the interactions between debt and currency crises ... · the interactions between debt and currency...

TRANSCRIPT

Universität Bayreuth

Rechts- und Wirtschaftswissenschaftliche Fakultät

Wirtschaftswissenschaftliche Diskussionspapiere

ISSN 1611-3837

Adresse: Adresse: Bernhard Herz Hui Tong Lehrstuhl für Wirtschaftspolitik Economics Department Universität Bayreuth University of California at Berkeley 95440 Bayreuth Berkeley, CA 94720-3880 Telefon: +49-921-552914 +001-510-6845159 Fax: +49-921-552949 +001-510-6426615 e-Mail: [email protected] [email protected]

Bernhard Herz

Hui Tong Diskussionspapier 17

Dezember 2004

The Interactions between Debt and Currency

Crises – Common Causes or Contagion?

Abstract

The Interactions between Debt and Currency Crises –

Common Causes or Contagion? In contrast to the well-known twin currency and banking crises the literature has so far

neglected a second type of twin crises, the simultaneous occurrence of currency and debt

crises. The decision of a government to devalue and/or to default is closely interlinked

through the government’s intertemporal budget constraint. In our empirical analysis we find

some evidence that one-year lagged debt crisis strongly Granger causes currency crisis and

two-year lagged currency crisis weakly Granger causes debt crisis. We find strong evidence

that debt and currency crises have common fundamental causes. Low reserve over imports

ratio, low domestic GDP growth rate, and low FDI over external debt ratio all increase the

likelihood of debt and currency crises.

JEL classification: F31, F33, F34, F41

Keywords: Currency crisis, debt crisis, panel data, developing countries

- 2 -

1. Introduction

The episodes of financial turmoil and distress in the 1990s led researchers to not only look at currency

crises as isolated events but also to take into consideration problems in the banking sector. Many of the

countries that have experienced currency crises also have undergone domestic banking crises around

the same time. Following Kaminsky and Reinhart (1999) this twin crisis approach has induced an

extensive theoretical and empirical research on the links between banking and currency crises. In

contrast, the literature has so far neglected a second type of twin crisis, the simultaneous occurrence of

currency and debt crises. Many countries which have faced balance of payments problems have been

confronted with severe debt problems at the same time, with recent examples including Argentina,

Ecuador and Russia.

As the literature has typically treated currency and debt crises as isolated events, it has not analyzed the

decision to default and/or to devalue as part of a wider menu of policy choices. What kind of

interrelations could exist between defaults and devaluations? First, the simultaneous occurrence of debt

and currency crises could be caused by common macroeconomic factors that at the same time

undermine a government’s resolve to pay back its debt and to defend its exchange rate peg. Secondly,

these events could be caused by some causal chains running from debt to currency crisis or the other

way around. In this case defaults and devaluations could be either substitutes or complements.

Devaluations and (partial) defaults are substitutes if the emphasis is on the aspect of financing a given

volume of public expenditures. If a government is constrained in its fiscal policy and cannot provide a

large enough primary surplus to service its debt coming due, e.g. because of institutional problems or

political pressure, it is left with the following alternatives to “finance” its expenditures (table 1):

• a (partial) default on its debt, i.e. an implicit tax on bond holders (debt crisis),

- 3 -

• an increase in the money stock, i.e. an inflation tax on money holdings implying a devaluation

of the currency (currency crisis), or

• a combination of a devaluation and a default (twin crisis)

According to this view the occurrence of a currency crisis should reduce the financing requirements of

the government, thereby making a debt crisis less likely. Correspondingly, a debt crisis should lower

the likelihood of a currency crisis.

Table 1: Debt, currency and twin crisis

No default Default

No devaluation no crisis Debt crisis

Devaluation Currency crisis Twin crisis

In contrast, currency and debt crises are complements if self-fulfilling expectations and contagion from

one type of crisis to the other are relevant. Let us assume, that speculators expect a devaluation and

demand higher interest rates which increase the financing requirements of the government. Then the

government may not only try to reduce its real debt via inflation but also by defaulting on its debt

coming due. Rational speculators take that possibility of a default into account and demand a higher

risk premium, thereby further increasing the public financing requirement and making both a debt and a

currency crisis more likely.

These interactions between debt and currency crises have so far been neglected in the theoretical and

empirical research with the exception of the policy literature (e.g. Chiodo and Owyang 2002, Mussa

2002). In the field of currency crises the first-generation models emphasize the role of (monetary)

fundamentals in a speculative attack (e.g. Krugman 1979 and Flood and Garber 1984). The second-

- 4 -

generation models of the currency crisis, e.g. Obstfeld (1994) and (1996), analyze how market

expectations and fundamentals interact to give rise to multiple equilibria. For example if speculators

believe that the government has less resolve to defend the exchange rate peg they demand higher

interest rates to compensate for the risk of a devaluation. The increased debt service may lead the

government to reduce its fiscal burden through inflation and subsequent devaluation, thereby validating

the speculators’ expectations. While currency crises have primarily been characterized as monetary

phenomena, fiscal factors can play a major role in theses crises because of the interconnections

between monetary and fiscal policy (see e.g. Giavazzi and Pagano 1990, Obstfeld 1994, and Benigno

and Missale 2001).

The extensive empirical work on currency crises, e.g. Eichengreen et al. (1995), Frankel and Rose

(1996), and Bordo et al. (2001), typically finds a higher likelihood of currency crises when the reserves

are low, the foreign direct investment dries up, the monetary growth is high, the world capital markets

are tight, and the domestic currency is overvalued. Institutional factors such as the degree of capital

controls also help to predict currency crashes (Kaminsky and Reinhart 1999).

The theoretical literature on debt crises is vast also, while there are fewer empirical studies. Major

factors in explaining debt crises are liquidity and expected deficits. If the creditors do not roll over all

of the maturing debt, a default is the optimal choice for the debtor. If creditors are small and cannot co-

ordinate there may be an equilibrium in which creditors do not roll over and the debtor defaults (Sachs

1984, Detragiache and Spilimbergo 2002). Calvo (1988) and Alesina et al. (1990) developed the idea

that a government partly repudiates its domestic currency debt through a surprise inflation in which

high expected inflation rates are self-fulfilling. More recently, Cole and Kehoe (1996, 2000) and

Detragiache (1996) analyzed self-fulfilling creditor runs in models of sovereign debt. Chang and

Velasco (1998, 2000) model foreign creditor runs when the borrowers are banks instead of the

- 5 -

government. A common feature of these models of self-fulfilling creditor runs is that the bad

equilibrium disappears if the amount of debt to be rolled over is small or the fundamentals are benign.

The empirical evidence on the role of debt maturity in debt crisis is mixed. Radelet and Sachs (1998)

and Rodrik and Velasco (1999) find evidence that the ratio of short-term debt to reserves helps to

predict reversals of capital flows. According to Eichengreen and Mody (1998, 1999) risk spreads on

emerging market debt instruments increase with the ratio of short-term debt to reserves. Finally,

Detragiache and Spilimbergo (2002) report that liquidity variables such as the share of short-term debt,

debt coming due, and foreign reserves are correlated with defaults concerning commercial creditors.

Among the conventional macroeconomic variables they only find the degree of overvaluation to predict

defaults.

Recently, a few theoretical papers have explicitly integrated aspects of debt and currency crises in the

framework of an intertemporal budget constraint, e.g. Calvo (1998), Aizenman et al. (2002), Benigno

and Missale (2001), Bauer et al. (2003), and Jahjah and Montiel (2003). On the empirical side,

Goldstein et al. (1998), Reinhart (2002), and Sy (2003) provide first steps to an empirical analysis of

twin debt and currency crises. Goldstein et al. (1998) report evidence that currency crises are closely

associated with the probability of sovereign defaults. Reinhart (2002) finds that sovereign credit ratings

usually are downgraded after currency crisis and that these downgradings help to predict defaults. She

takes that as an indication, that currency crises increase default risk. However, Reinhart (2002) does not

directly control for the possibility, that currency and debt crises might be caused by common factors. In

contrast, Sy (2002) concludes for a smaller and more recent sample of 13 emerging market economies

during the period 1994 – 2002 that currency crises are not linked to the probability of sovereign default.

Taken together, the nature of twin currency and debt crises is still an open question.

- 6 -

We analyze the interrelations between debt and currency crises in an Obstfeld (1994) type framework.

The welfare maximizing government decides on its monetary and fiscal policy by balancing the costs

of alternative means of financing its expenditures, in particular the costs of an inflation/devaluation and

the costs of a default. The government cannot commit itself to honor its debt and its exchange rate peg.

On the one side the government has an incentive to finance its expenditures by printing money

implying subsequently inflation and devaluation in order to avoid the costs of a default. These costs

include the loss of reputation on the international capital markets and the loss of GDP during the

economic turmoil typically following a debt crisis. One the other hand it has an incentive to default on

its debt in order to avoid the welfare costs of inflation and devaluation. As is typical for escape clause

models, this can give rise to multiple equilibria with self-fulfilling twin debt and currency crises. There

also exists the possibility of internal contagion from one policy field to another policy area within the

same country. The expectation of a debt crisis can increases the debt service due to the higher interest

rates thereby inducing a government to inflate and making a currency crisis more likely.

