the itc compliance · pdf fileitc compliance network member policies & procedures manual...

TRANSCRIPT

ITC Compliance Network Member Policies & Procedures Manual v1.3

1

i

The ITC Compliance Network

The Concept From 14th January 2005, any business engaging in General Insurance activity must be

regulated by the Financial Conduct Authority (FCA), formerly the Financial Services

Authority (FSA).

General Insurance activity is not limited to sales and includes other areas such as

administration and claims handling. There may be a number of employees within your

business that will be subject to the FCA rules and regulations.

The ITC Compliance Network provides an alternative to full FCA authorisation, where a fully

authorised Firm (ITC Compliance) takes responsibility for the regulated activities of Network

Members.

The sole purpose of the Network is to ensure that your customer’s needs are at the

forefront of everything you do, providing them with information that is clear, fair and not

misleading. To ensure this ITC Compliance provide you with all of the administration tools,

training resources; professional indemnity insurance (excluding travel companies) and

processes you need to enable you to sell General Insurance products in line with the FCA’s

Treating Customers Fairly (TCF) outcomes.

ITC Compliance also takes away the burden of being directly authorised by the FCA.

In line with clause 3.1.iii of the Terms and Conditions of ITC Compliance Network

Membership, ITC Compliance have provided this manual, which contains all the relevant

policies needed in order to maintain compliance with current FCA regulations and TCF

outcomes.

ITC Compliance Network Member Policies & Procedures Manual v1.3

2

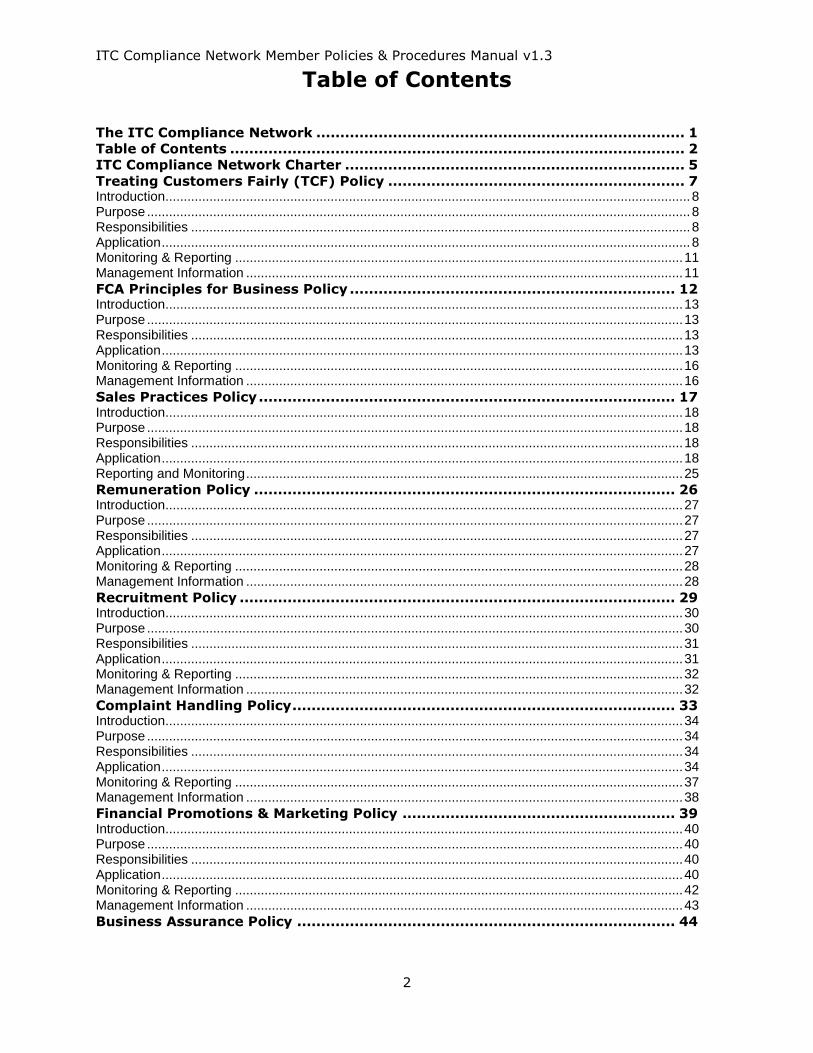

Table of Contents

The ITC Compliance Network ............................................................................. 1 Table of Contents ............................................................................................... 2 ITC Compliance Network Charter ....................................................................... 5 Treating Customers Fairly (TCF) Policy .............................................................. 7 Introduction............................................................................................................................................... 8 Purpose .................................................................................................................................................... 8 Responsibilities ........................................................................................................................................ 8 Application ................................................................................................................................................ 8 Monitoring & Reporting .......................................................................................................................... 11 Management Information ....................................................................................................................... 11 FCA Principles for Business Policy .................................................................... 12 Introduction............................................................................................................................................. 13 Purpose .................................................................................................................................................. 13 Responsibilities ...................................................................................................................................... 13 Application .............................................................................................................................................. 13 Monitoring & Reporting .......................................................................................................................... 16 Management Information ....................................................................................................................... 16 Sales Practices Policy ....................................................................................... 17 Introduction............................................................................................................................................. 18 Purpose .................................................................................................................................................. 18 Responsibilities ...................................................................................................................................... 18 Application .............................................................................................................................................. 18 Reporting and Monitoring ....................................................................................................................... 25 Remuneration Policy ........................................................................................ 26 Introduction............................................................................................................................................. 27 Purpose .................................................................................................................................................. 27 Responsibilities ...................................................................................................................................... 27 Application .............................................................................................................................................. 27 Monitoring & Reporting .......................................................................................................................... 28 Management Information ....................................................................................................................... 28

Recruitment Policy ........................................................................................... 29 Introduction............................................................................................................................................. 30 Purpose .................................................................................................................................................. 30 Responsibilities ...................................................................................................................................... 31 Application .............................................................................................................................................. 31 Monitoring & Reporting .......................................................................................................................... 32 Management Information ....................................................................................................................... 32

Complaint Handling Policy ................................................................................ 33 Introduction............................................................................................................................................. 34 Purpose .................................................................................................................................................. 34 Responsibilities ...................................................................................................................................... 34 Application .............................................................................................................................................. 34 Monitoring & Reporting .......................................................................................................................... 37 Management Information ....................................................................................................................... 38 Financial Promotions & Marketing Policy ......................................................... 39 Introduction............................................................................................................................................. 40 Purpose .................................................................................................................................................. 40 Responsibilities ...................................................................................................................................... 40 Application .............................................................................................................................................. 40 Monitoring & Reporting .......................................................................................................................... 42 Management Information ....................................................................................................................... 43 Business Assurance Policy ............................................................................... 44

ITC Compliance Network Member Policies & Procedures Manual v1.3

3

Introduction............................................................................................................................................. 45 Purpose .................................................................................................................................................. 45 Responsibilities ...................................................................................................................................... 45 Application .............................................................................................................................................. 45 Monitoring & Reporting .......................................................................................................................... 47 Management Information ....................................................................................................................... 48 Training & Competence Policy .......................................................................... 49 Introduction............................................................................................................................................. 50 Purpose .................................................................................................................................................. 50 Responsibilities ...................................................................................................................................... 50 Application .............................................................................................................................................. 50 Monitoring & Reporting .......................................................................................................................... 51 Management Information ....................................................................................................................... 52 Financial Crime Policy ...................................................................................... 53 Introduction............................................................................................................................................. 54 Purpose .................................................................................................................................................. 54 Responsibilities ...................................................................................................................................... 54 Application .............................................................................................................................................. 54 Monitoring & Reporting .......................................................................................................................... 57 Management Information ....................................................................................................................... 57 Conflicts of Interest Policy ............................................................................... 59 Introduction............................................................................................................................................. 60 Purpose .................................................................................................................................................. 60 Responsibilities ...................................................................................................................................... 60 Application .............................................................................................................................................. 60 Monitoring & Reporting .......................................................................................................................... 63 Management Information ....................................................................................................................... 63 Gifts & Hospitality Policy .................................................................................. 64 Introduction............................................................................................................................................. 65 Purpose .................................................................................................................................................. 65 Responsibilities ...................................................................................................................................... 65 Application .............................................................................................................................................. 65 Monitoring & Reporting .......................................................................................................................... 67 Management Information ....................................................................................................................... 67 Risk Management Policy ................................................................................... 68 Introduction............................................................................................................................................. 69 Purpose .................................................................................................................................................. 69 Responsibilities ...................................................................................................................................... 69 Application .............................................................................................................................................. 69 Business Continuity Plan Policy (BCP) .............................................................. 71 Introduction............................................................................................................................................. 72 Purpose .................................................................................................................................................. 72 Application .............................................................................................................................................. 72 Approved Persons Policy .................................................................................. 73 Introduction............................................................................................................................................. 74 Purpose .................................................................................................................................................. 74 Responsibilities ...................................................................................................................................... 74 Application .............................................................................................................................................. 74 Monitoring & Reporting .......................................................................................................................... 77 Management Information ....................................................................................................................... 78 Regulatory Breaches & Incidents Policy ........................................................... 79 Introduction............................................................................................................................................. 80 Purpose .................................................................................................................................................. 80 Responsibilities ...................................................................................................................................... 80 Application .............................................................................................................................................. 80 Monitoring & Reporting .......................................................................................................................... 82 Management Information ....................................................................................................................... 82 Whistleblowing Policy ...................................................................................... 83

