the influence of prior industry affiliation on …€¦ · · 2012-02-15strategic management...

TRANSCRIPT

Strategic Management JournalStrat. Mgmt. J., 33: 277–302 (2012)

Published online EarlyView in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.950

Received 25 September 2009; Final revision received 7 July 2011

THE INFLUENCE OF PRIOR INDUSTRY AFFILIATIONON FRAMING IN NASCENT INDUSTRIES: THEEVOLUTION OF DIGITAL CAMERAS†

MARY J. BENNER1* and MARY TRIPSAS2

1 Carlson School of Management, University of Minnesota, Minneapolis, Minnesota,U.S.A.2 Harvard Business School, Boston, Massachusetts, U.S.A.

New industries sparked by technological change are characterized by high uncertainty. In thispaper, we explore how a firm’s conceptualization of products in this context, as reflected byproduct feature choices, is influenced by prior industry affiliation. We study digital camerasintroduced from 1991–2006 by firms from three prior industries. We hypothesize and findthat: (1) prior industry experience shapes a set of shared beliefs that results in similar andconcurrent firm behavior; (2) firms notice and imitate the behaviors of firms from the same priorindustry; and, (3) as firms gain experience with particular features, the influence of prior industrydecreases. This study extends previous research on firm entry into new domains by examiningheterogeneity in firms’ framing and feature-level entry choices. Copyright 2011 John Wiley& Sons, Ltd.

INTRODUCTION

Firms entering a nascent product market face acontext characterized by tremendous ambiguityand uncertainty, particularly when the new mar-ket is sparked by radical technological change.Potential customers have little or no experiencewith products, and their preferences are thereforeunformed and unarticulated. Even basic assump-tions about what the product is and how it shouldbe used are subject to debate. Similarly, from atechnological perspective, uncertainty exists aboutthe rate of performance improvement of the newtechnology, how components of a technologi-cal system will interact, and whether different

Keywords: technological innovation; industry evolution;dominant designs; managerial beliefs; digital photography*Correspondence to: Mary J. Benner, Department of StrategicManagement and Organization, 3-422 Carlson School of Man-agement, University of Minnesota, 321-19th Avenue SouthMin-neapolis, MN 55455, U.S.A. E-mail: [email protected]† The authors are listed alphabetically and contributed equally.

technological variants will work at all. Market andtechnological uncertainty are often compounded bycompetitive uncertainty as firms grapple with shift-ing industry boundaries and the convergence offirms from previously distinct domains. During thisperiod of turbulence, firms experiment with alter-native product configurations, functions, and tech-nologies, with competing alternatives converging,in many cases, on what researchers have labeled adominant design—a standard set of technologiesand interfaces as well as a shared understanding ofwhat performance attributes are important (Utter-back and Abernathy, 1975; Clark, 1985; Andersonand Tushman, 1990; Klepper, 1996).

While this basic pattern of evolution has beenwell established, important gaps in our understand-ing remain. First, prior research on entry in theearly stages of industries has treated entry as adichotomous variable with the focus on predict-ing which firms enter and the timing of their entry(e.g., Klepper and Simons, 2000). We lack a moregranular understanding of the many individual

Copyright 2011 John Wiley & Sons, Ltd.

278 M. J. Benner and M. Tripsas

choices that entry comprises. In particular weknow little about the forces that influence het-erogeneity in entrants’ interpretations of the newproduct market as reflected in product variantsintroduced, specifically at the level of product fea-tures. Firms’ decisions about product features arecritical as they influence consumer adoption anddiffusion, and ultimately whether the new mar-ket emerges (Rindova and Petkova, 2007). Second,while firm heterogeneity is a central tenet in strat-egy research, ‘we lack a clear conceptual modelthat includes an explanation of how this hetero-geneity arises’ (Helfat and Peteraf, 2003: 997). Theconvergence of firms with diverse backgroundsin a new domain could provide an opportunityto explore the origins of heterogeneity, however,existing research has emphasized only the differ-ential capabilities associated with prior industryexperience, showing that firms with related expe-rience are more likely to enter a new industry (Sil-verman, 1999; Klepper and Simons, 2000; Dan-neels, 2002; Helfat and Lieberman, 2002). Theinfluence of heterogeneous beliefs and assumptionsthat result from different prior industry experiencemay also be important, and this terrain remainsrelatively unexplored.

Finally, although a dominant design representsconvergence of both technological (supply-side)and market (demand-side) characteristics (Clark,1985), empirical studies of the emergence of dom-inant designs have focused primarily on the tech-nological dimension. For example, the 23 papersreviewed in Murmann and Frenken’s (2006) recentsynthesis of the literature all assessed the emer-gence of a dominant design in terms of technolo-gies, broadly defined, while the features embodiedin the dominant design were rarely examined. Wetherefore have little understanding of the marketdimension of dominant designs, including both ini-tial variance in product features and eventual con-vergence on a standard set of features. Insight intothis aspect is important for improving our under-standing of how dominant designs emerge, andmore broadly, how industry evolution unfolds.

In this paper, we address these gaps by explor-ing how a firm’s background, represented byits prior industry affiliation, influences its con-ceptualization of a nascent product market, asreflected by the product features it incorporates.A firm’s prior industry experience is likely to mat-ter due to a combination of capabilities, beliefs,and imitative behavior. Existing capabilities might

influence product-level choices in that a firmis likely to introduce products that leverage itscore strengths (Montgomery and Hariharan, 1991;Helfat and Raubitschek, 2000; Sosa, 2011). Giventhe ambiguity associated with a nascent industry,socio-cognitive processes may also play an influ-ential role as managers attempt to make senseof confusing and often conflicting signals (Weick,1990). Perceptions of the emerging market may,thus, be influenced by managerial beliefs derivedfrom a firm’s industry history (Huff, 1982; Porac,Thomas, and Baden-Fuller, 1989; Spender, 1989;Tripsas and Gavetti, 2000). Finally, during periodsof high uncertainty, decision makers often imi-tate the behaviors of other salient firms (Haveman,1993; Haunschild and Miner, 1997; Rao, Greve,and Davis, 2001), and the most salient firms arelikely to be those competing in the same priorindustry. So, how a firm interprets the emergingopportunity and its conceptualization of productsin the nascent domain are likely to be influencedby its prior industry background.

Our empirical context, the emergence of thedigital camera market,1 is an ideal setting foraddressing these issues. First, the emergence ofconsumer digital cameras was characterized byhigh uncertainty and the entry of firms fromthree prior industries—photography, computing,and consumer electronics—enabling a compari-son of the influence of firm background on deci-sions about which features a digital camera shouldinclude. Second, the digital camera market isunique in that technical capabilities were likelynot a primary driver of firms’ choices of whichfeatures to introduce. As we discuss in detail later,although some firms invested in developing propri-etary camera technology, and we control for tech-nical capability using patent data, a well-developedsupply chain gave all firms access to the samecore features, even if they had no internal capabil-ity. This allowed us to study influences of indus-try affiliation apart from technical capabilities onfirms’ choices of features. Finally, although firms’strategic decisions about market position mightinfluence their corresponding choices of features,and there were specific market niches in the digi-tal camera market such as studio and professional

1 Consistent with research on dominant designs, we use as ourunit of analysis a product market, in this case a digital camera,although digital cameras exist in the broader context of digitalimaging.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 279

cameras, we focus specifically on the consumer(mass) market for digital cameras. Thus, we areable to study heterogeneity in choices—and under-lying beliefs—for firms participating in the samemarket segment. We utilize a unique longitudinaldataset that includes the entry date and features ofalmost every camera in the history of the U.S. con-sumer digital camera industry from its inception in1991 through 2006.

We find that prior industry affiliation had a sig-nificant influence on a firm’s initial framing of thenascent product market. Qualitative data indicatethat digital camera product concepts and expecteduses varied systematically, ranging from an analogcamera substitute (photography firms), to a videosystem component (consumer electronics firms), toa personal computer (PC) peripheral (computingfirms) before converging on a product concept thatincluded elements of all three frames. Quantita-tive analysis of the timing of initial product featureintroduction further supports these systematic dif-ferences. Our results suggest that firms from thesame prior industry shared similar beliefs aboutwhat consumers would value as reflected in theirconcurrent introduction of features—firms weresignificantly more likely to introduce a feature,such as optical zoom, to the extent that other firmsfrom the same prior industry entered with the fea-ture in the same year, whereas concurrent entry byfirms from different prior industries had no influ-ence. Firms were also likely to imitate the behaviorof firms from the same prior industry, as opposedto that of firms from different prior industries inintroducing some, but not all features. Finally, wefind that as a firm’s experience with a particularfeature increased, the influence of prior industrydecreased.

