the performance of lodging properties in an investment portfolio

TRANSCRIPT

The Performance of Lodging Properties

in an I n v e s t m e n t Por t fo l io

Hotel-property investments have some surprising characteristics--notably, their divergence from the performance of other commercial real estate.

BY DANIEL C. QUAN, JIE LI, AND ANKUR SEHGAL

T h e last decade of the twentieth century has seen con- siderable restructuring in t, he lodging industry. Promi- nent among the industry s changes has been the ad-

vent of a number of new lodging companies, development of new concepts and segments, and the increased merger and acquisition activities, all of which have piqued the interest of investors.

While lodging-stock returns have stagnated over the past decade or so, individual lodging properties have appreciated in value, demonstrating the strong macroeconomic growth in the U.S. economy.

The purpose of this article is to examine the viability of lodging properties as an investment option for portfolio man- agers. We focus on four main investment characteristics: namely, lodging-property returns, return risk or volatility, the

© 2002, CORNELL UNIVERSITY

portfolio-diversification benefits of lodging properties, and lodging's performance relative to inflation. In particular, we compare the investment performance of lodging properties, segregated by geographical regions and market segments, with S&P 500 stocks, small-company stocks, the NCREIF real- estate index, long-term corporate bonds, long-term govern- ment bonds, and U.S. Treasury bills (commonly called T-bills). Although there have been numerous studies that have looked at such performance statistics for these broad asset classes, in- cluding commercial real estate, none has explicitly considered lodging properties as a separate category.

The relationship of lodging-property returns to inflation is of particular interest. While lodging properties have histori- cally been classified as income properties, the nature of their revenue source, which differs considerably from that of other commercial real estate, is a defining feature of this asset class. Cash-flow income from commercial properties such as office

DECEMBER 2002 Cornell Hotel and Restaurant Administration Quarterly 81

FINANCE [ LODGING-INVESTMENT RETURNS

buildings usually arises from tenants who are committed to fixed, long-term, multi-year leases. In contrast, hotels derive their revenues from room rates that can change and respond to infla- tionary pressures with relative frequency. This flexibility will likely result in lodging-property returns' being more responsive to inflationary pressures than those of commercial real estate and, therefore, providing a certain degree of in- flation protection for investors. Such flexibility also suggests that lodging properties may behave

In the aggregate, lodging investments offer the

benefits of diversification in a portfol io that also

contains traditional commercial real estate.

differently from commercial real estate in gen- eral. We find evidence to indicate that lodging properties do, in fact, perform differently from commercial properties, a result that challenges the conventional view that lodging properties perform similarly to other income-producing real estate.

We use the American Hotel and Lodging Association (AH&LA) and the Cornell Univer- sity School of Hotel Administration's Lodging Property Index (LPI) as the measure of lodging- property performance. The LPI is a quarterly index that comprises unleveraged properties. It represents about 2 percent of the population of investment-grade lodging properties in the United States. The Lodging Property Index is divided into sub indexes based on market seg- ment (upscale, midprice, and economy) and ge- ography (the east, midwest, south, and west parts of the United States). This affords us the oppor- tunity to investigate differences among different market segments and geographical regions. Be- cause the LPI index was started in 1995, our sample size is much smaller than that of other similar studies. It therefore is prudent to state at the onset that our results are suggestive and may not represent relationships over a full business cycle or over longer horizons.

We find that lodging properties as a whole exhibited strong performance over our sample period, from 1995 through 2000. While raw re-

turns were comparable with the other asset classes that we considered, lodging-return volatilities, a measure of market risk, were in general lower thus suggesting a high risk-adjusted return. The ag- gregate lodging returns were found to have di- versification benefits when included in a portfo- lio with smal l -company stocks and with commercial real estate. Furthermore, lodging properties appear to offer some protection against inflation risk.

The following section provides an overview of our methodology and a brief literature review. This is followed by our comparison of risk and return characteristics of lodging properties, com- mercial real estate, stocks, and bonds for the pe- riod 1995 through 2000. Finally, lodging- property performance by price segment and geo- graphic region is then analyzed with respect to its co-movement with the other asset classes.

