the recovery of the brazilian economy · the economy reflects the adjusted policies booming capital...

TRANSCRIPT

WALTER BAÈRE FILHO

Deputy Executive Secretary of Planning, Development and Management

THE RECOVERY OF THE BRAZILIAN ECONOMY

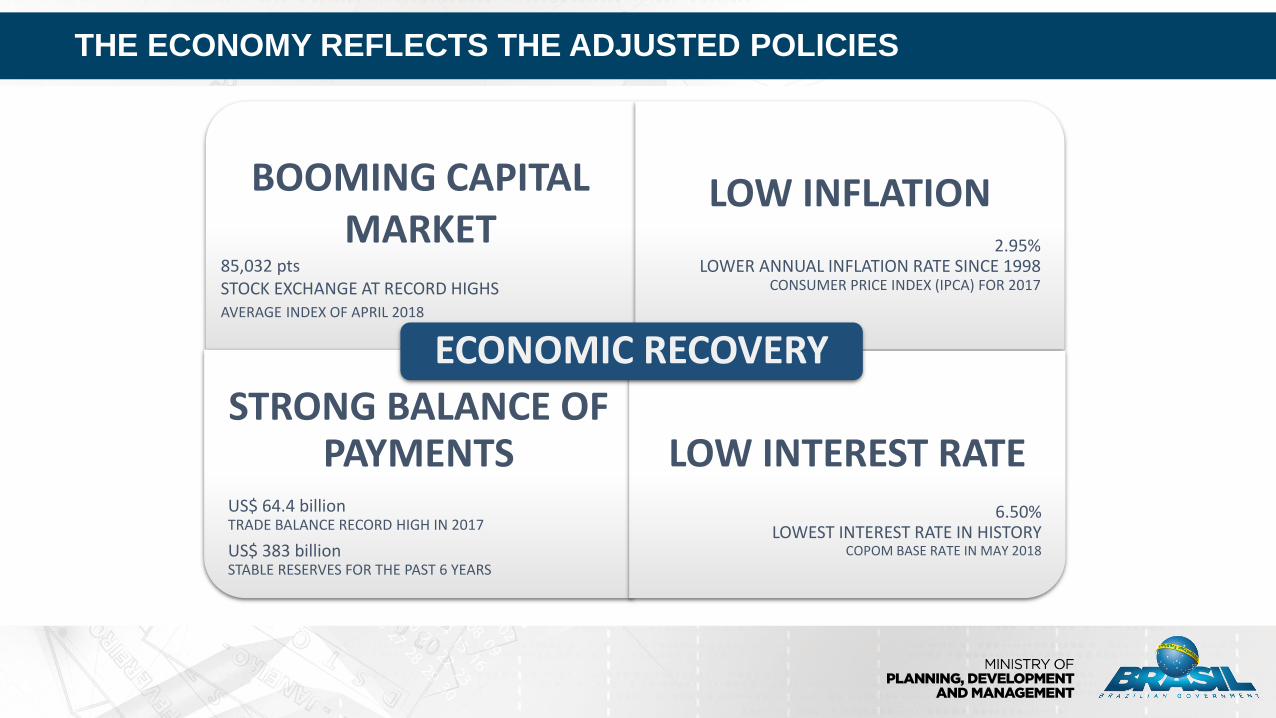

THE ECONOMY REFLECTS THE ADJUSTED POLICIES

BOOMING CAPITAL MARKET

85,032 ptsSTOCK EXCHANGE AT RECORD HIGHSAVERAGE INDEX OF APRIL 2018

LOW INFLATION2.95%

LOWER ANNUAL INFLATION RATE SINCE 1998CONSUMER PRICE INDEX (IPCA) FOR 2017

STRONG BALANCE OF PAYMENTS

US$ 64.4 billionTRADE BALANCE RECORD HIGH IN 2017

US$ 383 billionSTABLE RESERVES FOR THE PAST 6 YEARS

LOW INTEREST RATE6.50%

LOWEST INTEREST RATE IN HISTORYCOPOM BASE RATE IN MAY 2018

