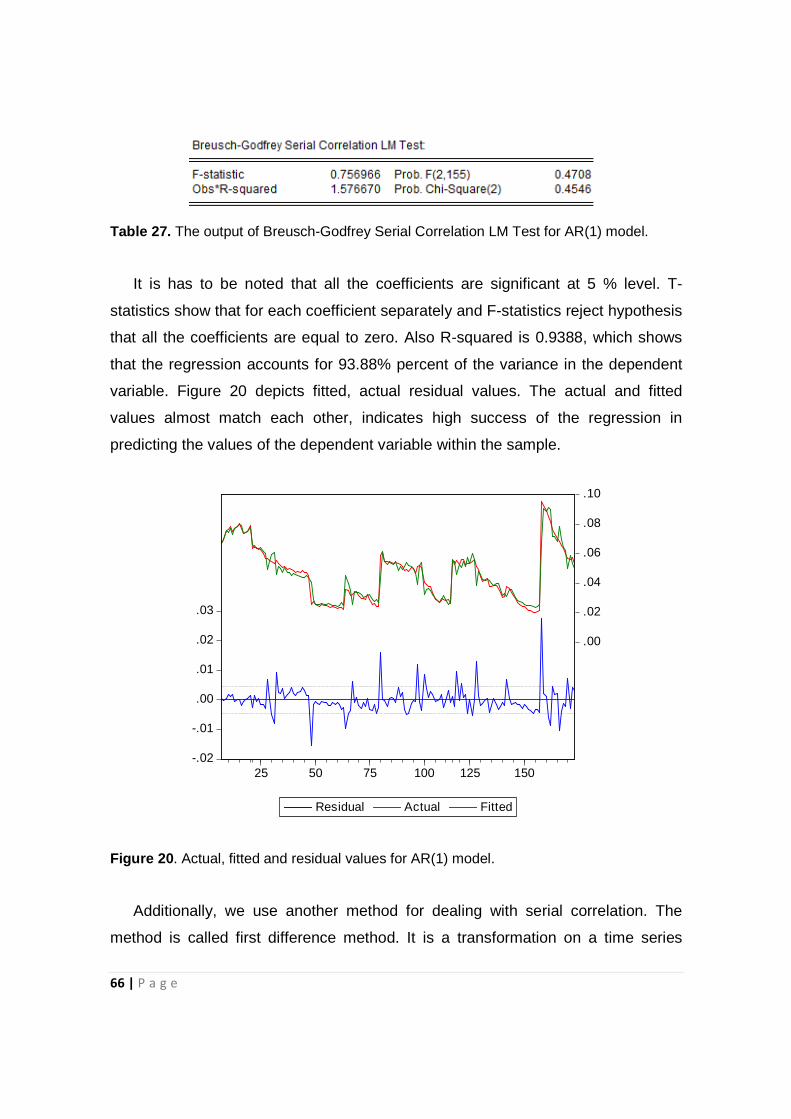

the relationship between tax rates and budgetary...

TRANSCRIPT

The relationship between tax rates and budgetary

income. Adaptability of the Laffer curve in

budgetary planning

MASTER THESIS

Authors Academic Advisor

Sarunas Cerekas Erik Strøjer Madsen

MSc in Finance and International Business Department of Economics and

Business

Arturas Gumuliauskas

MSc in Finance and International Business

June 2012

Table of Contents

1. INTRODUCTION ................................................................................................................. 3

2. THEORY OF TAXES .......................................................................................................... 5

2.1. Tax history ...................................................................................................................... 5

2.2. Concept of taxes ............................................................................................................. 7

2.3. Classification of taxes ..................................................................................................... 8

2.4. Laffer Curve .................................................................................................................... 9

2.5. Personal Income Tax ..................................................................................................... 15

2.6. Value Added Tax ........................................................................................................... 17

3. TAX ANALYSIS ................................................................................................................. 21

3.1. GDP dynamics .............................................................................................................. 21

3.2. Budgetary dynamics ..................................................................................................... 26

3.3. Revenue composition ................................................................................................... 33

3.4. Income tax overview .................................................................................................... 35

3.5. VAT overview ............................................................................................................... 47

4. LABOR TAX REVENUE ESTIMATION ........................................................................... 56

4.1. Labor tax ratio determination ....................................................................................... 56

4.2. Labor tax revenue determination ................................................................................. 58

4.3. The Data ....................................................................................................................... 61

4.4. Model ........................................................................................................................... 62

4.5. Results .......................................................................................................................... 69

5. VAT REVENUE ESTIMATION ......................................................................................... 71

5.1. VAT Revenue Determination......................................................................................... 72

5.2. The Data ....................................................................................................................... 76

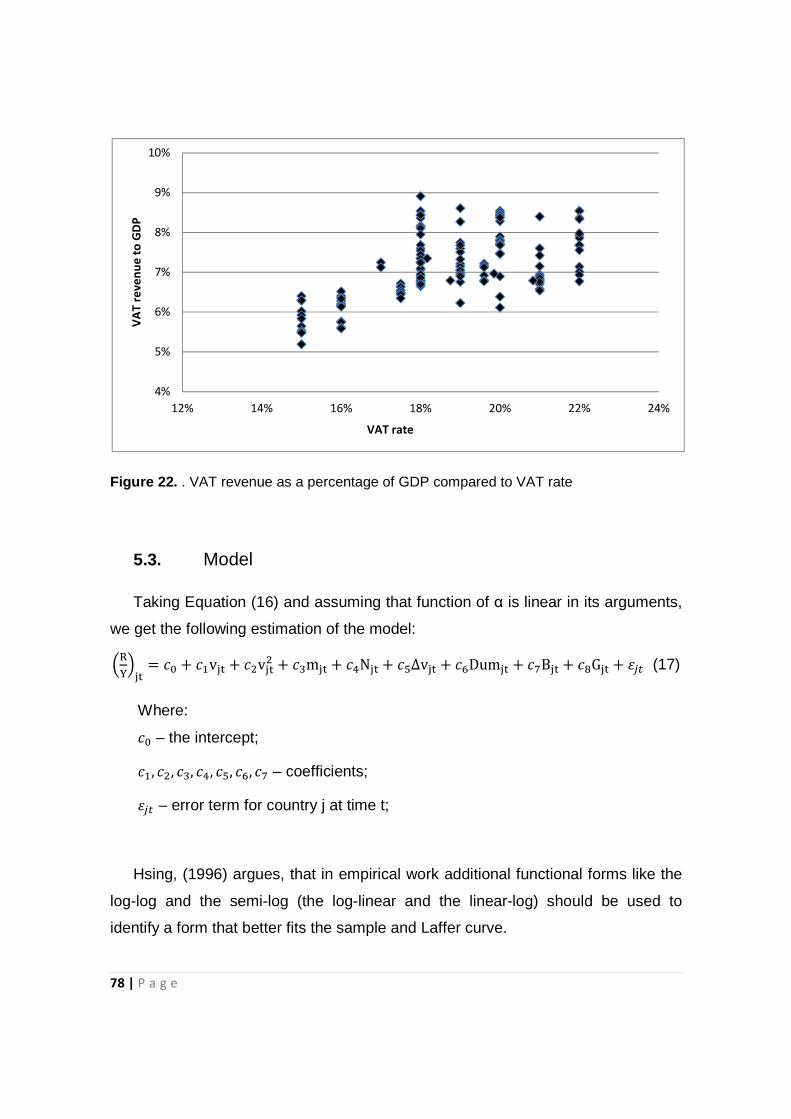

5.3. Model ........................................................................................................................... 78

5.3.1. Linear-Linear Model .................................................................................................. 79

5.3.2. Log- Log Model ......................................................................................................... 83

5.4. Results .......................................................................................................................... 86

6. CONCLUSION ................................................................................................................... 89

7. REFERENCES .................................................................................................................. 91

1. INTRODUCTION

"In this world nothing is certain but death and taxes."

--Benjamin Franklin, in a letter to M. Leroy, 1789.

Relying on these words of wisdom we should not fight taxes but learn to live

with them. History shows that changes in tax systems were common practice and

one can assume that the present system will continue to adopt changes based on

the state of public finances and extent of international trade, making the topic of

anticipating shift in taxation highly relevant. Taxes are the backbone of general

government revenue for countries across the globe and the imbalances between

revenue and expenditure often are the sources of political quarrels and economic

swings.

Due to the effects of globalization and free capital movement, which are

especially evident in economic and political unions, market participants are free to

choose the country of activity. Generally market participants are concerned with

the overall fiscal stability and tend to favor more stable countries. Countries with

the most significant or unexpected fiscal policy adjustments tend to be regarded as

slightly unstable and unpredictable, transforming them into risky markets with an

unattractive environment thus evoking the negative effect of capital flight from the

country.

Unsustainable levels of debt to GDP and budgetary deficits constitute a lethal

combination and have become a material topic for policy makers. Recent events

including the Greek debt restructuring deal, that was executed in March 2012 and

huge concerns aimed at similarly indebted South European countries of Portugal,

Italy and Spain raise the topic of austerity measures. Generally three ways of

budgetary balancing are used in practice: cuts in expenditures, increases in

revenues and borrowing, with the third option being the preferred choice of most

4 | P a g e

governments. However an initiative of fiscal austerity measures1 for most of the

European Union member states has been enacted on May 2012; it severely

curtailed the use of borrowing by general government, especially in the case of

member states that have and excessive and hardly sustainable debt to GDP ratio

of 60 %.

Since it is difficult to argue against the use of any of the two remaining

budgetary balancing measures, we will focus our thesis on the revenue maximising

measures that are at the disposal of individual countries. We identified the two

dominating taxes used by EU member states – labor tax and value added tax.

Each of the taxes will be estimated based on the Laffer theory of revenue

maximization. In theory Laffer Curve explains the parabolic relationship between

tax revenue and tax rate. The objective is to define the model for tax revenue to

see if the model is robust and fits with the theory of Laffer Curve. As a final result,

the revenue maximizing labor tax and value added tax rates will be computed and

compared to existing tax rates in different European countries.

The first section explores the basic theory of the taxes, including the concept of

the Laffer Curve. The second section presents the macroeconomic situation of the

sample countries and analyses labor tax and value added tax in more depth.

Finally, the models and estimations for both labor tax revenue and value added tax

revenue are estimated with the conclusions along with a summary presented at the

end of the paper.

1 Treaty on Stability, Coordination and Governance in the Economic and Monetary Union

5 | P a g e

2. THEORY OF TAXES

The Oxford dictionary states that a tax (Latin taxare: ‘to censure, charge,

compute‘) is a compulsory contribution to state revenue, levied by the government

on workers' income and business profits, or added to the cost of some goods,

services , and transactions. Taxes are not voluntary payments or donations in their

essence, but rather enforced contributions with failures to comply resulting in state

prosecution and punishment by law.

According to Meidūnas V., Puzinauskas (2001), no services or goods are

granted directly to the individual taxpayer for the payment of taxes. Funds are

accumulated and later dispensed through the budgetary mechanism according to

current National priorities. Budgetary expenditures exceeding revenue can only be

offset by borrowing or increasing tax rates, meaning that budgetary sustainability is

an essential element for the existence of a sovereign nation.

