the oil council's june 2010 edition of 'drillers and dealers

TRANSCRIPT

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 1/38

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 2/38

‘Drillers and Dealers’

Published by:

The Oil Council

“Engaging Oil & Gas Communities World - wide”

Foreword

‘Drillers and Dealers’ is our pioneering free monthly e-magazine for the upstreamindustry. It is entirely focused on sharing insight, analysis, intelligence and thoughtleadership across the E&P sector.

We hope you enjoy reading the articles our guest authors have so kindly contributed.

Ross Stewart CampbellChief Executive Officer,The Oil CouncilT: +44 (0) 20 7067 [email protected]

Iain PittChief Operating Officer,The Oil CouncilT: +27 (0) 21 700 [email protected]

Contact The Oil Council

For general enquiries and information on how to work with The Oil Council contact:

Ross Stewart Campbell, Chief Executive Officer, [email protected]

For enquiries about Corporate Partnerships, attending one of our Assemblies andadvertising in a future edition of ‘Drillers and Dealers’ contact:

Vikash Magdani, EVP, Corporate Development, [email protected]

Guillaume Bouffard, VP, Business Development, [email protected] Lafont, VP, Business Development, [email protected]

To receive free monthly editions of ‘Drillers and Dealers’ , as well as, discounts to allour upcoming Assemblies please visit our website now (www.oilcouncil.com) to sign upas a Member of The Oil Council. Membership is FREE to oil and gas executives.

Copyright, Commentary and IP Disclaimer

***Any content within this publication cannot be reproduced without the express permission of The Oil Council and the respective contributing authors. Permission can be sought by contacting

the authors directly or by contacting Iain Pitt at the above contact details. All comments within this magazine are the views of the authors themselves unless otherwise. attributed to their company / organisation.

They are not associated with, or reflective of, any official capacity, or any other person in their company / organisation unless so attributed.***

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 3/38

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 4/38www.oilcouncil.com/weca [email protected]

Forging Global Partnerships

to Capitalise on a New Era of

Oil & Gas Investment

The dening event for the global oil and gas, nance

and investment communities

• Industryleadersdiscussthedynamicsanddrivingfactorsoftoday’sneweconomicandnanciallandscapes

• OilandgasCEOsandCFOstalkonthechallengestheynowfaceinensuringnewgrowthagainstabackdropofmarketuncertainlyandincreasedvolatilityandregulation

• Bankingexpertsexplorethefutureofenergybanking,nancialreformandmarketliquidityandtheirimplicationsonoilandgascompanies

• Aplethoraofinvestors,capitalprovidersandnancierstacklethebigissuesfacingoilandgasexecutives:newinvestmentstrategies,capitalexpenditure,

accessingthecurrentpublicandprivatemoneymarkets,capitalraisingtrends,M&AandA&Ddealowandexplorationstrategies• PlusspecialsessionsfocussingonAfricaandtheMiddleEast,RussiaandtheCIS,

thefutureofoileldservicesprovision,theroleofprivateequityandemergingindustryleaders

LeadPartners:

Partners:

Mark GyetvayDeputy Chairman and CFO,

NOVATEK

Dr Christof RühlGroup Chief Economist and Vice

President,

BP

Jeffrey CurrieGlobal Head, Commodities

Research,

Goldman Sachs

Featuringover80oftheindustry’smostinuentialspeakers,including:

Dr Francisco Blanch

Global Head, Commodities

Research,Bank of America-Merrill Lynch

David MacFarlaneFinanceDirector,

DanaPetroleumplc

Said Arrata

Chairman and CEO,

Sea Dragon Energy

Oil & Gas Company Executives Register Today for only £995!

Special Industry Delegation Discounts Also Available!

Maarten Wetselaar

Executive Vice President Finance,Upstream International,

Shell

Tim Chapman

Managing Director and Head,International Energy,RBC Capital Markets

23 – 25 November 2010

MillenniumGloucesterHotel

andConferenceCentreLondon,UnitedKingdom

WORLD ENERGY CAPITAL ASSEMBLY

Oil Council

T AYLOR-DE JONGH

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 5/38

www.oilcouncil.com

Executive Q&A

With

Andrew Austin,CEO

IGas Energy Plc.

Talking withRoss Stewart Campbell, CEO, The Oil Council

Date: 10 th

June 2010

Ross Stewart Campbell (RSC) fromThe Oil Council: Andrew, many thanks for joining us to share your

thoughts on today’s markets. Tocover off introductions can you quickly introduce yourself and IGasEnergy?

Andrew Austin from IGas Energy(AA): Hi Ross, IGas Energy is anunconventional gas businesslisted on AIM. All our assets are inthe UK, principally across theNorth West of England. We have

drilled seven wells to date and are currentlyproducing from our pilot production site at DoeGreen, situated between Liverpool and

Manchester.

RSC: Looking first at the global picture of unconventional gas Andrew we’re seeing a growing number of new ventures shoot up across the globefollowing the ‘shale gale’ in the US and significant finds in Australia. Once considered a new industry fad unconventionals are now a new industry market in their own right.

What are your thoughts on this increasing globalisation (and appreciation) of unconventional gas and Coal Bed Methane (CBM)? How large amarket can unconventional gas become? And how large an impact are recent technological

advancements having on the growth and development of the market?

AA: We’ve already seen the effect that Shale hashad on the market for gas in North Americareflected in the reduced number of LNG importsto the US. In Australia CBM has changed thelandscape for gas to Asia by the sheer size andspeed of its growth.

In Europe currently there is something of a landgrab occurring for unconventional gas and I amsure that it will form a material part of the supplymix here over the next decade.

RSC: We’ve witnessed massive investment in thedevelopment of unconventional and CBM supply

chains in the US. How do the supply chains for CBM in other counties compare and how far advanced isthe UK’s supply chain? What timeline are we looking

at for the UK to build a sufficiently effective CBM supply chain?

AA: Clearly the supply chain is more developedin other countries. However there are currently anumber of groups that are looking atestablishing themselves as suppliers to theindustry. We‘re now seeing rigs being orderedfor use in the UK with service companies lookingto now aggregate the drilling programs of thedifferent players.

Furthermore we’re also seeing interest from thewater drilling industry and construction firms

looking to move into the market. In short it isearly days but it’s growing.

RSC: One of the big advantages to CBM is theability for some countries to decrease their dependency on foreign gas imports. How might CBM influence the future dynamics of energy security and geopolitics? And how important an ingredient will CBM be in future UK energy mix?

AA: I think that energy security is a growingtheme Ross. If you add to this the reducedcarbon impact of utilising local gas rather thanimported gas, domestic unconventional gas is avery interesting place to be.

I also believe that gas powered electricitygeneration is going to have an increased roll inthe UK as the coal fired stations near the end of their life and new nuclear struggles withpermitting issues. So a material amount of gasthat is close to customers is going to be a veryimportant ingredient in any future energy mix.

RSC: Moving to focus more on IGas now Andrew many small-cap companies have endured a rocky road in the past 12-18 months.

How resilient has IGas been in this period, both in

successfully navigating the choppy economic and financial seas, and in positioning yourself for new growth at the end of the testing storm?

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 6/38

www.oilcouncil.com

AA: Over the last three years we have increasedour resources markedly. We now have a 2Ccontingent resource of 807bcf.

We have tried to always be ready for the nextchallenges in our business and have ensured wehave enough funding available to take us frompilot production through to our first fullproduction site in 2011.

Running a small-cap company always haschallenges but I am convinced that we havepositioned ourselves extremely well for deliveryover the next couple of years

RSC: Your focus has always been onshore and offshore UK, do you see that changing at all Andrew? Are you looking to expand internationally, perhaps into Europe to look at new CBM playsthere? If not are you looking to increase your UK portfolio in the near future either through new

exploration, acquisitions or farm-ins?

AA: We see ourselves as UK focused and so arenot looking to expand internationally.

As to deals, we always look at opportunities asthey present themselves! However, our mainfocus is on delivering on what we have. Gettingthat right is our number one priority.

RSC: The UK of course has an important advantageof been very close to local and regional energy markets. Do you foresee your gas been sold regionally, nationally or within the wider European

markets?

AA: We are looking at supplying directly tocustomers in our core areas and via the gas grid.

RSC: What company milestones in the coming 6-12 months should our readers look out for?

AA: The next steps are pilot production at Keelein Staffordshire and we are on-site there now.Next will be a pilot site on our Point of Ayr acreage in North Wales.

In 2011 we are looking at establishing our firstfull commercial production site.

In the meantime we continue to evaluate thepotential of our acreage for shale gas and willupdate the market on this in due course.

RSC: Many of the readers will be interested in thefinancial position of IGas, can you shed some light Andrew on your finances: debt/equity ratio and available cash reserves. How healthy is your balance sheet in ensuring your can successfully finance your future developments?

AA: We currently have no debt and at the end of 2009 had £17.5M in cash on our balance sheet,

enough for our programs for 2010 and 2011.

RSC: You have a strong institutional investor base Andrew, how important to companies like IGas ishaving patience and knowledgeable investorsonboard?

AA: We are seeing an increase in interest fromoverseas investors, particularly those that havehad experience of the M&A activity around Shalegas in the US and CBM in Australia.

RSC: For our investor readers why should they look at IGas as their next investment and a new stock intheir portfolio?

AA: 807bcf of recoverable gas close tocustomers, demonstrated by pilot production.We have the gas; we now are about delivering itto surface and onto the market.

