the johannesburg office market shows resilience persistent ... 2017 johannesburg... · 1 central...

TRANSCRIPT

1 CentralLondonOfficeMarketReport | Q3 2016

Johannesburg Office Market ReportTheJohannesburgofficemarketshowsresilienceinthemidstofweightypoliticaluncertaintyandthepersistentpooreconomicenvironment.

Q1 2017

2 JohannesburgOfficeMarketReport | Q1 2017

Overview

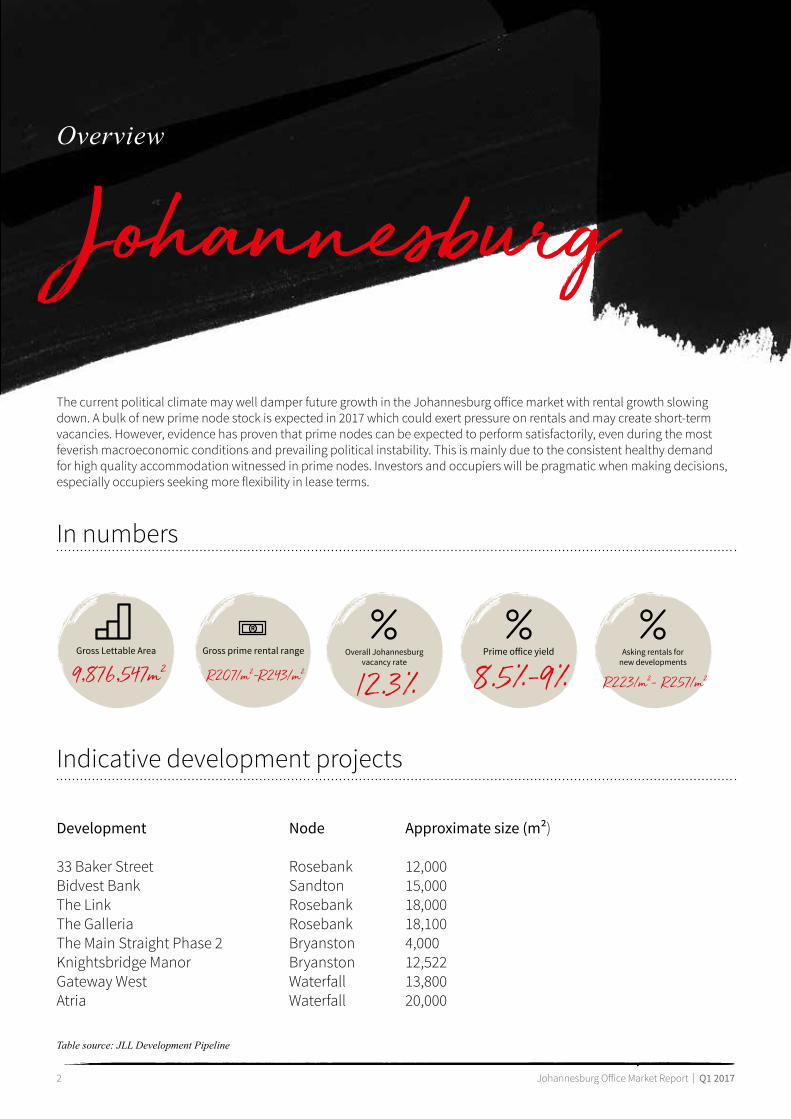

JohannesburgThecurrentpoliticalclimatemaywelldamperfuturegrowthintheJohannesburgofficemarketwithrentalgrowthslowingdown.Abulkofnewprimenodestockisexpectedin2017whichcouldexertpressureonrentalsandmaycreateshort-termvacancies.However,evidencehasproventhatprimenodescanbeexpectedtoperformsatisfactorily,evenduringthemostfeverishmacroeconomicconditionsandprevailingpoliticalinstability.Thisismainlyduetotheconsistenthealthydemandforhighqualityaccommodationwitnessedinprimenodes.Investorsandoccupierswillbepragmaticwhenmakingdecisions,especiallyoccupiersseekingmoreflexibilityinleaseterms.

