the path ahead: property/casualty insurance in the wake of

TRANSCRIPT

The Path Ahead: Property/Casualty Insurance

in the Wake of the Global Financial Crisis

Professional Liability Underwriting Society22nd Annual Conference

Chicago, IL

November 11, 2009

Robert P. Hartwig, Ph.D., CPCU, President & EconomistInsurance Information Institute ♦ 110 William Street ♦ New York, NY 10038

Tel: (212) 346-5520 ♦ Fax: (212) 732-1916 ♦ [email protected] ♦ www.iii.org

2

Presentation Outline• The Economic Storm: Financial Crisis & Recession

Exposure, Growth & Profitability• Insurance Industry Financial Overview & Outlook

ProfitabilityPremium GrowthUnderwriting Performance: Commercial & Personal LinesFinancial Market ImpactsCapital & Capacity

• Shifting Legal Liability & Tort EnvironmentFinancial Scandals and Economic Crises

• Professional Liability Insurance Operating EnvironmentMed Mal, D&O

• Key Threats and Issues Facing P/C Insurers Through 2015• Healthcare Debate Spillover Effects

• Financial Strength & RatingsKey Differences Between Insurer and Bank Performance During Crisis

Q&A

THE ECONOMIC STORM

What the Financial Crisis and Recession Mean for the

Industry’s Exposure Base,Growth, Profitability and

Investments

4

3.7%

0.8% 1.

6% 2.5%

3.6%

3.1%

2.9%

0.1%

4.8%

4.8%

-0.7

%

1.5%

-2.7

%

3.5%

2.4% 2.6% 2.7% 2.8% 2.9%

-0.7

%

-6.4%

-5.4%

-0.2%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

07:1

Q

07:2

Q

07:3

Q

07:4

Q

08:1

Q

08:2

Q

08:3

Q

08:4

Q

09:1

Q

09:2

Q

09:3

Q

09:4

Q

10:1

Q

10:2

Q

10:3

Q

10:4

Q

Real GDP Growth*

*Blue bars are Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 10/09; Insurance Information Institute.

Recession began in December 2007. Economic toll of credit crunch, housing slump, labor market contraction has been severe but recovery is in sight

The Q1:2009 decline was the steepest since the

Q1:1982 drop of 6.4%

Personal and commercial lines

exposure base have been hit

hard and will be slow to come

back

5

Length of U.S. Business Cycles, 1929-Present*

43

138 11 10 8 10 11

166

168 8

19

50

80

3745

39

24

106

36

58

12

92

120

73

0102030405060708090

100110120

Aug.1929

May1937

Feb.1945

Nov.1948

July1953

Aug.1957

Apr.1960

Dec.1969

Nov.1973

Jan.1980

Jul.1981

Jul.1990

Mar.2001

Dec.2007

Contraction Expansion Following

* Through June 2009 (likely the “official end” of recession) **Post-WW II period through end of most recent expansion. Sources: National Bureau of Economic Research; Insurance Information Institute.

Duration (Months)

Month Recession Started

Average Duration**Recession = 10.4 Months

Expansion = 60.5 MonthsLength of

expansions greatly exceeds

contractions

6

5.2%

-0.9

%-7

.4%

-6.5

%-1

.5%

1.8%

4.3%

18.6

% 20.3

%5.

8%0.

3%-1

.6%

-1.0

%-1

.8%

-1.0

%3.

1%1.

1%0.

8%0.

4%0.

6%-0

.4%

-0.3

%1.

6%5.

6%13

.7%

7.7%

1.2%

-2.9

% -0.5

%-3

.8%

-4.4

%-4

.5%

-10%

-5%

0%

5%

10%

15%

20%

25%78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Real

NW

P G

row

th

-4%

-2%

0%

2%

4%

6%

8%

Rea

l GD

P G

row

th

Real NWP Growth Real GDP

Real GDP Growth vs. Real P/C Premium Growth: Modest Association

P/C insurance industry’s growth is influenced modestly by growth

in the overall economy

Sources: A.M. Best, US Bureau of Economic Analysis, Blue Chip Economic Indicators, 10/09; Insurance Information Inst.

Regional Differences Will Significantly

Impact P/C Markets Recovery in Some Areas Will Begin Years Ahead of Others & Speed of Recovery Will Differ By Orders of

Magnitude

8

State Economic Growth Varied Tremendously in 2008

Eastern US growing more slowly than Plains,

Mountains

9

Fastest Growing States in 2008: Plains, Mountain States Lead

7.3%

4.4%3.5%

2.9%2.0%2.1%2.5%

2.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

ND WY SD CO OK WV IA TX, MN,NM, WA

Natural resource and agricultural states have done

better than most others recently, helping insurance

exposure in those areas

Source: US Bureau of Economic Analysis; Insurance Information Institute.

PercentReal State GDP Growth

10

Slowest Growing States in 2008: Diversity of States Suffering

-0.1%

-0.4%-0.6%-0.6%

-1.5%-1.6%-1.6%-1.7%-2.0%

-0.9%-0.6%-0.6%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%KY CT AZ GA IN NV RI MI DE FL OH AK

States in the North, South, East and West all represented among

hardest hit but for differing reasons

Source: US Bureau of Economic Analysis; Insurance Information Institute.

PercentReal State GDP Growth

P/C Premium Growth

Primarily Driven by the Industry’s Underwriting Cycle, Not the Economy

12

-6%-4%-2%0%2%4%6%8%

10%12%14%16%18%20%22%24%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

09:H

1

Sources: A.M. Best (historical and forecast), ISO, Insurance Information Institute

Strength of Recent Hard Marketsby NWP Growth

1975-78 1984-87 2000-03

12

Net written premiums fell 1.0%

in 2007 (first decline since 1943) by 1.4% in 2008, and 4.2% in H1 2009, the first 3-

year decline since 1930-33

Shaded areas denote “hard

market” periods

13

Average Commercial Rate Change,All Lines, (1Q:2004 – 3Q:2009)

-3.2

%-5

.9%

-7.0

%-9

.4%

-9.7

% -8.2

%-4

.6% -2

.7%

-3.0

%-5

.3%

-9.6

%-1

1.3%

-11.

8%-1

3.3% -1

2.0%

-13.

5%-1

2.9% -1

1.0%

-6.4

% -5.1

%-4

.9%

-5.8

%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%1Q

042Q

043Q

044Q

041Q

052Q

053Q

054Q

051Q

062Q

063Q

064Q

061Q

072Q

073Q

074Q

071Q

082Q

083Q

084Q

081Q

092Q

093Q

09

Source: Council of Insurance Agents & Brokers; Insurance Information Institute

KRW Effect

-0.1

% Magnitude of price declines is now

shrinking. Reflects shrinking capital,

reduced investment gains, deteriorating

underwriting performance, higher cat losses and costlier

reinsurance

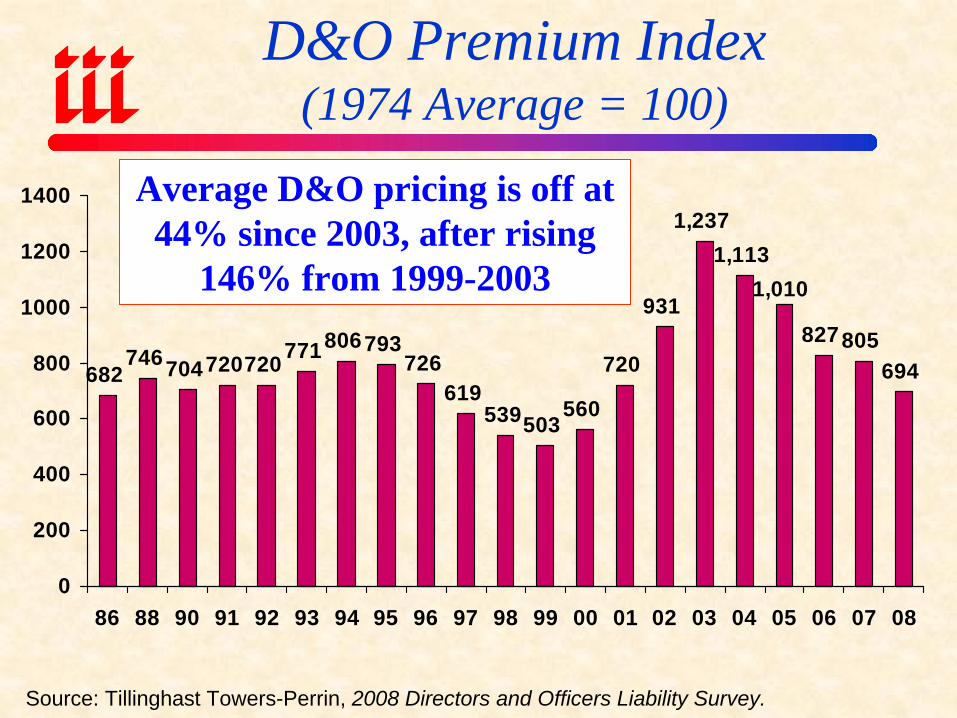

D&O Premium Index(1974 Average = 100)

682746704720720771806793

726619

539503560

720

931

1,2371,113

827805694

1,010

0

200

400

600

800

1000

1200

1400

86 88 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey.

Average D&O pricing is off at 44% since 2003, after rising

146% from 1999-2003

Investment Environment

Volatility Breeds Litigation

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Source: Ibbotson Associates, Insurance Information Institute. *Through November 9, 2008.