Our empirical analysis is based on a sample of 74 developing countries from 1975 to 2001. We find

strong evidence that debt and currency crises have common fundamental causes. We find that reserve

over imports ratio, domestic GDP growth rate, and FDI over external debt ratio affect both currency

and debt crises. We also find that one-year lagged debt crisis strongly Granger causes currency crisis

and two-year lagged currency crisis weakly Granger causes debt crisis.

The paper is organized as follows. Section 2 analyzes the interrelations between debt and currency

crises in an escape clause framework. Section 3 presents the data used in our empirical analysis and

provides some summary statistics. Section 4 discusses the statistical model and the main empirical

results. Section 5 concludes.

- 7 -

2. A simple model of debt cum currency crises

The following model builds on the very insightful contribution of Obstfeld (1994) to analyze a model

of self-fulfilling debt and currency crises. In Obstfeld (1994) the alternative instruments of government

financing are printing money and levying taxes. In the context of debt and currency crises our focus is

on the alternative of printing money and (partial) default. A main factor in explaining why a

government gives in to default and devaluation expectations is the increased costs of servicing the

public debt. Currency and debt crises are symptoms of the underlying weakness of the fiscal position. If

the fiscal position were robust a government could always prevent a debt crises by borrowing to service

its existing debt and it could also defend its currency by borrowing sufficient reserves.

The focus of our analysis is on the interaction between debt and currency crises. The government is not

able or not willing to further increase its tax revenues or to reduce the expenditures, e.g. because of

institutional problems or political pressure. In this situation the government could “finance” its debt

coming due and the public expenditures through a default on its debt (debt crisis), through inflation and

the subsequent devaluation (currency crisis) or through a combination of default and devaluation (twin

crisis).

The world lasts for two periods, labeled 1 and 2. The government issues the domestic currency M,

called the peso, and the foreign debt f denominated in dollars. The foreign debt f is risky and can be

subject to default. fmn denotes foreign debt that is issued in period m and is coming due in period n. i is

the nominal interest rates on the risky foreign currency debt, while i* is the nominal interest rate on risk

free dollar debt. The government enters in period 1 with obligations to pay f01. Real government

consumption in the two periods, g1 and g2, is given exogenously. Purchasing power parity is assumed

- 8 -

to hold so that the exchange rate is equal to the price level P, i.e. E = P with the foreign price level

being unity. In period 1 the peso-dollar-exchange rate is fixed at E1, but it can be changed to E2 in

period 2.

The government’s period 1 budget constraint is

(1) 01111121

1fEgE

ifE

+=+

.

The government finances its period 1 expenditures, i.e., the exogenous public expenditures E1g1 and the

debt coming due E1f01, by issuing foreign debt. Following the original sin hypothesis the government is

constrained to issue foreign currency debt only (see Eichengreen and Hausman 2002). For simplicity

we assume that taxes are levied only in period 2.

In period 2 the government’s budget constraint is

(2) yEMMgEfEfE τη 21222022122 ))(1( +−=++−

The government has to meet its period 2 debt service as well as its current expenditures. These

obligations may be financed by an increase of (high-powered) money held in period 2 over the amount

held in period 1, M2- M1, by an income tax τy, and by defaulting on the fraction η of the foreign debt

fmn. As we are interested in the interaction of debt and currency crises we take the real tax revenues

with the tax rate τ and output y as exogenously given.

Under the assumption of capital mobility the perfect-foresight equilibrium implies that the returns on

the risk free world interest rate i* and the interest rate on the risky foreign debt i are equal ex post,

(3) )1()1)(1( *ii +=−+ η .

Private money demand is given by the simple quantity equation

- 9 -

(4) ykEM tt = )2,1( =t .

The government aims at minimizing the distorting effects of debt and currency crisis. As the

inflation/devaluation rate and the default rate are assumed to be zero in period 1, the loss function of

the government can be written as

(5) 22

221 εθη +=L .

θ measures the relative weight of the exchange rate target vis-à-vis the debt service target in the

government’s loss function. ε is the domestic inflation rate which is also the peso depreciation rate

against the dollar

(6) 2

12

EEE −

=ε .

Simplifying equation (1) and combining equations (2), (4), and (6) leads to

(7) ))(1( 01112 fgif ++=

and

(8) ygffffky τηε −++=++ 202120212 )( .

In period 2 the government minimizes (5) subject to (8) if it cannot precommit to repay all the foreign

debt. This leads to the necessary condition

(9) 0212 ffky +

=ηθε

In the optimum the marginal costs of inflation equal the marginal costs of default on the risky debt.

Using (9) to eliminate ε from (8) gives the preferred default rate under discretion, i.e. the twin crisis, as

(10) 20212

2202120212

)()())((

ffkyygffff

TW++

−+++=

θτθη

- 10 -

Combining equations (7) and (10) shows how the optimal default rate depends on the interest rate of

the risky foreign debt. The arbitrage condition (3) also relates the default rate to the interest rate i

(3’) iii

M +−

=1

*η

In a perfect-foresight equilibrium the default rate that the market expects, equation (3), must be equal to

the default rate the government finds optimal for given market expectations, equations (7) and (10).

Together these conditions can give rise to multiple equilibria (figure 1).

-----------------------------------

Figure 1

------------------------------------

In figure 1 there are two equilibria if the government can not precommit to honor both its debt and its

exchange rate peg. The government’s loss is smaller in the low default equilibrium (iTW1). However,

there is no possibility to ensure that this better equilibrium is realized as the government cannot

credibly commit to not validate expectations if the bond market settles on the high default

equilibrium’s interest rate (iTW2). The high default equilibrium also implies a higher inflation and

depreciation rate (see equation 9), as the increased interest rate leads to higher interest expenditures for

the government. An improvement in the fundamentals shifts the government’s η-i-curve to the

southeast.

What does this analysis imply for the security of foreign debt and the viability of a fixed exchange rate

regime? In principle, a sovereign government can always renege on its debt if the economic conditions

warrant a default. Similarly, a sovereign government can always abandon a currency peg if the

economic conditions make a realignment advantageous. Governments abstain from using these escape

clauses if they face large enough fixed costs of defaulting Cη and of realigning Cε. These costs could

include the political embarrassment, the loss of credibility, and the output losses countries typically

- 11 -

face in the aftermath of currency or debt crashes (see e.g. Dooley 2000, Rose 2002, and Rose and

Spiegel 2002). Without these fixed costs governments would always choose the twin crisis instead a

currency or a debt crisis. As the variable costs are quadratic in the devaluation and the default rate it

would be more favorable to opt for the twin crisis to balance these costs.

With fixed default and devaluation costs the loss function is

(11) εεηη λλεθη CCL +++= 22

221 with λη=1 if η≠0, λε=1 if ε≠0, λη, λε=0 otherwise

instead of (5).

In the following we contrast the purely discretionary regime (twin crisis) analyzed so far with

(1) a no-default regime, in which the default rate η is constrained to be zero but devaluation is

possible (currency crisis only), and

(2) a fixed exchange rate regime, in which the depreciation rate ε is restricted to zero but default is

possible (debt crisis only).

Twin and Currency Crises

In a first step, we compare the purely discretionary policy (twin crisis) with the regime, in which the

government can credibly commit to honor its debt and finances its expenditures by inflation and the

associated devaluation (currency crisis only). Combining equations (9) and (11) yields the loss function

under the twin crisis LTW

(12a) εηθη

θη CC

ffkyLTW ++

+

+=2

0212

2

)(21

21

which together with (10) is

- 12 -

(12a’) εηθθτθ CC

ffky

ffkyygffffLTW ++

+

+

++

−+++=

)()(1

)()())((

21

0212

22

20212

2202120212 .

Accordingly, the loss function under the currency crisis LCU is obtained by combining equations (8) and

(11) and setting η=0

(12b) ετθ C

kyygffLCU +

−++=

220212

2.

with

(1’) ))(1( 01112 fgif ++= .