RSC: If I may Andrew I’ll wrap up by asking your one-word opinion (bullish, bearish or uncertain) on

the future of the following. Bullish, Bearish or Uncertain?

RSC: David Cameron

AA: Uncertain

RSC: New Nuclear Power Capacity in the UK by 2025

AA: Bearish

RSC: $100 oil before the end of 2010

AA: Bearish

RSC: Recovered Gas Prices by the end of 2010

AA: Bullish

RSC: North Sea Oil

AA: Bearish

RSC: North Sea Gas

AA: Uncertain

RSC: AIM

AA: Bullish

RSC: US Unconventional Gas Focussed Independents

AA: Uncertain

RSC: European Unconventional Gas Focussed Independents

AA: Bullish

RSC: Thanks Andrew, more info can of

course be found at: www.igasplc.com

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 7/38

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 8/38

www.oilcouncil.com

Korea and other countries) occurring in theCanadian oilsands, which again is another source of capital that certain companies havebeen able to tap. We’re also seeing an uptick inprivate financings, and hedge funds are slowlycoming back to the table in terms of privateequity investments.

Given the availability of financing, M&A activityhas been relatively quiet as the number of distressed/strategic M&A deals is less than ayear ago.

RSC: What common types of legal challenges areyour clients currently facing when looking to raisecapital, or close a transaction?

JP: Here in Canada, issuers who have tapped themarkets face few issues as the speed andefficiency of the bought deal system makes lifeeasy. New issuers (whether IPO or first time

short form prospectus) face issues to ensuretheir disclosure record is both up to date andaccurate, as well as, logistically managing thespeed of timing on a bought deal.

One of the benefits of having an experienced lawfirm involved in the process is that they are ableto assist companies with this process and keepthem up to speed.

RSC: Many companies are finding current market conditions tough to successfully launch an IPO.There’s been a lot of pain here in Europe (not just the LSE) with companies struggling to get their IPOs

away and when they do they are often at heavily discounted prices and at the mercy of damaging trading strategies. How much IPO activity has therebeen to date this year in Canada? Is there appetitefrom your investment community in new IPOs on theTSX/TSX-V?

JP: We’ve certainly seen several IPOs over thepast 6-12 months in Canada, including asignificant IPO by Athabasca Oil Sands of $1.35billion, which we was involved in. There wererelatively few IPOs in 2009 (Blakes beinginvolved in two of the largest ones involvingGenworth Financial and Capital Power Corp), butthis has been changing in 2010.

However, the recent downturn in the markets hashad an impact on some announced IPOs (suchas Lulu Ltd. which recently announced it waspulling its previously announced IPO). We’recertainly optimistic that the 3

rdand 4

thquarters

of 2010 will bring several new companies to

“We’re certainly optimistic that the 3 rd

and 4 th quarters of 2010 will bring several new companies to market,

including several international issuers.”

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 9/38

www.oilcouncil.com

market, including several international issuers.

RSC: How much international interest are you now seeing in companies looking at the TSX/TSX-V interms of both IPOs and secondary listings? Is this anincrease on last year?

JP: We’re seeing significantly more interest Rossfrom international issuers in the Canadianmarkets compared to 2009. The unavailability of capital over the past few years has forcedcompanies to look outside their traditionalsources and Canada has seen the benefit of this.

Companies are coming to appreciate the stabilityand relatively ease of capital raising in theCanadian markets. There’s certainly a learningcurve that companies will need to face whenlooking at listing in Canada, but once that ispassed, the process and system are relativelyeasy and (hopefully) painless.

RSC: In your own (non-biased) opinion Janan would you say the Canadian markets are currently the best place in the world to consider an IPO or a secondary listing for an oil and gas company?

JP: We definitely think it’s an excellent place for companies to consider when looking at IPO or secondary listing.

The TSX and TSX-Venture have always been veryresource focussed and investors in the NorthAmerican market have always understoodresource companies. One of the difficulties

international issuers have faced in the past is theperception that North American investors don’tunderstand issuers with foreign assets andresultantly their valuations were not fullyreflective of the issuer’s assets.

We think this has now changed and internationalissuers with a good story will be able to findwilling investors and appropriate valuations.From a cost perspective, we believe Canada isincredibly cost-effective.

We always tell issuers that are looking at Canadathat they need to invest in the offering andsubsequent listing by meeting with investors andstaying connected. This is one of the keys tomaintaining a successful listing in Canada.

RSC: Some of our readers might not be aware of recent developments in Canadian energy and banking legislation and regulation.

Could you share with us any updates or development to either regional/national energy legislation or new banking regulation now being

implemented by your government that could impact the dynamics of the Canadian markets and dampen possible new foreign investment?

JP: We don't think there is anything at this pointthat would hamper foreign investment or international issuers looking to list in Canada.

We’ve seen recently announced changes to our royalty regime to encourage the drilling of wellsrelating to "unconventional resources" (i.e. shalegas and CBM) or to those drilling horizontalwells, which appears to be a positive.

Recently we’ve seen several significant foreigninvestments (i.e. Sinopec's CAN$4.65 billioninvestment in oilsands being an example thatBlakes was recently involved in) and we expectthis trend to continue in the future.

RSC: We've seen a swathe of Canadian companiesinvesting heavily into Latin America, many of them

enjoying huge success, particularly in Columbia.What are your thoughts on the region and the legal challenges it poses for companies?

JP: South America is an extremely interestingarea and is expanding at a rapid pace. SeveralCanadian based companies have enjoyed greatsuccess in South America, particularly Colombia(Gran Tierra, Petrominerales and Petrolifera toname a few).

The Colombian regulatory regime seemsrelatively stable and encourages foreigncompanies. There’s always some concern in

these regimes in terms of political stability, butthis appears to be a relatively small risk inColombia.

Companies of course will need to haveexperienced people on the ground in order tomake these plays successful.

RSC: Thinking in terms of a legal checklist for addressing the challenges today’s markets present what new practices would you encourage (and evenurge) companies to incorporate to ensure they areoptimally protected to ride out this current financial storm?

JP: Clearly fiscal prudence is what companiesneed to consider. Capital is available, but people

“We’re seeing a

significant amount of foreign investment

(principally from China,but also Korea and other

countries) occurring in the Canadian oilsands ”

“ A strong business plan and solid assets are crucial to ride out any financial volatility.”

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 10/38

www.oilcouncil.com

are looking for more defined uses of proceedsand companies will have less flexibility than theyhave had in the past in deploying their capital. Astrong business plan and solid assets are crucialto ride out any financial volatility.

RSC: Of course it’s hard to escape the recent BP disaster in today’s news. What legal ramifications doyou think this disaster will have on oil and gascompanies in the short, medium and long term?

JP: A very difficult questions to answer Ross! Ithink the biggest ramification is the perceptionon the environmental unfriendliness of oil andgas, and I think specifically here about oilsands.

The oil spill is extremely unfortunate and tragicand no doubt steps need to be taken to addressthe concerns relating to offshore rigs, however the negative impact it will have on people'sperception of the oil and gas industry as a wholewill take a great deal of time and effort toreverse.

RSC: Before we wrap up looking at your own firm in

today’s financial climate, what are you own plans for growth in 2010? Are their new corporatedevelopments the market should look out for?

JP: We’ve a strong focus on internationalactivities. We’ve been in Beijing for over 10 yearsand London for over 20 years and have recentlyopened offices in Bahrain and an affiliated officein Saudi Arabia. We think international

investment in Canada will increase and havebeen committed to this for many years.

RSC: I’ll wrap up now by asking your one-word opinion (bullish, bearish or uncertain) on the future of the following. Bullish, Bearish or Uncertain?

RSC: The Canadian Economy

JP: Bullish

RSC: Stephen Harper

JP: Bullish

RSC: Offshore Drilling in North America

JP: Uncertain

RSC: TSX-V

JP: Bullish

RSC: AIM

JP: Bullish

RSC: Oilsands

JP: Bullish

RSC: Janan, thank you very much for your time, asalways good talking with you. If any of our readerswish to contact Janan they can do so via thefollowing email: [email protected]

About Janan: Janan Paskaran is a Senior Associate practising in the areas of corporate and securities law. He

spent two years in the Firm's London office from 2006 to 2008 before returning to the Calgary office. Janan hasextensive experience representing public and private issuers in a wide variety of financing, business combinationand acquisition transactions, including both private and publicly traded issuers. He has been involved innumerous cross-border debt and equity financings and mergers and acquisitions. Janan also provides counsel with respect to securities compliance matters, commercial transactions and corporate finance procedures and governance.

About Blakes: For more than 150 years, Blakes has proudly served many of Canada's and the world's leading businesses and organizations. The Firm has built a reputation during that time as both a leader in the businesscommunity and in the legal profession – leadership that continues to be recognized to this day. Thanks to our clients and the challenging legal work they generate, Blakes is recognized as "Canada's Law Firm of the Year" for 2009 by Who's Who Legal and, for the second year running, as "Law Firm of the Year: Canada" in the PLC Which Lawyer? Awards. We also consistently rank as one of the top Canadian firms on the Bloomberg, ThomsonReuters and mergermarket M&A league tables in terms of transactional value or number of deals for Canadianannounced transactions. We have more than 550 lawyers in offices in Montréal, Ottawa, Toronto, Calgary,

Vancouver, New York, Chicago, London, Bahrain, Beijing and associated offices in Al-Khobar and Shanghai. For more information on Blakes please visit: www.blakes.com

“Recently we’ve seen several significant foreign

investments and we expect this trend to

continue in the future.”

