the power of moving averages in financial markets by: michael viscuso

TRANSCRIPT

The Power of Moving Averages in Financial Markets

By: Michael Viscuso

Recall… A Moving Average is the average of the

past n days prices. A buy point is signaled when today’s

price is above its moving average and yesterday’s price is below its moving average.

A sell point is signaled when today’s price is below its moving average and yesterday’s price was above its moving average

Recall…. (cont.)

We are looking for the best n – the look-back period of the moving average

Small n’s are more responsive to daily changes

Large n’s are less responsive to daily changes

Pros and cons to both

Example of Moving Average for small n. (n=6)

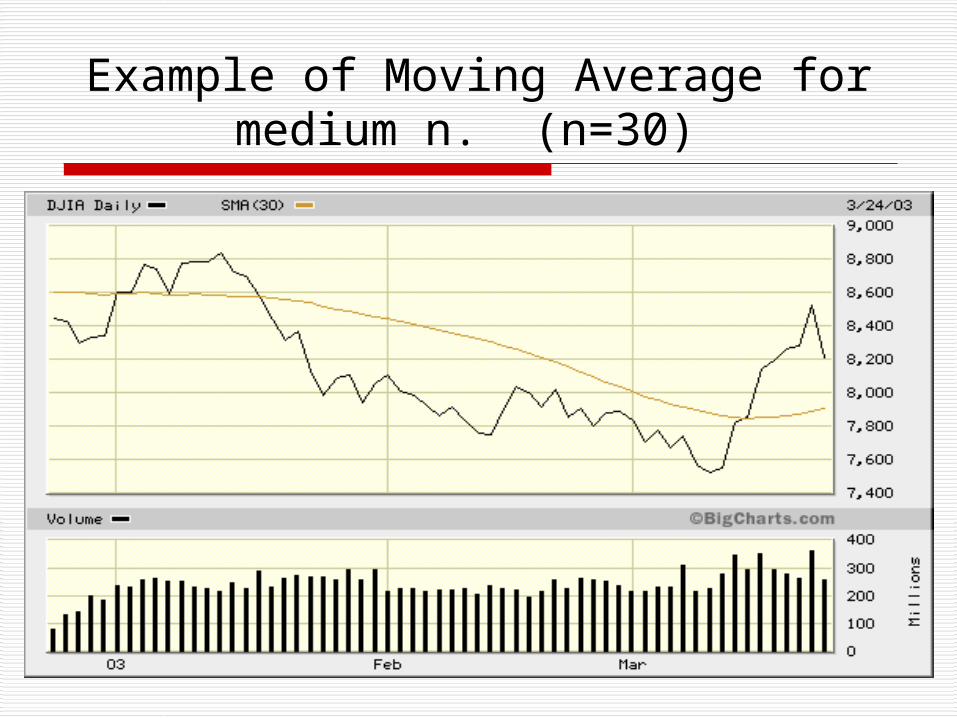

Example of Moving Average for medium n. (n=30)