Technological change, market uncertainty, andpatterns of industry emergence

Studies of industry evolution following majorchanges in technology2 have documented a con-sistent pattern of progress, falling into three proto-typical stages: an era of ferment, convergence on adominant design, and an era of incremental change(Utterback and Abernathy, 1975; Anderson and

2 Sometimes a radical technology from the perspective of oneindustry may actually be the application of technology that hasbeen incrementally developing over time in a different context(Levinthal, 1998; Tripsas, 2008).

Tushman, 1990; Klepper and Graddy, 1990).3 Highlevels of experimentation by both firms and cus-tomers dominate an era of ferment. For instance,early automobiles utilized a variety of mechanismsfor steering, ranging from a joy-stick-like tiller tosteering wheels; the internal combustion enginecompeted with electric and steam engines; andsome vehicles had three wheels, not four (Aber-nathy, 1978; Basalla, 1988). As Rao (1994: 33)put it, ‘The only point of agreement about theautomobile was that it could not be powered byanimals.’ In addition to technical variation, funda-mental beliefs about what the product is and whatfunctions it should perform vary. A customer’schoice in the era of ferment ‘involves both theformation of concepts with which to understandthe product, and the development of criteria tobe used in evaluation,’ (Clark, 1985: 244). Forinstance, early in the automobile industry’s his-tory, Americans conceived of an automobile as a‘horseless carriage’ whereas ‘the French thought interms of a road locomotive,’ (Langlois and Robert-son, 1989: 366). These different perspectives werereflected in the product design, features, and tech-nologies employed. Similarly, early in the evolu-tion of cochlear implants, alternative visions ofwhat the product should be resulted in completelydifferent performance metrics being valued (Garudand Rappa, 1994).

In some cases the industry coalesces around adominant design, which reflects both technologi-cal convergence—consensus about a set of stan-dard technologies, modules, and interfaces (Utter-back and Abernathy, 1975; Anderson and Tush-man, 1990; Utterback and Suarez, 1993)—as wellas cognitive convergence—a shared understandingof what the product is, how it will be used, andwhich core attributes will have value (Kaplan andTripsas, 2008). The process by which a dominantdesign emerges is a complex combination of eco-nomic, social, political, and cognitive dynamics,and scholars have demonstrated that the technolog-ically superior alternative does not necessarily win(Cusumano, Mylonadis, and Rosenbloom, 1992;Tushman and Rosenkopf, 1992; Utterback, 1994;Suarez, 2004). Although the dominant design rep-resents the core elements of a new product class,

3 These stages are essentially the same as what Utterback andAbernathy (1975) label fluid, transitional and specific stages,and what Klepper and Graddy (1990) label growth, shakeout,and stabilization stages.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

280 M. J. Benner and M. Tripsas

its emergence does not imply that products can nolonger be differentiated. In fact, competition afterthe emergence of a dominant design is often basedon quality, reliability, brand, and new peripheralfeatures (Utterback, 1994).

While this pattern of high variation and eventualconvergence on a dominant design has been docu-mented in a range of industries, our understandingof the sources of initial heterogeneity is limited.Other than the general argument that de novo firmsare an important source of entry and innovativetechnology in many industries (Cooper and Schen-del, 1976; Tushman and Anderson, 1986; Chris-tensen and Bower, 1996; Martin and Mitchell,1998), we lack a good sense of whether and whydifferent firms might introduce systematically dif-ferent product variants in the same nascent mar-ket. Diversifying entrants play an important rolein many new industries, but the focus of mostresearch has been on whether firms enter, whenthey enter, and whether they survive—not on thevariation in product artifacts they introduce (e.g.,Mitchell, 1989, 1991; Carroll et al., 1996; Dow-ell and Swaminathan, 2006). In addition, researchhas assumed that differences stemming from priorindustry affiliation are a result of variation inresources and capabilities. For instance, radio pro-ducers, which had capabilities that were close tothose needed to produce televisions, were morelikely to enter the television receiver industry, toenter early, and to survive (Klepper and Simons,2000). Similarly, of diversifying entrants in theautomobile industry, bicycle and carriage manu-facturers were more likely to survive than enginemanufacturers (Carroll et al., 1996). Much lessconsideration has been given to the possibilitythat prior industry affiliation also reflects sharedbeliefs and a common set of peers that are noticedand potentially imitated. Given that technologicalchange is increasingly resulting in the competi-tive convergence of firms from previously distinctindustries (Brusoni, Jacobides, and Prencipe, 2009)a deeper understanding of the influence of priorindustry affiliation—one that takes into accountboth capabilities and cognition—is needed.

Moreover, empirical studies of the evolutionof new product markets have focused on thetechnological, not market dimension of a domi-nant design. For example, in Christensen, Suarez,and Utterback’s (1998) study of the rigid diskdrive industry, they identify and track four tech-nologies that make up the eventual dominant

design, the: Winchester architecture, under-spindlepancake motor, rotary voice-coil actuator motors,and embedded intelligence interface electronics.The demand-side product features that might beassociated with different assumptions about cus-tomer preferences and use are not considered inthe dominant design measure. Similarly, in Baum,Korn and Kotha’s (1995) study of the facsimiletransmission equipment industry, the ConsultativeCommittee on International Telephone and Tele-graph technical standards for facsimile transmis-sion were used to define the dominant design. Byexamining the market dimension of a dominantdesign, this paper fills an important gap in ourunderstanding of how different actors arrive at acommon interpretation of what a new product cat-egory represents.

The influence of prior industry affiliation onframing of a nascent product market

We next develop a set of hypotheses about howa firm’s prior industry affiliation influences theway managers frame a new product market, basedon a firm’s initial introduction of particular prod-uct features and its ongoing commitment to thosefeatures. In doing so, we explicitly distinguishbetween the influence of shared industry beliefsand the influence of imitative behavior, both con-structs that can result from common industryaffiliation.

Existing research suggests that similar priorexperiences and ongoing interactions give rise toa shared set of beliefs for members of the sameindustry. Huff (1982: 125) proposed the theoret-ical argument that managers of organizations inthe same industry develop ‘shared or interlock-ing metaphors or worldviews’ such as commonbeliefs about customer preferences, the role ofregulation, and future levels of industry demand.In subsequent research, scholars have providedstrong empirical support for the notion of industry-level frames. Spender (1989: 188) identified setsof ‘industry recipes,’ noting that ‘executives adopta way of looking at situations that are widelyshared within their industry.’ Similarly, Poracet al. (1989: 400) articulated a set of shared causalbeliefs held by Scottish knitwear manufacturersconcerning customers, suppliers, retail, and com-petition, noting that ‘over time the mental modelsof competing strategists become similar thereby

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 281

creating ‘group level’ beliefs about the market-place.’ Extending this work, Porac et al. (1995)developed the concept of an ‘industry model,’which represents collective recognition on the partof producers about what fundamental attributesshould be used to categorize competitors andwhich firms belong in which categories.

Industry-level beliefs are important because theyinfluence decision making and action (Levitt andMarch, 1988). In the photolithography industry,firms developed shared, but mistaken, assump-tions about the direction of change in the under-lying technology, and these resulted in erroneousprojections about performance limits by firmsin the industry (Henderson, 1995). Bogner andBarr (2000: 221) proposed that in hypercompet-itive industries, constant, rapid change became thenorm, and this ‘common cognitive framework’ ofindustry members in turn perpetuated the hyper-competitive environment. The manner in whichfirms evaluate acquisition targets has also beenshown to vary depending on industry background(Hitt and Tyler, 1991).