Methodology Lodging real estate in the United States repre- sents well over $100 billion of unsecuritized investment-grade properties. The sheer size of this sector suggests that such properties should be in- cluded in a well-diversified portfolio. Portfolio- allocation rules can be broadly viewed as being dependent on the asset's performance, its riski- ness, its portfolio-diversification potential, and its performance during inflationary periods.

Because each performance measure differs, it's important to discuss their interpretations. A com- monly used measure of return performance for a single asset is its historical return. This measure in essence captures the change in the dollar value of a unit of funds invested over a particular hold- ing period. A holding-period return is calculated as the average of small-interval returns, such as quarterly or annual periods. The volatility of a return series over time is often interpreted as the asset's risk. Thus, a reasonable measure of risk is the standard deviation of the time series of pe- riod returns.

The correlation of the return series with other asset dasses and with the inflation rate represents the asset's portfolio-diversification potential, as well as its performance during inflationary periods. Two assets have strong portfolio-diversification benefits, for instance, if their returns are nega- tively correlated. The idea is that in a portfolio

82 Cornell Hotel and Restaurant Administration Quarterly DECEMBER 2002

LODGING-INVESTMENT RETURNS [ FINANCE

comprising negatively correlated assets, the poor performance of one can be offset by the strong performance of the other--thus resulting in a portfolio carrying lower risk than each of its com- ponents. In a similar manner, a positive correla- tion between an asset's performance and the in- flation rate suggests that the asset provides compensation to the investor in an inflationary environment--thus offering inflation protection.

Lodging Property Index. As we indicated above, our measure of lodging-property perfor- mance uses the American Hotel and Lodging Association (AH&LA) and the Cornell Univer- sity School of Hotel Administration's Lodging Property Index (LPI). The sample was compiled to avoid geographic and market-segment concen- trations and to include properties of varying sizes and property characteristics. As of the fourth quarter 1999, the LPI included 252 properties totaling $10.25 billion in value, with 45 located in the west, 43 in the midwest, 93 in the south, and 71 in the east. Market segments were deter- mined by ranking each property by their average daily rates, with the top one-third of the ranking defined as upscale (84 properties valued at $6.2 billion), the middle one-third as midprice (84 properties valued at $2.3 billion), and the lowest third as economy (84 properties valued at $0.84 billion).

By design, the LPI is constructed in a fashion similar to the National Council of Real Estate Investment Fiduciaries (NCREIF)'s Classic Apartment and R&D/Office index sample. The NCREIF index is an unleveraged index of U.S. commercial real-estate properties (apartment, industrial, office, and retail). For our research, we used the unweighted LPI because it eliminates the potential problem of inconsistent returns aris- ing from the presence of one or two large prop- erties in the sample.

The unweighted LPI suffers from certain limi- tations, however. For example, unlike the NCREIF index, which is constructed on the ba- sis of regular appraisals, the LPI is compiled by a committee of lodging-property-valuation experts who make necessary value estimates based on selected operating-performance measures and market data. Such valuations are estimates of unobserved market prices that may diverge from actual transaction prices. Therefore, any biases

in the estimates will likely contaminate our em- pirical results. ~ The second problem with the LPI is the imperfect marketability or illiquidity of lodging assets. Unlike stocks and bonds, which are highly liquid assets that can be converted into cash with relatively low transaction costs, lodg- ing properties cannot be sold instantaneously at the valuation experts' estimated prices.

A number of researchers have tried to solve the valuation problem created by real estate's illi- quidity. For the Lodging Property Index, Corgel, deRoos, and Davis attempted to find a solution by avoiding valuation altogether. 2 They turned to the stock market and used the value of REITs (Real Estate Investment Trusts) to create a pub- licly equivalent LPI index. To accomplish this, they decomposed REIT returns to arrive at the returns on hotels held by those REITs. Although the returns in the data set were dissimilar, the study presented an opportunity to overcome limitations in the Lodging Property Index. In our study, we use the unweighted LPI values without accounting for the above-mentioned limitations.