Total Returns for Large Company Stocks: 1970-2009*

S&P 500 was down 38.5% in 2008; Up 21.0% so far in 2009*

Market rebound of 2009 still leaves

investors underwater from pre-crisis highs

17

Business Bankruptcy Filings,1980-2009*

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

53 71,5

4970

,643

62,3

0452

,374

51,9

5953

,549

54,0

2744

,367

37,8

8435

,472

40,0

9938

,540

35,0

3734

,317

39,2

0119

,695 28

,322

43,5

4660

,000

010,00020,00030,00040,00050,00060,00070,00080,00090,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

% Change SurroundingRecessions

1980-82: 58.6%1980-87: 88.7%1990-91: 10.3%2000-01: 13.0%

2006-09: 204.6%*

*Based estimate of 60,000 business bankruptcies in 2009; actual first half total was 30,333.Source: American Bankruptcy Institute; Insurance Information Institute

There were 30,333 business bankruptcies during the first half of 2009, up 64% from 2008: H1 and on track for about 60,000 for all of 2009, the most since 1993. Current

recession will generate 200%+ surge.

Business bankruptcies contribute to litigation

18

Recession, InvestmentVolatility & Reveal Scandals

• Charles Ponzi Was a Two-Bit Scamster by Today’s Standards

Made $20 million in 1920 ($225 in today’s dollars)

• Bernard Madoff: $65 Billion Ponzi Scheme• R. Allen Stanford: $8 Billion Fraudulent Investment

Scheme Involving CDs• Raj Rajaratnam (Galleon Group co-Founder) & 19

Others: Criminally Charged With Making Millions from Insider Trading

• Recessions ALWAYS Reveal Financial Scandals• 2001: Enron/Tyco• 1991-92: Bank of Commercial & Credit International

Sources: SEC, Bloomberg, BusinessWeek.

Shareholder Class Action Lawsuits*

*Securities fraud suits filed in U.S. federal courts; 2009 figure is current through 11/05/09.Source: Stanford University School of Law (securities.stanford.edu); Insurance Information Institute

164202

163

231188

111

174

242209216

498

266227239

182119

177222

146

0

100

200

300

400

500

600

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*

Securities litigation activity continues to be driven by claims

against financial services firms.

P/C Investment Performance

Investments are a Principle Source of Declining

Profitability

21

Property/Casualty Insurance Industry Investment Gain:1994- 2009:H11

$ Billions

$35.4$42.8

$47.2$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.4

$12.4

$56.9$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08

09:H

1

1Investment gains consist primarily of interest, stock dividends and realized capital gains and losses. 2006 figure consists of $52.3B net investment income and $3.4B realized investment gain.*2005 figure includes special one-time dividend of $3.2B.

Sources: ISO; Insurance Information Institute.

Investment gains fell by 51% in 2008 due to lower yields, poor equity market

conditions. Falling again in 2009.

21

22

P/C Insurer Net Realized Capital Gains, 1990-2009:H1

$2.88$4.81

$9.89

$1.66

$6.00

$9.24$10.81

$13.02

$16.21

$6.63

-$1.21

$6.61$8.92

-$11.17

-$19.80

$18.02

$3.52

$9.70$9.13$9.82

-$20-$18-$16-$14-$12-$10-$8-$6-$4-$2$0$2$4$6$8

$10$12$14$16$18$20

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

09H

1

Sources: A.M. Best, ISO, Insurance Information Institute.

Realized capital losses hit a record $19.8 billion in 2008 due to financial market turmoil, a $27.7 billion swing from 2007, followed by an $11.2B

drop in H1 2009. This is a primary cause of 2008/2009’s large drop in profits and ROE.

$ Billions

22

23

0.06% 0.12% 0.21% 0.40%

0.96%1.48%

2.37%

3.02%3.40%

4.82% 4.96% 5.04% 4.96% 4.82% 4.82% 4.88% 5.00% 4.93% 5.00% 5.19%

4.19%4.14%

0%

1%

2%

3%

4%

5%

6%

1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 20Y 30Y

September 2009 Yield CurvePre-Crisis (July 2007)

Treasury Yield Curves: Pre-Crisis (July 2007) vs. Sept. 2009

Sources: Board of Governors of the United States Federal Reserve Bank; Insurance Information Institute.

Stock dividend cuts will further pressure investment income

Treasury Yield Curve is at its most depressed level in at least 45 years. Investment

income is falling as a result.

Distribution of P/C Insurance Industry’s Investment Portfolio

Cash & Short-Term Investments

7.2%

Common Stock17.9%

Bonds66.7%

Preferred Stock1.5%

Real Estate0.8%

Other5.9%

Portfolio Facts•Invested assets totaled $1.3 trillion as of 12/31/07•Insurers are generally conservatively invested, with 2/3 of assets invested in bonds as of 12/31/07•Only about 18% of assets were invested in common stock as of 12/31/07•Even the most conservative of portfolios was hit hard in 2008

Source: NAIC; Insurance Information Institute research;.

As of December 31, 2007

24

Distribution of P/C Insurance Industry’s Investment Portfolio

Cash & Short-Term Investments

8.0%

Common Stock14.8%

Bonds68.4%

Preferred Stock1.8%

Real Estate0.9%

Other6.2%

Portfolio Facts•Invested assets totaled $1.2 trillion as of 12/31/08, down from $1.3 trillion as of 12/31/07•Insurers are generally conservatively invested, with 2/3+ of assets invested in bonds as of 12/31/08•Only about 15% of assets were invested in common stock as of 12/31/08, down from 18% one year earlier•Even the most conservative of portfolios were hit hard in 2008

Source: NAIC; Insurance Information Institute research;.

As of December 31, 2008

25

Profitability

Historically Volatile

27

P/C Net Income After Taxes1991-2009:H1 ($ Millions)*

$14,

178

$5,8

40

$19,

316

$10,

870

$20,

598

$24,

404 $3

6,81

9

$30,

773

$21,

865

$3,0

46

$30,

029

$62,

496

$2,3

79

$5,7

57

-$6,970

$65,

777

$44,

155

$20,

559 $3

8,50

1

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,00091 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

09:H

1

*ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields an 4.5% ROAS for 2008 and 2.2%. 2009:Q1 net income was $10.0 billion excl. M&FG.Sources: A.M. Best, ISO, Insurance Information Inst.

2005 ROE= 9.4%2006 ROE = 12.2%2007 ROAS1 = 12.4%2008 ROAS = 0.5%*2009:H1 ROAS = 2.5%*

Insurer profits peaked in 2006 and 2007, but fell 96.2% during the economic

crisis in 2008

27

28

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 0809:H1

US P/C Insurers All US Industries

ROE: P/C vs. All Industries 1987–2009: H1*

*Excludes Mortgage & Financial Guarantee in 2008 and 2009Sources: ISO, Fortune; Insurance Information Institute.

Andrew Northridge

Hugo Lowest CAT losses in 15 years

Sept. 11

4 Hurricanes

Katrina, Rita, Wilma

P/C profitability is cyclical and volatile

Financial Crisis*

29

97.5

100.6 100.1 100.7

92.6

99.5101.0

8.9%4.2%

12.7%

14.3% 15.9%

9.6%

4.5%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2008* 2009:H1*

Com

bine

d R

atio

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Ret

run

on E

quity

*

Combined Ratio ROE*

* 2008/9 figures are return on average statutory surplus. Excludes mortgage and financial guarantee insurers.Source: Insurance Information Institute from A.M. Best and ISO data.

A 100 Combined Ratio Isn’t What it Used to Be: 95 is Where It’s At

Combined ratios must me must lower in today’s depressed

investment environment to generate risk

appropriate ROEs

Underwriting Trends

Financial Crisis Does Not Directly Impact Underwriting

Performance: Cycle, Catastrophes Were 2008’s Drivers

31

115.8

107.5

100.198.4

100.8

92.6

99.5101.0

95.7

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009:H1*

P/C Insurance Industry Combined Ratio, 2001-2009:H1*

*Excludes Mortgage & Financial Guaranty insurers in 2008. Including M&FG, 2008=105.1, 2009=100.9 Sources: A.M. Best, ISO.

Best combined ratio since 1949

(87.6)

As recently as 2001, insurers paid out nearly $1.16 for every

$1 in earned premiums

Relatively low CAT

losses, reserve releases

Cyclical Deterioration

31

2005 ratio benefited from heavy use of reinsurance which lowered net losses

32

P/C Reserve Development, 1992-2011E

-6.6

-9.8

13.7

9.9

7.3

-6.7

-9.5

-14.

6-1

6 -15

-5

23.2

11.7

1

-4.1

-9.9

-2.1

-8.3

-2.6

2.3

($20)($15)($10)($5)$0$5

$10$15$20$25$30

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10E 11E

Prio

r Yr.

Res

erve

Rel

ease

($ B

ill)

(6)

(4)

(2)

0

2

4

6

8

Impa

ct o

n Co

mbi

ned

Ratio

(Poi

nts)

Prior Yr Reserve Development ($ Bill) Impact on Combined Ratio (Points)

.Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including this transaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludes development from financial guaranty and mortgage insurance. Source: Barclay’s Capital; A.M. Best.

2009 off to a stronger start with AIG unit sales and

Bermuda consolidation

$ Value of deal up 20% in 2009,

volume down 12%

33

Calendar Year vs. Accident Year P/C Combined Ratio:1992- 2010E1

115.

7

106.

9

108.

4

106.

4

107.

8 110.

1

115.

9

107.

3

100.