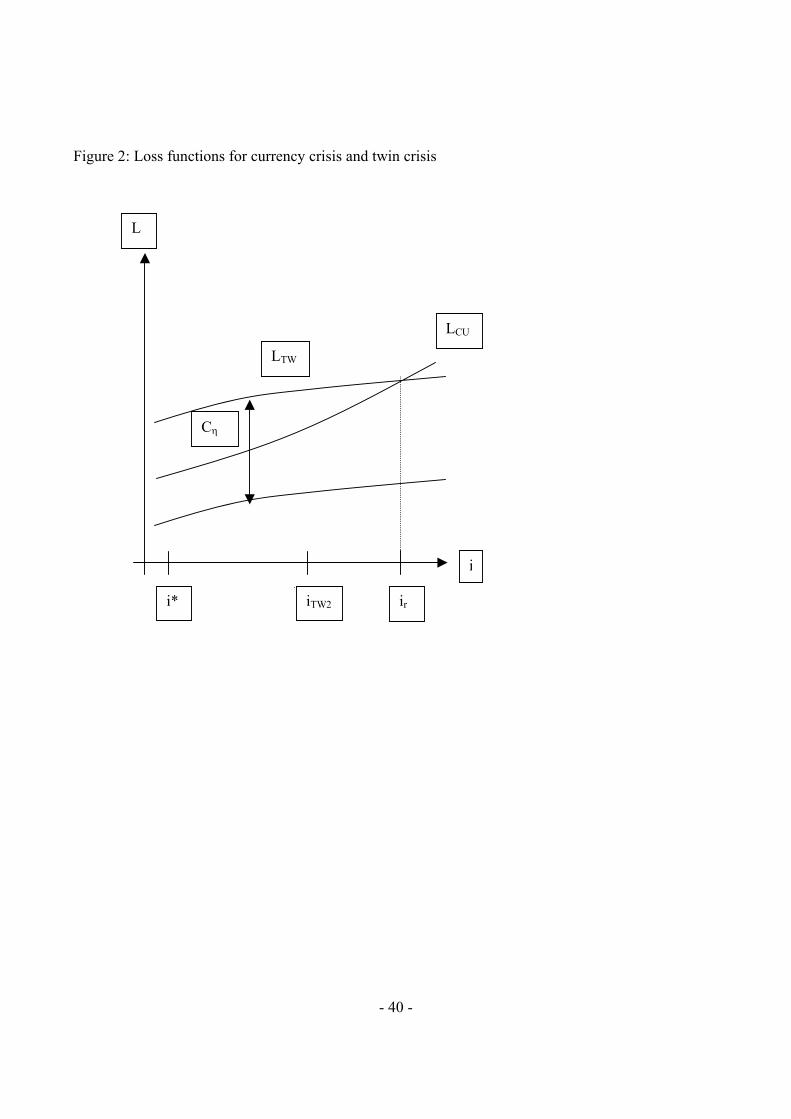

Both loss functions are increasing in the interest rates with i

Li

L CUTW∂

∂<

∂∂

<0 (see figure 2).1 The twin

crisis has the benefit that the government can balance the variable costs of a devaluation and a default

by using two policy instruments instead of only one in the case of a currency crisis. However, the twin

crisis has the disadvantage of the additional fixed costs of the default. With high interest rates the twin

crisis is more attractive as these fixed costs become less important. Also, with a higher debt service the

government can reduce its financing requirements to a larger degree for a given default rate. Therefore,

with higher interest rates it is more likely that the government does not only devalue but also defaults.

For interest rates lower than ir the loss in the case of the currency crisis is smaller than the loss under

the twin crisis and it is optimal for the government to devalue only. In figure 2 the risk free world

interest rate i* and the market interest iTW2 are both to the left of ir. In this case the government only

devalues and the risk free interest i* is realized.

-----------------------------------

Figure 2

------------------------------------

- 13 -

Obviously, any reduction in the fixed cost of an default Cη can cause a twin crisis to arise, ir < iTW2,

where none existed before, i.e. ir > iTW2. Figure 3 shows a situation in which the risk free world interest

rate i* is to the left of ir while the market interest i2 that is compatible with the default rate η2 is to the

right. In this case two very different outcomes are possible. In the relatively good state the market

participants do not expect a default, and the market interest rate is set equal to i* and the government

does not default as ** TWCU LL < . In the bad state the market expects the default rate η2 and the

nominal interest rate is set equal to iTW2. In this situation the loss under the twin crisis is smaller than

the loss under the currency crisis, 22 TWCU LL > . Accordingly, the government reneges on its foreign

debt in a self-fulfilling debt and currency crisis. In this situation there exists an equilibrium in which

there is only a currency crisis if the market expects the government to honor its debt, and an

equilibrium under the same fundamentals in which there is a twin debt and currency crisis if the market

expects the government to renege on its debt.

In an analogous way a deterioration of the fundamentals, e.g. an increase in public expenditures or

debt, also increases the likelihood of a twin crisis as the point of intersection between the two loss

functions moves to the left and the interest rate ir declines. The larger the financing requirements the

more likely a currency crisis leads to a twin crisis, in which the government not only devalues but also

defaults on its debt.

-----------------------------------

Figure 3

------------------------------------

1 For a detailed discussion of the properties of the loss functions see Herz (2003).

- 14 -

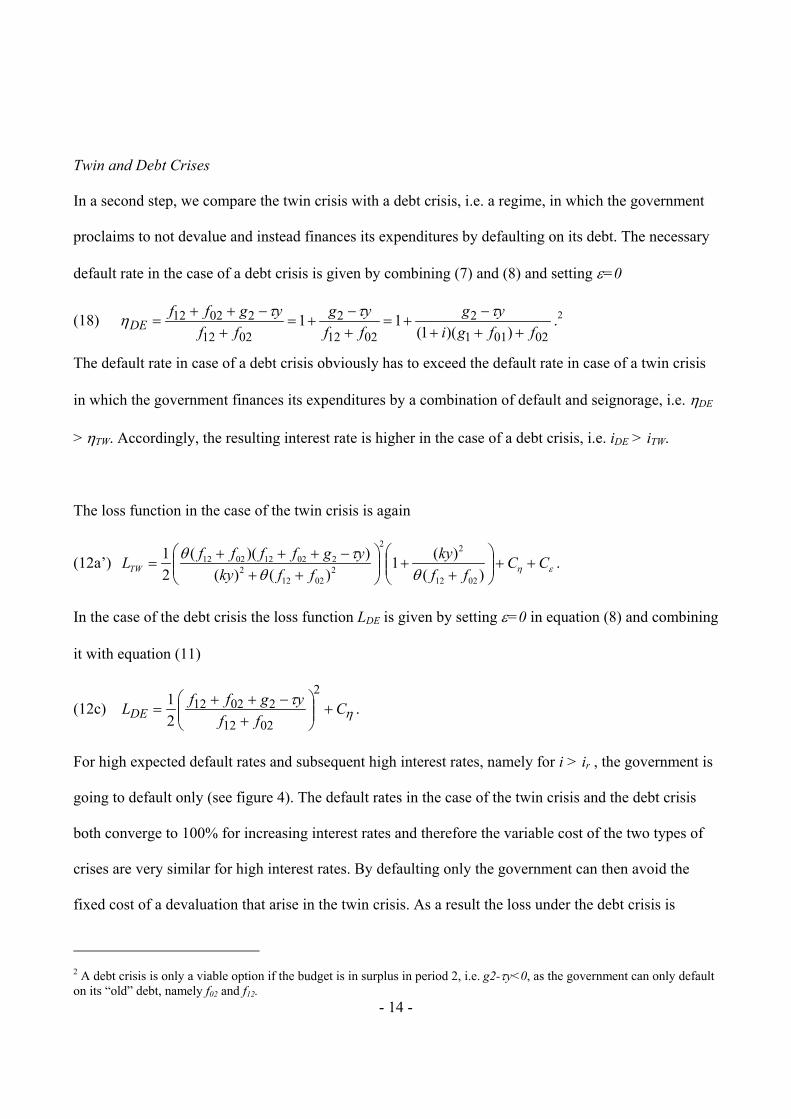

Twin and Debt Crises

In a second step, we compare the twin crisis with a debt crisis, i.e. a regime, in which the government

proclaims to not devalue and instead finances its expenditures by defaulting on its debt. The necessary

default rate in the case of a debt crisis is given by combining (7) and (8) and setting ε=0

(18) 02011

2

0212

2

0212

20212))(1(

11ffgi

ygffyg

ffygff

DE +++−

+=+−

+=+

−++=

τττη .2

The default rate in case of a debt crisis obviously has to exceed the default rate in case of a twin crisis

in which the government finances its expenditures by a combination of default and seignorage, i.e. ηDE

> ηTW. Accordingly, the resulting interest rate is higher in the case of a debt crisis, i.e. iDE > iTW.

The loss function in the case of the twin crisis is again

(12a’) εηθθτθ CC

ffky

ffkyygffffLTW ++

+

+

++

−+++=

)()(1

)()())((

21

0212

22

20212

2202120212 .

In the case of the debt crisis the loss function LDE is given by setting ε=0 in equation (8) and combining

it with equation (11)

(12c) ητ C

ffygffLDE +

+

−++=

2

0212

2021221 .

For high expected default rates and subsequent high interest rates, namely for i > ir , the government is

going to default only (see figure 4). The default rates in the case of the twin crisis and the debt crisis

both converge to 100% for increasing interest rates and therefore the variable cost of the two types of

crises are very similar for high interest rates. By defaulting only the government can then avoid the

fixed cost of a devaluation that arise in the twin crisis. As a result the loss under the debt crisis is

2 A debt crisis is only a viable option if the budget is in surplus in period 2, i.e. g2-τy<0, as the government can only default on its “old” debt, namely f02 and f12.

- 15 -

always smaller than the loss under the twin crisis for (very) high interest rates (for a detailed discussion

see Herz 2003).

If there exists exactly one intersection between the two loss functions than a situation of multiple

equilibria can exist similar to the situation discussed above. Such a situation is likely if the fixed and

variable cost of a devaluation are relatively low so that iTW < ir < iDE holds (see figure 4). Then a twin

crisis with the lower interest rate iTW is realized if the market participants expect the government to both

default and devalue and a debt crisis with the higher interest rate iDE is attained if the market

participants expect the government to default only.3 The government cannot make sure that the better

equilibrium, i.e., the twin crisis with the lower default rate is realized as it cannot bind itself to not

renege on its exchange rate peg.

