the next billions: business strategies to enhance food ... · strengthening food value chains in...

TRANSCRIPT

The Next Billions:Business Strategies to Enhance FoodValue Chains and Empower the Poor

COMMITTED TO IMPROVING THE STATE

OF THE WORLD

Prepared in collaboration with The Boston Consulting Group

World Economic ForumJanuary 2009

The views expressed in this publication do not necessarily reflect those of the World Economic Forum.

World Economic Forum91-93 route de la CapiteCH-1223 Cologny/GenevaSwitzerlandTel.: +41 (0)22 869 1212Fax: +41 (0)22 786 2744E-mail: [email protected]

© 2009 World Economic ForumAll rights reserved.No part of this publication may be reproduced or transmitted in any form or by any means, including photocopying andrecording, or by any information storage and retrieval system.

All photographs by Brent Stirton, courtesy of Getty Images.

REF: 150109

Contents

Preface 4

Executive Summary 6

Chapter 1 – Introduction 9

Chapter 2 – Understanding the Food Value Chain 11

2.1 A major opportunity 11

2.2 Overview of the food value chain 12

2.3 Diversity in food value chains 13

2.4 Turning a vicious cycle into a virtuous cycle 13

2.5 Business opportunities along the food value chain 15

Chapter 3 – Solutions to Unleash the Potential of Producers and Consumers 17

3.1 Business solutions for producers 18

3.2 Business solutions for consumers 25

3.3 The case for holistic solutions 28

Chapter 4 – Empowering Entrepreneurs through Business-enabling Products and Services 30

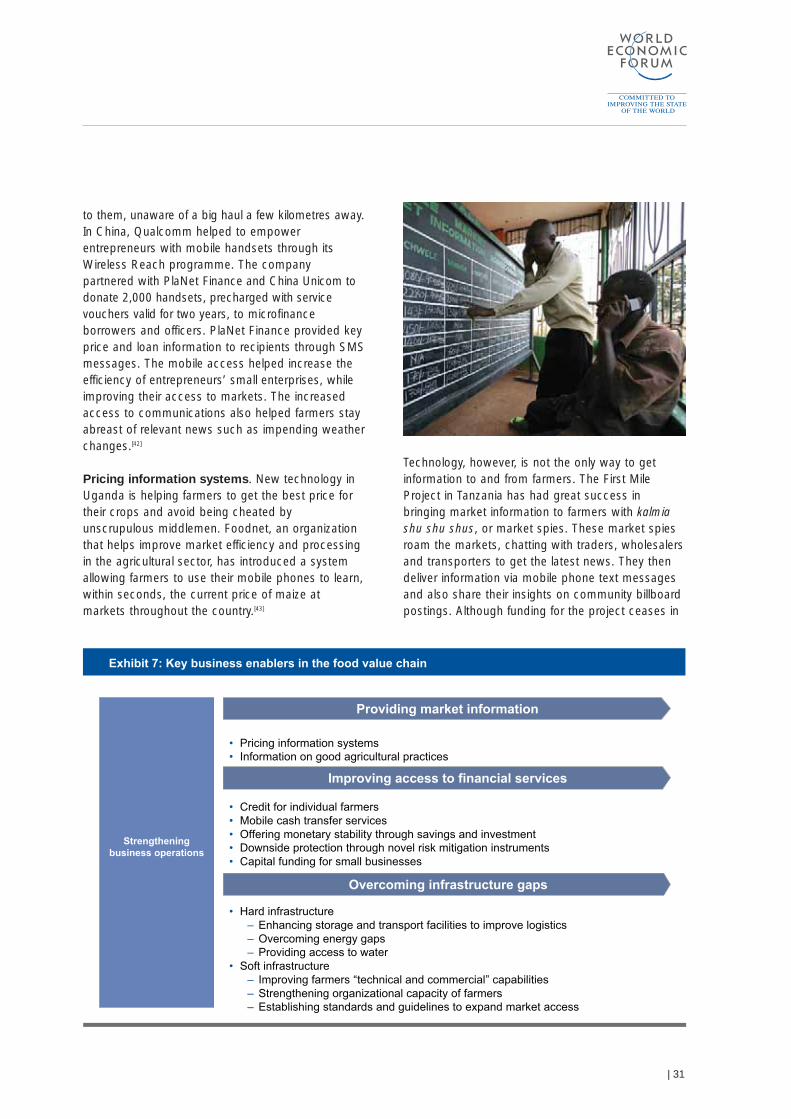

4.1 Providing Market Information 30

4.2 Increasing Access to Financial Services 32

4.3 Overcoming Infrastructure Gaps 36

Chapter 5 – Unleashing Potential: Design Principles for Success 39

5.1 Create life-enhancing offerings 40

5.2 Reconfigure the product supply chain 41

5.3 Educate through marketing communication 42

5.4 Collaborate to form non-traditional partnerships 43

5.5 Unshackle the organization 45

Chapter 6 – Conclusion: Key Actions for Scaling up 47

6.1 Strengthening incentives for business engagement 47

6.2 Prioritizing and sequencing business initiatives 48

6.3 Providing complementary funding and capacity 48

6.4 Facilitating corporate engagement 48

6.5 Establishing models and building momentum 49

6.6 Collaborating to accelerate progress 49

Terminology 51

References 52

Appendix 1: Methodology for Estimations of Population and Income 55

Appendix 2: Case Study Selection Process 59

Appendix 3: List of Case Studies Cited 60

Appendix 4: Actions for Scaling Up Business Models 63

The World Economic Forum is pleased to presentthis report on innovative business models that canimprove sustainable food production and help toreduce poverty in developing countries.

For the past four years, the Forum has served as aplatform for leaders to define and work together onbusiness-led and multi-stakeholder solutions forsustainable food production. Our activities includefacilitating multi-stakeholder leadership actionthrough the Global Agenda Council on FoodSecurity; undertaking the research and thoughtleadership seen in this and other reports; andfacilitating the Business Alliance Against ChronicHunger which is implementing on-the-groundsolutions in Kenya. This portfolio of work ischampioned by the Forum’s Consumer Industriescommunity with support from the Bill & MelindaGates Foundation. We greatly appreciate the GatesFoundation’s support for preparation of this report.This project was based on a broad research surveyplus three cross-industry, multistakeholder

roundtables conducted in Latin America, Africa andAsia during 2008. The research survey includedreview of 60 reports and collection of 200 casestudies from primary and secondary sources. Theroundtables provided ground-level insights frompractitioners – ranging from multinational andregional companies to social entrepreneurs – whoare pioneering these business models on theground.

The report documents a series of commerciallyviable business models that have proven effective atstrengthening food value chains in developingcountries, and offers recommendations for scalingthem up. It presents examples of specific businessapproaches that can engage poor producers,consumers and entrepreneurs along the food valuechain. It outlines design principles for companiesinterested in developing such initiatives, andsuggests actions that all stakeholders can take tofacilitate expansion of these business approaches.

Preface

4 |

Our conclusion is that the kinds of business modelsoutlined in this report offer substantial potential fordriving economic growth and food production,benefiting both companies and poor communities.Undertaken by global and local companies – often inpartnership with other organizations – they representthe highly dynamic business innovation and growthwhich is rapidly evolving in “base of the pyramid”(BOP) markets. The report builds on and intends tocomplement the work of thought leaders in thisarena such as C.K. Prahalad’s Fortune at theBottom of the Pyramid, the World ResourcesInstitute and IFC’s Next 4 Billion report, HarvardUniversity’s industry-specific Economic Opportunityreports, and the United Nations DevelopmentProgramme’s Growing Inclusive Markets initiative. Italso draws from leading works in the agriculturalarena by the World Bank, the International FoodPolicy Research Institute (IFPRI), and the UnitedNations Food and Agriculture Organization (FAO).

This report project was prepared by the WorldEconomic Forum in partnership with the BostonConsulting Group. Lisa Dreier led the initiative at theForum together with Jennifer Baarn and Pial Islam,with input from Helena Leurent, Sarita Nayyar,Cornelia Roettger and Rick Samans. The Forumwishes to thank the Boston Consulting Group for itswork, which was led by Arvind Subramanian, AnandRaghuraman and Nimisha Jain with Neetu Vasantu,S. Rajagopal and Marije van Mens.

