the performance data contained in this presentation represents past performance, which does not...

TRANSCRIPT

The performance data contained in this presentation represents past performance, which does not guarantee future results.Performance, especially for short time periods, should not be the sole factor in making your investment decisions.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE. NOT INSURED BY ANY GOVERNMENT AGENCY.

Patrick L. McFawn CFP®, CPA & Dale L. White CFP®, CPA

Lessons Learned

5 investing principlesfor today and beyond

22

Agenda

1. Every investment has risks, even cash

2. Diversification is not dead, it’s just misunderstood

3. Not all bonds—or bond funds —are created equal

4. Yes, it’s STILL stocks for the long run

5. Investing abroad shouldn’t be a foreign experience

33

1Principle

Every investmenthas risks ― even

cash

4

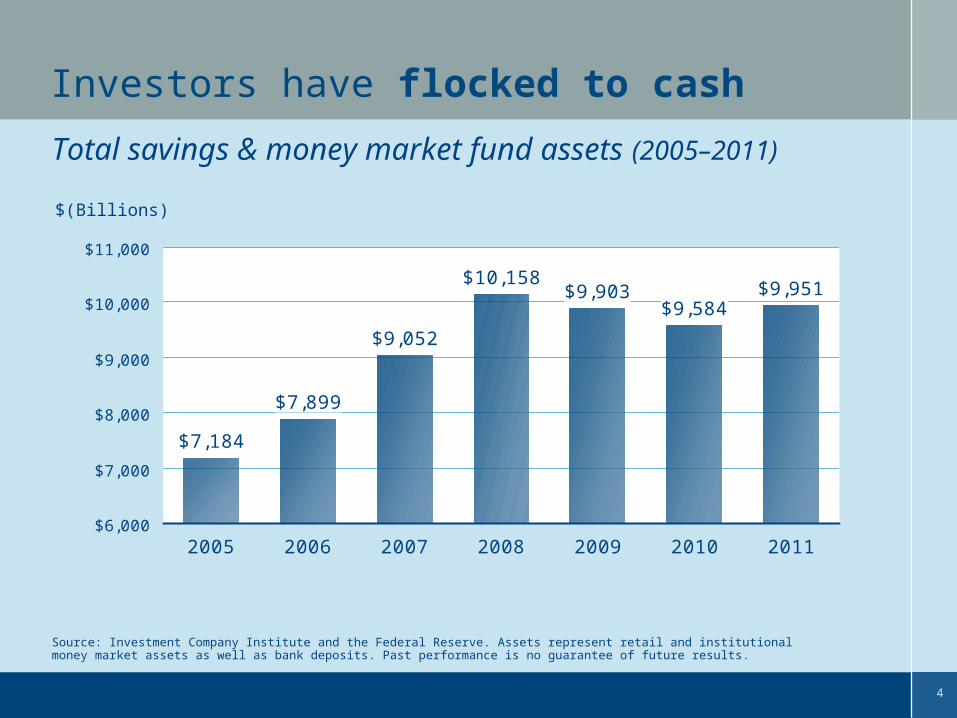

Investors have flocked to cash

Total savings & money market fund assets (2005–2011)

$7,184

$7,899

$9,052

$10,158$9,903

$9,584$9,951

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

2005 2006 2007 2008 2009 2010 2011

Source: Investment Company Institute and the Federal Reserve. Assets represent retail and institutional money market assets as well as bank deposits. Past performance is no guarantee of future results.

$(Billions)

5

0

10

20

30

40

50

60

Jan’05

May’05

Sep’05

Jan’06

May’06

Sep’06

Jan’07

May’07

Sep’07

Jan’08

May’08

Sep’08

Jan’09

May’09

Sep’09

Jan’10

May’10

Sep’10

Jan’11

May’11

Sep’11

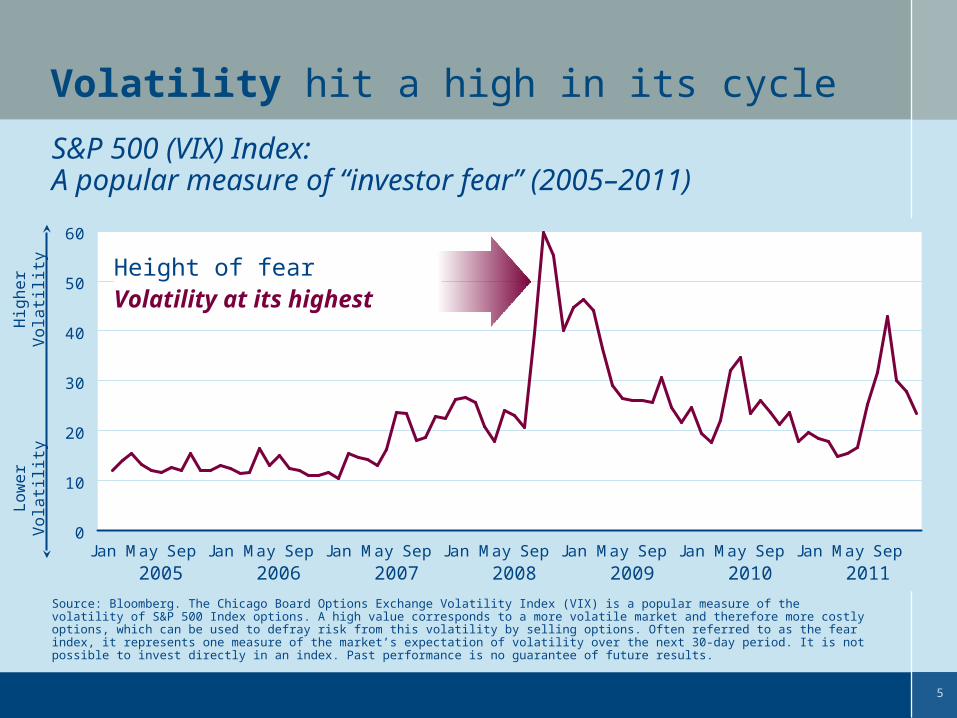

Volatility hit a high in its cycle

S&P 500 (VIX) Index: A popular measure of “investor fear” (2005–2011)

Source: Bloomberg. The Chicago Board Options Exchange Volatility Index (VIX) is a popular measure of the volatility of S&P 500 Index options. A high value corresponds to a more volatile market and therefore more costly options, which can be used to defray risk from this volatility by selling options. Often referred to as the fear index, it represents one measure of the market’s expectation of volatility over the next 30-day period. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Height of fearVolatility at its highest

Hig

her

Vola

tilit

yLo

wer

Vola

tilit

y

2005 2006 2007 2008 2009 2010 2011

6

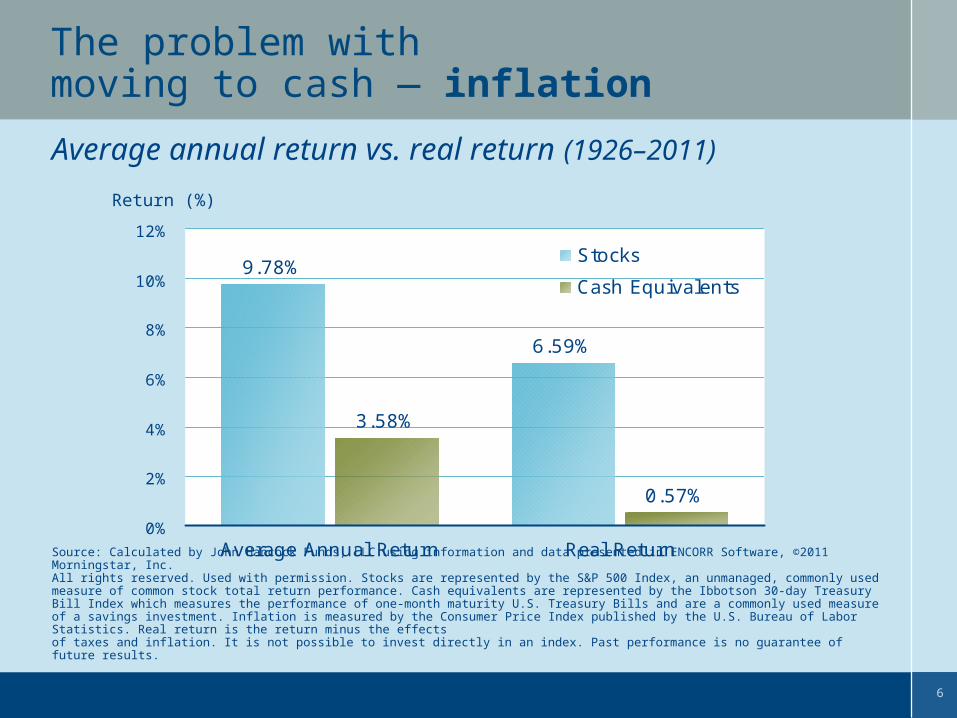

The problem with moving to cash — inflation

Source: Calculated by John Hancock Funds, LLC using information and data presented in ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. Stocks are represented by the S&P 500 Index, an unmanaged, commonly used measure of common stock total return performance. Cash equivalents are represented by the Ibbotson 30-day Treasury Bill Index which measures the performance of one-month maturity U.S. Treasury Bills and are a commonly used measure of a savings investment. Inflation is measured by the Consumer Price Index published by the U.S. Bureau of Labor Statistics. Real return is the return minus the effects of taxes and inflation. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Average annual return vs. real return (1926–2011)

Return (%)