Gross prime rental range

R207/m²-R243/m²Gross Lettable Area

9,876,547m²Overall Johannesburg

vacancy rate

12.3%Prime office yield

8.5%-9%Asking rentals for

new developments

R223/m²– R257/m²

Innumbers

Indicativedevelopmentprojects

Development

33BakerStreetBidvestBankTheLinkTheGalleriaTheMainStraightPhase2KnightsbridgeManorGatewayWestAtria

Node

RosebankSandtonRosebankRosebankBryanstonBryanstonWaterfallWaterfall

Approximate size (m²)

12,00015,00018,00018,1004,00012,52213,80020,000

Table source: JLL Development Pipeline

3 CentralLondonOfficeMarketReport | Q3 2016

Issue to watch :Theclimateisripeformoreflexibleleaseterms

andshowcasesthebenefitsoftheco-working

environment.

4 JohannesburgOfficeMarketReport | Q1 2017

DemandGeneral overview of SA’s current economic state

Thefirstquarterof2017wasthemosteventfulthreemonthsforSouthAfricasincethe“Nenegate”sagain2015,withpoliticsyetagaintakingcentrestage.Whilesomemayhavebeenshockedbythepresident’sdecisiontoreshuffletheexecutivecabinet,inrealitythiswasanexpectedalthoughunwelcome,decisionbythemarket.

Negativefeedbackheraldedthestartof2017withStatsSAreportinganeconomicgrowthof0.3%for2016,whichwaslowerthantheforecasted0.5%.ThismayhavebeendrivenbytheconsecutivenegativegrowthinGDPoverthelasttwoquartersof2016.

Zooming in on the Johannesburg Office MarketDespitethenegativity,marketactivityhasnotsloweddowninthefirstquarterof2017,withsignsofahealthydemandforhighqualityaccommodationmainlyinprimenodes.Recentlyconcludedtransactionsandotherdealsinthepipeline,suchasBidvestBank’smovetoSandton,illustratethis.

Thesetransactionscementthefactthattherewillstillbedemandforofficeaccommodation(mainlyforhighqualitygradeAandPstock).Howeveroccupiers,particularlysmallandmediumbusinesses,willbelookingformoreflexibleleaseterms.Landlordsshouldexpecttonegotiateforshorterterms,forinstanceathree-yearleaseinsteadoffive.Thedrivingfactorforthesechangeswillbea“fearoftheunknown”approach.Itwillnotbeeasyforbusinessestoforeseehowseverelythecreditdowngradewillaffectthemsocautiousmaybethewayforward.

Recently concluded deals

Table source: SARB, Stats SA

Source: JLL

Economic growth (2016)

0.3%

Repo rate

7%

CPI (March 2017)

6.1% Unemployment rate

26.6%

Prime lending rate

10.50%

Cricket South AfricaGlenhove - 4,000m²

Standard BankRosebank - 12,000m²

SABBryanston - 8,000m²

Anewtrendthathasbeenadisruptorfortheconventionalofficemarketisco-workingofficeaccommodation.Whileitsimpactontheestablishedofficemarkethasbeenminimalsofar,itwillserveasaworthyalternativeforsmallcompaniesavoidingexpansionsorenteringnewleasesinthesetryingtimes.Co-workingisstillinitsinfancystageinSouthAfrica,howeverthereareclearsignsofbusinessesbecomingmorereceptivetothistypeofoperationalenvironment.Consultancies,technologyrelatedcompaniesandsmallbusinessesareseentoberespondingwelltothisnewtrend

Needlesstosay,dealswillbehardtocomebyasbusinessesmayfreezeorpostponeanydecisionstomoveorexpandoffices.Andthisiswhereco-workingspaceswillcapitalise.Thesenewaccommodationoptionsofferseveralbenefits:

•flexibility-in“leasetermsandtoemployees•mobility-animportantfactorforglobalisation•noofficeset-upcostsallowingmorecapitalforinvestmentingrowthopportunities.

Perhapsthebiggestadvantageofthesharedworkspaceisitofferstenantstheopportunitytorentonaneed-bebasisunlikeconventionaloffices.Despiteallthepositives,theimpactofco-workingofficesisforecasttoremainminimalintheofficemarketduetosomeofitslimitationslikeavailabilityofparkingspace.

