the residential development handbook - deloitte · spanish housing transactions and prices ... jobs...

TRANSCRIPT

@ 2018 Deloitte Financial Advisory1

The Residential Development HandbookInvestment & Financing Keys

Spain 2018

Financial Advisory I Real Estate

March 2018

@ 2018 Deloitte Financial Advisory2

► There is a lack of fully

permitted land, therefore

investments in land

management are necessary.

► The scarcity of construction

workforce may be a challenge.

► The sector is growing under the

ramp-up phase with financing

requirements.

► The industry is fragmented.

Players concentration is

expected.

2Supply&

Demand

4Key Drivers & Trends in Spain

3Investment & Financing Market 5 The Future of

Development

The Residential Development HandbookSpain 2018

EXECUTIVE SUMMARY

Market Overview1

► Digitalisation: Product trends & client

focus.

► Inorganic growth: Size is crucial to gain

efficiency.

► Industrialization: new technologies in

construction process and development

based on rotation.

► Platforms scalability: The business model

must be adjusted in line with growth.

► The residential development sector is still

fragmented. The Top 5 players account for ~6% of

the market in terms of units delivered and ~12% in

terms of ongoing developments.

► Strong appetite of international investors. The

environment is under institutionalization process

with 3 listed players with a long-only shareholder base.

► Equity has been an entry barrier in the

development market.

► GDP growth: +3.3% 2016 (+3.1%2017E).

► Unemployment rate has decreased by9.5 p.p since 2013, currently stands at16.6%. 1.2 m jobs have been created inthe last 4 years.

► 21 million of the total population between25-55 years. Therefore they are potentialhousing buyers.

► Spanish housing transactions and pricesshow a healthy recovery from minimumlevels, but when compared to Europeanlevels, there is still room to grow.

► Spanish housing stock decreasedheterogen by 24% from 2009 to 2016.Heterogeneous per province.

► New residential mortgages are increasingwhile aggregated mortgages volume isstill decreasing.

► Started housings have increased by 98% from

2013 to 2016 but are still far away from run rate

levels.

► New ongoing supply DTTL Observatory: 2,305

developments and 116k housings.

► Almost 80% of the total supply is located in 10

provinces.

► Madrid is leading the recovery. There is a lack of

supply with 5.5 housings per 1,000 inhabitants.

The recovery is selective.

► DTTL has identified 272 Hotspots in Spain.

► Big cities maintain a solid demand, whilst several

small and medium-sized cities have higher

growth rates.

► Housing sales prices increased by 6.6% from

2014 to 3Q17, showing diversity of the recovery.

Su

pp

lyD

em

an

d

@ 2018 Deloitte Financial Advisory3

10,910,0

8,0 8,0 7,9 7,7

6,5 6,45,8 5,5 5,4 5,3 5,1 4,7 4,4

0,0

2,0

4,0

6,0

8,0

10,0

12,0

Czech R

ep.

UK

Fra

nce

Hungary

Slo

venia

Pola

nd

Irla

nd

Italy

Austr

ia

Port

ugal

Denm

ark

Belg

ium

Spain

Germ

any

Neth

erl

ands

Annualneccesary

wages

EXECUTIVE SUMMARY

Spain has consolidated solid pillars for a sustained recovery as shown in the main macroeconomic.

Source: Deloitte

EU countries sample breakdown housing transactions:Housing transactions / 1,000 citizens

Source: Eurostat, Ministerio de Fomento, INE, Deloitte

0

5

10

15

20

Esto

nia

UK

Sw

ed

en

Lu

xe

mbo

urg

Fin

lan

d

Ma

lta

De

nm

ark

Hu

nga

ry

Fra

nce

Ne

therl

and

s

Po

rtu

ga

l

Be

lgiu

m

Sp

ain

Au

str

ia

Ita

ly

Ire

land

Year 2015 2015 - 2016 Variation (if available)

UE (Y15): 10.3

2.5%

-7.3% 0.4%

-4.8%6.0% 18.0%

7.7%14.1%

6.1%

Europe vs Spain

GROWTH

GDP3.1%

growth in 2017E

UNEMPLOYMENT RATE

Has decreased since 2013 and currently

stands at 16%

JOB CREATION

Jobs creation in the RE sector, is not

complemented by the Construction

sector.