ECONOMIC RECOVERY

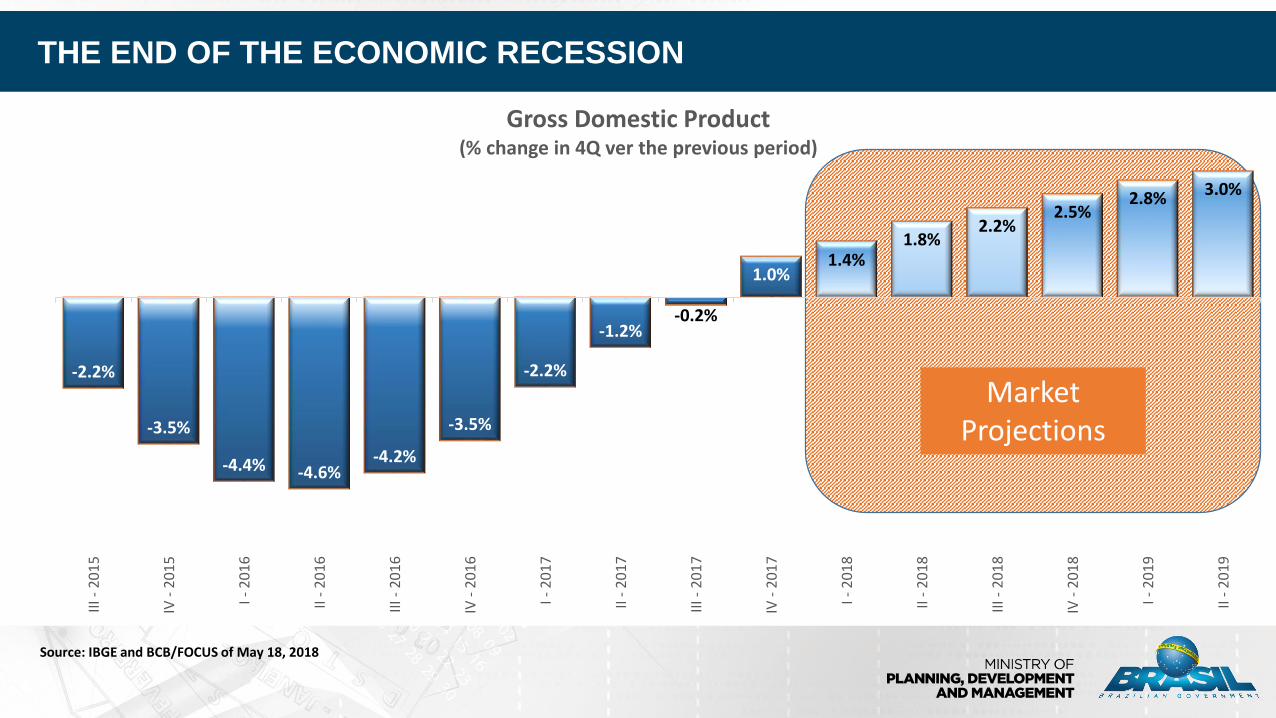

THE END OF THE ECONOMIC RECESSION

Source: IBGE and BCB/FOCUS of May 18, 2018

Market Projections

-2.2%

-3.5%

-4.4% -4.6%-4.2%

-3.5%

-2.2%

-1.2%-0.2%

1.0%1.4%

1.8%2.2%

2.5%2.8% 3.0%

III -

20

15

IV -

20

15

I - 2

01

6

II -

20

16

III -

20

16

IV -

20

16

I - 2

01

7

II -

20

17

III -

20

17

IV -

20

17

I - 2

01

8

II -

20

18

III -

20

18

IV -

20

18

I - 2

01

9

II -

20

19

Gross Domestic Product(% change in 4Q ver the previous period)

THE LABOR MARKET RECOVERS

4

Source: CAGED/MTE

2,629,827

2,026,571

1,372,5941,138,562

420,690

-1,534,989-1,326,558

-18,395

336,855

2010 2011 2012 2013 2014 2015 2016 2017 2018 - (JAN - APR)