How does an improvement in the credibility of the exchange rate peg change the government’s

decision? Let us assume that the costs of a devaluation are increased by making it more difficult and

costly for the government to give up the exchange rate peg, e.g. via a currency board, so that ir < iTW <

iDE holds. In this case the government is always going to choose the debt crisis and the equilibrium with

the higher default rate and the higher interest rate iDE is attained. Strengthening the fixed exchange rate

regime can therefore increase the likelihood and the severity of a debt crisis as the government is left

with only one instrument to finance its expenditures. Thus, sound fiscal policies are especially

important if governments want to fix their exchange rate.

Taken together currency and debt crises are generally caused by the interactions between fundamental

and expectational effects. The simultaneous occurrence of currency and debt crises can be caused by

common fundamental factors and/or internal contagion effects from one crisis to the other. This

- 16 -

internal contagion can arise from multiple equilibria in which the expectation of an imminent default

increases the interest rates and the debt service. The subsequent deterioration of the fiscal position can

induce the government to default and inflate/devalue. In the following section we empirically analyze

this role of common fundamental factors and/or internal contagion for the likelihood of twin currency

and debt crisis.

-----------------------------------

Figure 4

------------------------------------

3. Empirical Analysis

3.1 Data

There are two basic approaches to define currency crises. Frankel and Rose (1996) define a currency

crisis as a nominal depreciation of the currency of at least 25% p.a. and a change in the rate of

depreciation that is at least 10%. Following Eichengreen et al. (1995) and Kaminsky and Reinhart

(1999), Glick and Hutchison (1999) define currency crises according to an average of exchange-rate

and reserve changes to account for successful as well as unsuccessful speculative attacks. We follow

Frankel and Rose (1996)’s definition because our theoretical model focuses on successful currency

attacks.

To define debt crises we refer to the date of the Paris Club debt reschedulings (treatments) (see Sy

(2003) for “sovereign distress” as an alternative measure of debt crises). The Paris Club is an informal

3 For ir < iTW < iDE the debt crisis with the interest rate iDE is realized and for iTW < iDE < ir the twin crisis with the interest rate iTW is the only outcome.

- 17 -

group of official creditors whose role is to find coordinated and sustainable solutions to the payment

difficulties experienced by debtor nations (see Paris Club 2003). Debtor countries can initiate

negotiations to reschedule their debt, which are typically concluded within up to six months.

Rescheduling is a means of providing a country with debt relief through a postponement and, in the

case of concessional rescheduling, a reduction in debt service obligations. To account for the

negotiation process between the onset of the debt crisis and the reschedulings we use one–year ahead

treatment as an indicator for the debt crisis in the current year. So if there is a treatment in 2001, then

we record the year 2000 as having debt crisis.

In our sample there are 111 currency only crises, 126 debt only crises, and 24 twin crises (table 2). As

is evident from table 2 a debt crisis is much more likely to occur when there is a contemporary

currency crisis and vice versa. A debt crisis occurred in 10.9 per cent of the cases when there was no

currency crisis, while it occurred in 17.8 per cent of the cases where there was a currency crisis.

Accordingly, the likelihood of a currency crisis was 9.7 per cent if there was no debt crisis and 16 per

cent in case of a debt crisis.

-----------------------------------

table 2

------------------------------------

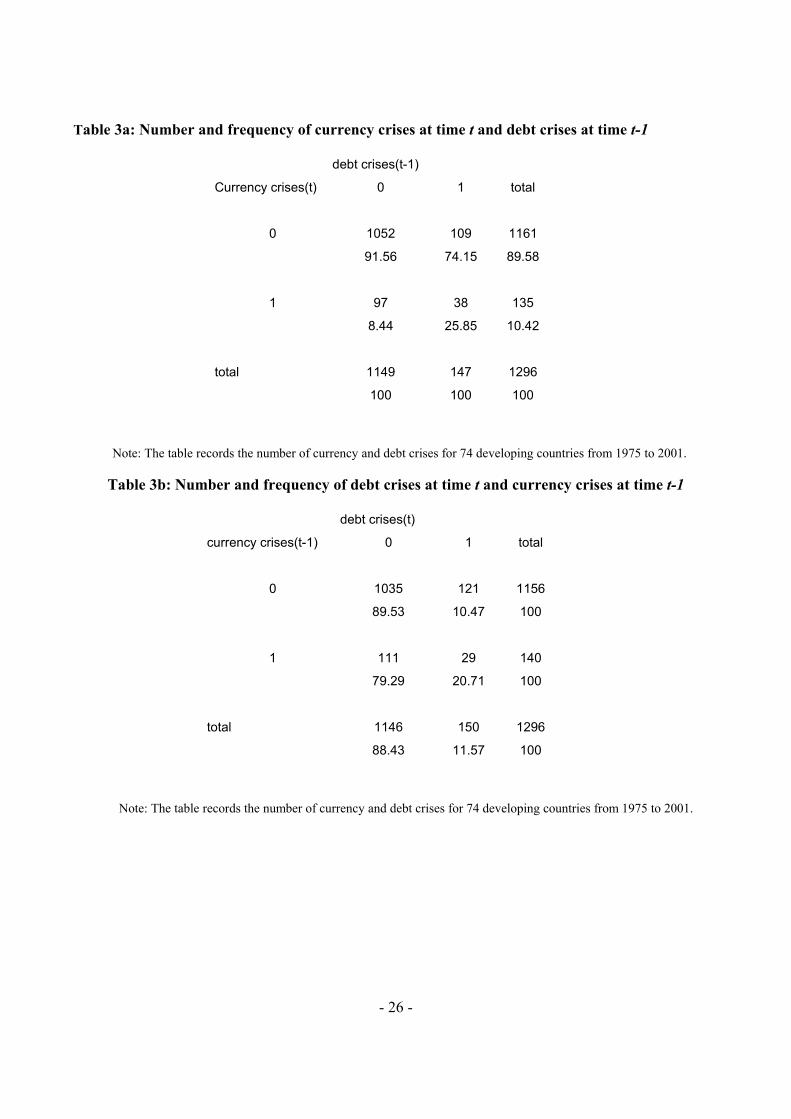

Tables 3a and 3b provide some additional information on the time pattern between debt and currency

crises. Table 3a gives the frequency of currency crises conditioned on whether there is a debt crisis in

year t-1, and table 3b presents the frequency of debt crises conditioned on whether there is a currency

crisis in year t-1. Tables 3a and 3b suggest that currency crises tend to lead debt crises, while a reverse

link also has strong support. Table 4a and 4b, which give similar information for the case of a two year

lag, suggest that currency crises tend to lead debt crises, while a reverse link has little support.

- 18 -

Obviously, these summary statistics only provide a univariate analysis of the correlation between debt

and currency crises, and do not take into account macroeconomic factors.

-----------------------------------

table 3a

------------------------------------

-----------------------------------

table 3b

------------------------------------

-----------------------------------

table 4a

------------------------------------

-----------------------------------

table 4b

------------------------------------

4. Statistical Model

4.1. The model

In this section we analyze the role of common macroeconomic factors and internal contagion from one

type of crisis to the other for the occurrence of twin crises, i.e. the simultaneous occurrence of debt and

currency crises. We also test for the Granger-type causality between the debt and currency crises.

Denote ty1 and ty2 as dummy indicators for currency and debt crises respectively. We assume there

are two latent variables for the currency crisis ( *1ty ), and the debt crisis ( *

2ty ). A currency crisis occurs

- 19 -

( )11 =ty when *1ty >0, a debt crisis occurs ( )12 =ty when *

2ty >0, and a twin crisis

( )1&1 21 == tt yy occurs when both *1ty >0 and *

2ty >0. We assume

ttttt

ttttt

yyXy

yyXy

2123112110*2

1123112110*1

εββββ

εαααα

++++=

++++=

−−−

−−−

The shock terms t1ε and t2ε are assumed to follow the stationary normal distribution

Ν

1

1,

00

~2

1

ρρ

εε

t

t .

No serial correlation exists between the shock terms, which is not a strong assumption if we include

enough lags of tX , ty1 and ty2 . 11 −ty and 12 −ty are the lagged currency and debt crises indicators, 1−tX

are lagged macroeconomic factors. 1−tX includes the variables discussed in the theoretical model above

which can be grouped into :

• fiscal conditions:

o level and structure of debt: the ratio of external debt over GDP, net inflows of foreign

direct investment over total external debt ratio; short-term debt over total external debt

ratio; government deficit over GDP ratio,

o debt services: debt service over GDP ratio.

• monetary conditions: domestic credit growth rate, real exchange rate overvaluation, foreign

reserves over imports ratio.

• other macroeconomic indicators: domestic and world GDP growth rate,

• structural variables (original sin): real GDP per capita and country size,

The construction of the exchange rate overvaluation is similar to Frankel and Rose (1996).

Overvaluation is defined as the deviation from purchasing power parity which is measured as the

country-specific average bilateral real exchange rate with the US dollar over the sample. We proxy the

- 20 -

world GDP growth rate with the U.S. real GDP growth. We assume that no correlation exists between

1−tX and t1ε , or between 1−tX and t2ε . To control for possible endogeneity, all the macroeconomic

variables are taken with one-year lag unless specified otherwise.

