the indian economy and icici bank - cafral is a global ... · pdf filesteep drop in global...

TRANSCRIPT

Restructuring Preserving and enhancing economic value

Mr. K M Jayarao

Senior General Manager

Risk Management Group

April 19, 2012

2

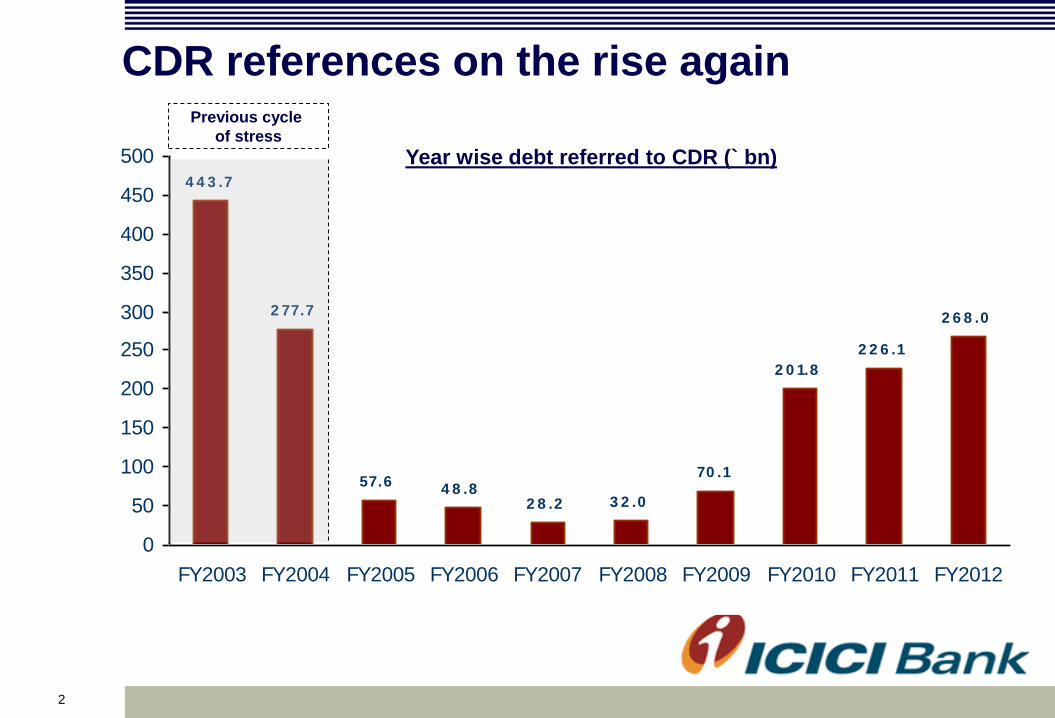

CDR references on the rise again

4 4 3 .7

2 77.7

57.64 8 .8

2 8 .2

70 .1

2 0 1.8

2 2 6 .1

2 6 8 .0

3 2 .0

0

50

100

150

200

250

300

350

400

450

500

FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012

Year wise debt referred to CDR (` bn)