Net Job Creation/Destruction (YTD)Number of People

5.90

4.31

5.91 6.50

5.84 5.91

6.41

10.67

6.29

2.95 3.50

4.01 4.00

-

2.00

4.00

6.00

8.00

10.00

12.00

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

IPCA (acum. 12m) Meta de Inflação Limite para efeito de cumprimento da meta

Source: IBGE and BCB2017-2020: BCB/Focus of of May. 18, 2018

BRAZIL ADOPTED A SUCCESSFUL INFLATION TARGET REGIME

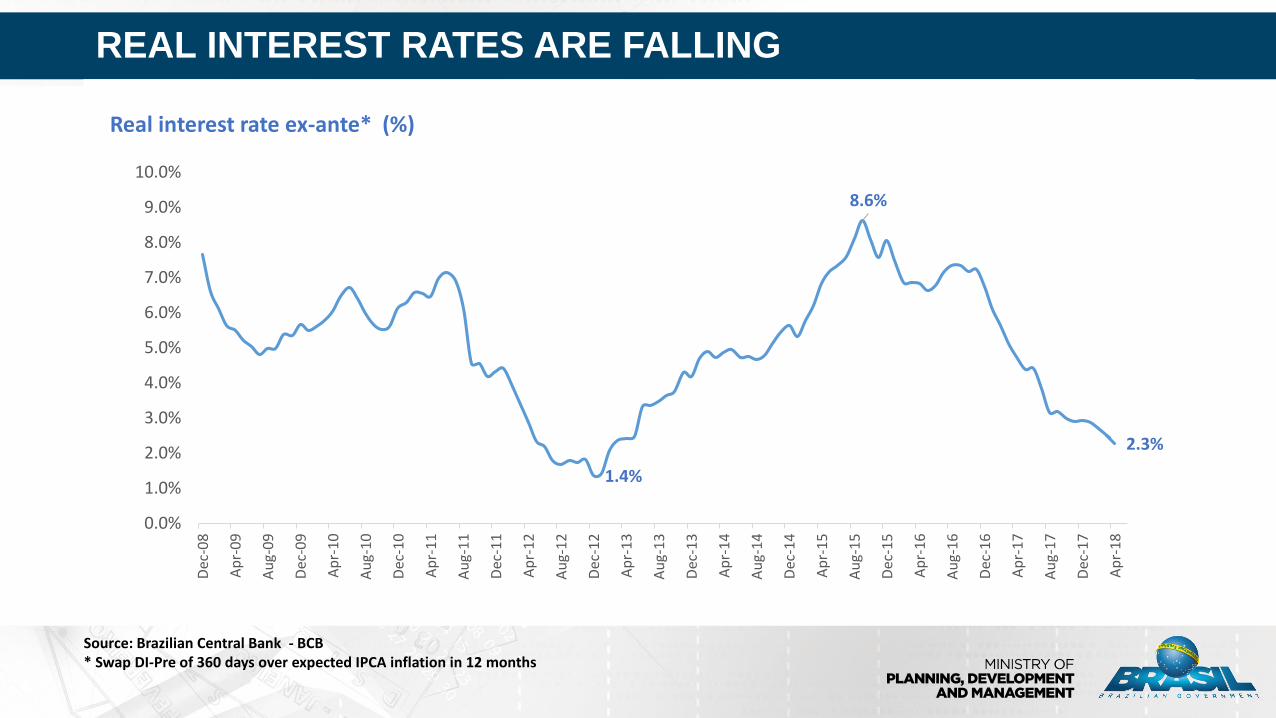

REAL INTEREST RATES ARE FALLING

Source: Brazilian Central Bank - BCB* Swap DI-Pre of 360 days over expected IPCA inflation in 12 months

1.4%

8.6%

2.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Dec

-08

Ap

r-0

9

Au

g-0

9

Dec

-09

Ap

r-1

0

Au

g-1

0

Dec

-10

Ap

r-1

1

Au

g-1

1

Dec

-11

Ap

r-1

2

Au

g-1

2

Dec

-12

Ap

r-1

3

Au

g-1

3

Dec

-13

Ap

r-1

4

Au

g-1

4

Dec

-14

Ap

r-1

5

Au

g-1

5

Dec

-15

Ap

r-1

6

Au

g-1

6

Dec

-16

Ap

r-1

7

Au

g-1

7

Dec

-17

Ap

r-1

8

Real interest rate ex-ante* (%)