9.78%

6.59%

3.58%

0.57%

0%

2%

4%

6%

8%

10%

12%

Average Annual Return Real Return

Stocks

Cash Equivalents

7

Source: Calculated by John Hancock Funds, LLC using information and data presented in ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. Cash equivalents are represented by the Ibbotson 30-day Treasury Bill Index which measures the performance of one-month maturity U.S. Treasury Bills and are a commonly used measure of a savings investment. Inflation is measured by the Consumer Price Index published by the U.S. Bureau of Labor Statistics. Real return is the return minus the effects of taxes and inflation. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

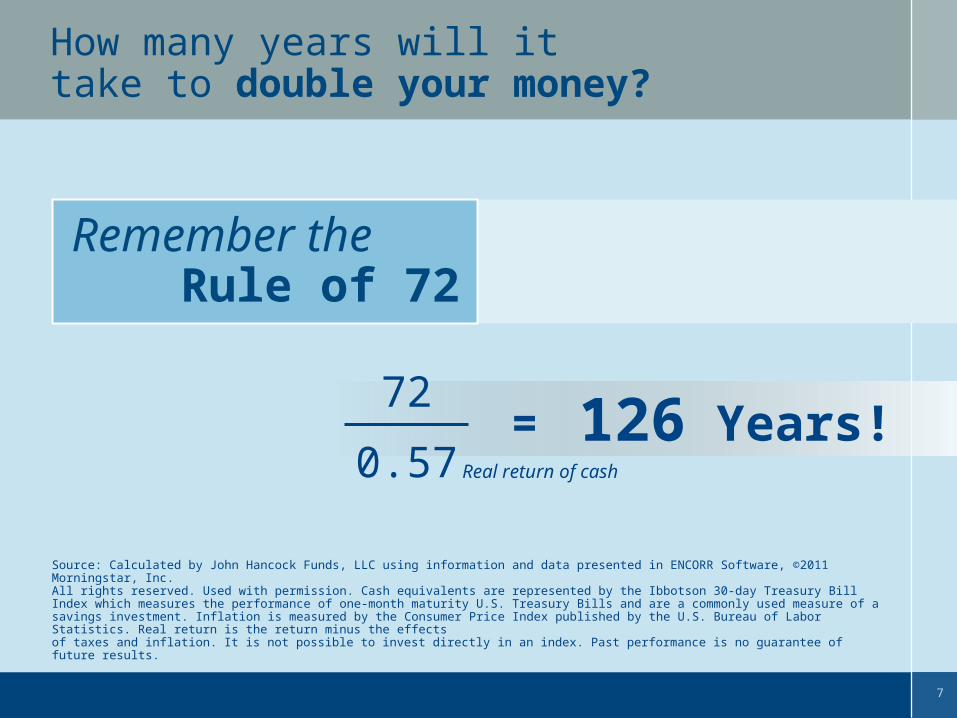

Remember the Rule of 72

How many years will it take to double your money?

126 Years!=0.57

72

Real return of cash

8

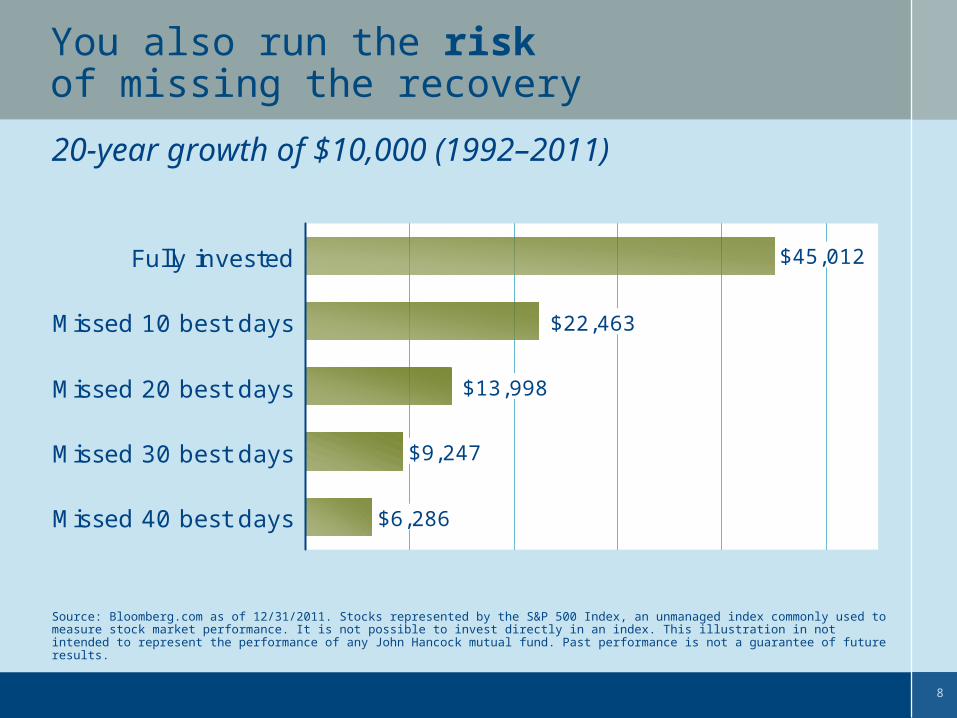

20-year growth of $10,000 (1992–2011)

You also run the risk of missing the recovery

Source: Bloomberg.com as of 12/31/2011. Stocks represented by the S&P 500 Index, an unmanaged index commonly used to measure stock market performance. It is not possible to invest directly in an index. This illustration in not intended to represent the performance of any John Hancock mutual fund. Past performance is not a guarantee of future results.

$9,247

$6,286

$45,012

$22,463

$13,998

Fully invested

Missed 10 best days

Missed 20 best days

Missed 30 best days

Missed 40 best days

9

What should investors remember?

When volatility is high, it’s hard to resist the temptation to get out of the markets.

Although cash and short-term investments seem safer, they may not keep pace with inflation in the long term.

Unless you can time it perfectly, you may also miss the gains when the market recovers.

The key is to be prepared for the “certainty of uncertainty!”

Every investment has risks, even cash

Although a money market fund may seeks to preserve the value of your investment at a $1.00 per share, it is possible to lose money by investing in the fund. The value of a company’s equity securities is subject to change in the company’s financial condition, and overall market and economic conditions.

1010

2Principle

Diversification is not dead,it’s just

misunderstood

11

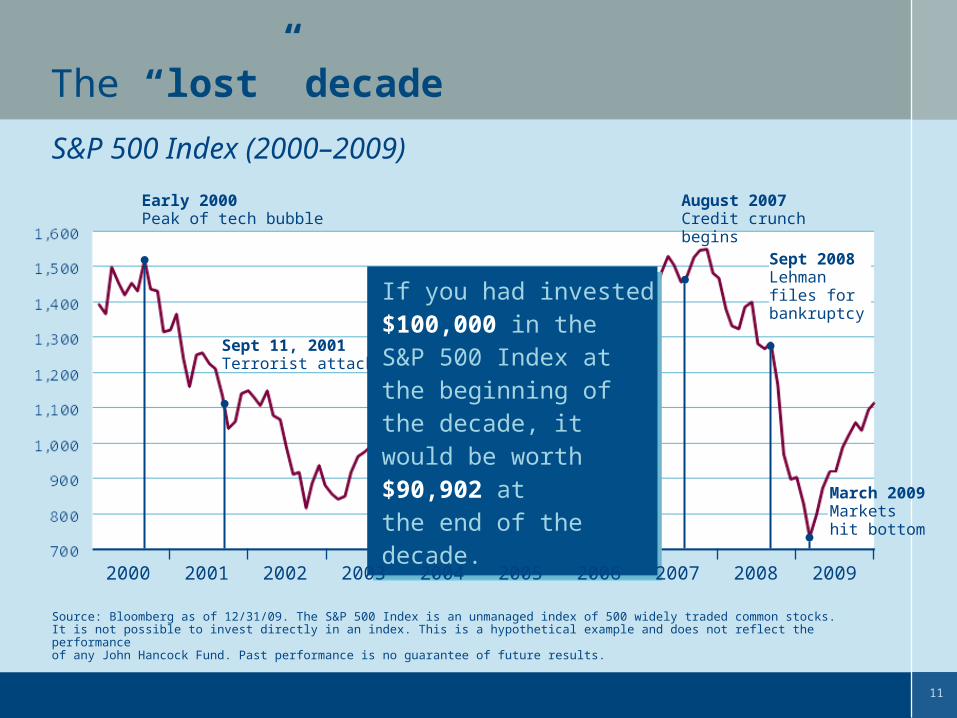

The “lost” decade

Source: Bloomberg as of 12/31/09. The S&P 500 Index is an unmanaged index of 500 widely traded common stocks. It is not possible to invest directly in an index. This is a hypothetical example and does not reflect the performance of any John Hancock Fund. Past performance is no guarantee of future results.

Sept 11, 2001Terrorist attack

Early 2000Peak of tech bubble

August 2007Credit crunch begins

Sept 2008Lehmanfiles forbankruptcy

If you had invested $100,000 in the S&P 500 Index at the beginning of the decade, it would be worth $90,902 at the end of the decade.

If you had invested $100,000 in the S&P 500 Index at the beginning of the decade, it would be worth $90,902 at the end of the decade.

S&P 500 Index (2000–2009)

March 2009Markets hit bottom

2001 2002 2003 2004 2005 2006 2007 2008 20092000

12

73.8

49.2

37.0

48.5

31.3

41.8

46.7

10.9

13.1

-17.5

31.8

26.5

Emerging Markets

International Small

Global Real Estate

Natural Resources

U.S. Real Estate

Loans

High Yield

TIPS

Global Bonds

Long-Term Govt.

