the private equity economic impact

DESCRIPTION

TRANSCRIPT

The Private Equity Economic Impact

Javier Echarri,EVCA Secretary General

Bratislava,

20th September 2005

Agenda

Current size and activity levels

Economic impact on companies

Economic impact on European economies

Recommendations

Introduction to EVCA

Established in 1983 and based in Brussels

Represents the European private equity and venture capital industry (PE/VC) and promotes the asset class both within Europe and throughout the World

Well over 900 members, mainly European

PE/VC fund management companies

Institutional investors (banks, pension funds, insurance companies...)

Professional advisors (lawyers, placement agents, investment bankers...)

National (European) Trade Associations

Current size and activity levels

Evolution Activity Flows

48.0

40.0

20.320.0

8.0

27.027.5

25.4

4.4

27.5

36.9

27.6

24.3

35

25.1

14.5

6.8

9.7

5.5

29.1

3.63.1

5.8

19.6

7.08.6

9.1

12.513.6

10.7

0

5

10

15

20

25

30

35

40

45

50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Funds Raised

Investments

Divestments

€ billion

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

Sources of New Funds Raised

Corporate Investors7.0%

Private Individuals7.6%

Academic Institutions

1.5%

Capital Markets2.2%

Other9.2%

Fund of Funds13.5%

Insurance Companies

12.0%

Pension Funds19.3%

Banks21.7%