ITC Compliance Network Member Policies & Procedures Manual v1.3

4

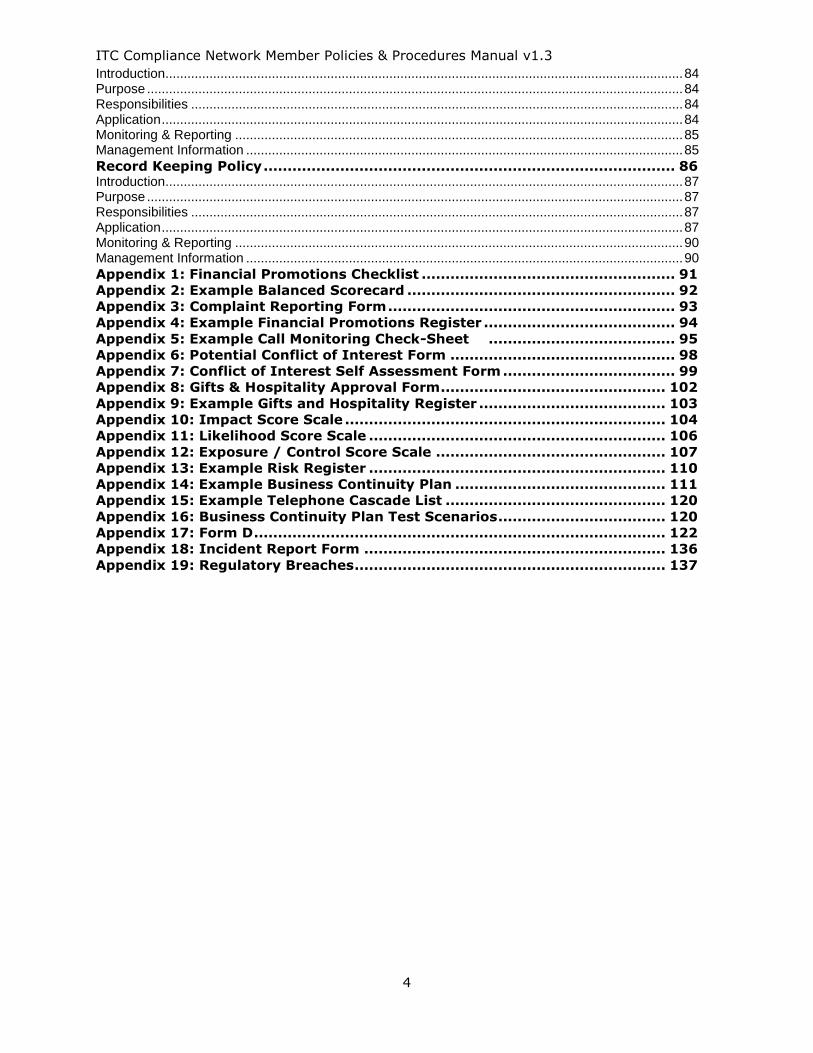

Introduction............................................................................................................................................. 84 Purpose .................................................................................................................................................. 84 Responsibilities ...................................................................................................................................... 84 Application .............................................................................................................................................. 84 Monitoring & Reporting .......................................................................................................................... 85 Management Information ....................................................................................................................... 85 Record Keeping Policy ...................................................................................... 86 Introduction............................................................................................................................................. 87 Purpose .................................................................................................................................................. 87 Responsibilities ...................................................................................................................................... 87 Application .............................................................................................................................................. 87 Monitoring & Reporting .......................................................................................................................... 90 Management Information ....................................................................................................................... 90 Appendix 1: Financial Promotions Checklist ..................................................... 91 Appendix 2: Example Balanced Scorecard ........................................................ 92 Appendix 3: Complaint Reporting Form ............................................................ 93 Appendix 4: Example Financial Promotions Register ........................................ 94 Appendix 5: Example Call Monitoring Check-Sheet ....................................... 95 Appendix 6: Potential Conflict of Interest Form ............................................... 98 Appendix 7: Conflict of Interest Self Assessment Form .................................... 99 Appendix 8: Gifts & Hospitality Approval Form ............................................... 102 Appendix 9: Example Gifts and Hospitality Register ....................................... 103 Appendix 10: Impact Score Scale ................................................................... 104 Appendix 11: Likelihood Score Scale .............................................................. 106 Appendix 12: Exposure / Control Score Scale ................................................ 107 Appendix 13: Example Risk Register .............................................................. 110 Appendix 14: Example Business Continuity Plan ............................................ 111 Appendix 15: Example Telephone Cascade List .............................................. 120 Appendix 16: Business Continuity Plan Test Scenarios ................................... 120 Appendix 17: Form D ...................................................................................... 122 Appendix 18: Incident Report Form ............................................................... 136 Appendix 19: Regulatory Breaches ................................................................. 137

ITC Compliance Network Member Policies & Procedures Manual v1.3

5

ITC Compliance Network Charter In allowing Network Members to operate under ITC Compliance’s authorised regulatory

status, ITC Compliance is obliged to provide you with tools, processes and procedures to

enable you to trade in line with FCA rules, regulations and principles.

The following Charter outlines the main commitments that ITC Compliance and you, the

Network Member, agree to undertake.

Network

ITC Compliance commit to:

1. Supplying Network Members with Appointed Representative (AR), Introducer Appointed

Representative (IAR), or Connected Contract Exemption (CCE) status to allow you to engage in General Insurance activity

2. Providing and updating as necessary the ITC Compliance Network Policies and Procedures Manual

3. Providing an on-line Training and Competence solution for all relevant staff Members

4. Providing and hosting an ITC Compliance portal for regular returns from appropriate Network Members

5. Giving 28 days’ notice of any changes that will affect Network Members (where possible)

6. Undertaking an audit of each site at least once a year

7. Providing a compliant sales process and systems to support this commitment

8. Complaints handling on your behalf

9. Provision of PI insurance (where applicable)

10. Provide Financial Promotions guidance and approval

11. Undertake Call monitoring (where applicable), providing feedback in a timely manner.

12. Undertake Mystery Shopping (where appropriate) to ensure continued compliance of

Network Members.

13. Undertake desk based audits, ensuring Network Members continued compliance with the

FCA Regulations and TCF Outcomes.

14. Undertake Website reviews, providing guidance and approval

15. Providing clear and concise feedback in a timely manner following a review that requires

further action from the Network Member.

16. Undertake Terms of Business Agreement (TOBA) reviews to ensure adequate risk transfer is

in place with regard to Client Money.

ITC Compliance Network Member Policies & Procedures Manual v1.3

6

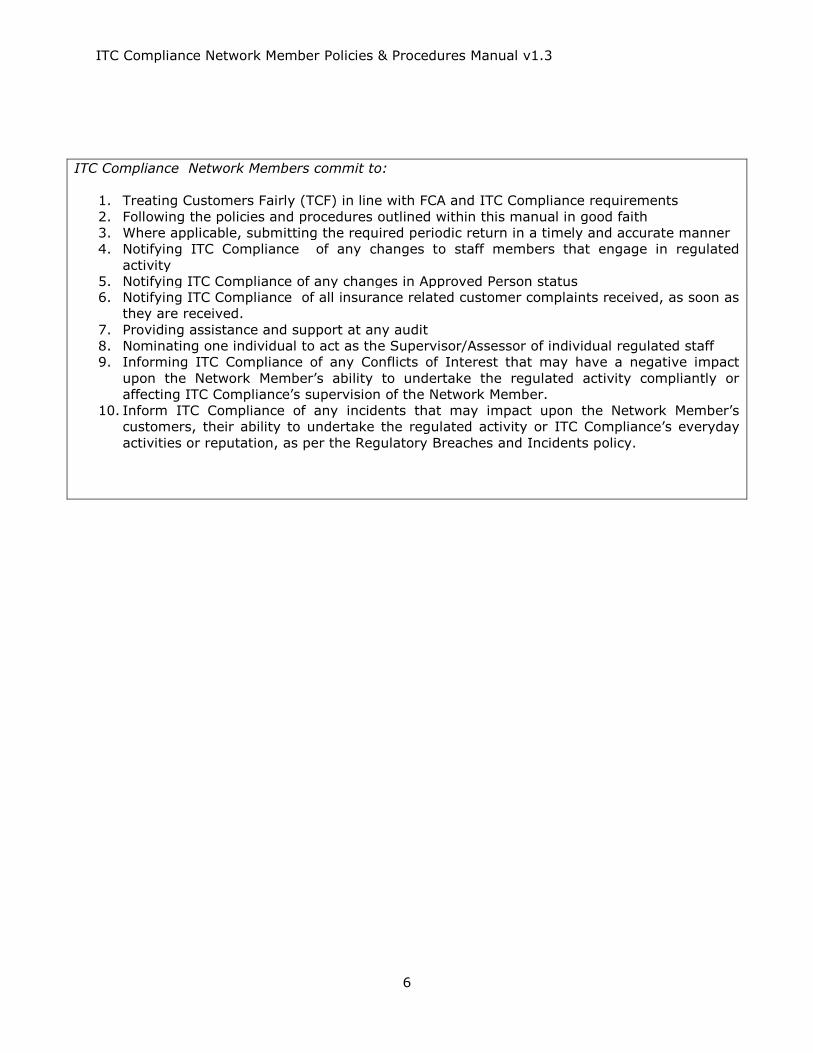

ITC Compliance Network Members commit to:

1. Treating Customers Fairly (TCF) in line with FCA and ITC Compliance requirements

2. Following the policies and procedures outlined within this manual in good faith

3. Where applicable, submitting the required periodic return in a timely and accurate manner

4. Notifying ITC Compliance of any changes to staff members that engage in regulated

activity

5. Notifying ITC Compliance of any changes in Approved Person status 6. Notifying ITC Compliance of all insurance related customer complaints received, as soon as

they are received.