1

98.3 10

0.9

92.4

95.5

105.

1

101.

9 105.

9

115.

7

106.

9

108.

4

106.

4

105.

8

101.

6 105.

6 107.

8 110.

0 112.

3

100.

8

96.6

96.0

100.

6

93.9

97.4

105.

5

105.

7 109.

4

105.

6

101.

6

105.

8

80

85

90

95

100

105

110

115

120

92 93 94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09E 10E

Calendar Year Accident YearAccident year results show a

more significant deterioration in underwriting performance.

Calendar year results are helped by reserve releases

33

.Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including this transaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludes development from financial guaranty and mortgage insurance. Source: Barclay’s Capital; A.M. Best.

34

-55-50-45-40-35-30-25-20-15-10-505

101520253035

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 0809

:Q1

Source: A.M. Best, ISO; Insurance Information Institute * Includes mortgage & finl. guarantee insurers

$ B

illio

ns

Insurers earned a record underwriting profit of $31.7B in 2006 and $19.3B in 2007, the largest ever but only the 2nd

and 3rd since 1978. Cumulative underwriting deficit from 1975 through 2008 is $442B.

Underwriting Gain (Loss)1975-2009:H1*

$19.8 Bill underwriting loss in 2008

incl. mort. & FG insurers, -$2.2B in H1:09

34

Large underwriting losses are NOT

sustainable in current investment environment

35

Number of Years With Underwriting Profits by Decade, 1920s –2000s

67

10

8

45

0 0

3

0

2

4

6

8

10

1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s*

Note: Data for 1920 – 1934 based on stock companies only.Sources: Insurance Information Institute research from A.M. Best Data. *2000 through 2008.

Number of Years with Underwriting ProfitsUnderwriting profits were common before the 1980s (40 of the 60 years

before 1980 had combined ratios below 100)—but then they vanished. Not a single underwriting profit was recorded in the 25 years from 1979

through 2003.

35

Capital/Policyholder Surplus (US)

Shrinkage, but Not Enough to

Trigger Hard Market

37

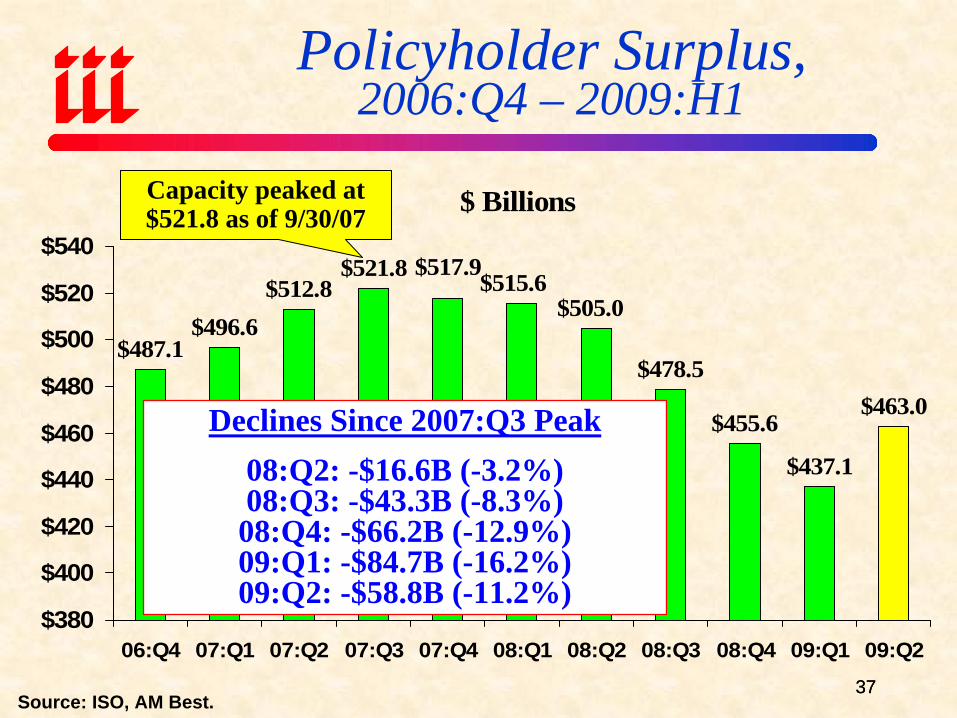

Policyholder Surplus, 2006:Q4 – 2009:H1

$ Billions

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$505.0$515.6

$517.9

$380

$400

$420

$440

$460

$480

$500

$520

$540

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2

Source: ISO, AM Best.

Declines Since 2007:Q3 Peak08:Q2: -$16.6B (-3.2%) 08:Q3: -$43.3B (-8.3%) 08:Q4: -$66.2B (-12.9%) 09:Q1: -$84.7B (-16.2%) 09:Q2: -$58.8B (-11.2%)

Capacity peaked at $521.8 as of 9/30/07

37

38

Ratio of Insured Loss to Surplus for Largest Capital Events Since 1989*

3.3%

9.6%6.9%

10.9%

16.2%13.8%

6.2%

0%2%4%6%8%

10%12%14%16%18%

6/30

/198

9H

urric

ane

Hug

o

6/30

/199

2H

urric

ane

And

rew

12/3

1/93

Nor

thrid

geEa

rthq

uake

6/30

/01

Sept

. 11

Atta

cks

6/30

/04

Flor

ida

Hur

rican

es

6/30

/05

Hur

rican

eK

atrin

a

Fina

ncia

lC

risis

as

of3/

31/0

9**

*Ratio is for end-of-quarter surplus immediately prior to event. Date shown is end of quarter prior to event. **Date of maximum capital erosion; As of 6/30/09 (latest available) ratio = 11.2%.Source: PCS; Insurance Information Institute.

The financial crisis now ranks as the largest

“capital event” over the past 20+ years

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

NWP % changeSurplus % change

*2009 NWP and Surplus figures are % changes for H1:09 vs H1:08Sources: A.M. Best, ISO, Insurance Information Institute

Historically, Hard Markets Follow When Surplus “Growth” is Negative*

Sharp decline in capacity is a necessary but not sufficient

condition for a true hard market

Labor Market Trends

Fast & Furious: Massive Job LossesSap the Economy and P/C Exposure & Can Also Cause EPL Problems

41

2.0

3.04.0

5.0

6.07.0

8.0

9.010.0

11.0

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

January 2000 through October 2009*

Unemployment will likely peak near 10.5 % during this cycle, impacting payroll

sensitive p/c and l/h exposures

Source: US Bureau of Labor Statistics; Insurance Information Institute.

Oct. 2009 unemployment was 10.2%, up 0.4% from Sept. and nearing its

highest level since April 1983 (10.8%)

Unemployment Rate:On the Rise

Average unemployment rate 2000-07 was 5.0%

Previous Peak: 6.3% in June 2003

Trough: 4.4% in March 2007

Oct

-09

42

Monthly Change Employment*(Thousands)

-72-144-122

-160-137-161-128

-175

-321-380

-597

-681-741

-681-652

-519

-303

-463

-304

-154-219-190

-800

-700

-600

-500

-400

-300

-200

-100

0

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Job losses since the recession began in Dec. 2007 total 8.2 mill; 15.7 million people are now

defined as unemployed.

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Info. Institute

Monthly losses in Dec. – May were the largest in the post-WW II period

but pace of loss is diminishing

January 2008 through October 2009

43

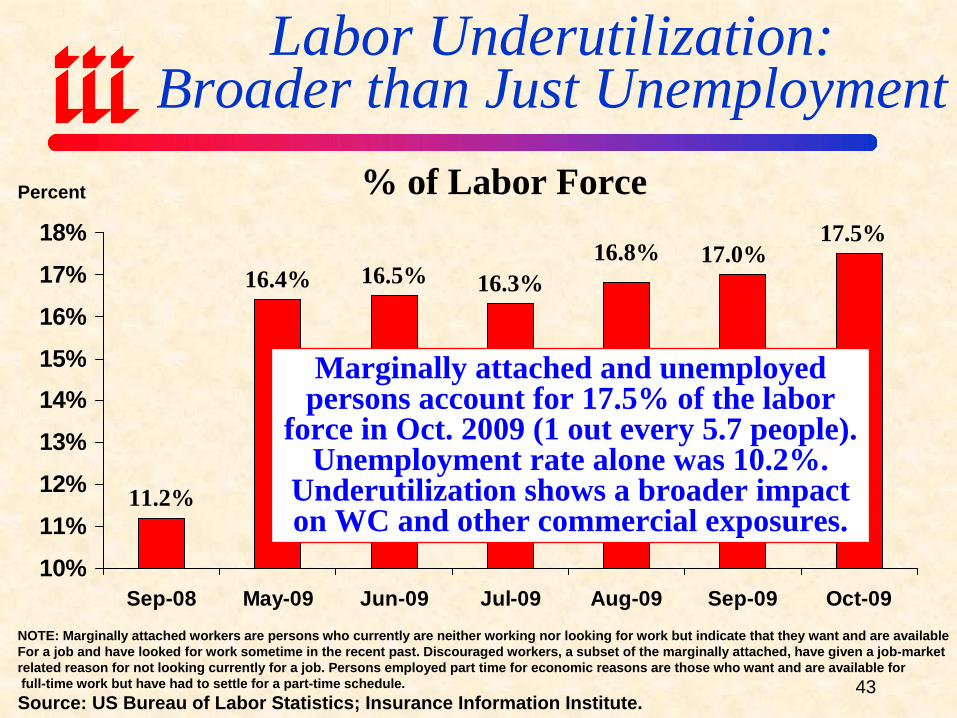

Labor Underutilization: Broader than Just Unemployment

11.2%

16.4% 16.5% 16.3%

17.5%17.0%16.8%

10%

11%

12%

13%

14%15%

16%

17%

18%

Sep-08 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09

Marginally attached and unemployed persons account for 17.5% of the labor

force in Oct. 2009 (1 out every 5.7 people). Unemployment rate alone was 10.2%.