Government Agencies

6.1%

2004 2003

Corporate Investors4.8%

Private Individuals3.2%

Government Agencies

6.8%

Other17.3%

Capital Markets0.3%

Academic Institutions

1.5%Banks21.5%

Pension Funds19.4%

Fund of Funds16.4%

Insurance Companies

8.7%

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

2004: €37 Billion Invested. Record Level

3.65.6

8.5

14.4 15.312.1

17.920.7

26.6

2.63.2

4.1

6.0

10.7

19.6

12.2

9.8

8.4

10.3

2.90

5

10

15

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

€ billion

Venture Capital

Buyout

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

Stage Distribution of InvestmentsAmount Invested

Buyout63.4%

Replacement Capital7.9%

Expansion21.4%

Seed0.5% Start-up

6.8%

Buyout69.7%

Replacement Capital2.5%

Expansion21.4%

Start-up6.0%

Seed0.4%

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

2004 2003

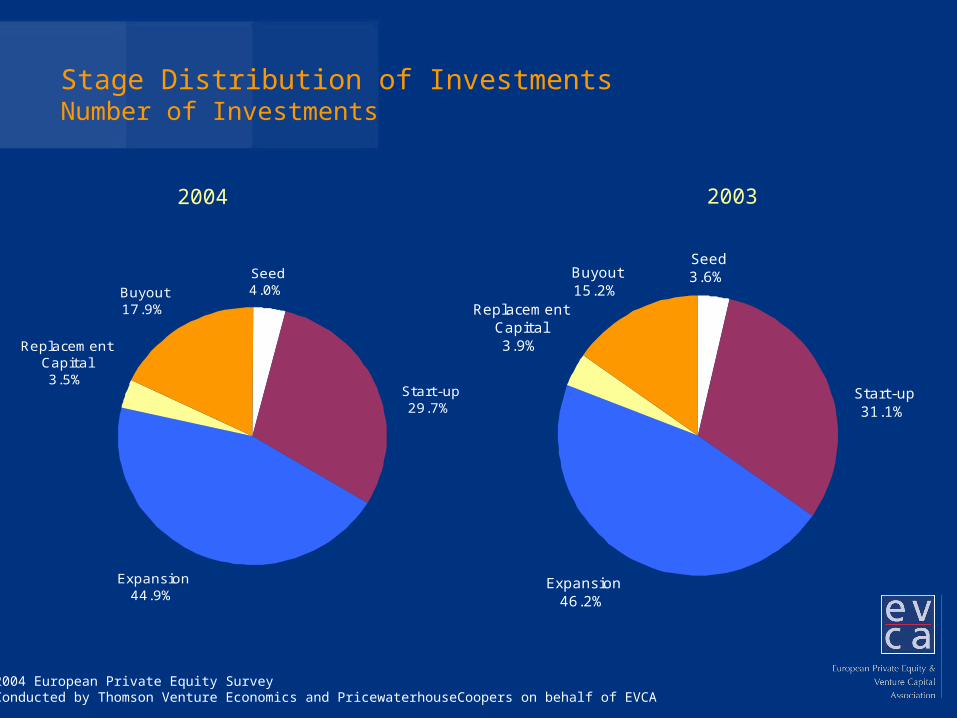

Stage Distribution of InvestmentsNumber of Investments

Buyout17.9%

Replacement Capital3.5%

Expansion44.9%

Start-up29.7%

Seed4.0%

Buyout15.2%

Replacement Capital3.9%

Expansion46.2%

Start-up31.1%

Seed3.6%

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

2004 2003

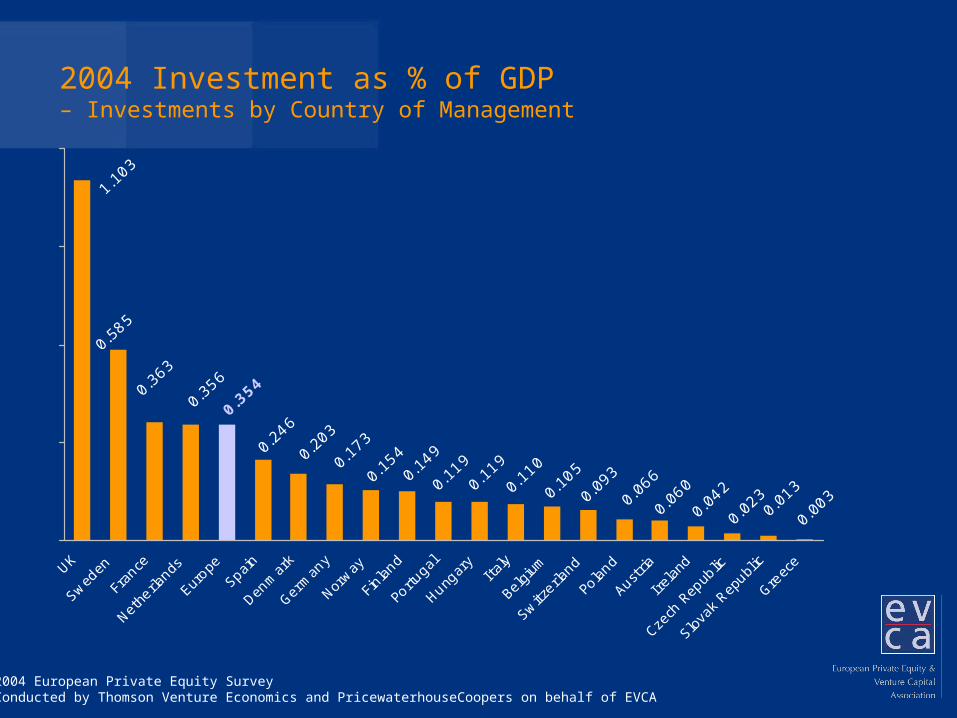

2004 Investment as % of GDP – Investments by Country of Management

0.00

30.

013

0.02

30.

042

0.06

00.

066

0.09

30.

105

0.11

00.

119

0.11

90.

149

0.15

40.