Literature Review For commercial real estate in general, a number of authors have shown that commercial real es- tate offered diversification benefits to institutional investors because of its low correlation with stocks. For example, Ibbotson and Siegel showed a correlation of-0.06 between S&P stocks and real estate for the years 1947 through 19822 Similarly, Hartzell estimated a correlation of -.25 using quarterly data from 1977 to 1986, 4 while Worzala and Vandell calculated the corre- lation to be-.097 using quarterly data from 1980

1 For a more thorough discussion of the effects of appraisal errors on return measurements, see: Daniel C. Quan and John Quigley, "Price Formation and the Appraisal Func- tion in Real Estate Markets," Journal of RealEstate Finance and Economics, Vol. 4, No. 2 (1991), pp. 127-146.

z Jan A. deRoos, Jack B. Corgel, and G.B. Davis, "Publicly Traded Equivalent of the Lodging Property Index," Real Estate Finance, Vol. 15, No. 3 (Fall 1998), pp. 57-64.

3 Roger G. Ibbotson and Lawrence B. Siegel, "Real Estate Returns: A Comparison with Other Investments," AREUEA Journal, Vol. 12 (1984), pp. 219-241.

4 David J. Hartzell, "Real Estate in the Portfolio," in The Institutional Investor: Focus on Investment Management, ed. EJ. Fabozzi (Cambridge, MA: Ballinger, 1986).

DECEMBER 2002 Cornell Hotel and Restaurant Administration Quarterly 83

FINANCE I LODGING-INVESTMENT RETURNS

:X H I B l i

Cumulative wealth indices of capital-market securities (1995-2000)

180'-

1 =

• 120' :I

> 100'

,-~ 8 0 '

6 0 + , ' ,

40' . ~ a ' ~ f ~ -

20' ~ ~'~ ~"x ~+' / \ ' ~ : : ~ I ; : = ~ i : ~

0 -- 1995 1996 1996 1997 1997 1998 1998 1999 1999 2000

4 2 4 2 4 2 4 2 4 2 Quarter

• S&P 500 stocks

• Lodging Property Index

i t& Small-company stocks

; X NCREIF real-estate index

~ i Long-term government bonds I * Long-term corporate bonds

U.S. Treasury bills Inflation

to 1991. 5 Using data from 17 countries, Quan and Titman found positive long-term correlations between stocks and commercial real-estate price changes. 6 Their reasoning was that both real es- tate and stocks were driven up or down by chang- ing economic conditions that can only be ob- served over long time horizons.

Similarly, numerous studies were conducted such as those done by Gyourko and Linneman to examine real estate's viability as an inflation hedge. 7 While the outcome is still not completely clear, it seems that real estate is not such a sig- nificant inflation hedge as it was believed to be.

5 E. Worzala and K. Vandell, "International Direct Real Estate Investments as Alternative Portfolio Assets for Insti- tutional Investors: An Evaluation," Paper presented at the 1993 AREUEA meetings, Anaheim, CA.

6 Daniel C. Quan and Sheridan Titman, "Do Real Estate Prices and Stock Prices Move Together? An International Analysis," RealEstateEconomics, Vol. 27 (1999), pp. 183- 207.

7 j. Gyourko and P. Linneman, "Owner-occupied Homes, Income-producing Properties, and REIT's as Inflation Hedges: Empirical Findings," Journal of Real Estate Finance and Economics, Vol. 1 (1988), pp. 347-372.

Little research has been done on portfolio al- location for lodging properties. Firstenberg, Ross, and Zisler showed that hotels have the highest returns and risks compared to other property types. 8 Since that time the lodging industry has seen a full cycle--experiencing a serious down- turn, consolidation, and recovery. DeRoos and Corgel showed that lodging assets have more vari- ability than other real-estate classes. 9 However, the appropriate allocation of lodging could not be evaluated before its correlations with other classes were properly measured.

Following Firstenberg, Ross, and Zisler, our initial assumption was that lodging properties would have both a higher return and a higher

s Paul M. Firstenberg, Steven A. Ross, and Russell C. Zisler, "Real Estate: The Whole Story," Journal of Portfolio Man- agement, Vol. 14, No. 3 (Spring 1988).