5 JohannesburgOfficeMarketReport | Q1 2017

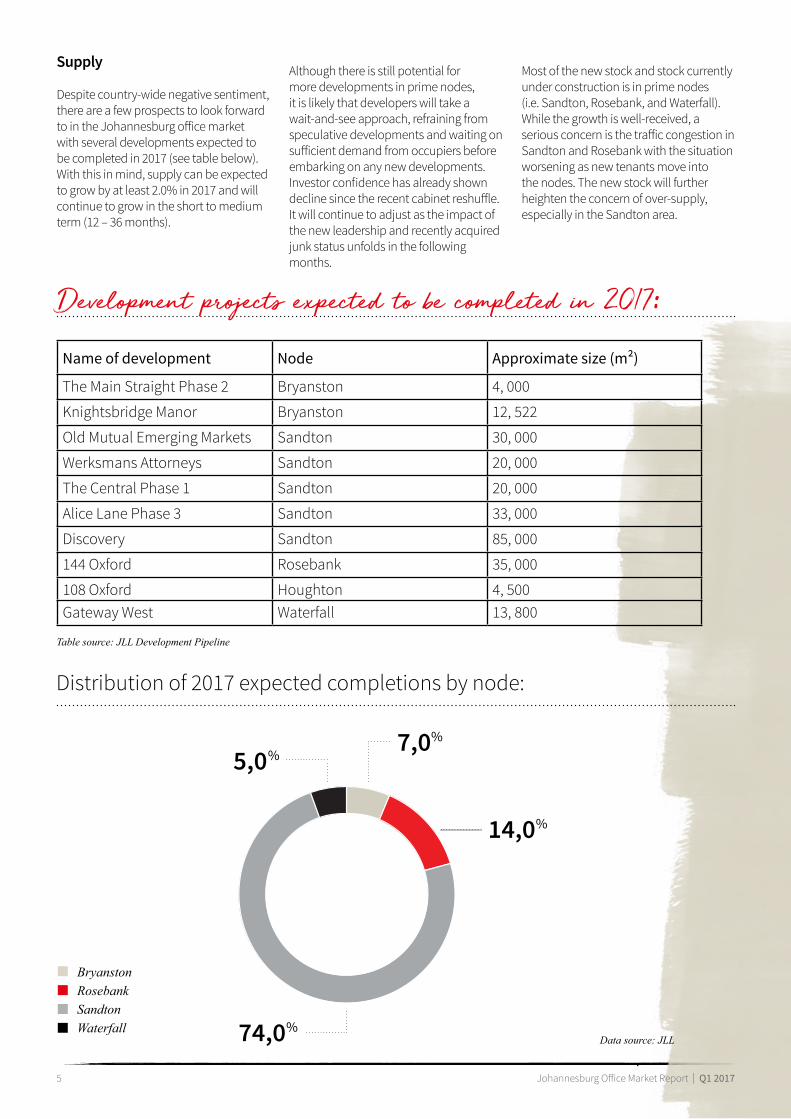

Supply

Despitecountry-widenegativesentiment,thereareafewprospectstolookforwardtointheJohannesburgofficemarketwithseveraldevelopmentsexpectedtobecompletedin2017(seetablebelow).Withthisinmind,supplycanbeexpectedtogrowbyatleast2.0%in2017andwillcontinuetogrowintheshorttomediumterm(12–36months).

Althoughthereisstillpotentialformoredevelopmentsinprimenodes,itislikelythatdeveloperswilltakeawait-and-seeapproach,refrainingfromspeculativedevelopmentsandwaitingonsufficientdemandfromoccupiersbeforeembarkingonanynewdevelopments.Investorconfidencehasalreadyshowndeclinesincetherecentcabinetreshuffle.Itwillcontinuetoadjustastheimpactofthenewleadershipandrecentlyacquiredjunkstatusunfoldsinthefollowingmonths.

Mostofthenewstockandstockcurrentlyunderconstructionisinprimenodes(i.e.Sandton,Rosebank,andWaterfall).Whilethegrowthiswell-received,aseriousconcernisthetrafficcongestioninSandtonandRosebankwiththesituationworseningasnewtenantsmoveintothenodes.Thenewstockwillfurtherheightentheconcernofover-supply,especiallyintheSandtonarea.

Development projects expected to be completed in 2017:

Distributionof2017expectedcompletionsbynode:

Name of development Node Approximate size (m²)