173

1.10

3

0.58

5

0.36

3

0.35

6

0.35

4

0.24

6

0.20

3

UK

Swed

en

Fran

ce

Nethe

rland

s

Euro

pe

Spain

Denm

ark

Germ

any

Norway

Finl

and

Portu

gal

Hunga

ryItaly

Belg

ium

Switz

erland

Poland

Aust

ria

Irel

and

Czec

h Re

publ

ic

Slov

ak R

epub

lic

Greec

e

2004 European Private Equity SurveyConducted by Thomson Venture Economics and PricewaterhouseCoopers on behalf of EVCA

Economic Impact on Companies

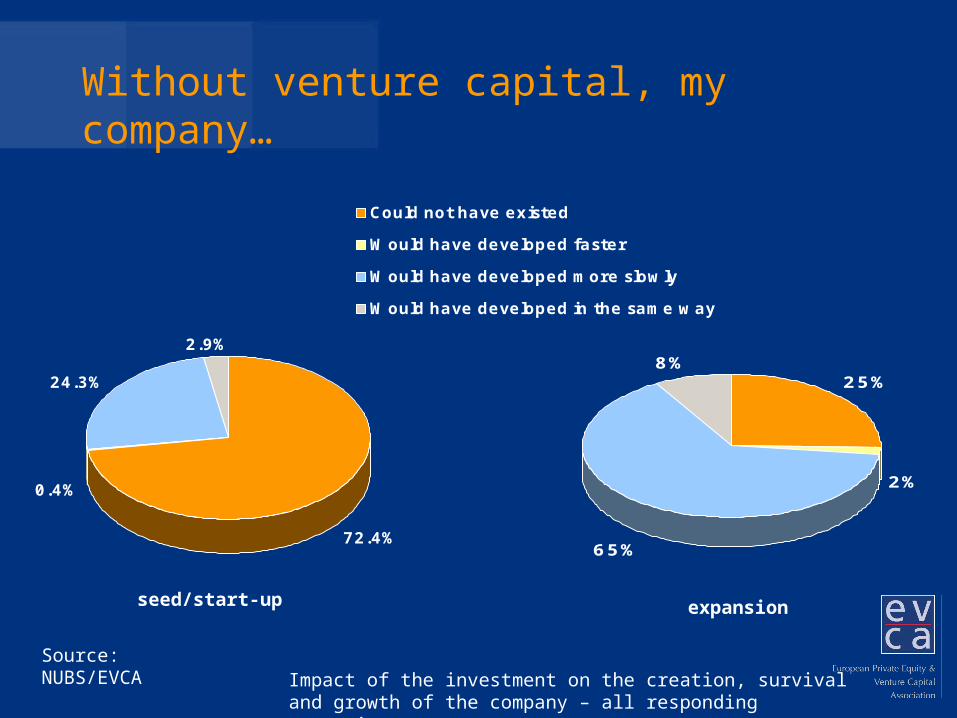

Without venture capital, my company…

would have developed

faster (0.8% )

would have developed in

the same way (4.7% )

could not have existed or

would have developed

more slowly (94.5% )

Impact of the investment on the creation, survival and growth of the company – all responding companies

Source: NUBS/EVCA

Without venture capital, my company…

72.4%

0.4%

24.3%

2.9%

Could not have existed

Would have developed faster

Would have developed more slowly

Would have developed in the same way

25%

2%

65%

8%

seed/start-up expansion

Impact of the investment on the creation, survival and growth of the company – all responding companies

Source: NUBS/EVCA

In the absence of a Buyout, my company…

would have developed in

the same way (14% )

would have developed

faster (2% )

would no longer exist or

would have developed

more slowly (84% )

The overall impact of the buyout on the survival and growth of the company

Source: CMBOR/EVCA

Venture backed: Comparison with competitors – increase in turnover and EBIT

0% 10% 20% 30% 40% 50%

Much less

Slightly less

About the same

Slightly more

Much more

Turnover EBIT

Source: NUBS/EVCA

Respondent’s perceptions of post-investment increases in turnover and EBIT in comparison to competitors – all responding companies

Post buyout increases in turnover and Post buyout increases in turnover and EBIT in comparison to competitors: EBIT in comparison to competitors: respondents’ perceptionsrespondents’ perceptions

0.00% 10.00% 20.00% 30.00% 40.00%

Much less

Slightly less

About the same

Slightly more

Much more

Turnover EBIT

Source: CMBOR/EVCA

Percentage increase in expenditure between the time of the initial investment and the time of the survey