The report reflects extensive inputs, discussion andreview by a number of Forum partners and experts,to whom we are greatly indebted. Corporatereviewers include: Marco Ferroni of SyngentaFoundation, Willem Jan Laan of Unilever, ChristianMaas of Metro Cash & Carry International, SusanMorgan of BT, Herbert Oberhaensli of Nestlé S.A.,Mara Russell of Land O’Lakes, Chris Shea ofGeneral Mills, Gabriel Solomon of the GSMAssociation, Christina Ulardic of Swiss ReinsuranceCompany, and Steve Yucknut of Kraft Foods. Non-business and expert reviewers include: Marc vanAmeringen and Bérangère Magarinos of the GlobalAlliance for Improved Nutrition (GAIN), Andrew Aulisiof the World Resources Institute (WRI), Alain deJanvry of the University of California at Berkeley,Jane Nelson of Harvard University, Richard Rogersof the Bill & Melinda Gates Foundation, MirjamSchoening of the Schwab Foundation for SocialEntrepreneurship, and David Spielman of theInternational Food Policy Research Institute (IFPRI).Harvard University, the World Resources Instituteand the Schwab Foundation for SocialEntrepreneurship also served as independentreviewers of the case study selections for the report.

During 2008, the global food crisis starkly illustratedthe urgent need to develop sustainable solutions forfood security and economic growth benefiting allstakeholders, including the poorest. The ideas in thisreport intend to contribute toward that larger goal.

| 5

Richard SamansManaging DirectorWorld Economic Forum

Sarita NayyarSenior Director, Consumer IndustriesWorld Economic Forum

Overview

Business actions to strengthen food value chains indeveloping countries fulfil two vital goals. For theprivate sector, they open up opportunities in agrowing, profitable and largely untapped market. Forpoor communities, innovative approaches canimprove livelihoods. Challenges in the businessoperating environment have historically limitedbusiness incentives to engage in poor regions. Butmany companies are discovering new approacheswhich can overcome such challenges and eventransform them into opportunities.

This report focuses on business models that areproving effective along the food value chain in poorregions. It presents an array of specific examples,outlines design principles that companies andpartners can use to guide new initiatives, andrecommends actions that all stakeholders can taketo scale up effective models.

The Opportunity

Globally, 3.7 billion people are largely excluded fromformal markets. This group, earning US$ 8

aper day

or less, comprises the “base of the pyramid” (BOP)in terms of income levels. With an annual income ofUS$ 2.3 trillion a year that has grown at 8% inrecent years, this market spends US$ 1.3 trillion ayear on food. Around 70% of the BOP (2.5 billionpeople) depends on the food value chain for theirincomes, either directly as small-scale farmers andfarm labourers, or indirectly as small-scaleentrepreneurs.

While it is highly diversified, much of the BOPrepresents a fast-growing consumer market, anunderutilized farming sector, and a source ofuntapped entrepreneurial energy. Engaging the BOPas producers, consumers and entrepreneurs istherefore key to both reducing poverty and drivingbroader economic growth along the food valuechain.

Understanding Food Value Chains

The process of growing, producing and marketingfood involves a variety of industries and stakeholdersalong multiple steps, forming the food value chain.

• Private-sector actors in the food value chaininclude agricultural input companies, farmers(particularly smallholders and women),intermediaries, processors and retailers. Business-enabling services such as telecommunications,financial services, energy and logistics play a vitalrole throughout the chain. Non-businessstakeholders are central to food value chainoperations; these include governments, NGOs,donor agencies and international organizations.

• In developing regions, food value chains areconstrained by limitations related to infrastructure,producer capacity, availability of finance, public-sector capacity, and other factors. Theseproblems often create a “vicious cycle”, in whichlow productivity and a lack of access to capitaldepresses income and consumption, trapping theBOP in a downward spiral of deepening poverty.Coordinated engagement by business and otherstakeholders can reverse this dynamic, creating amutually reinforcing “virtuous cycle” of increasedproduction, consumption and entrepreneurship atthe local level.

Innovative Business Solutions

Businesses can take a holistic approach to the foodvalue chain with specific interventions at three stages:producers, consumers and entrepreneurs.

Business solutions for producersCompanies can deploy a range of innovativestrategies to provide opportunities to BOPproducers. These include:• Develop agricultural inputs targeted to BOP

needs. New product design, and targetedresearch and development, can create offeringssuited to poor producers’ needs and budgets

Executive Summary

6 |

a The US$ 8/day income threshold is in Purchasing PowerParity (PPP) dollars, and was defined by the WorldResources Institute report, The Next 4 Billions.

| 7

• Improve farmers’ access to inputs byexpanding and strengthening rural retail networks,and offering financial services to farmers.Companies can also empower retailers to expandtheir product and service offerings

• Strengthen farmer capacity through trainingand outreach. Input companies can strengthenfarmer awareness of new products andtechniques. Buyers can work with farmers toimprove production and meet quality standards

• Improve supply-chain efficiency throughstreamlined logistics and warehousing, andworking with value-adding intermediaries

• Optimize sourcing processes by sourcing fromlocal producers, commercializing local rawmaterials and creating markets for sustainabletrade in high-value products

Business solutions for consumersCompanies can meet growing consumer demand inthe BOP market through several key strategies:• Design nutritious food for poor consumers,

by offering nutritionally fortified, affordable foodsthat meet the preferences of the BOP

• Expand retail distribution networks byleveraging informal retail and distribution channelsto empower entrepreneurs and expand reach.Reduce delivery costs by partnering with otherbusinesses

• Strengthen consumer demand througheducational marketing strategies, partnershipswith trusted parties, and using certification andlabelling to build consumer trust

Business solutions to empower entrepreneursIndustries such as financial services,telecommunications, energy and transportation areimportant enablers of business activity along foodvalue chains. Companies can develop innovativestrategies to provide needed services in suchmarkets, such as:• Provide market information through

telecommunications applications that helpfarmers access information on market prices andgood farming practices

• Increase access to financial services byadopting innovative strategies to provide credit,savings and insurance for individual farmers;creating mobile cash transfer systems; developingnew novel risk-mitigation instruments; andproviding capital funding for small business

• Overcome infrastructure gaps throughbusiness-led solutions targeted at both hardinfrastructure (storage and transportation, energy,water infrastructure) and soft infrastructure(organizations, policies and regulations thatstrengthen business operations)

Design Principles for SuccessfulBusiness Models

While BOP markets vary widely, companies canadapt successful strategies to specific regions orincome segments. This report identifies a set ofdesign principles that companies and partners canuse in developing effective business models tostrengthen food value chains:• Create life-enhancing offerings: Develop new

products and services that improve livelihoodsand trigger economic multipliers at the BOP

• Reconfigure the product supply chain: Createcost-efficient distribution systems by sourcingfrom local producers and leveraging existing localdistribution channels

• Educate through marketing communication:Design marketing programmes that containeducational as well as persuasive messages

• Collaborate to form non-traditionalpartnerships: To lower costs and broadendistribution, move beyond traditional roles topartner with communities, invest in skill building,and create incentives for self-governance amongBOP business partners

• Unshackle the organization: Design corporateorganizational structures – including metrics,incentives and accountability systems – tosupport, measure and reward long-term successin business initiatives targeting the BOP

8 |

Scaling Up: Key Actions forStakeholders

Scaling up BOP business strategies requires adecentralized and localized approach, in whichsuccessful concepts are adapted for transfer fromone region to another, often with a new set ofpartners and collaborators. Achieving scale in thesebusiness models, therefore, often requirescooperation among many actors includingcompanies, governments, NGOs, donor agenciesand international institutions. Partners can worktogether on several fronts:• Strengthen incentives for business

engagement through boosting incentives,removing barriers and reducing costs that impedecommercial activity. This includes establishingfinancial or market incentives, and improving theenabling environment (policy, infrastructure andservices)

• Prioritize and sequence business initiatives,working with partners to develop key capacitiesrequired for specific business models, andprioritizing high-impact and essential initiatives

• Provide complementary funding andcapacity to overcome gaps (for example in R&Dfunding) and strengthen hard and softinfrastructure required for business models tosucceed

• Facilitate corporate engagement amongdiverse industries and stakeholders, unitingpartners’ complementary capacities aroundcommon goals to reach the BOP

• Establish effective models and buildmomentum, sharing knowledge and highlightingsuccesses to accelerate learning and encouragebroad adoption

• Collaborate to accelerate progress, engagingleaders and “orchestrators” to catalyse andsupport multistakeholder cooperation

The business models discussed in this report havethe potential to create substantial value for poorconsumers, producers and entrepreneurs as well asfor companies. They represent a roadmap fororganizations seeking to take a win-win approach inemerging markets. Companies that establishworkable, profitable and scalable business modelsto include the BOP will secure a strong advantage,both commercially and in terms of community andpartner relationships. Success in the end will requirenew thinking, close coordination and alliancesamong unconventional partners – governments, civilsociety organizations and the BOP communitiesthemselves.