Intl (MSCI EAFE)

Lg Cap (S&P 500)Large Cap (S&P 500)

Emerging Markets

International Small

Global Real Estate

Natural Resources

International (MSCI EAFE)

U.S. Real Estate

Loans

High Yield

TIPS

Global Bonds

Long-Term Government

-54.4

-49.0

-46.6

-48.8

-39.6

-29.7

-26.4

-4.1

-1.6

27.7

-43.4

-37.0

Emerging Markets

International Small

Global Real Estate

Natural Resources

U.S. Real Estate

Loans

High Yield

TIPS

Global Bonds

Long-Term Govt.

Intl (MSCI EAFE)

Lg Cap (S&P 500)

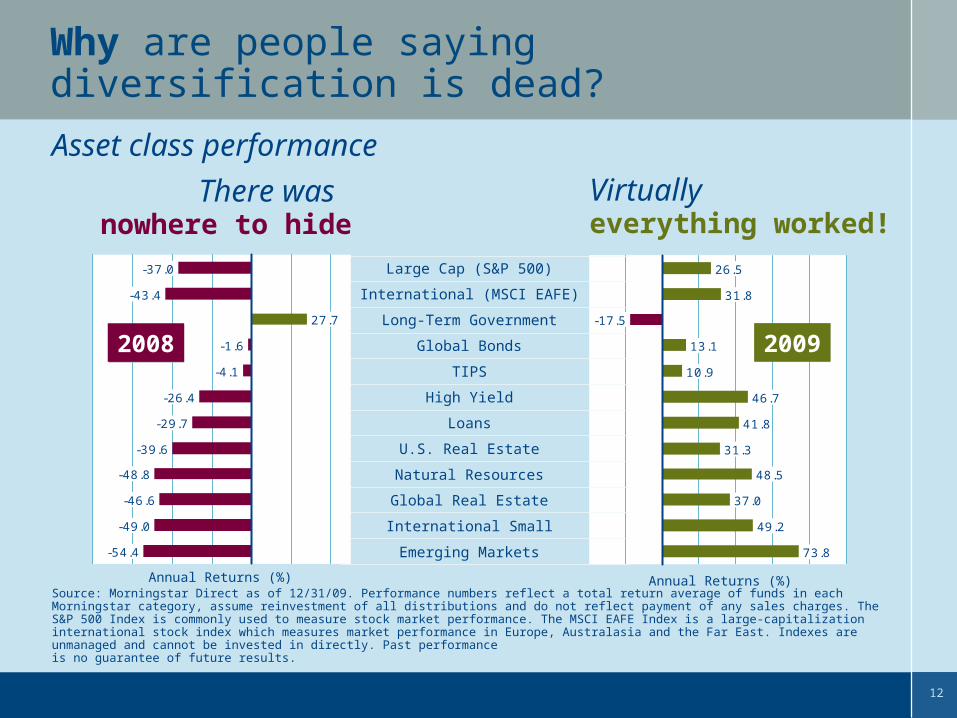

Why are people saying diversification is dead?

Source: Morningstar Direct as of 12/31/09. Performance numbers reflect a total return average of funds in each Morningstar category, assume reinvestment of all distributions and do not reflect payment of any sales charges. The S&P 500 Index is commonly used to measure stock market performance. The MSCI EAFE Index is a large-capitalization international stock index which measures market performance in Europe, Australasia and the Far East. Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Asset class performance

Virtually everything worked!

There was nowhere to hide

2009200920082008

Annual Returns (%) Annual Returns (%)

13

However, even over the lost decade, diversification worked

Average annual returns by category (2000–2009)

-1.0

1.2

6.1 6.2 6.6

4.73.5

10.512.2

10.6

3.6

8.7

- 5

0

5

10

15

Larg

e C

ap

(S&

P 5

00)

Inte

rnational

(MS

CI

EA

FE)

Long-T

erm

Govern

ment

Glo

bal

Bonds

TIP

S

Hig

h Y

ield

Loans

U.S

. R

eal

Est

ate

Natu

ral

Reso

uce

s

Glo

bal R

eal

Est

ate

Inte

rnational

Sm

all

Em

erg

ing

Mark

ets

Annual Returns (%)

Source: Morningstar Direct as of 12/31/09. Performance numbers reflect a total return average of funds in each Morningstar category, assume reinvestment of all distributions and do not reflect payment of any sales charges. The S&P 500 Index is commonly used to measure stock market performance. The MSCI EAFE Index is a large-capitalization international stock index which measures market performance in Europe, Australasia and the Far East. Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

14

Understand investment cycles ― a tale of three fundsWhich of these funds would you invest in?

Source: Morningstar Direct and John Hancock Funds. Large-Cap Growth Fund 1 (John Hancock Large Cap Equity Fund) was ranked 1564 of 1683, 1297 of 1478, 164 of 1279 and 312 of 804 against large growth funds for the 1-, 3-, 5- and 10-year time periods respectively. Large-Cap Growth Fund 2 (John Hancock Rainier Growth Fund) was ranked 77 of 1683, 178 of 1478, 255 of 1279 and 319 of 804 against large growth funds for the 1-, 3-, 5- and 10-year time periods respectively. Large-Cap Growth Fund 3 (John Hancock U.S. Global Leaders Growth Fund) was ranked 1164 of 1683, 1016 of 1478, 830 of 1279 and 310 of 804 against large growth funds for the 1-, 3- 5- and 10-year time periods respectively. Performance is for Class A shares as of 12/31/2011. Rankings are based on total return and do not include sales charges.John Hancock Large Cap Equity Fund’s total annual operating expense ratio as of the current prospectus is 1.22%. John Hancock Rainier Fund’s net annual operating expense ratio as of the current prospectus is 1.35%. The gross annual operating expense ratio of 1.39% is reduced due to a contractual expense reimbursement, which is in effect until at least 7/31/11 and may be terminated by the Adviser any time after this date. John Hancock U.S. Global Leaders Growth Fund’s net annual operating expense ratio as of the current prospectus is 1.30%. The gross annual operating expense ratio of 1.73% is reduced due to a contractual expense reimbursement, which is in effect until at least 2/28/11 and may be terminated by the Adviser any time after this date. Expenses for other share classes will vary, which will affect returns. Performance figures assume that all distributions are reinvested. For performance data current to the most recent month end, contact your financial professional or call John Hancock Funds at 1-800-225-5291. The performance data contained within this material represents past performance, which does not guarantee future results. The return and principal value of an investment will fluctuate, so that shares, when redeemed, may be worth more or less than the original cost. The Fund’s current performance may be higher or lower and is subject to substantial changes. *On 4/28/08 John Hancock Rainier Growth Fund acquired all of the assets of the Rainier Large Cap Growth Equity portfolio, the Fund’s predecessor, pursuant to reorganization. Performance prior to 4/28/08 reflects the performance of the Fund’s predecessor and does not include sales charges.

Morningstar Peer Group Rankings and Average Annual Returns, as of 12/31/11Morningstar Peer Group Rankings and Average Annual Returns, as of 12/31/11

Fund Name 1-Year 3-Year 5-Year 10-Year

Large-Cap Growth Fund 1 % Rank 92 87 13 39(Average Annual Return with 5% sales charge) 8.50% -2.85% 8.07% 2.83%

Large-Cap Growth Fund 2* % Rank 69 69 65 39(Average Annual Return with 5% sales charge) 10.78% -6.46% 1.13% -0.49%

Large-Cap Growth Fund 3 % Rank 5 12 10 40(Average Annual Return with 5% sales charge) 6.56% 0.10% 1.07% 1.05%

Top Quartile 2nd Quartile 3rd Quartile 4th Quartile

15

Same category, very different performance

Full market cycle coverage (2002–2011)

Fund 1

Fund 2

20112005200420032002 2009200820072006 2010

Fund 3

Large Growth CategoryLarge Growth Category

Source: Morningstar Direct and Bloomberg. Rankings for each Fund within Morningstar Large Growth category are based on total return and do not include sales charges. Past performance is no guarantee of future results.

Large Growth CategoryLarge Growth Category

Top Quartile 2nd Quartile 3rd Quartile 4th Quartile

% Rank99

Total Ret (37.84%)

% Rank81

Total Ret23.29%

% Rank96

Total Ret 4.14%

% Rank59

Total Ret 14.20%

% Rank54

Total Ret 33.73%

% Rank91

Total Ret 3.67%

% Rank44

Total Ret 8.51%

% Rank86

Total Ret2.16%

% Rank90

Total Ret1.44%

% Rank78

Total Ret 12.16%

% Rank40

Total Ret (26.16%)

% Rank49

Total Ret7.24%

% Rank77

Total Ret (43.89%)

% Rank66

Total Ret 31.68%

% Rank38

Total Ret 16.59%

% Rank69

Total Ret -4.45%

% Rank92

Total Ret -9.03%

% Rank2

Total Ret 33.77%

% Rank1

Total Ret16.26%

% Rank3

Total Ret20.22%

% Rank19

Total Ret (36.82%)

% Rank16

Total Ret33.88%

% Rank18

Total Ret 11.60%

% Rank16

Total Ret11.61%

% Rank3

Total Ret (14.51%)

% Rank14

Total Ret 44.32%

% Rank94

Total Ret19.24%

% Rank5

Total Ret 3.85%

% Rank17

Total Ret 20.57%

% Rank10

Total Ret (34.77%)