7. Providing assistance and support at any audit

8. Nominating one individual to act as the Supervisor/Assessor of individual regulated staff

9. Informing ITC Compliance of any Conflicts of Interest that may have a negative impact

upon the Network Member’s ability to undertake the regulated activity compliantly or

affecting ITC Compliance’s supervision of the Network Member.

10. Inform ITC Compliance of any incidents that may impact upon the Network Member’s

customers, their ability to undertake the regulated activity or ITC Compliance’s everyday

activities or reputation, as per the Regulatory Breaches and Incidents policy.

ITC Compliance Network Member Policies & Procedures Manual v1.3

7

Treating Customers Fairly (TCF) Policy

ITC Compliance Network Member Policies & Procedures Manual v1.3

8

Introduction Treating Customers Fairly (TCF) is central to the corporate culture of ITC Compliance and

therefore as a Network Member, you should also be able to demonstrate this.

This ethos is underpinned by the FCA requirement to demonstrate the following TCF

outcomes.

1. Consumers can be confident that they are dealing with firms where the fair treatment of

customers is central to the corporate culture.

2. Products and services marketed and sold in the retail market are designed to meet the

needs of identified consumer groups and are targeted accordingly.

3. Consumers are provided with clear information and are kept appropriately informed

before, during and after the point of sale.

4. Where consumers receive advice, the advice is suitable and takes account of their

circumstances.

5. Consumers are provided with products that perform as firms have led them to expect,

and the associated service is of an acceptable standard.

6. Consumers do not face unreasonable post-sale barriers imposed by firms to change

product, switch provider, submit a claim or make a complaint

Purpose

To ensure compliance with these outcomes, ITC Compliance have appropriate procedures

which will encourage your staff to uphold the principle of TCF and the associated outcomes.

This policy sets out guidance to aid understanding of the requirements to comply with the

Treating Customers Fairly outcomes.

Responsibilities

The Approved Person should ensure they are able to evidence a culture of TCF across all

staff and management levels

Application

The requirements for each key area are as follows:

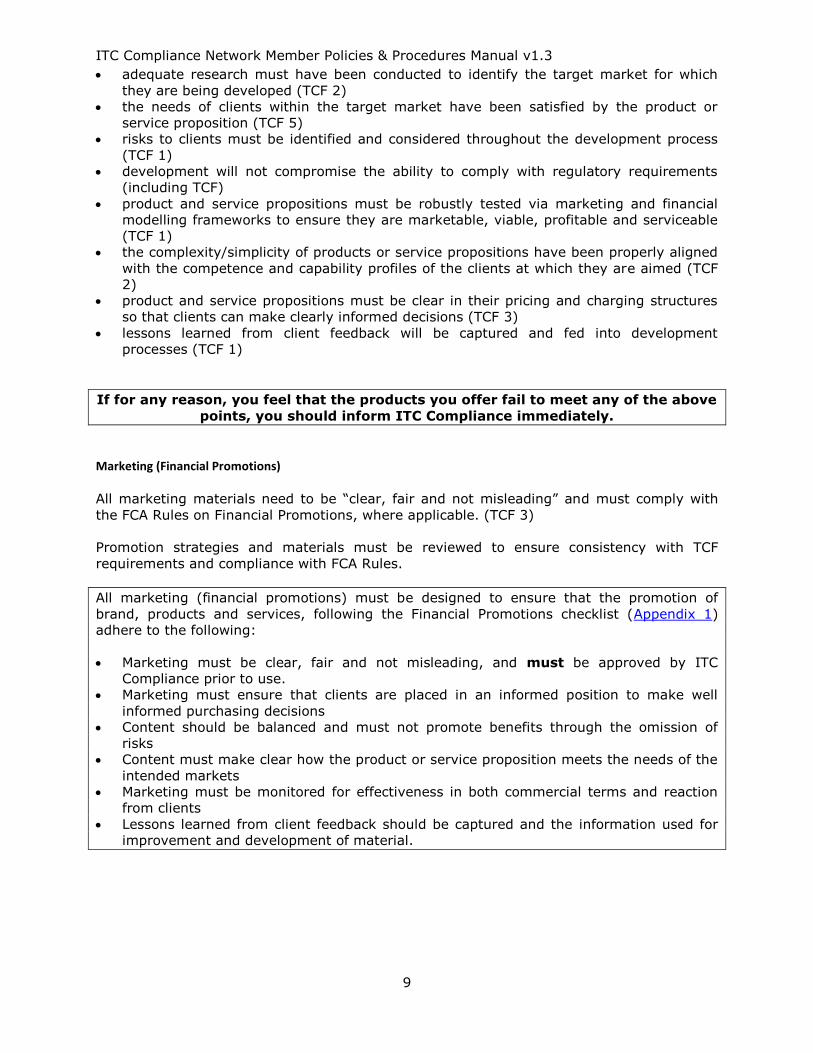

Product Development

As part of the development of new and or enhanced products or service propositions prior to

launch, the product provider will undertake the following:

ITC Compliance Network Member Policies & Procedures Manual v1.3

9

adequate research must have been conducted to identify the target market for which

they are being developed (TCF 2)

the needs of clients within the target market have been satisfied by the product or

service proposition (TCF 5)

risks to clients must be identified and considered throughout the development process

(TCF 1)

development will not compromise the ability to comply with regulatory requirements

(including TCF)

product and service propositions must be robustly tested via marketing and financial

modelling frameworks to ensure they are marketable, viable, profitable and serviceable

(TCF 1)

the complexity/simplicity of products or service propositions have been properly aligned

with the competence and capability profiles of the clients at which they are aimed (TCF

2)

product and service propositions must be clear in their pricing and charging structures

so that clients can make clearly informed decisions (TCF 3)

lessons learned from client feedback will be captured and fed into development

processes (TCF 1)

If for any reason, you feel that the products you offer fail to meet any of the above

points, you should inform ITC Compliance immediately.

Marketing (Financial Promotions)

All marketing materials need to be “clear, fair and not misleading” and must comply with

the FCA Rules on Financial Promotions, where applicable. (TCF 3)

Promotion strategies and materials must be reviewed to ensure consistency with TCF

requirements and compliance with FCA Rules.

All marketing (financial promotions) must be designed to ensure that the promotion of

brand, products and services, following the Financial Promotions checklist (Appendix 1)

adhere to the following:

Marketing must be clear, fair and not misleading, and must be approved by ITC

Compliance prior to use.

Marketing must ensure that clients are placed in an informed position to make well

informed purchasing decisions

Content should be balanced and must not promote benefits through the omission of

risks

Content must make clear how the product or service proposition meets the needs of the

intended markets

Marketing must be monitored for effectiveness in both commercial terms and reaction

from clients

Lessons learned from client feedback should be captured and the information used for

improvement and development of material.

ITC Compliance Network Member Policies & Procedures Manual v1.3

10

Sales and Advice Process

As a Network Member you may conduct transactions through a number of distribution

channels including face to face, the telephone, web-based, directly with clients, on both an

advised and non-advised basis.

An Advised Sale (you give advice) is where you give advice to a potential customer on the

merits of them buying a specific general insurance product, explaining how this meets their

demands and needs and recommending its purchase. This will be specific and individual

advice to the customer and should not be generic. This is in addition to all of the relevant

documentation, including the Status Disclosure Document, Policy Summary and full policy

terms and conditions

A Non-Advised Sale (you don’t give advice) is where you provide information only to a

potential customer leaving them to make a choice about how they wish to proceed and with

no recommendation made.

In this situation it is imperative that the customer is supplied with all of the relevant

documentation, including the Status Disclosure Document, Policy Summary and full policy

terms and conditions to enable the customer to make an informed buying decision.

The following TCF Sales and Advice requirements apply to all:

All sales and advice processes must be reviewed against the Financial Promotions

Checklist (Apendix 1) and authorised by ITC Compliance before they are implemented.

All sales and advice processes must be applied in a consistent and competent manner

that complies with regulatory requirements such as being clear, fair and not misleading,

informing customers of your regulatory status and providing the customer with enough

information for them to make an informed buying decision.

All sales documentation (paper and electronic) must satisfy appropriate creation and

retention standards.

Management information must enable the effective oversight of sales and advice to

clients to ensure compliance with regulatory requirements. For example records of the

number of complaints received, number of customer cancellations, and number of

policies sold etc.

Staff remuneration policies must not conflict with the overarching need to act in the

interests of customers.

Lessons learned from client feedback should be used for improvement and

developments of sales and advice processes.

To ensure compliance with this ITC Compliance provide a number of platforms on which to

conduct sales, and through the online training tool, ITC Compliance ensure that your staff

are able to undertake the specific regulated activity competently.

After Sales Support

This includes documentation of transactions, advice and evidence of cover, midterm

adjustments and cancellations, renewals and access to products, services and information

required by clients.