The private sector can play a pivotal role in the foodand agriculture sector. However, in developingregions, where both the need and the potential forincreased production are greatest, it is oftenengaged only peripherally. Expanding sustainablebusiness engagement in these areas could bringsizeable gains to both poor, food-insecurecommunities and the private sector itself.

Globally, 3.7 billion people are largely excluded fromformal food markets. This group, earning US$ 8b perday or less, comprises the “base of the pyramid”(BOP) in terms of income levels. Around 70% of theBOP (2.5 billion) depends on the food value chainfor their incomes, either directly as small-scalefarmers and farm labourers, or indirectly as small-scale entrepreneurs.[1-3] (For a detailed account of themethodology used to reach the estimates in thischapter, see Appendix 1). While it is highlydiversified, much of the BOP represents a fast-growing consumer market, an underutilized farmingsector, and a source of untapped entrepreneurialenergy. Engaging the BOP as producers,consumers, and entrepreneurs is therefore the keyto both reducing poverty and driving broadereconomic growth along the food value chain.

The total income of the BOP is US$ 2.3 trillion (in2008 real terms),c and has been growing rapidly at8% annually in recent years [1-3]. The group spendsover 50% of their income – an estimated US$ 1.3trillion annually – on food. As their income grows,BOP consumers are demanding higher value andmore diverse food, as well as other goods andservices. Many poor producers have the potential tosubstantially increase their production, given access

to inputs and training. The BOP is also host to ayoung and growing population of potentialentrepreneurs, many of whom currently lack theessential tools – such as bank accounts, mobilephones or electricity – needed to start a smallbusiness. These trends represent a set of businessopportunities that cut across industry sectors, fromfood, beverage and agribusiness to retail andconsumer goods, financial and telecommunicationsservices, and others. Those at the BOP who can beprofitably engaged by business – referred to here asthe “next billions” – represent a large, untapped market.

Early movers can establish several advantages inthis growing market. By being first to develop newofferings and innovative delivery channels, companiescan gain valuable insights, secure greater marketshare and win the loyalty of BOP consumers andproducers – a key success factor in this market. Bycreating opportunities for sustainable economic andsocial gains at the BOP, they will contribute to long-term market growth that benefits their investments.In fact, the BOP market offers an attractive meetingground where corporate economic benefit and socialimpact can be realized together.

Chapter 1 – Introduction

| 9

• 3.7 billion people around the world live on annual incomes of less than US$ 3,000 (2002 PPP$). 70% ofthem, or 2.5 billion, live in rural areas where agriculture is often the primary economic activity

• Companies, which often play a limited role in the food value chains of developing countries, can enter thismarket in a way that both meets a social need and creates profitable business opportunities

• This report explores how businesses can achieve this potential, outlining examples of successful businessmodels and basic design principles for operating along food value chains at the base of the pyramid (BOP)

The “BOP” and the “Next Billions”“Base of the Pyramid” (BOP) is a collectivereference to 3.7 billion people populating thelowest income strata in the world. The incomelevels for this group range from 0 to a maximumof US$ 3,000 per person per year (in 2002PPP$), or roughly US$ 8 per person per day.

Within this group are the “next billions” – a largegroup of consumers, producers andentrepreneurs who can be profitably engaged orserved by business, albeit with new andinnovative approaches.

b The threshold for BOP incomes was defined by the WorldResources Institute report, The Next 4 Billions.[1]

c All numbers related to income, expenditure and price inthis report are in current US$, unless stated otherwise.

Despite this potential, the business opportunitiesembedded within the food value chains of poorregions remain largely untapped. A host of issuescombine to prevent, discourage or derail businessengagement. These include fragmented and poorquality food production; difficulty in tappingconsumer demand; and poor infrastructure andgovernance. Surveying this landscape, manycompanies have concluded that their standardbusiness models would not be profitable in such asetting, and they may be right. But the story shouldnot end there.

While many remain on the sidelines, an increasingnumber of companies are developing innovativestrategies to tap into the economic potential thatexists throughout the food value chain. Whethersupplying inputs to farmers, sourcing high-valueproducts from small-scale producers, or developingand retailing an array of new products and servicesthat meet the needs of poor consumers andentrepreneurs along the chain, these companies arefinding approaches that work. Those that aresuccessful are establishing viable business modelsfor an untapped market, while also improving thelivelihoods of the BOP.

What are these companies doing right? And howcan other companies tap the potential of thismarket, while also benefiting the poor? Moreimportantly, how can successful businessapproaches be mainstreamed and scaled up, tohelp drive sustainable economic growth in theregions that need it most?

This report attempts to answer these questions. Itpresents a series of specific business models thatare proving effective along the food value chain;outlines design principles for companies seeking todevelop new models; and recommends priorityactions for all stakeholders interested in catalysingsuch pro-poor business engagement.

Chapter 2 provides an overview of the food valuechain, and maps out the role of business and otheractors in making it work. Chapter 3 presents specificbusiness models that target both producers andconsumers along the food value chain. Chapter 4outlines innovative private-sector approaches thatprovide entrepreneurs and small business at the

BOP with the key tools – such as finance,communications and infrastructure – that areneeded to create an enabling environment forefficient marketing. Chapter 5 presents designprinciples to guide the development of effectivebusiness models in these markets; and Chapter 6recommends ways in which these models can beadapted and scaled more broadly, throughconcerted action by all stakeholders.

This report is a companion to The Next Billions:Unleashing the Business Potential of PoorCommunities, published by the World EconomicForum and The Boston Consulting Group. Thatpublication outlines strategies for “win-win”approaches to poor markets that cut across all industrysectors and regions. Both volumes address thebusiness strategies that can be effective at the BOP,often requiring collaboration or partnership with otheractors. While recognizing that the public sector plays avital role in establishing and managing the enablingenvironment for business operations, both reportslimit their discussion of public sector actions to thosedirectly related to the targeted business models.

The need for both public and private sector action toimprove global food production and food securityhas never been greater. In 2008, as economicgrowth slowed, food shortages and price increaseshad a dramatic effect on the world’s poor. Tens ofmillions of additional people were driven into hunger,bringing the global total close to one billion.Establishing sustainable solutions to this problem willrequire innovation, leadership and cooperationamong all sectors. Through the types of businessmodels outlined in this report, business can becomea catalyst and core partner in advancing sustainablegrowth that benefits poor communities as well asthe bottom line.

10 |

In most developing countries, the agriculture sectoris the largest source of employment and a driver ofeconomic growth. Almost 70% of the poor indeveloping countries – over 2.5 billion people – livein rural areas where agriculture is the main economicactivity[1-3] (for a detailed account of the methodologyused to reach the numerical estimates in thischapter, see Appendix 1). Either directly or indirectly,the rural poor are dependent on the food valuechain. The complexities of the food value chain, andthe inter-dependence of its different components,present both a challenge and an opportunity. Atpresent, food value chains in many poor regions arefragmented and inefficient, making them unprofitableand risky for both the people who depend uponthem for survival, and the companies that coulddrive improvements. As discussed below, acoordinated set of business-led interventions tostrengthen operations throughout the chain can

activate a “virtuous cycle” of mutually reinforcinggains in productivity and consumption, resulting insubstantial income gains for the BOP.

2.1 A major opportunity

The current income of the BOP totals US$ 2.3 trillionand has historically been growing at 8% per year[1-3].The group spends over half of this income – anestimated US$ 1.3 trillion annually – on food. Of the2.5 billion members of the BOP who live in ruralareas, about 60% are directly dependent on a smallfarm for their household income. The other 40% areoften closely linked to the food value chain, eitherthrough business linkages (e.g. as agricultural inputretailers or small traders), or through other means[1-3].Together, these rural members of the BOP accountfor between US$ 850 billion and US$ 1.1 trillion inincome, nearly half of the total BOP income[4-10].