DEMOGRAPHY21 million potential buyers between 25-

55 years

CONSUMER CONFIDENCE

INDEX102.8 points (base 100)

The Residential Development Handbook Spain 2018

Total housing affordability by annual necessary wages | 2015 DataSource: Eurostat, INE, Euromonitor International

Annual wage

=Average housing unit

@ 2018 Deloitte Financial Advisory4

EXECUTIVE SUMMARY

Source: Deloitte

Barcelona

Madrid

Guadalajara

Balears

Melilla

Palmas

Sevilla

Navarra

Araba

Cuenca

S.C. Tenerife

Segovia

Tarragona

Burgos

Lugo

Málaga

Coruña (A)

Asturias

Gipuzkoa

Cantabria

Ceuta

Huelva

Girona

Cádiz

Lleida

Huesca

Pontevedra

Salamanca

Soria

Ourense

Alicante

Murcia

Cáceres

Valladolid

Bizkaia

Teruel

Castellón

Valencia

Jaén

Toledo

Badajoz

Córdoba

Zamora

Ciudad Real

Zaragoza

La Rioja

Almería

Granada

Albacete

León

Palencia

Ávila

0%-5% -4% -2% -1%-3%-6%

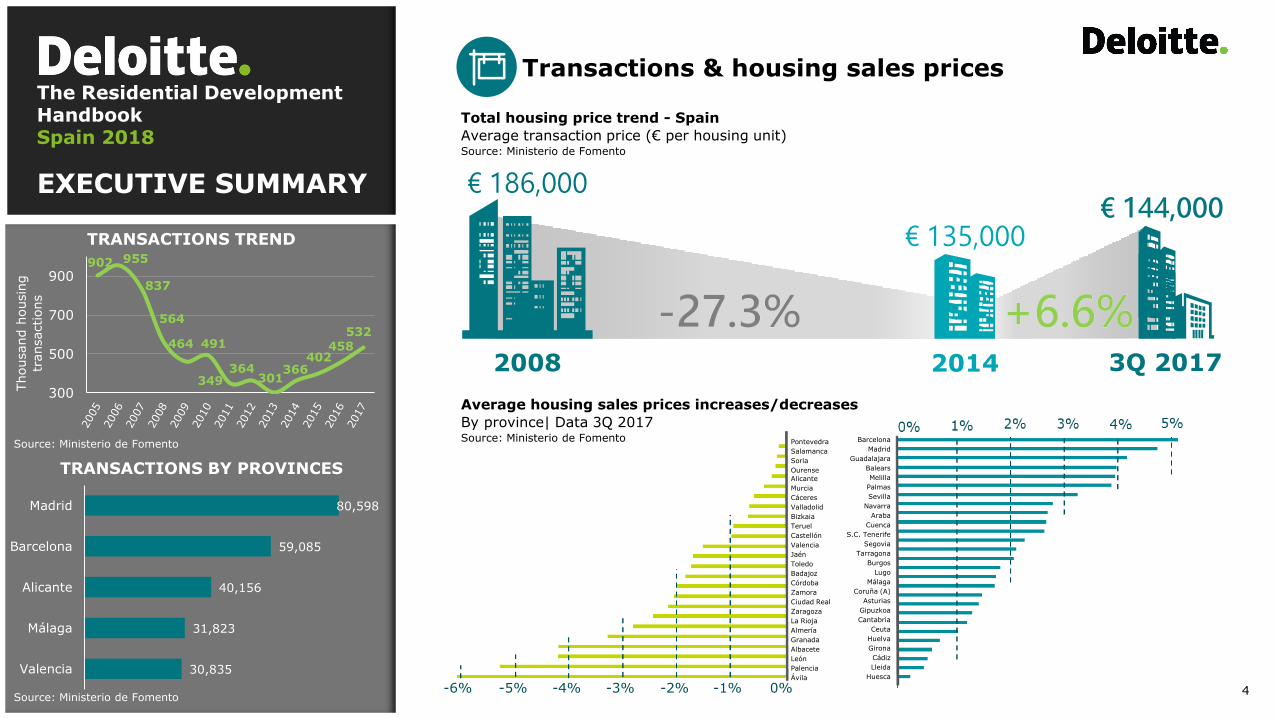

Total housing price trend - Spain

Average transaction price (€ per housing unit)Source: Ministerio de Fomento

Transactions & housing sales prices

2008 2014

€ 186,000

€ 135,000€ 144,000

3Q 2017

TRANSACTIONS TREND

The Residential Development Handbook Spain 2018

TRANSACTIONS BY PROVINCES

Average housing sales prices increases/decreases

By province| Data 3Q 2017Source: Ministerio de Fomento