Commonly held perceptions, expectations, andassumptions become particularly salient whenfirms enter a highly uncertain emerging industrythat incorporates novel technologies with noveluses (Benner, 2010). In this context, managerslack concrete data about what consumers value andtherefore must make assumptions about how cus-tomers will use the product and what features willhave merit. The process by which firms with thesame prior industry affiliation may apply commonassumptions is twofold. First, managers may ‘rea-son by analogy,’ transferring beliefs about priorsituations to novel situations that they perceive tobe similar (Gavetti, Levinthal, and Rivkin, 2005).Past experience with similar customers may createcommon expectations about what customers willvalue in a new domain. Second, ongoing inter-action among firms from the same prior industrymay create a forum for direct sharing of infor-mation about the emerging industry since firmsare more likely to pay attention to and inter-act with familiar peers (Ocasio, 1997). A varietyof venues such as industry consortia, standardscommittees, trade associations, and industry con-ferences have been shown to facilitate relation-ships and sharing of information (Lampel, 2001;Rosenkopf, Metiu, and George, 2001). In aggre-gate, these mechanisms may reinforce common

expectations among firms from the same priorindustry.

Thus, firms from the same prior industry arelikely to make similar assessments of which prod-uct features customers will value and are thereforelikely to first introduce a given feature at a similartime. Put differently, we propose that concurrentintroduction of a feature is an indication of sharedbeliefs about the value of that particular feature.

Hypothesis 1: In the nascent stage of an indus-try, the greater the number of other firms fromthe same prior industry that introduce a prod-uct feature during a period (as opposed to firmsfrom a different prior industry) the greater thelikelihood a firm will introduce the product fea-ture in that period.

Neoinstitutional theory holds that firms in thesame industry, subject to similar institutionalforces, are also likely to imitate each other (DiMag-gio and Powell, 1983). Researchers have docu-mented that firms facing similar institutional envi-ronments tend to adopt similar structures andpractices, including, for example, civil servicereforms (Tolbert and Zucker, 1983), multidivi-sional structures (Fligstein, 1985), or naming con-ventions (Glynn and Abzug, 2002). Moreover,firms are more likely to imitate the practices andbehaviors of similar, comparable firms than to imi-tate firms they categorize as distant (Haveman,1993; Haunschild and Miner, 1997; Baum, Li,and Usher, 2000). The tendency for mimetic iso-morphism or imitation is heightened under condi-tions of high uncertainty such as entry into newmarkets (Haveman, 1993; Greve, 1996; Korn andBaum, 1999). Imitation is likely a factor not onlyin decisions about whether to enter new, emerg-ing domains but also in choices about how firmsenter, that is, how they conceptualize the new prod-uct and which features they include. In the highlyuncertain setting of an era of ferment, therefore,firms are likely to imitate the features that havealready been introduced by other firms from thesame industry background.

Hypothesis 2: In the nascent stage of an indus-try, the greater the previous introductions of agiven product feature by other firms from thesame prior industry, the greater the likelihood

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

282 M. J. Benner and M. Tripsas

a firm will imitate them and enter with that fea-ture (as opposed to imitate firms from a differentprior industry).

Thus, Hypothesis 1 suggests that due to sharedbeliefs, firms with the same background are likelyto behave in similar ways, while Hypothesis 2suggests that even absent shared beliefs, firmsare likely to imitate other firms from the sameprior industry, first observing the product attributesintroduced, and then engaging in the same behav-ior in a subsequent period.

Our discussion so far concerns the choices thatfirms make in their initial introductions of prod-uct features when they have limited data and mustrely on prior beliefs or observations of other salientfirms for making decisions. But these influencesmay dissipate over time as firms gain knowledgebased on their own experience. A wide body oforganizational learning research has shown that asthey gain experience in a product market, firmstend to engage in local search, introducing newproduct variants that are similar to previous models(Martin and Mitchell, 1998; Katila, 2002; Katilaand Ahuja, 2002). And in a study of South Koreanfirms in China, Guillen (2002) found that whilefirms imitated other firms from the same homecountry industry in their rate of foreign expan-sion, this effect decreased once a firm had made itsfirst foreign entry. Prior research has also shownthat although decision makers may initially imi-tate other firms in situations of high uncertainty,updated information based on experience can leadto abandoning a particular course of action (Fiskeand Taylor, 1991; Rao et al., 2001). Similarly, inour context, once a firm has introduced productswith particular features, it gains knowledge aboutthe level of demand and has access to informationfrom customers to better understand usage behav-ior. Thus, a firm’s own experience with featuresis likely to play a heightened role in subsequentdecisions about whether to continue to incorporatethose features in its products, and the influenceof prior industry beliefs and peers is likely todecrease.

Hypothesis 3: In the nascent stage of an indus-try, the more experience a firm has with aparticular product feature, the lower the influ-ence of other firms from the same prior indus-try on the firm’s commitment to that productfeature.

DATA AND RESEARCH SETTING

Overview of the digital camera industry

Digital camera technology utilizes semiconductorchips such as charge-coupled devices (CCDs) tocapture and convert light images to binary data,replacing the role of silver halide film in analogcameras. Beyond image capture, digital technol-ogy offers the benefits of transfer, manipulation,and storage of digital images. The first consumerdigital camera in the United States, a noncolorgrayscale, 90,240 pixel4 camera that could store 32images in internal memory, was available in 1991,and by 2003 sales of digital cameras exceededthose of analog cameras.

The emergence of consumer digital cameras pro-vides an ideal context in which to study the dif-ferential effects of prior industry background sincethe majority of the 83 entrants in the United Statesfrom 1991 to 2006 came from three prior indus-tries: photography (25 firms), consumer electronics(19 firms), and computing (25 firms). There wereonly nine de novo start-ups and five diversifyingentrants from unrelated industries (e.g., Mattel andDisney). Firms were classified as follows: if a firmmade analog cameras or film, it was coded as pho-tography, even if it also made other products (e.g.,Canon). Similarly, if a firm produced camcorders,televisons, stereos, or MP3 players, it was codedas consumer electronics (e.g., Sony). Firms thatmade PCs, peripherals, software and/or compo-nents were coded as computing. Table 1 providesa list of entrants’ prior industry classifications.There is clearly variation within our broad industrygroupings, but our approach is conservative in thatthis variation would tend to decrease the likelihoodof finding a prior industry effect. While selectionbias is an issue in some studies of entry, in this caseevery major analog camera, photographic film, andconsumer electronics firm entered the market, lim-iting possible selection issues to computing firmsthat could have entered, but did not (e.g., Dell,Microsoft). However the range of computing firmsthat did enter is reasonably broad, and based on acomparison, we have no reason to believe that thecomputing firms that did not enter differ system-atically from those that did.

The digital camera market is also ideal forstudying the role of prior industry affiliation in

4 Pixels measure the resolution of digital cameras.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 283

Table 1. Prior industry affiliation of firms that enteredthe consumer digital camera market

Photography Consumerelectronics

Computing

Achiever Archos AiptekAgfa Casio AppleArgus Creative DXG BTCCanon Hitachi BenQChinon JVC D-LinkConcord LG Electronics DolphinFuji Photo Mitsubishi Epson

FilmJazz Photo Oregon Scientific Gallant ComputerKodak Panasonic GatewayKonica Philips Hawking TechnologyKyocera RCA Hewlett-PackardLeica Relisys IO MagicMinolta Samsung IntelMinox Sanyo JenimageNikon Sharp KB GearOlympus SiPix LogitechPentax Sony Micro Innovations

Syntax BrillianPolaroid Microtek LabsPraktica MustekPremier NECRicoh SoundvisionRitz Camera Spot TechnologyRollei ToshibaSigma UMAX TechnologiesVivitar Visioneer

shaping perceptions and interpretations in that wecan largely separate decisions about introducingproduct features from the capabilities required toimplement those features. While a subset of firmsinvested in developing technical capability thatallowed them to design and manufacture digitalcameras, firms with no technical expertise couldalso introduce digital cameras by utilizing a well-developed supply chain that had the expertiserequired to develop the features that were eventu-ally standard. For instance, Ritz Camera, a photog-raphy retailer with no product development exper-tise, introduced a consumer digital camera in 1995.‘Digital camera components are readily available,products can be developed fairly quickly and pro-duction (part assembly) can be done relativelyeasily,’ explained a financial analyst who coveredFuji Photo Film (HSBC Chemicals, 2000: 14).In addition, camera manufacturers could choosefrom multiple suppliers for each feature. A MorganStanley analyst report identified nine zoom lenssuppliers, 10 LCD screen suppliers, and 16 image

sensor chip suppliers (the ability to introducehigher megapixels was driven by sensor chips)(Hsu, Ho, and Gupta, 2002). Even componentdevelopers that participated in the digital cameraindustry generally supplied their components toothers. Kodak, an early leader in high-end CCDsensor technology created a separate Image Sen-sor Solutions division to serve as a merchantmarket supplier of both CCD and complementarymetal–oxide–semiconductor(CMOS) sensors, andKodak’s consumer digital cameras mostly incor-porated sensors from other suppliers.