0% 200% 400% 600% 800% 1000% 1200% 1400% 1600%

Research andDevelopment

MarketingExpenditure

CapitalExpenditure

Training

Mean Median

0% 100% 200% 300% 400% 500% 600% 700%

Seed/start-up stage companies Expansion stage companies

Source: NUBS/EVCA

Expenditure in four areas as a percentage of sales before and after the buyout

0% 1% 2% 3% 4% 5% 6% 7%

Research &Development

Marketingexpenditure

Capitalexpenditure

Training

At time of buyout Last Year

Source: CMBOR/EVCA

Impact on European Economies

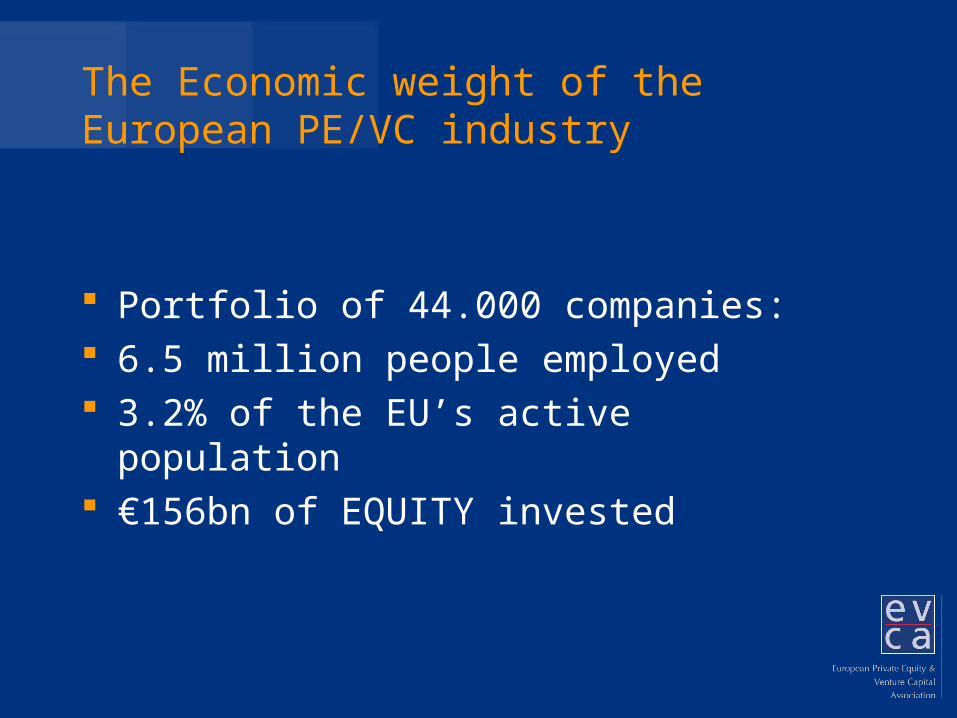

The Economic weight of the European PE/VC industry

Portfolio of 44.000 companies: 6.5 million people employed 3.2% of the EU’s active population €156bn of EQUITY invested

The Economic weight of the European PE/VC industry

Between 1999 and 2003: Created 1.1 million jobs 585.000 in Early stage companies 450.000 in Later stage companies

Recommendations

Competitiveness of the Economies

Competitiveness Factors

Macroeconomic conditions

Monetary Policy

Fiscal Policy

Policy initiatives

Factor endowments(infrastructure

et al.)

ICT

Access tofinance

Entre-preneurship

Productivity&

innovationAdministrative& regulatoryenvironment

Structuralconditions

Access tohumancapital

Innovation&

knowledgediffusion

Open &well-functioningmarkets

But ICT is only a part of the story

A need to boost entrepreneurship in Europe

Total Entrepreneurial activity by advanced economies 2000-2003

Source: EVCA based on Global Entrepreneurship Monitor - 2003 Executive Report and International Monetary Fund

Country Ranking Country Ranking

Korea 1 Greece 14

New Zealand 2 Israël 15

Australia 3 United Kingdom 16

United States 4 Spain 17

Iceland 5 Germany 18

Canada 6 Singapore 19

Ireland 7 Sweden 20

Norway 8 The Netherlands

21

Italy 9 France 22

Switzerland 10 Taiwan 23

Portugal 11 Belgium 24

Denmark 12 Japan 25

Finland 13 Hong Kong 26

Both in Europe and in the US, finance is an obstacle in setting up a business. Red tape is more an European obstacle

0% 10% 20% 30% 40% 50% 60% 70% 80%

It is difficult to obtainsufficient information on how

to start a business

One should not start abusiness if there is a risk it

might fail

The current economic climateis not favourable for peoplewho want to start their own

business

It is difficult to start one'sown business due to thecomplex administrative

procedures

It is difficult to start one'sown business due to a lack

of available financial support

USA EU 25

Source: Flash Eurobarometer – Entrepreneurship 2004

Do you … with the following opinions?% Agree (Strongly + Agree)

Current problems

Difficult to finance a project

Difficult to establish a company Difficult to run a new company

Policy Measures: More efforts should be targeted at entrepreneurship in education and the reduction of red tape