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 11/38www.oilcouncil.com/ecaa [email protected]

Forging Global Partnerships

to Capitalise on a New Era of

Oil & Gas Investment

The dening event for the global oil and gas, nanceand investment communities

• Industryleadersdiscussthedynamicsanddrivingfactorsoftoday’sneweconomicandnanciallandscapes

• OilandgasCEOsandCFOstalkonthechallengestheynowfaceinensuringnewgrowthagainstabackdropofmarketuncertainlyandincreasedvolatilityandregulation

• Bankingexpertsexplorethefutureofenergybankinganditsimplicationsonoilandgascompanies

• Aplethoraofinvestors,capitalprovidersandnancierstacklethebigissuesfacingoilandgasexecutives:newinvestmentstrategies,capitalexpenditure,

accessingthecurrentpublicandprivatemoneymarkets,capitalraisingtrends,M&AandA&Ddealowandexplorationstrategies

• Plusspecialsessionsfocussingonprivateequity,theindependentoilandgasmarkets,thefutureofunconventionalsandLatinAmerica

Jan Stuart Global Oil Economist,

Macquarie Group

Ed MorseGlobal Head, Commodity Research,

Credit Suisse

Tom PetrieVice Chairman,

Bank of America–Merrill Lynch

Featuringover80oftheindustry’smostinuentialspeakers,including:

Matt Simmons

Chairman,

Simmons & Company International

John Schiller Jr Chairman and CEO,

Energy XXI

Luis Giusti

CEO,

Alange Energy Corp

Oil & Gas Company Executives Register Today for only $999!Special Industry Delegation Discounts Also Available!

Ken Hersh

CEO,NGP Energy Capital Management

John Moon

Managing Director, Morgan Stanley Private Equity

26-28October,2010

EventiHotel,

NewYorkCity,USA

ENERGY CAPITAL ASSEMBLY AMERICAS

Oil Council

LeadPartners:

Partners:

T AYLOR-DE JONGH

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 12/38

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 13/38

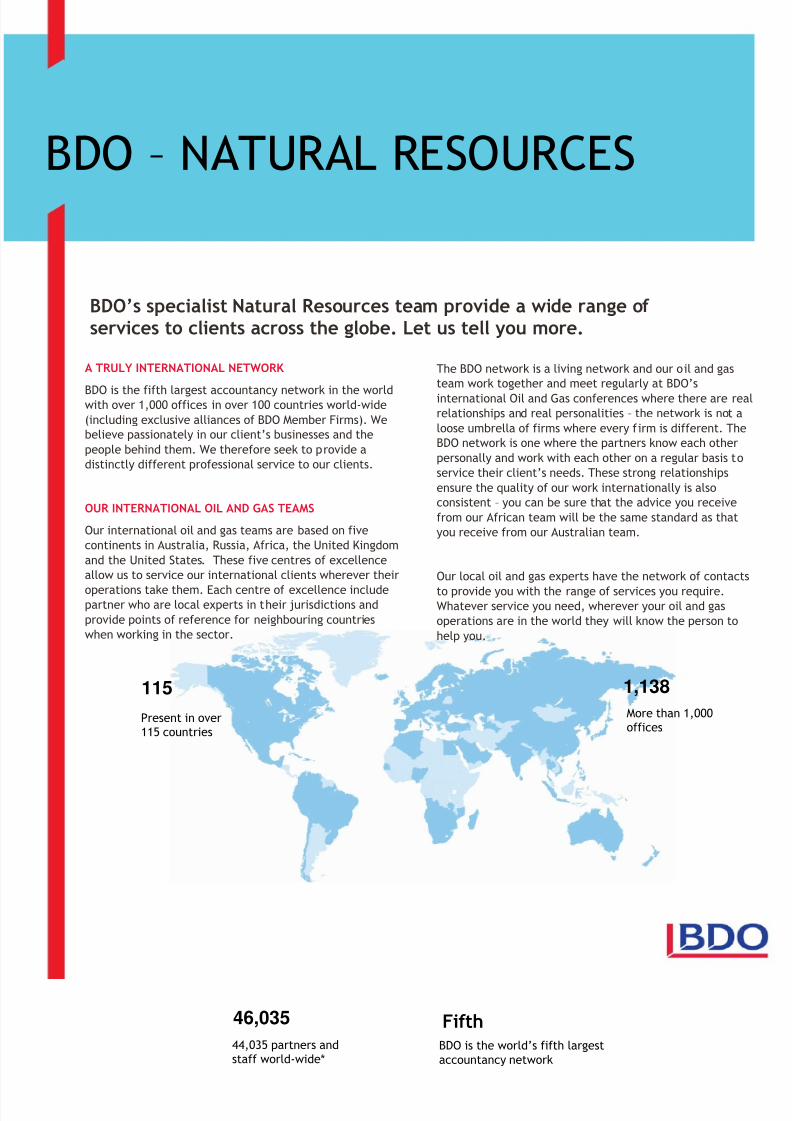

BDO – NATURAL RESOURCES

BDO’s specialist Natural Resources team provide a wide range of services to clients across the globe. Let us tell you more.

A TRULY INTERNATIONAL NETWORK

BDO is the fifth largest accountancy network in the worldwith over 1,000 offices in over 100 countries world-wide

(including exclusive alliances of BDO Member Firms). We

believe passionately in our client’s businesses and the

people behind them. We therefore seek to provide a

distinctly different professional service to our clients.

OUR INTERNATIONAL OIL AND GAS TEAMS

Our international oil and gas teams are based on five

continents in Australia, Russia, Africa, the United Kingdom

and the United States. These five centres of excellence

allow us to service our international clients wherever their

operations take them. Each centre of excellence includepartner who are local experts in their jurisdictions and

provide points of reference for neighbouring countries

when working in the sector.

BDO is the world’s fifth largest

accountancy network

Fifth

1,138

More than 1,000offices

Present in over115 countries

46,035

44,035 partners andstaff world-wide*

115

The BDO network is a living network and our oil and gas

team work together and meet regularly at BDO’s

international Oil and Gas conferences where there are real

relationships and real personalities – the network is not a

loose umbrella of firms where every firm is different. The

BDO network is one where the partners know each other

personally and work with each other on a regular basis to

service their client’s needs. These strong relationships

ensure the quality of our work internationally is also

consistent – you can be sure that the advice you receive

from our African team will be the same standard as that

you receive from our Australian team.

Our local oil and gas experts have the network of contacts

to provide you with the range of services you require.Whatever service you need, wherever your oil and gas

operations are in the world they will know the person to

help you.

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 14/38

This publication has been carefully prepared, but should be seen as general guidance only. You should not act upon the information contained in this publication without obtainingspecific professional advice. Please contact BDO LLP to discuss these matters in the context of your particular circumstances. BDO accepts no responsibility for any loss incurred as a

result of acting on information in this publication.BDO LLP operates across the UK with some 3,000 partners and staff. BDO LLP is a UK limited liability partnership and a UK Member Firm of BDO International. BDO Northern Ireland is aseparate partnership operating under a licence agreement. BDO International is a world-wide network of public accounting firms, called BDO Member Firms. Each BDO Member Firm is anindependent legal entity world-wide and no BDO Member Firm is responsible for the acts and omissions of another member. The network is coordinated by BDO Global Coordination B.V.,incorporated in the Netherlands with its statutory seat in Eindhoven (trade register registration number 33205251) and with an office at Boulevard de la Woluwe 60, 1200 Brussels,Belgium, where the International Executive Office is located.

BDO LLP and BDO Northern Ireland are both separately authorised and regulated by the Financial Services Authority to conduct investment business.

BDO is the brand name for the BDO International network and for each of the BDO Member Firms.

BDO LLP and BDO Northern Ireland are the Data Controllers for any personal data that they hold about you. We may disclose your information, under a confidentiality agreement, to aData Processor (Shamrock Marketing Ltd). To correct your personal details or if you do not wish us to provide you with information that we believe may be of interest to you, pleasetelephone (Great Britain - 0870 567 5678 or Belfast - 028 9043 9009).

Copyright © January 2010 BDO LLP. All rights reserved.

Website: www.bdo.co.uk

CORPORATE FINANCE

Our international Corporate Finance teams provide a wide

range of specialist services ranging from flotations (LSE,

TSX, NYSE, ASX, AIM), due diligence and professional

advice in relation to mergers and acquisitions. We are also

able to provide assistance to companies looking to raise

private equity finance and fund private finance initiatives.

FORENSIC SERVICES

BDO has a dedicated and highly experiences international

forensic accounting team who have the insight to help you

to solve the most challenging disputes and litigation. We

have a wealth of knowledge and technological expertise to

provide you with the right advice to meet your forensic

accounting needs.

We have a strong track record of working with clients in

the sector. Our teams forensic accounting services include

expert witness services, alternate dispute resolution,

fraud and financial crime, asset investigation andrecovery, anti-money laundering provisions, technology

forensics and valuations.

WHO TO CONTACT

If you are interested in discussing any of our services

further, require more information on BDO or you require

assistance in an overseas jurisdiction please contact:

ASSURANCE

Our international assurance practice provides our clients

with a robust external audit reporting service which

utilises a consistent audit methodology throughout the

world. Our audit teams spend the majority of their time

working with clients in the sector therefore they

understand your business and the issues you face.