Source: Ministerio de Fomento

Source: Ministerio de Fomento

902 955

837

564

464 491

349364

301366

402458

532

300

500

700

900

Thousand h

ousin

g

transactions

30,835

31,823

40,156

59,085

80,598

Valencia

Málaga

Alicante

Barcelona

Madrid

@ 2018 Deloitte Financial Advisory5

EXECUTIVE SUMMARY

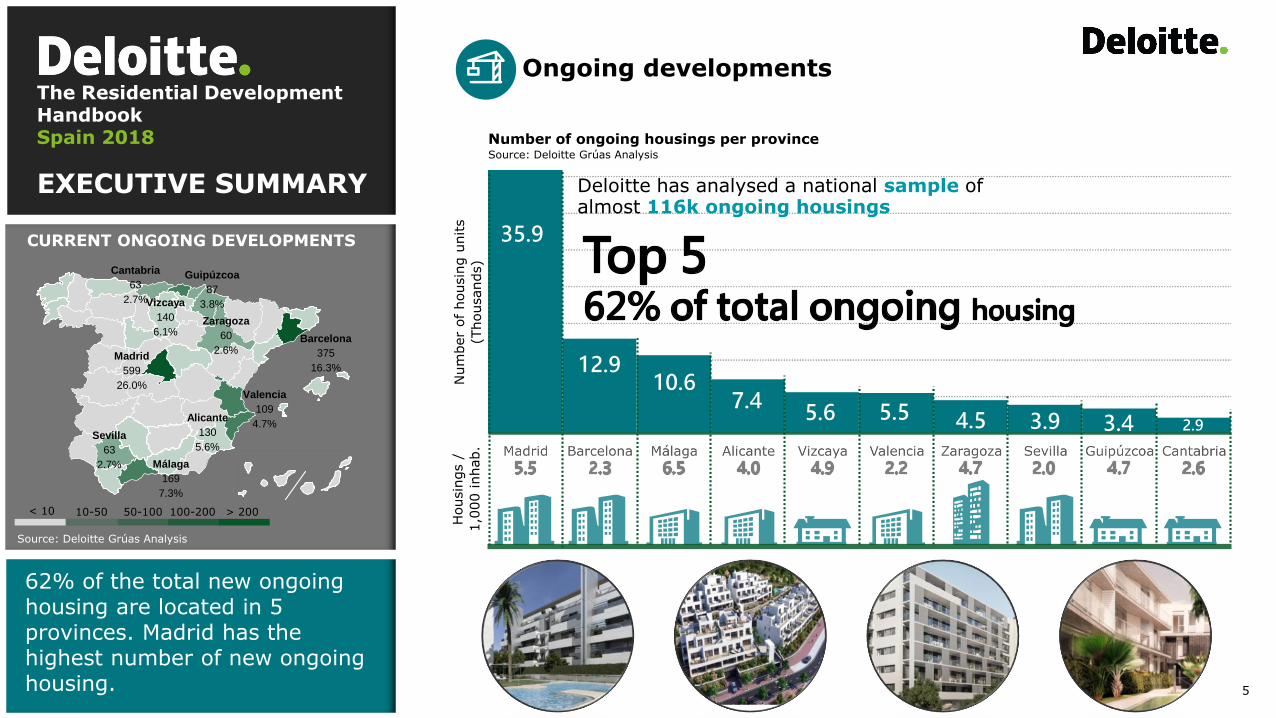

62% of the total new ongoing housing are located in 5 provinces. Madrid has the highest number of new ongoing housing.

Source: Deloitte

Ongoing developments

CURRENT ONGOING DEVELOPMENTS

The Residential Development Handbook Spain 2018 Number of ongoing housings per province

Source: Deloitte Grúas Analysis

50-10010-50 100-200 > 200< 10

Source: Deloitte Grúas Analysis

Madrid

599

26.0%

Málaga

169

7.3%

Barcelona

375

16.3%

Vizcaya

140

6.1%

Alicante

130

5.6%

Valencia

109

4.7%Sevilla

63

2.7%

Zaragoza

60

2.6%

Guipúzcoa

87

3.8%

Cantabria

63

2.7%

Num

ber

of

housin

g u

nits

(Thousands)

12.9

3.4

10.6

5.6 5.57.4

4.5 3.9 2.9

35.9

Housin

gs /

1,0

00 inhab.

Deloitte has analysed a national sample of almost 116k ongoing housings

@ 2018 Deloitte Financial Advisory6

EXECUTIVE SUMMARY

272 Hotspots have been identified in 158 locations in Spain.Most of the Hotspots are located in Madrid, the Mediterranean coast and the north of Spain.