9 See: Jan A. deRoos and Jack B. Corgel, "Hotel Invest- ments in the Portfolio: Are They Part of the Core?," Real Estate Finance, Vol. 14, No. 2 (Summer 1997), pp. 29-37; and Jan A. deRoos and Jack B. Corgel, "The Lodging Prop- erty Index," Real Estate Review, Vol. 27, No. 2 (Summer 1997), pp. 35-38.

84 Cornell Hotel and Restaurant Administration Quarterly DECEMBER 2002

LODGING-INVESTMENT RETURNS I FIN.,~NCE

volatility than does commercial real estate, and would have low correlation with real-estate re- turns. This assumption is attributable to the lodg- ing sector's ability to lead the real-estate cycle because it does not have the same "inertia" as long-term real-estate leases. While hotel rates and occupancies drop quickly in periods of economic recession, they also react quickly to periods of boom--something not witnessed in commercial real estate.

Comparing Lodging-proper V Returns with Other Capital-market Assets Although we would have preferred a longer time horizon for our analysis, the period of 1995 to 2000 constitutes an intriguing time to analyze lodging returns against those of other asset classes. First, this period represents an upswing in the lodging cycle. Second, this period can be broken down into two macroeconomic cycles due to the Asian currency crisis and later the technology boom--thereby representing a suitable period to show lodging's ability to be a common-stock- diversification vehicle. Finally, the lodging indus- try has undergone fundamental changes during this period in terms of mergers and acquisitions (M&A) and REIT activities, all of which have major effects on returns.