Chapter 2 – Understanding the Food Value Chain

| 11

• The food value chain involves multiple steps and engages diverse actors; its complexity and inter-dependence is both a challenge and an opportunity for business

• A coordinated set of business-led interventions can activate a “virtuous cycle” of productivity andconsumption along the chain, resulting in substantial income gains for the BOP and broad-basedeconomic growth

• With a current income pool of US$ 2.3 trillion and food expenditure of US$ 1.3 trillion annually, the base ofthe pyramid has the potential to significantly grow their incomes over the next decade, given the right setof initiatives

Exhibit 1: 2.5 billion people in rural areas are part of the BOP

Worldpopulation

Rest of theworld

High-incomecountries

Income >US$ 3,000

PPP*

IncomeUS$ 3,000

PPP*the BOP

UrbanBOP

RuralBOP

Rural BOPnon-

smallholderhousehold**

Rural BOPsmallholderhousehold**

Pop

ulat

ion

(bn)

*Income based on annual income per person per year in 2002 PPP$**Smallholder farming households are households of farmers and rural labourers working on a farm of 2 ha or smallerSource: United Nations, World Bank, WRI.

1.7

0.9

3.7

1.2

2.51.0

1.5

6.34.6

0

2

4

6

8

2.2 Overview of the food value chain

The process of growing, producing and marketingfood accounts for most of the activity in theagriculture sector and drives many other parts of theeconomy. It involves multiple steps, engages adiverse set of actors, and depends heavily on theoperating environment, which is influenced byclimate, governance and other external factors.

The food value chain starts with agricultural inputcompanies supplying seeds, equipment and otherinputs such as fertilizers. Farmers procure the inputsand combine them with other resources needed foragricultural production: land, water, finance, labourand knowledge. After harvesting, on-farm orcommunity processing may take place to add valueto the crop. Farmers sell the resulting producedirectly to consumers or to intermediaries, who inturn trade with consumers, food processors ortraders. Industrial-scale processing, packaging anddistribution deliver finished products to consumersthrough retail outlets or other channels. At eachstep, participants depend upon business enablers tofacilitate commerce, such as provision of financialand communications services, and energy, transportand water management infrastructure. They also

depend upon the larger public-sector enablingenvironment, which includes government-providedinfrastructure and services, policy and regulation.Finally, the chain is influenced by the naturalenvironment (including soil fertility, water supply andclimate variations) as well as the larger political andeconomic context.

There are many different participants in the foodvalue chain. To efficiently link consumers, producersand entrepreneurs, food chains require coordinatedparticipation from industry, governments and non-governmental organizations (NGOs). Other groupssuch as research institutions, donors and the mediaalso play key roles.

Because smallholder farmers are the mainagricultural producers in many poor regions, theymerit special consideration from companies andother organizations seeking to enhance business-ledgrowth. Given adequate support to overcome theconstraints that they face, these farmers havesignificant potential to increase their productivity,generating potentially substantial economic gains.Smallholders also represent a large and currentlyunder-served consumer market for relevant goodsand services.

12 |

Exhibit 2: Opportunities for intervention in the food value chain

Business enablers

Consumers Agricultural producers

Food valuechain

Strengtheningbusiness

operations

Providing market information

Improving access to financial services

Overcoming infrastructure gaps

Agriculturalinput

Retail(of agri input)

Agriculturalproduction

SourcingProduct designand processing

Retail anddistribution

Marketing

Public sector and policy environment

Gender is another important aspect of the food valuechain, since in most developing countries womenundertake the majority of food production, processingand preparation. In the developing world as a whole,women produce 60-80% of food[11] but earn 22%less than men and have more limited access to credit,training and land rights[12]. Yet, there is compellingevidence from Burkina Faso and Kenya thatagricultural productivity could be raised by as muchas 20%, simply by reallocating existing agriculturalassets more equally between men and women[13].

2.3 Diversity in food value chains

Food value chains, and the value captured at eachstep, can vary widely depending on the product andthe region. For example, maize grown primarily forfamily consumption has a relatively short value chain,whereas fruit that is harvested, processed and thenexported involves a more complex chain. Valuechains for the same product can also look quitedistinct in different regions.

The diversity of food value chains is driven partly bythe difference between staple crops, high-value andperishable products – since each has differenttransport, storage and processing requirements.

Value chains also vary depending on whether theproduct is for commercial or subsistence use and forlocal or international markets. Lastly, the assets andcapacities of the farmer and the intermediaries withinthe chain heavily influence the value that is capturedat each step. The graph below illustrates the varietyof value capture in several food value chains.

This report discusses the basic steps in food valuechains in broad terms, but does not discuss differentiationin great detail. Instead it focuses on business-ledsolutions to constraints that are common across awide range of food value chains involving the BOP.

2.4 Turning a vicious cycle into avirtuous cycle

Communities in poor, rural regions face numerouschallenges and constraints to increase their incomesand engage with the private sector. These include alack of basic or efficient infrastructure, essentialservices, education systems and regulatory regimes.These constraints affect the livelihoods of the BOPas they participate in the food value chain asagricultural producers, consumers andentrepreneurs, often acting in two or more of theseroles simultaneously.

| 13

Exhibit 3: Examples of diversity in food value chains

Yam value chain, Ghana

Kaja Apple value chain, Pakistan

* Value added = price received by actor – price paid by actor.Source: Yam value chain, Ghana: KIT + IIRR; Kaja apple value chain, Pakistan: Asian Journal of Plant Sciences; Cocoa value chain,Ivory Coast: Department of Agricultural Economics, Purdue University

*

Cocoa value chain, Ivory Coast

Producers often lack access to inputs and inputretailers, support services, credit and the knowledgethey need to boost production. They are also highlyvulnerable to risk, such as climate shocks (floodsand droughts) or pests and disease outbreaks, andhave limited access to risk reduction strategies or“safety nets”. They are therefore cautious aboutinvesting in new ventures. In many areas they cannotaccess storage, processing and distribution facilitiesand suffer high transaction costs and large post-harvest losses. With little information, resources, orbargaining power, they face substantial barriers toaccessing markets and securing fair prices. As aresult, many small-scale farmers are trapped in low-input, labour intensive, low-yielding farming systems.

Consumers at the BOP also present a challenge tobusiness investment. They have low and volatileincomes and little access to credit facilities. As aresult, they are highly price sensitive and risk averse.They spend upwards of 50% of their householdbudget on food. Their choices are constrained by alack of information and the cost or lack of access toneeded inputs. Similar challenges face potential

entrepreneurs at the BOP, who generally have littleaccess to the training, information and finance theyneed to realize their business goals.

These problems often create a “vicious cycle”, in whichlow productivity and a lack of access to capital trapsthe BOP in a downward spiral of deepening poverty.This limits demand for consumer goods andopportunities for entrepreneurship in BOP communities.To reverse the vicious cycle, companies can developstrategies to engage the BOP as producers, consumersand entrepreneurs. Strengthening and enablingthese different roles can create a mutually reinforcing“virtuous cycle”. For example, a successful producerwill direct surplus income towards increasedconsumption, benefiting local entrepreneurs such asretailers of consumer goods, agricultural inputs andtelecom services. In addition to alleviating povertyand hunger, productivity gains and increasedincomes allow farmers to invest in the future of theirfarms (e.g. improving soil fertility or diversifying intolivestock enterprises), improve their family’s diet andhealth, and educate their children, all of which buildthe family income-generating potential still further.

14 |

Exhibit 4: Targeted interventions are required to unlock the potential of the BOP

Newbusinessmodels

Tailoredoffers

Improveproductivity

Relianceon

middlemen

Limitedinvestments

Uncertainquantity

and pricesLowerprofits

Producers

Low productivity and high wastage Consumers

Lowlivelihood impact

Unprofitable to reach and serve

Unable tocreate

demand

Low fluctuating incomes

Lowthroughput

Businessenablers

Unwilling to invest

Lack ofinfrastructure

Lowerrealization

Supply chaininefficiencies

Unprofitableto serve

Invest inbusinessenablers

2.5 Business opportunities along thefood value chain

Engaging with the BOP in business activities relatedto the food value chain can generate value forcompanies in a variety of ways. This value may befound through commercial returns; expanded marketaccess; increased quality, reliability or cost-efficiencyof a company’s supply base; or new businesslinkages to local entrepreneurs. Despite the evidentchallenges, many companies are adopting innovativeapproaches to reap the benefits. Although theyemploy different models, their collective experiencesprovide valuable insights into how companies canunlock the potential of the next billions. Thesebusinesses have uncovered opportunities all alongthe food value chain, working with agriculturalsuppliers and farmers, intermediaries (traders,wholesalers and other middlemen) and processors.They have also uncovered related opportunities inretailing, telecom and financial services. Examples ofthese strategies and their effects on business andthe BOP are discussed in Chapters 3 and 4.