Source: Deloitte

Deloitte Observatory

HOTSPOTS BY CHANCE OF SUCCESS

This study based on an algorithm filled with Deloitte Big Data Analytics, definesHotspots as locations with high chances of success for the real estateresidential development business.

The Residential Development Handbook Spain 2018

Hotspots

272

A #76

B #129

Extremely high28%

C #67

Very high47%

High25%

18

10

7

7

6

6

5

4

4

4

4

3

3

3

3

3

3

3

3

3

Madrid

Barcelona

Valencia

Zaragoza

Alicante

Sevilla

Málaga

Bilbao

Marbella

Murcia

Sabadell

Badalona

Benidorm

Coruña, A

Gijón

Oviedo

Palma de Mallorca

Pamplona

Terrassa

Torrejón de Ardoz3-9 10-19 20-40 >40<3

Hotspots

By provinceSource: Deloitte Grúas Analysis

59

47

22

14

11

11

9

7

7

6

5

5

5

44

33

3

3

3

3

3

2

2

2

2

2

#

20

Ranking of municipalities – Top 20

By Hotspots areasSource: Deloitte Grúas Analysis

Source: Deloitte Grúas Analysis

@ 2018 Deloitte Financial Advisory7

EXECUTIVE SUMMARY

Most of the residential development business is comprised by small & medium-sized developers:79% of them are developing a 30%

DevelopersThe Residential Development Handbook Spain 2018 # Developers

>560100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

# Housings

>116k

# Developers

>>>

# Housings

< 5 developments 5 - 15 developments 16 - 30 developments > 30 developments

1% >>> 12%

3% >>> 19%

17% >>> 39%

79% >>> 30%

Sm

all

& m

ed

ium

-siz

ed

develo

pers

Most of the residential development business

comprises small & medium-sized

developers:

i) 80%* have less than

5 ongoing

developments.

ii) c.96%* of them are

developing 70% of the

total ongoing housings.

* The significance of small & medium-sized

developers could even be greater; however,

the available public information shows these

market shares

Source: Company´s Public Available Information

Source: Deloitte Grúas Analysis

Top 5 Developers Rest of the Market

39%

61%

42%58%

6%

94%

@ 2018 Deloitte Financial Advisory8

EXECUTIVE SUMMARY

Spanish residential market continues to be attractive for international investors.