History shows that changes in tax systems were common practice and one can

assume that the present system will continue to adopt changes based on the state

of public finances and extent of international trade, making the topic of anticipating

shift in taxation highly relevant.

2.1. Tax history

Taxation can be considered as an integral part of society. With the evolution of

states came changes in the means of raising funds for military activities, expansion

and common social affairs (Meidūnas V., Puzinauskas, P, 2001). Taxes in all its

forms played a crucial role in the development of the modern state. The first

documented tax system was recorded in Ancient Egypt around 3000 BC, when

during a biennial event the Pharaoh would appear before his people and collect

taxes. Along with taxation came immunity from taxation to the privileged groups

with the first documented occurrence around 2600 BC for temple staff and the

property of temples and foundations.

6 | P a g e

Ancient Mesopotamian records provide more insight to the extent and methods

used in the primitive taxation systems. Due to the lack of a unified measure of

value, currently played by currency, taxes were paid in kind. Some periods saw

excessive taxation with a poll tax requiring each man to deliver a cow or a sheep to

the authorities, tolls and duties levied on the merchants required a portion of

transported goods to be paid. The most burdensome obligation frequently recorded

in history is the labor obligation, meaning that households were required to perform

certain deeds, including military service, for the state or local powers. A form of

labor obligation- serfdom- was common in Europe until its cancellation in late XIX

century, with obligations reaching 6 days of labor per week for every employable

household member.

Taxation levels varied depending on the state of public finance and in certain

countries displayed high levels of flexibility. In 167 BC due to successful expansion

and income generated from recently captured provinces, the Roman Empire

revoked the tax against land owned by its citizens in Italy. The Roman Empire also

practiced a novel approach to tax collection by introducing the model of private tax

collectors called ‘publicani’ at the expense of tax payers resulting in excess tax

rates.

As stated by Meidūnas V., Puzinauskas, (2001), the process of centralization of

political power in Europe that started in XV-XVI century caused serious financial

problems due to increased military, administrative and other expenses and was a

catalyst for change in taxation. The new movement, called mercantilism, focused

on enriching the state from international trade by decreasing taxation on exports

and increasing taxation on imports and laid the foundation of the basic principles of

modern customs and duty policies. Successive years saw growing concerns on the

topic of taxes with numerous proposals offered, from the Physiocratic position of a

single tax based on land ownership, since all the goods produced stem from land,

to the classical finance school position of minimizing taxes and the role of the state

altogether.

Two major schools of the modern economic thought on taxation are the ones of

Neo-Keynesian and Neo-classicists. The first movement envisions taxes as a

7 | P a g e

regulatory mechanism for manufacturing and industry and the tax system as an

anti-inflation and anti-recession model aimed at countering economic cycles and

thus smoothening economic swings. This is theoretically achieved by increasing

the tax burden and imposing additional constraints during the growth cycle and

contrary - decreasing the tax burden and increasing public expenditure during the

contraction cycle in the economy. The opposing economic school – the Neo-

classicists – holds a contradicting approach to taxes and believes in the self

regulating capabilities of the free market. According to them competition itself holds

the necessary regulatory power and the role of taxes and government in general

should be limited to warranting an effective balance of supply and demand and

ensuring local and national security (Stačiokas, R.,Rimas, J., 2003)

However taxation systems are constantly changing and the current model is

most likely simply a stage of the ongoing transition.

2.2. Concept of taxes

According to Stačiokas, R.,Rimas, J., (2003), taxes are the primary means of

funding public services such as security from external threats, internal policing and

sustaining public order, health care, social care, education, major infrastructure

projects, etc. Global practice shows that most of the public services cannot be

successfully outsourced through private businesses, since in many instances

projects might have negative net present value or the service might generate

insufficient return on investment. In the case of policing functions, privately owned

subjects might not be trustworthy with extremely fertile ground for corruption.

Generally it is difficult to evaluate the extent of public services consumed by

separate individuals, therefore common practice is taxation based on capability by

the subject.

In modern economics, fiscal policy and taxation rates can be a distortive

element. A lag factor exists in the administrative and functional level as well as in

the identification of economic cycles. This means that fiscal policy adjustments and

taxation rate changes require extensive discussion in the government level prior to

8 | P a g e

the decision. Substantial lag is also evident between the moment of resolution and

the actual effect that the resolution produces. Economic cycles are judged by major

macroeconomic rates such as inflation rates and Gross Domestic Product (GDP)

rates which by themselves are lagging indicators. Therefore reacting to economic

cycles through fiscal changes presents significant challenges and has the power to

trigger severe budgetary constraints.

2.3. Classification of taxes

In modern times individual taxes are composed of five essential elements

(classification supplied by Meidūnas V., Puzinauskas, P, 2001):

• A tax subject is a person who is assigned the obligation to pay taxes.

Commonly the tax subject and the actual tax payer are congruous, but in

certain cases they might not coincide (in the case of value added tax, the tax

subject is the consumer of the product, but the payer is the seller of the

product).

• A tax object is the actual object that is being taxed like income, services,

goods, assets, etc.

• The unit of taxation is a unit of measurement that is required for the estimation

of the amount of tax payable, like a currency unit for income tax, a hectare for

land taxes, capacity for excise duties.

• The tax rate is amount of tax required per unit of taxation. Usually the tax rate

is expressed in a percentage value (income tax, goods and services tax), it can

also be expressed as a fixed amount (diesel, tobacco).

• A tax exemption is a special tax rate reduction for certain tax subjects. Tax

exemptions may be temporary or permanent, compulsory or allowable. A tax

credit (a delay of payments) and tax holiday (a waiver of taxes for a certain

period of time) are both forms of tax exemption.

In modern tax theory, taxes are broadly categorized into two branches- direct

and indirect taxes. The distinction is made based on tax object and the relation

9 | P a g e

between the tax subject and state- directly from income and assets or indirectly

from the price system (added to the price of goods sold within a state). Classifying

individual taxes into these major branches is a fairly subjective matter because

most direct taxes like corporate revenue taxes can be argued to be transferable to

the consumer in the pricing process, but the dominant classification is common and

based on best practice.

The most widespread direct tax is the income tax, levied on personal income

and corporate revenue. Other examples of direct taxes are property taxes, land

taxes, inheritance taxes, capital, capital gains taxes and other. The most common

indirect taxes are levied on goods and services, like the Value Added Tax, the

Goods and Sales Tax and other taxes that actually fall on the consumer but are

paid by the seller, like excise duties on oil products, alcohol, tobacco and other

goods that are generally regulated by the government or belong to monopolist

industries.

A different type of tax is the Ecological tax, the subject of which is the

consumption of polluting materials like most oil products. The tax revenue is not

directed to the national or municipal budgets but is rather accumulated for dealing

with prevention and consequences of pollution. Another specific tax exists in the

European Union and is levied on the imports of agricultural products, the proceeds

of which are directed to the EU budget.

In our thesis we will focus on two major taxes- one from each branch- personal

income tax and Value Added Tax. The particular taxes were chosen based on their

prevalence globally and the extent of budgetary income they generate.

2.4. Laffer Curve

As the stagflation, high unemployment and high inflation appeared in the 1970s,

demand side policies were unable to solve such type of the problems (van Duijn,

1982). However, supply-side economists believed that the reason for stagflation is

an excessive tax burden and an economical over-regulation by the government. In

10 | P a g e

order to solve stagflation problem, the policy of a tax reduction and a deregulation

of the economy must be pursued (Burda, Wyplosz, 1993). Supply

expressed in the Laffer curve which depicts the expected rel

revenue and tax rate.

The Laffer curve is named after economist Art Laffer, who is said to have drawn

this curve on a napkin in a Washington restaurant in 1974. The Laffer curve states

that there is parabolic relationship between tax

noted, “there are always two tax rates that yield the same revenues” (Laffer, 1986).

That means that taxable income changes when tax rate is altered, but there is a

point where reduction in taxable income from higher ta

enough to completely offset the higher tax rate. This point is called “revenue

maximizing” point.

Laffer curve is the illustration of a dynamic scoring model (Fig

scoring model (Figure 1a) assumes that the higher the ta

revenue is collected. One can contradict that if tax rate was 100 per cent, no one

would work and thus no tax revenue would be collected. Also, if tax rate was 0 per

cent, obviously no tax revenue would be collected as well. This lead

that relationship between tax rate and tax revenue must be parabolic.

Figure 1. Comparison of the static scoring and dynamic scoring.

order to solve stagflation problem, the policy of a tax reduction and a deregulation

of the economy must be pursued (Burda, Wyplosz, 1993). Supply

expressed in the Laffer curve which depicts the expected relationship between tax

The Laffer curve is named after economist Art Laffer, who is said to have drawn

this curve on a napkin in a Washington restaurant in 1974. The Laffer curve states

that there is parabolic relationship between tax rates and tax revenue. As Art Laffer

noted, “there are always two tax rates that yield the same revenues” (Laffer, 1986).

That means that taxable income changes when tax rate is altered, but there is a

point where reduction in taxable income from higher tax rates becomes large

enough to completely offset the higher tax rate. This point is called “revenue

Laffer curve is the illustration of a dynamic scoring model (Fig

igure 1a) assumes that the higher the tax rate the higher tax

revenue is collected. One can contradict that if tax rate was 100 per cent, no one

would work and thus no tax revenue would be collected. Also, if tax rate was 0 per

cent, obviously no tax revenue would be collected as well. This lead

that relationship between tax rate and tax revenue must be parabolic.

. Comparison of the static scoring and dynamic scoring.

order to solve stagflation problem, the policy of a tax reduction and a deregulation

of the economy must be pursued (Burda, Wyplosz, 1993). Supply-side ideas are

ationship between tax

The Laffer curve is named after economist Art Laffer, who is said to have drawn

this curve on a napkin in a Washington restaurant in 1974. The Laffer curve states

rates and tax revenue. As Art Laffer

noted, “there are always two tax rates that yield the same revenues” (Laffer, 1986).

That means that taxable income changes when tax rate is altered, but there is a

x rates becomes large

enough to completely offset the higher tax rate. This point is called “revenue-

Laffer curve is the illustration of a dynamic scoring model (Figure 1b). Static

x rate the higher tax

revenue is collected. One can contradict that if tax rate was 100 per cent, no one

would work and thus no tax revenue would be collected. Also, if tax rate was 0 per

cent, obviously no tax revenue would be collected as well. This leads to a notion

that relationship between tax rate and tax revenue must be parabolic.

11 | P a g e

Laffer assumes that too high tax rates make people to be inactive

Figure 2 illustrates extreme occasion when tax rate is 100 per cent. High taxation

rate leads to low production, low incomes and, consequently, to low tax revenues

(Heijman, van Ophem, 2005). Additionally, people may become active in the black

labor economy. As Friedman et al

are generally correlated with a higher share of the unofficial economy. Lower tax

rates, conversely, make people to withdraw from the black economy and become

officially active. Point B in Figure 2 shows “reve

government can reach optimum tax rate and collect maximum possible tax

revenue.