While the strategies deployed for one product orarea are not uniformly applicable to other markets,specific examples discussed in this report havesucceeded in boosting the income of BOPparticipants substantially, for example a tripling ofagricultural yields within a year. When taken together,the business strategies outlined in this report couldhave an enormous impact on BOP income if theywere scaled up broadly. Within the BOP, the greatestgains are likely to be captured by farmers andentrepreneurs active in business-enabling sectorssuch as telecommunications and finance. Farmersstand to benefit most from multiple value-chaininterventions (i.e. the combined effects of newtechnologies, policies and institutions) and are thelargest BOP group operating within the food valuechain. Business-enabling sectors currently have asmall presence in rural areas but can grow rapidly inwhat is currently a large and virtually untapped market.

The following chapters present a systematic analysisof the untapped business opportunities that lie alongthe food value chain, which can be important drivers

| 15

16 |

and contributors to mutually reinforcing growth. Thefocus is on models that serve, engage or benefit theBOP in their various roles along the chain. Forcompanies and partner organizations seeking todevelop or broaden their approaches in suchmarkets, the report also distils key insights on whatis needed to create sustainable, scalable businessmodels to develop these opportunities.

Hellen Awuor, farmer and entrepreneur, Kenya

Siaya is the poorest district in Kenya, with 64% ofits 500,000 inhabitants living below the nationalrural poverty line. Most of the district’s inhabitantsare subsistence farmers growing maize, andmany experience seasonal hunger. The districthas limited market-related infrastructure andaccess, further restricting farmer incomes.Diversifying into high-value crops is one wayfarmers can increase their incomes from smallplots of land.

Hellen Awuor, a farmer and entrepreneur in Siayadistrict, has successfully diversified her farmproduction and income sources. In addition togrowing maize and beans for home consumption,she has expanded into horticulture (onions,tomatoes, spinach, avocados and bananas)which she sells in the local market. She spendsthe resulting earnings (which range from US$ 2 to12 per week) on processed goods like sugar, aswell as children's school fees and medicine. Acow and 10 chickens provide additional familynutrition. Through training received from a localagricultural extension officer, Hellen plans toexpand her chicken brood for sale in the localmarket. Hellen also buys and sells used clothingto local residents, and describes herself as "abusinesswoman". Her son, Carlos, recentlystarted beekeeping on the land, producing honeyfor a local company which provided training andequipment.

Source: World Economic Forum, BAACH Kenya2007[14]

In an era of rising food demand, companies areincreasingly seeking ways to expand their supplybase and meet the needs of new consumers. Doingso effectively will require companies to developstrategies for working effectively with smallholderfarmers – who form the majority of the farm sector inmost developing countries – as well as the poor intheir capacity as consumers and entrepreneurs.Companies can work with local farmers tosubstantially increase the volume and quality of theirproduction by facilitating access to inputs andtraining, and by establishing local and internationalmarket linkages. Demand-driven business modelsare highly effective in justifying front-end investmentsin the food value chain.

As BOP incomes grow, companies are also seekingnew ways of meeting the rising demand for foodand other products from BOP consumers. Innovativeapproaches, such as designing affordable,nutritionally fortified foods and extending retaildistribution networks deep into poor communitiesthrough unconventional partnerships, are provingeffective for meeting the needs of BOP consumerswhile also contributing to their health and livelihoods.

This chapter describes specific interventions thathave reached the BOP at different points along thefood value chain. The business models presentedhere are aimed at both BOP producers andconsumers, and can have a substantial impact onimproving the livelihoods of the poor while also

Chapter 3 – Solutions to Unleash the Potential of Producers and Consumers

| 17

• Successfully engaging the BOP as both producers and consumers requires new and innovative businessmodels. This chapter presents examples of effective models being applied along the food value chain

• Business models targeted to agricultural producers include developing and expanding distributionnetworks to increase BOP access to agricultural inputs, improving farmer productivity and supply chainefficiency, and sourcing products for local and international markets

• Models targeted to consumers include: designing nutritious foods targeted to BOP needs; expanding retaildistribution through entrepreneurs and business-to-business collaboration; and conducting educationalmarketing campaigns to stimulate demand

• Holistic business models addressing whole value chains are some of the most effective; companies canlead or coordinate action throughout the chain

Exhibit 5: Business solutions for producers and consumers along the food value chain

Developingagriculturalinputs targetedto the BOP

Improvingfarmers’ accessto agriculturalsupplies

Improvingfarmers’ skillsand techniques

Improvingmarket linkagesand supplychain efficiency

Optimizing ofsourcingprocesses

Designingnutritious foodfor poorconsumers

Expandingretaildistributionnetworks

Strengtheningconsumerdemand througheffectivemarketing

ConsumersAgricultural producers

Agricultural input

Retail(of agri input)

Agriculturalproduction

Marketing ConsumersSourcingProduct

design andprocessing

Retail anddistribution

Successful business models can either target one step or integrate different elements of the chain, adopting a holistic approach to alignopportunities on the demand side with improvements on the supply side.

providing financial returns to farmers andcommercial enterprises. However, it should be notedthat adopting such models is a deliberate choiceand requires innovations and commitment from allpartners.

3.1 Business solutions for producers

Companies seeking to expand their market shareand distribution networks for agricultural inputs, theirsupply base for agricultural products, and theirbusiness linkages in new markets can find significantuntapped potential and unmet demand in poorregions. However, effectively engaging the potentialof these markets often requires entirely newbusiness approaches that involve working withfarmers and entrepreneurs at the BOP.

Companies can adapt their business approaches toserve and empower BOP producers. The followingsections outline business models that are provingeffective in developing targeted products, expandingdistribution and spurring demand-driven productionfor local and international markets.

Developing agricultural inputs targeted to the BOP

Traditionally, agricultural suppliers have targetedmore affluent farmers. Companies that haveventured into BOP markets have done so throughre-packaging existing products to make them moreaffordable, or through adapting products for localconditions and needs. They have also offered farmequipment, such as processing and storagefacilities, for lease rather than for purchase to reducefarmers’ upfront investment costs.

Tailored new product design and R&D. A newgeneration of agricultural technologies is emerging,focused on the practical needs and constraints facedby the BOP, to deliver near-term benefits for farmers.International Development Enterprises India (IDEIndia), a social enterprise, shows how treadle pumpsuppliers can actively engage farmers and other actorsin the chain to achieve profitable results. (See box 1).

Syngenta, a global seed and crop protectioncompany, has demonstrated the payoff of long-termcommitment to developing locally-targeted solutions.The company has spent 11 years developing sugarbeet varieties suitable for tropical climates. Byswitching to the new sugar beet variety, farmers canobtain the same quantity of sugar (or alcohol orethanol) per unit of land, in half the time. Thissignificantly improves productivity and the efficiencyof land use. Using almost 30% less water thantypically required for sugar cane, the sugar beet canserve as a raw material for both the food and thebiofuel sectors. Almost 2,000 farmers in India andup to 1,000 in Colombia have participated in thepilot project. The goal is to bring 100,000 ha underproduction in the medium term in Asia, Africa andLatin America, while also improving the technologytransfer methodology to facilitate replication.

[16]

18 |

• By adopting innovative business models,companies can work with BOP producers tosignificantly boost the quality and quantity oftheir agricultural production, thus expandingthe company’s supply base and the farmer’sincome

• Companies can expand and deepen marketsfor agricultural inputs by developing productstargeted to BOP producers’ needs, adoptingnew retail distribution strategies combined withcredit access and other services, andextending training and information to farmers

• Demand-driven models are most effective forboosting production; agricultural, food andbeverage companies that support BOPproducers at each step of the farming andmarketing process can secure the best results

For many companies, financing a long-term R&Deffort to develop products for a low-margin marketposes a financial challenge. In some cases, publicfinancing or private donor funding can help catalyseR&D focused on BOP needs. The ConsultativeGroup on International Agricultural Research(CGIAR), for example, is a donor-funded organizationthat works with governments, private enterprisesand NGOs. The organization conducts research oncrops and other commodities that benefit poorfarmers. The CGIAR provides genetic and breedingmaterials to other research organizations, whichadapt them to local conditions and make themavailable to private seed companies. This approachhas produced hybrid maize breeding lines in Mexicoand other parts of Latin America through the work ofCentro International de Mejoramiento de Maíz yTrigo (CIMMYT), and hybrid millet, sorghum andpigeon pea lines in parts of India and Africa throughthe work of the International Crops ResearchInstitute for the Semi-Arid Tropics, (ICRISAT)

[17]. The

adoption of these technologies varies widelybetween countries and regions, and faces greaterlimitations in Africa.