Underutilization shows a broader impact on WC and other commercial exposures.

NOTE: Marginally attached workers are persons who currently are neither working nor looking for work but indicate that they want and are availableFor a job and have looked for work sometime in the recent past. Discouraged workers, a subset of the marginally attached, have given a job-marketrelated reason for not looking currently for a job. Persons employed part time for economic reasons are those who want and are available forfull-time work but have had to settle for a part-time schedule.Source: US Bureau of Labor Statistics; Insurance Information Institute.

Percent % of Labor Force

Unemployment Rates by State, September 2009: Highest 25 States*

10.5

9.8

9.610

.110

.110

.5

9.3

9.1

9.2

8.89.

3

8.9

8.99.

5

11.4

11.6

10.7

10.8

10.9

11.011

.5

13.3

13.0

12.2

15.3

0

2

4

6

8

10

12

14

16

MI NV RI CA SC OR DC FL KY NC AL IL TN OH GA NJ IN MO WA MA MS AZ NY WV ID

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for September 2009, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

The unemployment rate has been rising across the country, but some states are doing much

better than others.

Insurers with heavy footprints in these states will lag behind

6.8

6.7

6.7

6.7

6.76.97.

27.

2

4.84.9

6.27.

07.1

4.2

6.7

8.2

8.3

7.27.37.47.

78.38.

58.

48.

48.8

0

2

4

6

8

10

PA ME AK CT WI DE TX NM LA MN HI MD NH AR CO KS WY IA OK VT MT VA UT NE SD ND

Une

mpl

oym

ent R

ate

(%)

Unemployment Rates By State, September 2009: Lowest 25 States*

The unemployment rate has been rising across the country, but some states are doing much

better than others.

*Provisional figures for September 2009, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Crisis-Driven Exposure Drivers

Economic Obstaclesto Growth in P/C

Insurance

47

Private Sector Business Starts,1993:Q2-2008:Q4*

175

186

174 18

0 186 19

218

818

7 189

186 19

0 194

191

199 20

420

219

519

619

620

620

620

119

2 198

206

206

203

211

205

212

200 20

520

420

419

7 203 20

9

203

192

192

193

201 20

420

221

0 212

209

216 22

0 223

220

220

210

221

212

204

218

210

209

195

187 18

9

201

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Business starts are down 15% in the current downturn, holding back most types of commercial

insurance exposure

*Latest available as of Oct. 2009.Source: Bureau of Labor Statistics: http://www.bls.gov/news.release/cewbd.t07.htm

Thousands189,000 business starts

were recorded 2008:Q4, the lowest

level since 1995

GREEN SHOOTS

Business Mix & Geographic Footprint Will Impact P-C

Insurer Growth Opportunities

49

Hopeful Signs that theEconomic Recovery Is Underway

• Recession Appears to be Bottoming Out, Freefall Has Ended• GDP shrinkage has ended; Economy is expanding• Pace of job losses is slowing• Major stock market indices well off record lows, anticipating recovery• Some signs of retail sales stabilization are evident

• Financial Sector is Stabilizing• Banks are reporting quarterly profits• Many banks expanding lending to very credit worthy people & businesses

• Housing Sector Seems To Be Bottoming Out• Home are much more affordable (attracting buyers)• Mortgage rates are still low relative to pre-crisis levels (attracting buyers)• Freefall in housing starts and existing home sales is ending in many areas

• Inflation & Energy Prices Are Under Control• Consumer & Business Debt Loads Are Shrinking Source: Ins. Info. Inst.

50

11 Industries for the Next 10 Years: Insurance Solutions Needed

GovernmentEducation

Health CareEnergy (Traditional)Alternative Energy

AgricultureNatural Resources

EnvironmentalTechnology

Light ManufacturingExport Oriented Industries

Inflation Trends: Concerns Over

Stimulus Spending and Monetary Policy

Mounting Pressure on Claim Cost Severities?

52

Annual Inflation Rates(CPI-U, %), 1990-2010F

4.9 5.1

3.0 3.22.6

1.51.9

3.3 3.4

1.3

2.5 2.3

3.0

3.8

2.8

3.8

(0.5)

1.9

2.82.92.4

(1.0)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09F10F

Sources: US Bureau of Labor Statistics; Blue Chip Economic Indicators, Oct. 10, 2009 (forecasts).

Inflation peaked at 5.6% in August 2008 on high energy and commodity crisis. The

recession and the collapse of the commodity bubble have produced temporary deflation.

There is so much slack in the US economy that inflation should not be a concern through 2010, but depreciation of dollar is concern longer run.

-$2,000

-$1,500

-$1,000

-$500

$0

$50019

69

1975

1980

1985

1990

1995

2000

2005

2010

2015

2019

Fede

ral D

efic

it

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Def

icit

as %

of G

DP

Federal Deficit ($ Bill) % GDP

US Budget Deficit, 1969-2019F

Deficit expected to hit record $1.8 trillion in 2009 or 13% or GDP, a post-WW II high

Sources: Congressional Budget Office analysis of President’s budget, March 2009; Insurance Information Institute.

Concerns that deficit spending will drive up inflation. This would

harmful to insurance claim severity.

54

$903

.7

$903

.6

$899

.4

$911

.6

$922

.9

$921

.3

$926

.4 $1,1

86.2

$2,2

70.4

$2,1

06.5

$2,1

79.0

$2,0

52.2

$0

$500

$1,000

$1,500

$2,000

$2,500

Dec-06

Mar-07

Jun-07

Sep-07

Dec-07

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Balance Sheet of theFederal Reserve, Dec. 2006- Sept. 2009*

*As of final Friday in each quarter.Source: Federal Reserve: http://www.federalreserve.gov/releases/h41/hist/h41hist1.htm

The size of the Fed’s balance sheet has more than doubled since the crisis began in 2007 from about

$900 billion to $2.2 trillion, fueling inflation concerns.

$ Billions

55

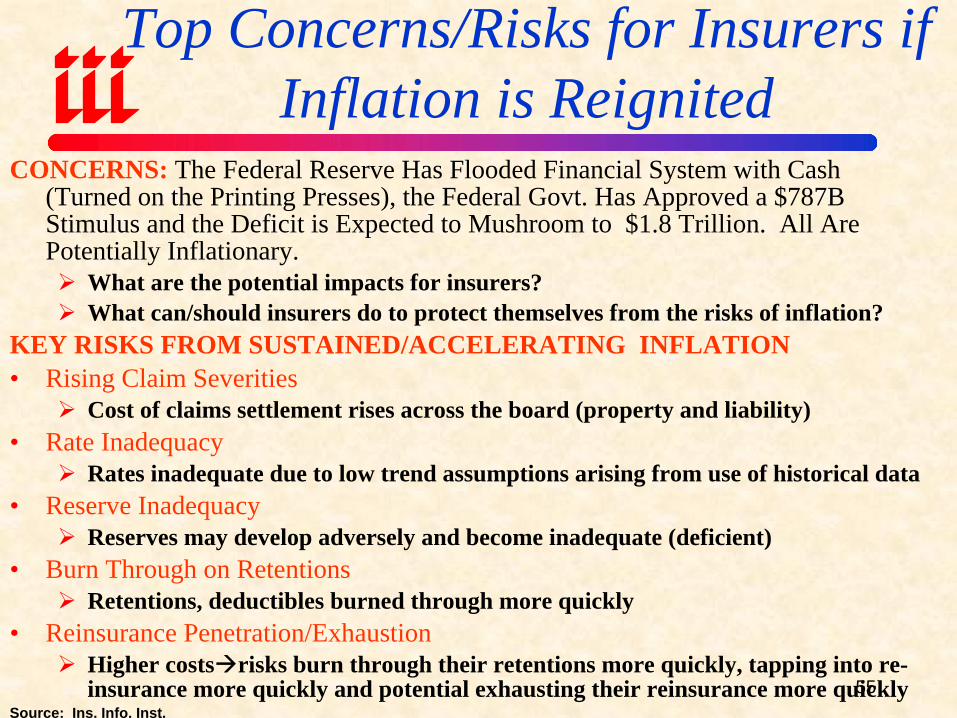

Top Concerns/Risks for Insurers if Inflation is Reignited

CONCERNS: The Federal Reserve Has Flooded Financial System with Cash (Turned on the Printing Presses), the Federal Govt. Has Approved a $787B Stimulus and the Deficit is Expected to Mushroom to $1.8 Trillion. All Are Potentially Inflationary.

What are the potential impacts for insurers?What can/should insurers do to protect themselves from the risks of inflation?

KEY RISKS FROM SUSTAINED/ACCELERATING INFLATION• Rising Claim Severities

Cost of claims settlement rises across the board (property and liability)• Rate Inadequacy

Rates inadequate due to low trend assumptions arising from use of historical data • Reserve Inadequacy

Reserves may develop adversely and become inadequate (deficient)• Burn Through on Retentions

Retentions, deductibles burned through more quickly• Reinsurance Penetration/Exhaustion

Higher costs risks burn through their retentions more quickly, tapping into re-insurance more quickly and potential exhausting their reinsurance more quickly

Source: Ins. Info. Inst.