35000

45000

55000

65000

75000

85000

95000

Bo

vesp

a In

dex

THE STOCK EXCHANGE IS AT RECORD HIGHS

Source: Bloomberg

May 17, 2018 January 26, 2016 Change %

Ibovespa 83,622 37,497 123%

Petrobras (PETR3) 30.21 5.96 407%

Vale do Rio Doce (VALE3) 55.38 8.94 519%

Banco do Brasil (BBAS3) 32.86 12.89 155%

Eletrobras (ELET3) 18.98 4.88 289%

Closing prices as of Mar. 17, 2018

TRADE BALANCE AT RECORD HIGH

64,060

901

637

0

200

400

600

800

1000

1200

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000Fe

b-1

0A

pr-

10

Jun

-10

Au

g-1

0O

ct-1

0D

ec-1

0Fe

b-1

1A

pr-

11

Jun

-11

Au

g-1

1O

ct-1

1D

ec-1

1Fe

b-1

2A

pr-

12

Jun

-12

Au

g-1

2O

ct-1

2D

ec-1

2Fe

b-1

3A

pr-

13

Jun

-13

Au

g-1

3O

ct-1

3D

ec-1

3Fe

b-1

4A

pr-

14

Jun

-14

Au

g-1

4O

ct-1

4D

ec-1

4Fe

b-1

5A

pr-

15

Jun

-15

Au

g-1

5O

ct-1

5D

ec-1

5Fe

b-1

6A

pr-

16

Jun

-16

Au

g-1

6O

ct-1

6D

ec-1

6Fe

b-1

7A

pr-

17

Jun

-17

Au

g-1

7O

ct-1

7D

ec-1

7Fe

b-1

8A

pr-

18

Trade Balance Exports Imports

Trade BalanceAccumulated in 1 yearUS$ mm. FOB

Exports and ImportsDaily average accumulated in 1 year

US$ mm. FOB

Source: MDIC

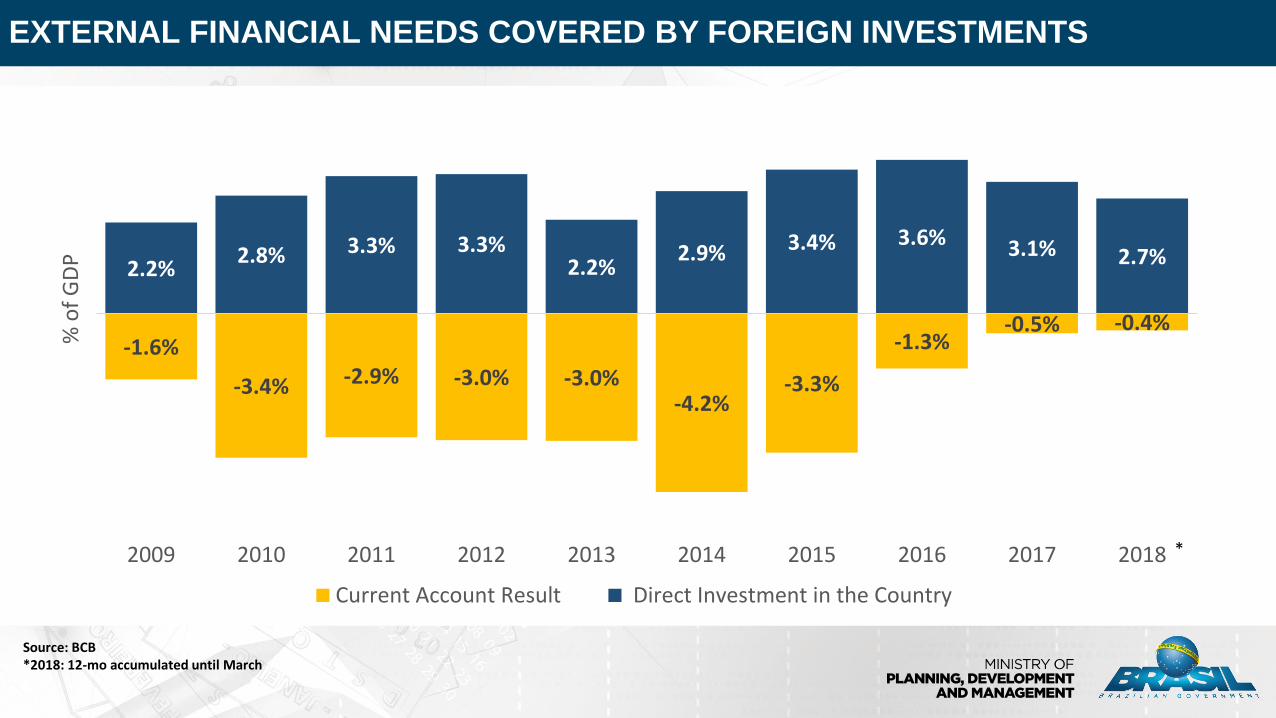

EXTERNAL FINANCIAL NEEDS COVERED BY FOREIGN INVESTMENTS

-0.4%-0.5%-1.3%

-3.3%-4.2%

-3.0%-3.0%-2.9%-3.4%

-1.6%

2.7%3.1%3.6%3.4%2.9%2.2%

3.3%3.3%2.8%2.2%

2018201720162015201420132012201120102009

% o

f G

DP

Current Account Result Direct Investment in the Country