Choosing the best n Choose which n’s you are going to

test Start with the first 12 months and see

which n did best over that time period; record it

Calculate best n for month 13 record the pair

Continue for all months in the data set

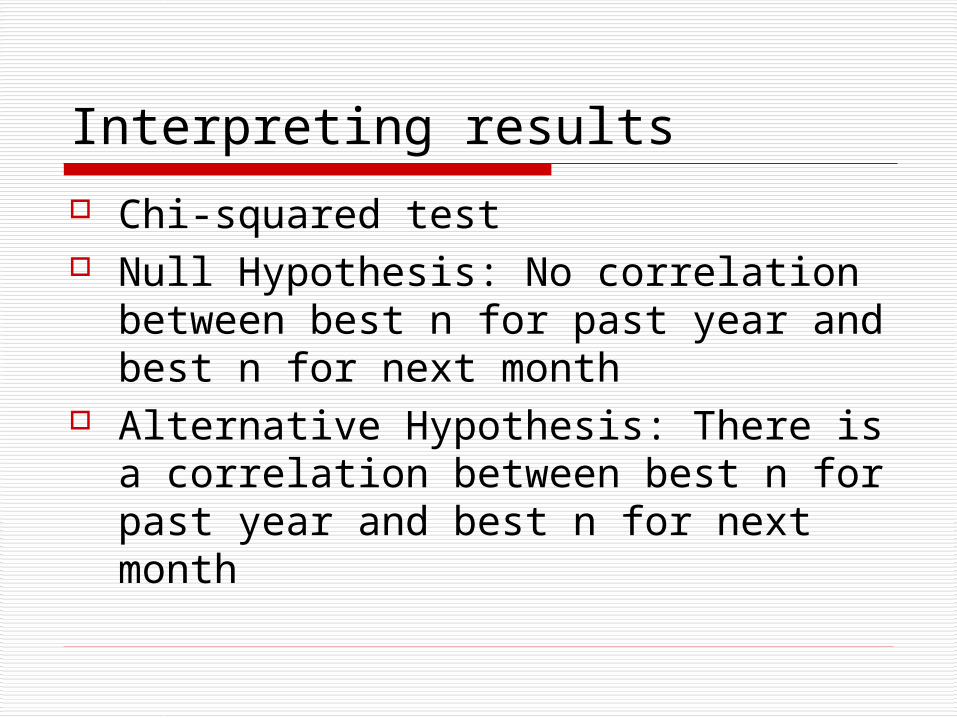

Interpreting results

Chi-squared test Null Hypothesis: No correlation

between best n for past year and best n for next month

Alternative Hypothesis: There is a correlation between best n for past year and best n for next month

Observed Results

Year

5 10 15 20 Totals

5 85 30 11 32 158

Month 10 59 21 12 14 106

15 27 10 4 10 51

20 27 16 0 14 57

Totals 198 77 27 70 372

Interpretation

Using the Chi-Squared formula we obtain a test statistic of 11.838

Given 9 degrees of freedom this test statistic returns a p-value > alpha = .05 so we do not have enough evidence to reject the Null Hypothesis. Therefore, no correlation.

Where to go from here??

Suggestions? Look back

Example of Moving Average for small n. (n=6)

Introduction to Stops

Set a price x percent away from the buy/sell price and if at some future date the price exceeds this stop then sell/buy back

Regular Stops Trailing Stops Full Stops Partial Stops

Picking your stop

One problem has now become two Pick best n Pick best stops

Also, different method of solving Chi-squared cannot be used because

expected counts would be too low

Best Attempt Find best combination since (inception

minus a few years) and then test that combination on the years you left out

No worries of expected counts so use as many MAs and %s as you want

List of MAs: 3, 4, 5, 6, 7, 8, 9, 10, 12, 14, 16, 18, 20, 25, 30, 40, 50

List of %s (top and bottom): 0.0, 0.5, 1.0, 1.5, 2.0, 2.5, 3.0, 3.5, 4.0, 4.5, 5.0

Results of Long Side Trading

Best MA: 3 Bottom Percent: 0.5% Top Percent: 1.0% Percent Correct: 50.157% MA %APR from 1970-1998: 9.26% DJIA %APR from 1970-1998: 8.48%

Results of Short Side Trading Best MA: 3 Bottom Percent: 0.0% Top Percent: 0.0% Percent Correct: 56.326% MA %APR from 1970-1998: 4.95% DJIA %APR from 1970-1998: 8.48% Both Long and Short Side trading together