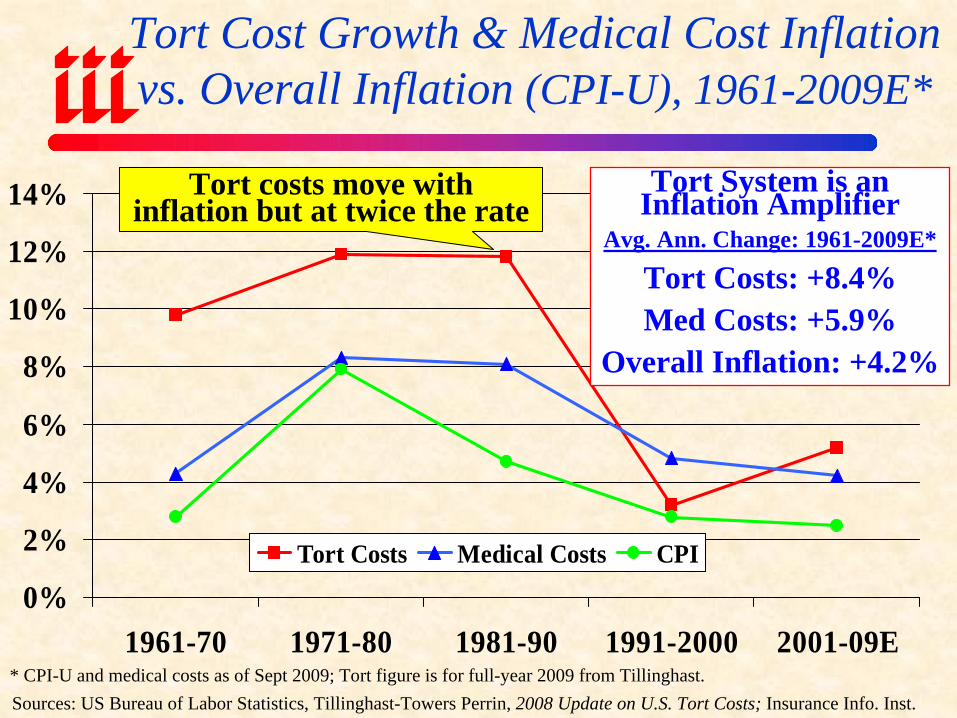

Tort Cost Growth & Medical Cost Inflation vs. Overall Inflation (CPI-U), 1961-2009E*

0%

2%

4%

6%

8%

10%

12%

14%

1961-70 1971-80 1981-90 1991-2000 2001-09E

Tort Costs Medical Costs CPI

* CPI-U and medical costs as of Sept 2009; Tort figure is for full-year 2009 from Tillinghast.

Tort System is an Inflation Amplifier

Avg. Ann. Change: 1961-2009E*

Tort Costs: +8.4%Med Costs: +5.9%

Overall Inflation: +4.2%

Sources: US Bureau of Labor Statistics, Tillinghast-Towers Perrin, 2008 Update on U.S. Tort Costs; Insurance Info. Inst.

Tort costs move with inflation but at twice the rate

Shifting Legal Liability & Tort

EnvironmentIs the Tort Pendulum

Swinging Against Insurers?

58Source: Insurance Information Inst.

Emerging Tort ThreatNo tort reform (or protection of recent reforms) is forthcoming from the current Congress or AdministrationErosion of recent reforms is a certainty (already happening)Innumerable legislative initiatives will create opportunities to undermine existing reforms and develop new theories and channels of liabilityTorts twice the overall rate of inflationHistorically extremely costly to p/c insurance industryLeads to reserve deficiency, rate pressureBottom Line: Tort “crisis” is on the horizon and will be recognized as such by 2012-2014

Important Issues & Threats Facing Insurers: 2009 -2015

Over the Last Three Decades, Total Tort Costs* as a % of GDP Appear Somewhat Cyclical

$0

$50

$100

$150

$200

$250

$300

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

E

2010

E

Tor

t Sys

tem

Cos

ts

1.50%

1.75%

2.00%

2.25%

2.50%

Tor

t Cos

ts a

s % o

f GD

P

Tort Sytem Costs Tort Costs as % of GDP

Sources: Tillinghast-Towers Perrin, 2008 Update on US Tort Cost Trends, Appendix 1A; I.I.I. calculations/estimates for 2009 and 2010

Billions

*Excludes the tobacco settlement, medical malpractice

2009-2010 Growth in Tort Costs as % of GDP is due in part to shrinking GDP

The Nation’s Judicial Hellholes (2008/2009)

Source: American Tort Reform Association; Insurance Information Institute

ALABAMAMacon and

Montgomery Counties

South Florida

ILLINOISCook County West Virginia

Watch ListRio Grande

Valley & Gulf Coast, TX

Madison County, IL

Baltimore, MDSt Louis (the city of), St Louis and

Jackson Counties, MO

Dishonorable Mentions

MA Supreme Judicial CourtMO Supreme

Court

NEVADAClark County (Las Vegas)

NEW JERSEYAtlantic County (Atlantic City)

CALIFORNIALos Angeles

County

Sum of Top 10 Jury Awards, 2004-2008

$ Millions

$1,344.0$615.0$815.0

$2,953.7

$5,158.8

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

2004 2005 2006 2007 2008Source: Insurance Information Institute from LawyersWeekly USA, January 2005, 2006, 2007, 2008 and 2009.

Total of Top 10 awards in 2008 was 74% lower

than in 2004

Number of Top 10 Jury Awards, 1995 - 2008

23 2321

17

8 7 64 3 2 2 2 2 2 1 1

7

0

5

10

15

20

25

TX NY CA FL

MO

DC*

GA AL IL TN LA MD OR SC NV NM NJ

TX, NY and CA lead the U.S. in jumbo-size jury awards

Source: LawyersWeekly USA,, January 1996-2009 issues. *All against Iran for terrorist activity

MEDICAL & HEALTH CARE

COST INFLATION

National Problem & Insurer Cost Driver

Consumer Price Index for Medical Care vs. All Items, 1960-2009*

213.1*

373.3*

0

100

200

300

400

60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

All Items Medical Care

*First Half 2009 data.Source: Department of Labor (Bureau of Labor Statistics).

(Base: 1982-84=100)

Inflation for Medical Care has been surging ahead of general inflation (CPI) for

25 years. Since 1982-84, the cost of medical care has more than tripled.

National Health Expenditures Per Capita, 1960-2018E ($Bill)

$4,5

23$4

,790

$5,1

48$5

,560

$5,9

67$6

,319

$6,6

87$7

,062

$7,4

21$7

,804

$8,1

60$8

,459

$8,8

51$9

,282

$9,7

67$1

0,31

2$1

0,92

9$1

1,59

8$1

2,32

5$1

3,10

1

$356

$2,8

13$1

,100

$148

$3,4

69$4

,104

$4,2

97

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000$9,000

$10,000$11,000$12,000$13,000$14,000$15,000

60 70 80 90 93 97 98 99 00 01 02 03 04 05 06 07 08E

09E

10E

11E

12E

13E

14E

15E

16E

17E

18E

Source: Centers for Medicare & Medicaid Services, Office of the Actuary; Insurance Information Institute.

Health costs on a per capita basis continue to rise rapidly, as health expenditures rise faster

than population growth

National Health Expenditures and Health Expenditures as a Share of GDP,

1960-2018F ($ Billions)$2

8

$1,9

81$2

,113

$2,2

41$2

,379

$2,5

10$2

,624

$2,7

70$2

,931

$3,1

11$3

,313

$3,5

41$3

,790 $4,0

62 $4,3

53

$1,6

03

$1,7

35

$253

$714

$1,3

54

$75

$1,1

91

$1,8

55

$1,4

70

$1,1

25$9

13 $1,2

66

5.2%

7.2%

9.1%

13.7

%

14.5

%15

.3%

15.9

%15

.9%

16.0

%16

.2%

16.6

%

20.3

%

19.8

%19

.3%17

.6%

17.7

%17

.9%

18.0

%18

.2%

18.5

%18

.9%

12.3

% 13.6

%

13.8

% 15.8

%

13.6

%

13.7

%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,00060 70 80 90 93 97 98 99 00 01 02 03 04 05 06 07 08E

09E

10E

11E

12E

13E

14E

15E

16E

17E

18E

Nat

iona

l Hea

lth E

xps

0%

5%

10%

15%

20%

25%

Nat

iona

l Hea

lth E

xp. a

s % o

f GD

P

National Health Expenditures National Health Expenditures as % of GDP

Health care expenditures consumed an estimated

16.6% of GDP in 2008 and are expected to rise to 20.3%

by 2018

Source: Centers for Medicare & Medicaid Services, Office of the Actuary; Insurance Information Institute.

Average Annual Growth in US Per Capital Health Care Costs, 1960-2018F

14.1%

20.9%

15.6%

7.0% 7.9%6.2%

0%

5%

10%

15%

20%

25%

1960-1970 1970-1980 1980-1990 1990-2000 2000-2007 2007-2018

The 1970s were the most inflationary decade for medical costs at nearly

21% per year

Over the net decade health care expenditures will likely

increase well ahead of economic growth and the general pace of inflation

Source: Insurance Information Institute calculations based on data from the Centers for Medicare &Medicaid Services, Office of the Actuary.