Previous cycle

of stress

3

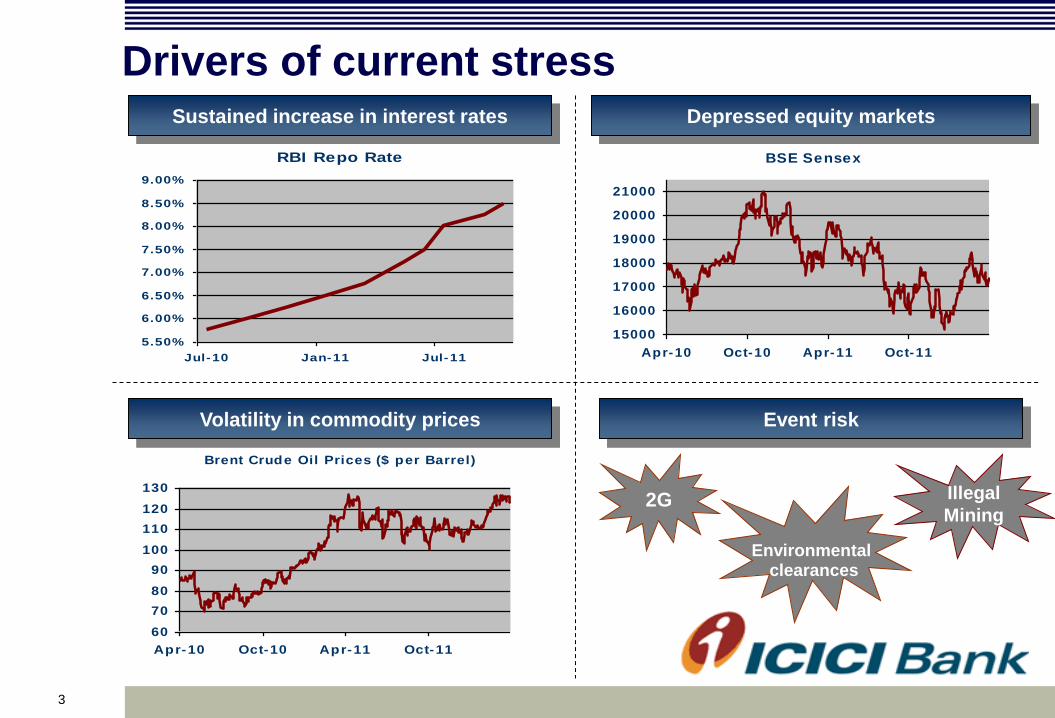

Drivers of current stress

RBI Repo Rate

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

Jul-10 Jan-11 Jul-11

BSE Sensex

15000

16000

17000

18000

19000

20000

21000

Apr-10 Oct-10 Apr-11 Oct-11

Brent Crude Oil Prices ($ per Barrel)