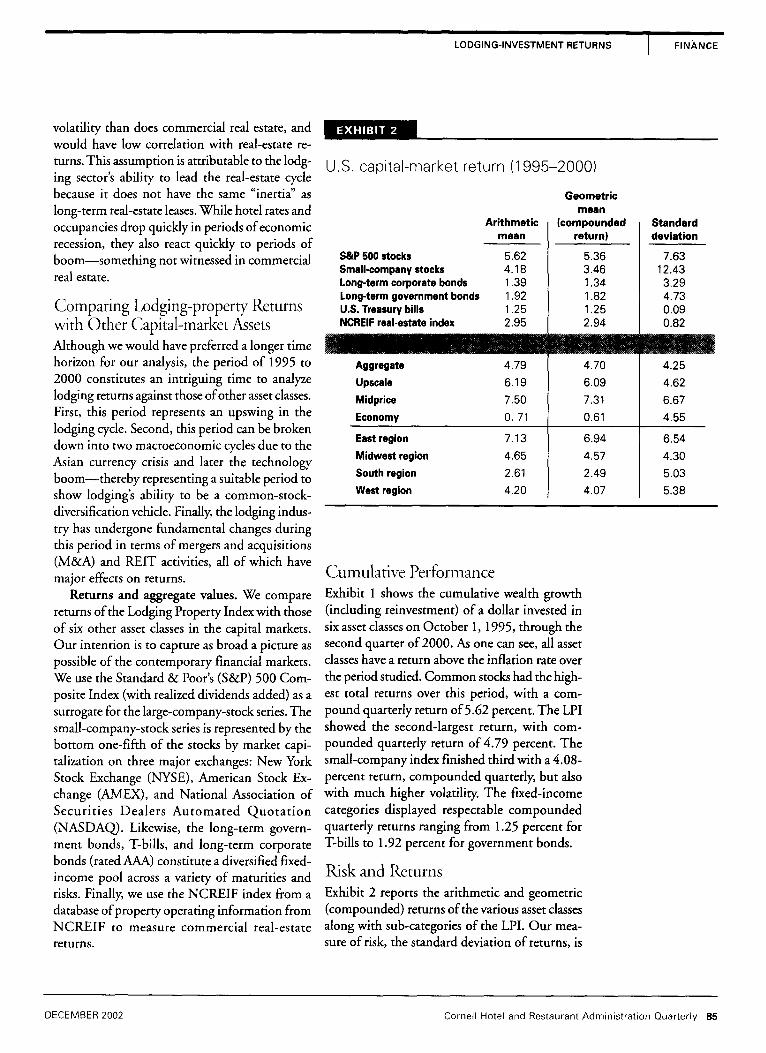

Returns and aggregate values. We compare returns of the Lodging Property Index with those of six other asset classes in the capital markets. Our intention is to capture as broad a picture as possible of the contemporary financial markets. We use the Standard & Poor's (S&P) 500 Com- posite Index (with realized dividends added) as a surrogate for the large-company-stock series. The small-company-stock series is represented by the bottom one-fifth of the stocks by market capi- talization on three major exchanges: New York Stock Exchange (NYSE), American Stock Ex- change (AMEX), and National Association of Securities Dealers Automated Quotat ion (NASDAOO. Likewise, the long-term govern- ment bonds, T-bills, and long-term corporate bonds (rated AAA) constitute a diversified fixed- income pool across a variety of maturities and risks. Finally, we use the NCREIF index from a database of property operating information from NCREIF to measure commercial real-estate returns.

iXHIBIT

U.S. capital-market return (t995-2000)

Arithmetic mean

S&P 500 stocks 5.62 Small-company stocks 4.18 Long-term corporate bonds 1.39 Long-term government bonds 1.92 U.S. Treasury bills 1.25 NCREIF real-estate index 2.95

Aggregate 4.79

Upscale 6.19 Midprice 7.50 Economy 0.71

East region 7,13

Midwest region 4.65

South region 2.61

West region 4.20

Geometric mean

(compounded return)

5.36 3.46 1.34 1.82 1.25 2.94

4.70

6.09

7.31

0.61

6.94

4.57

2.49

4.07

Standard deviation

7.63 12.43 3.29 4.73 0.09 0.82

4.25

4.62

6.67

4.55

6.54

4.30

5.03

5.38

Cumulative Performance Exhibit 1 shows the cumulative wealth growth (including reinvestment) of a dollar invested in six asset classes on October 1, 1995, through the second quarter of 2000. As one can see, all asset classes have a return above the inflation rate over the period studied. Common stocks had the high- est total returns over this period, with a com- pound quarterly return of 5.62 percent. The LPI showed the second-largest return, with com- pounded quarterly return of 4.79 percent. The small-company index finished third with a 4.08- percent return, compounded quarterly, but also with much higher volatility. The fixed-income categories displayed respectable compounded quarterly returns ranging from 1.25 percent for T-bills to 1.92 percent for government bonds.

Risk and Returns Exhibit 2 reports the arithmetic and geometric (compounded) returns of the various asset classes along with sub-categories of the LPI. Our mea- sure of risk, the standard deviation of returns, is