16

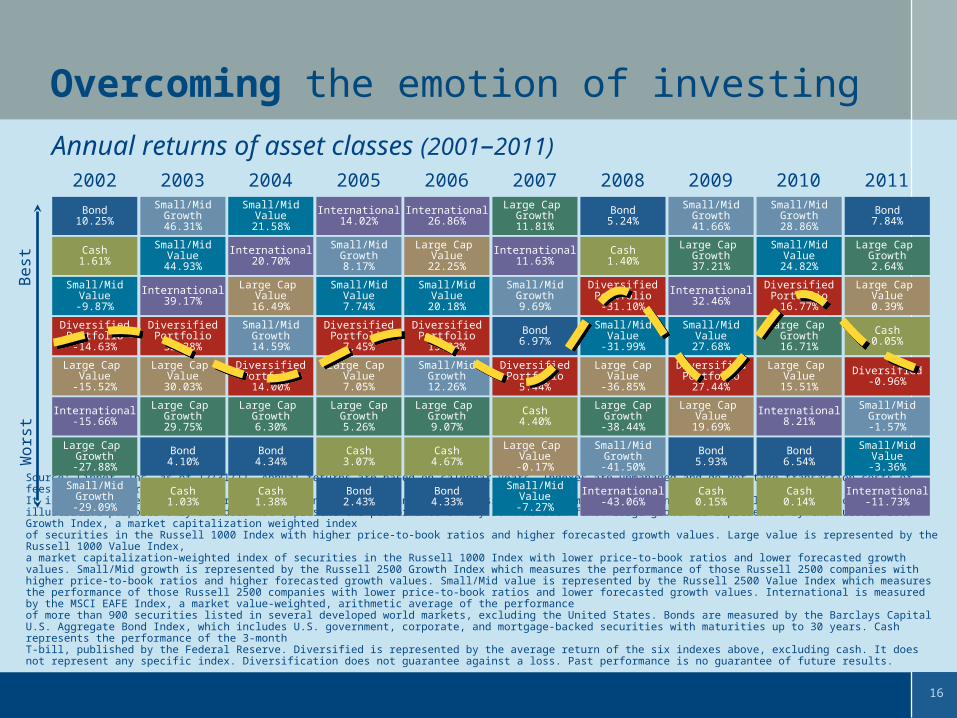

Source: Lipper, Inc. as of 12/31/11. Annual returns are based on calendar years. Indexes are unmanaged and do not take transaction costs or fees into consideration. It is not possible to invest directly in an index. Performance figures assume reinvestment of dividends and capital gains. This chart is for illustrative purposes only and does not represent the performance of any John Hancock fund. Large growth is represented by the Russell 1000 Growth Index, a market capitalization weighted index of securities in the Russell 1000 Index with higher price-to-book ratios and higher forecasted growth values. Large value is represented by the Russell 1000 Value Index, a market capitalization-weighted index of securities in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth values. Small/Mid growth is represented by the Russell 2500 Growth Index which measures the performance of those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. Small/Mid value is represented by the Russell 2500 Value Index which measures the performance of those Russell 2500 companies with lower price-to-book ratios and lower forecasted growth values. International is measured by the MSCI EAFE Index, a market value-weighted, arithmetic average of the performance of more than 900 securities listed in several developed world markets, excluding the United States. Bonds are measured by the Barclays Capital U.S. Aggregate Bond Index, which includes U.S. government, corporate, and mortgage-backed securities with maturities up to 30 years. Cash represents the performance of the 3-month T-bill, published by the Federal Reserve. Diversified is represented by the average return of the six indexes above, excluding cash. It does not represent any specific index. Diversification does not guarantee against a loss. Past performance is no guarantee of future results.

Overcoming the emotion of investing

Annual returns of asset classes (2001–2011)

Small/MidValue

-3.36%

Cash0.05%

Large Cap Value0.39%

Small/MidGrowth-1.57%

Large Cap Growth2.64%

International-11.73%

Bond7.84%

Bond6.97%

Large Cap Growth11.81%

Small/MidGrowth12.26%

Large Cap Value

19.69%

Large Cap Value

-15.52%

Large Cap Value

30.03%

Large Cap Value7.05%

Small/MidGrowth41.66%

Small/MidValue

24.82%

Bond10.25%

Small/MidGrowth46.31%

Small/MidValue

21.58%

International14.02%

International26.86%

International32.46%

Large Cap Value

15.51%

Small/MidValue

-9.87%

International39.17%

Large Cap Value

16.49%

Small/MidValue7.74%

Small/MidValue

20.18%

Cash0.14%

Small/MidGrowth14.59%

Cash0.15%

International8.21%

International-15.66%

Large Cap Growth29.75%

Large Cap Growth6.30%

Large CapGrowth5.26%

Large Cap Growth9.07%

Small/MidValue

27.68%

Small/MidGrowth28.86%

Large Cap Growth-27.88%

Bond4.10%

Bond4.34%

Cash3.07%

Cash4.67%

Bond5.93%

Large Cap Growth16.71%

Small/MidGrowth-29.09%

Cash1.03%

Cash1.38%

Bond2.43%

Bond4.33%

Large Cap Growth37.21%

Bond6.54%

Cash1.61%

Small/MidValue

44.93%

International20.70%

Small/MidGrowth8.17%

Large Cap Value

22.25%

Small/MidGrowth9.69%

Large Cap Value

-0.17%

Cash4.40%

International11.63%

Small/MidValue

-7.27%

Large CapValue

-36.85%

Bond5.24%

Small/MidValue

-31.99%

Large CapGrowth-38.44%

Small/MidGrowth-41.50%

International-43.06%

Cash1.40%

Best

Wors

t

Diversified-0.96%

DiversifiedPortfolio16.77%

DiversifiedPortfolio14.00%

DiversifiedPortfolio27.44%

DiversifiedPortfolio-14.63%

DiversifiedPortfolio32.38%

DiversifiedPortfolio7.45%

DiversifiedPortfolio15.83%

DiversifiedPortfolio5.44%

DiversifiedPortfolio-31.10%

20092002 2003 2004 2005 2006 2007 2008 2010 2011

17

What should investors remember?

Judging the entire market by the performance of the S&P 500 Index is not diversifying.

Asset allocation and diversification are long-term strategies — they may appear not to work over short periods, but they do work long term.

Go deeper with diversification and include more asset classes, styles and managers.

Asset allocation is not dead, but it is misunderstood

Asset allocation and diversification do not guarantee a profit nor protect against a loss. The value of a company’s equity securities is subject to change in the company’s financial condition, and overall market and economic conditions. Fixed-income investments are subject to interest rate and credit risk; their value will normally decline as interest rates rise or if the creditor is unable or unwilling to make principal or interest payments. Foreign investing, especially in emerging markets, has additional risks such as currency and market volatility and political and social instability.

1818

3Principle

Not all bonds ―or bond funds ―

are created equal

19

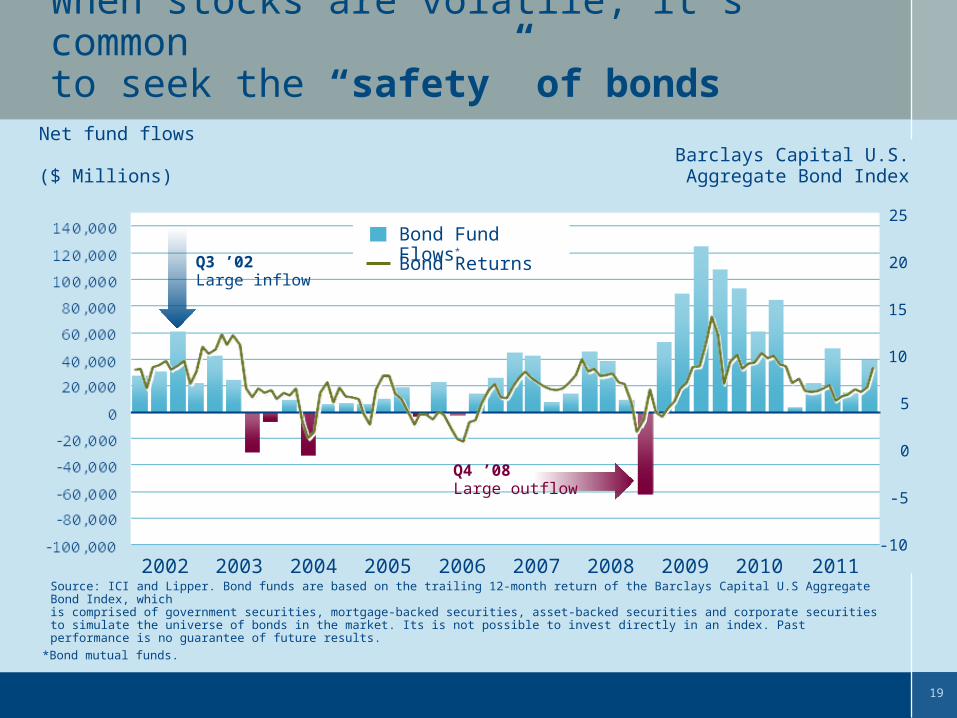

Source: ICI and Lipper. Bond funds are based on the trailing 12-month return of the Barclays Capital U.S Aggregate Bond Index, which is comprised of government securities, mortgage-backed securities, asset-backed securities and corporate securities to simulate the universe of bonds in the market. Its is not possible to invest directly in an index. Past performance is no guarantee of future results.

*Bond mutual funds.