Source: BCB*2018: 12-mo accumulated until March

*

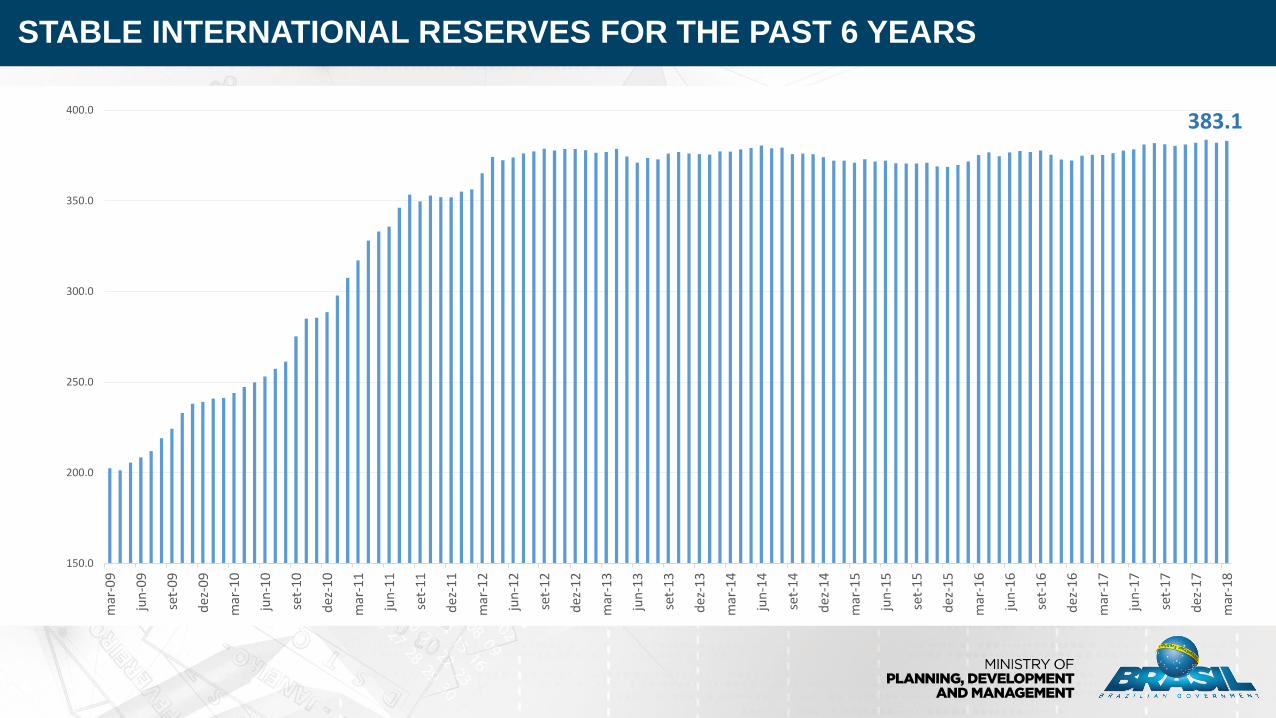

STABLE INTERNATIONAL RESERVES FOR THE PAST 6 YEARS

383.1

150.0

200.0

250.0

300.0

350.0

400.0m

ar-0

9

jun

-09

set-

09

dez

-09

mar

-10

jun

-10

set-

10

dez

-10

mar

-11

jun

-11

set-

11

dez

-11

mar

-12

jun

-12

set-

12

dez

-12

mar

-13

jun

-13

set-

13

dez

-13

mar

-14

jun

-14

set-

14

dez

-14

mar

-15

jun

-15

set-

15

dez

-15

mar

-16

jun

-16

set-

16

dez

-16

mar

-17

jun

-17

set-

17

dez

-17

mar

-18

ECONOMIC RECOVERY

Fiscal Consolidation Structural Reforms

Public-Private Partnership

Improvement of the regulatory framework and

business environment

ECONOMIC GROWTH

FISCAL CONSOLIDATION

New Fiscal Regime: Constitutional Amendment 95/2016 of the Public

Expenditure Cap.

Modernization of Public Management: improvement of electronic systems

and processes, strengthening and expanding Digital Government

practices.

Modernization of State Enterprises Management: Strict rules for

purchases, bids and for the appointment of managerial positions and

reduction in the effective staff of non-dependent state companies.

12

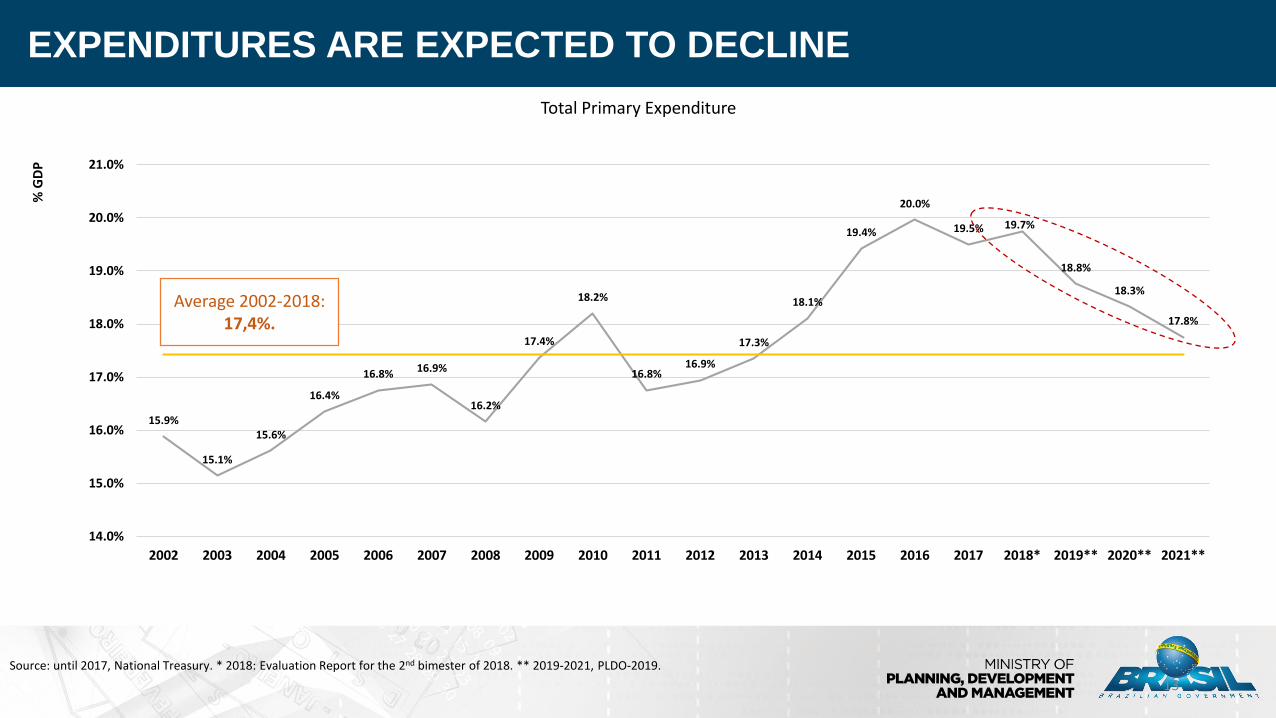

EXPENDITURES ARE EXPECTED TO DECLINE

13

15.9%

15.1%

15.6%

16.4%

16.8% 16.9%

16.2%

17.4%

18.2%

16.8%16.9%

17.3%

18.1%

19.4%

20.0%

19.5% 19.7%

18.8%

18.3%

17.8%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018* 2019** 2020** 2021**

% G

DP

Total Primary Expenditure

Average 2002-2018:17,4%.