In addition to component suppliers providingaccess to features, a vibrant OEM/ODM industrydeveloped early on providing design, integration,and manufacturing services to firms wishing tointroduce a digital camera. Firms could choosefrom a menu of features available in digital cam-era reference designs developed by original equip-ment manufacturers/original design manufacturers(OEMs/ODMs). Japanese firms such as Chinonwere producing cameras for others as early as1993. Taiwanese firms entered the OEM/ODMindustry in 1997, and by 1999 it was estimated that10 percent of digital cameras worldwide were pro-duced by Taiwanese OEMs/ODMs (Taiwan Eco-nomic News, 1999) rising to 20 percent in 2000(Taiwan Economic News, 2000).

Some firms that entered the digital camera mar-ket did invest in developing technological capa-bility, but these firms were the minority. Of the83 firms that entered the market, 31firms had nopatents in classes related to digital cameras from1983–2003, 20 firms had fewer than 50 patents,and a core set of 20 firms had over 1,000 patents(see Table 2 for a list of patent classes relatedto digital cameras.) One might expect that firmswould be more likely to introduce features thatleverage their technical capabilities, and we testfor this effect in our quantitative analysis, how-ever, qualitative data indicate that even amongthese firms, the timing of a new feature wasnot driven by this technological capability. Forinstance, although Kodak had one of the highestpatenting rates, the president of the digital andapplied imaging unit from 1997–2005 explainedto us in an interview that,

Kodak’s decisions to offer consumer digitalcameras with features such as optical zoom,movie clips, or higher resolution were driven byour perception of what consumers were willing

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

284 M. J. Benner and M. Tripsas

Table 2. Digital camera patent classes included in con-trols for technical capabilities

250 Radiant energy257 Active solid-state devices324 Electricity: measuring and testing327 Miscellaneous active electrical nonlinear

devices, circuits, and systems345 Computer graphics processing, operator

interface processing, and selective visualdisplay systems

348 Television355 Photocopying356 Optics: measuring and testing358 Facsimile and static presentation processing359 Optics: systems (including communications)

and elements360 Dynamic magnetic information storage or

retrieval361 Electricity: electrical systems and devices377 Electrical pulse counters, pulse dividers, or

shift registers: circuits and systems378 X-ray or gamma ray systems or devices382 Image analysis386 Television signal processing for dynamic

recording or reproducing396 Photography428 Stock material or misc articles430 Radiation imagery chemistry: process,

composition, or product thereof438 Semiconductor device manufacturing: process711 Electrical computers and digital processing

systems: memory725 Interactive video distribution systems

to pay for, not by our technical capability todevelop or manufacture the underlying compo-nents (Dr. Willy Shih, in-person interview, 23February, 2009).

By taking advantage of the characteristics ofthis setting, as well as directly controlling fortechnological capabilities in our models, we aretherefore able to better untangle firms’ framingand conceptualizations of the appropriate featuresfor a digital camera from considerations of theirtechnical capabilities in our tests of the influenceof prior industry.

Sources and data

Our dataset includes comprehensive longitudinaldata covering the history of consumer digital imag-ing in the United States from 1991 through 2006.It covers every firm to introduce a branded digital

camera in the United States (private label cam-eras are excluded), and every digital camera intro-duced by these firms from 1991 through 2006.Since we focus on the mass market for digitalcameras, we excluded from our analysis types ofdigital cameras that we determined were distinctproduct markets that would experience their ownseparate processes of variation and convergenceon a dominant design: studio/professional cameras,Webcams, single lens reflex cameras (SLRs), andmobile phone cameras.5

Quantitative data were hand collected from abroad range of primary and secondary industrysources including company and industry associ-ation archives. Detailed information on digitalcamera specifications came from a combinationof trade publications (e.g., Future Image Report,6

PC Photo, and Popular Photography), researchreports (e.g., International Data Corporation andForrester), archived product specifications fromcompany Web sites, archives from photographyindustry Web sites (primarily dpreview.com,imaging-resource.com, and dcviews.com), andpress coverage of the industry throughout the timeperiod. The entry date and specifications for eachcamera were cross-checked and confirmed by atleast two of these sources. In all, our datasetincludes 1,629 digital cameras introduced by 83firms during this period. Quantitative data weresupplemented by extensive field work, includingattendance at multiple industry conferences suchas the annual Photo Marketing Association con-ference, as well as in-person interviews with over50 individuals involved in the industry includingemployees of photography, consumer electronics,and computing firms, as well as outside industryexperts such as the editors of the Future ImageReport.

5 The earliest digital cameras in the mid-1980s were studio andprofessional cameras that resembled scanners, captured up to16 megapixels, were priced in the $16,000 to $20,000 range,and were produced and sold primarily by graphic arts firmsthat did not enter consumer digital photography. Webcams,sometimes called ‘eyeball’ cameras, were tethered to a PCand provided video-conferencing capability over the Internet.Consumer-oriented digital SLRs, while sharing some attributeswith consumer-oriented digital cameras, did not really emergeas a category until 2002, at which point non-SLR cameras werealready beginning to coalesce on a dominant design. Similarly,the first mobile phone cameras were not introduced in the UnitedStates until 2002, largely after our period of study.[0]6 Published 10 times a year by Future Image, Inc. of San Mateo,California, Future Image Report provides news and analysis ofnew technology in the photo-imaging industry.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 285

Emergence of a dominant design in consumerdigital cameras

Consistent with the pattern found in prior researchon technological change (e.g., Utterback, 1994;Anderson and Tushman, 1990), the advent of digi-tal photography triggered rapid innovation, uncer-tainty, and competition among product designs,features, and technical variants, with eventualconvergence on a standard camera—a dominantdesign. To trace the emergence of a dominantdesign for digital cameras, we identified andtracked adoption of a set of key camera features.This approach is unique in that it focuses on themarket dimension in contrast to prior empiricalmeasures, which have focused almost exclusivelyon the technological dimension (e.g., Andersonand Tushman, 1990; Christensen et al., 1998, Sosa,2009). For instance, we examined whether a firmintroduced higher levels of camera resolution, butdid not examine what underlying sensor technol-ogy (CCD or CMOS) firms used to deliver thatresolution. Similarly, we examined whether a firmintroduced a removable memory feature on a cam-era, but not what technical variant of removablememory was included (e.g., Compact Flash ver-sus Microdrive). As suggested by Suarez (2004),we considered a dominant design to have emergedonly when over 50 percent of new models had allof the elements that were included in the design,and that percentage was continuing to increase.

The features we tracked were: liquid crystal dis-play (LCD), optical zoom lens, digital zoom soft-ware, movie clips, resolution, removable storage,and dual Webcam capability. We chose these fea-tures because they were included systematicallyin descriptions of digital cameras in both indus-try trade publications such as the Future ImageReport, and mass market publications such as Con-sumer Reports. Our goal was to capture featuresthat had uncertainty associated with them, so weexcluded features such as ‘color,’ since it seemedcolor would be an obvious choice for firms. Wealso excluded features that diffused rapidly suchas ‘flash,’ since they did not provide enough vari-ation in the timing of firm introduction to allowfor analysis. With the exception of dual Webcamcapability, all features became part of the dominantdesign.

Whether to include most camera features was abinary choice for a firm—either the camera had thefeature or it didn’t. Image resolution, however, is

what Rosenkopf and Tushman (1994) call a dimen-sion of merit. All digital cameras have resolution,so the choice firms faced was whether to incorpo-rate higher levels of resolution. We therefore sortedcameras into resolution categories, enabling us toalso analyze introduction of higher resolution cam-eras as a binary choice. The first category includedcameras with video graphics array (VGA) reso-lution (the 307,200 pixels of a computer screen)or lower. The next category comprised cameraswith higher than VGA resolution, up to and includ-ing 1 megapixel cameras. For higher resolutions,we followed the norm in the industry and cate-gorized models as 2 megapixel (2 million through2.9 million pixels), 3 megapixel, and so on.