Improving farmers’ access to agricultural inputs

Even when appropriate inputs are available in-country,poor farmers have to overcome both logistical andfinancial hurdles to access them. In sub-SaharanAfrica, farmers face some of the highest fertilizer pricesworldwide, a trend that worsened as global fertilizerprices nearly doubled in 2007-2008. Distance is alsoa barrier: 40% of African farmers live four hours ormore from the nearest input retailer.

[2]A lack of financial

services and fertilizer subsidies makes purchasesimpossible for many at the start of the planting season,when cash supplies are low. As a result, Africanfarmers have the lowest rates of fertilizer useworldwide, using only 13 kg per hectare compared to190 kg per hectare in East Asia.

[2]Some companies

are introducing innovative approaches to extendtheir distribution networks to small-scale farmersthrough direct investment or partnerships withintermediaries. These models have several commonelements: a) they aggregate both farmers’ goodsand buyers’ demand to create critical mass; b) theyact as a two-way trading platform; and c) they bundleservices and products to enhance their appeal.

| 19

International Development Enterprises India (IDEIndia) is a social enterprise that engages with small-scale farmers by supplying manually operatedtreadle pumps. The pumps help farmers to boosttheir productivity, increasing their earnings byaround US$ 400 per annum. The cost of the pumpcan be recovered within three months from the firstharvest. In order to build awareness of the benefitsof irrigation pumps, IDE India conducts live andvideo demonstrations and distributes flyers. Theyalso engage the support of village opinion leaders –influential farmers who are trained to market theproduct to their peers.

IDE India trains farmers to use and repair thepumps; select crops, planting material and fertilizer;and utilize market information. To keep retail priceslow, product manufacturing is outsourced to localmanufacturers, who follow a stringent qualityassurance program and participate in IDE India’s

warranty scheme. The enterprise has also facilitatedpartnerships in service hubs that provide processingfacilities and allow for intermediary sales of produce.In addition, IDE India facilitates an innovativefinancing mechanism, where the agricultural inputcompanies directly finance the farmers, thusbypassing the need for external financiers.

This broad-based support has helped farmersincrease their productivity; many have doubled theirincome within two years of purchase. IDE India hasalso created jobs by establishing and training localdistributors. This multi-pronged approach hasproven highly successful for the commercial pumpsuppliers and, to date, more than 650,000 treadlepumps have been sold through IDE India’s networkof dealers and distributors.

Source: International Development Enterprises,India[15]

Box 1 – International Development Enterprises, India: A coordinated approach to servicing small-scale farmers

Retail hubs in high-density areas. In rural India,Godrej Agrovet Ltd, a leading agribusinesses player,has established a chain of rural outlets, each servingapproximately 20 villages and 20,000 farmingfamilies. These outlets offer one-stop shops,providing agricultural equipment and useful servicessuch as soil and water testing, veterinary andfinancial services, post offices and pharmacies. Thecompany has partnered with other companies, suchas Tata Agrico (a subsidiary of Tata Steel) to expandits offering of services

[18]. Other farm outlets in India

are starting to provide weather and commodity priceinformation and even trading services. Some retailhubs offer post-harvest services such as processingand warehousing.

Empowerment of retailers in low-density areas.In low population density or remote rural areas,companies can link to micro retail networks todeliver supplies and to disseminate knowledge tofarmers. Some companies have empowered localretailers to become their dealers and to educatefarmers on the use and benefits of their products.The dealers receive training in both technicalknowledge and retail management skills. BayerCropScience introduced practical, small packagesizes of fertilizer and pesticides in Kenya whilesimultaneously running its Green World trainingprogramme,

[19]which also provided training for more

than 2,000 dealers on crop protection andagricultural practices. Such agro-dealer networkscan provide both dealers and farmers with access tofunding. In another Kenyan example, Equity Banklaunched a US$ 50 million credit line for 15,000agro-dealers and other small-scale enterprisesoperating along the food value chain. In complementto this initiative, the Government of Kenya launcheda subsidy programme through which farmers canredeem vouchers at agro-dealer stores to expandaccess to and demand for inputs

[20].

Strengthening farmer capacity

Farmers in developing countries often lack technicalinformation on new products and farming techniquesand, given the limitations of government-sponsoredagricultural extension services, have fewopportunities to access training. Smallholders oftenhave many dependents and limited income, with norisk protection or safety net. Given their high

exposure to risk, they are understandably cautiousabout trying new products and techniques. Privatecompanies, which trade with farmers as eitherbuyers or suppliers, can bridge this gap by offeringfarmer training programmes – so-called outgrowerschemes – increase farmers’ knowledge andwillingness to adopt the new technology.

Training and outreach by agricultural suppliers.Seed and fertilizer companies have taken the lead inproviding coordinated educational and trainingservices to farmers. Both sides benefit from theseprogrammes. Farmers gain know-how and themeans to improve their productivity, while suppliersbenefit from feedback and customer loyalty.Suppliers can take these programmes a step furtherby adding services that will not only improveproductivity but also enable farmers to enter newmarkets or to meet more stringent qualityrequirements.

In Brazil, seed company Bayer CropScience hascollaborated with HortiBrasil, an NGO, to enable 500small-scale fruit producers obtain an internationalcertification through the Garantia de Sabor – the“good flavour guarantee” – label. Bayer suppliesseeds and education to farmers through anoutgrower programme,

[21]while third-party monitors

regularly review their adherence to sustainablefarming techniques and certify the quality standardsof the fruit. In parallel, Bayer builds marketacceptance by educating wholesale traders aboutthe new label. The produce sold under the label ispriced at a premium in retail markets and is suitablefor export, providing a considerable opportunity forfarmers to improve their productivity and incomes.By investing in the brand, the partners hope tocreate regular consumer demand for the products inlocal and international markets.

Training and capacity-building by buyers.Buyers or traders who want to ensure adequatesupply and quality often develop outgrowerprogrammes with farmers. These programmes canrange from supplying seeds and fertilizers toproviding training and monitoring programmes.Under these programmes, buyers will guaranteepurchase of certain volumes at specified prices.They will sometimes make payments in advance ofthe harvest, smoothing out cash flow and creating

20 |

stability that can give farmers the confidence toinvest in goods and services that will further improvetheir incomes. Such advance-payment schemesmust be structured equitably to ensure a competitiveprice at harvest time.

Buyers can also take an extra step and ensure thatpost-harvest loss is minimized between farm andfactory, thereby increasing profitability for bothfarmers and wholesalers. Metro Cash & Carry, oneof the largest food wholesalers in Vietnam, buysfresh produce from several smallholders in the LamDong province, a vegetable-growing region. Inpartnership with local authorities and NGOs, Metrohas invested in training programmes for farmers andother small-scale service providers along the foodsupply chain. So far the company and its localpartners have trained 18,000 farmers in Vietnam andare running similar programmes in other countries.

[22]

Improving market linkages and supply chainefficiency

Inefficient supply chains raise costs and reduceprofits for companies and farmers alike. Investmentsin better transportation, warehousing, infrastructure,storage and intermediaries can boost returns overthe long term for all participants in the supply chain.

Improving logistics and warehousing. Post-harvestlosses in developing regions can be significant. Forperishable products, such as milk and vegetables,50% of the product may be spoiled before it reachesthe consumer market. Losses affect farmers bothdirectly (when their products spoil before sale) andindirectly (by lowering prices paid by traders andprocessors, who are also affected by wastage).Investing in on-farm processing, warehouse systems,logistics and training can increase the speed and

| 21

efficiency of delivery to market. Sometimes, simplemeans are sufficient. Metro’s Cash & Carry outlet inIndia suffered losses in its tomato supply as high as40%. It turned out that during their breaks, handlerssat or slept on top of bagged tomatoes. Bychanging its packaging to crates, Metro was able toreduce waste to 15%.