ITC Compliance Network Member Policies & Procedures Manual v1.3

11

As a Network Member, you should ensure after sales support delivers the required TCF

outcomes, by:

ensuring clients are kept up to date with details of the business relationship with them

ensuring that relationships with clients is underpinned with appropriate communications

and contact to provide clients with access to relevant products, services and information

ensuring that communications and contact with clients are appropriately targeted and

are clear, fair and not misleading

ensuring that clients are provided with the levels of service both promised to the clients

and required by them as their needs dictate

Claims and Complaints Handling

It is extremely important that all complaints about the sale of a regulated insurance product

are directed to ITC Compliance to investigate fully on your behalf. For more information,

please refer to the complaints handling policy further on in this manual.

When dealing with claims, whether acting for the policyholder or the insurer:

Make it clear for who you are acting for with reference to the Conflicts of Interests Policy

Ensure all communications are clear, fair and not misleading

Deliver standards of service consistent with the importance of claims to customers

Ensure that staff are appropriately trained to equip them with the necessary skills to

deal with claims and complaints effectively

Ensure regulatory requirements are observed at all times

Gather appropriate management information to ensure lessons learned from feedback

are fed into this and other processes

Monitoring & Reporting

ITC Compliance and the Network Members are responsible for maintaining compliance with

the FCA Treating Customer Fairly outcomes. To ensure this happens ITC Compliance has

robust procedures in place for the monitoring and the sign off of Financial Promotions, the

monitoring of Network Member’s websites and sales practises.

As well as this, as a Network Member, you should act upon any feedback provided by ITC

Compliance within agreed timescales and sales documentation must be completed clearly

and with the customer’s agreement.

Management Information

ITC Compliance collates Management Information including the number of policies sold and

the number of complaints received. This is periodically reviewed and considered against the

TCF Outcomes.

This Management Information will also form a standard agenda point of periodic board

meetings.

ITC Compliance Network Member Policies & Procedures Manual v1.3

12

FCA Principles for Business Policy

ITC Compliance Network Member Policies & Procedures Manual v1.3

13

Introduction

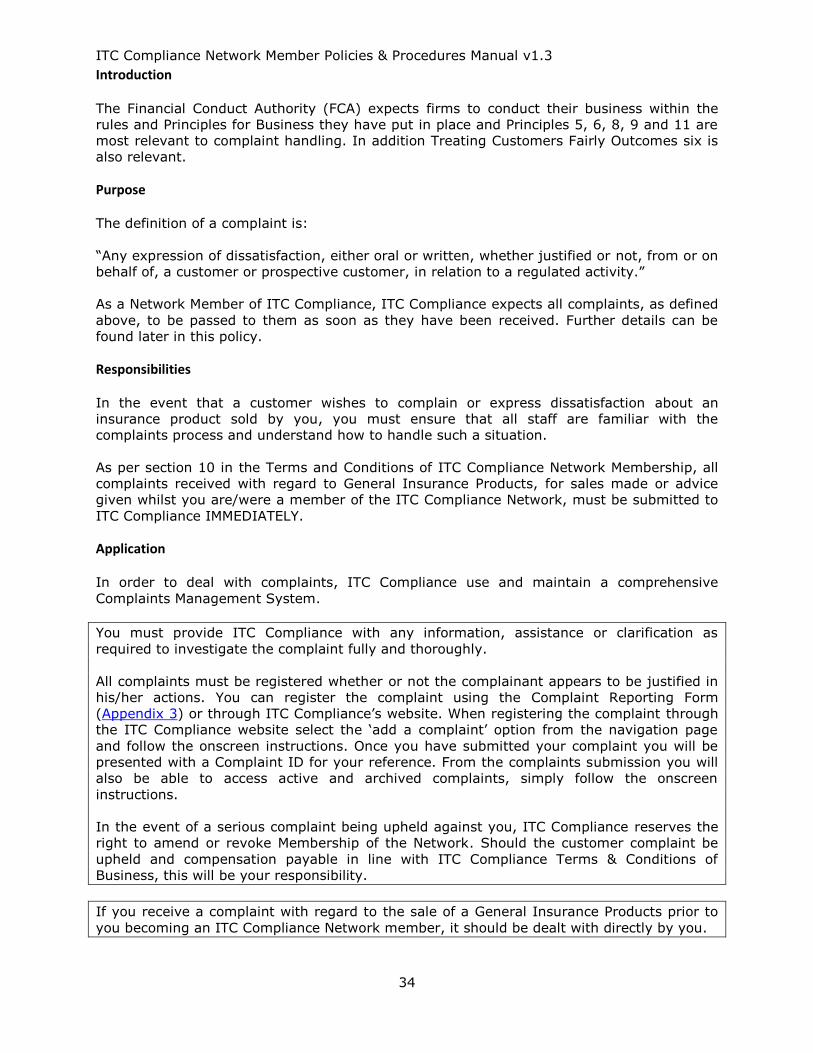

The Financial Conduct Authority (FCA) expects firms to conduct their business within the

rules and Principles for Business they have put in place. There are 11 Principles.

Purpose

These 11 Principles, along with the 6 Treating Customers Fairly (TCF) outcomes, are central

to everything you do.

This policy sets out the FCA 11 Principles for Business and explains how to adhere to them.

Responsibilities

You should understand that ITC Compliance are required by the FCA to commit to these

Principles and recognise the importance as they impose a wider duty, not only to adhere to

the regulatory rules, but also to conduct activities in the spirit of the principles. This includes

ITC Compliance ’s Network Members.

It is the responsibility of ITC Compliance , to ensure that you fully adhere to these Principles

and therefore this forms the basis of the Terms and Conditions of ITC Compliance Network

Membership. These Terms and Conditions can be found by logging onto ITC Compliance’s

website (www.itccompliance.co.uk) and once logged in clicking on the ‘Terms and

Conditions’ link on the footer of your Home page.

Application

The 11 FCA Principles for Business and how ITC Compliance adheres to them are set out

below:

1. Integrity: ‘A Firm must conduct its business with integrity’. ITC Compliance ensures that

ITC Compliance is able to demonstrate the business is based on honesty, trustworthiness

and sound business dealings.

This is demonstrated in the submission of your regular returns, documented sales practices,

such as the provision of an Initial Disclosure Document (IDD), the completion of a Demands

& Needs documents etc. and within clause 8 of the Terms and Conditions of the ITC

Compliance Network Membership.

2. Skill, Care & Diligence: ‘A Firm must conduct its business with due skill, care and

diligence’. ITC Compliance ensures that you are able to show that your business activities

are structured in such a way that care and diligence are exercised on a continual basis.

This is demonstrated through provision of the on-line training tool, ensuring that every

member of staff is competent to perform their role within your firm. ITC Compliance also

ensures that this Principle is met through monitoring Financial Promotions, website reviews

and the reconciliation of your monthly figures.

3. Management & Control: ‘A Firm must take reasonable care to organise and control its

affairs responsibly and effectively, with adequate risk management systems’.

ITC Compliance has developed robust systems to stay in control of its affairs. These include

the on-line training tool and as previously mentioned this enables ITC Compliance to

demonstrate that all staff undertaking a regulated activity are competent to carry out that

ITC Compliance Network Member Policies & Procedures Manual v1.3

14

activity. ITC Compliance has also developed systems to ensure that policies sold are done

so in a compliant manner, providing the customer with all of the relevant documentation

and information.

As well as this ITC Compliance undertake regular audits, desk based and site based,

monthly call monitoring (where applicable), website reviews and reviews of all Financial

Promotions, providing guidance and approval before they are used in circulation.

We collate all of the information received within Monthly ‘MI’ and this is reviewed on a

regular basis by Senior Management.

4. Financial Prudence: ‘A Firm must maintain adequate financial resources’. ITC

Compliance ensures that it is a financially sound and suitably resourced firm to enable the

undertaking of regulated activities.

It is a requirement within ITC Compliance’s Terms and Conditions of ITC Compliance

Network Membership, under clause 4.1.i) that you shall remain solvent as assessed in

accordance with the Regulations and throughout the term of ITC Compliance’s Agreement.

ITC Compliance shall use Credit Referencing firms to ensure that this is adhered to.

5. Market Conduct: ‘A Firm must observe proper standards of market conduct’. ITC

Compliance conducts business affairs in a manner that is regarded as ‘proper conduct’ and

expects you, as a Network Member, to do the same.

Section 4 of the Terms and Conditions of ITC Compliance Network Membership sets out how

ITC Compliance expects you to comply with this Principle. For example, as an Appointed

Representative Network Member, you must have an Approved Person who meets the FCA’s

criteria and you must be able to deliver the same level of protection to the Customer’s as if

they had dealt with ITC Compliance itself. This can be achieved by following the policies

within this manual and making full use of the systems available to you through the Network.

6. Customers’ Interests: ‘A Firm must pay due regard to the interests of its customers

and treat them fairly’. All customers must be placed at the centre of everything ITC

Compliance do.

ITC Compliance meet this Principle by reviewing Financial Promotions, websites and through

call monitoring to ensure that information is presented in a way that is clear, fair and not

misleading. As a Network Member, this Principle is extremely important and you must place

the same importance upon this as ITC Compliance. For example this Principle can be met by

issuing customers with appropriate IDD/SDD documents, undertaking Demands and Needs

assessments (where appropriate) and by following authorised procedures when selling

insurance to a customer.

7. Client Communication: ‘A Firm must pay due regard to the information needs of its

clients, and communicate information to them in a way which is clear, fair and not

misleading’.

This also falls in line with Treating Customers Fairly and is particularly important when using

Financial Promotions and is the main reason ITC Compliance review all promotions before

they are used. This is explained in more detail within the Financial Promotions and

Marketing Policy.