Auto Claim Costs Rise Faster than CPI or Health Care Costs

9%

4%

8%

6%

3%4%

0%1%2%3%4%5%6%7%8%9%

10%

Claimed BIEconomic

Loss

Total BIPayment

Claimed PIPEconomic

Loss

Total PIPPayment

CPI CPI-Medical

Sources: Insurance Research Council, Auto Insurance Claims: Countrywide Patterns in Treatment, Cost and Compensation, 2008 Edition; Insurance Information Institute.

Inflation in auto insurance claims is a significant and long-

term cost driver

Claimed BI economic

losses are 3 times the overall

inflation rate

MEDICAL MALPRACTICE

OPERATING ENVIRONMENT

Improved, But Still Vulnerable

103.

7

108.

0

96.4 99

.8 106.

6

107.

9 115.

7

130.

4 136.

0

155

142.

9

128.

2

106.

6

95.0

87.3

83.8

77.6

108.

8 115.

7

107.

0

108.

3

106.

7

106.

0

102.

0

105.

9

108.

0

109.

2 117.

6

106.

1

98.8

97.6

105.

5

89.5

90.9

103.

1

127.

9

70

80

90

100

110

120

130

140

150

160

170

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Medical Malpractice All Lines Combined Ratio

Medical Malpractice Combined Ratio

Source: AM Best, Insurance Information Institute

Insurers in 2008 paid out an estimated $0.77 for every $1

they earned in premiums.As recently as 2002,

med mal insurers paid out $1.55 for

every dollar earned

The dramatic improvement has

restored med mal’s viability

Medical Malpractice: Losses & Expenses Paid vs. Premiums Earned

$ Billions

$4.0

$4.0

$4.1

$4.2 $4

.9

$5.2 $6

.0 $6.3 $6

.9

$8.8

$10.

3

$10.

3

$10.

8

$11.

3

$10.

7

$10.

4

$4.2

$4.1 $5

.2

$4.6

$4.5 $5

.1

$5.3 $6

.0

$7.8 $8

.6

$10.

7

$12.

6

$13.

2

$11.

0

$10.

2

$9.9

$9.0

$8.1

$4.7

$4.8

$4.8

$4.8

$2

$4

$6

$8

$10

$12

$14

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Earned Premiums Losses & Expenses Paid

Source: Computed from A.M. Best data by the Insurance Information Institute

Before reforms took hold in the mid-2000s, premium earned rose ?% while losses and expenses rose 93% over the

period from 1990 through 2008

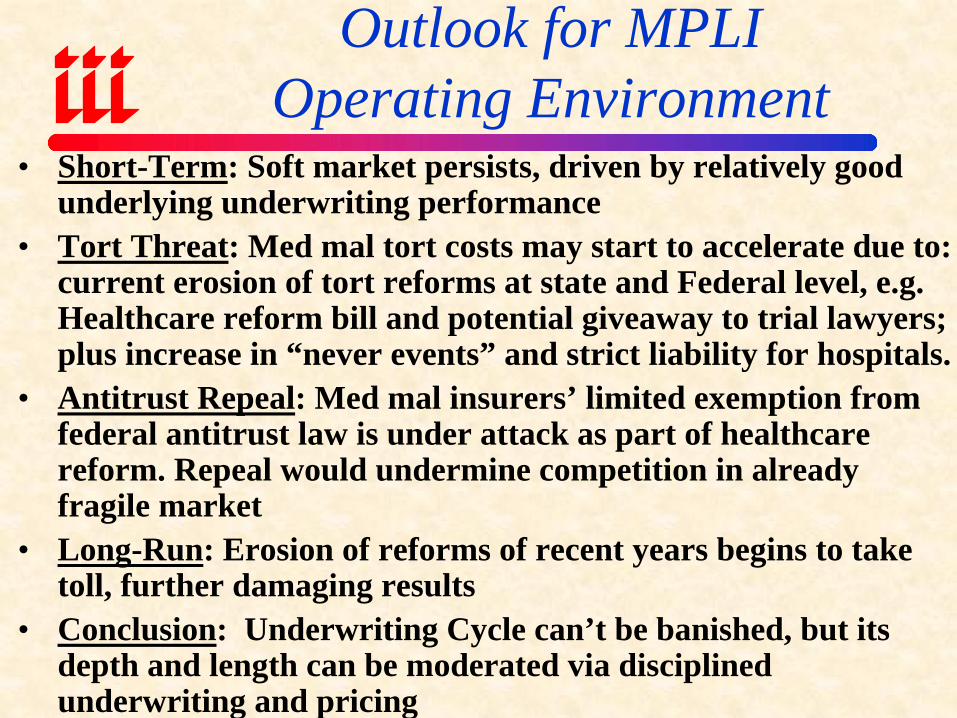

Outlook for MPLIOperating Environment

• Short-Term: Soft market persists, driven by relatively good underlying underwriting performance

• Tort Threat: Med mal tort costs may start to accelerate due to: current erosion of tort reforms at state and Federal level, e.g.Healthcare reform bill and potential giveaway to trial lawyers; plus increase in “never events” and strict liability for hospitals.

• Antitrust Repeal: Med mal insurers’ limited exemption from federal antitrust law is under attack as part of healthcare reform. Repeal would undermine competition in already fragile market

• Long-Run: Erosion of reforms of recent years begins to take toll, further damaging results

• Conclusion: Underwriting Cycle can’t be banished, but its depth and length can be moderated via disciplined underwriting and pricing

The Affordable Health Care for America Act (H.R. 3962) includes the following benefit to the trial bar:

Section 2531, entitled “Medical Liability Alternatives,” establishes an incentive program for states to adopt and implement alternatives to medical liability litigation. [BUT]…… “a state is not eligible for the incentive payments if that state puts a law on the books that limits attorneys’fees or imposes caps on damages.”

Jeopardizes some $54 billion in savings in medical care costs that Congressional Budget Office (CBO) says litigation reform would bring.

Source: Andrew Breitbart, http://biggovernment.com; Congressional Budget Office (CBO)

Healthcare Reform Bill is a Trial Lawyer Dream Come True

Investment Componentof Medical Malpractice

Operating Results

Investment Gain: Med Mal vs.All Commercial Lines*

*As a % of net earned premium. Investment gains consists primarily of interest, dividends andrealized capital gains and losses.

Source: A.M. Best; Insurance Information Institute estimate

12.5

%

14.3

%

14.1

%

16.8

%

16.9

%

15.1

%

16.8

%

14.3

%

9.6%

8.9% 9.4% 10

.3%

10.4

%

10.3

%

5.7%

27.4

%

29.3

%

30.2

%

30.0

%

28.0

%

23.7

% 27.9

%

19.1

%

12.8

%

15.5

%

15.1

%

14.0

% 18.8

%

16.6

%

7.4%

0%

5%

10%

15%

20%

25%

30%

35%

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Commercial Lines Med Mal

Investment returns have generally shrunk since 2000, but are still important. “Heavy Lifting” must be done through underwriting & pricing

Medical Malpractice Investment Gain*

$ Billions

$1.5 $1.5

$2.1

$1.8

$1.5 $1.4$1.2

$1.5

$1.1$0.9

$1.3 $1.2 $1.3

$1.8

$1.5

$0.7

$1.3$1.4 $1.5

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08*Imputed from investment gain data as a % of net earned premium. Investment gains consistsprimarily of interest, dividends and realized capital gains and losses.

Source: A.M. Best; Insurance Information Institute estimate

Investment returns have risen, but poor investment environment today implies “Heavy Lifting” must be done through

underwriting & pricing

Medical Malpractice Tort

Environment

Harvesting the Fruitsof Reform

Medical Malpractice Tort Cost: Growth Continues, Though Modestly

$ Billions

$1.2

$1.4

$1.8

$2.2 $4

.8 $5.8 $6

.8$6

.7$6

.9$7

.3$7

.6 $8.5 $9.2 $1

0.1

$10.

6$1

1.5

$12.

5$1

3.3

$14.

1$1

5.5

$16.

4$1

7.9

$19.

6 $21.

7 $24.

2 $26.

5$2

8.2

$29.

4$3

0.1

$30.

4

$2.7

$3.4

$4.1

$0$2$4$6$8

$10$12$14$16$18$20$22$24$26$28$30$32

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Sources: Tillinghast-Towers Perrin, US Bureau of Labor Statistics, Insurance Information Institute

•Over the period from 1990 through 2007, medical malpractice tort costs rose 230%, more than double the 94% increase in tort costs generally over the same period.

•Over the period from 1975 through 2007, medical malpractice tort costs have increased at an annual rate of ? percent, versus ? percent for all other tort costs.

ME

NH

MACT

PA

WVVA

NC

LATX

OK

NE

ND

MN

MI

IL

IA

ID

WA

OR

AZ

HI

NJ

RI

MDDE

AL

VT

NY

DC

SC

GA

TN

AL

FL

MS

ARNM

KYMOKS

SD WI

INOH

MT

CA

NVUT

WY

CO

Med Mal Crises Across theU.S in the Early 2000s.*

Crisis states at height of 2000s

AMA: Crises reached in 22 states in the 2000s

PR

AK

*The AMA is no longer categorizing states as crisis states.

Source: American Medical Association, February 2008

Source: LawyersWeekly USA, January 15, 2009.

2008 Top Ten Verdicts

Value Issue State

$388 Million Fraud, Intentional Infliction of Emotional Distress

Nevada

$316 Million Breach of Contract Georgia$188 Million Defamation New York$85 Million Premises Liability Pennsylvania$84 Million Negligence, Personal Injury Texas$66 Million Breach of Fiduciary Duty Oklahoma$60 Million Insurance Bad Faith Nevada$55 Million Negligence California$54 Million Wrongful Death Georgia$48 Million Negligence Indiana

2007 Top Ten Verdicts

Source: LawyersWeekly USA, January 22, 2008.