If it is more than a statutory audit you require we also

provide specialist audit services covering PSC contracts, JV

requirements or governmental fiscal regimes, on top of

International Financial Reporting Standard conversions,

technology risk reporting and internal audit services.

TAXATION

Companies operating in the oil and gas sector often have

complex cross-border structures and employees who spend

long periods of time overseas. It is also becomingincreasingly important for companies to ensure they

minimise their exposure to costly tax regimes through

effective tax planning and for them to also look to

incentivise key employees in a tax efficient way.

Our tax teams provide a wide range of specialist services

covering international tax planning, compliance services

through to advising on the structure of share schemes,

remuneration and reward planning.

OUR INTERNATIONAL OIL AND GAS SERVICE

STREAMS

BDO can provide you with the wide range of services

you would expect from a major international firm

including:

• Assurance

• Taxation

• Corporate finance, and

• Forensic services.

All our services are tailored to the specific needs

and circumstances of our clients.

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 15/38

www.oilcouncil.com

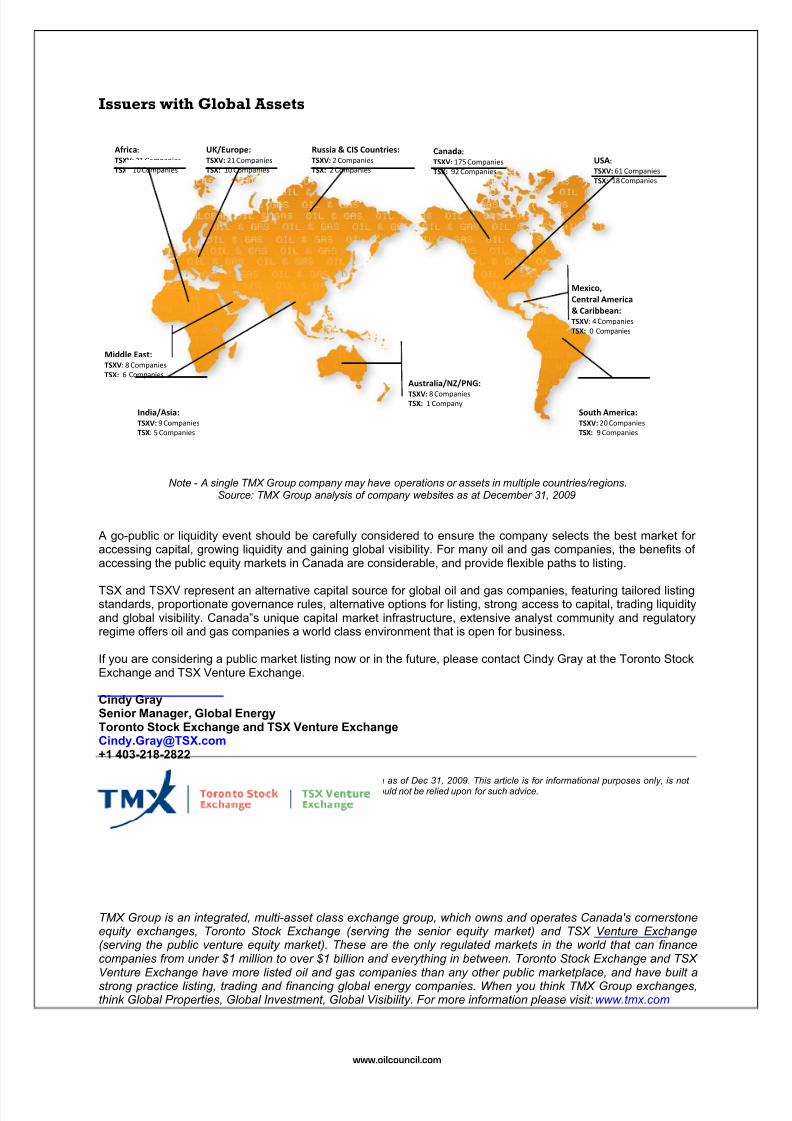

A Capital Opportunity for Global Oil & Gas

Written by the Global Energy Team of Toronto Stock Exchange and TSX Venture Exchange

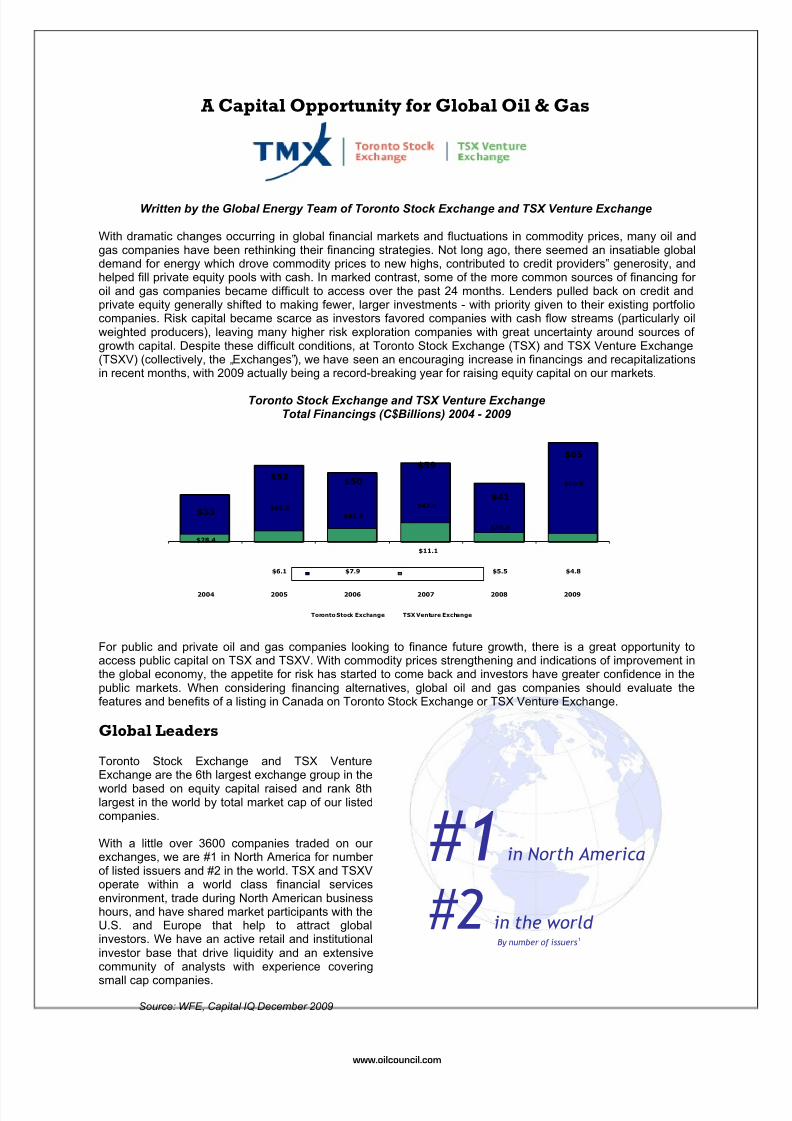

With dramatic changes occurring in global financial markets and fluctuations in commodity prices, many oil andgas companies have been rethinking their financing strategies. Not long ago, there seemed an insatiable globaldemand for energy which drove commodity prices to new highs, contributed to credit providers‟ generosity, andhelped fill private equity pools with cash. In marked contrast, some of the more common sources of financing for oil and gas companies became difficult to access over the past 24 months. Lenders pulled back on credit andprivate equity generally shifted to making fewer, larger investments - with priority given to their existing portfoliocompanies. Risk capital became scarce as investors favored companies with cash flow streams (particularly oilweighted producers), leaving many higher risk exploration companies with great uncertainty around sources of growth capital. Despite these difficult conditions, at Toronto Stock Exchange (TSX) and TSX Venture Exchange(TSXV) (collectively, the „Exchanges‟), we have seen an encouraging increase in financings and recapitalizationsin recent months, with 2009 actually being a record-breaking year for raising equity capital on our markets.

Toronto Stock Exchange and TSX Venture ExchangeTotal Financings (C$Billions) 2004 - 2009

For public and private oil and gas companies looking to finance future growth, there is a great opportunity toaccess public capital on TSX and TSXV. With commodity prices strengthening and indications of improvement inthe global economy, the appetite for risk has started to come back and investors have greater confidence in thepublic markets. When considering financing alternatives, global oil and gas companies should evaluate thefeatures and benefits of a listing in Canada on Toronto Stock Exchange or TSX Venture Exchange.

Global Leaders

Toronto Stock Exchange and TSX VentureExchange are the 6th largest exchange group in the

world based on equity capital raised and rank 8thlargest in the world by total market cap of our listedcompanies.

With a little over 3600 companies traded on our exchanges, we are #1 in North America for number of listed issuers and #2 in the world. TSX and TSXVoperate within a world class financial servicesenvironment, trade during North American businesshours, and have shared market participants with theU.S. and Europe that help to attract globalinvestors. We have an active retail and institutionalinvestor base that drive liquidity and an extensivecommunity of analysts with experience covering

small cap companies.