Source: until 2017, National Treasury. * 2018: Evaluation Report for the 2nd bimester of 2018. ** 2019-2021, PLDO-2019.

• Fiscal recovery of States

• Federal Government posts primary deficits since 2014: Fiscal challenges involve both expenditures and revenues. The fiscal crisis promotes the search for efficiency of public

expenditures. At the same time, the Federal Government implements an agenda of

modernization of public management. Better public services are related to the revision of public expenditures

and to the improvement in revenues.

THE FISCAL CHALLENGE

14

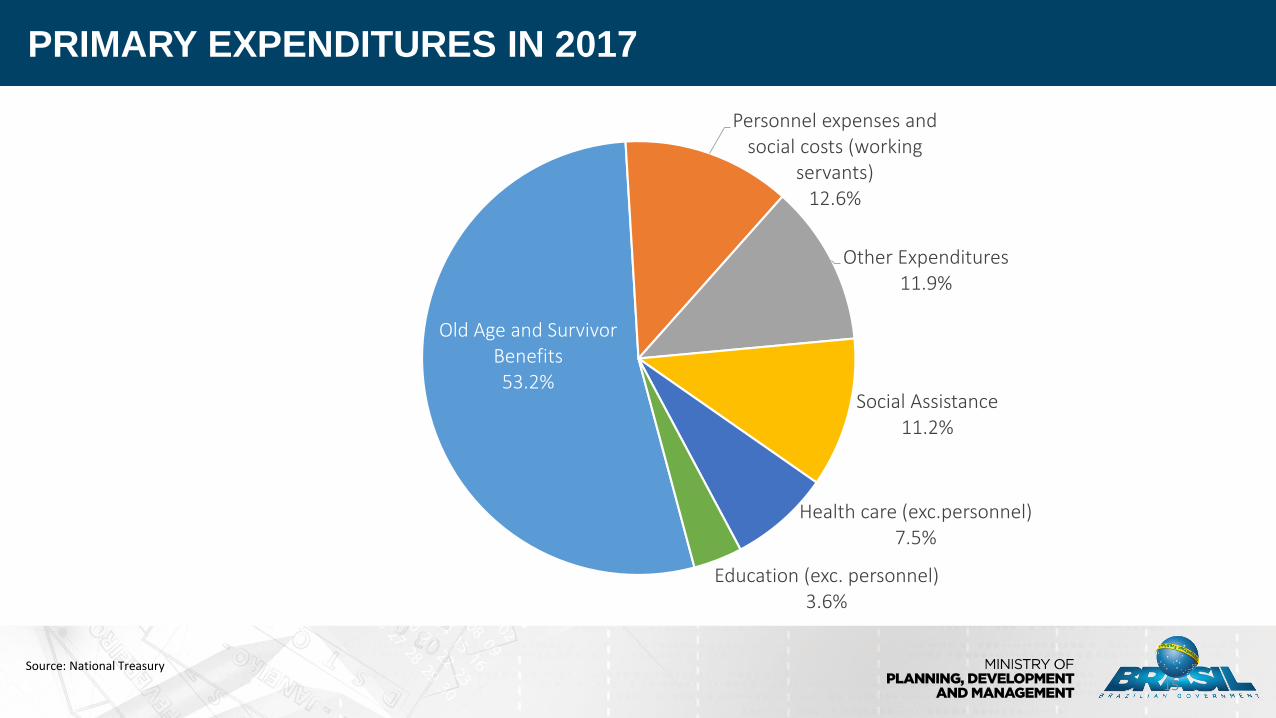

PRIMARY EXPENDITURES IN 2017

15

Source: National Treasury

Old Age and Survivor Benefits53.2%

Personnel expenses and social costs (working

servants)12.6%

Other Expenditures11.9%

Social Assistance 11.2%

Health care (exc.personnel)7.5%

Education (exc. personnel)3.6%

A REFORM OF THE SOCIAL SECURITY SYSTEM IS NEEDED

16

-1.2% -1.3% -1.1%-0.8% -0.8% -0.9% -1.0%

-1.4%

-2.4%-2.8% -2,9% -2.8% -2.9% -3.1%

5.3% 5.5% 5.5% 5.6% 5.7% 5.8% 5.8% 5.8% 5.7% 5.7% 5.6% 5.7% 5.7% 5.7%

6.4%6.7% 6.6% 6.4% 6.6% 6.7% 6.8%

7.3%

8.1%8.5% 8.5% 8.4% 8.6% 8.8%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018* 2019** 2020** 2021**

% P

IB

Resultado RGPS Receita Líquida RGPS Despesa Líquida RGPS

% G

DP

Revenues Net RevenuesExpenditures

Source: until 2017, National Treasury. * 2018: Evaluation Report for the 2nd bimester of 2018. ** 2019-2021, PLDO-2019.