A maximum likelihood estimation of the above two-equation Probit model is performed to efficiently

estimate the parameters. Compared with the separate estimation of a single equation Probit model, the

joint estimation considers the correlation between the shock terms t1ε and t2ε , and thus uses more

information and provides more efficient estimators. The joint probability distribution of ( ty1 , ty2 ) is

given by the following expressions:

( ) ( )( ) ( )( ) ( )( ) ( )ttttt

ttttt

ttttt

ttttt

UVBinormyyPUVBinormyyP

UVBinormyyPUVBinormyyP

ρβαρβα

ρβαρβα

,,0,0Pr,,1,0Pr

,,0,1Pr,,1,1Pr

2100

2101

2110

2111

−−====−−====

−−========

where

123112110

123112110

−−−

−−−

+++=+++=

tttt

tttt

yyXUyyXV

βββββααααα

and ( )321 ,, λλλBinorm is the cumulative distribution function evaluated at (λ1,λ2) for a standardized

Bivariate normal distribution, which has means (0,0), standard errors (1,1) and a correlation coefficient

λ3. The total number of observations is the multiplication of the number of countries and the number of

observed years. To estimate the parameters, we maximize the following likelihood function

( ) ( ) ( )( )21212121 1100

101

11011

yyyyyyyy

tPPPPL −−−−Π=

which is the multiplication over the whole sample of observations. We report in table 5 the robust

variance-covariance matrix for the estimated parameters to account for the possibility of likelihood-

function misspecification as suggested in White (1982).

- 21 -

4.2. Estimation results

Our main estimation results can be summarized as follows. First, when estimating simultaneously

the *1ty equation (currency crisis) and the *

2ty equation (debt crisis), we find strong evidence for a

Granger-type causality from debt crises to currency crises, and weak evidence for a Granger-type

causality from currency crises to debt crises (see table 5). The coefficient of the one-year lagged debt

crisis in the *1ty equation (currency crisis) is 0.52, which is different from zero at the 0.001%

significance level. The coefficient of the two-year lagged currency crisis in the *2ty equation (debt

crisis) is 0.27, which is different from zero only at the 8% significance level. We have not included any

contemporary effect from the occurrence of a debt crisis on the currency crisis and vice versa.

Secondly, we find strong evidence that debt and currency crises have common fundamental causes. We

find that reserve over imports ratio, domestic GDP growth rate, and FDI over external debt affect both

currency and debt crises. External debt over GDP, domestic credit growth rate, overvaluation, and the

log of GDP as a proxy for original sin affect the currency crises, but not the debt crises (table 5).

Detragiache and Spilimbergo (2002) find that the debt service due over the government revenue ratio,

one-period lagged short-term debt, and one-period lagged foreign reserve are significant factors for the

debt crisis. Our results are partially consistent with theirs in that foreign reserve is an important factor

for the debt crisis. However, we do not find that the debt service due and the one-period lagged short-

term debt are significant.

Thirdly, the correlation ρ (rho) across the shock terms ε1t and ε2t is -.0001, which is not significantly

different from zero. So it is unlikely that there are unobserved common macroeconomic factors that

- 22 -

affect both crises. Also, it is not likely that there is contemporary contagion between currency and debt

crises.

Fourthly, we also include as structural variables the GDP per capita and country size as a proxy for

original sin effects (see Eichengreen and Hausman 2002). Both of theses measures are not significant in

debt crisis equation at conventional significance levels. However, the (log) level of GDP affects the

currency crises. Its coefficient is 0.096, different from 0 at the 1% significance level. This suggests that

among developing countries, as the GDP level goes up, a currency crisis is more likely to occur. This

could be due to the fact that economically bigger countries are more likely to participate in

international market transactions.

Finally, we find that the M3 over total external debt has a significant impact on the debt crisis. The

coefficient for M3 over total external debt is –0.15, significantly different from 0 at 2% level. This is

consistent with our hypothesis that as the money supply goes up the inflation tax yields more revenues

relative to the default, so that the debt crisis will be less likely to occur. M3 over total external debt has

no significant impact on the currency crisis, however.

Sensitivity Analysis

To get a better understanding of the role of the direct linkages between the two types of crises relative

to the role of the common factors we also estimate each crisis separately without including the other

crisis as predetermined explanatory variable and compare our results with previous work that estimates

currency crisis only (e.g. Frankel and Rose 1996) and the debt crisis only (e.g. Detragiache and

Spilimbergo 2002). We use the Probit model for each crisis. As far as the macroeconomic variables are

concerned, the results from the individual estimations (in table 6a, 6b) are similar to the joint estimation

results in table 5. This is consistent with the finding in table 5 that the correlation across error terms

- 23 -

(rho) is not significantly different from 0. However, the log-likelihood of the joint estimation is –728.1

(table 5) , while the sum of log-likelihoods for Table 6a and 6b is –737.44 . So joint estimation in table

5 is better in that it has a higher log-likelihood, which is consistent with the significant coefficient of

lagged debt (currency) crisis indicator in the currency (debt) crisis equation.

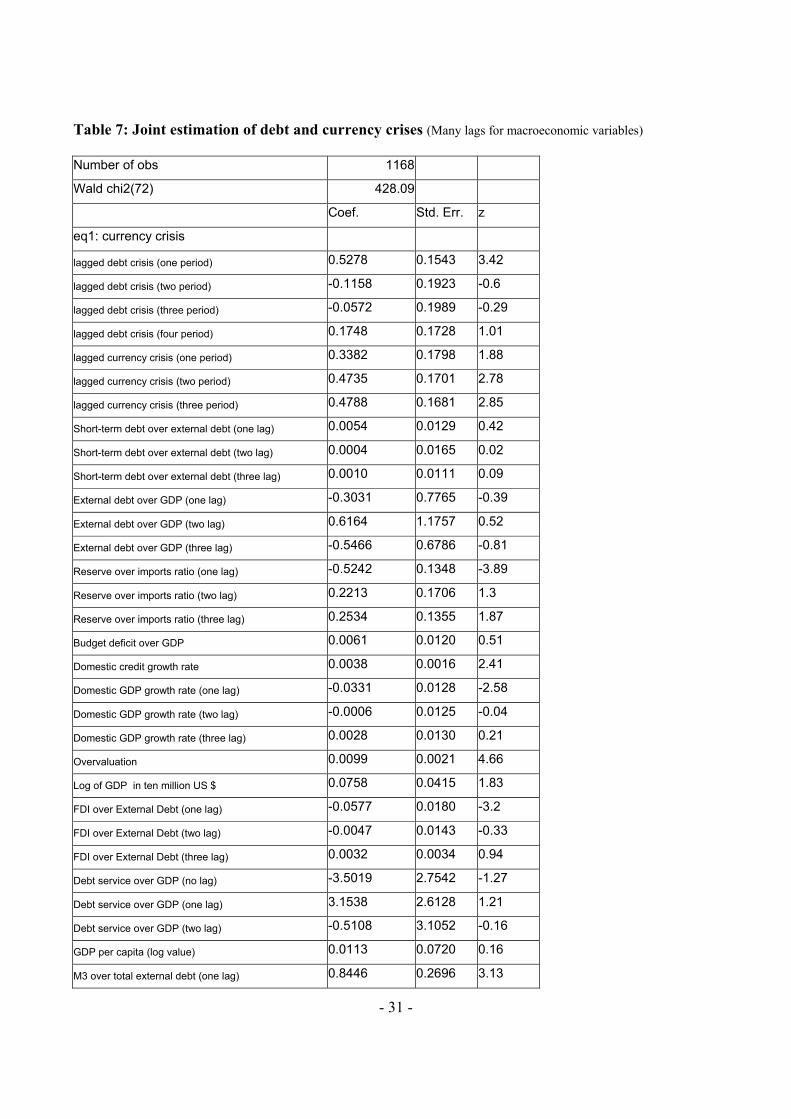

A major point in our analysis is the possible role of one type of crisis on the other class of crisis after

controlling for other common fundamental factors. Therefore, we jointly estimate the two equations

with the same lag length for fundamentals as well as crises and get results similar to those in table 5.

We still have the following key results: the correlation across error terms( rho) is not significantly

different from 0; and one-year lagged reserve over imports ratio and one-year lagged domestic GDP

growth rate are the common factors (see table 7). For the debt crisis, FDI over external debt ratio now

is different from 0 only at 14% significance level instead of the 7% level as in table 5. We do not want

to overinterpret the results when the fundamental variables have many lags, in that there can be high

correlation among them. For example, the correlation between “M3 over external debt ratio” and its

one-year lag is as high as 0.98.

Detragiache and Spilimbergo (2002) use a four-year window for the debt crisis, because they want to

distinguish the beginning of a new crisis from the continuation of the preceding one. They treat crises

beginning within four years since the end of the past crisis as the continuation of the crisis, and they

analyze the onset of the debt crisis only. We use Paris Club treatments as debt crisis indicators which

are less autocorrelated than the indicators employed by Detragiache and Spilimbergo. Therefore we

impose only a one-year window, and get results that are similar to our baseline estimates (see table 8).

Table 8 shows that reserve over imports ratio, FDI over external debt, and M3 over total external debt

still have significant impact on debt crisis occurrence. But domestic GDP growth rate is not as

significant as in table 5.