Table 3 describes each of these features inmore detail and summarizes when they were firstintroduced and how quickly they were adopted.Figure 1 shows the percentage of new camerasintroduced each year that incorporated each fea-ture. Wide variance in features is evident in theearly years. For instance, in 1997, LCDs wereoffered in 63 percent of new cameras, optical zoomin 17 percent, digital zoom in five percent, movieclips in 12 percent, over VGA resolution in 28percent, removable storage in 70 percent, and dualWebcam capability in 10 percent. Uncertainty isalso evident in that the majority of features expe-rienced both increases and decreases in penetrationover time. By 2006, however, all features, exceptfor dual Webcam capability, were present in almostall new cameras (only 13% of new models haddual Webcam capability.) While individual fea-tures were introduced earlier, the first camera toincorporate all elements of the dominant designwas introduced in 1999, and it was not until 2004that the dominant design was solidified, with over50 percent of new models incorporating all ele-ments. We, therefore, define the nascent stage ofthe market as extending from 1991 through 2003and exclude subsequent years from our quantitativeanalysis.

The role of prior industry affiliation onframing: descriptive analysis

Before turning to a quantitative analysis of theintroduction of features, we first examine descrip-tive data on the initial introduction and subse-quent diffusion of features to identify prelimi-nary patterns that distinguish the influence of priorindustry. While in retrospect the elements of the

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

286 M. J. Benner and M. Tripsas

Table 3. Summary of Digital Camera Features

Feature Description ofmodel features

First year featurewas introduced

/firm(s) thatintroduced it

Year >50%of new

models havefeature

Percent ofmodels

with featurein 2006

Dominant Contains all elements of the dominant 1999 2004 88%design design: LCD, optical zoom, digital

zoom, movie clips, overVGAresolution, and removable storage

Sony, Casio, Toshiba

Optical zoom Incorporates a zoom lens with a 1992 2000 92%range of focal lengths instead of alens with a fixed focal length.

Fuji

Removable Incorporates a slot for memory 1992 1997 97%storage (typically a flash memory card)

that can be removed to transferimages to a PC or printer.

Fuji

Greater than Sensor captures more pixels than the 1995 1998 98%VGA VGA (640x480) resolution of a Kodakresolution computer display

LCD Includes an LCD that allows the user 1995 1997 99%to see an image before taking apicture and preview/selectivelydelete pictures after image capture.

Casio

Movie clips Has the ability to capture and store 1996 2000 98%short video clips. Ricoh

Digital zoom Enables software manipulation of the 1997 1999 95%image within the camera to createa “close-up,” which is a croppedversion of the original image.

Fuji, Epson, Hitachi

Dual webcam Has the ability to switch to a webcam 1997 Never 13%mode, which enables real time Apple, Soundvision, (peak 24% in 2002)streaming video through a PC. UMAX, Ricoh, Vivitar

dominant design may seem obvious, in the momentthere was high uncertainty about how productswould be used and what features would be valued(Munir, 2005; Srinivasan, Haunschild, and Grewal,2007). For example, in 1993, a vice president ofbusiness development from Leaf Systems notedin an interview, ‘the thing about scanning is thatthere already was a perception in the marketplaceof what a scanner was. . .Electronic photographyis quite different’ (Gerard, 1993). Table 4 com-pares the initial introduction and adoption rates offeatures by firms from each prior industry. Thesedescriptive data seem to reflect different interpreta-tions of what a digital camera represented depend-ing upon what industry a firm originated in.

Photography firms

Photography firms appear to have conceived of adigital camera as a device that would be used in a

manner similar to an analog point-and-shoot cam-era, including the printing of images. Indicativeof this mindset, these firms: led the introductionof high resolution, optical zoom, and removablestorage features; were later in their introductionof movie clips; and introduced few models withdual Webcam capability. Although the resolutionof digital cameras ultimately emerged as an impor-tant product feature, early on the perceived valueof exceeding the VGA resolution of a computerscreen depended upon whether members of a firmbelieved that consumers would primarily displayimages on a television or a computer, or whetherthey would also want to print pictures (in whichcase high resolution would be valued). The firstcamera to offer higher than VGA resolution wasintroduced by Kodak in 1995 and by 1996 overhalf of the photography firm models had high

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 287

Figure 1. Percentage of new cameras with feature, by year

resolution (compared with 1998 for consumer elec-tronics and computing firm models). Fuji was thefirst to introduce an optical zoom model in 1992,and by 1998 over half of the photography firmmodels had optical zoom, a feature that was com-mon in analog film point-and-shoot cameras. Incontrast, it wasn’t until 2004 that half of computerfirm models had optical zoom. Removable stor-age enabled users to remove a memory card andtake it to either a digital minilab or a retail kioskfor prints, similar to the behavior of consumersusing analog film cameras. This feature was alsofirst introduced by Fuji in 1992 and by 1995 overhalf of the photography firm models had removablestorage (compared to 1997 for consumer electron-ics and computing firms).

In contrast, photography firms were later tointroduce the movie clips feature, which allowedthe user to capture and store short video clips.As one photography industry executive told usin an interview, ‘Photography firms figured thatif people wanted to take movies, they’d use acamcorder. They didn’t need that feature in acamera.’ It wasn’t until 2001 that half of thephotography firm models had the movie clip fea-ture, compared to 1999 for consumer electronicfirm models. Similarly, the Webcam feature wasalso not perceived as valuable by photographyfirms, and the penetration of that feature peakedat 17 percent of camera models for photographyfirms.

Consumer electronics firms

Consumer electronics firms appear to have con-ceived of a digital camera as a video system com-ponent, and consistent with this vision, they ledthe introduction of LCDs and movie clip featuresand were slower introducing high resolution andremovable storage. LCDs were already a standardfeature of camcorders, and on digital cameras theyallowed the user to preview and selectively deleteimages taken with the camera. LCDs were firstintroduced in 1995 in the QV10 camera intro-duced by Casio. ‘Because it was not a camera orfilm company, Casio was unencumbered by tradi-tional concepts of what a ‘digital camera’ oughtto be,’ noted an industry analyst (Simpson andYeh, 1997). In fact, the original concept for theQV10 was not ‘a digital camera with an LCDscreen, it was to be an LCD television with abuilt-in digital camera’ (Aoshima and Fukushima,1998: 369). The television tuner feature was even-tually taken out as the product concept evolved.By 1996, half of the consumer electronics indus-try models had LCDs (compared with 1997 and1998 for photography and computing firm mod-els). Consumer electronics firms also led the adop-tion of the movie clips feature, reflective of theexpectation that consumers view a digital cameraas similar to a camcorder. Half of their mod-els incorporated the feature by 1999 (comparedwith 2001 for photography and computing firms.)The expectation that consumers would not print is

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

288 M. J. Benner and M. Tripsas

Table 4. Adoption of digital camera features, by prior industry

Feature Photographyindustry firms firms firms

(analog camerasubstitute frame)

Computerindustry(video system

component frame)

Consumerelectronics

(PC-peripheral frame)

Optical zoomFirst year introduced 1998 1996Year >50% new models have attribute 2004 1999

Removable storageFirst year introduced 1997 1996Year >50% new models have attribute 1997 1997

Greater than VGA resolutionFirst year introduced 1995 1996Year >50% new models have attribute 1998 1998

LCDFirst year introduced 1996 1996Year >50% new models have attribute 1997 1998

Movie clipsFirst year introduced 1996 1997Year >50% new models have attribute 2001 2001

Digital zoomFirst year introduced 1997Year >50% new models have attribute 1999

Dual WebcamFirst year introduced 1997 1998Peak adoption 17% in 2001 20% in 2002

19921998

19921995

19951996

19971998

1997200148% in

19971999

19951996

19971998

reflected in the later adoption of the high resolu-tion and removable storage features. One of thedevelopers of Casio’s first digital camera stated,‘It started with a more or less simple idea to feedthe image to a television. In this respect, imagequality similar to a VHS frame [76,200 pixels]was quite acceptable’ (Aoshima and Fukushima,1998:375). Similarly, in 1997 an industry analystnoted, ‘It never occurred to Sony that images froma digital camera would be displayed predominantlyon a computer as opposed to a TV’ (Gerard,1998).