Figure 2. Laffer Curve

As Mitchell (2009) argues revenue maximizing point is not the best for whole

economy. Ideal policy is reached in growth max

somewhere on upward sloping section of the Laffer curve. Growth maximizing

point is greater than zero, because there is a need for tax revenue to ensure

market economy function. Society needs such things as public safety,

courts, and healthcare.

The Laffer curve explains relationship between tax rate and tax revenue.

However, in the real world tax rate changes are not made in isolation with other

economic aspects. Beczi (2000) analyses what happens if the government

Laffer assumes that too high tax rates make people to be inactive

extreme occasion when tax rate is 100 per cent. High taxation

rate leads to low production, low incomes and, consequently, to low tax revenues

(Heijman, van Ophem, 2005). Additionally, people may become active in the black

labor economy. As Friedman et al (Friedman et al, 2000) shows, higher tax rates

are generally correlated with a higher share of the unofficial economy. Lower tax

rates, conversely, make people to withdraw from the black economy and become

officially active. Point B in Figure 2 shows “revenue-maximizing” level where

government can reach optimum tax rate and collect maximum possible tax

As Mitchell (2009) argues revenue maximizing point is not the best for whole

economy. Ideal policy is reached in growth maximizing point (Figure 2), which is

somewhere on upward sloping section of the Laffer curve. Growth maximizing

point is greater than zero, because there is a need for tax revenue to ensure

market economy function. Society needs such things as public safety,

The Laffer curve explains relationship between tax rate and tax revenue.

However, in the real world tax rate changes are not made in isolation with other

economic aspects. Beczi (2000) analyses what happens if the government

Laffer assumes that too high tax rates make people to be inactive – Point C in

extreme occasion when tax rate is 100 per cent. High taxation

rate leads to low production, low incomes and, consequently, to low tax revenues

(Heijman, van Ophem, 2005). Additionally, people may become active in the black

(Friedman et al, 2000) shows, higher tax rates

are generally correlated with a higher share of the unofficial economy. Lower tax

rates, conversely, make people to withdraw from the black economy and become

maximizing” level where

government can reach optimum tax rate and collect maximum possible tax

As Mitchell (2009) argues revenue maximizing point is not the best for whole

imizing point (Figure 2), which is

somewhere on upward sloping section of the Laffer curve. Growth maximizing

point is greater than zero, because there is a need for tax revenue to ensure

market economy function. Society needs such things as public safety, honest

The Laffer curve explains relationship between tax rate and tax revenue.

However, in the real world tax rate changes are not made in isolation with other

economic aspects. Beczi (2000) analyses what happens if the government actively

12 | P a g e

spend its revenues, as it is obvious in the real world. If the government spends

more revenues on taxed goods, it will increase the demand for good. This action

will offset the decrease in tax revenue caused by tax increase. Therefore, revenue

maximizing tax rate will rise. In Figure 3 one can see that because of demand

curve shift, revenue-maximizing tax rate moves from Point A to Point E. Finally

Beczi (2000) concludes that if government cuts taxes and at the same time rises

government consumption and decreases public investments, it increases the

likelihood that optimal tax revenues are lost. Tax policy must be related to both

public investment and public spending.

Figure 3. The impact on tax rate due to demand curve shift.

Furthermore, Henderson (1981) points out interesting idea that real

curve is more complex. It looks like in Figure 4, because, as Henderson argues,

tax rate cut would not necessarily cause people to work more.

spend its revenues, as it is obvious in the real world. If the government spends

more revenues on taxed goods, it will increase the demand for good. This action

will offset the decrease in tax revenue caused by tax increase. Therefore, revenue

ximizing tax rate will rise. In Figure 3 one can see that because of demand

maximizing tax rate moves from Point A to Point E. Finally

) concludes that if government cuts taxes and at the same time rises

on and decreases public investments, it increases the

likelihood that optimal tax revenues are lost. Tax policy must be related to both

public investment and public spending.

The impact on tax rate due to demand curve shift.

Furthermore, Henderson (1981) points out interesting idea that real

curve is more complex. It looks like in Figure 4, because, as Henderson argues,

tax rate cut would not necessarily cause people to work more.

spend its revenues, as it is obvious in the real world. If the government spends

more revenues on taxed goods, it will increase the demand for good. This action

will offset the decrease in tax revenue caused by tax increase. Therefore, revenue-

ximizing tax rate will rise. In Figure 3 one can see that because of demand

maximizing tax rate moves from Point A to Point E. Finally

) concludes that if government cuts taxes and at the same time rises

on and decreases public investments, it increases the

likelihood that optimal tax revenues are lost. Tax policy must be related to both

Furthermore, Henderson (1981) points out interesting idea that real-life Laffer

curve is more complex. It looks like in Figure 4, because, as Henderson argues,

13 | P a g e

Figure 4. Complex shape of the

If the government cuts tax rate, tax revenues move from point A to point B.

People get higher income because of tax cut, but they might work less and spend

more time for leisure. Therefore, tax revenues decrease.

Another aspect, discussed by

which is also a tax. If tax rate cut does not cause immediate rise of tax revenue

and government does not decrease spending, the increase in budget deficit will

appear. Therefore, in countries, which have

would increase. Also increase in tax revenues might appear simpl

population growth.

Feige, Edgar L., and Robert T. McGee (1982) developed a simple model for

Laffer curve. The model shows that the shape and

Sweden depend on the power supply, the progressivity of the tax system and the

size of the observed economy.

Jonas Agell and Mats Persson (2000) analyze the government budget balance

in a simple endogenous growth model, by

transfer-adjusted tax rates in OECD countries to determine if countries apply

theoretically optimal tax rates. Jesús Alfonso Novales and Ruiz (2002) analyze

Complex shape of the Laffer Curve.

If the government cuts tax rate, tax revenues move from point A to point B.

People get higher income because of tax cut, but they might work less and spend

more time for leisure. Therefore, tax revenues decrease.

Another aspect, discussed by Henderson, is that tax cut can increase inflation,

which is also a tax. If tax rate cut does not cause immediate rise of tax revenue

and government does not decrease spending, the increase in budget deficit will

appear. Therefore, in countries, which have the power of currency issue, inflation

would increase. Also increase in tax revenues might appear simpl

Feige, Edgar L., and Robert T. McGee (1982) developed a simple model for

Laffer curve. The model shows that the shape and position of the Laffer curve for

Sweden depend on the power supply, the progressivity of the tax system and the

size of the observed economy.

Jonas Agell and Mats Persson (2000) analyze the government budget balance

in a simple endogenous growth model, by conducting an empirical study of

adjusted tax rates in OECD countries to determine if countries apply

theoretically optimal tax rates. Jesús Alfonso Novales and Ruiz (2002) analyze

If the government cuts tax rate, tax revenues move from point A to point B.

People get higher income because of tax cut, but they might work less and spend

Henderson, is that tax cut can increase inflation,

which is also a tax. If tax rate cut does not cause immediate rise of tax revenue

and government does not decrease spending, the increase in budget deficit will

the power of currency issue, inflation

would increase. Also increase in tax revenues might appear simply because of

Feige, Edgar L., and Robert T. McGee (1982) developed a simple model for

position of the Laffer curve for

Sweden depend on the power supply, the progressivity of the tax system and the

Jonas Agell and Mats Persson (2000) analyze the government budget balance

conducting an empirical study of

adjusted tax rates in OECD countries to determine if countries apply

theoretically optimal tax rates. Jesús Alfonso Novales and Ruiz (2002) analyze

14 | P a g e

how to manage deficit by substituting debt with taxes. They find that tax cuts on

labor and capital income have a positive effect on growth rate of the economy.

Trabandt Mathias and Harald Uhlig (2006) used a neoclassical growth model,

calibrated with constant Frisch elasticity for the US, and EU-14 economy. The

results show that both US and EU-14 economies can increase tax rates on labor

and capital income and gain higher tax revenues. However the Laffer curve in

consumption taxes does not have a peak.

The discussion about implementation of the Laffer curve in practice spread

widely in the USA in 1970’s. At that time top federal tax rate was 70 per cent and

encouraged people from that tax bracket to withdraw from official economy.

Proponents of the Laffer curve suggested politicians to cut tax rate and collect

higher tax revenues. Finally in 1988 top tax rate dropped to 28 per cent leading to

the increase of tax revenue five times as much revenue as was collected when top

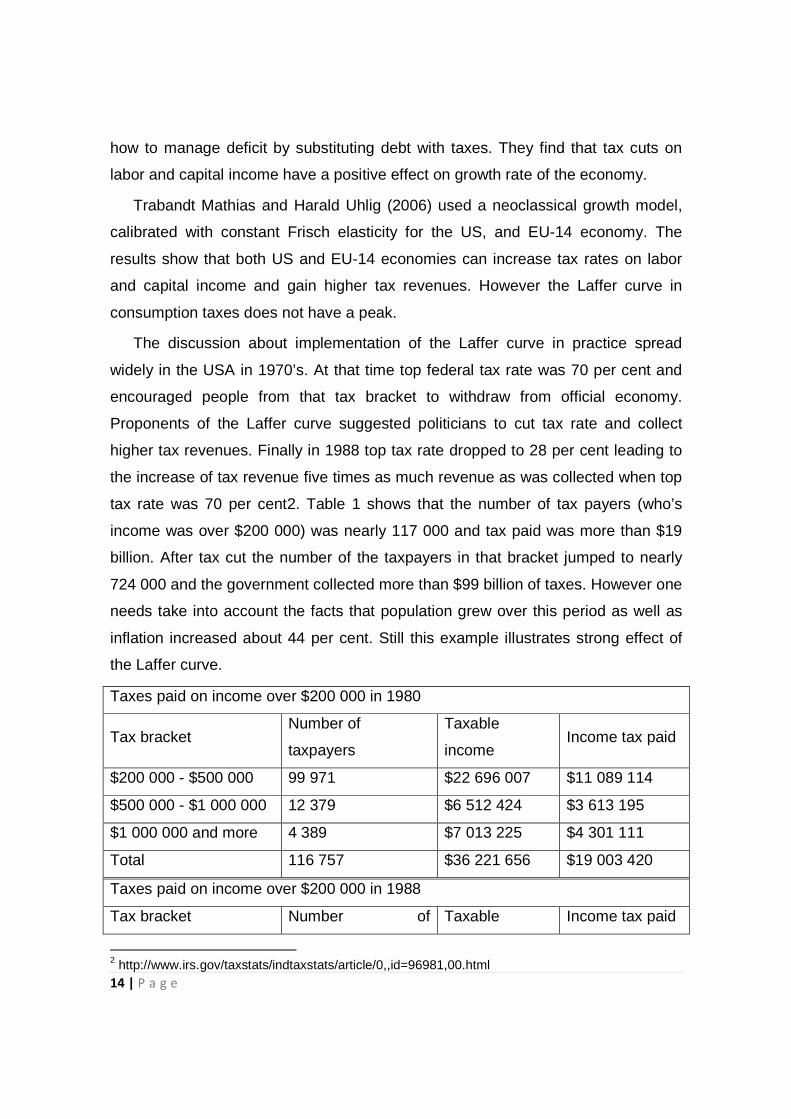

tax rate was 70 per cent2. Table 1 shows that the number of tax payers (who’s

income was over $200 000) was nearly 117 000 and tax paid was more than $19

billion. After tax cut the number of the taxpayers in that bracket jumped to nearly

724 000 and the government collected more than $99 billion of taxes. However one

needs take into account the facts that population grew over this period as well as

inflation increased about 44 per cent. Still this example illustrates strong effect of

the Laffer curve.