- 24 -

Note that we use M3 over Debt and Debt over GDP in regressions of table 5. Instead of these two

variables, we also try the following two variables: external debt over GDP, and money over GDP. For

the currency crisis equation, external debt over GDP still has a significant negative coefficient, while

money over GDP has no effect. For the debt crisis equation, external debt over GDP has a positive

coefficient and different from 0 at 7% significance level. Again money over GDP has no effect on the

debt crisis (table 9).

5. Conclusion

In this paper, we have systematically investigated the potential linkages between debt and currency

crises. Our starting point was the question whether the strong contemporary association between these

two types of crises is caused by linkages between the debt and currency crisis or by common

macroeconomic factors.

We find Granger-type causality between debt and currency crises. One-year lagged debt crises can

significantly help predict currency crises, while two-year lagged currency crisis also has some weak

power in predicting debt crises. Our empirical results indicate that some macroeconomic variables help

predict debt as well as currency crises. Low FDI relative to external debt, low foreign reserve relative

to imports and low GDP growth rate all increase the likelihood of debt and currency crises. These

results are a first indication that common macroeconomic fundamentals play an important role for the

occurrence of twin crises. This broader view on both debt and currency crises strengthens the role of

sound macroeconomic policies. By pursuing stability orientated policies governments can earn a

double dividend of lowering the likelihood of debt as well as currency crises.

- 25 -

The results presented in this paper are a first step in evaluating and understanding the complex linkages

between debt and currency crises which can give rise to twin crises. Evidently, examining how the

government deals with single crises and how this affects default and devaluation expectations helps to

better understand when single crises give rise to twin crises.

Table 2: Number of debt, currency and twin crises from 1975 to 2001

debt crises(t)

currency crises(t) 0 1 total

0 1035 126 1161

89.15 10.85 100

90.31 84 89.58

1 111 24 135

82.22 17.78 100

9.69 16 10.42

total 1146 150 1296

88.43 11.57 100

100 100 100

Note: The table records the number of currency and debt crises for 74 developing countries from 1975

to 2001

- 26 -

Table 3a: Number and frequency of currency crises at time t and debt crises at time t-1

debt crises(t-1)

Currency crises(t) 0 1 total

0 1052 109 1161

91.56 74.15 89.58

1 97 38 135

8.44 25.85 10.42

total 1149 147 1296

100 100 100

Note: The table records the number of currency and debt crises for 74 developing countries from 1975 to 2001.

Table 3b: Number and frequency of debt crises at time t and currency crises at time t-1

debt crises(t)

currency crises(t-1) 0 1 total

0 1035 121 1156

89.53 10.47 100

1 111 29 140

79.29 20.71 100

total 1146 150 1296

88.43 11.57 100

Note: The table records the number of currency and debt crises for 74 developing countries from 1975 to 2001.

- 27 -

Table 4a: Number and frequency of currency crises at time t and debt crises at time t-2

debt crises(t-2)

currency crises(t) 0 1 total

0 1037 124 1161

89.78 87.94 89.58

1 118 17 135

10.22 12.06 10.42

total 1155 141 1296

100 100 100

Note: The table records the number of currency and debt crises for 74 developing countries from 1975 to 2001.

Table 4b: Number and frequency of debt crises at time t and currency crises at time t-2

Note: The table records the number of currency and debt crises for 74 developing countries from 1975 to 2001.

debt crises(t)