DECEMBER 2002 Cornell Hotel and Restaurant Administration Quarterly 85

FINANCE I LODGING-INVESTMENT RETURNS

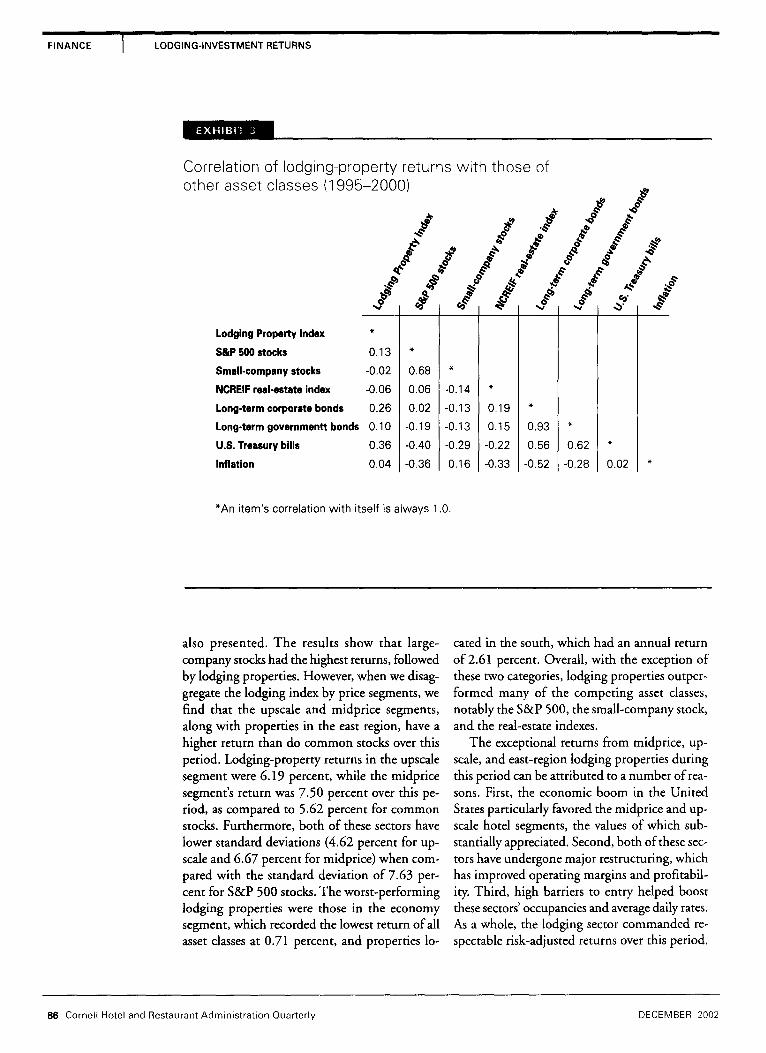

~ X H I B t [ :

Correlation of lodging-property returns with those of other asset classes (1995-2000)

/ ! /

0.13 *

-0.02 0.68

-0.06 0.06

0.26 0.02

0.10 -0.19

0.36 -0.40

0.04 -0.36

Lodging Property index

S&P 500 stocks

Small-company stocks

NCREIF real-estate index

Long-term corporate bonds

Long-term governmentt bonds

U.S. Treasury bills

Inflation

/ /

d

-0.14 *

-0.13 0.19

-0.13 0.15

-0.29 -0.22

0.16 -0.33

Y : oo* ;

#" ,o- _~

0.93

0.56

-0.52

0.62

-0.28 0.02

*An i tem's correlation wi th itself is always 1.0.

also presented. The results show that large- company stocks had the highest returns, followed by lodging properties. However, when we disag- gregate the lodging index by price segments, we find that the upscale and midprice segments, along with properties in the east region, have a higher return than do common stocks over this period. Lodging-property returns in the upscale segment were 6.19 percent, while the midprice segment's return was 7.50 percent over this pe- riod, as compared to 5.62 percent for common stocks. Furthermore, both of these sectors have lower standard deviations (4.62 percent for up- scale and 6.67 percent for midprice) when com- pared with the standard deviation of 7.63 per- cent for S&P 500 stocks. The worst-performing lodging properties were those in the economy segment, which recorded the lowest return of all asset classes at 0.71 percent, and properties lo-

cated in the south, which had an annual return of 2.61 percent. Overall, with the exception of these two categories, lodging properties outper- formed many of the competing asset classes, notably the S&P 500, the small-company stock, and the real-estate indexes.

The exceptional returns from midprice, up- scale, and east-region lodging properties during this period can be attributed to a number of rea- sons. First, the economic boom in the United States particularly favored the midprice and up- scale hotel segments, the values of which sub- stantially appreciated. Second, both of these sec- tors have undergone major restructuring, which has improved operating margins and profitabil- ity. Third, high barriers to entry helped boost these sectors' occupancies and average daily rates. As a whole, the lodging sector commanded re- spectable risk-adjusted returns over this period.