Taxes paid on income over $200 000 in 1980

Tax bracket Number of

taxpayers

Taxable

income Income tax paid

$200 000 - $500 000 99 971 $22 696 007 $11 089 114

$500 000 - $1 000 000 12 379 $6 512 424 $3 613 195

$1 000 000 and more 4 389 $7 013 225 $4 301 111

Total 116 757 $36 221 656 $19 003 420

Taxes paid on income over $200 000 in 1988

Tax bracket Number of Taxable Income tax paid

2 http://www.irs.gov/taxstats/indtaxstats/article/0,,id=96981,00.html

15 | P a g e

$200 000 - $500 000

$500 000 - $1 000 000

$1 000 000 and more

Total

Table 1. Labor tax statistics in the USA

Another example is Ireland. In 1985 with corporate tax rate of 50 per cent

Ireland collected tax revenues equal to 1.1 per cent of GDP

steadily decreased corporate tax rate until it was 12.5 per cent in 2000. As shown

in Figure 5, corporate tax revenues increased about three times and reached 3.6

percent of GDP. It must be noted that GDP figures are corrected for inflatio

Laffer curve effect is obvious in this case.

Figure 5. Corporate Tax Rate and Corporate Tax Revenue dynamics in Ireland.

2.5. Personal Income Tax

Personal Income Tax is a direct tax levied on income of a person. A person

means an individual, an

Generally, a person pay tax calendar year basis.

3 http://www.oecd.org.dataoecd/48/27/41498733.pdf

taxpayers income

547 239 $134 655 949

114 562 $67 552 225

61 896 $150 744 777

723 697 $352 952 951

Labor tax statistics in the USA

Another example is Ireland. In 1985 with corporate tax rate of 50 per cent

Ireland collected tax revenues equal to 1.1 per cent of GDP3. The government

steadily decreased corporate tax rate until it was 12.5 per cent in 2000. As shown

, corporate tax revenues increased about three times and reached 3.6

percent of GDP. It must be noted that GDP figures are corrected for inflatio

Laffer curve effect is obvious in this case.

Corporate Tax Rate and Corporate Tax Revenue dynamics in Ireland.

Personal Income Tax

Personal Income Tax is a direct tax levied on income of a person. A person

means an individual, an ordinary partnership, a non-juristic body of person.

Generally, a person pay tax calendar year basis.

http://www.oecd.org.dataoecd/48/27/41498733.pdf

$38 446 620

$19 040 602

$42 254 821

$99 742 043

Another example is Ireland. In 1985 with corporate tax rate of 50 per cent

. The government

steadily decreased corporate tax rate until it was 12.5 per cent in 2000. As shown

, corporate tax revenues increased about three times and reached 3.6

percent of GDP. It must be noted that GDP figures are corrected for inflation. So

Corporate Tax Rate and Corporate Tax Revenue dynamics in Ireland.

Personal Income Tax is a direct tax levied on income of a person. A person

juristic body of person.

16 | P a g e

Taxpayers are classified into residents and non-residents. The definition of a

concept “resident” differs from country to country. Basically, “resident” means any

person residing in certain country for a certain period of time. A resident of certain

country is liable to pay tax on income from sources both in the country he/she

resides and in foreign countries. A non-resident is a person who does not reside in

certain country but still earns income in that country.

Income can be in cash and in kind. Both of these income types are chargeable

to the personal income tax. The income which is subject to income taxation is

called assessable income. Certain deductions and allowances are allowed in the

calculation of the taxable income. Taxpayer shall make deductions from

assessable income before the allowances are granted. Therefore, taxable income

is calculated by the following formula:

Taxable income = Assessable Income - deductions - allowances

Taxes can have a significant effect on income distribution in an economy. As

Adam Smith (1904) noted tax should be linked to ability to pay. Therefore, tax

systems can be distinguished as follows:

• Progressive tax system – a system in which tax represents a greater proportion

of a person's income as their income rises. In other words, the average rate of

taxation rises.

• Regressive tax system – a system in which tax represents a smaller proportion

of a person's income as their income rises. In other words, the average rate of

taxation falls.

• Proportional tax system – a system in which tax is paid as the percentage if the

income. The percentage remains the same despite the level of income. In this

system the average rate of taxation is constant.

There is always an open discussion about the difficulties in administering the

tax and maintaining a sense of fairness of who is paying and how much. Proposals

to modify the income tax system to make it “flat” (fewer tax rates and fewer

deductions) arise more often (Kiefer, 2010). Still, income tax is an important source

of budgetary income. However, each country has its own specifics on personal

17 | P a g e

income tax. The review of personal income tax along with labor taxes are depicted

in Section 3.4.

2.6. Value Added Tax

Value added tax (VAT) is one of the most widespread indirect taxes in the world

with increasingly more countries adopting it for taxation of consumption. According

to the Organization of Economic Cooperation and Development (OECD), over 150

countries have implemented a VAT/GST and there is a need for a global platform

where the economic, social and cross border issues of operating a VAT/GST can

be discussed. A VAT is levied on the difference between a business’s sales and

its purchases of goods and services. Typically, a business calculates the tax due

on its sales, subtracts a credit for taxes paid on its purchases, and remits the

difference to the government (United States Accountability Office Report to

Congressional Requests, Value Added Taxes, 2008.)

The Lithuanian Ministry of Finance proposes the following definition of the VAT

subject: ‘the subject of VAT is the supply of goods and services by a taxable

person in the performance of his/its economic activities within the territory of the

country that are affected for consideration’. The value added tax system is

designed to address various problems associated with the conventional sales tax

system such as cascading- the term describing a situation when the end consumer

of a product is obliged to pay taxes on an input that has already been taxed earlier

in the production chain. The clarity and transparency of the VAT system enables

effective elimination of the cascade problem and the associated tax evasion

problem. In regard of International trade, VAT is seen by some countries as

discriminatory. The American Manufacturing Trade Action Coalition (AMTAC)

express concerns that the rebate of taxes upon export normally is prohibited under

the World Trade Organization trading regime, but within the Value Added Tax

system, taxes are rebated on exports and assessed on imports, triggering

International imbalances and providing certain countries with a competitive

advantage. According to the OECD, research suggests that the current

18 | P a g e

international environment for consumption taxes, especially with respect to trade in

services and intangibles, is hindering business activity and economic growth and

distorts competition. The US Government Accountability Office also discusses

initiatives of introducing a VAT equivalent in the US. The creation of a global

framework for applying VAT/GST on international trade is therefore a key priority

for the OECD.

Our Master thesis will be primarily focused on members of the European Union

therefore the European VAT systems will be addressed in more depth. VAT was

invented in 1954 by a French economist and introduced by Maurice Laure, the joint

director of the French tax authority. It was introduced for large businesses but later

expanded to remaining sectors of the economy. On 11 April 1967 the first two VAT

Directives were adopted, establishing a general, multi-stage but non-cumulative

turnover tax to replace all other turnover taxes in the Member States. The first two

VAT Directives laid down only the general structures of the system with Member

States being free to determine the VAT coverage. In May 1977 the Sixth VAT

Directive was adopted and established a uniform VAT coverage. On 1 January

2007, the Sixth Directive was replaced by the VAT Directive which guarantees that

the VAT contributed by each of the Member States to the Community's own

resources can be calculated. It still however, allows Member States many possible

exceptions and derogations from the standard VAT coverage. Moreover, it does

not set out the rates of VAT to be applied in Member States, only a minimum rate

of 15%. For transactions between taxable persons it is still a destination based

VAT system, but it is a Transitional VAT System, and the intention is eventually to

have a common system of VAT where VAT is charged by the seller of goods - an

origin based VAT system with VAT being charged at the rate in force where the

supplier is established4.

The European e-Justice portal under the European Commission provides the

following explanation of a VAT system: ‘The common system of VAT applies to the

production and distribution of goods and services bought and sold for consumption

4 European Commission on the history of value added taxes in Europe

19 | P a g e

within the European Union and the actual tax burden is visible at each stage in the

production and distribution chain. To ensure that the tax is neutral in impact,

irrespective of the number of transactions, taxable persons for VAT may deduct

from their VAT account the amount of tax which they have paid to other taxable

persons. VAT is finally borne by the final consumer in the form of a percentage

addition to the final price of the goods or services’. Double taxation is avoided and

tax is paid only on the value added at each stage of production and distribution. In

this way, as the final price of the product is equal to the sum of the values added at

each preceding stage, the final VAT paid is made up of the sum of the VAT paid at

each stage. The tax is paid to the revenue authorities by the seller of the goods,

who is the taxable person, but it is actually paid by the buyer to the seller as part of

the price thus making it an indirect tax.

For VAT purposes, a taxable person is any individual, partnership, company or

any other subject which supplies taxable goods and services in the course of

business. However, if the annual turnover of this person is less than a certain limit

(the threshold), which differs according to the Member State, the person does not

have to register as a payer and charge VAT on their sales. EU Member States

have freedom of choice setting the values of thresholds for VAT registration and for

the minimum standard and reduced rates as long as they comply with the minimum

requirements. Supplies of goods and services subject to VAT are normally subject

to a standard rate of at least 15% but Member States may apply one or two

reduced rates of not less than 5% to goods and services enumerated in a restricted

list. However, these rules are complicated by a multitude of derogations granted to

certain Member States which were granted during the negotiations preceding the

adoption of the VAT rates Directive of 1992 and in the Acts of Accession to the

European Union. Such derogations prevent a coherent system of VAT rates in the

EU from being applied.

In order to eliminate any competitive disadvantages stemming from tax rate

differences between Member states and for the purpose of exports between the

Community and non-member countries, no VAT is charged on the transaction and

the VAT already paid on the inputs of the good for export is deducted - this is an

20 | P a g e

exemption with the right to deduct the input VAT. There is thus no residual VAT

contained in the export price. However, as far as imports are concerned, VAT must

be paid at the moment the goods are imported so they are immediately placed on

the same footing as equivalent goods produced in the Community. Taxable people

registered for VAT will be allowed to deduct this VAT in their next VAT return5 The

significance of value added tax proceeds in European Union member states both in

its nominal form and as a proportion of total tax revenue with associated

implications will be discussed in a later chapter of the thesis.

5 The European e-Justice Portal under the European Commission,

http://ec.europa.eu/taxation_customs/index_en.htm

21 | P a g e

3. TAX ANALYSIS

Differing taxation policies and trends, as well as the political and business

environment, are basic factors affecting the level of competitiveness of countries.

As was already mentioned, consistency in countries‘ economic and taxation policy

is of vital importance to the subjects pursuing business objectives both in their

home markets and abroad. Specific data on the dynamics of national budgetary

revenue, the composition of the revenue depending on specific taxes, levels of

expenditure and borrowing should be addressed in order to substantiate the

problem of possible tax changes Europe-wide.