[23]TNT, a global mail, express

and logistics provider, has provided analyses andrecommendations to public agencies and partnershipswith a goal of improving efficiency of transport andsupply chain networks in several African countries toreduce transport costs and travel time.

[24]

Investing in intermediaries that add value. Whileintermediaries in developing markets are often seenas one of the main causes of supply chaininefficiency, they can be useful in providing funding,marketing, logistics and other goods or services thatwould be otherwise unavailable to farmers. Theymay also hold valuable knowledge about producercommunities that they can communicate to buyers.Moreover, they help aggregate a highly fragmentedsupply base, increasing efficiency for buyers whowant to buy larger volumes of produce. Companiesneed to determine which intermediaries add value,so that they can then be supported. Retailer PT

Carrefour Indonesia has done this with freshproduce wholesaler Bimandiri. The wholesaler helpsCarrefour establish and enforce quality and quantitystandards and, at the same time, helps smallholdersto receive a negotiated and fair price.

[25]

Optimizing of sourcing processes

Local procurement systems can benefit poor farmersas well as processing and retail companies.Initiatives to establish such systems are often theresult of commercial incentives to reduce costs.These can entail replacing high-cost imports withlow-cost local goods or new products developedlocally.

Switching from imports to local sourcing. Risingdemand for processed foods, combined with hightariffs and increasing production costs, are drivingcompanies to view local small-scale farm produceas a viable alternative to imports. For example, toincrease its supply of high-quality corn in China,General Mills switched from imports to local sourcingand reduced procurement costs by 25% in theprocess. The company currently sources corn forthe Chinese version of its Bugles snack from 528

22 |

small farms in Yongqing Village, in the Heilongjiangprovince. General Mills partnered with a local miller,Xingda, which provided logistical support andmanaged local relationships.

[26]Such partnerships

are essential in improving farmers’ efficiency and totap the benefits these farmers can add in terms ofcosts, reliability and quality. Likewise, Olam, one ofNigeria’s largest food processing companies, haspartnered with the United States Agency forInternational Development (USAID) to procure ricefrom small-scale farmers after an increase in tariffsmade imports less attractive. Olam provided farmerswith inputs, technical assistance and access toprocessing facilities. Because the farmers needed toproduce a better and more consistent quality, Olamand USAID also established model farms, used forextensive training and research. In addition, Olamlaunched a high-quality branded rice product toensure it would capture sufficient margins. Collaborationwith Olam resulted in an average yield increase of75% in the first two years and a net income growthof over 155%. The programme currently involvesover 8,000 farmers.

[27]Such local-supply

programmes can maximize value capture whenfocused on premium products. However, as SABMiller has proven (see Box 2), sourcing for lower-priced products can benefit smallholders as well.

Commercializing local raw material. Local staplecrops or raw materials often hold untapped potentialfor commercialization. Unilever has cooperated witha wide range of partners to unlock hidden value inprocessing the Allanblackia seed, a traditionalsource of cooking oil in a number of Africancountries. The resulting Novella Africa project hasdesigned a supply and processing chain to procure,extract and market the oil as an alternative to othervegetable oils in soap and processed foods. In theproject’s second commercial phase, farmers aresupplying several additional processing companies.One of the key success factors is cooperationamong the private sector, government and NGOpartners, which provided an international perspectiveand on-the-ground experience. This enabled theinitiative to be scaled out from Ghana to Tanzania,Nigeria, Liberia and Cameroon.[29]

| 23

Liu Fuyou, farmer, People’s Republic of China

Liu Fuyou lives in Yongqing Village in Heilongjiangprovince in China. For generations, his family hasbeen growing corn on 2.5 acres of land. In 2003,Fuyou signed a contract farming agreement withGeneral Mills, which guaranteed an above-marketprice for 100% purchase of his crop. GeneralMills provides technical assistance, quality seedsand financing for purchasing inputs such asfertilizers. Liu Fuyou previously had no access tosuch services, and his income varied unpredictablybased on weather and market prices.

Since becoming a contract farmer, Liu Fuyou’syields have tripled. His household income hasmore than tripled, from a range of US$ 680-800to US$ 3,300. Liu Fuyou has invested theincreased income in improving the life of hisfamily. He built a new house to replace theirprevious mud and grass structure, and installedstorage buildings and a perimeter wall. He alsobought a small tractor, a television, radio, mobilephones and other household appliances. Thefamily has improved its diet, buying more meatand varied foodstuffs.

Similar impacts are visible in the livelihoods ofother contract farmers in the community. Manyfamilies have invested in housing improvements,tractors and motorcycles, and other items.Increased spending has catalysed the growth oflocal micro-enterprises such as small shops andrestaurants. The village road has been paved,improving the community’s access to nearbytowns and markets.

Source: General Mills 2008[28]

Building markets for high-value sustainabletrade. Trade barriers, inadequate logistics and alack of agents to advocate and promote productsgenerally restrict or prevent small-scale farmers fromaccessing high-end markets. Sustainable tradepractices, partly based on principles of the fair trademovement, help farmers circumvent such roadblocks.The main aim is to provide consumers with food thathas been grown in accordance with environmental,health, safety and fair-wage or pricing standards.Sustainable trade practices also make the sourcingand certification process an essential part of the finalconsumer product, justifying a price premium. Forexample, the cooperative Kuapa Kokoo, representing40,000 cocoa farmers in Ghana, partly owns DivineChocolate Ltd, a trading company that markets apremium chocolate made with Kuapa Kokoomembers’ products.[31] Although adhering tosustainable trade practices, the brand also targetsthe broader market for high-quality chocolate.

Large companies are increasingly applying theseideas in their international supply chains. Forexample, Kraft Foods sources several keycommodities from developing countries facingunique environmental, economic and socialconcerns. In the early 1990s, the company beganadopting sustainable practices in procuring coffee. In2003, the company sought certification from theRainforest Alliance certification. Certified productscomply with the Sustainable Agriculture Networkd

standards for protecting wildlife, wild lands, workers’rights and local communities. Today, with eightcoffee brands in more than 20 countries carrying theRainforest Alliance seal, Kraft is the largest buyer ofRainforest Alliance Certified beans.[32]

24 |

Brewer SABMiller has rolled out several newproduct innovation, quality improvement and importsubstitution projects in Africa and India. Whenidentifying suitable regions, SABMiller looks atgrowing markets with an undersupply in agriculturalproducts, supportive partners, and existinginfrastructure in critical areas such as water supplyand transportation. One of the key challenges isidentifying and managing relationships withgovernment, NGO partners and other stakeholders.Currently over 10,000 smallholder farmers areinvolved in projects in India, Tanzania, South Africa,Uganda and Zambia. The company expects toincrease the number of participating farmers to30,000 by 2012. In most cases, the businessbenefits have already exceeded the initial investmentand farmers have seen a significant increase in theirincomes.

With the introduction of the Eagle Lager brand inUganda, SABMiller expanded its import substitutionmodel and redesigned its products to accommodatethe availability of local supplies of sorghum. Thebrewer participated with the local government inresearch on sorghum and designed a supply chainthat accommodates small-scale farmers. WhileSABMiller also works with commercial farmers, forthe Eagle brand it is committed to buying fromsubsistence and more vulnerable producers. Thebrand is expected to provide direct financial benefitsto more than 5,000 farming families in 2009.

Source: SABMiller Company Information 2008[30]

Box 2 – SABMiller: Global smallholder sourcing strategy

d The Sustainable Agriculture network is an internationalcoalition of leading conservation groups

3.2 Business solutions for consumers

Companies often find it difficult to access the BOPas a consumer market, since they generally havelow and fluctuating incomes and are often located atthe end of informal and inefficient market chains. Inaddition, there is little information available on theirbehaviour and preferences, and marketing strategiesdevised for higher-income markets are oftenineffective in creating or strengthening consumerdemand. Companies can overcome these obstaclesand launch successful products by introducing newproducts developed through well-targeted design,cost-efficient processing and effective marketing.Executing such business models effectively oftenrequires partnerships with other organizations.

Designing nutritious food for poor consumers

Nutritional deficiencies cause substantial damage tohuman health and economic productivity. Providingfood enriched with micronutrients such as iron andvitamin A is recognized as one of the most cost-effective solutions. Fortified foods in the form ofenriched staples, such as flour and salt, orprocessed foods with nutritional supplements are aneffective delivery mechanism for such micronutrients.Although fortifying food is technically a relativelystraightforward process, large-scale fortificationefforts have to overcome a number of hurdles. Manydeveloped countries lack regulation, leaving foodcompanies to introduce fortification on a voluntarybasis, often at added cost. Consumers may bewilling to prioritize fortified foods once aware of theirbenefits, but reaching them with the information is achallenge. Companies seeking to provide fortifiedfoods to the BOP must therefore invest in effectiveand affordable products, establish cost-effectivelocal processing capacity and undertake welldesigned and targeted marketing campaigns.