%APR from 1970-1998: 7.66%

Now use these parameters…

Long Side MA %APR from 1998-2003: 5.22%

Short Side MA %APR from 1998-2003: 6.82%

Long and Short Side MA %APR from 1998-2003: 6.03%

DJIA %APR from 1998-2003: 1.07%

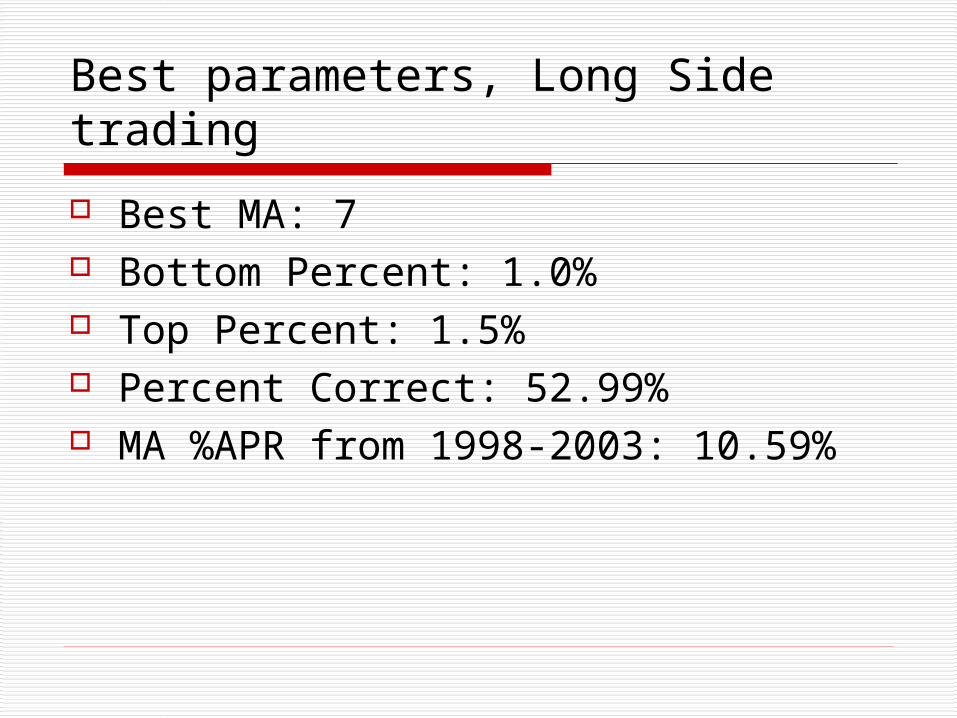

Best parameters, Long Side trading

Best MA: 7 Bottom Percent: 1.0% Top Percent: 1.5% Percent Correct: 52.99% MA %APR from 1998-2003: 10.59%

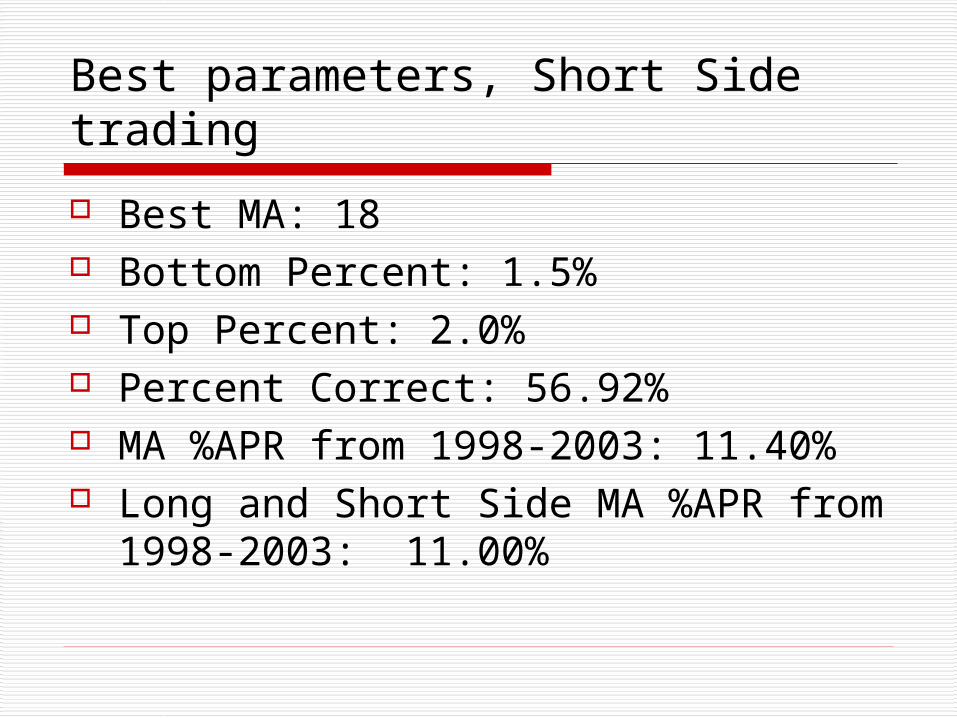

Best parameters, Short Side trading

Best MA: 18 Bottom Percent: 1.5% Top Percent: 2.0% Percent Correct: 56.92% MA %APR from 1998-2003: 11.40% Long and Short Side MA %APR from

1998-2003: 11.00%

Leveraging

Using indicators means you are picking and choosing when to be in or out of the market

Therefore, when you are in you have to make it account for all the times you’re out.