60

70

80

90

100

110

120

130

Apr-10 Oct-10 Apr-11 Oct-11

Sustained increase in interest rates Depressed equity markets

Volatility in commodity prices Event risk

2G Illegal

Mining

Environmental clearances

4

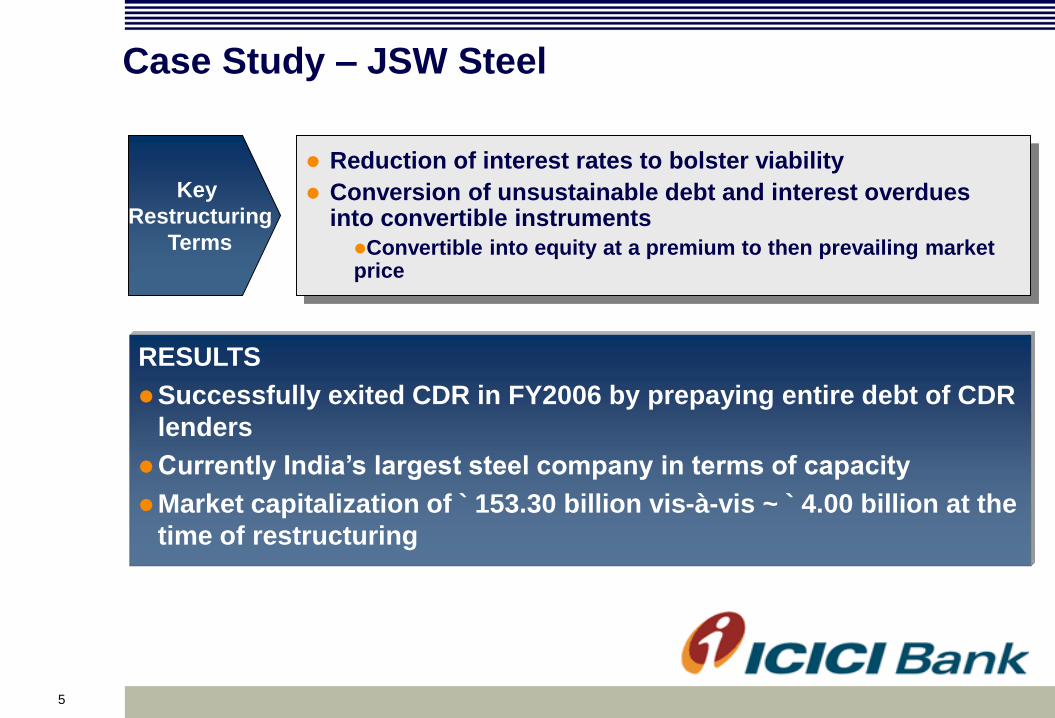

Case Study – JSW Steel

Time and cost overrun due to accident at site due to heavy rains

Inability of promoters to tie-up funds due to overrun

Steep drop in global steel prices due to prevailing overcapacity Problems

Long term viability of steel industry was intact

Willingness of promoters to share upside with lenders and adhere to stringent terms

Including pledge of 100% of shareholding with lenders

Promoter commitment - write down of equity by 40%

Lenders willingness to provide last mile funding to meet cost overrun and WC support post restructuring, subject to current ratio of 1.0

Key

Enablers

5

Case Study – JSW Steel

Reduction of interest rates to bolster viability

Conversion of unsustainable debt and interest overdues into convertible instruments

Convertible into equity at a premium to then prevailing market price

Key

Restructuring

Terms

RESULTS

Successfully exited CDR in FY2006 by prepaying entire debt of CDR

lenders

Currently India’s largest steel company in terms of capacity

Market capitalization of ` 153.30 billion vis-à-vis ~ ` 4.00 billion at the

time of restructuring

6

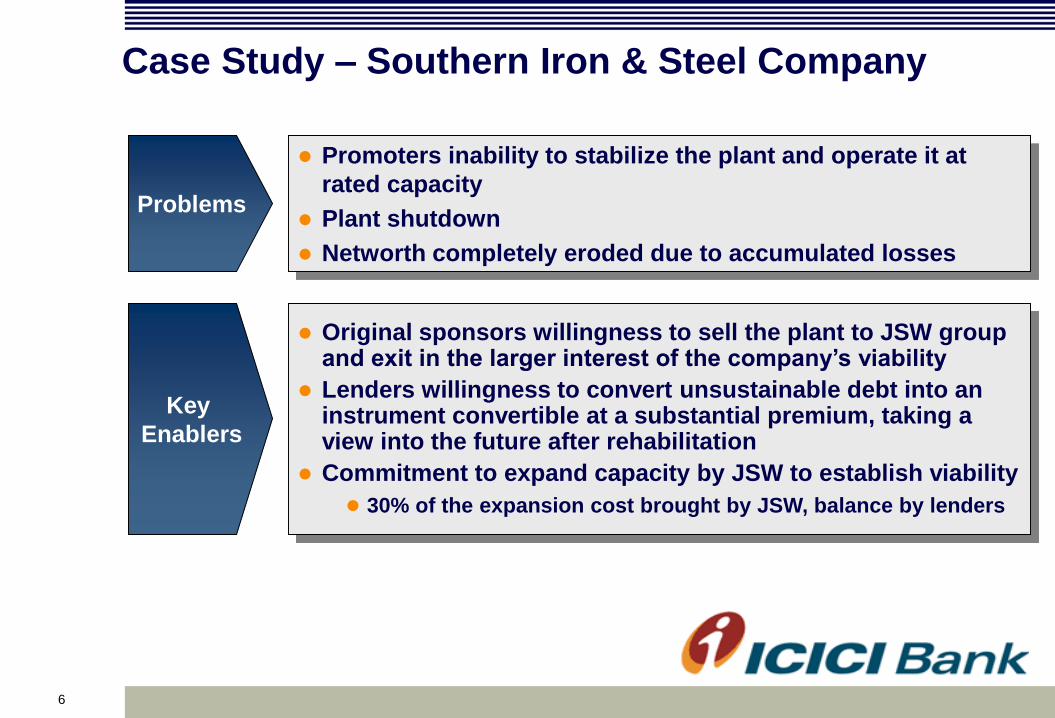

Original sponsors willingness to sell the plant to JSW group and exit in the larger interest of the company’s viability