Value Issue State

$109 Million Medical Malpractice New York

$102.7 Million Premises Liability, Death Florida

$55.2 Million Product Liability, Death California

$54 Million Private Air Crash Florida

$54 Million Nursing Home, Death New Mexico

$50 Million DUI Crash Florida

$50 Million Product Liability, Death Alabama

$47.6 Million Prempro Nevada

$47.5 Million Vioxx New Jersey

$45 Million Auto Crash, Death Florida

2002 Top Ten Verdicts

Source: LawyersWeekly USA, January 2003.

Value Issue State

$28 Billion Tobacco (Product Liability) Florida

$2.2 Billion Negligence (Pharmacy Mal) Missouri

$270 Million Personal Injury (Burn) Kentucky

$225 Million Product Liability (Rollover) Texas

$150 Million Tobacco (Product Liability) Oregon

$122 Million Product Liab. (Auto Accident) Virginia

$97.2 Million Business Fraud California

$95.2 Million Med Mal (Birth Injury) New York$91 Million Medical Malpractice New York

$80 Million Med Mal (Birth Injury) New York

$80 Million Prod. Liab/Personal Inj. (Auto) Missouri

2001 Top Ten Verdicts

Source: LawyersWeekly USA, January 2002.

Value Issue State$3 Billion Tobacco California$1 Billion Land Contamination Louisiana$480 Million Private Airplane Crash Florida$312.8 Million Nursing Home Texas$ 256 Million Police Auto Crash Colorado

$116 Million Intellectual Property Theft Virginia$114.9 Million Medical Malpractice New York$108.2 Million Inheritance Dispute Texas$107.8 Million Medical Malpractice New York$94.5 Million Real Estate California

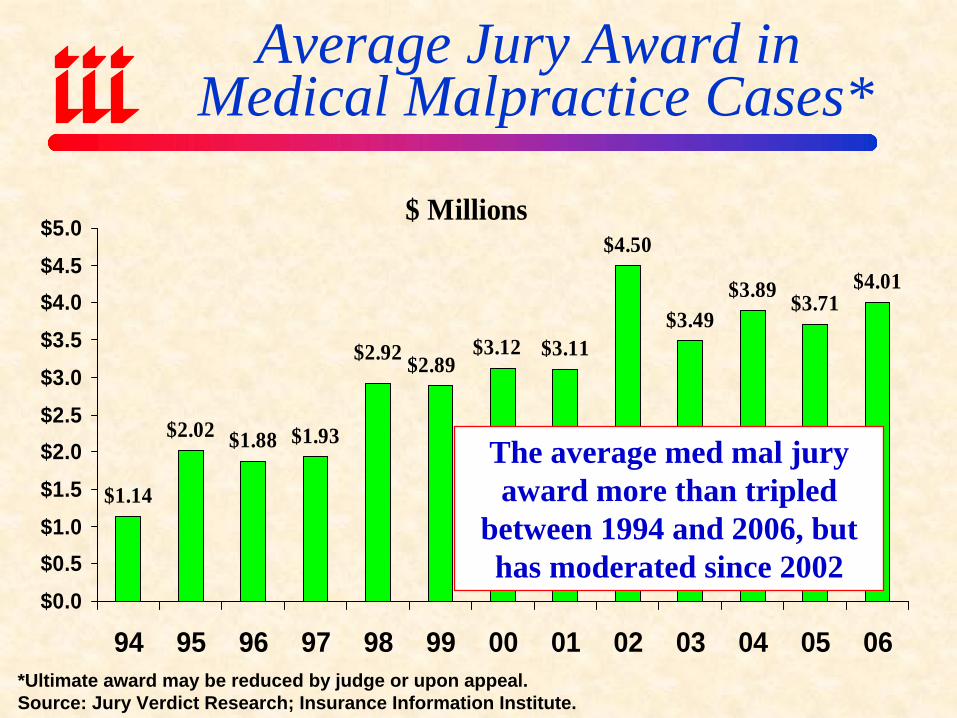

Average Jury Award inMedical Malpractice Cases*

$ Millions

$1.14

$2.02 $1.88 $1.93

$3.11

$4.50

$3.49$3.89 $3.71

$4.01

$2.92 $2.89$3.12

$0.0$0.5$1.0$1.5$2.0$2.5$3.0$3.5$4.0$4.5$5.0

94 95 96 97 98 99 00 01 02 03 04 05 06*Ultimate award may be reduced by judge or upon appeal.Source: Jury Verdict Research; Insurance Information Institute.

The average med mal jury award more than tripled

between 1994 and 2006, but has moderated since 2002

*Verdicts of $1 million or more **2006-2007 is latest available data

Source: Jury Verdict Research; Insurance Information Institute.

Trends in Million Dollar Verdicts*13

%

4%

11% 13%

29% 37

%

48%

59%

5%

17%

11%

41%

53%

17%

6%

14%

15%

33%

51% 57

% 65%

60%

15%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AllLiabilities

VehicularLiability

PersonalNegligence

PremisesLiability

BusinessNegligence

GovernmentNegligence

MedicalMalpractice

ProductsLiability

2001-2003 2004-2005 2006-2007Frequency of multi-million dollar awards is increasing across most types of defendants. In med mal, million dollar-plus awards rose from 48% of all awards from 2001-03 to 57% in 2006-07, well above most other categories.

DIRECTORS & OFFICERS

ENVIRONMENT

Financial Crisis Considerations

Changes in D&O Limits, All Business Classes, 2008

Increased,12%

Decreased,3%Same,

86%

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey

Only 3 percent of participants

reported decreasing their

D&O policy limit in 2008, compared

to 18% in 2007.

Increases in D&O Limits by Classof Business, 2008

46%22%

19%17%

15%15%

14%14%

11%10%10%

9%9%9%

7%7%

12%

0% 50%

UtilitiesMerchandising

Transport. & CommunicationsPetro., Mining & Ag.

Biotech & Pharma.Nondurable Goods

Personal & Business ServicesOther

Health ServicesNonbanking Financial Services

Real Estate, ConstructionDurable Goods

Govt. & Other NonprofitTechnology

BankingEducation

All Business Classes

Some 46% of Utilities reported increasing their

D&O policy limits. Meanwhile, 0%

reported a decrease and 54%

reported no change in their

policy limit.

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey

Changes in D&O Policy Enhancements, All Business Classes, 2008

Increased,54%

Decreased,1%

Same,45%

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey

Only 1 percent of participants reported a

decrease in D&O policy

enhancements in 2008, compared to

3% in 2007.

Increases in Enhancements by Class of Business, 2008

79%77%77%

76%76%

75%75%

71%66%

62%57%

55%46%

38%7%7%

54%

0% 100%

Biotech & PharmaHealth Services

Nonbanking Financial ServicesPersonal & Business Services

Transport. & CommunicationsMerchandising

OtherReal Estate, Construction

Nondurable GoodsDurable Goods

TechnologyBanking

Petro., Mining & Agr.Utilities

EducationGovt. & Other Nonprofit

All Size Groups

Some 79% of Biotech & Pharmaceutical

companies reported an increase in coverage

enhancements to their D&O policies.

Meanwhile, 0% reported a decrease

and 45% no change in policy enhancements.

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey

Prevalence of EPL Coverage by Full-Time Employees, 2008

D&O With EPL,57%

No EPL,10%Stand-Alone EPL,

33%

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey

The percentage of participants

purchasing EPL coverage as part of their D&O policy decreased slightly, from 60% in 2007

to 57% in 2008.

Only 10% of respondents

reporting buying no EPL coverage.

D&O Premium Index(1974 Average = 100)

682746704720720771806793

726619

539503560

720

931

1,2371,113

827805694

1,010

0

200

400

600

800

1000

1200

1400

86 88 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Source: Tillinghast Towers-Perrin, 2008 Directors and Officers Liability Survey.

Average D&O pricing is off at 44% since 2003, after rising

146% from 1999-2003

Key Threats Facing P/C Insurers Amid

Financial CrisisChallenges for the

Next 5-8 Years

94

Important Issues & Threats Facing Insurers: 2010 - 2015

Source: Insurance Information Inst.

Reloading Capital After “Capital Event”Continued asset price erosion coupled with major “capital event” would have led to shortage of capital among somecompaniesPossible Consequences: Insolvencies, forced mergers, calls for govt. aid, requests to relax capital requirementsP/C insurers have come to assume that large amounts of capital can be raised quickly and cheaply after major events (post-9/11, Katrina).

This assumption may be incorrect in the current environmentCost of capital is much higher today (relative “risk-free”rates), reflecting both scarcity & riskImplications: P/C (re)insurers need to protect capital today and develop detailed contingency plans to raise fresh capital & generate internally. Already a reality for some life insurers.

95

Important Issues & Threats Facing Insurers: 2010 - 2015

Source: Insurance Information Inst.

Long-Term Reduction in Investment EarningsLow interest rates, risk aversion toward equities and many categories of fixed income securities lock in a multi-year trajectory toward ever lower investment gainsFed actions in Treasury markets keep yields lowMany insurers have not adjusted to this new investment paradigm of a sustained period of low investment gainsRegulators will not readily accept it; Many will reject itImplication 1: Industry must be prepared to operate in environment with investment earnings account for a smaller fraction of profitsImplication 2: Implies underwriting discipline of a magnitude not witnessed in this industry in more than 30 years. Yet to manifest itself.Lessons from the period 1920-1975 need to be relearned

96Source: Insurance Information Inst.