Typology of objectives Share in percentage

Fostering and Innovation Culture 29.9

Including: Education & Training 5.8

Establishing a Framework conducive to Innovation 20.7

Including: Administrative Simplification 0.9

Including: Legal and Regulatory Environment 0.6

Including: Financing 14.2

Gearing Research to Innovation 49.2

Including: Start-up of technology-based companies 11.5

Including: Co-operation Research/Universities/Companies 14.4

Other Objectives 0.3

Total 100.0

Share of the respective objectives of policy measures % of total number of policie measures targeting innovation in the EU-15

Source: TrendChart/European Commission / note: information as of 2004

EVCA’s Recommendations

Foster Europe’s entrepreneurial environment, culture and education:

Entrepreneurship through an adequate regulatory framework

Requirements for company formation, lighten the burden of regulation, improve access to finance and adjust insolvency and bankruptcy rules to allow for an orderly end or restructuring of a failed business

Entrepreneurship through education and support programmes

Integrate entrepreneurship into education at all levels; enhance awareness of the positive relationship between entrepreneurs and private equity and venture capital firms

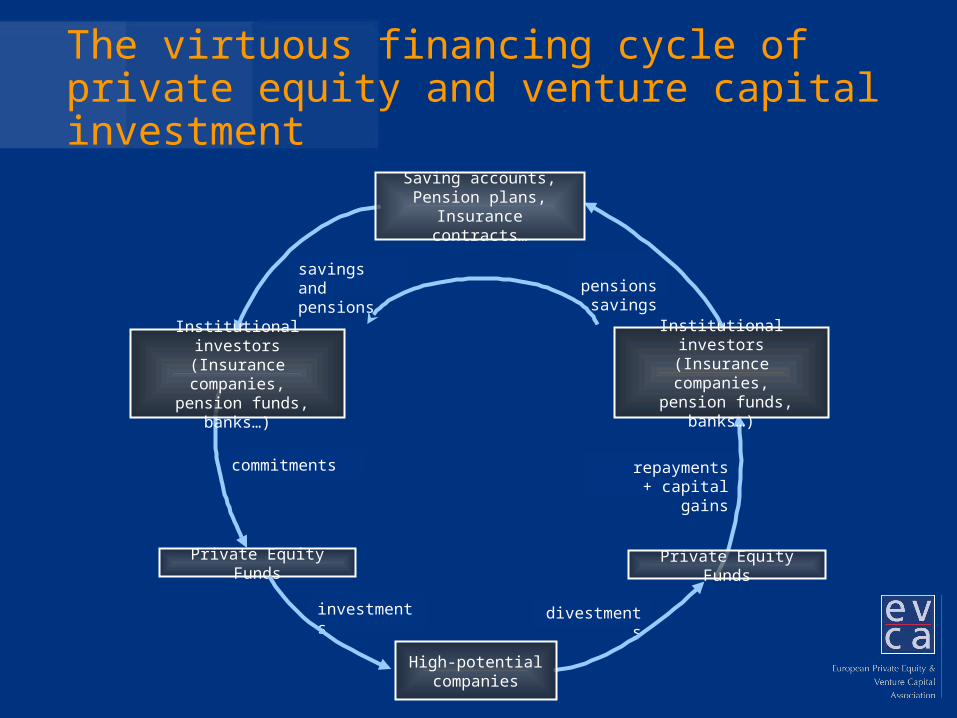

The Private Equity Ecosystem and Virtuous Cycle

The virtuous financing cycle of private equity and venture capital investment

repayments+ capital gains

commitments

divestments

pensions savings

savings and pensions

investments

Private Equity Funds

High-potential companies

Institutional investors(Insurance companies,

pension funds, banks…)

Private Equity Funds

Institutional investors(Insurance companies,

pension funds, banks…)

Saving accounts, Pension plans,

Insurance contracts…

repayments+ capital gains

commitments

divestments

pensions savings

savings and pensions

investments

Private Equity Funds

High-growth companies

Institutional investors(Insurance companies,

pension funds, banks…)

Private Equity Funds

Institutional investors(Insurance companies,

pension funds, banks…)

Saving accounts, Pension plans,

Insurance contracts…

Legal vehicle

Young innovative companies, family companies,

development potential, …High Growth Markets, trade sales,… who is buying?

Long term investment plans: Pension Funds

(Prudent Man Rule), Banks, Insurance

companies, …

Double Taxation

Permanent establishment

The virtuous financing cycle of private equity and venture capital investment

Thank You