When stocks are volatile, it’s common to seek the “safety” of bonds

Barclays Capital U.S. Aggregate Bond Index

Net fund flows ($ Millions)

Q4 ’08Large outflow

-10

-5

0

5

10

15

20

25

Bond Returns

Bond Fund Flows*

2004 2005 2010 2011200820072006 200920032002

Q3 ’02Large inflow

20

0123456

01/0

2/20

0202

/01/

2002

03/0

1/20

0204

/01/

2002

05/0

1/20

0206

/03/

2002

07/0

1/20

0208

/01/

2002

09/0

3/20

0210

/01/

2002

11/0

1/20

0212

/02/

2002

01/0

2/20

0302

/03/

2003

03/0

3/20

0304

/01/

2003

05/0

1/20

0306

/02/

2003

07/0

1/20

0308

/01/

2003

09/0

2/20

0310

/01/

2003

11/0

3/20

0312

/01/

2003

01/0

2/20

0402

/02/

2004

03/0

1/20

0404

/01/

2004

05/0

3/20

0406

/01/

2004

07/0

1/20

0408

/02/

2004

09/0

1/20

0410

/01/

2004

11/0

1/20

0412

/01/

2004

01/0

3/20

0502

/01/

2005

03/0

1/20

0504

/01/

2005

05/0

2/20

0506

/01/

2005

07/0

1/20

0508

/01/

2005

09/0

1/20

0510

/03/

2005

11/0

1/20

0512

/01/

2005

01/0

3/20

0602

/01/

2006

03/0

1/20

0604

/03/

2006

05/0

1/20

0606

/01/

2006

07/0

3/20

0608

/01/

2006

09/0

1/20

0610

/02/

2006

11/0

1/20

0612

/01/

2006

01/0

3/20

0702

/01/

2007

03/0

1/20

0704

/02/

2007

05/0

1/20

0706

/01/

2007

07/0

2/20

0708

/01/

2007

09/0

4/20

0710

/01/

2007

11/0

1/20

0712

/03/

2007

01/0

2/20

0802

/01/

2008

03/0

3/20

0804

/01/

2008

05/0

1/20

0806

/02/

2008

07/0

1/20

0808

/01/

2008

09/0

2/20

0810

/01/

2008

11/0

3/20

0812

/01/

2008

01/0

2/20

0902

/02/

2009

03/0

2/20

0904

/01/

2009

05/0

1/20

0906

/01/

2009

07/0

1/20

0908

/03/

2009

09/0

1/20

0910

/01/

2009

11/0

2/20

0912

/01/

2009

01/0

1/20

1002

/01/

2010

03/0

1/20

1004

/01/

2010

05/0

1/20

1006

/01/

2010

07/0

1/20

1008

/01/

2010

09/0

1/20

1010

/01/

2010

11/0

1/20

1012

/01/

2010

2011

-01

2011

-02

2011

-03

2011

-04

2011

-05

2011

-06

2011

-07

2011

-08

2011

-09

2011

-10

2011

-11

2011

-12

(%)

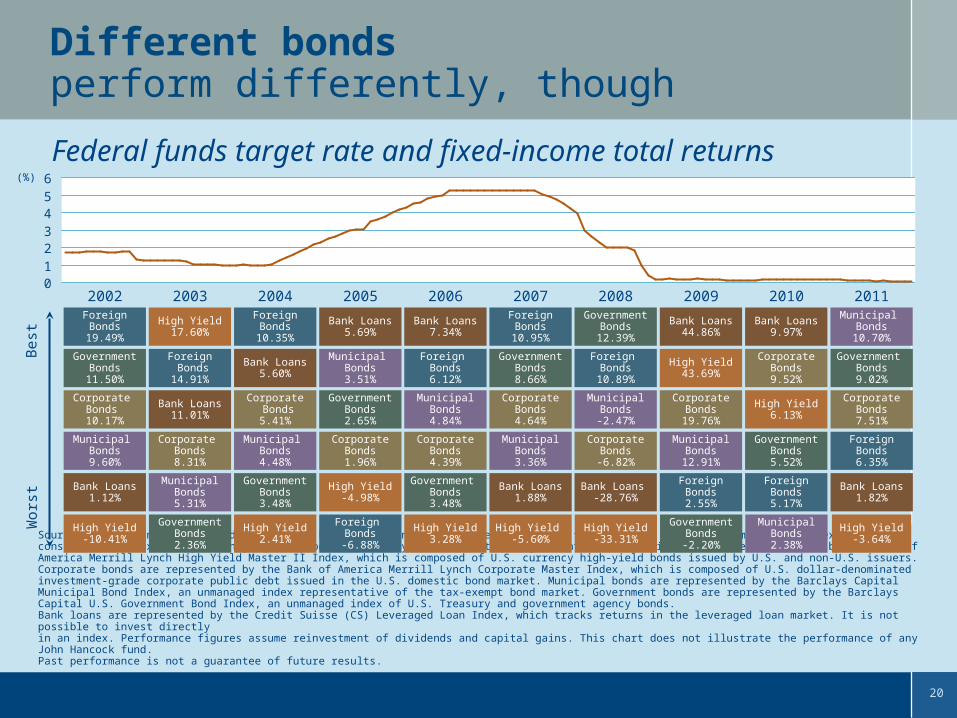

Different bonds perform differently, though

Source: Lipper, Inc and the Federal Reserve Board. Foreign bonds are represented by the Citigroup World Government Bond Index, which consists of approximately 600 high-quality bonds issued by 17 different foreign countries. High-yield bonds are represented by the Bank of America Merrill Lynch High Yield Master II Index, which is composed of U.S. currency high-yield bonds issued by U.S. and non-U.S. issuers. Corporate bonds are represented by the Bank of America Merrill Lynch Corporate Master Index, which is composed of U.S. dollar-denominated investment-grade corporate public debt issued in the U.S. domestic bond market. Municipal bonds are represented by the Barclays Capital Municipal Bond Index, an unmanaged index representative of the tax-exempt bond market. Government bonds are represented by the Barclays Capital U.S. Government Bond Index, an unmanaged index of U.S. Treasury and government agency bonds. Bank loans are represented by the Credit Suisse (CS) Leveraged Loan Index, which tracks returns in the leveraged loan market. It is not possible to invest directly in an index. Performance figures assume reinvestment of dividends and capital gains. This chart does not illustrate the performance of any John Hancock fund. Past performance is not a guarantee of future results.

Federal funds target rate and fixed-income total returns

Best

Wors

t

MunicipalBonds

12.91%

High Yield43.69%

CorporateBonds

19.76%

ForeignBonds2.55%

GovernmentBonds-2.20%

Bank Loans44.86%

Bank Loans1.12%

ForeignBonds

19.49%

Corporate Bonds 10.17%

Municipal Bonds9.60%

High Yield-10.41%

GovernmentBonds

11.50%

MunicipalBonds5.31%

High Yield17.60%

Bank Loans11.01%

Corporate Bonds8.31%

GovernmentBonds2.36%

Foreign Bonds14.91%

Municipal Bonds4.48%

ForeignBonds

10.35%

Bank Loans5.60%

Corporate Bonds5.41%

GovernmentBonds3.48%

High Yield2.41%

CorporateBonds1.96%

Bank Loans5.69%

High Yield-4.98%

GovernmentBonds2.65%

Foreign Bonds-6.88%

Municipal Bonds3.51%

CorporateBonds4.39%

High Yield3.28%

Foreign Bonds6.12%

MunicipalBonds4.84%

Government Bonds3.48%

Bank Loans7.34%

High Yield -5.60%

ForeignBonds

10.95%

CorporateBonds4.64%

MunicipalBonds3.36%

Bank Loans1.88%

GovernmentBonds8.66%

High Yield-33.31%

GovernmentBonds

12.39%

MunicipalBonds-2.47%

CorporateBonds-6.82%

Bank Loans -28.76%

Foreign Bonds

10.89%

GovernmentBonds5.52%

High Yield6.13%

CorporateBonds9.52%

ForeignBonds5.17%

MunicipalBonds2.38%

Bank Loans9.97%

Bank Loans1.82%

CorporateBonds7.51%

Municipal Bonds

10.70%

High Yield-3.64%

ForeignBonds6.35%

Government Bonds9.02%

20092002 2003 2004 2005 2006 2007 2008 2010 2011

21

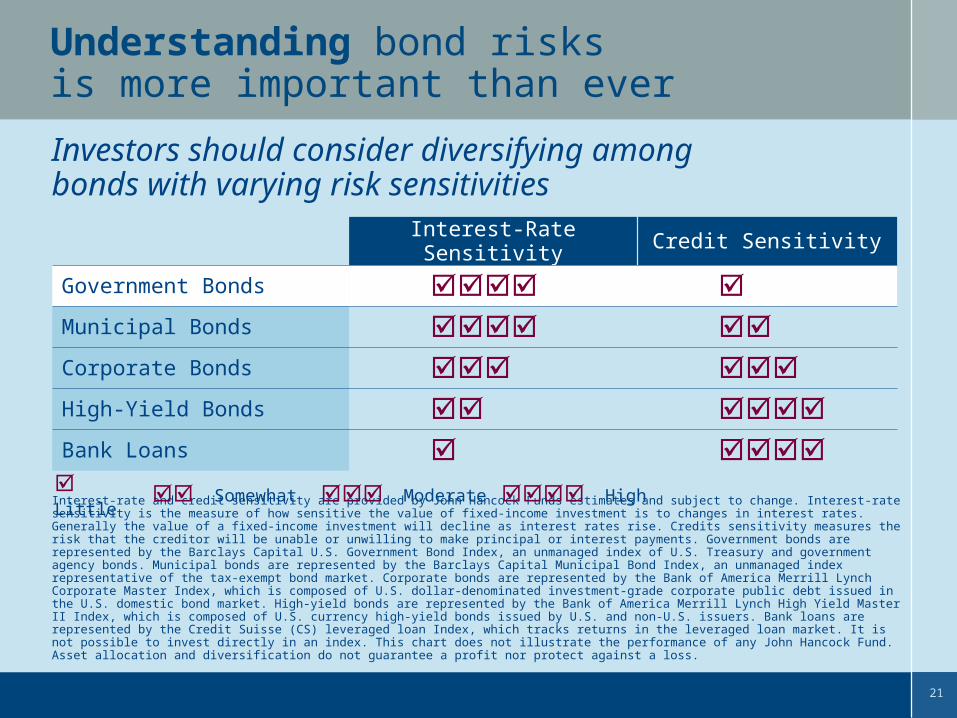

Understanding bond risks is more important than ever

Investors should consider diversifying among bonds with varying risk sensitivities