86 Cornell Hotel and Restaurant Administration Quarterly DECEMBER 2002

LODGING-INVESTMENT RETURNS I FINANCE

E X H I B I T

Correlation of lodging-property subindexes with other asset classes (1995-2000)

/ / fl/ , _o,* o,o ..,,,

o.,o oo .f

Lodging Property Index Upscale Midprice Economy

East region Midwest region South region West region

.x-

0.81 * 0.90 0.66 * 0.67 0.29 0.39 *

0.81 0.52 I0.75 0.64 * 0.64 0 .28 !0 .59 0.64 0.52 0.69 0.76 !0.58 0.31 0.16 0.88 0 .89 !0 .74 0.46 0.58

S~P 500 stocks 0.13 Small-company stocks -0.02 NCREIF real-estate index -0.06 Long-term corporate bonds 0.26 Long-term gov't, bonds O. 10 U.S. Treasury bills 0.36 Inflation 0.04

0.30 * 0.37 0.74

*An item's correlation with itself is always 1.0.

Lodging Properties in Diversified Portfolios Owning lodging properties offers limited diver- sification potential in a portfolio comprising stocks, long-term government bonds or corpo- rate bonds, and T-bills, as indicated by the cor- relations displayed in Exhibit 3) 0 Given the posi- tive correlation of lodging properties with the aforementioned assets, a portfolio made up of those assets will not be strongly diversified.

On the other hand, lodging properties are negatively correlated with commercial real estate. This relationship suggests that lodging proper-

10 In recognition of our small sample size, we also calcu- lated the Spearman's rho, a nonparametric correlation mea- sure that is not sensitive to sample size. The qualitative re- lationships were similar to our parametric results. The decision to use our correlations was to facilitate the com- parison of similar relationships in prior studies.

ties have investment characteristics that are dis- tinct from other commercial real estate. This is contrary to the widely accepted view that lodg- ing properties are identical to other commercial income properties. This difference is made more evident when one notes that while lodging prop- erties are positively correlated with U.S. Treasury bills (0.36), the NACREIF real-estate index is negatively correlated with T-bills (-0.29).

With respect to inflation protection, lodging properties (0.04), small-company stocks (0.16), and U.S. Treasury bills (0.02) appear to be the only assets that perform well in an inflationary environment. These three assets therefore may offer some degree of protection from inflation risk. This finding supports the notion that hotel properties do have the ability to pass along in- creases in operating costs by increasing room rates in an inflationary environment. It also seems clear

DECEMBER 2002 Cornell Hotel and Restaurant Administration Quarterly 87

FINANCE I LODGING-INVESTMENT RETURNS

from this finding that rents in commercial real estate do not move with inflation, owing to the fact that tenants sign long-term leases. This dis- tinction may be one plausible explanation for the negative correlation between NCREIF and the inflation rate (-0.33) while lodging properties are positively correlated with inflation (0.16).

Lodging Sub-indexes In this section, we investigate the LPI's price seg- ment and geographic sub-indexes. Sub-index correlations are presented in Exhibit 4 (on the previous page). Within price segments, we note that upscale and midprice hotels had the highest correlation with each other (0.66), followed by

As an investment, lodging commands respect-

able returns with relatively low volatility in

comparison with stocks and bonds.

the midprice and economy group (0.39), and fi- nally by the upscale and the economy segments (0.29). That the economy sector performs in a markedly different fashion from the other two segments seems reasonable given the difference in the various segments' market focus. On a re- gional basis, we also note that with the excep- tion of lodging properties located in the south and the east, which recorded the lowest regional correlation (0.16), lodging-property perfor- mances in the four regions are relatively corre- lated with each other. The strongest relationship was for properties in the western and the south- ern regions, with a correlation of 0.74.

The sub-indexes display remarkable diversifi- cation alternatives for other asset classes and present a new dimension for portfolio managers as they make their asset-allocation decisions. For example, all sub-indexes, with the possible ex- ception of the midprice segment and hotels lo- cated in the midwest, have low correlations with S&P common stocks. Also of interest is the uni- formly low and frequently negative correlation of these sub-indexes with small-company stocks. Taken together, lodging properties would per- form well in a well-diversified stock portfolio.