TheMainStraightPhase2 Bryanston 4,000

KnightsbridgeManor Bryanston 12,522

OldMutualEmergingMarkets Sandton 30,000

WerksmansAttorneys Sandton 20,000

TheCentralPhase1 Sandton 20,000

AliceLanePhase3 Sandton 33,000

Discovery Sandton 85,000

144Oxford Rosebank 35,000

108Oxford Houghton 4,500GatewayWest Waterfall 13,800

14,0%

74,0%

7,0%

5,0%

BryanstonRosebankSandtonWaterfall

Table source: JLL Development Pipeline

Data source: JLL

6 JohannesburgOfficeMarketReport | Q1 2017

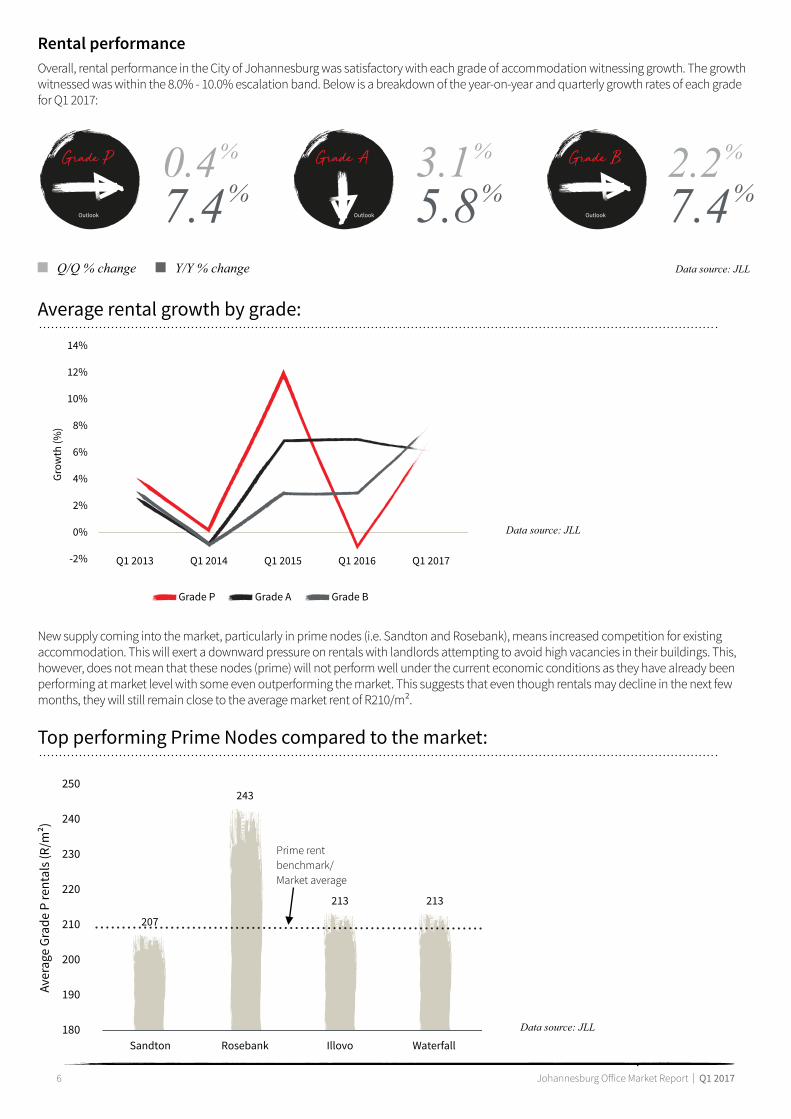

Newsupplycomingintothemarket,particularlyinprimenodes(i.e.SandtonandRosebank),meansincreasedcompetitionforexistingaccommodation.Thiswillexertadownwardpressureonrentalswithlandlordsattemptingtoavoidhighvacanciesintheirbuildings.This,however,doesnotmeanthatthesenodes(prime)willnotperformwellunderthecurrenteconomicconditionsastheyhavealreadybeenperformingatmarketlevelwithsomeevenoutperformingthemarket.Thissuggeststhateventhoughrentalsmaydeclineinthenextfewmonths,theywillstillremainclosetotheaveragemarketrentofR210/m².

Data source: JLL

Data source: JLL

Data source: JLL

Rental performanceOverall,rentalperformanceintheCityofJohannesburgwassatisfactorywitheachgradeofaccommodationwitnessinggrowth.Thegrowthwitnessedwaswithinthe8.0%-10.0%escalationband.Belowisabreakdownoftheyear-on-yearandquarterlygrowthratesofeachgradeforQ12017:

Grade P

Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017-2%

0%

2%

4%Grow

th (%

)

6%

8%

10%

12%

14%

Grade A Grade B

250

240

230

220

210

Aver

age

Grad

e P

rent

als (

R/m

²)

200

190

180Sandton Rosebank Illovo

207

213

243

213

Prime rentbenchmark/Market average

Waterfall

Average rental growth by grade:

Top performing Prime Nodes compared to the market:

Grade P

Outlook

Grade A Grade B

OutlookOutlook

0.4%

7.4%3.1%

5.8%2.2%

7.4%

Q/Q % change Y/Y % change

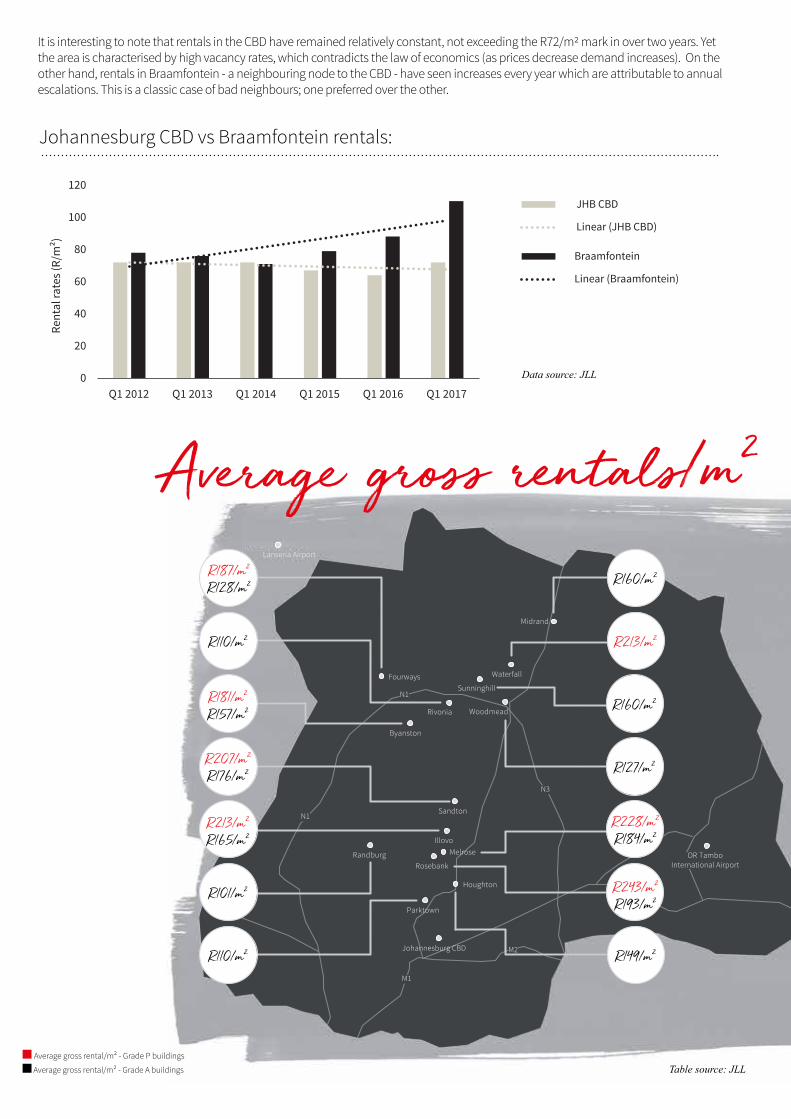

ItisinterestingtonotethatrentalsintheCBDhaveremainedrelativelyconstant,notexceedingtheR72/m2markinovertwoyears.Yettheareaischaracterisedbyhighvacancyrates,whichcontradictsthelawofeconomics(aspricesdecreasedemandincreases).Ontheotherhand,rentalsinBraamfontein-aneighbouringnodetotheCBD-haveseenincreaseseveryyearwhichareattributabletoannualescalations.Thisisaclassiccaseofbadneighbours;onepreferredovertheother.

Q1 20120

20

Rent

al ra

tes (

R/m

²)

JHB CBD

Linear (JHB CBD)

Braamfontein

Linear (Braamfontein)

40

60

80

100

120

Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017

JohannesburgCBDvsBraamfonteinrentals:

Data source: JLL

Rosebank

Houghton

Fourways

Byanston

Rivonia

Sunninghill

Sandton

Waterfall

Illovo

M1

N3

N1

N1

M2

Randburg

Lanseria Airport

R213/m²

R207/m²R176/m²

R187/m²R128/m²

R110/m²

R110/m²

R160/m²

R149/m²

R101/m²

R160/m²R181/m²R157/m²

R127/m²

R213/m²R165/m²

R228/m²R184/m²

R243/m²R193/m²

Johannesburg CBD

Woodmead

Midrand

Melrose

Parktown

OR TamboInternational Airport

Average gross rentals/m²

Table source: JLL Averagegrossrental/m²-GradePbuildings

Averagegrossrental/m²-GradeAbuildings

8 JohannesburgOfficeMarketReport | Q1 2017

Q1 2013

10.6%

11.4%

12.7%

12.3% 12.3%

9.5%

10.0%

Vaca

ncy

rate

(%)