currency crises(t-2) 0 1 total

0 1037 118 1155

89.78 10.22 100

1 109 32 141

77.3 22.7 100

total 1146 150 1296

88.43 11.57 100

- 28 -

Table 5: Joint estimation of debt and currency crises

Number of obs 1275

Wald chi2(42) 375.23

Log-likelihood -728.11373

eq1: currency crisis eq2: debt crisis

Coef. Std. Err. z Coef. Std. Err. z

lagged debt crisis (one period) 0.5059 0.1433 3.53 -0.0662 0.1555 -0.43

lagged debt crisis (two period) -0.2174 0.1756 -1.24 0.7263 0.1384 5.25

lagged debt crisis (three period) -0.0138 0.1767 -0.08 0.4784 0.1597 3

lagged debt crisis (four period) 0.2374 0.1671 1.42 0.3705 0.1541 2.4

lagged currency crisis (one period) 0.2230 0.1689 1.32 0.0391 0.1646 0.24

lagged currency crisis (two period) 0.3219 0.1636 1.97 0.2722 0.1574 1.73

lagged currency crisis (three period) 0.4022 0.1543 2.61 0.1265 0.1620 0.78

Short-term debt over external debt 0.0047 0.0058 0.82 -0.0003 0.0058 -0.05

External debt over GDP -0.2662 0.1263 -2.11 0.0717 0.0979 0.73

Reserve over imports ratio -0.0009 0.0003 -3.31 -0.0009 0.0003 -3.22

Budget deficit over GDP 0.0037 0.0111 0.33 -0.0074 0.0107 -0.69

Domestic credit growth rate 0.0041 0.0014 2.90 -0.0011 0.0013 -0.89

Domestic GDP growth rate -0.0318 0.0100 -3.17 -0.0243 0.0097 -2.51

Overvaluation 0.0073 0.0020 3.61 0.0012 0.0017 0.71

World GDP growth rate -0.0256 0.0234 -1.09 0.0133 0.0237 0.56

Log of GDP in ten million US $ 0.0965 0.0379 2.55 0.0200 0.0360 0.56

FDI over External Debt -0.0521 0.0168 -3.11 -0.0296 0.0165 -1.79

Debt service over GDP 1.8193 1.5268 1.19 1.7280 1.4080 1.23

GDP per capita (log value) 0.0100 0.0647 0.16 0.0109 0.0658 0.17

M3 over total external debt -0.0556 0.0602 -0.92 -0.1525 0.0640 -2.38

_cons -1.4007 0.6190 -2.26 -0.2609 0.6138 -0.43

eq3: correlation across error

terms( rho) -0.001 0.0825 0

- 29 -

Table 6a. Probit Estimation of Currency Crises

Probit estimates

Number of obs 1296

Wald chi2(17) 134.92

Log-likelihood -365.17

Pseudo R2 0.1785

Coef. Std. Err. z

lagged currency crisis (one period) 0.2115 0.1662 1.27

lagged currency crisis (two period) 0.3371 0.1585 2.13

lagged currency crisis (three period) 0.4912 0.1526 3.22

Short-term debt over external debt 0.0038 0.0057 0.68

External debt over GDP -0.2477 0.1175 -2.11

Reserve over imports ratio -0.0010 0.0003 -3.64

Budget deficit over GDP 0.0002 0.0107 0.02

Domestic credit growth rate 0.0038 0.0014 2.73

Domestic GDP growth rate -0.0303 0.0100 -3.02

Overvaluation 0.0071 0.0019 3.71

World GDP growth rate -0.0285 0.0233 -1.22

Log of GDP in ten million US $ 0.0995 0.0371 2.68

FDI over External Debt -0.0559 0.0165 -3.39

Debt service over GDP 1.7149 1.4969 1.15

GDP per capita (log value) 0.0063 0.0048 1.33

M3 over total external debt 0.0245 0.0641 0.38

_cons -0.0852 0.0563 -1.51

- 30 -

Table 6b. Probit Estimation of Debt Crises

Probit estimates

Number of obs 1275

Wald chi2(18) 188.02

Log-lkelihood -372.25

Pseudo R2 0.2077

Coef. Std. Err. z

lagged debt crisis (one period) -0.0572 0.1545 -0.37

lagged debt crisis (two period) 0.7401 0.1367 5.42

lagged debt crisis (three period) 0.5186 0.1544 3.36

lagged debt crisis (four period) 0.3744 0.1504 2.49

Short-term debt over external debt 0.0002 0.0057 0.03

External debt over GDP 0.0488 0.0989 0.49

Reserve over imports ratio -0.0009 0.0003 -3.2

Budget deficit over GDP -0.0082 0.0107 -0.76

Domestic credit growth rate -0.0004 0.0012 -0.32

Domestic GDP growth rate -0.0269 0.0096 -2.8

Overvaluation 0.0004 0.0016 0.25

World GDP growth rate 0.0103 0.0240 0.43

Log of GDP in ten million US $ 0.0241 0.0356 0.68

FDI over External Debt -0.0312 0.0165 -1.9

Debt service over GDP 1.5798 1.4222 1.11

GDP per capita (log value) 0.0144 0.0656 0.22

M3 over total external debt -0.1715 0.0627 -2.73

_cons -0.0982 0.6036 -0.16

- 31 -

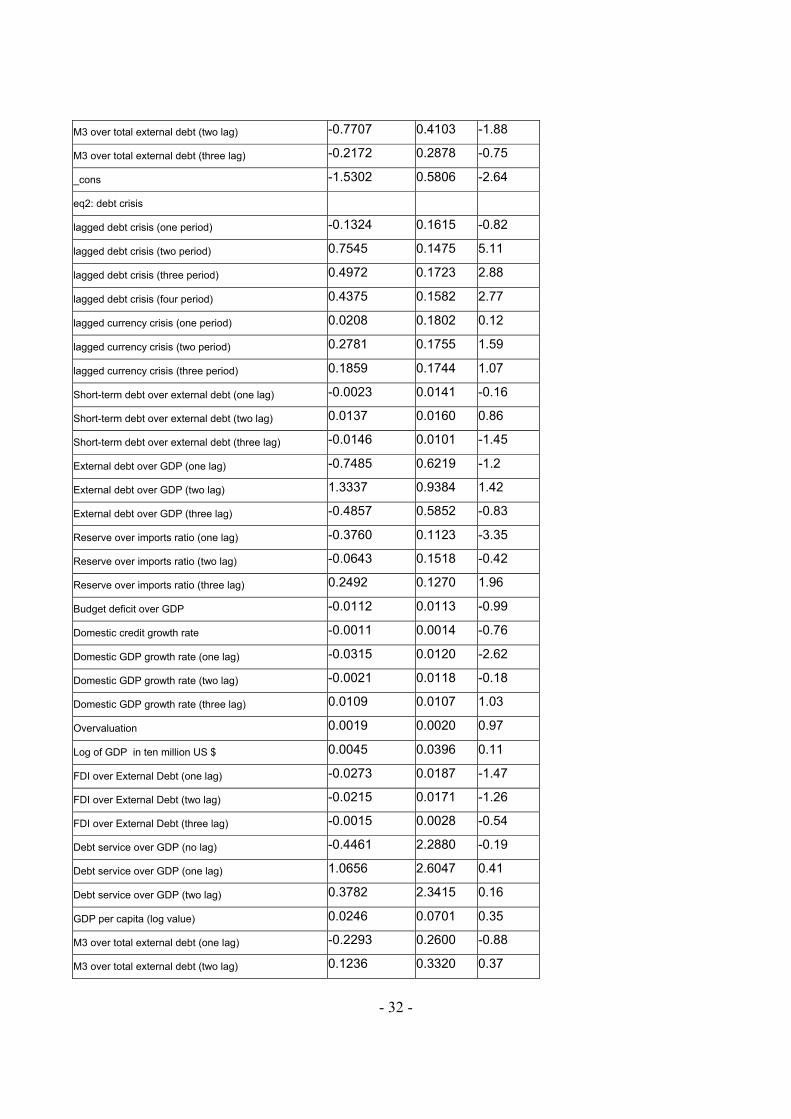

Table 7: Joint estimation of debt and currency crises (Many lags for macroeconomic variables)