Options are one type of leveraging

Options

Option pricing is difficult because it is dependent upon six factors, only one of which is price

No source of test data Approximate the amount of

leveraging by buying/selling four times as much as your money allows.

The Option Effect

Long Side MA %APR from 1998-2003: 14.14%

Short Side MA %APR from 1998-2003: 24.57%

Long and Short Side MA %APR from 1998-2003: 19.81%

DJIA %APR from 1998-2003: 1.07%

Greedy Perhaps?

19.81% using the best of the past 28 years vs. 43.06% if you had used the best parameters of the current five years

How do we refine the system to capture more recent advances in other parameters?

First Attempt

Use the best parameters of last year for current year

Result: 20.06% vs. 19.81% Occurred by Chance?....maybe Also, the percent correct dropped

drastically from 50% to 20% … not good

Second Attempt

Use the best parameters from the past 3 years, 5 years, and 10 years

Results: 3 years: 13.05% 5 years: 7.90% 10 years: 12.74% Random … not random?

Summary of Results

Back Data: As much as possible: 19.81% 10 years: 12.74% 5 years: 7.90% 3 years: 13.05% 1 year: 20.06% 1 month: 0.49%

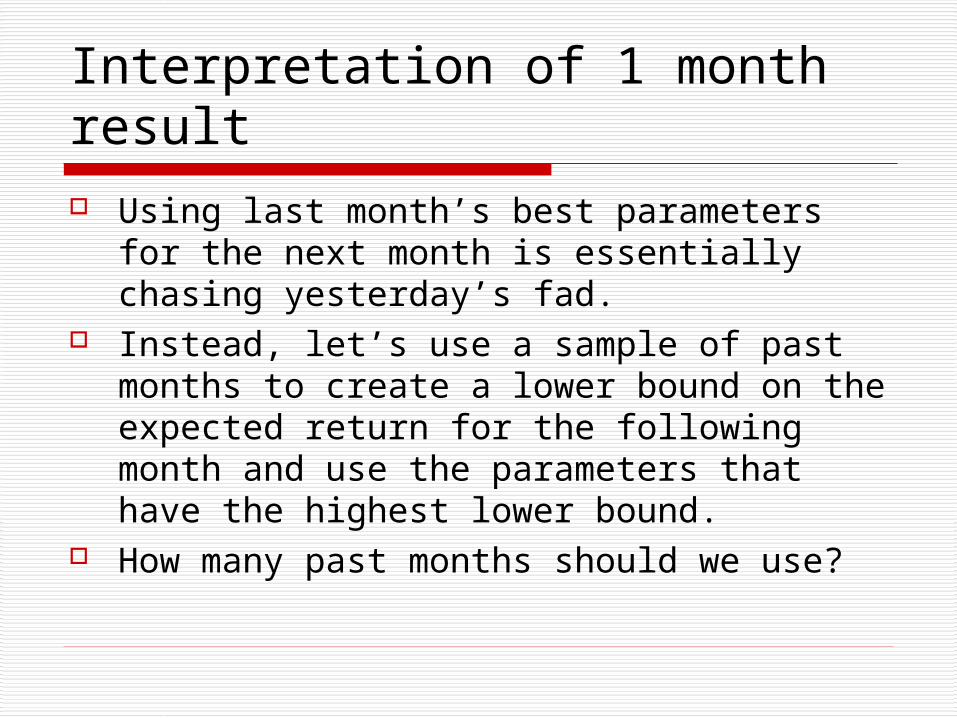

Interpretation of 1 month result Using last month’s best parameters for the

next month is essentially chasing yesterday’s fad.

Instead, let’s use a sample of past months to create a lower bound on the expected return for the following month and use the parameters that have the highest lower bound.

How many past months should we use?

Results Run test on previous five years to

determine best number of past months Best number of past months = 9 Use this number of past months in choosing

which parameters to use for the next month Result: 0.00% APR Not any better than 0.49%, however the

percent correct, 88.3% (shouldn’t this be around 99%?), was much higher than before

Conclusions Can we conclude anything? How well was the moving average able to

predict buy/sell points? By itself… Using stops

Where was chaotic behavior exhibited? Moving Average predictions? Market? System? All or none of the above?

Conclusions (cont.)

What amount of Back Data would you use? ... Why?

How much of the results are dependent not upon how much Back Data but the characteristics of that Back Data

How likely is a programming error?

Questions??