However you should note that this Principle applies to all communication you have with a

customer, including information given/provided before, during and after point of sale.

ITC Compliance Network Member Policies & Procedures Manual v1.3

15

8. Conflicts of Interest: ‘A Firm must manage conflicts of interest fairly, both between

itself and its customers and between a customer and another client’.

All Conflicts of Interest are to be identified and managed in line with the Conflicts of Interest

policy. Examples of a Conflict of Interest would be if a member of staff was placing large

amounts of business to a particular insurer because they previously worked at the insurer

and still had friends there. Or a product provider who offers a loan and cash gift in the

expectation of getting more business in return. Both of these would have to be reported to

ITC Compliance, in line with the Conflicts of Interest Policy immediately.

9. Relationships of Trust: ‘A Firm must take reasonable care to ensure the suitability of

its advice and discretionary decisions for any customer who is entitled to rely upon its

judgement’.

When selling regulated insurance products, there are two routes that, as a Network

Member, you can take. These are Advised and Non-Advised Sales.

An Advised Sale (you give advice) is where you give advice to a potential customer on the

merits of them buying a specific general insurance product, explaining how this meets their

demands and needs and recommending its purchase. This will be specific and individual

advice to the customer and should not be generic.

The suitability of advice and any other recommendations made by you forms a key part of

the insurance regulatory regime. Therefore the Statement of Demands and Needs is

extremely important in regard to endorsing this Principle. You must always ensure that it

is completed diligently on every occasion and used to examine (amongst other things)

customer eligibility, attitude to risk, other existing insurance policies, and any major

exclusions and benefits.

A Non-Advised Sale (you don’t give advice) is where you provide information only to a

potential customer leaving them to make a choice about how they wish to proceed and with

no recommendation made.

10. Clients Assets: ‘A firm must arrange adequate protection for clients’ assets when it is

responsible for them’.

It is a requirement within the Terms and Conditions of ITC Compliance Network

Membership, under clause 30.1 that no Network Members handle Client Money and under

clause 9.5.ii) that all Network Members shall have risk transfer granted by their Product

Provider(s).

This is usually granted within the Terms of Business Agreement (TOBA) between you and

the specific product provider. In essence it means that all premium monies received by you

should be held in a trust account, separate to all other assets you may hold, and receipt of

these monies by yourself is deemed as being received by the insurer. You are therefore

acting as agent of the insurer in the collecting of these premiums.

11. Relations with Regulators: ‘A firm must deal with its regulators in an open and

cooperative way, and must disclose to the FCA appropriately anything relating to the firm of

which the FCA would reasonably expect notice’.

ITC Compliance makes a point of keeping the FCA informed as to business activities in an

accurate and timely manner. In order to do this ITC Compliance, where applicable, obtain

regular returns from you which enable completion of the Retail Mediation Activities Return

ITC Compliance Network Member Policies & Procedures Manual v1.3

16

(RMAR) report.

It is also a requirement under clause 8.3 of the Terms and Conditions of ITC Compliance

Network Membership that all Network Members co-operate fully with the FCA if they gather

information on their own initiative. This will include information on any Notifiable Incidents

that may have occurred. Such Incidents should also be reported to ITC Compliance in line

with the Regulatory Breaches and Incidents Policy.

Monitoring & Reporting

As previously mentioned, there are a number of ways that ITC Compliance expect you to

report this required information and further details are provided in subsequent policies

within this manual.

Management Information

If ITC Compliance’s systems are used, accurate records in regard to all activities affecting

these Principles will be maintained. However ITC Compliance also expects you to keep your

own records, reviewing them periodically to ensure that compliance is maintained.

ITC Compliance Network Member Policies & Procedures Manual v1.3

17

Sales Practices Policy

ITC Compliance Network Member Policies & Procedures Manual v1.3

18

Introduction

The Financial Conduct Authority (FCA) expects firms to conduct their business within the

rules and Principles for Business they have put in place and Principles 1, 2, 3, 6, 7 & 9 are

the most relevant in relation to selling practises. In addition TCF outcomes 1, 2, 3, 4 and 5

also apply.

The Insurance Conduct of Business Sourcebook (ICOBs) within the FCA Handbook outlines

the requirements for the selling of insurance products. Its overall aim is to ensure that

customers are treated fairly by providing them with clear and fair information when they are

sold an insurance product.

Purpose

This document outlines ITC Compliance and Network Member’s regulatory requirements

with regard to undertaking regulated insurance sales (non-advised and advised). It provides

guidance on what should be incorporated into face to face and telephone sales processes in

order to ensure sales are made in a compliant manner and that customer detriment is

avoided.

Responsibilities

ITC Compliance as the Principal will ensure that as a Network Member, you are able to

evidence a culture of good sales practices across all staff and management levels

Application

As per clause 9.2 in the Terms & Conditions of ITC Compliance Network Membership, the

following process should be followed. This process applies to all sales staff on the Network.

It is your responsibility to ensure that the information contained within this policy is

provided to, and understood by, all members of staff for whom ITC Compliance have

regulatory responsibility.

The Sales Process

The sales process described below and the requirements imposed apply to all sales of

insurance products.

There are essentially five broad stages to the sales process (not including the renewal

process):

Step 1 Status Disclosure

Step 2 Eligibility and Disclosure of Material facts

Step 3 Statement of Demands and Needs

Step 4 Product Disclosure

Step 5 Price Disclosure

The specific requirements that need to be followed under each of the headings above are

discussed in more detail below.

The sales process that needs to be followed will vary depending upon whether the firm

operates on an advised or a non-advised basis and applies to all customers. ITC Compliance

operates on both an advised and a non-advised basis, i.e. some firms operate an advised

sales process and others have a non-advised sales process.

ITC Compliance Network Member Policies & Procedures Manual v1.3

19

Advised Sale

An Advised Sale (you give advice) is where you give advice to a potential customer on the

merits of them buying a specific general insurance product, explaining how this meets their

demands and needs and recommending its purchase. This will be specific and individual

advice to the customer and should not be generic.

In this situation it is imperative that the customer is supplied with all of the relevant

documentation, including the Status Disclosure Document, Policy Summary and full policy

terms and conditions to enable the customer to make an informed buying decision

If a firm (Network Member) elects to operate on an advised basis then it must hold the

relevant permissions to do so with ITC Compliance.

It is therefore essential that all staff and agents are aware of what they can and can’t say

when selling insurance products on behalf of the business.

Status Disclosure and Scope of Service

As part of the sales process (both advised and non-advised) all customers must be provided

with the following information:

The name of the firm and the address.

That the firm is an Appointed Representative of ITC Compliance that is authorised and

regulated by the FCA.

The scope of the service to be provided (i.e. that the customer will receive advice).

Whose products the firm will offer, i.e. does the firm only deal with one insurer or will

products/service from a range of insurers be offered?

Whether the customer will have to pay a fee for the services offered.

The process for making a complaint and the availability of the Financial Ombudsman

Service.

That the firm is covered by the Financial Services Compensation Scheme (FSCS).

This information must be provided before the sale is completed. In most cases this

information is provided in an Initial Disclosure Document (IDD). A paper based, bespoke

version of this document can be found under the “Compliance Documents” section of the

ITC Compliance website. The ITC system will also generate a bespoke copy of this document

as you proceed to undertake a sale.

For a face to face sale it is sufficient to provide the customer with a copy of the IDD at the

time of the sale.

For a telephone sale, it is permissible for limited information to be provided over the

telephone, if express consent to receiving only limited information is obtained from the

customer. This is of course on the basis that the full information (i.e. an IDD) is provided to

the customer in written format immediately afterwards (i.e. sent via the post or by email, in

a pdf format, to the customer).

For telephone sales there are two possible scenarios that can be followed, depending on

whether the customer agrees to receive limited information.

If the customer agrees to receive limited information verbally the information that must be

provided is:

ITC Compliance Network Member Policies & Procedures Manual v1.3

20

The name of the sales agent, the firm they represent and the purpose of the call.

Details about the service that can be provided by the firm, i.e. You are an insurance

broker, you will be providing advice.

Whether the customer will have to pay a fee for the services offered.

The possibility of other taxes that may be payable.

Details on the cancellation rights (cancellation rights are only applicable for retail

consumers).

That other information is available on request.

Important: If the customer does not agree to receive limited information, the full

information as set out in the IDD, must be provided verbally to the customer.

Statement of Demands and Needs

If you are following an advised sales process, you must complete a Statement of Demands

and Needs form with the customer. The suitability of advice and any other

recommendations made by you forms a key part of the insurance regulatory regime.

Therefore the Statement of Demands and Needs is extremely important. You must always

ensure that it is completed diligently on every occasion and used to examine (amongst

other things) customer eligibility, attitude to risk, other existing insurance policies, and any

major exclusions and benefits. The form should include the following:

The customer’s specific demands and needs

An assessment of the customer’s affordibility to ensure that purchasing the product will

not cause financial hardship

Confirm that a personal recommendation has been made

Confirm the reasons why that contract is being recommended – i.e. the reasons why the

policy meets the demands and needs of the customer

When operating on an advised basis there are additional requirements that must be fulfilled.

Primarily you must take appropriate steps to ensure the suitability of the insurance product

that you are recommending.

This Statement of Demands and Needs is available through ITC Compliance’s different

systems and therefore does not need to be generated by you. However if for any reason

you feel that the Statement of Demands and Needs does not fit the product being sold, you

must notify ITC Compliance immediately so that any amendments can be made.