Result (RGPS)

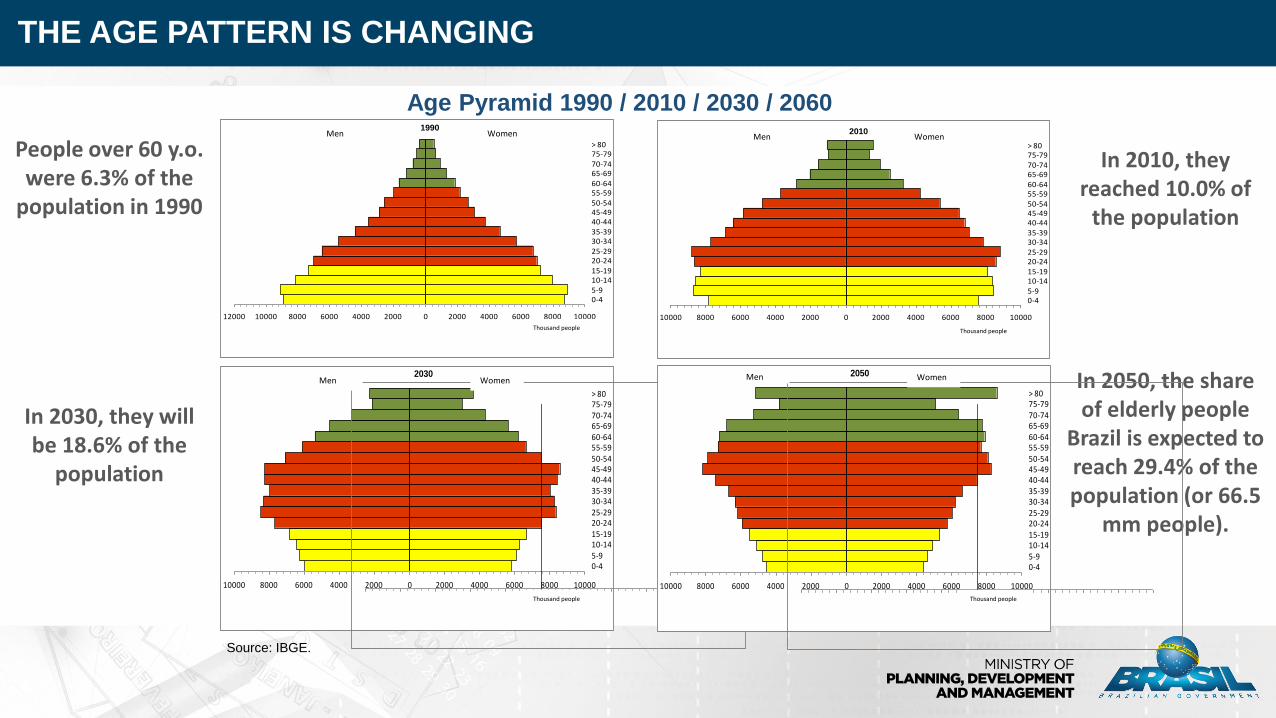

THE AGE PATTERN IS CHANGING

Age Pyramid 1990 / 2010 / 2030 / 2060

Source: IBGE.

People over 60 y.o. were 6.3% of the

population in 1990

In 2010, theyreached 10.0% of

the population

In 2030, they willbe 18.6% of the

population

In 2050, the shareof elderly people

Brazil is expected toreach 29.4% of thepopulation (or 66.5

mm people).

12000 10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres1990

10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres2010

10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres2030

10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres

10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres2050

10000 8000 6000 4000 2000 0 2000 4000 6000 8000 10000

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79> 80

Milhares

Homens Mulheres

Men Women

Thousand people

Men Women

Thousand people

Men Women

Thousand people

Men Women

Thousand people

GENERAL GOVERNMENT GROSS DEBT

Sources: BCB and National Treasury. *PLDO-2019.