Interest-rate and credit sensitivity are provided by John Hancock Funds estimates and subject to change. Interest-rate sensitivity is the measure of how sensitive the value of fixed-income investment is to changes in interest rates. Generally the value of a fixed-income investment will decline as interest rates rise. Credits sensitivity measures the risk that the creditor will be unable or unwilling to make principal or interest payments. Government bonds are represented by the Barclays Capital U.S. Government Bond Index, an unmanaged index of U.S. Treasury and government agency bonds. Municipal bonds are represented by the Barclays Capital Municipal Bond Index, an unmanaged index representative of the tax-exempt bond market. Corporate bonds are represented by the Bank of America Merrill Lynch Corporate Master Index, which is composed of U.S. dollar-denominated investment-grade corporate public debt issued in the U.S. domestic bond market. High-yield bonds are represented by the Bank of America Merrill Lynch High Yield Master II Index, which is composed of U.S. currency high-yield bonds issued by U.S. and non-U.S. issuers. Bank loans are represented by the Credit Suisse (CS) leveraged loan Index, which tracks returns in the leveraged loan market. It is not possible to invest directly in an index. This chart does not illustrate the performance of any John Hancock Fund. Asset allocation and diversification do not guarantee a profit nor protect against a loss.

Interest-Rate Sensitivity Credit Sensitivity

Government Bonds Municipal Bonds Corporate Bonds High-Yield Bonds Bank Loans

Little Somewhat Moderate High

22

Balancing risk with yield

Fixed income yields (2006–2011)

0

4

8

12

16

20

2006 2007 2008 2009 2010 2011

High Yield Bonds

Corporate Bonds

Government Bonds

Inflation

3.88%

8.29%

1.05%Inflation 2.99%

Yie

ld (

%)

Source: Bloomberg as of 12/31/11. High-yield bonds are represented by the Bank of America Merrill Lynch High Yield Master II Index, which is composed of U.S. currency high-yield bonds issued by U.S. and non-U.S. issuers. Corporate bonds are represented by the Bank of America Merrill Lynch Corporate Master Index, which is composed of U.S. dollar-denominated investment-grade corporate public debt issued in the U.S. domestic bond market. Government bonds are represented by the Bank of America U.S. Treasury Master Index, an unmanaged index of U.S. Treasury and government agency bonds. Inflation is measured by the Consumer Price Index published by the U.S. Bureau of Labor Statistics. It is not possible to invest directly in an index. Performance figures assume reinvestment of dividends and capital gains. This chart does not illustrate the performance of any John Hancock fund. Past performance is not a guarantee of future results.

2006 2007 2008 2009 2010 2011

23

What should investors remember?

Holding bonds in your portfolio may provide the income you need with less volatility than stocks.

Different types of bonds perform well in different economic environments.

Bond funds should be diversified too.

Not all bonds — or bond funds — are created equal

Fixed-income investments are subject to interest rate and credit risk; their value will normally decline as interest rates rise or if the creditor is unable or unwilling to make principal or interest payments. Investments in higher-yielding, lower-rated securities involve additional risks as these securities include a higher risk of default and loss of principal. Asset allocation and diversification do not guarantee a profit nor protect against a loss.

2424

4Principle

Yes, it’s STILL stocksfor the long run

25

$8,000

$10,000

$12,000

$14,000

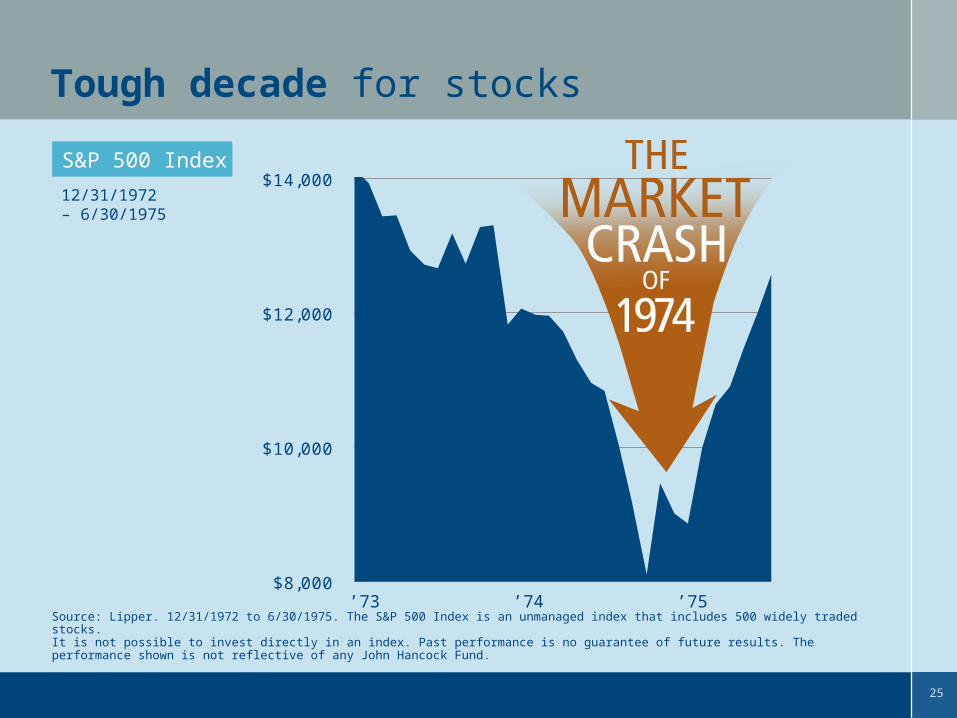

Tough decade for stocks

Source: Lipper. 12/31/1972 to 6/30/1975. The S&P 500 Index is an unmanaged index that includes 500 widely traded stocks.It is not possible to invest directly in an index. Past performance is no guarantee of future results. The performance shown is not reflective of any John Hancock Fund.

S&P 500 Index S&P 500 Index

12/31/1972 – 6/30/1975

’73 ’74 ’75

26

$0

$200

$400

$600

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Thousands

Put the market in perspective

Source: Lipper. 1/1/1970 to 12/31/2011. The S&P 500 Index is an unmanaged index that includes 500 widely traded stocks.It is not possible to invest directly in an index. Past performance is no guarantee of future results. The performance shown is not reflective of any John Hancock fund.

S&P 500 Index (1970–2011)

27

Stocks outperform over the long term

Average annual returns (1926–2011)

Source: Calculated by John Hancock Funds, LLC using information and data presented in ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. Stocks are represented by the S&P 500 Index, an unmanaged, commonly used measure of common stock total return performance. Corporate bonds are represented by the Ibbotson U.S. Aggregate Index which is comprised of government securities, mortgage-backed securities, asset-backed securities and corporate securities to simulate the universe of bonds in the market. U.S. government bonds are represented by the Ibbotson Government Bond Index which is an unmanaged index of U.S. Treasury and government agency bonds. Cash equivalents are represented by the Ibbotson 30-day Treasury Bill Index which measures the performance of one-month maturity U.S. Treasury Bills and are a commonly used measure of a savings investment. Inflation is measured by the Consumer Price Index published by the U.S. Bureau of Labor Statistics. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Stocks 9.78%

Corporate Bonds 6.06%

Long-Term Government Bonds 5.72%

Cash Equivalents 3.58%

Inflation (CPI) 2.99%

28

4 4 4 4

10

12

4

89

12

6

< 0 0 to2%

2 to4%

4 to6%

6 to8%

8 to10%

10 to12%

12 to14%

14 to16%

16 to18%

> 18%

Rolling 10-year stock market returns

For calendar year-end periods (1926–2011)

Source: Calculated by John Hancock Funds, LLC using information and data presented in ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. Stocks are represented by the S&P 500 Index, an unmanaged, commonly used measure of common stock total return performance. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Number of OccurrencesNumber of Occurrences

