, Belot Ours

epl back Overall employment protection prolonged backwards via backcast by use of ERTOT bo from Belot and Ours

epl back 1 Employment protection open ended contracts, prolonged backwards via backcast by use of EP bo from Belot and Ours

icoord Coordination, OECD, interpolated

co back Coordination with backcast by use of Kenworthy

co ken Coordination, Kenworthys

ho Housing (percentage owner occupied), Oswald53

Figure 20: Actual unemployment. Data set 2 over the years 1960 to 2007. label ur

54