Computer industry firms

Computer industry firms appear to have vieweda digital camera as a PC peripheral, with theexpectation that consumers would either leave theircamera tethered to a PC, or after taking pictures,upload them to a PC for transmission or display.Intel brochures from 1997 were quite explicit,promoting their product as a ‘PC camera.’ Sim-ilarly, the company press release announcing theLogitech Fotoman in 1991 described it as, ‘aportable, ergonomically designed digital camera

for IBM PCs’ (Logitech, 1991). This perceptionwas reflected in the relatively late adoption of highresolution, removable storage, and optical zoomas well as the relatively early adoption of dig-ital zoom and Webcam capability. Digital zoominvolves software manipulation of the image tocreate a ‘close-up,’ which is a cropped version ofthe original image. Over half of computing firmmodels had the feature in 1998 (compared with1999 for photography firms). The dual Webcamfeature enabled a camera to serve as a Webcam anddo real time streaming video through a personalcomputer over the Internet in addition to function-ing as a stand-alone camera. Although almost halfof the models from computer firms had the featurein 2001, for photography and consumer electron-ics firms the percentage of models with the featurepeaked at about 20 percent.

The role of prior industry affiliation onframing: quantitative analysis

The descriptive data suggest that prior industryaffiliation was an important influence on how firms

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 289

conceptualized a digital camera. We next use quan-titative data on the timing of camera feature intro-ductions to more formally test our hypotheses.

MEASURES

Dependent variables

Initial introduction of features

For testing Hypotheses 1 and 2, we used a binarydependent variable that has a value of 1 in thefirst year that a firm introduces a model with agiven product feature (e.g., LCD). The firm isat risk of introducing a feature starting the yearafter a digital camera with that product featurewas first introduced into the industry and endingonce the firm introduces a model, the firm exitsthe digital camera industry, or the time periodunder consideration (through 2003) ends. Since thechoice of features for a firm’s initial digital camerareflects the firm’s framing of the opportunity in thecontext of high uncertainty, we included the firstmodel introduced by a firm in the analysis.

Ongoing commitment to features

To test Hypothesis 3, we used two different depen-dent variables. For all features other than resolu-tion, we measured a firm’s ongoing commitmentto a feature as the number of digital cameras intro-duced by firm i in year t that had a particular fea-ture. The data for these analyses began in the yearfollowing the firm’s initial year of entry into thefeature. For the analyses of the digital camera reso-lution feature, we examined the timing of a firm’sentry into each subsequent megapixel generationfrom 2 megapixels to 6 megapixels, since an ongo-ing commitment to high resolution is indicated bya firm continuing to introduce increasingly higherresolution cameras, (as opposed to more cameraproducts with greater than VGA up to 1 megapixelresolution).

Independent variables

To test Hypothesis 1, that firms from the sameprior industry held shared beliefs, we comparedthe effect of concurrent entry by other firms fromthe same prior industry, and concurrent entry byfirms from a different prior industry , counts of thenumber of other firms with the same and with

different prior industry affiliations that introduceda particular feature in year t . If firms from thesame prior industry have similar beliefs about whatfeatures to incorporate in a camera, then theyshould be more likely to introduce a feature at thesame time, as opposed to at the same time as firmsfrom a different industry.

To test Hypothesis 2, that firms are likely tonotice and imitate firms from the same prior indus-try more than firms from a different prior industry,we compared the effect of cumulative previousentry by firms from the same prior industry andcumulative previous entry by firms from a differentprior industry, counts of the cumulative number ofother firms with the same and with different priorindustry affiliation that have introduced a partic-ular feature as of year t − 1 . For example, forphotography firms such as Nikon or Kodak, wemeasured the cumulative number of other photog-raphy firms that had introduced a camera with afeature (e.g., optical zoom) in prior years and thecumulative number of non-photography firms thathad introduced the feature in prior years.

For testing Hypothesis 3, that firm experiencewith a feature moderates the relationship betweenprior industry affiliation and a firm’s ongoing com-mitment to a feature, we examined the interactionbetween the market presence of firms from thesame prior industry in the feature and a firm’s ownexperience with the feature. Both main effects weremean centered, with mean-centered values used tocompute the interaction. We measured firms fromthe same prior industry present in feature as acount of the number of firms from the same priorindustry that are currently in the market with acamera that has the feature. We measured firmexperience in feature using the cumulative num-ber of models with the feature that the firm hasintroduced as of year t − 1 . If prior industry influ-ence diminishes with experience, the interactionbetween these two measures should be negative.Finally, we also controlled for firms from a differ-ent prior industry present in feature, a count of thenumber of firms from a different prior industry thatare currently in the market with a camera that hasthe feature.

Control variables

We controlled for several other factors that mightaffect the introduction of digital camera features,including a firm’s technological knowledge and

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

290 M. J. Benner and M. Tripsas

related capabilities, which may affect its intro-duction of particular features. Therefore, we con-trolled for technical capability using a cumulativecount of granted digital camera patents, coded byapplication date, starting in 1983. We obtainedpatent data from the National Bureau of Eco-nomic Research patent database (Hall, Jaffe, andTrajtenberg, 2001). Since the technologies usedin a digital camera are categorized in multiplepatent classes, we generated a comprehensive listof classes by searching the United States Patentand Trademark Office database for patent titles andabstracts related to each digital camera feature andrecording the classes. A list of the patent classesincluded for all features is shown in Table 2. Weused the log of patent counts (adding one beforelogging) in our models.

A firm’s commitment to and participation inthe broader digital imaging industry may influ-ence introduction of features, so we controlled forthe breadth of a firm’s digital imaging offerings,a time-varying measure calculated as the numberof digital imaging product categories in which afirm participates in a given year, including photoprinters, photo finishing/sharing Web sites, photoediting software, desktop scanners, and removablememory cards. Participation in closely related mar-kets may also influence feature introduction, so weincluded controls for whether a firm is present inthe Webcam, camcorder, and digital SLR marketsin year t. Each of these variables was set to 1 if thefirm was in that market in the current year. A Web-cam was defined as a device that is tethered to aPC and, with appropriate PC software, enables livevideo/audio streaming—videoconferencing. MostWebcams can also capture still images, which arestored on the PC. A camcorder was defined aseither an analog or a digital device that has aprimary function to capture video. A digital SLRcamera was defined as a device that has exchange-able lenses and through-the-lens viewing.

Firms that have more digital camera modelsavailable in the consumer market may have ahigher likelihood of introducing a feature simplybecause they offer more cameras. We thereforecontrolled for firm models on the market in year tusing a count of the number of digital cameras thatthe firm has on the market in the year. Since largerfirms may have the resources to experiment in abroader range, we controlled for firm size, mea-sured as sales at the corporate level. The firm sizedistribution is skewed, so we took the log of sales.

For public firms, data was obtained from Compu-stat. For private firms, data came from a combi-nation of Wards, Dun & Bradstreet, OneSource,and trade press articles in which the firm disclosedsales figures. Missing years for private firms wereinterpolated based on the years for which data wasavailable. Nine firms had no publicly availablesales data, but based on press releases and infor-mation about number of employees, these firmswere all classified as having sales of less than$10M. The firm size variable was constructed in$10M increments, so for firms with sales less than$10M, firm size = 1, $10–$20M, firm size = 2,$20–$30M, firm size = 3 and so forth. We con-trolled for whether a firm is public with a dummyvariable that equals 1 if it is publicly traded in thecurrent year. Finally, non-US is a dummy variableset to one if a firm has its headquarters outside ofthe United States.

Models

To test Hypotheses 1 and 2 concerning the influ-ence of prior industry background on the initialintroduction of product features, we used eventhistory analysis, specifically a Cox ProportionalHazard model. Event history models analyze thelength of time it takes for a specific event to occur.In our case, the event is a firm’s initial entry with aparticular camera feature. The hazard function canbe interpreted as the likelihood that a firm intro-duces a particular feature at time t . A Cox modelis advantageous because it does not make assump-tions about the particular shape of the underlyinghazard function. This method is appropriate for ouranalysis, since there is no theory to suggest anyspecific underlying functional form for the hazardof a firm introducing a new product feature duringthe advent of a new industry. In a Cox model, thehazard rate is a function of the unspecified baselinerate and the exponential of a vector of covariates,as represented by the following equation:

r(t) = h(t) exp(βX) (1)

where h(t) is the baseline hazard rate and βX rep-resents the influence of the vector of covariates.We split the data into annual spells to allow fortime-varying covariates and used robust standarderrors clustered by firm to account for interdepen-dence between observations from the same firm.We ran separate models for each feature since,

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 291

while we hypothesize that the effect of the vari-ables of interest will be in the same direction, wehave no reason to believe that the magnitude ofthe coefficients will be the same for all features.We ran the models using stcox in STATA.