The following additional steps should be incorporated into the advised sales process:

Step 1 Establish the

customer’s demands

and needs

Seek relevant information from the customer

concerning their circumstances and objectives

in order to identify their requirements. This

must include any facts that would affect the

type of insurance recommended, such as any

relevant existing insurance policies.

Take into account information known to them,

in respect of other contracts where advice or

information has been provided.

Explain to the customer their duty to not

misrepresent any material facts both before the

contract commences and throughout its

ITC Compliance Network Member Policies & Procedures Manual v1.3

21

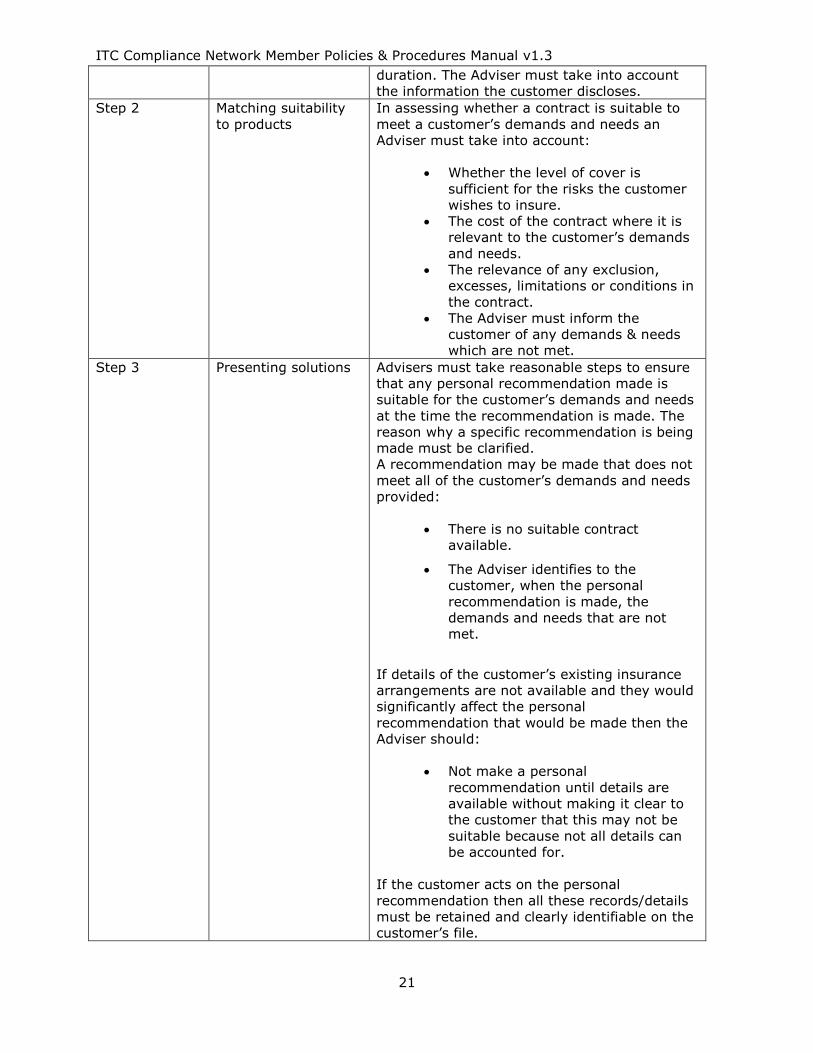

duration. The Adviser must take into account

the information the customer discloses.

Step 2 Matching suitability

to products

In assessing whether a contract is suitable to

meet a customer’s demands and needs an

Adviser must take into account:

Whether the level of cover is

sufficient for the risks the customer

wishes to insure.

The cost of the contract where it is

relevant to the customer’s demands

and needs.

The relevance of any exclusion,

excesses, limitations or conditions in

the contract.

The Adviser must inform the

customer of any demands & needs

which are not met.

Step 3 Presenting solutions Advisers must take reasonable steps to ensure

that any personal recommendation made is

suitable for the customer’s demands and needs

at the time the recommendation is made. The

reason why a specific recommendation is being

made must be clarified.

A recommendation may be made that does not

meet all of the customer’s demands and needs

provided:

There is no suitable contract

available.

The Adviser identifies to the

customer, when the personal

recommendation is made, the

demands and needs that are not

met.

If details of the customer’s existing insurance

arrangements are not available and they would

significantly affect the personal

recommendation that would be made then the

Adviser should:

Not make a personal

recommendation until details are

available without making it clear to

the customer that this may not be

suitable because not all details can

be accounted for.

If the customer acts on the personal

recommendation then all these records/details

must be retained and clearly identifiable on the

customer’s file.

ITC Compliance Network Member Policies & Procedures Manual v1.3

22

Non Advised Sales

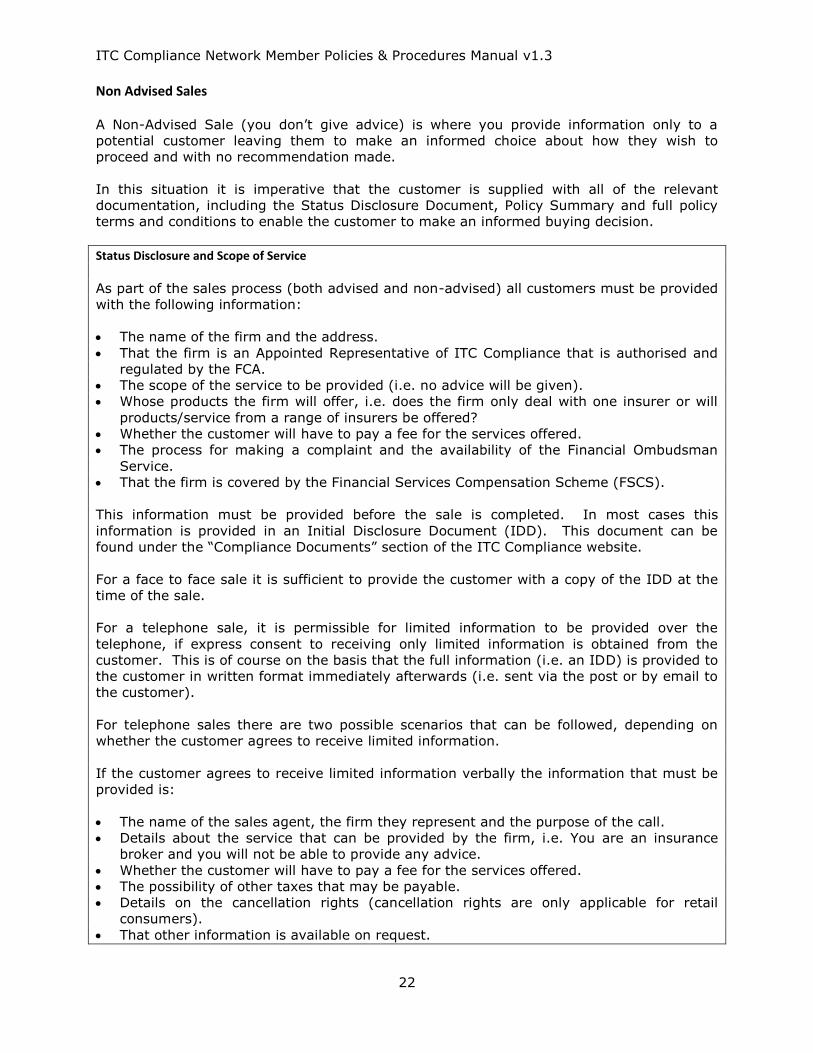

A Non-Advised Sale (you don’t give advice) is where you provide information only to a

potential customer leaving them to make an informed choice about how they wish to

proceed and with no recommendation made.

In this situation it is imperative that the customer is supplied with all of the relevant

documentation, including the Status Disclosure Document, Policy Summary and full policy

terms and conditions to enable the customer to make an informed buying decision.

Status Disclosure and Scope of Service

As part of the sales process (both advised and non-advised) all customers must be provided

with the following information:

The name of the firm and the address.

That the firm is an Appointed Representative of ITC Compliance that is authorised and

regulated by the FCA.

The scope of the service to be provided (i.e. no advice will be given).

Whose products the firm will offer, i.e. does the firm only deal with one insurer or will

products/service from a range of insurers be offered?

Whether the customer will have to pay a fee for the services offered.

The process for making a complaint and the availability of the Financial Ombudsman

Service.

That the firm is covered by the Financial Services Compensation Scheme (FSCS).

This information must be provided before the sale is completed. In most cases this

information is provided in an Initial Disclosure Document (IDD). This document can be

found under the “Compliance Documents” section of the ITC Compliance website.

For a face to face sale it is sufficient to provide the customer with a copy of the IDD at the

time of the sale.

For a telephone sale, it is permissible for limited information to be provided over the

telephone, if express consent to receiving only limited information is obtained from the

customer. This is of course on the basis that the full information (i.e. an IDD) is provided to

the customer in written format immediately afterwards (i.e. sent via the post or by email to

the customer).

For telephone sales there are two possible scenarios that can be followed, depending on

whether the customer agrees to receive limited information.

If the customer agrees to receive limited information verbally the information that must be

provided is:

The name of the sales agent, the firm they represent and the purpose of the call.

Details about the service that can be provided by the firm, i.e. You are an insurance

broker and you will not be able to provide any advice.

Whether the customer will have to pay a fee for the services offered.