200620052002

19801972

1970

1966194919471945

1944

1942

2000

1992199119891988

19611960

19571955

1954

1952

1951

2007

19791946

1935

2003

19831968

1965

19821981

1976

1973

1971196919481943

19411936

2004

20011990

1986

196719641962

1950

199619951994

199319871985

1984

1963

1953

1999199819971959

19581956

2008

1939

1938

2009

19741940

1937

201019781977

1975

2011

29

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

'70 '75 '80 '85 '90 '95 '00 '05 '10

Without dividends

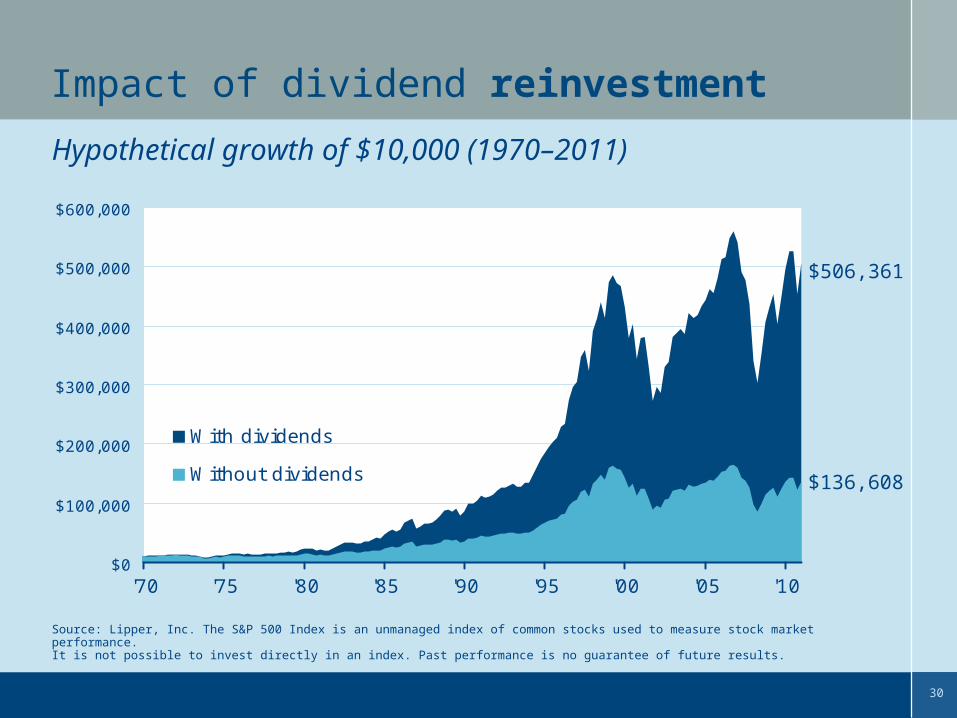

Impact of dividend reinvestment

Source: Lipper, Inc. The S&P 500 Index is an unmanaged index of common stocks used to measure stock market performance. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Hypothetical growth of $10,000 (1970–2011)

Are Dividends Important?

$136,608

30

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

'70 '75 '80 '85 '90 '95 '00 '05 '10

With dividends

Without dividends

Impact of dividend reinvestment

Source: Lipper, Inc. The S&P 500 Index is an unmanaged index of common stocks used to measure stock market performance. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Hypothetical growth of $10,000 (1970–2011)

$136,608

$506,361

31

7.81%

10.98%9.84%

9.27%

0%

2%

4%

6%

8%

10%

12%

14%

20 Years 30 Years 40 Years 50 Years

What is your investment horizon?

Annual total returns inclusive of the last decade

Source: ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. This information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Stocks are represented by the S&P 500 Index — an unmanaged index of 500 widely traded common stocks. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

32

What should investors remember?

Equities remain a great way to fight inflation over the long term.

By maintaining a long-term perspective, you will be better positioned to maintain arationale mindset during periods of volatility.

Reinvesting dividends can enhance total return.

Yes, it’s STILL stocks for the long run!

The value of a company’s equity securities is subject to change in the company’s financial condition, and overall market and economic conditions. Past performance is no guarantee of future results.

3333

5Principle

Investing abroadshouldn’t be a

foreign experience

Patrick L. McFawn CFP®, CPA & Dale L. White CFP®, CPA

34

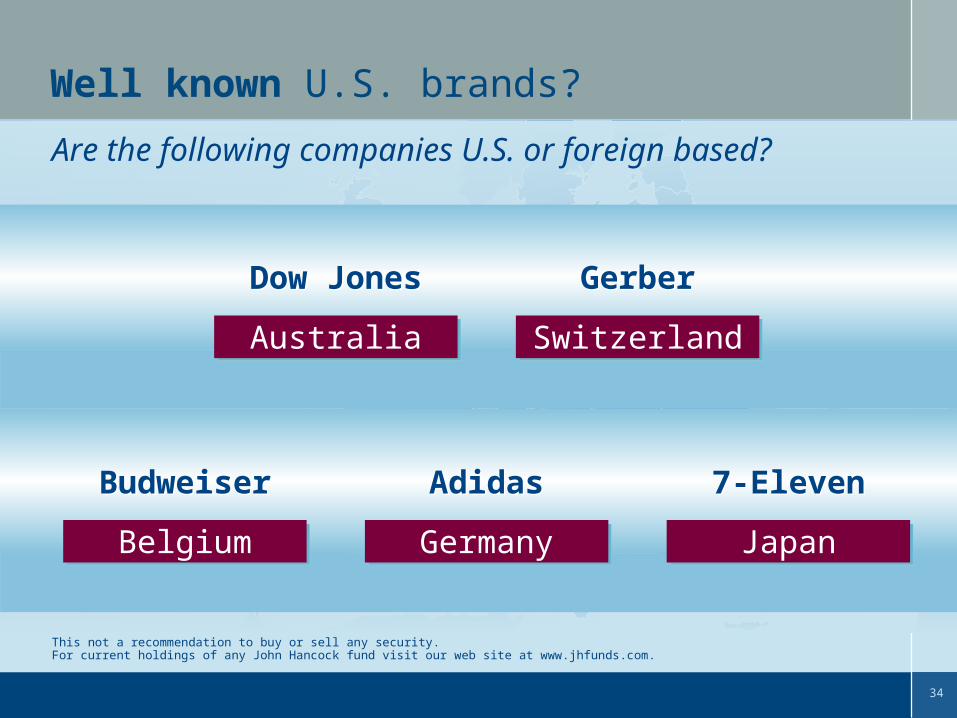

Well known U.S. brands?

Are the following companies U.S. or foreign based?

This not a recommendation to buy or sell any security.For current holdings of any John Hancock fund visit our web site at www.jhfunds.com.

BelgiumBelgium

SwitzerlandSwitzerlandAustraliaAustralia

GermanyGermany JapanJapan

Dow JonesDow Jones GerberGerber

BudweiserBudweiser AdidasAdidas 7-Eleven7-Eleven

35

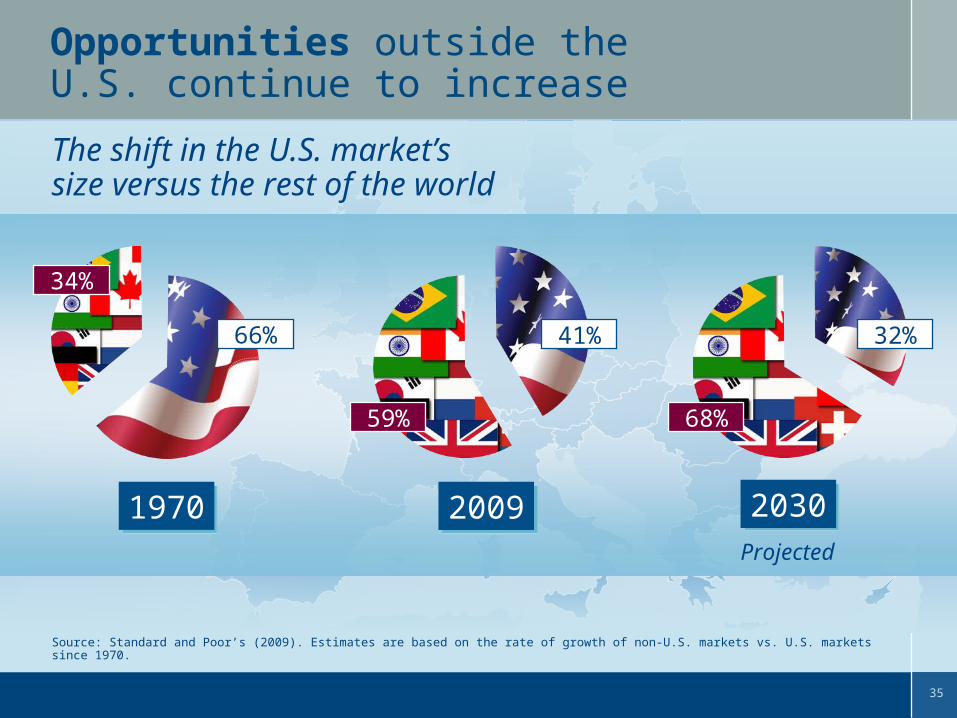

Opportunities outside the U.S. continue to increase

Source: Standard and Poor’s (2009). Estimates are based on the rate of growth of non-U.S. markets vs. U.S. markets since 1970.

The shift in the U.S. market’s size versus the rest of the world

66%

19701970

34%

20092009

41%

59%

Projected

20302030

32%

68%

36

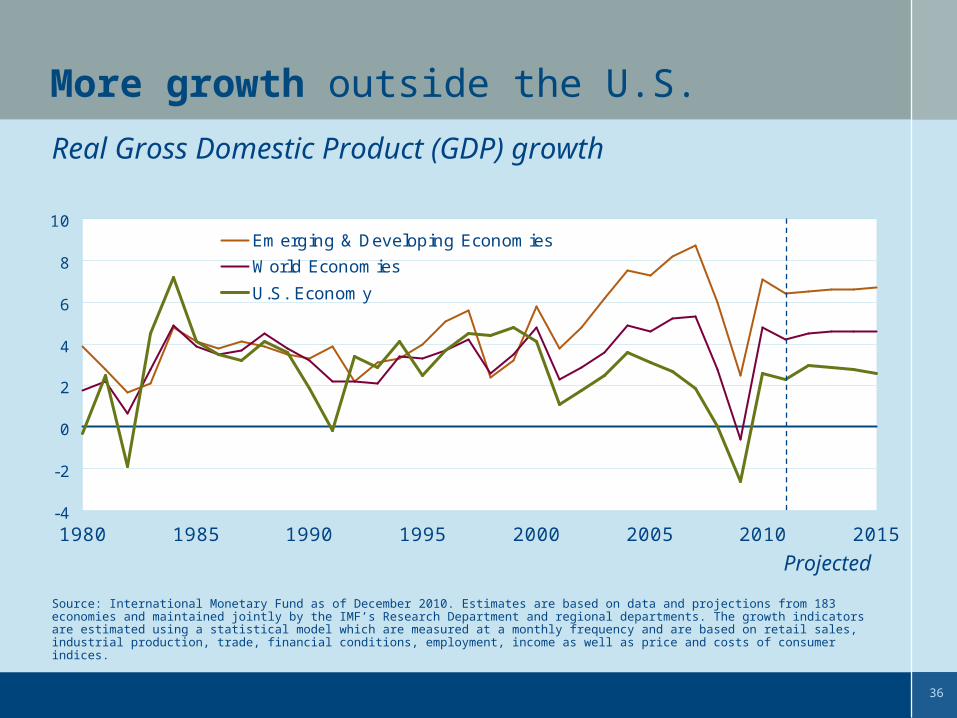

Source: International Monetary Fund as of December 2010. Estimates are based on data and projections from 183 economies and maintained jointly by the IMF’s Research Department and regional departments. The growth indicators are estimated using a statistical model which are measured at a monthly frequency and are based on retail sales, industrial production, trade, financial conditions, employment, income as well as price and costs of consumer indices.