Number of obs 1168

Wald chi2(72) 428.09

Coef. Std. Err. z

eq1: currency crisis

lagged debt crisis (one period) 0.5278 0.1543 3.42

lagged debt crisis (two period) -0.1158 0.1923 -0.6

lagged debt crisis (three period) -0.0572 0.1989 -0.29

lagged debt crisis (four period) 0.1748 0.1728 1.01

lagged currency crisis (one period) 0.3382 0.1798 1.88

lagged currency crisis (two period) 0.4735 0.1701 2.78

lagged currency crisis (three period) 0.4788 0.1681 2.85

Short-term debt over external debt (one lag) 0.0054 0.0129 0.42

Short-term debt over external debt (two lag) 0.0004 0.0165 0.02

Short-term debt over external debt (three lag) 0.0010 0.0111 0.09

External debt over GDP (one lag) -0.3031 0.7765 -0.39

External debt over GDP (two lag) 0.6164 1.1757 0.52

External debt over GDP (three lag) -0.5466 0.6786 -0.81

Reserve over imports ratio (one lag) -0.5242 0.1348 -3.89

Reserve over imports ratio (two lag) 0.2213 0.1706 1.3

Reserve over imports ratio (three lag) 0.2534 0.1355 1.87

Budget deficit over GDP 0.0061 0.0120 0.51

Domestic credit growth rate 0.0038 0.0016 2.41

Domestic GDP growth rate (one lag) -0.0331 0.0128 -2.58

Domestic GDP growth rate (two lag) -0.0006 0.0125 -0.04

Domestic GDP growth rate (three lag) 0.0028 0.0130 0.21

Overvaluation 0.0099 0.0021 4.66

Log of GDP in ten million US $ 0.0758 0.0415 1.83

FDI over External Debt (one lag) -0.0577 0.0180 -3.2

FDI over External Debt (two lag) -0.0047 0.0143 -0.33

FDI over External Debt (three lag) 0.0032 0.0034 0.94

Debt service over GDP (no lag) -3.5019 2.7542 -1.27

Debt service over GDP (one lag) 3.1538 2.6128 1.21

Debt service over GDP (two lag) -0.5108 3.1052 -0.16

GDP per capita (log value) 0.0113 0.0720 0.16

M3 over total external debt (one lag) 0.8446 0.2696 3.13

- 32 -

M3 over total external debt (two lag) -0.7707 0.4103 -1.88

M3 over total external debt (three lag) -0.2172 0.2878 -0.75

_cons -1.5302 0.5806 -2.64

eq2: debt crisis

lagged debt crisis (one period) -0.1324 0.1615 -0.82

lagged debt crisis (two period) 0.7545 0.1475 5.11

lagged debt crisis (three period) 0.4972 0.1723 2.88

lagged debt crisis (four period) 0.4375 0.1582 2.77

lagged currency crisis (one period) 0.0208 0.1802 0.12

lagged currency crisis (two period) 0.2781 0.1755 1.59

lagged currency crisis (three period) 0.1859 0.1744 1.07

Short-term debt over external debt (one lag) -0.0023 0.0141 -0.16

Short-term debt over external debt (two lag) 0.0137 0.0160 0.86

Short-term debt over external debt (three lag) -0.0146 0.0101 -1.45

External debt over GDP (one lag) -0.7485 0.6219 -1.2

External debt over GDP (two lag) 1.3337 0.9384 1.42

External debt over GDP (three lag) -0.4857 0.5852 -0.83

Reserve over imports ratio (one lag) -0.3760 0.1123 -3.35

Reserve over imports ratio (two lag) -0.0643 0.1518 -0.42

Reserve over imports ratio (three lag) 0.2492 0.1270 1.96

Budget deficit over GDP -0.0112 0.0113 -0.99

Domestic credit growth rate -0.0011 0.0014 -0.76

Domestic GDP growth rate (one lag) -0.0315 0.0120 -2.62

Domestic GDP growth rate (two lag) -0.0021 0.0118 -0.18

Domestic GDP growth rate (three lag) 0.0109 0.0107 1.03

Overvaluation 0.0019 0.0020 0.97

Log of GDP in ten million US $ 0.0045 0.0396 0.11

FDI over External Debt (one lag) -0.0273 0.0187 -1.47

FDI over External Debt (two lag) -0.0215 0.0171 -1.26

FDI over External Debt (three lag) -0.0015 0.0028 -0.54

Debt service over GDP (no lag) -0.4461 2.2880 -0.19

Debt service over GDP (one lag) 1.0656 2.6047 0.41

Debt service over GDP (two lag) 0.3782 2.3415 0.16

GDP per capita (log value) 0.0246 0.0701 0.35

M3 over total external debt (one lag) -0.2293 0.2600 -0.88

M3 over total external debt (two lag) 0.1236 0.3320 0.37

- 33 -

M3 over total external debt (three lag) 0.0393 0.2260 0.17

_cons -0.7912 0.5407 -1.46

eq3: correlation across error terms( rho) -0.0241 0.0847 -0.28

- 34 -

Table 8. Debt Crises with One-Year Exclusion Window

Probit estimates

Number of obs 1241

Wald chi2(13) 80.26

Prob > chi2 0

Pseudo R2 0.1225

Coef. Std. Err. z

Short-term debt over external debt -0.0082 0.0062 -1.31

External debt over GDP 0.1139 0.0977 1.17

Reserve over imports ratio -0.0008 0.0003 -2.7

Budget deficit over GDP 0.0003 0.0106 0.03

Domestic credit growth rate -0.0003 0.0013 -0.2

Domestic GDP growth rate -0.0155 0.0105 -1.48

Overvaluation 0.0008 0.0017 0.49

World GDP growth rate 0.0198 0.0257 0.77

Log of GDP in ten million US $ 0.0381 0.0361 1.06

FDI over External Debt -0.0430 0.0189 -2.28

Debt service over GDP 0.6304 1.5139 0.42

GDP per capita (log value) 0.0111 0.0661 0.17

M3 over total external debt -0.2534 0.0555 -4.57

_cons -1.3993 0.4458 -3.14

- 35 -

Table 9: Joint estimation of debt and currency crises

Number of obs 1275

Wald chi2(42) 376.64

Log-likelihood -730.9

eq1: currency crisis eq2: debt crisis

Coef. Std. Err. z Coef. Std. Err. z

lagged debt crisis (one period) 0.5414 0.1419 3.81 -0.0512 0.1531 -0.33

lagged debt crisis (two period) -0.2002 0.1732 -1.16 0.7626 0.1379 5.53

lagged debt crisis (three period) 0.0036 0.1749 0.02 0.5082 0.1610 3.16

lagged debt crisis (four period) 0.2391 0.1666 1.43 0.3777 0.1549 2.44

lagged currency crisis (one period) 0.2265 0.1685 1.34 0.0619 0.1626 0.38

lagged currency crisis (two period) 0.3293 0.1626 2.02 0.2963 0.1555 1.91

lagged currency crisis (three period) 0.4171 0.1542 2.71 0.1469 0.1596 0.92

Short-term debt over external debt 0.0050 0.0057 0.88 0.0001 0.0057 0.02

External debt over GDP -0.2330 0.1208 -1.93 0.1687 0.0940 1.8

Reserve over imports ratio -0.0009 0.0003 -3.36 -0.0009 0.0003 -3.24

Budget deficit over GDP 0.0044 0.0113 0.39 -0.0079 0.0113 -0.7

Domestic credit growth rate 0.0040 0.0014 2.88 -0.0017 0.0013 -1.29

Domestic GDP growth rate -0.0324 0.0101 -3.2 -0.0250 0.0097 -2.58

Overvaluation 0.0081 0.0019 4.26 0.0013 0.0017 0.74

World GDP growth rate -0.0270 0.0232 -1.16 0.0147 0.0236 0.63

Log of GDP in ten million US $ 0.0938 0.0377 2.49 0.0197 0.0358 0.55

FDI over External Debt -0.0521 0.0164 -3.17 -0.0321 0.0164 -1.96

Debt service over GDP 1.9387 1.5196 1.28 2.3772 1.3998 1.7

GDP per capita (log value) -0.0063 0.0652 -0.1 0.0016 0.0653 0.02

M3 over GDP 0.0001 0.0031 0.01 -0.0043 0.0031 -1.38

_cons -1.7811 0.4433 -4.02 -1.4501 0.4403 -3.29

eq3: correlation across error terms( rho) 0.0083 0.0823 0.1

- 36 -

References

Aizenman, Joshua, Kletzer, Kenneth and Brian Pinto, 2002. Sargent-Wallace meets Krugman-Flood-

Garber, or: why sovereign debt swaps do not avert macroeconomic crises, NBER Working Paper 9190.

Bauer, Christian, Herz, Bernhard and Volker Karb, 2003. The other twins: debt and currency crises,

University of Bayreuth Discussion Papers # 4-2003.

Benigno, Peripaolo and Alessandro Missale (2001). High Public debt in Currency Crises:

Fundamentals versus Signaling Effects, CEPR Discussion Paper 2862.

Bordo, Michael, Barry Eichengreen, Daniela Klingebiel and Maria Soledad Martinez-Peria , 2001.

Financial crises – lessons from the last 120 years, Economic Policy, 53-82.

Burnside, Craig, Martin Eichenbaum, and Sergio Rebelo, 2001. On the fiscal implications of twin

crises, NBER Working Paper No. 8277.

Chang, Roberto and Andres Velasco (1999). Liquidity Crises in Emerging Markets: Theory and Policy,

NBER Working Paper 7272.

Chiodo, Abbigail and Michael Owyang, 2002. A case study of currency crisis: The Russian default of

1998, Review, Federal Reserve Bank of St. Louis, 7-17.

Corsetti, Giancarlo and Bartosz Mackowiak, 2000. Nominal debt and the dynamics of currency crises,

Yale Economic Growth Center Discussion Paper no. 820.

Dooley, Michael, 2000. A model of crises in emerging markets, The Economic Journal , 110, 256-272.

Dornbusch, Rudiger, 1998, Debt and Monetary Policy: The Policy Issues, in Guillermo Calvo and

Mervyn King (Eds.), The Debt Burden and its Consequences for Monetary Policy, IEA Conference

Volume No. 118, pp. 3-22.

Eichengreen, Barry, Andrew Rose, and Charles Wyplosz, 1995. Exchange market mayhem: The

Antecedents and aftermath of speculative attacks, Economic Policy, 251-312.

Eichengreen, Barry, Ricardo Hausmann, and Ugo Panizza, 2002. Original Sin: The Pain, the Mystery,

and the Road to Redemption, mimeo.

- 37 -

Flood, Robert, and Peter Garber, 1984. Collapsing exchange rate regimes: Some linear examples

Journal of International Economics, 17, 1 – 13.

Frankel, Jeffrey and Andrew Rose, 1996. Currency crashes in emerging markets: An empirical

treatment, Journal of International Economics 41, 351-366.

Giavazzi, Franceso, and Marco Pagano, 1990. Confidence crises and public debt management, in R.

Dornbusch and M. Draghi (Eds.), Public debt management: Theory and History, 94-124, Cambridge

University Press.

Goldfajn, I. and R. Valdés, 1995. Balance-of-Payments crises and capital flows: the role of liquidity,

(MIT, Cambridge).

Goldstein, Morris, Graciela L. Kaminsky, Carmen M. Reinhart, 1998, Assessing Financial

Vulnerability: An Early Warning System for Emerging Markets, Institute for International Economics,

Washington D.C.

Hamilton, James D., 1994. Time Series Analysis (Princeton)

Herz, Bernhard, 2003, The logic of twin currency and debt crisis, mimeo.

Kaminsky, Graciela L. and Carmen M. Reinhart, 1999. The Twin Crises: The Causes of Banking and

Balance-of-Payments Problems, American Economic Review 89, 473-500.

Krugman, Paul, 1979. A model of balance of payments crises, Journal of Money, Credit, and Banking,

11, 311-325.

Masson, Paul, 1999. Contagion: macroeconomic models with multiple equilibria, Journal of

International Money and Finance 18, 587-602.

Mussa, Michael, 2002, Argentina and the Fund: From Triumph to Tragedy,Policy Analyses in

International Economics 67, Institute of International Economics, Washington D.C.

Obstfeld, Maurice 1994. The logic of currency crises, NBER Working Paper No. 4640.

Paris Club, 2003. http://www.clubdeparis.org/en/index.php.

- 38 -

Reinhart, Carmen, 2002. Default, currency crises and sovereign credit ratings, NBER Working paper

8738.

Rose, Andrew, 2002. One reason countries pay their debts: Renegotiation and International Trade,

NBER Working Paper no. 8853.

Rose, Andrew, and Mark Spiegel 2002. A gravity model of Sovereign Lending: Trade, Default and

Credit, NBER Working Paper no. 9285.

Rossi, Marco (1999). Financial Fragility and Economic Performance in Developing Countries, IMF

Working Paper WP/99/66.

Sy, Amadou, 2003, Rating the Rating Agencies: Anticipating Currency Crises or Debt Crises?,

International Monetary Fund, mimeo.

Sargent, Thomas, and Neil Wallace, 1981. Some unpleasant monetarist arithmetics. Federal Reserve

Bank of Minneapolis Quarterly Review, 1-17.

Velasco, Andres, (1987). Financial Crises and Balance of Payments Crises: A Simple Model of the

Southern Cone Experience. Journal of Development Economics, 27, 263-283.

- 39 -

Figure 1: Interest rate and default rate: Government and market reaction functions

ηM

iTW2 i*

η

i

ηTW

iTW1

- 40 -

Figure 2: Loss functions for currency crisis and twin crisis

LCU

LTW

ir i*

Cη

iTW2

L

i

- 41 -

Figure 3: Loss functions for (self-fulfilling) currency crisis and twin crisis

LCU

LTW

ir i*

Cη

iTW2

L

i

- 42 -

Figure 4: Loss functions for debt crisis and twin crisis

LTW

iTW

Cε

L

i

LDE

ir iDE

Universität Bayreuth Rechts- und Wirtschaftswissenschaftliche Fakultät

Wirtschaftswissenschaftliche Diskussionspapiere 2003 bislang erschienen:

01-03 Albers, Brit S.: Investitionen in die Gesundheit, Humankapitalakkumulation und langfristiges Wirtschaftswachstum

02-03 Schneider, Udo: Asymmetric Information and the Demand for Health Care - the Case of Double Moral Hazard

03-03 Fleischmann, Jochen Oberender, Peter:

Gentests aus gesundheitsökonomischer Sicht

04-03 Bauer, Christian; Herz, Bernhard; Karb, Volker:

Another Twin Crisis: Currency and Debt

05-03 Bauer, Christian; Herz, Bernhard:

Noise Traders and the Volatility of Exchange Rates

06-03 Bauer, Christian; Herz, Bernhard;:

Technical trading and exchange rate regimes: Some empirical evidence

07-03 Bauer, Christian: Products of convex measures: A Fubini theorem

08-03 Schneider, Udo: Kostenfalle Gesundheitswesen? Ökonomische Herausforderung und Perspektiven der Gesundheitssicherung

09-03 Ulrich, Volker: Demographische Effekte auf Ausgaben und Beitragssatz der GKV

10-03 Albers, Brit: Arbeitsangebot und Gesundheit: Eine theoretische Analyse

11-03 Oberender, Peter Zerth, Jürgen:

Die Positivliste aus ökonomischer Sicht: eine ordnungsökonomische Analyse

12-03 Oberender, Peter Rudolf, Thomas:

Das belohnte Geschenk - Monetäre Anreize auf dem Markt für Organtransplantation

13-03 Herz, Bernhard Vogel, Lukas:

Regional Convergence in Central and Eastern Europe: Evidence from a Decade of Transition

14-03 Schröder, Guido: Milton Friedmans wissenschaftstheoretischer Ansatz - über die Methodologie der Ökonomik zu einer Ökonomik der Methodologie

15-03 Fleischmann, Jochen Oberender, Peter Reiß, Christoph:

Gradualismus vs. Schocktherapie oder lokale vs. globale Optimierung als relevante Alternativen der Transformationspolitik? Eine theoretische Analyse.

16-03 Schneider, Udo Erfolgsorientierte Arzthonorierung und asymmetrische Information