To test Hypothesis 3, assessing whether firmexperience with a feature diminishes the influenceof prior industry, we used a negative binomialspecification. Our dependent variable for this anal-ysis is a count of camera models with a featureintroduced by firm i in year t . Models with countmeasures as dependent variables may be mis-specified if estimated with ordinary least squaresregression (King, 1988) and are more appropriatelymodeled with a Poisson specification. However,Poisson models rely on the strong assumption of aPoisson distribution, which requires that the meanand variance be equal. Overdispersion, when thevariance is not equal to the mean, violates thePoisson assumption (Cameron and Trivedi, 1990).Overdispersion can occur if the probability of laterevents exceeds that of earlier events, suggestingcontagion or diffusion. This situation is particu-larly likely in our setting with the growth in adop-tion of specific digital camera product attributesand technologies over time. To correct for overdis-persion, we employed a negative binomial model,which relaxes the assumption of equal mean andvariance and includes an error term to captureoverdispersion.

We used a panel data negative binomial specifi-cation with random effects (e.g., Guo, 1996), (thextnbreg command with the random effects optionin STATA). A random effects specification con-siders both between-firm as well as within-firmvariation, thus accounting for the nonindependenceof multiple observations for each firm and provid-ing robust standard errors. Results were similar formodels with and without random effects.

The panel negative binomial models are repre-sented by the following equation, modeled as thelogarithm of the mean count λit:

log λit = Xit β + σεi + µi (2)

alternatively, Pr (yit = r) = (λr ελ)/r!; where yit

is the observed count and r is an integer; X isa vector of characteristics of firm i at time t , σ isa correction for overdispersion, and µi is a time-invariant firm i effect, which in our model is treatedas a random effect.

For testing Hypothesis 3 in the context of cam-era resolution, we used a multiple event hazardmodel in which we examined a firm’s initial entryinto subsequent megapixel generations (using thestcox procedure in STATA). Following Wei, Lin,and Weissfeld (1989), we combined all megapixelgenerations (2–6 megapixels) into one model,such that a firm is at risk of entering eachmegapixel generation and can have multiple entryevents—one for each generation. We stratifiedthe data on megapixel generation, thus allowingeach generation to have its own baseline hazardfunction. We also clustered on firm and used robuststandard errors to control for the lack of indepen-dence of observations.

RESULTS

Table 5 shows the descriptive statistics broken outby each feature analyzed.

Table 6 displays the results of the hazard rateanalysis to test Hypotheses 1 and 2, examininghow a firm’s initial introduction of digital camerafeatures in the market was influenced by the firm’sindustry background.7 In support of Hypothesis1, concurrent entry by other firms from the sameprior industry was significantly associated with thelikelihood of entry for all features except higherthan VGA resolution. For each additional firmfrom the same prior industry that introduced aproduct with a particular feature during the year,the likelihood of a firm introducing that featureincreased, ranging from a 22 percent increase foran LCD (Model 1) to an 87 increase increase forthe dual Webcam feature (Model 7). In contrast,concurrent entry by firms from a different priorindustry did not have a significant effect on theintroduction of any features, and its coefficientwas significantly different from that of concurrententry by other firms from the same prior industryexcept for resolution. For the resolution feature(Model 4), the lack of significance may indicatethat uncertainty surrounding the desirability ofgreater resolution was not actually high. If thenotion that ‘more is better’ was widely sharedthroughout the industry, then the introduction of

7 We ran separate models to test Hypotheses1 and 2, and theresults were the same as when we ran one model with bothindependent variables of interest, so we have included only themodels with both independent variables in Table 4.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

292 M. J. Benner and M. Tripsas

Tabl

e5.

Des

crip

tive

stat

istic

s

Fea

ture

LC

DO

ptic

alzo

omD

igit

alzo

omO

ver

VG

Are

sM

ovie

clip

sR

emov

stor

age

Dua

lW

ebca

m

Var

iabl

esM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SD

Firm

entr

yin

tofe

atur

e0.

141

0.34

90.

107

0.31

00.

127

0.33

40.

138

0.34

60.

153

0.36

00.

164

0.37

10.

090

0.28

7Fi

rmex

peri

ence

infe

atur

e3.

912

7.75

12.

223

5.56

42.

542

6.03

01.

850

3.27

01.

884

4.46

64.

079

7.80

30.

585

1.60

9C

oncu

rren

ten

try,

sam

epr

ior

indu

stry

2.11

02.

647

1.67

21.

164

2.14

12.

169

2.03

11.

240

2.49

71.

922

2.34

52.

043

1.48

01.

345

Con

curr

ent

entr

y,di

ff.

prio

rin

dust

ry4.

621

4.10

23.

398

2.08

24.

768

3.90

64.

605

1.87

35.

729

3.34

25.

517

3.62

63.

712

2.57

2C

umul

ativ

epr

ev.

entr

y,sa

me

prio

rin

d.9.

249

6.42

47.

339

5.98

06.

444

6.42

49.

124

6.36

37.

308

6.68

011

.429

6.81

14.

153

4.30

3C

umul

ativ

epr

ev.

entr

y,di

ff.

prio

rin

d.17

.345

10.4

8614

.028

9.18

212

.009

10.3

7017

.917

11.7

7615

.581

14.0

4423

.205

13.4

639.

316

8.86

9Fi

rms

from

sam

epr

ior

indu

stry

w/f

eat

9.38

45.

570

7.12

14.

681

7.32

25.

797

7.68

14.

101

7.57

35.

933

10.3

285.

194

4.08

53.

331

Firm

sfr

omdi

ffer

ent

prio

rin

d.w

/fea

t17

.695

9.19

112

.876

6.90

914

.130

10.2

1315

.325

7.46

716

.282

12.3

4220

.655

9.59

29.

845

7.83

6

Con

trol

sM

ean

SD

Firm

size

(log

)5.

054

2.85

8N

on-U

.S.

HQ

0.68

60.

465

Firm

mod

els

onm

arke

t5.

347

5.80

3Pu

blic

0.72

00.

449

InW

ebca

ms

0.15

30.

360

Inca

mco

rder

s0.

246

0.43

1In

SLR

s0.

161

0.36

8B

read

thof

digi

tal

imag

ing

offe

ring

s1.

158

1.22

7Te

chni

cal

capa

bilit

y(l

npa

tent

s)3.

882

2.26

9

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

Prior Industry and Framing in Nascent Industries 293

higher resolution cameras would not be influencedmore by prior industry peers. Overall, a firm wasmore likely to introduce a feature at a given timeif other firms from the same prior industry werealso introducing it (as opposed to firms from adifferent prior industry), reflecting stronger sharedbeliefs among firms with similar backgrounds thanamong all firms entering the new market.

Hypothesis 2, that firms will imitate other firmsfrom the same prior industry was supported forthree features: LCDs, digital zoom, and high reso-lution. As seen in Models 1, 3, and 4 of Table 6,cumulative previous entry by firms from the sameprior industry had a positive and significant coef-ficient whereas the coefficient on cumulative previ-ous entry by firms from a different industry was notsignificant. The strongest impact was for the digi-tal zoom feature; for each additional firm from thesame prior industry that had previously introduceda digital zoom camera, a firm was 17 percent morelikely to introduce a camera with the feature. Forother features, however, imitation of firms from thesame prior industry was not evident; and, for themovie clips feature, it appears that firms imitatedfirms from other prior industries. While imitationhas proven to be a powerful force in other set-tings, at the level of introducing product features,the results are mixed. It appears in this settingthat shared beliefs from prior industry affiliation,reflected by concurrent entry, had a stronger andmore consistent influence than mimetic behavior.

Technical capability, which we controlled forwith a cumulative count of digital imaging patents,did not have a significant effect on the timingof firm entry into particular features, and includ-ing these controls did not alter our core results.As a robustness check, we also ran models withfeature-specific technical capability measures thatwere created using a smaller, focused set of patentclasses for each feature and the results weresimilar.

Controls for experience with other imaging-related products had a significant effect in somecases. Not surprisingly, a firm’s presence in dedi-cated Webcams was a positive and significant fac-tor that more than tripled the likelihood that a firmwould introduce a camera with Webcam capabil-ity. Presence in the Webcam market significantlydecreased the likelihood of introducing an LCD,optical zoom, digital zoom, and removable stor-age. Since Webcams had no LCDs, zoom lensesor removable storage, firms present in this market

may have had a diminished belief in the value ofthese features.