We will present a basic overview of the present-day European Union member

states Gross Domestic Product (GDP) dynamics, revenue and expenditure levels

of the general government and analyze the composition of revenue and its trends.

General government data will be used as an aggregate proxy allowing us to

perform country level comparison and bypass the variations in the extent of

centralization, municipal taxation and compulsory social welfare charges.

3.1. GDP dynamics

Gross domestic product is a measure of the economic activity, defined as the

value of all goods and services produced less the value of any goods or services

used in their creation. It is important to review the extent of and dynamics of

economic activity in all the EU member states and grasp the underlying differences

between them. Due to limited availability of valid statistical data for the full sample,

only the period of 1996-2011 will be reviewed in this section.

Table 2 demonstrates the significant disparity of nominal GDP growth in the EU

member states from year 1996 to 2011 with 1996 as the base year. As visible in

the table, the greatest growth was displayed by member states that were admitted

during the final two enlargement stages with exceptionally high figures

demonstrated by the former states of the Soviet Union and its satellites of the

Warsaw Pact. The economies of these highly dynamic countries are extremely

22 | P a g e

sensitive to economic and fiscal policy changes and represent a potential obstacle

in the homogenization of the tax environment. The column depicting nominal GDP

change in national currency for the Euro Zone countries is calculated as Euro-fixed

series by applying the Euro fixed rate on the national currencies data with

discrepancies of the GDP change data compared to nominal GDP change in Euros

stemming from the pre-Euro exchange rate fluctuations. The column is intended to

display the heterogeneity of the economies of the member states with Romania

and Bulgaria having recently experienced a period of significant inflation, and

Czech Republic, Slovakia and Lithuania appreciating the value of their currencies

during the period of 1996-2011. Furthermore, while Czech Republic and Slovakia

(Slovakia joined the Euro Zone in January 1st 1999) have evolved from a pegged

currency rate to a managed and eventually floating exchange rate with its positive

effects on the economy and trade, Lithuania achieved the depreciation by merely

swapping the base currency used for the peg from US Dollar to the Euro. This

means that even in this respect the three countries are not readily comparable.

Country

Nominal GDP

Change, EUR

Nominal GDP

Change, National currency Country

Nominal GDP

Change, EUR

Nominal GDP

Change, National currency

Belgium 69,81% 74,00% Luxembourg 157,65% 171,08%

Bulgaria 386,28% 4173,53% Hungary 178,51% 301,56% Czech Republic 203,02% 116,24% Malta 121,08% 107,37% Denmark 65,23% 67,04% Netherlands 82,84% 88,30% Germany 33,86% 37,11% Austria 62,92% 66,87% Estonia 328,82% 339,11% Poland 199,36% 260,92% Ireland 165,47% 163,50% Portugal 79,24% 83,46% Greece 96,01% 118,59% Romania 370,21% 4982,06% Spain 118,85% 126,52% Slovenia 113,84% 198,32% France 60,40% 62,05% Slovakia 314,47% 220,79% Italy 58,42% 56,59% Finland 89,43% 93,25% Cyprus 143,22% 140,49% Sweden 77,77% 88,52%

Latvia 348,25% 352,54% United Kingdom 81,08% 92,85%

Lithuania 362,62% 214,54% Table 2. Nominal GDP growth in 1996-2011

23 | P a g e

Figures 6 and 7 have intentionally been projected on a uniform vertical axis

range to depict the real GDP growth rate for year 1996 to 2011 for two groups of

countries based on the years of accession to the European Union. The duration of

membership is likely to reflect the qualitative effect resulting from prolonged

exposure to the unified market conditions, broader experience in the competitive

market setting and the inveteracy of democratic rule and correspondent values.

The first group consists of the EU – 15 countries that have been member states

during the whole sample period and the second group is comprised of countries

admitted during the latest stages of EU enlargement most of which have

experienced a transition to the competitive market setting during the sample

period. The calculation of the annual growth rate of GDP volume is intended to

allow comparisons of the dynamics of economic development both over time and

between economies of different sizes. For measuring the growth rate of GDP in

terms of volumes, the GDP at current prices are valued in the prices of the

previous year and the thus computed volume changes are imposed on the level of

a reference year. This type of measurement eliminates the effects of price changes

during the period and allows for adequate comparison. Among the EU – 15

member states Ireland and Luxembourg initially demonstrated a higher growth rate

in and Greece experienced significant contraction in the end of the period. The 12

EU member states that have joined the Union during the last stages of

enlargement are depicted individually with the bold line representing the average

arithmetical real GDP growth rate for the 15 EU countries. The three newly

independent Baltic states of Lithuania, Latvia and Estonia have experienced the

greatest fluctuations in the growth rate with Malta and Cyprus showing generally

milder deviations and Poland demonstrating a sustainably higher growth rate with

increased resilience to significant changes.

24 | P a g e

Figure 6. Real GDP growth rate in 1996-2011 for EU – 15 states

Figure 7. Real GDP growth rate in 1996-2011 for new Member States

2009 was the peak year of the recent economic crisis and all member states

saw a contraction of their GDP, however the timing of the crisis varied across

countries: a third of the Union suffered a contraction as early as 2008 whilst the

average real GDP growth for the EU – 27 member states was 1.33 %. It is

-20

-15

-10

-5

0

5

10

15R

ea

l G

DP

gro

wth

ra

te

-20

-15

-10

-5

0

5

10

15

Re

al

GD

P g

row

th r

ate

25 | P a g e

essential to stress at this point that average target group (EU – 15, EU – 27, new

member states) statistics will represent the arithmetical mean without adjustments

for the weight of individual countries to the consolidated values unless specifically

stated otherwise. This type of analysis is performed because the subsequent

model will be based on country ratios not regarding individual weights.

Even though the new member countries have demonstrated prolonged above-

average growth, the graph supports the notion of most of these countries being

significantly more sensitive to changes in the economic and fiscal environment with

a significantly wider range of fluctuations. Fraser Cameron in a 2010 working paper

suggests that the EU has adopted a more flexible approach to integration which

resulted in a multi-speed Europe with several tiers of integration. A differing

member-country base for the Euro zone, the European Union and the Schengen

passport free-zone is an example of the arrangement. Table 3 depicts the standard

deviations of real GDP growth for the target groups and indicates that the EU – 27

and especially the newest member states demonstrate higher variations of

macroeconomic data. It suggests that immediate unification of the EU – 27

member states would evoke additional obstacles due to the low level of

homogeneity for the two groups and supports the idea of allowing for a multi-speed

Europe. According to Christian B. Jensen and Jonathan B. Slapin (2010), there are

no less than two primary legal mechanisms for pursuing a multispeed approach

within the treaty framework; however the question of decision making by only a

portion of member states remains.

Year 1996 1997 1998 1999 2000 2001 2002 2003

EU - 15 2,50 2,32 1,75 2,22 1,81 1,24 1,65 1,88

EU - 27 3,42 3,87 2,20 2,51 2,42 2,03 2,12 2,78

New member states 4,52 5,45 2,80 2,50 3,12 2,46 1,94 2,77

Year 2004 2005 2006 2007 2008 2009 2010 2011

EU - 15 1,12 1,42 1,19 1,37 1,24 1,64 2,14 2,56

EU - 27 2,19 2,47 2,44 2,61 2,85 4,12 1,90 2,64

New member states 2,46 2,26 2,47 2,80 3,46 5,72 1,65 2,34 Table 3. Standard deviation of real GDP growth in 1996-2011

26 | P a g e

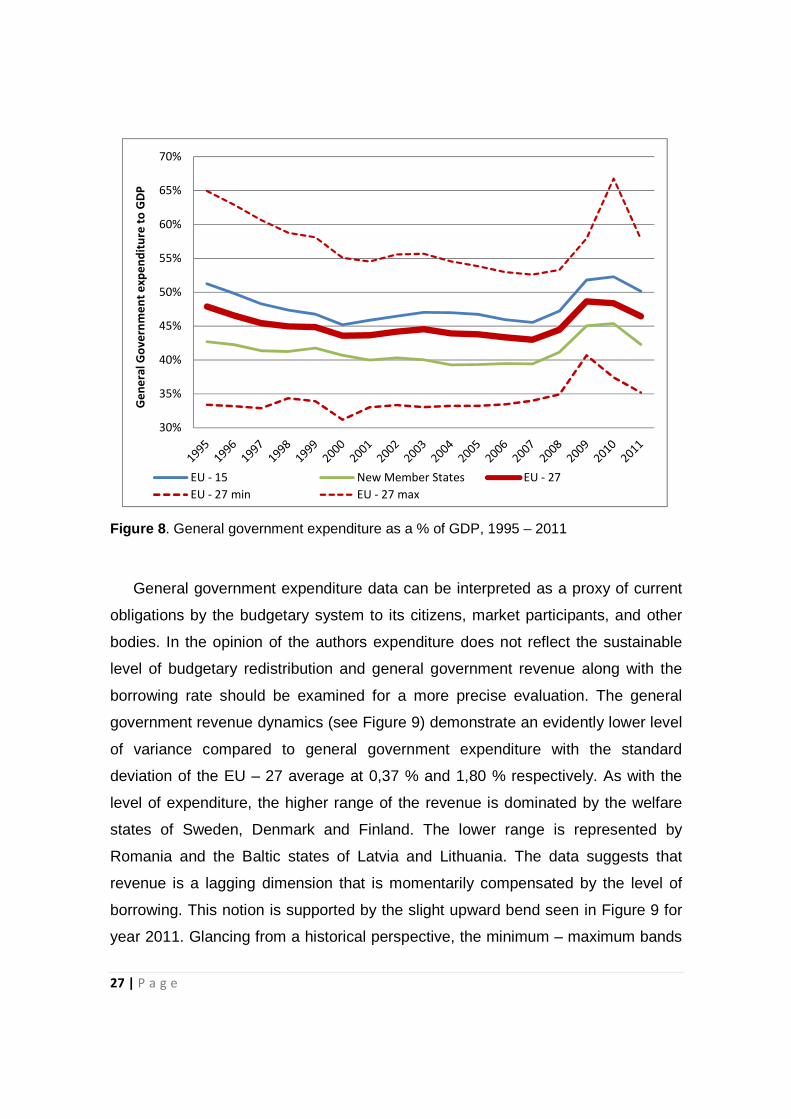

3.2. Budgetary dynamics

As mentioned, general government data will be used as an aggregate proxy

allowing us to perform country level comparison and bypass the variations in the

extent of centralization, municipal taxation and compulsory social welfare charges.

The European System of Accounts (ESA 95), section 2.69 defines the general

government sector as ‘all institutional units which are other non-market producers

whose output is intended for individual and collective consumption, and mainly

financed by compulsory payments made by units belonging to other sectors, and/or

all institutional units principally engaged in the redistribution of national income and

wealth‘ and is made up of the following four sub-categories: central government,

state government, local government and social security funds.