Source: WFE, Capital IQ December 2009

#1 in North America

#2 in the world By number of issuers1

$28.4

$46.2

$41.8

$47.6

$35.3

$60.0

$6.1 $7.9

$11.1

$5.5 $4.8

$33

$52$50

$59

$41

$65

2004 2005 2006 2007 2008 2009

Toronto Stock Exchange TSX Venture Exchange

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 16/38

www.oilcouncil.com

Tailored Listing Standards

The listing standards on TSX and TSXV are tailored to companies of various stages of development and take intoaccount more than just market cap or profitability metrics.

o Canada’s proportionate governance standards are right sized for the market and our rules and regulations facilitate faster, often less costly capital raises.

o A listing on TSX or TSXV exposes the issuer not only to Canadian capital pools, but U.S. and international pools as well.

o Global companies interested in listing on TSX or TSXV are not required to be incorporated or haveoperations in Canada; nor are companies required to have Canadian officers or directors.

o Companies wanting to go public in Canada are afforded further flexibility because we offer several options for listing in addition to a traditional IPO.

Companies that are ready to go public can select the method of listing that makes the most sense for their company and current market conditions.

Methods for Going Public on Toronto Stock Exchange or TSX Venture Exchange

Access to Capital Companies listed on TSX and TSXV have historically been able to access the capital needed to grow their business -- even for financing international operations and projects in higher risk locations. Our Exchanges areunique in that we offer listing criteria and transaction policies that are specific to oil & gas, and have Exchangestaff with relevant energy business experience. Canada‟s securities and regulatory environment facilitaterelatively fast equity raisings within a framework that affords investors transparency, integrity and high corporategovernance standards, without over-burdening the issuers.

Oil & Gas Equity Capital Raised on Toronto Stock Exchange and TSX Venture Exchange (C$B)

2002 2003 2004 2005 2006 2007 2008 2009

$4.1B

$10.5B

$5.3B

$11.7B

$2.6B

$10.4B

$9.2B

Secondary Offerings Private Placements IPOs

$8.2B

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 17/38

www.oilcouncil.com

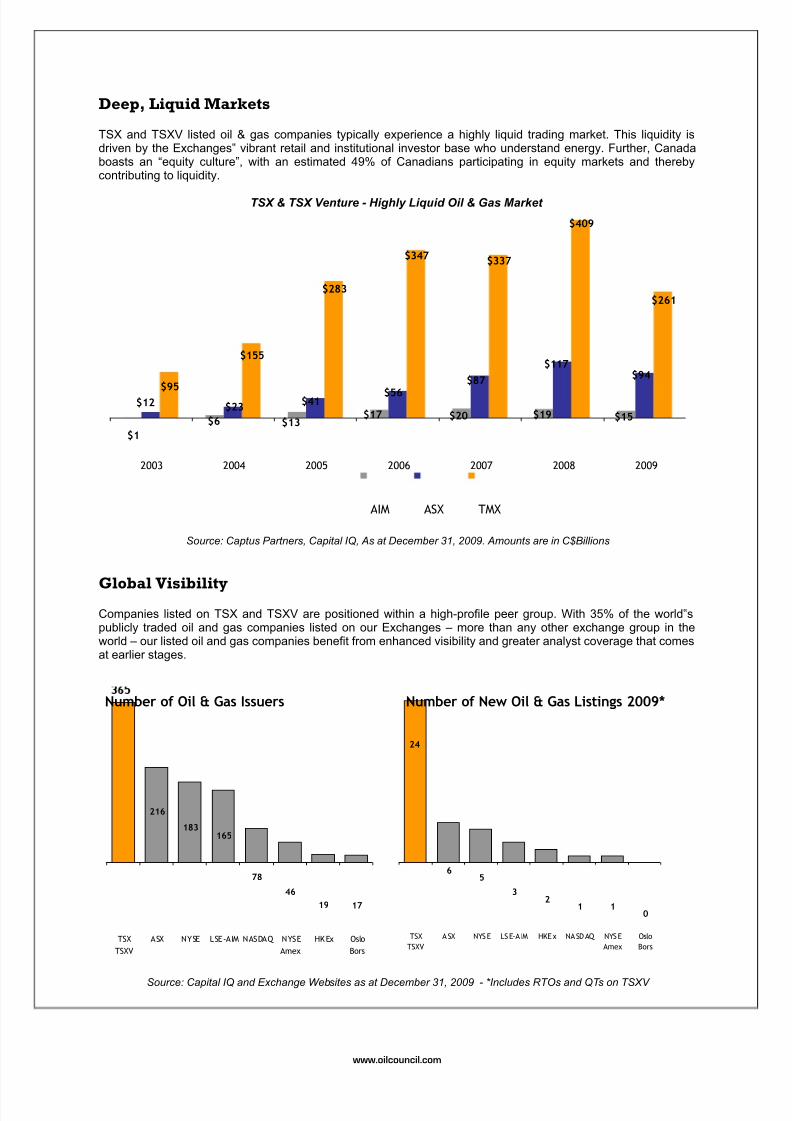

Deep, Liquid Markets

TSX and TSXV listed oil & gas companies typically experience a highly liquid trading market. This liquidity isdriven by the Exchanges‟ vibrant retail and institutional investor base who understand energy. Further, Canadaboasts an “equity culture”, with an estimated 49% of Canadians participating in equity markets and therebycontributing to liquidity.

TSX & TSX Venture - Highly Liquid Oil & Gas Market

Source: Captus Partners, Capital IQ, As at December 31, 2009. Amounts are in C$Billions

Global Visibility

Companies listed on TSX and TSXV are positioned within a high-profile peer group. With 35% of the world‟spublicly traded oil and gas companies listed on our Exchanges – more than any other exchange group in theworld – our listed oil and gas companies benefit from enhanced visibility and greater analyst coverage that comesat earlier stages.

Source: Capital IQ and Exchange Websites as at December 31, 2009 - *Includes RTOs and QTs on TSXV

216

183165

78

46

19 17

TSX

TSXV

ASX NYSE LSE-AIM NAS DAQ NYS E

Amex

HK Ex Oslo

Bors

65

32

1 10

24

TSX

TSXV

A SX NYS E LS E-A IM HKE x NA SD AQ NYS E

Amex

Oslo

Bors

$1

$6 $13$17 $20 $19 $15

$12 $23$41 $56

$87

$117$94

$95

$155

$283

$347 $337

$409

$261

2003 2004 2005 2006 2007 2008 2009

AIM ASX TMX

Number of Oil & Gas Issuers Number of New Oil & Gas Listings 2009*

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 18/38

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 19/38

www.oilcouncil.com

Analyst

Insights European E&Ps – Hope and Exploration

We think that exploration is being inconsistently valued across the mid-cap E&Ps. With the market in arelatively bullish mood and seemingly willing to factor in a higher long-term oil price, the E&Ps as agroup have found themselves with more cash to drill due to both higher oil prices and an apparentlygreater willingness among investors to fund drilling. 2010 exploration budgets amongst our coverageuniverse are set to increase 20% on average YoY.

However, we believe that too much of the value has gone into high-risk, high-reward andgeographically-restricted exploration programmes. In general terms, 1 in 5 exploration wells are

successful. In frontier terms, this decreases to 1 in 10. We favour backing what we view as reasonablypriced exploration programmes that are either well diversified across numerous prospects or that do nothave success priced in yet.

European Unconventional Gas – A Tough Nut to Frac

We considered whether it is possible to repeat the recent North American success with unconventionalgas resources in Europe and concluded that significant obstacles must first be overcome. We requiremore technical data points from drilling activity, but identify the presence of multiple farmstead holders,environmental management of scarce water resources and the lack of a developed services industry asindicating higher exploitation costs in Europe.

As such, we opine that unconventional gas exploitation will require oil-indexed gas prices to be

sustained in Europe. In any event, it appears unlikely that unconventional gas exploitation will have thesame transformational affect in Europe as it has had in the North American market in the last decade andwe expect Europe to continue to increasingly rely on imported pipeline gas and LNG in the face of declining domestic production.

Credit Suisse AG: As one of the world's leading banks, Credit Suisse provides its clients with private banking,investment banking and asset management services worldwide. Credit Suisse offers advisory services,comprehensive solutions and innovative products to companies, institutional clients and high-net-worth private clients globally, as well as retail clients in Switzerland. Credit Suisse is active in over 50 countries and employs approximately 46,700 people. Credit Suisse is comprised of a number of legal entities around theworld and is headquartered in Zurich. The registered shares (CSGN) of Credit Suisse's parent company, Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York.Further information can be found at: www.credit-suisse.com

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 20/38

www.oilcouncil.com

‘On the Spot ’ with our Question of the Month (Part One)

“We’re experiencing another period of volatility

and uncertainly in the financial markets. Do you foresee this as a small market blip or the start of

something more significant, perhaps a new

capital crunch, or a double dip recession?”

““I could possibly make a meaningful projection if someone could tell me; if the „GreeceRescue‟ by the EU will be successful (highly unlikely): if Spain and Portugal will be sucked into the same financial disaster (quite likely): if the President and Congress continue on the path of ever larger budget deficits and stratospheric debt, moving the US in the direction of the European problem countries (very likely): if the insane Dictator of North Korea will expand the torpedoing of a South Korean Navy Vessel into a full-blown war (flip a coin), etc,etc. In the absence of that information my SWAG is that it will get a lot worse before we canexperience a relatively stable and growth-supporting environment.”