COMPETITIVE LANDSCAPE

Investment trendsThe Residential Development Handbook Spain 2018

Solid fundamentals

Institutional profile

New competitive landscape

Different typologies of players

High investment activity

@ 2018 Deloitte Financial Advisory9

EXECUTIVE SUMMARY

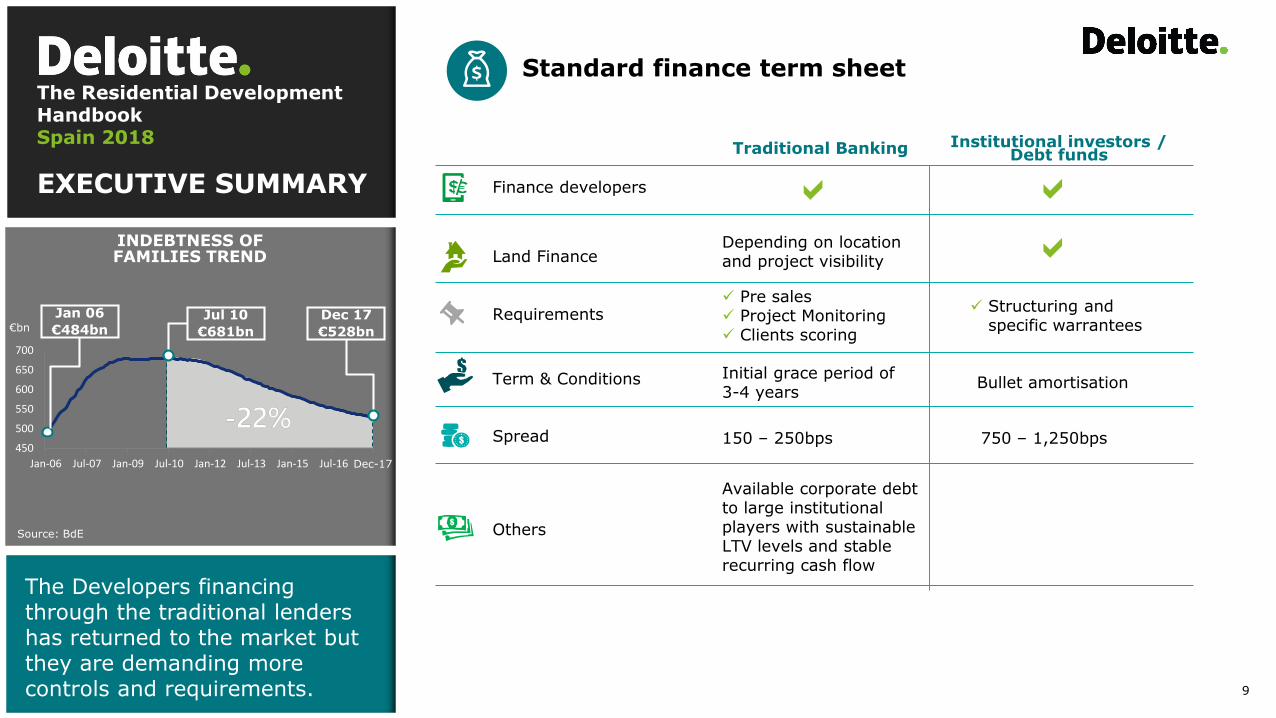

The Developers financing through the traditional lenders has returned to the market but they are demanding more controls and requirements.

INDEBTNESS OF FAMILIES TREND

Requirements

Finance developers

Pre sales Project Monitoring Clients scoring

Land Finance

Term & Conditions

Depending on location and project visibility

Spread 150 – 250bps 750 – 1,250bps

Initial grace period of 3-4 years

Bullet amortisation

Others

Available corporate debt to large institutional players with sustainable LTV levels and stable recurring cash flow

Structuring and specific warrantees

Standard finance term sheet

Traditional Banking Institutional investors / Debt funds

The Residential Development Handbook Spain 2018

€bnDec 17

€528bn

Jul 10

€681bn

Jan 06

€484bn

450

500

550

600

650

700

Jan-06 Jul-07 Jan-09 Jul-10 Jan-12 Jul-13 Jan-15 Jul-16 Dec-17

Source: BdE

@ 2018 Deloitte Financial Advisory10

EXECUTIVE SUMMARY

Key factorsThe Residential Development Handbook Spain 2018

Players

• Fragmented industry

• Changing landscape

Demand & Supply

• Diverse speeds of growth with and demanding customers

• Lack of supply and risks of productivity capacity

Construction costs

• Scarcity of qualified workforce

• Material costs

Financing

• Financing has returned

• Higher control and requirements

Growth/Land acquisition

• Lack of Fully Permitted Land land

• Entry barriersM&A

Advisory

Multidisciplinary

DD

Valuation &

Business

Modelling

Technical

Advisory &

Project

Monitoring

Debt

Advisory &

Treasury

ServicesCapital

Advisory

Land

Management

NPLs/REOs

Expertise

Prop

Tech

@ 2018 Deloitte Financial Advisory11

WHAT IS

NEXT?

The Residential Development Handbook Spain 2018

@ 2018 Deloitte Financial Advisory12

EXECUTIVE SUMMARY

BREEAM and LEED certifications are the most significant sustainability certifications worldwide. Both standards are regularly updated in line with the market.

The Future of DevelopmentThe Residential Development Handbook Spain 2018

Residential

Development

Trends

Digitalisation

IndustrializationPlatforms

scalability

Inorganic

Growth

LEADING SUSTAINABILITY CERTIFICATIONS

@ 2018 Deloitte Financial Advisory13

Deloitte. Alberto Valls, MRICSManaging Partner

Financial Advisory || Real Estate

Gonzalo Gallego, MRICSPartner

Financial Advisory || Real Estate

Juan Ramón Rubio ZalabardoDirectorFinancial Advisory || Real [email protected]

Francisco BoisoDirectorFinancial Advisory || Real [email protected]

Pablo Rodríguez FominayaSenior ManagerFinancial Advisory || Real [email protected]

Mónica CayuelaManagerFinancial Advisory || Real Estate [email protected]

Javier CuarteroAssociateFinancial Advisory || Real [email protected]

Jose Luís Martin PérezAnalystFinancial Advisory || Real [email protected]

Juan GalobartAnalystFinancial Advisory || Real [email protected]

Angela LarrabeitiAnalystFinancial Advisory || Real [email protected]

The Residential Development HandbookInvestment & Financing KeysSpain 2018

#TheResidentialDevelopmentHandbook