The possibility of other taxes that may be payable.

Details on the cancellation rights (cancellation rights are only applicable for retail

consumers).

That other information is available on request.

ITC Compliance Network Member Policies & Procedures Manual v1.3

23

Important: If the customer does not agree to receive limited information, the full

information as set out in the IDD, must be provided verbally to the customer.

Statement of Demands and Needs

When following a non-advised sales process, the format of the Statement of Demands and

Needs is different as it is simply a statement informing the customer, which of their

demands and needs have been met by the policy. For example; “This product meets the

demands and needs of those wishing to insure the contents of their home.”

A Demands and Needs statement must be provided in writing to the customer before they

buy the policy. If the customer is sold the insurance policy over the telephone this

information can be provided verbally but must be sent to the customer in writing

immediately afterwards.

This Statement of Demands and Needs is available through ITC Compliance’s different

systems and therefore does not need to be generated by you. However if for any reason

you feel that the Statement of Demands and Needs does not fit the product being sold, you

must notify ITC Compliance immediately so that amendments can be made.

Eligibility and Misrepresentation

Eligibility

As a Network Member, it is your responsibility to ensure that their sales process confirms a

customer’s eligibility to claim under the policy. If there are any known exclusions, checks

should be undertaken to see whether these would mean that the customer would be unable

to claim on a policy should the need arise. For example, if the policy would not cover a car

for racing purposes should the policy be sold to the driver looking to take his car racing at

the weekends?

If during the sales process it is identified that only parts of the insurance cover apply to the

customer, then steps must be taken to ensure that the customer is made aware of this.

The golden rule is that the customer must be provided with sufficient information about

what the insurance policy will and will not do, to be able to make an informed decision

about whether that policy is right for them.

Misrepresentation

The insurer will use the information provided by the customer to assess the risks of

providing the cover and to determine whether or not to accept that risk and what the

premium will be. Since the CIA (Consumer Insurance Act) came into effect in April 2013

customers are under a duty not to misrepresent. It is therefore imperative that the

customer is asked specific questions for underwriting purposes and you should not rely

solely on the customer’s disclosures. If key information is omitted during the sales process

but comes to light during the claims process, the insurer could be entitled to reject the

claim. However Insurers cannot decline claims if they have not asked the correct and

relevant question.

ITC Compliance Network Member Policies & Procedures Manual v1.3

24

Important: At any time during the contractual relationship the consumer is entitled, at their request, to receive the contractual terms and conditions on paper. The consumer is also entitled to change the means of distance

communication used unless this is incompatible with the contract concluded or the nature of the service provided.

Product Disclosure

As part of the sales process (both advised and non-advised) customers must be provided

with sufficient and appropriate information about the product to allow them to make an

informed decision. The information should be modified to reflect the type of customer

purchasing the policy.

The information can be provided in a Policy Summary, which must be provided in writing

and must be provided to the customer at the time of the sale (for a face to face sale) or

immediately afterwards (for a telephone sale).

It is not mandatory to provide a policy summary for all products however where this is

provided, the responsibility for creating a policy summary rests with the insurer, whilst the

responsibility for providing the policy summary to the customer rests with you.

Price Disclosure

Before the customer makes the decision to purchase the policy they must be provided with

details of the full price to be paid for the insurance product to ensure that purchasing the

policy will not cause any financial hardship to the customer. This will need to be broken

down to include:

The cost of the insurance policy, including IPT

The cost of any optional extras (i.e. legal expenses), including IPT

The total cost payable (i.e. the insurance premium plus the cost of optional extras)

Providing Evidence of Cover

Following the conclusion of the sale the customer should be provided with:

Confirmation of the insurance, including a breakdown of the total premium paid

Evidence of the cover provided

Full policy wording containing all the terms and conditions

Details on how to cancel the policy (NB cancellation rights are only applicable for retail

consumers)

Details on how to make a claim

Details on how to complain and the right to refer complaints to the Financial

Ombudsman Service (FOS)

Details of the Financail Services Compensation Scheme (FSCS)

Cancellations

Retail consumers are provided with cancellation rights. Effectively this means that they

have 14-days (30 days for protection policies) in which to change their mind about the

purchase of their insurance policy. If a retail consumer wants to cancel their insurance

policy they do not have to provide any reason for the cancellation.

The cancellation period begins from the day the policy is sold; or if later, from the day that

the retail consumer receives the policy terms and conditions.

ITC Compliance Network Member Policies & Procedures Manual v1.3

25

Where a retail consumer chooses to cancel their policy within the cancellation period they

are entitled to a full refund of the premium paid. The only exceptions to this are where a

claim has already been made and paid under the policy, or if a cancellation/administration

fee is payable.

Renewals

This section is only applicable if you carry out policy renewals on behalf of an Insurer.

The customer must be provided with full renewal terms, including a breakdown of the cover

and price. The renewal terms must include the following information:

Details of the insurance cover provided, including any optional extras selected (NB it

must be clear to the customer what level of cover is provided and which extras selected

are optional).

A full breakdown of the renewal premium (see Section 3.7 Price Disclosure)

Details of the renewal date and whether the policy will renew automatically or if the

customer needs to take some action

Evidence of the cover provided.

A statement of any changes to the terms of the policy and an explanation of those

changes.

A statement advising the customer who they should contact if their circumstances have

changed and they need to make amendments to their policy.

The materials facts disclosure (see Section 3.4)

As a general rule, customers should be provided with renewal documentation at least 21

days before the renewal date. This is to ensure that all customers have sufficient time to

review the documents, make any amendments if necessary or seek alternative providers.

Reporting and Monitoring

ITC Compliance’s bespoke system allows for the monitoring and reporting of both advised

and non-advised sales.

Where appropriate it is your responsibility to report your sales figures to ITC Compliance

through your periodic returns.

All scripted sales processes are approved by ITC Compliance prior to use; any new script

request should follow the Financial Promotions Policy procedure.

ITC Compliance Network Member Policies & Procedures Manual v1.3

26

Remuneration Policy

ITC Compliance Network Member Policies & Procedures Manual v1.3

27

Introduction

The Financial Conduct Authority (FCA) expects firms to conduct their business within the

rules and Principles for Business they have put in place and Principle 3 is the most relevant

to remuneration. In addition Treating Customers Fairly outcome 1 also applies.

In addition the following rule from the Systems and Controls Rulebook: SYSC 3.1.1R A firm

must take care to establish and maintain such systems and controls as are appropriate to its

business.

Purpose

ITC Compliance is required to manage Network Member’s staff remuneration, including

incentives in such a way that any potential risk of miss-selling is reduced.

As per clause 5.3 within the Terms and Conditions of ITC Compliance Network Membership,

you may not accept any secret profit, income or inducement from any Product Provider,

which provides an incentive to promote or recommend any one product in preference to

other products.

The FCA has published guidance in this area including good and bad practice.

This policy refers to that guidance to aid understanding of the requirements when

considering how staff and management working in an FCA regulated environment should be

remunerated. It also details the risk mitigation actions that both ITC Compliance and you

should take.

Responsibilities ITC Compliance has documented and implemented robust procedures for the effective management of remuneration schemes.

Application

It is acceptable to incentivise staff to sell, but this must never be at the customer’s expense

and the risks will be managed appropriately.

The FCA has highlighted a series of failings, which are detailed below. Management must

consider these when any incentive or remuneration scheme is created or reviewed:

Firms failing to identify how incentive schemes might encourage staff to miss-sell,

suggesting they had not sufficiently thought about the risks.

Firms failing to understand their own incentive schemes because they are so complex,

therefore making it harder to control them.

Firms not having enough information about their incentive schemes to understand and

manage the risks.

Firms relying too much on routine monitoring, rather than taking account of the specific

features of their incentive schemes.

Sales managers with clear conflicts of interest that are not properly managed.

Firms having links to sales quality built into their incentive schemes that were

ineffective.

Firms not doing enough to control the risk of miss selling in face-to-face situations.

ITC Compliance Network Member Policies & Procedures Manual v1.3

28

Your remuneration scheme must be documented and available upon request at audits

undertaken by ITC Compliance.

ITC Compliance use the term ‘mis-selling’ in this document to refer to a failure to deliver the

following fair outcomes for consumers:

customers are treated fairly (TCF 1)

customers understand the key features of the product and whether they are being given

advice or information (TCF 3, 4)

customers are given information that is clear, fair and not misleading (TCF 3)

information that enables them to make an informed decision before purchasing a

product or service (TCF 3)

customers buying on an advised basis are recommended suitable products. (TC4)

As part of your remuneration policy, management must consider the following:

if the incentive schemes increase the risk of mis-selling

review whether the governance and controls are adequate

take action to address any inadequacies – this might involve changing the scheme

where risks cannot be mitigated, take action to change the scheme

consider the impact of performance management for scheme members

A good Incentive Scheme should include the following:

a quality (compliant) element

consideration of client cancellations

a capped (or decreasing) incentive i.e. reducing or capping bonus’ when a sales volume

is approached. This avoids the temptation to rush sales through

deferred bonus payment (maybe subject to quality over a longer period e.g. half year,

yearly)

balanced scorecard, incorporating 4 measures that the sales staff will be assessed

against. One of these measures must be from a customer’s perspective (TCF). An

example of this is shown in Appendix 2.

No scheme must contain significant remuneration boosts for achieving sales targets alone at

given points in time. These are known as ‘cliff edges’ or ‘precipices’.