... Franz Ehrhardt, CEO, CASCA Consulting LLC (Oil Council Committee Member)

“There are many financial and economic imbalances that need significant correction before wecan look forward to a period of stability, let alone predictability. For all the talk of thegovernment budget deficits, credit-starved businesses and poorly capitalised banks (with their under-performing assets and continuing bad loan exposure), we can now add anunprecedented layer of sovereign debt risk. There is much speculation about the default risk and economic weakness of many countries in the Eurozone, which has served to deflect a lot of attention away from what is arguably the more challenging economic problems of the US.

My feeling is that all these factors will lead to a prolonged period of volatility, perhaps lasting 5

to 10 years more, and it will take resolute and determined government action to restore theeconomic fundamentals and investor confidence. We need to get used to the idea that we arein for a roller-coaster ride for many years to come. Flexibility and adaptability will be key toride out the bumps ahead.”

... Robert Lambert, CEO, GB Petroleum Ltd (Oil Council Member)

“We are experiencing and will continue to experience significant volatility in capital markets for the coming months. Markets are nervous and so respond extremely to news flows. We see this as a continuation of the credit crunch rather than a new credit crunch as you describe it. It goes without saying that we have experienced asevere correction and while we may be bouncing along the bottom it will be a long slow road to recovery especially in the developed economies of Europe and USA where public and private debt are an important drag and growth is slow to re-emerge. Commercial Banks in particular are forced to contract their balance sheets,

which removes what had been an easy source of liquidity to the industry. Overall debt gearing will continue to bemore challenging and large scale projects will need bilateral and multilateral agencies to fill the void left by banks”

... Keith O’Donnell, Head, Natural Resources (EMEA), KBC (Oil Council Member)

“This current period of volatility and uncertainty is partly driven by concerns about Europeandebt. We see these concerns as much more than a market blip; however, we don‟t expect themto lead to another credit crunch and double dip recession, at least not in North America. Europefaces several years of painful fiscal retrenchment that at the very least will greatly hold back itsexpansion and likely spur a recession in several Eurozone countries.

It‟s the contagion effect that is much more worrisome and is the unknown variable that may ultimately cause a pan-European recession. The recent sharp selloff of North American oil and gas equities is in response to the collapse of the WTI crude oil price over the last few weeks.This drop in crude pricing is partly due to WTI-specific factors rather than a broad-based decline in global oil and product markets. The less severe decline in Brent pricing reflects both the decline in the North American crude oil

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 21/38

www.oilcouncil.com

price and the current European uncertainty, amongst other complex factors. Global crude benchmarks and petroleum product prices have recently suggested that end-use demand for crude oil (i.e., petroleum products) isimproving, especially in emerging markets. This should set the stage for higher world-wide crude oil prices withNorth America leading the way.”

... Adam Janikowski, Vice President, Investment Banking, BMO Capital Markets (Oil Council Member)

“There is undoubtedly a fear of a double dip recession with increased country debt in Europe amajor contributory factor. Governments have borrowed on a massive scale to shore up fragileeconomies. The measures to be undertaken to service and ultimately repay this debt will affect every single individual and will lead to significant public sector cuts resulting in increased unemployment and service cuts.

While the chance of a double dip recession was thought to be slight in early 2010 investors arenow giving greater credence to the possibility. Worryingly, as recently evident, investors havebolted to the safe haven of short-dated US government bonds. This flight from risk was a

precursor to the collapse of Lehmans and it is clear that the markets are continuing to sense trouble for theremainder of 2010 and maybe beyond.”

... Alan Ross, Senior Manager, Oil & Gas, Lloyds Banking Group (Oil Council Partner)

“It is certainly not a small market blip, but the market, and more importantly governments, arenow more agile in responding to the potential global crisis (part two) and mitigating contagioncoming from the sovereign debt crisis. Already we see a capital and credit crunch, which isthen followed by a lower oil price. I don‟t think the crisis and the recession will repeat itself withthe correct measures but this should be considered a potential threatening aftershock,cracking the emergency foundations which have been put in place after the 2008 crash.”

... Ennio Senese di Sisto, Executive Partner, Energy, Accenture (Oil Council Member)

“US prospects for economic growth in 2010 look good and a V-shaped recovery is still thebase case among most economists. However, the impact of the Euro crisis, if not

contained, will have a major impact on the global economy and could lead to another recession in 2011. The pendulum can swing either way, i.e. a continued but modest recovery,or, a 2011 recession caused by worsening developments in the Eurozone.”

... Dr Herman Franssen, President, International Energy Associates (Oil CouncilCommittee Member)

“Volatility and uncertainty are essentially becoming a trend, with increased lower and middlemarket activity, M&A, and debt financing efforts ultimately heralding consolidation in thewake of a disjointed economy. While these are harbingers for continued uncertainty in themarkets, they are also indicators of anticipated recovery. However, international default will no doubt continue to run its course well into 2011, only to be met by the rise of emerging markets, triggering a shift of wealth and exploitation.”

... Chris Valenti, Energy Investment Banker, Starlight Investments, LLC (Oil CouncilMember)

“The market volatility seen in May was an overdue correction in the markets‟ expectations for economic recovery. The problems that can constrain growth remain largely unsolved. The huge public debt levels, record unemployment and rising inflation cannot be controlled and contained easily especially as the developed world has become accustomed to a high standard of living.

The Greek near-default situation and the warnings from other countries such as Portugal,Ireland and Spain, have served as reminders of the grave dangers still present in the financial system. Despite governmental plans for budget cut-backs and austerity measures, it will bedifficult to convince the public that their belts need tightening; it will take time and pain, political

and economic, even to start such programmes. Capital will be constrained as many of the leading banks have to

make provisions for losses on government paper, in addition to tighter regulation and operational constraint imposed by the authorities.

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 22/38

www.oilcouncil.com

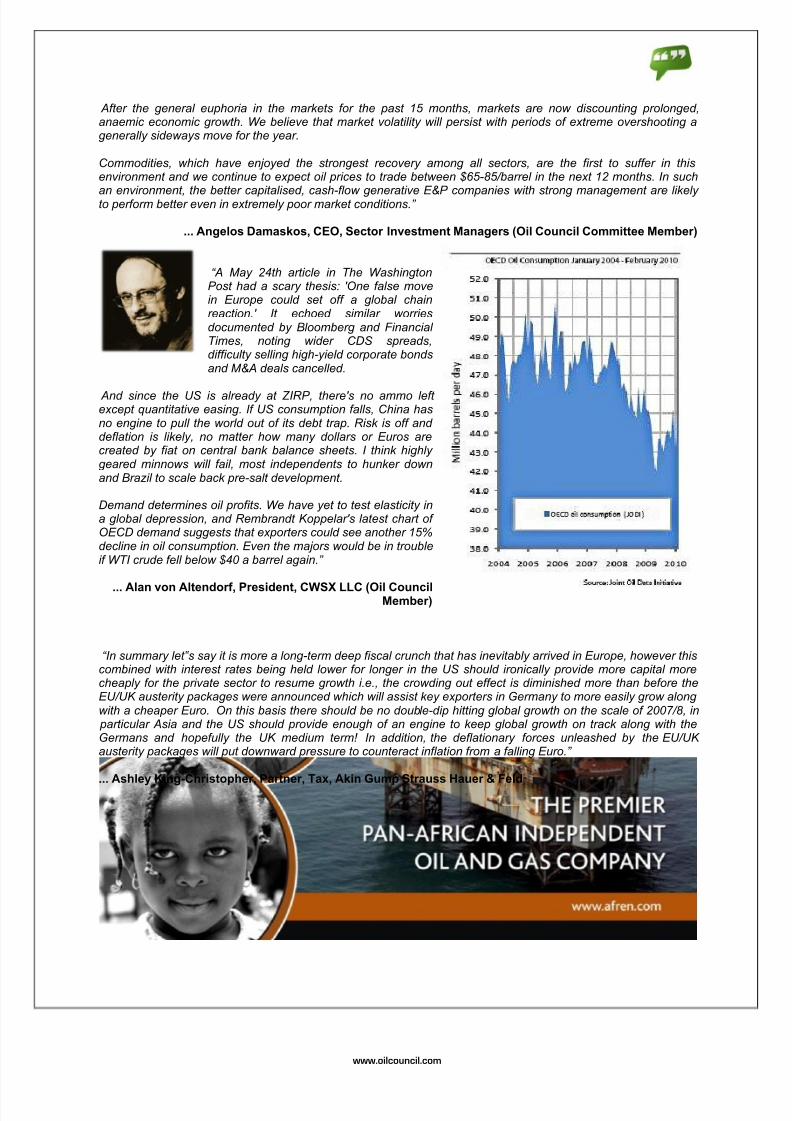

After the general euphoria in the markets for the past 15 months, markets are now discounting prolonged,anaemic economic growth. We believe that market volatility will persist with periods of extreme overshooting agenerally sideways move for the year.

Commodities, which have enjoyed the strongest recovery among all sectors, are the first to suffer in thisenvironment and we continue to expect oil prices to trade between $65-85/barrel in the next 12 months. In such

an environment, the better capitalised, cash-flow generative E&P companies with strong management are likely to perform better even in extremely poor market conditions.”

... Angelos Damaskos, CEO, Sector Investment Managers (Oil Council Committee Member)

“A May 24th article in The WashingtonPost had a scary thesis: 'One false movein Europe could set off a global chainreaction.' It echoed similar worriesdocumented by Bloomberg and Financial Times, noting wider CDS spreads,difficulty selling high-yield corporate bondsand M&A deals cancelled.