As seen in Figure 8, the dynamics of general government expenditure as a

percentage of GDP for both target groups follow a nearly identical trend with the

coefficient of correlation reaching a significant value of 0,897. The EU – 15

member states tend to have a higher level of GDP redistribution through the

budgetary system with the Scandinavian countries consistently holding the highest

levels during the sample period thus demonstrating the most typical characteristic

of welfare states. The lower range is dominated by the newest member states with

Romania, the three Baltic states and Ireland displaying the lowest redistribution

rates during the sample period; During the financial downturn Ireland moved from

the lower boundary to the highest value with an increase from 36,61 percent in

year 2007 to 66,79 percent in year 2010. The minimum and maximum bands of the

full EU – 27 sample period clearly visualizes the extreme differences of aggregate

expenditure incurred by the sectors of general government.

27 | P a g e

Figure 8. General government expenditure as a % of GDP, 1995 – 2011

General government expenditure data can be interpreted as a proxy of current

obligations by the budgetary system to its citizens, market participants, and other

bodies. In the opinion of the authors expenditure does not reflect the sustainable

level of budgetary redistribution and general government revenue along with the

borrowing rate should be examined for a more precise evaluation. The general

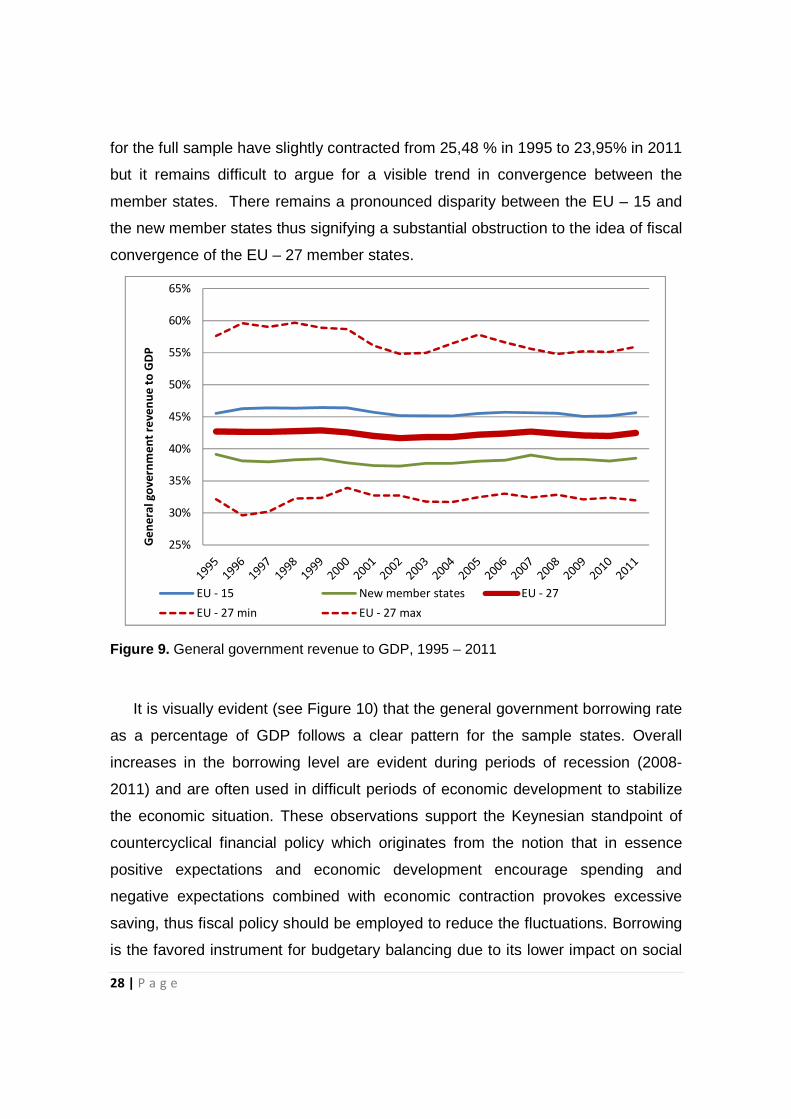

government revenue dynamics (see Figure 9) demonstrate an evidently lower level

of variance compared to general government expenditure with the standard

deviation of the EU – 27 average at 0,37 % and 1,80 % respectively. As with the

level of expenditure, the higher range of the revenue is dominated by the welfare

states of Sweden, Denmark and Finland. The lower range is represented by

Romania and the Baltic states of Latvia and Lithuania. The data suggests that

revenue is a lagging dimension that is momentarily compensated by the level of

borrowing. This notion is supported by the slight upward bend seen in Figure 9 for

year 2011. Glancing from a historical perspective, the minimum – maximum bands

30%

35%

40%

45%

50%

55%

60%

65%

70%

Ge

ne

ral

Go

ve

rnm

en

t e

xp

en

dit

ure

to

GD

P

EU - 15 New Member States EU - 27

EU - 27 min EU - 27 max

28 | P a g e

for the full sample have slightly contracted from 25,48 % in 1995 to 23,95% in 2011

but it remains difficult to argue for a visible trend in convergence between the

member states. There remains a pronounced disparity between the EU – 15 and

the new member states thus signifying a substantial obstruction to the idea of fiscal

convergence of the EU – 27 member states.

Figure 9. General government revenue to GDP, 1995 – 2011

It is visually evident (see Figure 10) that the general government borrowing rate

as a percentage of GDP follows a clear pattern for the sample states. Overall

increases in the borrowing level are evident during periods of recession (2008-

2011) and are often used in difficult periods of economic development to stabilize

the economic situation. These observations support the Keynesian standpoint of

countercyclical financial policy which originates from the notion that in essence

positive expectations and economic development encourage spending and

negative expectations combined with economic contraction provokes excessive

saving, thus fiscal policy should be employed to reduce the fluctuations. Borrowing

is the favored instrument for budgetary balancing due to its lower impact on social

25%

30%

35%

40%

45%

50%

55%

60%

65%

Ge

ne

ral

go

ve

rnm

en

t re

ve

nu

e t

o G

DP

EU - 15 New member states EU - 27

EU - 27 min EU - 27 max

29 | P a g e

disorder and its immediate effect since the alternative rout of cutting budgetary

expenses and increasing the tax burden evokes immediate protests and resistance

and is not able to deliver the necessary results in a desirable time frame. However,

extensive borrowing causes certain hazards with a recent example demonstrated

by Greece and increasing distrust mounting on the EU – 15 states of Portugal,

Spain and Italy. European level discussions on fiscal austerity requirements hint on

limiting the use of borrowing for budgetary balancing.

Figure 10. General government borrowing to GDP, 1995 - 2011

Even though Maastricht criteria on the general deficit level were set out

demanded member states to limit their total government deficit to 3% of GDP as

well as limit total gross general government debt to 60% of GDP, changes were

introduced on 2nd May 2012. The new rule that is introduced in the present EU

Fiscal Compact Treaty6 allows limited temporary deviations and stipulates:

• ‘the budgetary position of the general government of a Contracting Party shall

be balanced or in surplus; 6 see Treaty on Stability, Coordination and Governance in the Economic and Monetary Union,

European Council

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Ge

ne

ral

go

ve

rnm

en

t b

orr

ow

ing

to

GD

P

EU - 15 New member states EU - 27

EU - 27 min EU - 27 max

30 | P a g e

• the rule under point (a) shall be deemed to be respected if the annual structural

balance of the general government is at its country-specific medium-term

objective, as defined in the revised Stability and Growth Pact, with a lower limit

of a structural deficit of 0,5 % of the gross domestic product at market prices.

The Contracting Parties shall ensure rapid convergence towards their

respective medium-term objective. The time-frame for such convergence will

be proposed by the European Commission taking into consideration country-

specific sustainability risks. Progress towards, and respect of, the medium-term

objective shall be evaluated on the basis of an overall assessment with the

structural balance as a reference, including an analysis of expenditure net of

discretionary revenue measures, in line with the revised Stability and Growth

Pact;

• the Contracting Parties may temporarily deviate from their respective medium-

term objective or the adjustment path towards it only in exceptional

circumstances, as defined in point (b) of paragraph 3;

• where the ratio of the general government debt to gross domestic product at

market prices is significantly below 60 % and where risks in terms of long-term

sustainability of public finances are low, the lower limit of the medium-term

objective specified under point (b) can reach a structural deficit of at most 1,0

% of the gross domestic product at market prices;

• in the event of significant observed deviations from the medium-term objective

or the adjustment path towards it, a correction mechanism shall be triggered

automatically. The mechanism shall include the obligation of the Contracting

Party concerned to implement measures to correct the deviations over a

defined period of time.’

The full content of the article 3, point 1 of the aforementioned treaty was quoted

in order not to distort or restrict the purport intended by the treaty. Provisions of the

Treaty are to be employed by Contracting Parties at the latest one year after the

entry into force. On 2nd May, 2012 the treaty was signed by – thus the Contracting

Parties constitute – all members of the European Union except two: United

31 | P a g e

Kingdom and Czech Republic. The key provision of the Treaty, as noted in the

quote, is the imposed limits on the use of borrowing in the budgetary balancing

process thus putting an emphasis on fiscal austerity consisting of expenditure

cutting and revenue boosting measures.

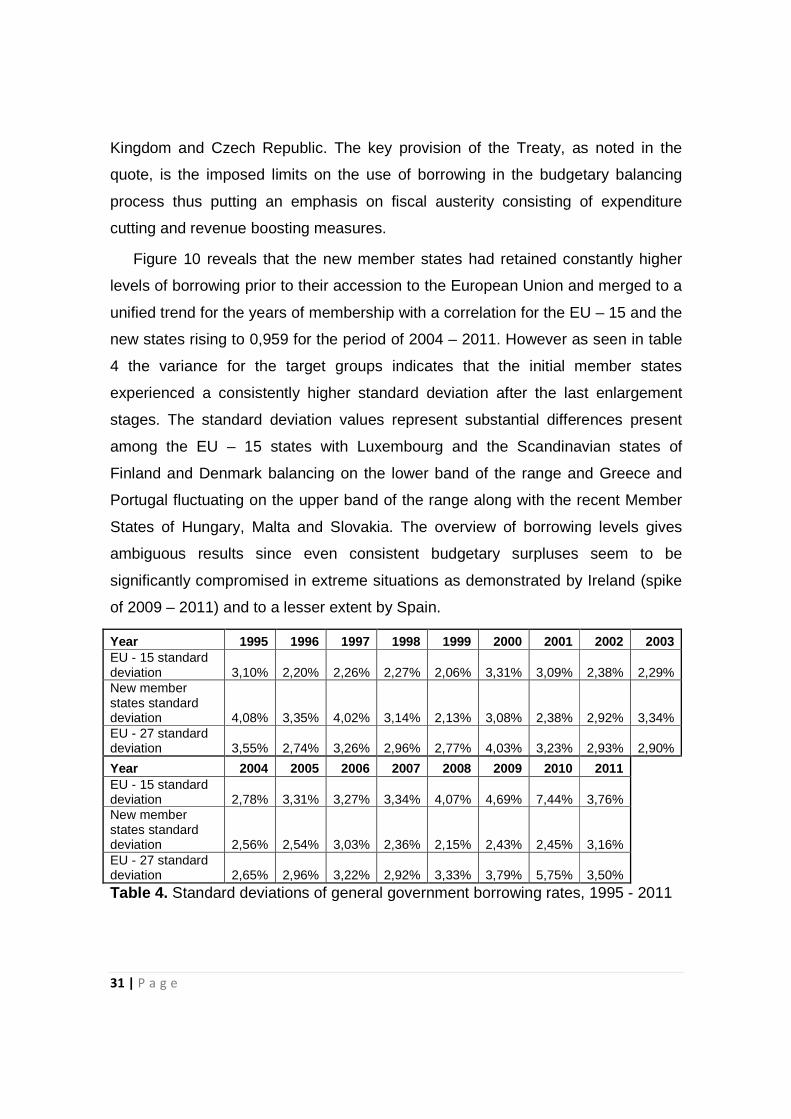

Figure 10 reveals that the new member states had retained constantly higher

levels of borrowing prior to their accession to the European Union and merged to a

unified trend for the years of membership with a correlation for the EU – 15 and the

new states rising to 0,959 for the period of 2004 – 2011. However as seen in table