O f all asset classes considered, long-term cor- porate bonds appear to behave in the most simi- lar fashion to the various lodging segments over the different regions. With the exception of prop- erties in the southern region, the correlations were some of the highest, ranging from 0.36 for midwest properties to 0.20 for the upscale and midprice category. A similar, but lesser relation- ship exists between the sub-indexes and long-term government bonds. With regard to the sub- indexes, the government-bond correlations were uniformly smaller than those for corporate bonds, and both sets of correlations appear to move in tandem across the various sub-indexes. The pat- tern of correlations for T-bills is diverse from one sub-index to another and does not appear to fol- low a pattern. All correlations with the U.S. Trea- sury bills were positive and ranged in value from a low of 0. I i for the economy price segment to a high of 0.54 for upscale properties. Thus, taken together, investing in lodging properties in the three price segments and the four regions does not appear to provide significant diversification benefits in a portfolio that is strong in bonds or fixed-income investments.

Somewhat interesting is the relationship be- tween our sub-indexes and the NCREIF com- mercial real-estate index. Between price segments, the correlation with the NCREIF index ranges considerably, from -0.30 for upscale properties to 0.07 for midprice and 0.03 for economy prop- erties. The large negative value for upscale prop- erties indicates that the clientele for upscale prop- erties is less price sensitive than patrons in other segments, and thus upscale guests are more will- ing to pay consistently high prices. As a conse- quence, the high negative correlation with real estate can be explained by the greater degree of flexibility in increasing rates that hotels enjoy during periods of strong demand. This flexibil- ity is attributed to a high number of price- insensitive customers at upscale properties who are willing to pay high rates to attain high levels of service and amenities. This scenario stands in contrast to commercial real estate, which is of- ten encumbered by long-term leases that result in stable revenues. On a regional basis, the midwest had the highest correlation with com- mercial real estate at 0.30, but is negatively cor- related at -0.10 with the other regions.

88 Cornell Hotel and Restaurant Administration Quarterly DECEMBER 2002

LODGING-INVESTMENT RETURNS FINANCE

By price segment, and to a lesser extent by region, lodging-property investments appear to perform well in inflationary environments. Within price segments, the correlation with the inflation rate is consistent with previous results. That is, upscale properties had the highest corre- lation at 0.16 with inflation, followed by midprice at 0.02 and economy at -0.08. Once again, this reaffirms the notion that upscale ho- tel guests are not price sensitive while economy clients are extremely price sensitive--making it difficult for economy properties to pass cost in- creases on to their guests in an inflationary envi- ronment. The regional inflation correlations are more mixed, with the east reporting a correla- tion o f -0 .16 and the midwest a correlation of -0.33. In sharp contrast, the correlation for the south was relatively large and positive, at 0.36, and the west was not far behind, at 0.19. While inflation shows considerable regional effects, however, taken together, lodging properties over- all provide relatively good inflation protection.

Respectable Returns Our results reveal an interesting picture of lodging-property returns from 1995 through

2000. First, they show the sector's ability to com- mand respectable returns with relatively low vola- tility in comparison to both stock and bond markets. Additionally, certain sub-categories of lodging properties provide even higher returns than does the overall sector, with lower volatili- ties. Second, the low correlation of the lodging sector with common stocks generally and with small-company stocks particularly indicates that investing in lodging properties would provide strong portfolio-diversification benefits. An in- triguing finding is that both in the aggregate and in disaggregated results, lodging properties ap- pear to perform quite differently from the way other income-producing real estate performs. This result challenges the conventional notion that lodging properties perform similar to other commercial properties. Finally, lodging proper- ties appear to be one of the few asset classes that perform well in an inflationary environment. However, there is considerable regional and seg- ment variability with regard to inflation. Thus, the investor hoping to use lodging investments as an inflation hedge would have to determine the appropriate region or segment that offers the highest level of protection. •

Daniel C. Quan, Ph.D., is an associate professor of financial management at the Cornell University School of Hotel Administration ([email protected]). • l ie Li, B.S., is with Shangri-la Hotel and Resorts ([email protected]). Ankur Sehgal, B.S., is with Voyager Capital ([email protected]).

© 2002, Cornell University

DECEMBER 2002 Cornell Hotel and Restaurant Administration Quarterly 89