And since the US is already at ZIRP, there's no ammo left except quantitative easing. If US consumption falls, China hasno engine to pull the world out of its debt trap. Risk is off and deflation is likely, no matter how many dollars or Euros arecreated by fiat on central bank balance sheets. I think highly geared minnows will fail, most independents to hunker downand Brazil to scale back pre-salt development.

Demand determines oil profits. We have yet to test elasticity ina global depression, and Rembrandt Koppelar's latest chart of OECD demand suggests that exporters could see another 15%decline in oil consumption. Even the majors would be in troubleif WTI crude fell below $40 a barrel again.”

... Alan von Altendorf, President, CWSX LLC (Oil CouncilMember)

“In summary let‟s say it is more a long-term deep fiscal crunch that has inevitably arrived in Europe, however thiscombined with interest rates being held lower for longer in the US should ironically provide more capital morecheaply for the private sector to resume growth i.e., the crowding out effect is diminished more than before theEU/UK austerity packages were announced which will assist key exporters in Germany to more easily grow along with a cheaper Euro. On this basis there should be no double-dip hitting global growth on the scale of 2007/8, in particular Asia and the US should provide enough of an engine to keep global growth on track along with theGermans and hopefully the UK medium term! In addition, the deflationary forces unleashed by the EU/UK austerity packages will put downward pressure to counteract inflation from a falling Euro.”

... Ashley King-Christopher, Partner, Tax, Akin Gump Strauss Hauer & Feld

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 23/38

www.oilcouncil.com

‘On the Spot ’ with our Question of the Month (Part Two)

“How significant an impact will BP’s Gulf of Mexico disaster have on the future

landscape of the oil and gas industry?

““There are two components to consider, political and technical. Based on past experience,only very few politicians will let the opportunity (feeding frenzy) pass to create enormousspectacles, to arrange theatrical show cases and hearings, and to call loudly for a full rangeof legislative and regulatory actions from „punishment with extra taxes‟ all the way to totally banning any offshore drilling and production in US territorial waters. Therefore, we canexpect a considerable and burdening legislative, regulatory and fiscal impact resulting from

this political “Schlachtfest”.

On the technical side every catastrophic failure, especially those in technological frontiers,has always led to tremendous efforts to find the causes of such failures and to expeditiously develop new processes, procedures, superior materials and products to safeguard against repetition (e.g. Spaceships „Challenger‟ and „Columbia‟ and the „Piper Alpha‟ Platform events).

Therefore, tremendous progress can be expected in the much better understanding of the peculiarities of thehighly challenging frontier environment of deep sea drilling and production, especially in the area of temperatures, pressures, the total absence of – or highly restricted – visibility, and extraordinary difficulty in performing mechanical tasks, and the subsequent development of new technologies, materials, approaches, processes, as well as, internal and external guidelines.

Then there is the „Industry Impact‟. Almost every company will undertake all reasonable and feasible efforts toreview and update their processes, policies, procedures, guidelines and applied technologies to effectively reflect protection against catastrophic failures like the one that happened to BP. The experience of this spill and itsenormity also could (and should!) lead to an industry-wide task force to coordinate the progress in effectivetechnologies and applications in operations in highly volatile and hostile environments, as well as, theestablishment of an industry-wide emergency response task force. „Industry‟ in this regards would include the Oil & Gas Industry and the Oil & Gas Service and Equipment companies, all enhanced by the inclusion of therespective Federal and State organizations.”

... Franz Ehrhardt, CEO, CASCA Consulting LLC (Oil Council Committee Member)

“The Macondo blowout in the Gulf of Mexico is a tragedy for those who lost their lives and their relatives, as well as, an ongoing disaster for the offshore drilling industry. It is of coursetoo early to tell with certainty what will be the long-term implications of the spill for BP and the wider industry. However some themes are emerging. From the industry's perspective in

the US it could not have happened at a worse time, just one month after Washington had signalled an expansion of offshore drilling to balance its new legislative proposals on climatechange and clean energy. The key question is whether there will be significant long-termeffects, or whether business will eventually return to its previous trend and modus operandi.It is noteworthy that previous major incidents have slowed but not ultimately blocked the pace of expansion. One obvious change will be the push for stricter, and inevitably more costly regulation toreduce risk and improve safety and damage to fragile environments. In the UK, Chris Huhne, the new Energy Secretary, recently announced plans to double inspections of rigs in UK waters and may require an increase ininsurance cover. Tighter regulation will clearly delay and slow down drilling programmes. This pressure will not only come from the regulators.

Directors of operating companies, particularly the juniors without the deepest pockets, will also be very concerned as to their own responsibilities and potential liability.

There will be a boost for the developers of alternative sources of energy and the clean tech industry. But in thenear-term this will not provide the solution to security of energy supply in a time of increasing world demand. Thecurrent offshore model of outsourcing the work, particularly to independent contractors, will come under scrutiny,

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 24/38

www.oilcouncil.com

perhaps resulting in the majors taking more work in house, though abandoning the current model cannot happenquickly and almost certainly will be less efficient. This will prove to be bad news for the contractors, but to what extent? New exploration areas will be left untouched, at least for a time. In the US this includes the recently licensed blocks off Virginia, Alaska and California, and further afield potentially in the waters around Greenland and elsewhere in the Arctic.

Finally, under pressure from environmentalists, the offshore drillers' fiscal regime may well become lessattractive, with the recent tax breaks implemented in the US already under considerable threat. Overall though,the outlook for the industry generally remains positive and one suspects that the Deepwater Horizon disaster,serious as it is, will not alter its long-term trend.”

... Neil Vickers, Partner, Corporate, Denton Wilde Sapte LLP (Oil Council Member)

“Whilst the disaster will impact on many aspects of the industry the impact on the structuring of JOAs will be interesting to see. Can we continue with the concept of „no gain/no loss‟ for theOperator, with the Operator and Non-Operators sharing any loss in proportion to their respective participating interest, other than where the Operator‟s gross negligence or wilful misconduct is the cause of the loss – and then the gross negligence or wilful misconduct of asenior manager of the Operator at that? Will the Non-Operators accept such a submissive rolein the future when it comes to how the Operator conducts petroleum operations? Will they

want to be more intrusive? Will the role of the Operating Committee change from supervisory and advisory to include monitoring and enforcement? Will the mechanisms for dealing with

default need to change? How can we be sure the Operator and Non-Operators will have the financial capability tomeet a call to cover such loss? What about sole risk? Will the rules of sole risk be changed? Will the non-solerisk parties rely on a contractual indemnity by the sole risk parties? So many questions – time will give us someanswers.”

... Dr Kenneth Mildwaters, Senior Partner, Mildwaters Consulting LLP (Oil Council Member)

“I am actually quite worried about the BP GOM situation. It is bad enough that such acatastrophe has occurred (with the devastating impact on people‟s lives and the environment)but I am equally dismayed and disappointed with the immediate politicisation of the disaster by the White House. Wild accusations, xenophobic threats and over-aggressive pontification have

done no credit to the Obama Administration. Obviously, there had to be a degree of tablethumping and corporate bashing in order to appease a nervous electorate but, on a wider context, fresh lines may have been drawn between the US government on one side and “Big Business” on the other. I see a much more difficult operating environment (and not just in theUS) for the whole industry.

The US domestic offshore petroleum industry could be about to get a whole lot more expensive and tougher. If we also add in the rising environmental objections in North America to onshore shale gas and oilsandsoperations, there are serious supply concerns ahead for the US. The Obama Administration‟s reaction to thisevent could also be a worrying presage of a more interventionist attitude in general, perhaps with wildly unpredictable consequences. Over-reaction to such stresses tells us a lot about the capability of this Administration and gives serious cause for concern when even larger issues of an economic, political or military nature present themselves in the future.”

... Robert Lambert, CEO, GB Petroleum Ltd (Oil Council Member)

“Longer term this could have a severe impact and may be viewed in the future as the watershed moment when a significant move towards a post-oil economy gathered pace. A shift of focus inthe near-term towards identifying fail safe solutions over identifying reserves may become the priority for CEOs worldwide. From a layman‟s point of view it has also highlighted the unedifying behaviour endemic following any disaster where avoiding responsibility is the priority.

The sector doesn‟t help itself when the multinational big boys outsource everything (BP contract,Transocean operated rig and Halliburton as a service provider for other critical tasks) to service

companies and everyone looks to everyone else to take the blame. Perhaps Big Oil will no longer be seen tobe untouchable. Lastly, is it really state of the art technology in the industry to deploy a hastily prepared „funnel‟ inresponse to the disaster? In this day and age it all seems a bit inadequate to the general public.”

... Alan Ross, Senior Manager, Oil & Gas, Lloyds Banking Group (Oil Council Member)

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 25/38

www.oilcouncil.com

“It‟s important to remember that the number one issue that drives this industry is the global demand for oil. The unfortunate accident in the Gulf will not have an impact on demand for mergers and acquisitions. In fact, it might give another boost to the already robust pipeline of deals we can expect this year because of companies needing to adjust their practices and operations to any potential technical changes that we expect will be mandated to improveoverall environmental safety.

PwC works with energy companies to help them better understand new opportunities in themarket, especially when there are unforeseen events like this. Based on our experience,there will be more companies looking for additional insights and perspectives into how potential changes will impact their current businesses and strategies. And, since today‟s energy deals are not just focused on acquiring reserves, but technology, talent, and inherent 'know-how',” there will be an appetite for a new wave of transactions that can add proven capabilities to a portfolio of services. We are actively helping energy companiesnavigate the complicated road of M&A, and with any unique event that takes the spotlight, there is a heightened sense of being prepared for a variety of scenarios and making sure they uncover every potential risk and opportunity for reward.”