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

Q1 2014 Q1 2015 Q1 2016 Q1 2017

Q1 20130.0%

Vaca

ncy

rate

(%)

2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

Q1 2014 Q1 2015 Q1 2016 Q1 2017

Prime nodes - Johannesburg

Decentralised Johannesburg

Johannesburg CBD + Braamfontein + Newtown

Vacancies

OverallJohannesburgvacancyrate:

Data: SAPOA

Data: SAPOA

Onayear-on-yearbasis,thevacancyrateremainedunchanged,whileonaquarterlybasisitincreasedfrom11.9%(Q42016)to12.3%inQ12017.TheCityofJohannesburgrecordedoneofthehighestvacancyratesamongthelargermetrosinSouthAfrica.AccordingtoSAPOA,thehighvacancyrateismainlydrivenbythehighvacancyratesintheinnercity.Whileprimenodescontinuetorecordthelowestvacancies,therehasbeenanincreaseinvacancyratesonaquarterlybasisgoingfrom7.2%to9.1%.Thisislikelyasaresultofnewstockinthemarketthathasnotbeenoccupiedyet.

Wecanexpecttoseeanincreaseinvacancyratesoverthenexttwotothreequartersasdevelopmentswithspeculativeportionswillbecomingtocompletion.Anotherdrivingfactorforvacancyincreaseswillbeupcomingofficeconsolidations(example:PWC,Discovery).Thegoodnewsisthattheseeffectswillnotbepermanentastherecontinuestobeverydynamicdemandforhighqualityofficeaccommodation.

9 JohannesburgOfficeMarketReport | Q1 2017

AfewmonthsagoitwouldhavebeensafetosaythattheJohannesburgofficemarketwillcontinuetoperformwellinthemediumtermdespiteweakeconomicconditions.Howeverrecenteventshavecreatedfurtherrestraintamongstdecisionmakersandwilldamageinvestorconfidenceinthecity.

A couple of things to expect in the short to medium term:

• Developmentactivitytoslowdownafterthecompletionofongoingdevelopments-fewernewprojectswillbeannounced.• Developerstoholdbackonspeculativedevelopmentsduetohigherriskofalackoftenants.• Potentialoccupiersnegotiatingfornewleaseswillseekflexibleandshorterleaseterms.• Vacancyratesexpectedtoincreasebeforeimprovinginfuture.

WhilemostdevelopmentsintheSandtonnodearetenant-drivenwithspeculativeportions,theremaybeanover-supplyofofficeaccommodationintheshortterm,thisislikelytocausedownwardpressureonrentalsinthearea.Needlesstosay,theramificationsofthecabinetreshuffleandthecreditdowngradearestilltobefeltinthefollowingmonths,possiblyyears,andmaybeworsethanexpected.TheSARBforecastGDPgrowthat1.2%for2017,butconsideringrecenteventsandfurtherpossiblecreditdowngradesbyotherratingagencies,SouthAfrica’sgrowthwilllikelyremainstagnantandbelow1%.Aseconomicgrowthandemploymentdatafeedstheperformanceoftheofficemarket,suppressedgrowthandhighunemploymentratesindicatestagnancyintheofficemarket.

Rental growthaccelerating

Rental growthslowing

Rentsbottomingout

Rents falling

Grade B

Grade A

The JLL Property Clock™

Grade P

Market outlook

10 CentralLondonOfficeMarketReport | Q3 2016

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. The information contained in this document is proprietary to JLL and shall be used solely for the purposes of evaluating this proposal. All such documentation and information remains the property of JLL and shall be kept confidential. Reproduction of any part of this document is authorised only to the extent necessary for its evaluation. It is not to be shown to any third party without the prior written authorisation of JLL. All information contained herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof.

JLL South AfricaJohannesburg3rd Floor, The FirsCnr Biermann & Cradock AveRosebank, South Africa, 2196Phone: +27 11 507 2200

Tom MundyHead: Research, Sub-Saharan [email protected]

Omphile Ramokhoase Head: Research, South [email protected]

www.jll.co.zawww.jllpropertysearch.co.za

Contact us

With other regional offices in Dubai, Abu Dhabi, Riyadh, Jeddah, Al Khobar, Cairo, Casablanca, Lagos and Nairobi