For these reasons, many food fortificationprogrammes still involve donor funding, at least inthe development or transitional phases. Donorfunding often focuses on supporting fortification ofstaple foods, due to their broader reach and lowercost. Processed foods, by comparison, are moreoften sold at a premium. However, several foodcompanies have achieved commercial success withfortified products, based on transitional or no donor

funding. As income levels rise among the BOP,those with discretionary income can become a strongmarket for nutritionally enhanced products. Successrequires creating low-cost products that meet marketconditions and have durable packaging, a long shelflife and little need for clean water or electricity.

Brittania Industries, the Naandi Foundation and theGlobal Alliance for Improved Nutrition (GAIN) recentlycooperated to make fortified foods more widelyavailable for lower-income groups in India. Britanniais a leading Indian food manufacturer and its biscuitsreach more than 70% and 45% of urban and ruralmarkets, respectively. The Naandi Foundation is apublic trust that focuses on the protection of childrights, particularly in education and nutrition. GAIN isa Swiss foundation that works to catalysepartnerships and create an enabling environment forfortification. The partners utilized Naandi’sestablished infrastructure of school feedingprogrammes in Andhra Pradesh to distribute iron-fortified biscuits to over 150,000 children. Britanniahas now launched commercially an iron-fortifiedversion of its popular Tiger biscuits called Bananabiscuits. Over 2 billion packets of Banana biscuitshave been sold to date using traditional marketchannels to reach the general population. In additionto improving children’s nutritional status, the initiativehelped Britannia to gain insight into the BOPconsumer market and position itself as a foodcompany with a nutritional focus. Furthermore, itcreated opportunities to explore the development ofadditional lines of fortified food products for bothlow-income and affluent consumers.[33]

| 25

The French company Nutriset developed a ready-to-use peanut-based paste, Plumpy’Nut, to providenutritional support to malnourished children indeveloping countries. In addition to tasting good, thepaste is packaged in foil packets so that it can bedistributed easily throughout relief camps and otherchallenging environments. To reduce cost andexpand distribution, the company has set up afranchise system in Central and Eastern Africa tolicense Plumpy’Nut to local producers.[34]

Expanding retail distribution networks

One of the main challenges to commercial enterprisein BOP markets is reaching consumers. While allpoor consumers tap into retail networks to purchaseessential goods, these mostly informal systems areoften comprised of multiple small-scaleintermediaries with limited incentive or opportunity tocreate economies of scale. Poor infrastructure, suchas roads and warehousing, compounds existinginefficiencies and raises costs. As a result, the pooroften pay higher costs per unit for essential servicesthan wealthier members of the community, the so-called “BOP penalty”. Companies can reducedelivery costs and make goods more affordable toconsumers through both conventional andunconventional means. Effective strategies includeworking with existing informal channels, trainingentrepreneurs and collaborating with othercompanies.

Leverage informal retail and distributionnetworks. Providing small-scale retailers with toolsand information can allow companies to utilizeexisting informal trading channels and turn small-scale retailers into product agents, therebyexpanding their reach. Given the right training andtools, many poor consumers themselves canbecome successful small-scale retailers, assistingcompanies providing last-mile access to theconsumers that are hardest to reach. In Brazil,Nestlé engages rural women to operate asdistributors. They travel door-to-door demonstratingproduct benefits and selling directly to consumers.By creating incentives for local retail entrepreneursrather than hiring salaried employees or franchiseholders, the company reduces its need to monitorindividual sales performance. Once a company hasestablished a critical mass of micro-retailers, it canstart to provide additional services such as credit orportfolio expansion. These arrangements helpcompanies build trust within a community and reachthe target segment efficiently.

Organized retail is one of the fastest growing sectorsin developing countries. For example, in Thailand,the US$ 56 billion retail market has grown annuallyby 12% since 2002.[36] While they are sometimesseen as a threat, large-scale retailers can alsoprovide commercial opportunities for small-scaleentrepreneurs. Instead of striving to replace micro-retailers, some of these large players are partneringwith them to extend their own footprint. India’sSubhiksha Trading, an arm of Subhiksha, an urban

26 |

supermarket, pharmacy and telecom chain, forexample, is becoming a wholesaler to micro-retailersin urban and suburban areas.[37]

Business-to-business collaboration to extendand improve distribution networks. Collaborationwith other companies can help reduce delivery coststo the BOP. Hariyali Kisaan Bazaar, a rural retailchain managed by DCM Shriram Consolidated Ltdin India, bundles the services and products of 80different suppliers into one single store.[38] Mi Tienda,a Mexican retail association, helps small rural shopsmaintain a diversified and current inventory. Theorganization’s network of regional buyers acts as anintermediary between large wholesalers and thesmall shops. They deliver fresh produce daily, evenin small quantities.[39] Such initiatives save costs,diversify inventory and expand distribution networks.

Strengthening consumer demand througheffective marketing

Educational marketing. Since they are unfamiliarwith many commercial products, BOP consumerscommonly look to trusted sources such as friendsand family for advice in making purchasingdecisions, rather than relying on messages from themedia. Numerous companies have developedinnovative pathways of communication, oftenborrowing from social marketing models to useword-of-mouth advocacy, peer marketing, villagemeetings and performance art.

Creation of partnerships with “trusted parties”.Successful marketing strategies often depend onpartnerships, especially with organizations andbrands that are deemed trustworthy. In China, a

| 27

In launching a national campaign to combat irondeficiency, China’s Center for Disease Control (CDC)partnered with GAIN and Zhenji (Shijiazhuang ZhenjiBrew Group Co., Ltd), a leading soy manufacturer,to introduce an affordable soy product fortified withiron. The campaign has been a major success for allplayers. Sales of the fortified soy sauce increasedfrom 1,500 to 20,000 tons per year over two years,reaching sales of nearly US$ 5 million. The productis marketed in nearly 90% of Chinese stores that sellsoy sauces. Zhenji increased production capacity to100,000 tons per year to meet growing demand.Awareness levels among high-risk individuals inmany provinces was close to 100%, and anaemiarates fell from 20% to approximately 8%.

Several key strategies helped drive this success:

• Aligning public and private incentives: CDCprovided the fortification formula and manufacturingtechnology to Zhenji for free and conducted anationwide educational campaign. In return, thecompany agreed to keep the price affordable.

• Leveraging public-sector resources: CDC createdteams at national and local levels to manage

relationships with various government agencies,including coordination with the health departmenton quality control.

• Clear value proposition to consumers: Thecampaign offered consumers a superior productwith health benefits priced at only 1 cent more perbottle than traditional soy products, which was farcheaper than medicinal treatments for iron-deficiency anaemia (IDA).

• Combined marketing efforts: The CDCspearheaded an educational media campaignthrough TV, newspapers, flyers, and other mediathat targeted consumers directly. It was able topromote the product on television through itsaccess to free “educational” airtime. This lentgovernment credibility and raised awareness of theproduct, while lowering costs for Zhenji. Zhenjifocused its marketing efforts on retailers and ruraldoctors, using promotions and discounts to drivetraffic to stores and garner support for the product

Source: Global Alliance for Improved Nutrition, 2008[35]

Box 3 – Zhenji: Fortifying soy sauce in China

successful marketing campaign for a fortified soysauce involved China’s Center for Disease Control(CDC), a governmental institution that is viewed bylocal consumers and medical professionals as theleading authority on nutrition. (See box 3)

Certification and labelling. Certified labels help todifferentiate products and increase consumer trust.When the South African government introducedlarge-scale fortification of maize flour, it developed adistinctive logo to set the product apart. One of thekey lessons of this project, however, was thatcertified labels require a level of investment andmarketing similar to that required for brandedproducts. After initial donor funding for the start-upphase, the maize fortification project is fullycommercially viable.[40]

3.3 The case for holistic solutions

While many companies engage in just one stage ofthe food value chain, holistic approaches can unlockeven greater value. Holistic business models takeinto account all three roles played by the BOP – thatof producers, consumers and entrepreneurs – and