... Michael Collier, Partner, PwC (Oil Council Member)

“The BP disaster is likely to be a game changer for the GOM and many other deep offshore locations. It has

focussed media attention on the technical challenges as never before and it is likely that there will be a significant increase in regulation and supervision that will add time and complexity for players wishing to explore suchregions. In the longer term the need to recover reserves from these locations will be paramount and so a way will be found to continue to have economic exploration in the most challenging locations. In terms of players therewill be no change – it remains the preserve of super majors and it is very unlikely that national governmentswould want to be more than regulators one step away from ultimate responsibility.”

... Keith O’Donnell, Head, Natural Resources (EMEA), KBC (Oil Council Member)

“The traditional hydrocarbon model is really a dying one. Even with the oil reserves in Iraq,Iran and the Kingdom of Saudi Arabia, easy oil will be running out in less than 12 years.Difficult oil, strictly seen from the economics, would require an oil price of at least US$75 tomake it break even. The market will not accept a US$150+ price and alternative energy will

mushroom again because their break-even prices will be graciously surpassed.

Companies and experts claim that technology will improve to a level that will make difficult oil cheaper to access. Indeed technology has improved – back in the early days 1,000 feet of water was astonishingly cutting edge, now they‟re drilling at 12,000+ feet of water – but the

costs have not decreased. The opposite is true. The environmental impact was big anyway, but with accidentssuch as the BP one in the Gulf, the stopwatch will be put on hold for at least another two years. Companiesshould really re-think their models in that perspective. The gas sector will get more attention as a consequenceand already we‟re seeing a number of new sites coming on-stream with gas substituting oil as chemical feedstock increasingly more so.”

... Ennio Senese di Sisto, Executive Partner, Energy, Accenture (Oil Council Member)

“If BP are able to cap the well (Wednesday 26 May is first top kill attempt) then this will enable any „worst case‟ scenario to be avoided, and BP's efforts to correct the situation and clean up the impact of the spill can become(even) more focused. Their visibility and proactive response has been exemplary in my view, and the industry should take note of such commitment for future incidents - which is a read across in itself. There is of course asignificant environmental impact already.

However the US Gulf and other sensitive offshore environments have recovered from spills and other disastersbefore and while there will be lessons learnt in response and application of clean up techniques –this may not bethe main ramification for the industry. Indeed, the key change for the industry has to be in avoiding suchcatastrophe again. This implies a need to focus on the failure of a number of processes, systems and equipment with multiple control-mechanisms, procedures and tools that obviously did not work in either a) preventing theaccident or b) reducing the impact of the accident.

In years to come, BP may be measured on its clean up commitment and the rectification of the spill. However, it will also be measured on the very steep learning curve it has had to climb to kill the well at such depths and

improvise in such a frontier territory. The industry will likely be measured on its ability to improve safety procedures and avoid such damaging disasters in the first place, and this will involve inclusion of the lessons

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 26/38

www.oilcouncil.com

learnt from this whole episode. Any repeat catastrophes of such magnitude cannot be allowed to happen – and BP's experience will be core to ensuring this going forward.”

... Jason Kenney, Head, Oil & Gas Research, ING Bank; and President, Scottish Oil Club

“What lessons have we learned already? In summary... A woeful lack of preparation on the part of BP to cope with these types of oil spill disasters. It‟s an eye

opener for the industry as a whole to add additional redundant safety measures. The multi-level, devastating damage that such an oil spill disaster can cause worldwide.

Government agencies in charge of regulating the industry are staffed with personnel having neither thetechnical knowledge associated with offshore drilling, nor the sufficient power to enforce regulations.

What does the future now hold for the industry? In summary...

Deep water drilling is a necessity, and it will continue. At the present, there are not enough viable oil substitutes to produce energy at the massive scale needed globally.

New rigorous safety / maintenance regulations applied on a global basis.

Sky rocketing insurance coverage, which adds to the cost of drilling, particularly subsea.

Additional taxes levied on the industry. Revitalized efforts to develop energy renewables.”

... Philippe Mitterrand, Chair, International Study Group, SPE-Gulf Coast Section (Oil Council Member)

“The impact of the Gulf disaster will be significant on the future regulatory climate for offshoreand in particular deepwater drilling. At the very least, it will add regulations in an effort to prevent future blowouts. These expected regulations will add to the cost of exploring for and developing deepwater oil and gas resources. If liability for major spills rises from US$75 millionto billions of dollars, it could mean that only the IOCs can continue to explore and developdeepwater projects. One would also expect that the review process prior to approval of futureoffshore projects will take more time and that leasing of offshore acreage on Federal lands will be slowed.

While the Obama Administration had already excluded the Pacific OCS from future oil and gas development, this potentially oil and gas rich region will not be opened for development for a very long time. Outside of the US, it may become more difficult for Brazil to raise the funds necessary to develop the pre-salt blocs where major oil and gas files have been discovered. Delays in developing the pre-salt can be expected. It is possible that thetechnology to find, develop and produce oil and gas from ultra deepwater oil and gas accumulations, is way ahead of the technology to deal with serious potential problems. Perhaps some time is needed for thosetechnologies to be developed.”

... Dr Herman Franssen, President, International Energy Associates (Oil Council Member)

“The BP Gulf of Mexico disaster has raised public awareness of the risks associated withoffshore drilling for oil. Given the size of the industry and the fact that virtually all recent significant discoveries are offshore, it is unlikely that a regulatory response will have a lasting impact on operations. It is possible that there will be delays in projects as companies and government officials try to introduce new controls and practices, but given the demand for

hydrocarbons as the world‟s main energy source, the adaptation period should be relatively short. After all, it is becoming clear that the BP disaster comes down to human error rather that poor practice and regardless of what any manual says, human error is very difficult to control.BP might have failed in instilling its policies and (high) standards, as stated in its manuals, to itsemployees, but such management quality is very hard to regulate. Drilling offshore should continue especially given the decline in reserves in onshore fields around the world.”

... Angelos Damaskos, CEO, Sector Investment Managers Ltd (Oil Council Committee Member)

“Gulf of Mexico produces ca. 1.6 mln bpd of oil ca. 24% of all US oil production and ca. 25% of global deepwater oil production. Gulf of Mexico and other deepwater areas remain crucial for the global oil supply. Following areview of the accident, new safety, operational and environmental regulation are likely for offshore drilling in Gulf of Mexico and other regions are likely to follow suit and to include them in their operating guidelines. The

regulation, liabilities and insurance cost for deepwater operations are likely to increase cost and also delay tofuture deepwater production (Deepwater is likely to remain the marginal barrel for conventional oil production).Governments and consumers should remain pragmatic and realise that production from deepwater areas is

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 27/38

www.oilcouncil.com

essential in order to meet global demand. Currently only a few select operators have the expertise and financial muscle to manage full cycle deepwater operations. Lessons learnt from BP‟s Macondo will be shared by industry players to build better awareness and standards on deepwater operations.

Collaboration between service companies and upstream players has built a vibrant deepwater industry in a safeway over the past two decades. A tragic accident like Macondo should encourage the industry, policy makers and

consumers to strive even harder to achieve new levels in safety and environmental standards while addressing the global energy challenge.”

... Unnamed Industry Advisory Perspective

“It depends in part on BP's success in executing remediation strategies, but will in time bereduced by the mere tendency to forget. Litigations will drag on and influence public perception, which is the objective of such efforts, aimed at invoking legislative reforms tofurther restrict and regulate oil and gas companies and command environmental accountability and stewardship. All things considered, the impact could be damaging for those companies that cannot adapt, or at least appear to.”

... Chris Valenti, Energy Investment Banker, Starlight Investments, LLC (Oil Council

Member)

“BP‟s newly released Statistical Review of World Energy shows the US making major progress in oil and gas production in 2009. It overtook Russia last year as the largest natural gas producer in the world after US output increased 5.3% in 2008 and another 3.5% in 2009 on the back of rising unconventional gas production. Last year the US showed the best growth rate in oil output (+7%) for over forty years – largely due to a 34% increase inGOM oil output, which was in turn to a large extent driven by a 58% jump in BP‟s oil production in deepwater GOM. Both unconventional gas and deepwater oil carry environmental and technological risks as indeed any new technologies would do.

Without America‟s ability to encourage technological innovation and take investment risks last year‟sbreakthrough would not be possible. Would Obama‟s administration now want to reverse this? I don‟t think so.However, the industry will likely face more stringent regulation in GOM with a commensurate rise in production

costs and insurance premiums. Taxes and royalties may also rise but probably not to the level where new investments would be discouraged.

The EU may follow with a review of their offshore regulations but other major new deepwater areas such asBrazil or Angola are unlikely to respond with any material changes.”

... Evgeny Solovyov, Director, Oil and Gas, Global Equity Research, Societe Generale Corporate &Investment Banking (Oil Council Member)

8/9/2019 The Oil Council's June 2010 Edition of 'Drillers and Dealers'

http://slidepdf.com/reader/full/the-oil-councils-june-2010-edition-of-drillers-and-dealers 28/38

RegesterLarkin

Reputation Strategy and Management

Regester Larkin helps IOCs, NOCs, Independents

and utilities – both upstream and downstream - toprotect and capitalise on their reputation.