4 the variance for the target groups indicates that the initial member states

experienced a consistently higher standard deviation after the last enlargement

stages. The standard deviation values represent substantial differences present

among the EU – 15 states with Luxembourg and the Scandinavian states of

Finland and Denmark balancing on the lower band of the range and Greece and

Portugal fluctuating on the upper band of the range along with the recent Member

States of Hungary, Malta and Slovakia. The overview of borrowing levels gives

ambiguous results since even consistent budgetary surpluses seem to be

significantly compromised in extreme situations as demonstrated by Ireland (spike

of 2009 – 2011) and to a lesser extent by Spain.

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 EU - 15 standard deviation 3,10% 2,20% 2,26% 2,27% 2,06% 3,31% 3,09% 2,38% 2,29% New member states standard deviation 4,08% 3,35% 4,02% 3,14% 2,13% 3,08% 2,38% 2,92% 3,34% EU - 27 standard deviation 3,55% 2,74% 3,26% 2,96% 2,77% 4,03% 3,23% 2,93% 2,90%

Year 2004 2005 2006 2007 2008 2009 2010 2011 EU - 15 standard deviation 2,78% 3,31% 3,27% 3,34% 4,07% 4,69% 7,44% 3,76% New member states standard deviation 2,56% 2,54% 3,03% 2,36% 2,15% 2,43% 2,45% 3,16% EU - 27 standard deviation 2,65% 2,96% 3,22% 2,92% 3,33% 3,79% 5,75% 3,50% Table 4. Standard deviations of general government borrowing rates, 1995 - 2011

32 | P a g e

A visualization of the debt to GDP ratios for the target groups is presented in

Figure 11. These ratios generally represent the cumulative total of the borrowing

levels throughout a certain period that have to be adjusted for the changes in GDP.

EU – 15 states tend to have a significantly higher debt to GDP ratio with a

correspondingly higher absolute standard deviation however despite the initial

differences a contraction of the range ensued with a common trend developing

afterwards. The EU – 15 and new member states have demonstrated a rather

uniform development of the debt to GDP ratio for 2004 – 2011 correlating at 0,91.

For individual countries Greece, Italy and Belgium dominate the upper range and

Luxembourg and Estonia consistently lead the lower range. An example of the

Baltic states of Latvia, Lithuania and Estonia suggest that significant differences

can exist between countries that share a common history, hold independence for a

unified period of time and are located in a relatively close proximity thus impeding

their comparability. Extreme deviations of debt to GDP and especially the growing

range pose a serious obstacle to the convergence of fiscal policies.

Figure 11. Debt to GDP ratio, 1995 – 2011

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

1,80

De

bt

to G

DP

ra

tip

EU - 15 New member states EU - 27 EU - 27 min EU - 27 max

33 | P a g e

3.3. Revenue composition

The key component of budgetary revenue for all member states is the revenue

from taxes and social contributions averaging 85,84 % of the total revenue in 2010

with lower and upper bands respectively at 76,50 % and 93,27 %. Deviations in the

percentage stem from varying proportions of European Union structural funding,

privatization proceeds, public company profits and other sources. The general level

of revenue from taxes and social contributions remained relatively stable during the

period of 1995 – 2010 with an evident slight downtrend.

The three major groups of revenue are indirect taxes (included in the ESA 95

under codes TRD211, TRD214, TRD29), direct taxes (TRD51, TRD59, TRD91)

and actual social contributions (TRD611). As depicted in figure 12 the proportions

of these groups vary significantly across the member states for year 2010 with

average values of the target countries reaching 35,73 % for indirect taxes, 29,82 %

for direct taxes, 30,86% for social contributions and 3,59% for other taxes which

includes voluntary social contributions, imputed social contributions and amounts

assessed but unlikely to be collected. The coefficient of variance for the sample

countries in year 2010 is lowest (0,192) for indirect taxes which allow us to assume

that direct taxes and their regulations are relatively more uniform in the EU

countries. Additionally it is important to note an essential difference in the

composition of tax revenue for Denmark – direct taxes correspond 61,75 % of the

total tax revenue and actual social contributions gather only 2,15 % of the total

revenue. The huge discrepancy should be treated as a mere misclassification if the

principle of substance over form would be used since commonly the compulsory

social contribution charges are directly dependent on personal income taxation and

comprise the total labor tax burden.

34 | P a g e

Figure 12. Composition of taxes and social contributions revenue as a % of GDP, 2010

Figure 13 shows decomposition of direct taxes for EU-15 in 2010. As one can

see personal income takes biggest proportion of all direct taxation.

Figure 13. Composition of direct, 2010

0%

10%

20%

30%

40%

50%

60%R

ev

en

ue

to

GD

P

Other Social contributions Indirect taxes Direct taxes

6%

29%

65%

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1

EU-15

Personal income tax

Corporate tax

Other

35 | P a g e

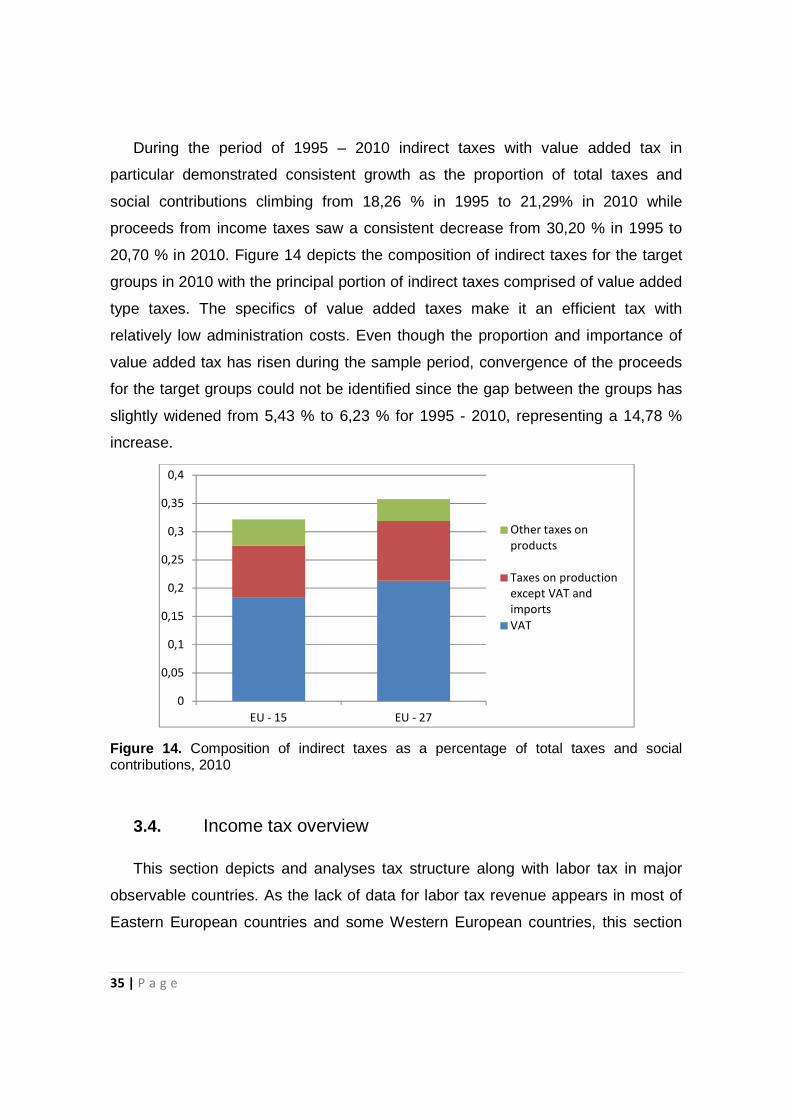

During the period of 1995 – 2010 indirect taxes with value added tax in

particular demonstrated consistent growth as the proportion of total taxes and

social contributions climbing from 18,26 % in 1995 to 21,29% in 2010 while

proceeds from income taxes saw a consistent decrease from 30,20 % in 1995 to

20,70 % in 2010. Figure 14 depicts the composition of indirect taxes for the target

groups in 2010 with the principal portion of indirect taxes comprised of value added

type taxes. The specifics of value added taxes make it an efficient tax with

relatively low administration costs. Even though the proportion and importance of

value added tax has risen during the sample period, convergence of the proceeds

for the target groups could not be identified since the gap between the groups has

slightly widened from 5,43 % to 6,23 % for 1995 - 2010, representing a 14,78 %

increase.

Figure 14. Composition of indirect taxes as a percentage of total taxes and social contributions, 2010

3.4. Income tax overview

This section depicts and analyses tax structure along with labor tax in major

observable countries. As the lack of data for labor tax revenue appears in most of

Eastern European countries and some Western European countries, this section

0

0,05

0,1

0,15

0,2

0,25

0,3

0,35

0,4

EU - 15 EU - 27

Other taxes on

products

Taxes on production

except VAT and

imports

VAT

36 | P a g e

provides tax analysis for the following 12 countries: Austria, Belgium, Denmark,

Finland, France, Germany, Italy, Netherland, Norway, Spain, Sweden, UK.

Generally, Sweden collects the highest labor tax revenue

GDP in comparison to other EU countries. UK, on the other hand, has the lowest

labor tax revenue ratio to GDP (Figure

Figure 15. Labor tax revenue as a percentage of GDP 1996

UK has the lowest implicit labor tax rate amongst EU countries. This is

illustrated in Figure 16. EU

cent in the period 1996-2010.

provides tax analysis for the following 12 countries: Austria, Belgium, Denmark,

Finland, France, Germany, Italy, Netherland, Norway, Spain, Sweden, UK.

Generally, Sweden collects the highest labor tax revenues as a proportion of

GDP in comparison to other EU countries. UK, on the other hand, has the lowest

labor tax revenue ratio to GDP (Figure 15).

Labor tax revenue as a percentage of GDP 1996-2010.