Monitoring & Reporting

You must maintain records of all incentive schemes for all employees

Management Information

You should ensure all staff have documented Key Performance Indicators (KPI’s) which may

be periodically reviewed to ensure there are no incentives to mis-sell as per the FCA

guidance.

ITC Compliance Network Member Policies & Procedures Manual v1.3

29

Recruitment Policy

ITC Compliance Network Member Policies & Procedures Manual v1.3

30

Introduction

The Financial Conduct Authority (FCA) expects businesses to conduct their business within

the rules and Principles for Business they have put in place. There are 11 Principles in total;

however Principles 1 and 3 are most relevant to recruitment:

1. Integrity: A Firm must conduct its business with integrity.

3. Management & Control: A Firm must take reasonable care to organise and control its

affairs responsibly and effectively, with adequate risk management systems.

In addition the following rule applies from the Systems and Controls Rulebook: SYSC 3.1.1R

A firm must take care to establish and maintain such systems and controls as are

appropriate to its business.

In addition, Treating Customers Fairly customer outcome 1 is;

1. Customers can be confident that they are dealing with a firm where the fair

treatment of consumers in central to the corporate culture.

If the recruitment is for an Approved Person then there is an additional requirement that

ITC Compliance satisfies the FCA that a candidate is fit and proper to perform the controlled

function applied for.

Purpose

ITC Compliance perform adequate due diligence when recruiting new staff into a regulated

environment

Recruiting an inappropriate individual could lead to customer detriment and/or negative

action against ITC Compliance which could lead to regulatory fines or penalties.

This policy sets out guidance to aid understanding of the requirements when recruiting in an

FCA regulated environment. It is not intended to cover all Human Resource or Equal

Opportunities obligations.

Responsibilities

ITC Compliance has documented and implemented robust procedures for the effective

recruitment of new staff.

ITC Compliance Network Member Policies & Procedures Manual v1.3

31

Application

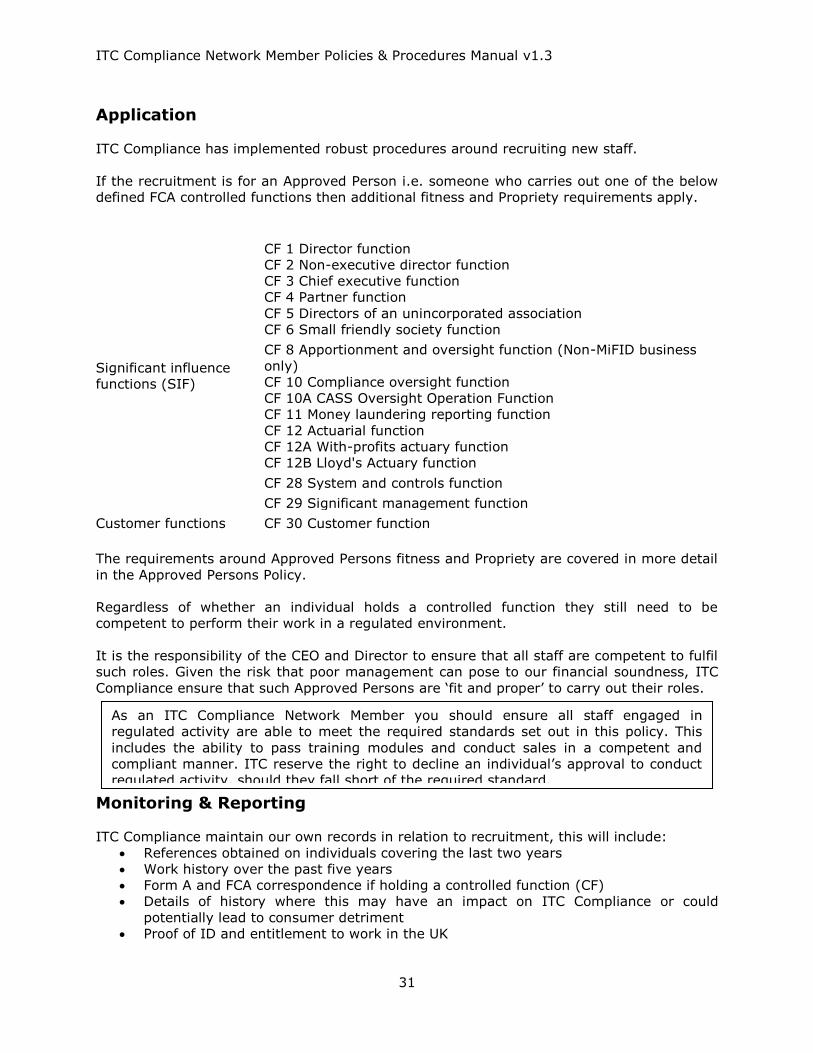

ITC Compliance has implemented robust procedures around recruiting new staff.

If the recruitment is for an Approved Person i.e. someone who carries out one of the below

defined FCA controlled functions then additional fitness and Propriety requirements apply.

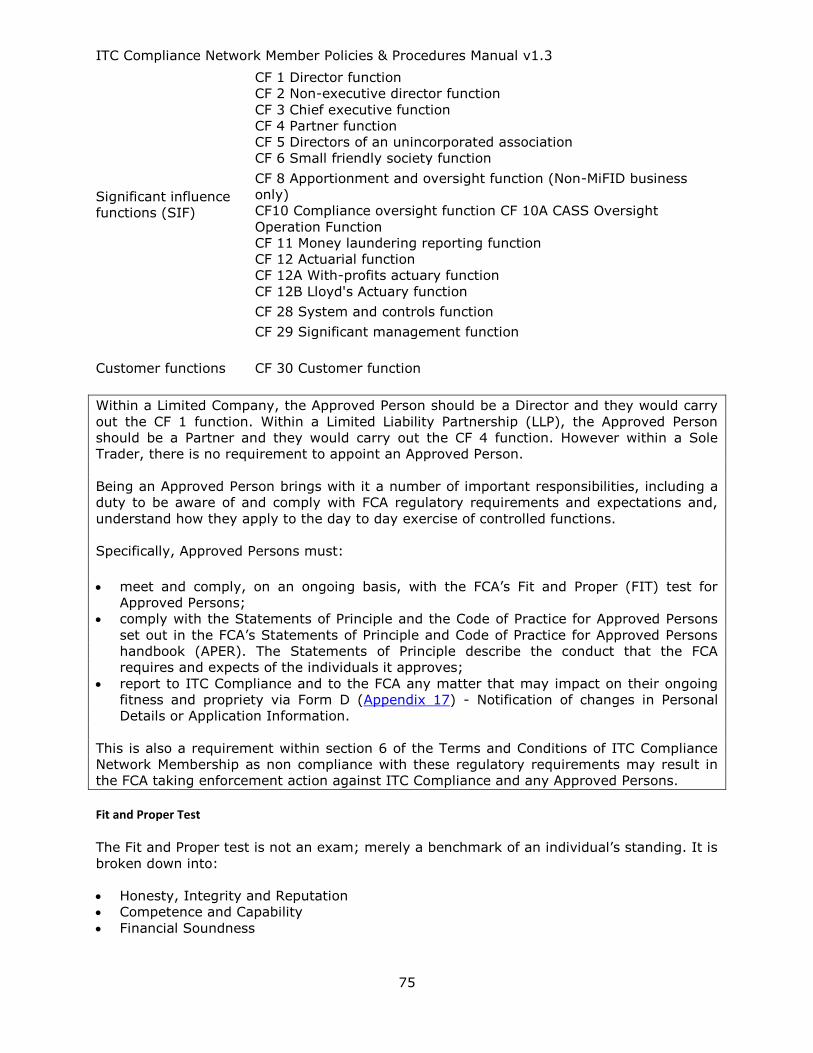

Significant influence

functions (SIF)

CF 1 Director function

CF 2 Non-executive director function

CF 3 Chief executive function

CF 4 Partner function

CF 5 Directors of an unincorporated association

CF 6 Small friendly society function

CF 8 Apportionment and oversight function (Non-MiFID business

only)

CF 10 Compliance oversight function

CF 10A CASS Oversight Operation Function

CF 11 Money laundering reporting function

CF 12 Actuarial function

CF 12A With-profits actuary function

CF 12B Lloyd's Actuary function

CF 28 System and controls function

CF 29 Significant management function

Customer functions CF 30 Customer function

The requirements around Approved Persons fitness and Propriety are covered in more detail

in the Approved Persons Policy.

Regardless of whether an individual holds a controlled function they still need to be

competent to perform their work in a regulated environment.

It is the responsibility of the CEO and Director to ensure that all staff are competent to fulfil

such roles. Given the risk that poor management can pose to our financial soundness, ITC

Compliance ensure that such Approved Persons are ‘fit and proper’ to carry out their roles.

Monitoring & Reporting

ITC Compliance maintain our own records in relation to recruitment, this will include:

References obtained on individuals covering the last two years

Work history over the past five years

Form A and FCA correspondence if holding a controlled function (CF)

Details of history where this may have an impact on ITC Compliance or could

potentially lead to consumer detriment

Proof of ID and entitlement to work in the UK

As an ITC Compliance Network Member you should ensure all staff engaged in

regulated activity are able to meet the required standards set out in this policy. This

includes the ability to pass training modules and conduct sales in a competent and

compliant manner. ITC reserve the right to decline an individual’s approval to conduct

regulated activity, should they fall short of the required standard.

ITC Compliance Network Member Policies & Procedures Manual v1.3

32