More growth outside the U.S.

Real Gross Domestic Product (GDP) growth

-4

-2

0

2

4

6

8

10

1980 1985 1990 1995 2000 2005 2010 2015

Emerging & Developing Economies

World Economies

U.S. Economy

Projected

37

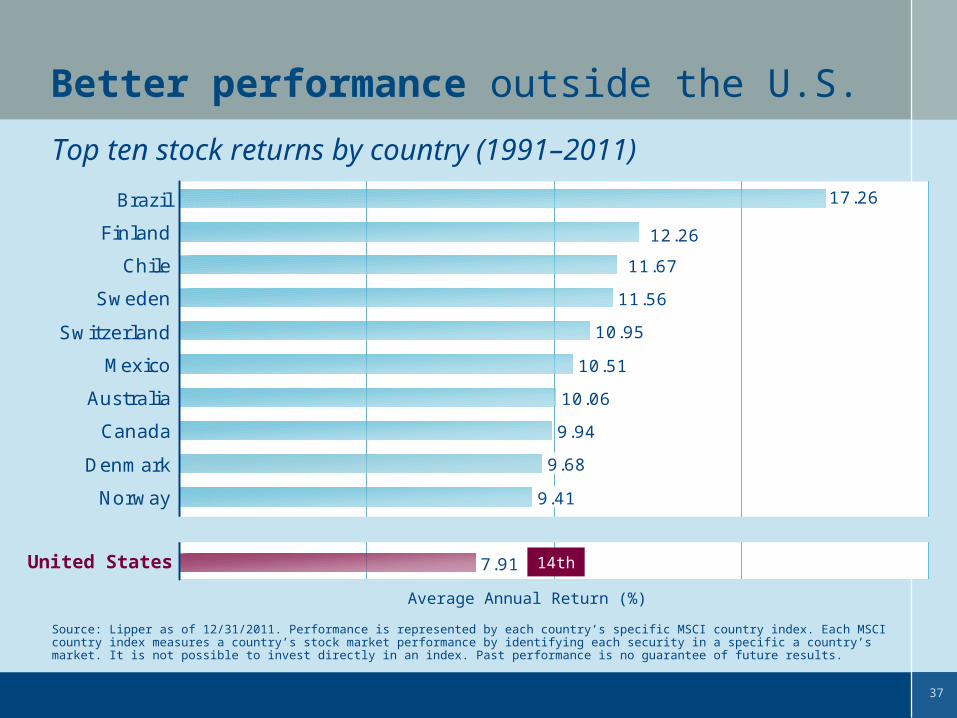

Top ten stock returns by country (1991–2011)

Better performance outside the U.S.

Source: Lipper as of 12/31/2011. Performance is represented by each country’s specific MSCI country index. Each MSCI country index measures a country’s stock market performance by identifying each security in a specific a country’s market. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

11.56

10.95

10.51

9.94

9.68

9.41

7.91

10.06

17.26

12.26

11.67

Brazil

Finland

Chile

Sweden

Switzerland

Mexico

Australia

Canada

Denmark

Norway

United States 14thUnited States

Average Annual Return (%)

38

What should investors remember?

Foreign companies offer some of the best opportunities for growth.

Diversifying with foreign companies may actually improve returns while also reducing overall portfolio volatility.

Investing abroad shouldn’t be a foreign experience

Foreign investing, especially in emerging markets, has additional risks such as currency and market volatility and political and social instability.

3939

Where do wego from here?

40

24

3032

< -0.2% -0.2 to 19.8% >19.8%

Stocks are a market of extremes — investors should expect volatility in the short term

Source: Calculated by John Hancock Funds, LLC using information and data presented in ENCORR Software, ©2011 Morningstar, Inc. All rights reserved. Used with permission. Based on average annual percentage returns for the S&P 500 Index over 85 one-year periods from 1926–2011, assuming reinvestment of dividends and capital gains. The S&P 500 Index is an unmanaged index of 500 widely traded common stocks. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

What’s the most common occurrence in the stock market in a calendar year?What’s the most common occurrence in the stock market in a calendar year?

Calendar year returns of 8–12% have occurred ONLY 5 TIMES IN THE 86 YEARS SINCE 1926

37.2%34.9%

27.9%

1926–2011

# of Occurrences /% of Occurrences

< 0% 0 to 20% > 20%

41

Market performance

Positive

Negative

But invest for the long term

This hypothetical scenario is for illustration purposes only and is not a prediction of future market conditions.

Riskiesttime

Best opportunityto make money

EUPHORIC“I should quit my job and do this full-time!

Look at the money I’m making!”

Confident“I’ve already

made money. This is great.”

Nervous“What happened? What is going on?”

Desperate“There’s no

point in selling now, I’ve lost

too much.”

DEFEATED“There go my dreams of

an early retirement.”

Hopeful“Things seem like they’re

turning around.”

42

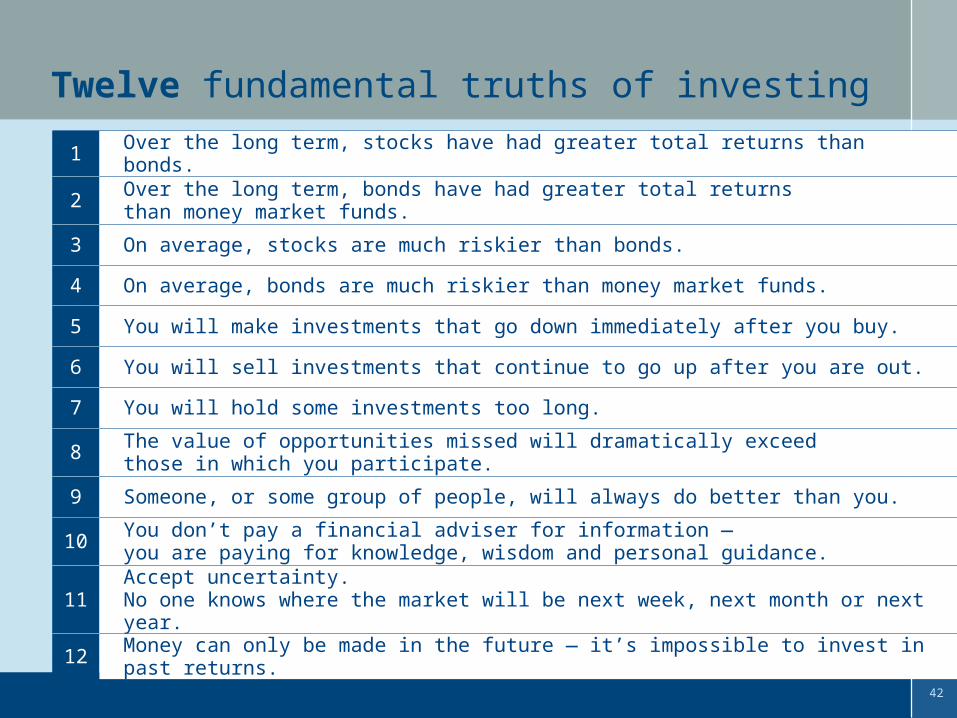

Twelve fundamental truths of investing

Source: Horsesmouth LLC.

1 Over the long term, stocks have had greater total returns than bonds.

2 Over the long term, bonds have had greater total returns than money market funds.

3 On average, stocks are much riskier than bonds.

4 On average, bonds are much riskier than money market funds.

5 You will make investments that go down immediately after you buy.

6 You will sell investments that continue to go up after you are out.

7 You will hold some investments too long.

8 The value of opportunities missed will dramatically exceed those in which you participate.

9 Someone, or some group of people, will always do better than you.

10 You don’t pay a financial adviser for information ― you are paying for knowledge, wisdom and personal guidance.

11 Accept uncertainty. No one knows where the market will be next week, next month or next year.

12 Money can only be made in the future ― it’s impossible to invest in past returns.

43

A fund’s investment objectives, risks, charges and expenses should be considered before investing. The prospectus contains this and other important information about the fund. To obtain a prospectus, call your financial professional or John Hancock Funds at 1-800-225-5291 or visit our Web site at www.jhfunds.com. Please read the prospectus carefully before investing or sending money.

A word about risk

The performance data contained in this presentation represents past performance, which does not guarantee future results. Performance, especially for short time periods, should not be the sole factor in making your investment decisions.

LLCP 8/12

John Hancock Funds, LLC • MEMBER FINRA/SIPC • 601 Congress Street, Boston, MA 02210-2805 • www.jhfunds.com

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE. NOT INSURED BY ANY GOVERNMENT AGENCY.