UK has the lowest implicit labor tax rate amongst EU countries. This is

. EU-27 implicit labor tax rate ranges from 35 .5 to 36.5 per

2010.

provides tax analysis for the following 12 countries: Austria, Belgium, Denmark,

Finland, France, Germany, Italy, Netherland, Norway, Spain, Sweden, UK.

s as a proportion of

GDP in comparison to other EU countries. UK, on the other hand, has the lowest

UK has the lowest implicit labor tax rate amongst EU countries. This is

27 implicit labor tax rate ranges from 35 .5 to 36.5 per

37 | P a g e

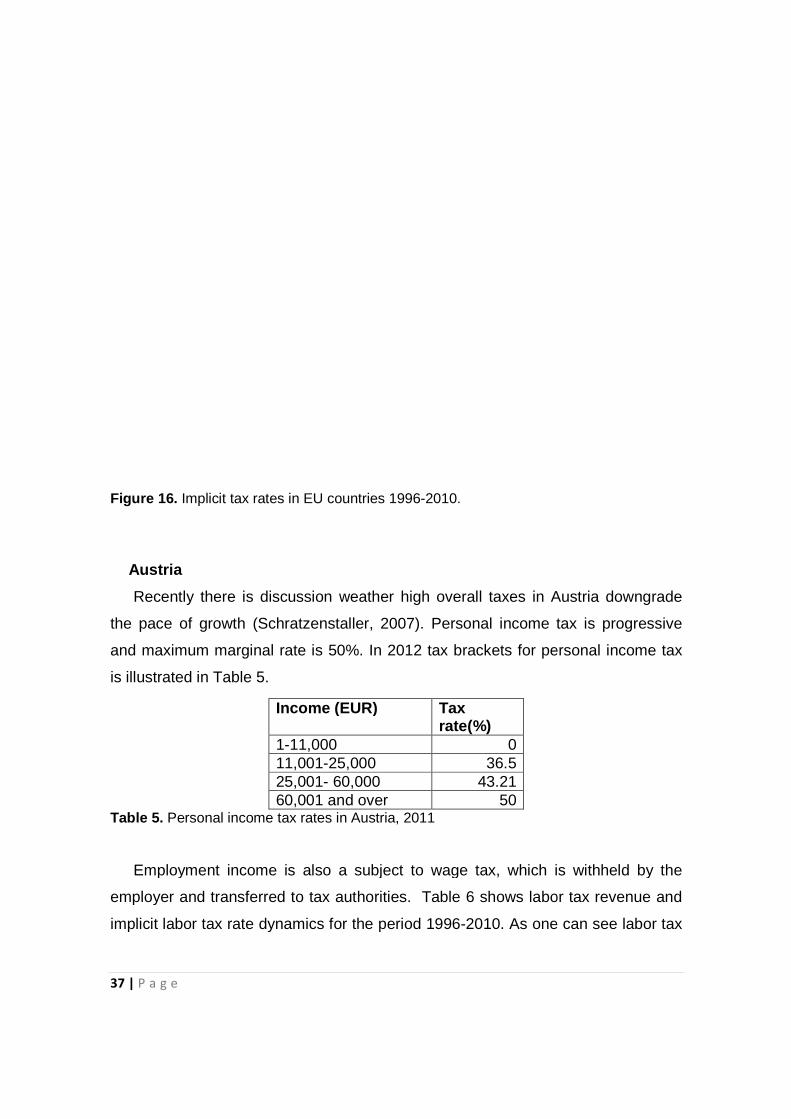

Figure 16. Implicit tax rates in EU countries 1996

Austria

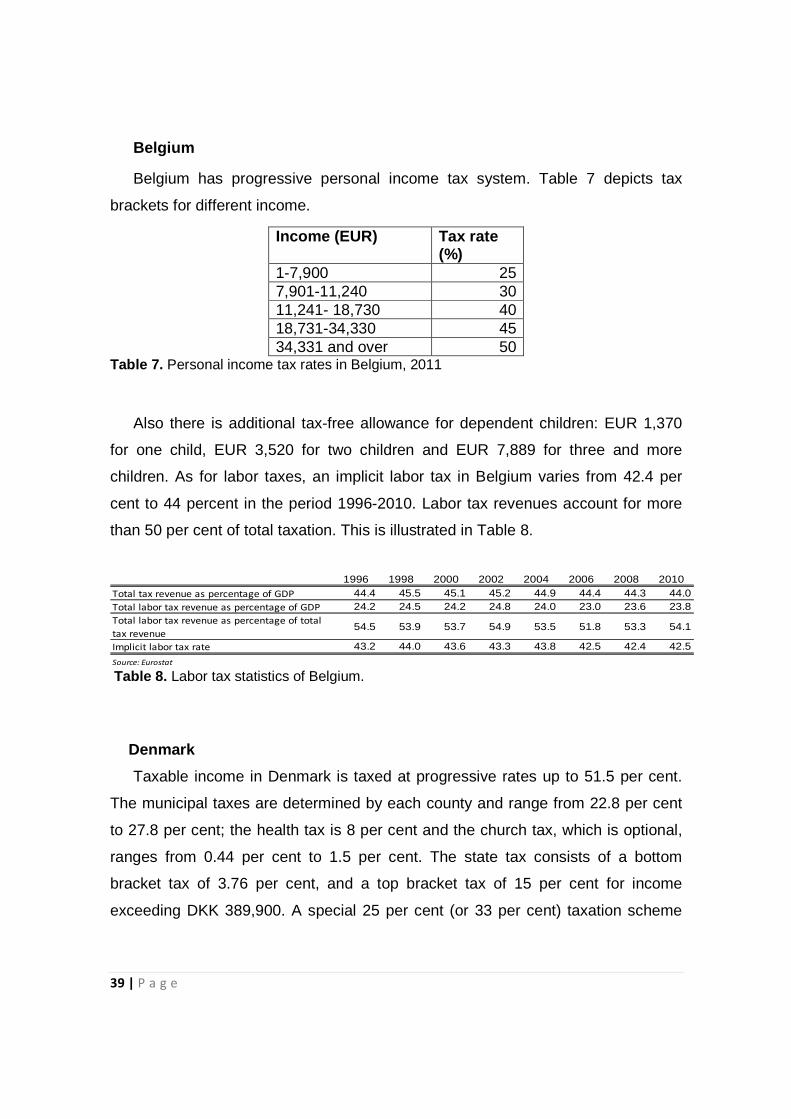

Recently there is discussion weather high overall taxes in Austria downgrade

the pace of growth (Schratzenstaller, 2007). Personal income tax is progressive

and maximum marginal rate is 50%. In 2012 tax brackets for personal income tax

is illustrated in Table 5.

Income (EUR)

111,00125,00160,001 and over

Table 5. Personal income tax

Employment income is also a subject to wage tax, which is withheld by the

employer and transferred to tax authorities. Table

implicit labor tax rate dynamics for the period 1996

Implicit tax rates in EU countries 1996-2010.

Recently there is discussion weather high overall taxes in Austria downgrade

the pace of growth (Schratzenstaller, 2007). Personal income tax is progressive

and maximum marginal rate is 50%. In 2012 tax brackets for personal income tax

Income (EUR) Tax rate(%)

1-11,000 0 11,001-25,000 36.5 25,001- 60,000 43.21 60,001 and over 50

Personal income tax rates in Austria, 2011

Employment income is also a subject to wage tax, which is withheld by the

employer and transferred to tax authorities. Table 6 shows labor tax revenue and

implicit labor tax rate dynamics for the period 1996-2010. As one can see labor tax

Recently there is discussion weather high overall taxes in Austria downgrade

the pace of growth (Schratzenstaller, 2007). Personal income tax is progressive

and maximum marginal rate is 50%. In 2012 tax brackets for personal income tax

Employment income is also a subject to wage tax, which is withheld by the

shows labor tax revenue and

2010. As one can see labor tax

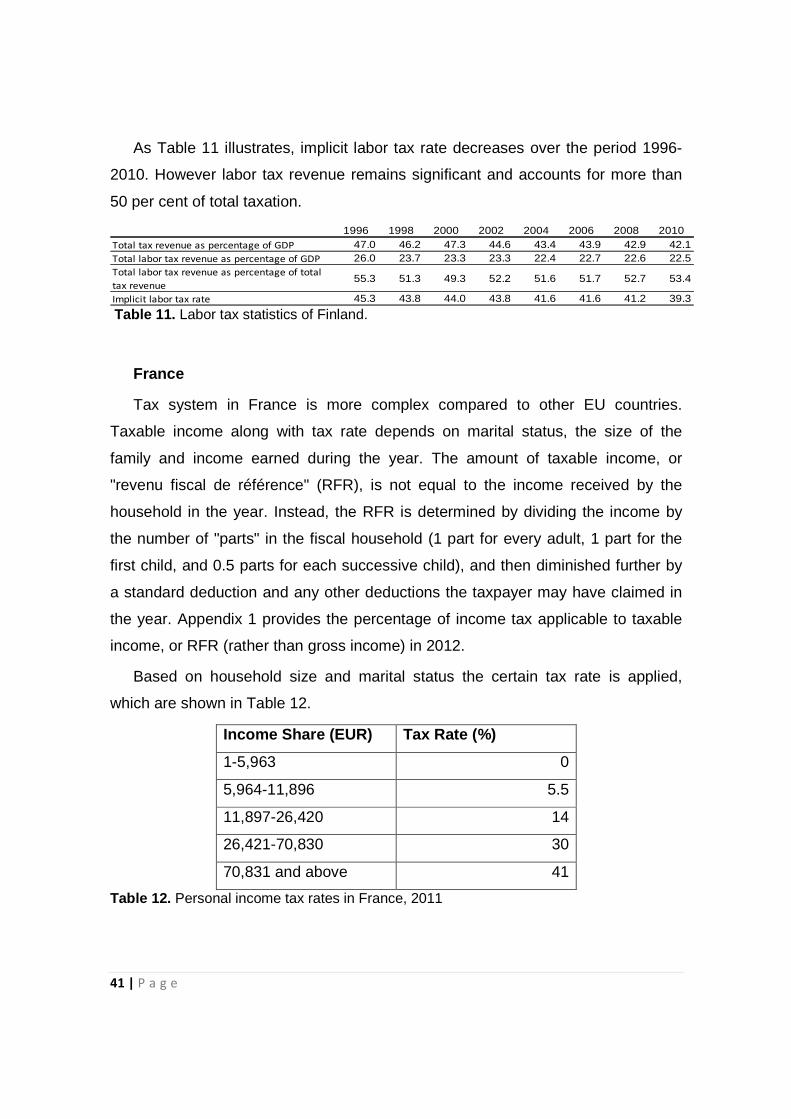

38 | P a g e

revenues amount more than half of total taxation, therefore taxes on labor are

significant in taxation system in Austria.

1996 1998 2000 2002 2004 2006 2008 2010Total tax revenue as percentage of GDP 42.8 44.1 43.0 43.7 43.0 41.5 42.7 41.9Total labor tax revenue as percentage of GDP 23.8 24.4 23.9 24.1 23.8 23.2 23.8 23.8Total labor tax revenue as percentage of total

tax revenue55.6 55.3 55.6 55.2 55.3 55.9 55.8 56.8

Implicit labor tax rate 39.4 40.3 40.1 40.8 41.1 40.9 41.3 40.5