Other firm controls had the expected effects foralmost all seven product features. With the excep-tion of the optical zoom feature, the more digitalcameras a firm had on the market in a given year,the more likely it was to introduce a camera witha particular feature. Firm size had a significanteffect on introduction of two features, and whetherheadquarters are outside the United States had asignificant effect on only one feature. Whether afirm is public had no effect on entry into anyfeatures. Exclusion of these variables from themodels does not change the primary results. A like-lihood ratio test comparing models that incorpo-rated only control variables with models reportedin Table 6 showed a significant improvement in fit,and coefficients on the control variables were con-sistent across models. (These results are not shownfor space considerations.)

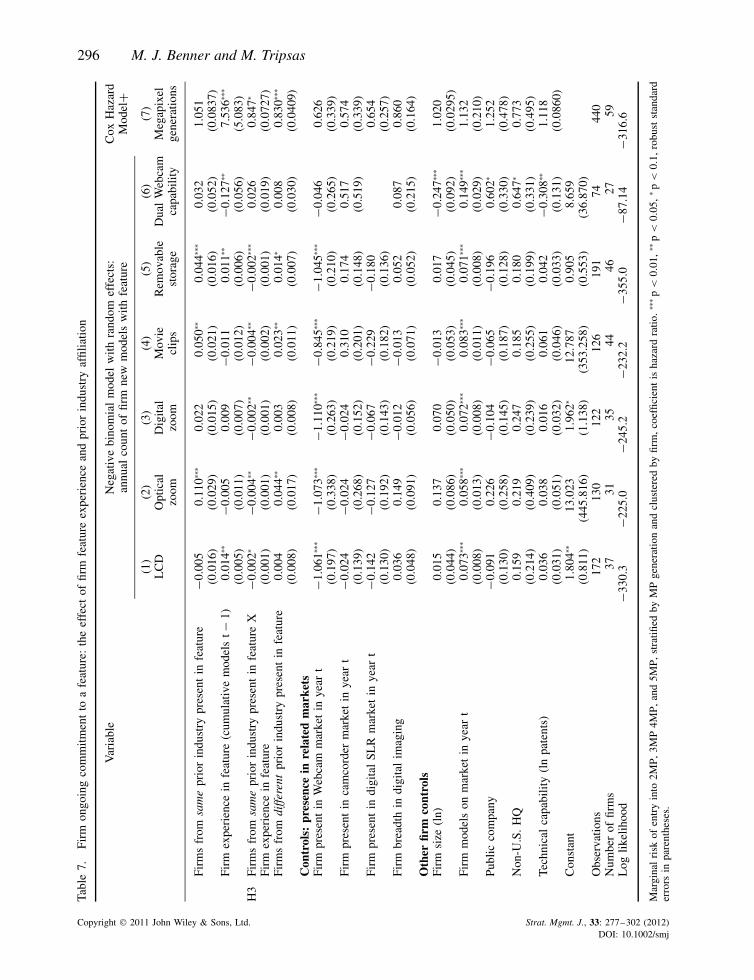

Table 7 shows the results of analyses using neg-ative binomial count models to test Hypothesis 3,assessing whether firm experience with a featurediminishes the influence of prior industry on thecontinued introduction of models with specific dig-ital camera features.

Models 1–5 in Table 7 show strong support forHypothesis 3. For the optical zoom, digital zoom,movie clips, and removable storage features, theeffect of other firms from the same prior indus-try being present in a feature diminished as afirm gained experience with the feature as indi-cated by the negative and significant coefficienton the interaction term (between firms from sameprior industry present in feature and firm featureexperience), and for LCDs the interaction effectwas marginally significant. For instance, for theoptical zoom feature, the marginal effect of onemore firm from the same prior industry presentin the market was to increase a firm’s count ofoptical zoom cameras by 13.8 percent if the firmhad previously introduced only one product withoptical zoom, but if the firm had introduced 10products with optical zoom, the marginal effectof one more peer firm decreased to 9.4 percent.Similarly, for movie clips, the marginal effect ofan additional firm from the same prior industrywent from a 7.8 percent increase to a 3.7 percentincrease in movie clip cameras when a firm’sexperience with movie clips increased from oneto 10 products. Once a firm gains its own expe-rience with a product feature, beliefs based on

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 277–302 (2012)DOI: 10.1002/smj

294 M. J. Benner and M. Tripsas

Tabl

e6.

The

influ

ence

ofpr

ior

indu

stry

shar

edbe

liefs

and

imita

tion

onin

trod

uctio

nof

digi

tal

cam

era

feat

ures

,C

oxH

azar

dm

odel

CO

EFF

ICIE

NT

(1)

(2)

(3)

(4)

(5)

(6)

(7)

LC

DO

ptic

alzo

omD

igita

lzo

omO

ver

VG

Are

solu

tion

Mov

iecl

ips

Rem

ovab

lest

orag

eD

ual

Web

cam

capa

bilit

y

H1

Shar

edbe

liefs

:co

ncur

rent

entr

yby

othe

r1.

224∗∗

∗1.

674∗∗

∗1.

340∗∗

∗1.

232

1.44

9∗∗∗

1.29

7∗∗∗

1.87

4∗∗∗

firm

sfr

omsa

me

prio

rin

dust

ry(0

.065

3)(0

.281

)(0

.098

4)(0

.171

)(0

.152

)(0

.087

2)(0

.307

)C

oncu

rren

ten

try

byfir

ms

from

a0.

986

0.97

61.

036

0.89

81.

031

0.99

71.

088

diff

eren

tpr

ior

indu

stry

(0.0

414)

(0.1

23)

(0.0

510)

(0.0

986)

(0.0

694)

(0.0

407)

(0.1

78)

H2

Imita

tion:

cum

ulat

ive

prev

ious

entr

yby

1.09

4∗∗1.

077

1.16

6∗∗∗

1.11

9∗∗0.

915

1.00

71.

032

firm

sfr

omth

esa

me

prio

rin

dust

ry(0

.045

0)(0

.054

2)(0

.043

5)(0

.059

5)(0

.058

9)(0

.032

4)(0

.090

9)C

umul

ativ

epr

evio

usen

try

byfir

ms

1.02

10.

983

1.02

60.

982

1.08

3∗∗∗

1.01

71.

026

From

adi

ffer

ent

prio

rin

dust

ry(0

.019

7)(0

.031

1)(0

.024

6)(0

.020

2)(0

.030

3)(0

.016

6)(0

.043

5)

Con

trol

s:pr

esen

cein

rela

ted

mar

kets

Firm

pres

ent

inW

ebca

mm

arke

tin

year

t0.

385∗∗

∗0.

181∗∗

0.23

6∗∗0.

978

0.65

70.

270∗∗

∗2.

932∗∗

∗

(0.1

42)

(0.1

39)

(0.1

51)

(0.3

06)

(0.2

37)

(0.0

904)

(1.1

90)

Firm

pres

ent

inca

mco

rder

mar

ket

inye

art

1.33

51.

967

1.06

81.

823

1.25

22.

140∗

0.95

9(0

.634

)(1

.139

)(0

.555

)(0

.706

)(0

.417

)(0

.912

)(0

.810

)Fi

rmpr

esen

tin

digi

tal

SLR

mar

ket

inye

art

0.40

20.

332

0.36

9∗0.

176∗∗

∗0.

270∗∗

0.64

10.

149∗∗

(0.2

35)

(0.2

54)

(0.2

17)

(0.1

09)

(0.1

80)

(0.2

56)

(0.1

28)

Bre

adth

inot

her

digi

tal

imag

ing

prod

ucts

1.29

90.

925

1.25

71.

432∗

0.97

41.

247∗

0.84

2(0

.245

)(0

.213

)(0

.298

)(0

.266

)(0

.125

)(0

.148

)(0

.215

)

Oth

erfir

mco

ntro

lsFi

rmm

odel

son

mar

ket

inye

art

1.18

3∗∗∗

1.07

41.

142∗∗

∗1.

359∗∗

∗1.

137∗∗

∗1.

293∗∗

∗1.

099∗∗

(0.0

623)

(0.0

803)

(0.0

504)

(0.0

615)

(0.0

385)

(0.0

503)

(0.0

467)

Firm

size

(ln)

1.26

6∗∗1.

297

1.41

6∗∗0.

972

1.03

51.

085

0.87

9(0