Regulatory Overreach Principle danger is that P/C insurers get swept into vast federal regulatory overhaul and subjected to inappropriate, duplicative and costly regulation (Dual Regulation)Strong arguments for Optional Federal Charter, but…Pushing for major change is not without risk in the current highly charged political environmentDangers exist if feds get their nose under the tentStatus Quo is viewed as unacceptable by allDisunity within the insurance industryInsurance & systemic risk—Who is important?Impact of regulatory changes will be felt for decadesBottom Line: Regulatory outcome is uncertain and risk of adverse outcome exists

Important Issues & Threats Facing Insurers: 2010 – 20??

97

Health Insurance Reform Debate—Potential Spillover Impacts on P/C Insurers

• 24-Hour Coverage ProposalWould roll WC and med components of auto into natl. health care plan

• Rollback of McCarran-Ferguson ActWould repeal or restrict for health and medical malpractice insurersSlippery slope—Med Mal is a p/c line; Congress will not hesitate to breach M-F for other p/c lines in the future to show its ire over an issue (e.g., after major cat)

• Exclusion of Med Mal Reform from Health Care BillShows powerful influence of trial bar with Congress/Administration

• FTC granted authority to conduct studies “related to insurance” –All Lines!• Reporting of Claims• Adjustments to Medicare Fee Schedules• Patient “Bill of Rights” or Vague Standards of Care• Cost Shifting into WC, Auto from Health System

WC/Auto Medical: more lucrative from provider perspective• “Windfall” Profit Taxes? Additional Premium Taxes?• Executive Compensation Restrictions?• Public “Option” in P/C Lines—Nat Cat/Wind?• Perception that Feds Regulate Insurance Industry Taking Root

FINANCIAL STRENGTH &

RATINGSIndustry Has Weathered

the Storms Well

99

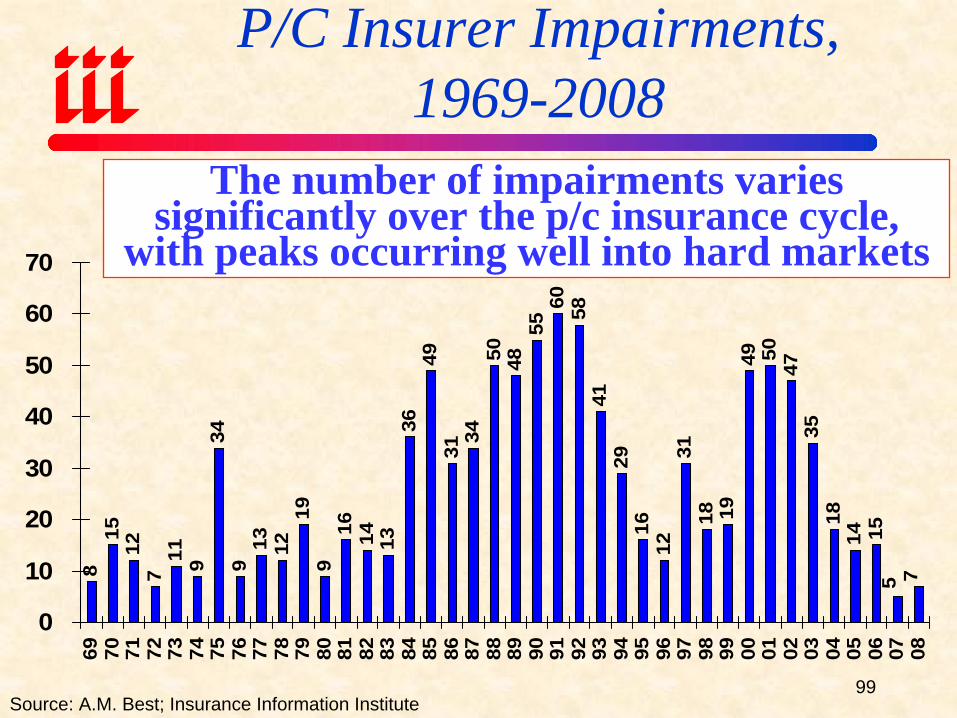

P/C Insurer Impairments,1969-2008

815

127

11 934

913 12

199

16 14 1336

4931

3450 48

5560 58

4129

1612

3118 19

49 5047

3518

14 15

75

0

10

20

30

40

50

60

70

69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

The number of impairments varies significantly over the p/c insurance cycle,

with peaks occurring well into hard markets

Source: A.M. Best; Insurance Information Institute

100

P/C Insurer Impairment Frequency vs. Combined Ratio, 1969-2008

90

95

100

105

110

115

120

69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Com

bine

d R

atio

0.00.20.40.60.81.01.21.41.61.82.0

Impa

irmen

t Rat

e

Combined Ratio after DivP/C Impairment Frequency

Impairment rates are highly

correlated with underwriting

performance and reached record lows in 2007/08

Source: A.M. Best; Insurance Information Institute

2008 impairment rate was a record low 0.23%, second only to the 0.17% record low in 2007 and barely one-fourth the 0.82% average since 1969

101

Summary of A.M. Best’s P/C Insurer Ratings Actions in 2008*

Under Review, 63 , 4.3%

Upgraded, 59 , 4.0%

Initial, 41 , 2.8%

Other, 59 , 4.0%

Affirm, 1,183 , 81.0%

Downgraded, 55 , 3.8%

*Through December 19.Source: A.M. Best.

101

Despite financial market turmoil, high cat losses

and a soft market in 2008, 81% of ratings actions by A.M. Best

were affirmations; just 3.8% were downgrades

and 4.0% upgrades

P/C insurance is by design a resilient in business. The dual threat of financial

disasters and catastrophic losses are

anticipated in the industry’s risk

management strategy.

102

Historical Ratings Distribution,US P/C Insurers, 2008 vs. 2005 and 2000

Source: A.M. Best: Rating Downgrades Slowed but Outpaced Upgrades for Fourth Consecutive Year, Special Report,November 8, 2004 for 2000; 2006 and 2009 Review & Preview. *Ratings ‘B’ and lower.

A/A-48.4%

D0.2%C++/C+

1.9%

E/F2.3% A++/A+

11.5%

C/C-0.6%

B++/B+28.3%

B/B-6.9%

2008 2005

P/C insurer financial strength has improved since 2005 despite financial crisis

A/A-52.3%

A++/A+9.2%

B++/B+26.4%

Vulnerable*12.1%

A/A-60.0%

A++/A+10.8%

B++/B+21.3%

Vulnerable*7.9%

2000A++/A+ and A/A- gains

103

Reasons for US P/C Insurer Impairments, 1969-2008

Source: A.M. Best: 1969-2008 Impairment Review, Special Report, Apr. 6, 2008

Deficient loss reserves and inadequate

pricing are the leading cause of

insurer impairments,

underscoring the importance of

discipline. Investment

catastrophe losses play a much smaller role.

Reinsurance Failure3.7%

Rapid Growth14.3%

Misc.9.1%

Affiliate Impairment

7.9%

Sig. Change in Business

4.2%

Deficient Loss

Reserves/In-adequate Pricing38.1%

Investment Problems

7.0%

Alleged Fraud8.1%

Catastrophe Losses7.6%

Critical Differences Between P/C

Insurers and BanksSuperior Risk Management Model

& Low Leverage Makea Big Difference

105

How Insurance Industry Stability Has Benefitted Consumers

BOTTOM LINE:• Insurance Markets—Unlike Banking—Are Operating

Normally• The Basic Function of Insurance—the Orderly Transfer

of Risk from Client to Insurer—Continues Uninterrupted• This Means that Insurers Continue to:

Pay claims (whereas 145 banks have gone under as of 11/6/09)The Promise is Being Fulfilled

Renew existing policies (banks are reducing and eliminating lines of credit)Write new policies (banks are turning away people and businesses who want or need to borrow)Develop new products (banks are scaling back the products they offer)Compete Intensively (banks are consolidating, reducing consumer choice)

Source: Insurance Information Institute105

106

• Emphasis on UnderwritingMatching of risk to price (via experience and modeling)Limiting of potential loss exposureSome banks sought to maximize volume and fees and disregarded risk

• Strong Relationship Between Underwriting and Risk BearingInsurers always maintain a stake in the business they underwrite, keeping “skin in the game”at all timesBanks and investment banks package up and securitize, severing the link between risk underwriting and risk bearing, with (predictably) disastrous consequences—straightforward moral hazard problem from Econ 101

• Low LeverageInsurers do not rely on borrowed money to underwrite insurance or pay claims There is no credit or liquidity crisis in the insurance industry

• Conservative Investment PhilosophyHigh quality portfolio that is relatively less volatile and more liquid

• Comprehensive Regulation of Insurance OperationsThe business of insurance remained comprehensively regulated whereas a separate banking system had evolved largely outside the auspices and understanding of regulators (e.g., hedge funds, private equity, complex securitized instruments, credit derivatives—CDS’s)

• Greater TransparencyInsurance companies are an open book to regulators and the public

Source: Insurance Information Institute106

Reasons Why P/C Insurers Have Fewer Problems Than Banks:

A Superior Risk Management Model

107

Insurance Information Institute On-Line

THANK YOU FOR YOUR TIME AND

YOUR ATTENTION!

107