18

56.0%59.2%

51.8% 51.3%53.7%

51.5%

56.3%

65.5%

70.0%

74.0%75.7%

77.7%79.7% 81.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

% P

IB%

GD

P

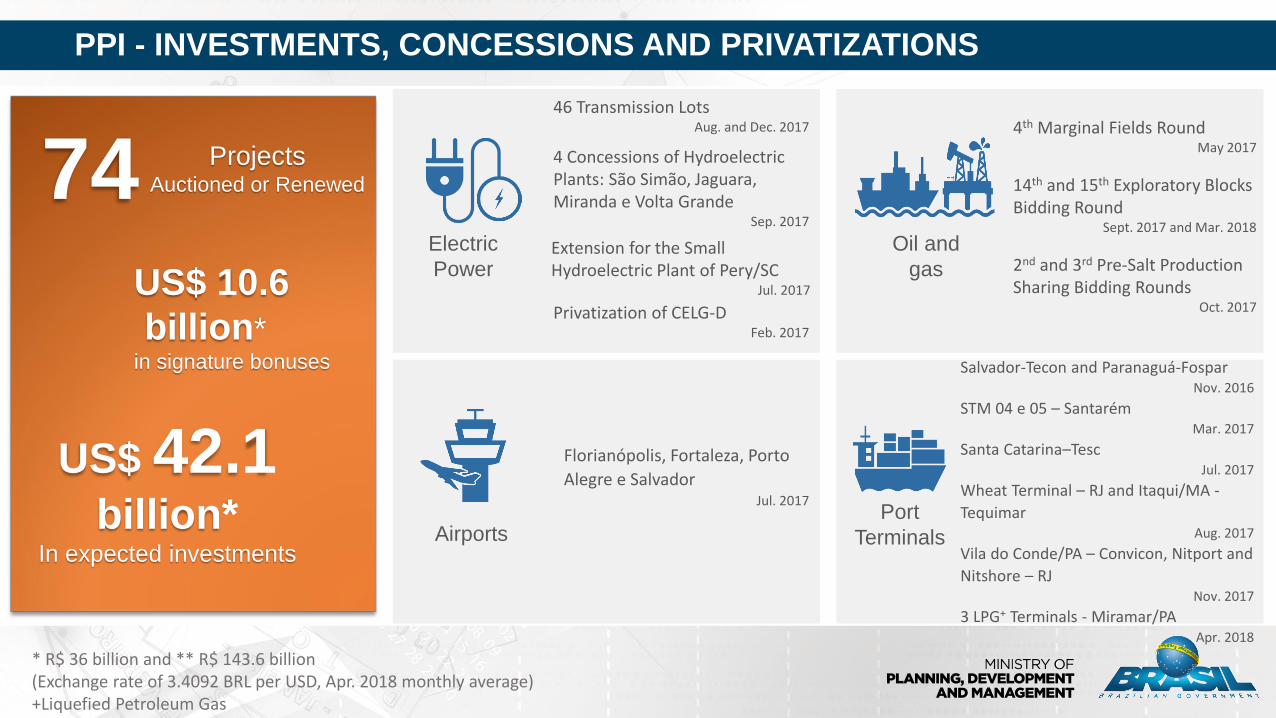

PPI - INVESTMENTS, CONCESSIONS AND PRIVATIZATIONS

US$ 10.6

billion*in signature bonuses

* R$ 36 billion and ** R$ 143.6 billion(Exchange rate of 3.4092 BRL per USD, Apr. 2018 monthly average)+Liquefied Petroleum Gas

74 ProjectsAuctioned or Renewed

US$ 42.1 billion*

In expected investments

Electric

Power

Privatization of CELG-DFeb. 2017

46 Transmission LotsAug. and Dec. 2017

4 Concessions of Hydroelectric Plants: São Simão, Jaguara, Miranda e Volta Grande

Sep. 2017

Extension for the Small Hydroelectric Plant of Pery/SC

Jul. 2017

Oil and

gas

4th Marginal Fields RoundMay 2017

14th and 15th Exploratory Blocks Bidding Round

Sept. 2017 and Mar. 2018

2nd and 3rd Pre-Salt Production Sharing Bidding Rounds

Oct. 2017

Port

Terminals

Florianópolis, Fortaleza, Porto

Alegre e SalvadorJul. 2017

Airports

Salvador-Tecon and Paranaguá-FosparNov. 2016

STM 04 e 05 – SantarémMar. 2017

Santa Catarina–TescJul. 2017

Wheat Terminal – RJ and Itaqui/MA -

TequimarAug. 2017

Vila do Conde/PA – Convicon, Nitport and

Nitshore – RJNov. 2017

3 LPG+ Terminals - Miramar/PAApr. 2018

ONGOING PROJECTS

20

101PPI Projects

US$ 39.4 billion*

in expected investmentsPort Terminals

25

Highways Railways

8 8Oil and gas

Electric PowerMining

21 Pre-salt sharing

1 Marginal accumulation

32UHE - 1 Extension

Privatization

6 Distributors and Eletrobras

Concession

24 Transmission Lots

4Concession to exploitation

of Mining areas

4 Biddings 5 Renewals

Lottery

1Concession of the

right to exploit

3 Biddings4 Studies

17Airports

13 Concessions

4 Shareholding selling

COMAER

1Public-Private Partnership

(PPP)

Currency House

1Privatization

Supply

2CEASAMINAS

CASEMGPrivatization

*R$ 134.3 billion(Exchange rate of 3.4092 BRL per USD, Apr. 2018 monthly average)

PRIORITY AGENDA

Tax simplification: Social Contribution Reform

Central Bank autonomy

New legal framework for tenders and public

procurements

New public finance law

Regulation on civil servants’ salaries

21

Business improvement and recovery program of

state-owned companies

New real estate purchase contracts law

Update of the General Telecommunications Law

Privatization of Eletrobras

Strengthening of Regulatory Agencies

High-level event for CEOs

2 full days of Panels with Ministers and CEOs

Macroeconomic Scenario

Investment Opportunities

Regulatory Framework

More information and pre-register: www.brasilinvestmentforum.com

BRASIL INVESTMENT FORUM 2018

May 29-30, in São Paulo, Brazil

Unique opportunity for direct meetings with high-level Brazilian authorities

WALTER BAÈRE FILHO

Deputy Executive Secretary of Planning, Development and Management

THANK YOU!