Lenders willingness to convert unsustainable debt into an instrument convertible at a substantial premium, taking a view into the future after rehabilitation

Commitment to expand capacity by JSW to establish viability

30% of the expansion cost brought by JSW, balance by lenders

Case Study – Southern Iron & Steel Company

Promoters inability to stabilize the plant and operate it at

rated capacity

Plant shutdown

Networth completely eroded due to accumulated losses

Problems

Key

Enablers

7

Case Study – Southern Iron & Steel Company

Lenders facilitated transfer of management control to JSW Group

Conversion of unsustainable debt into Optionally Convertible Loan (OCL), convertible at a premium

Convertible at the option of both Issuer / Subscriber

Key

Restructuring

Terms

RESULTS

Capacity expansion successfully completed, Company merged with

JSW Steel in FY2008

Lenders were able to recoup sacrifice due to upside accrued from

OCL/equity

8

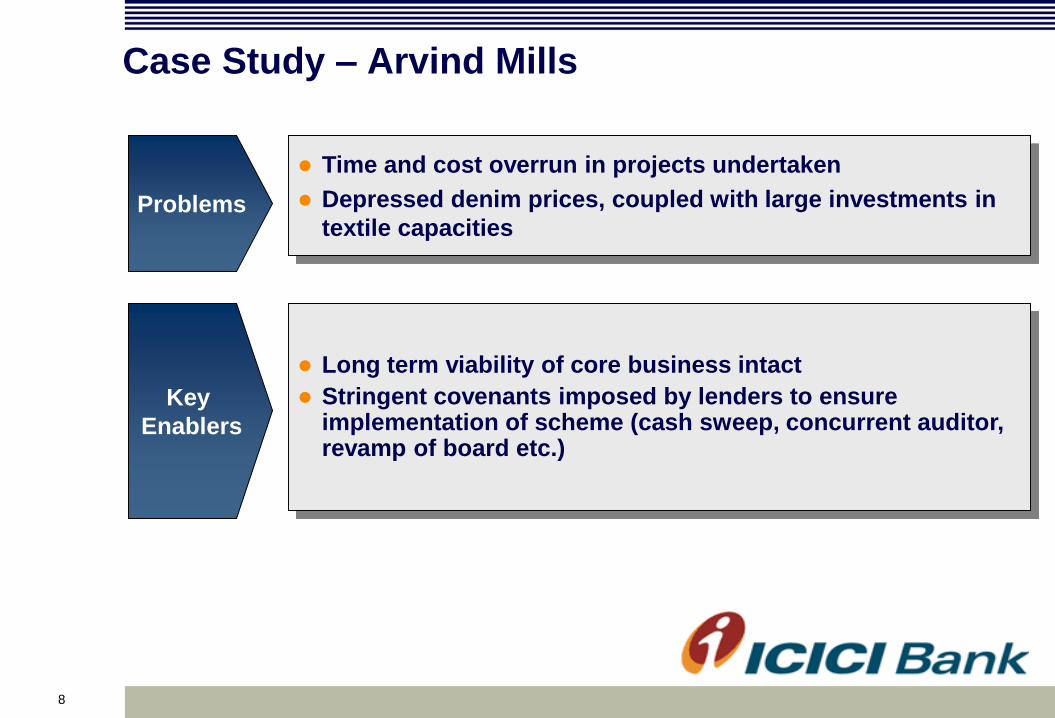

Case Study – Arvind Mills

Time and cost overrun in projects undertaken

Depressed denim prices, coupled with large investments in

textile capacities Problems

Long term viability of core business intact

Stringent covenants imposed by lenders to ensure implementation of scheme (cash sweep, concurrent auditor, revamp of board etc.)

Key

Enablers

9

Case Study – Arvind Mills

Buyback of debt aggregating over ` 8.60 billion at a discount of ~55%

Funded by sale of non core assets, rights issue and new debt

Rationalisation of repayment and interest stream for balance debt

Key

Restructuring

Terms

RESULTS

Successfully completed restructuring of debt involving over 90

lenders (including foreign banks)

Debt burden reduced by over ` 8.00 billion post buyback

10

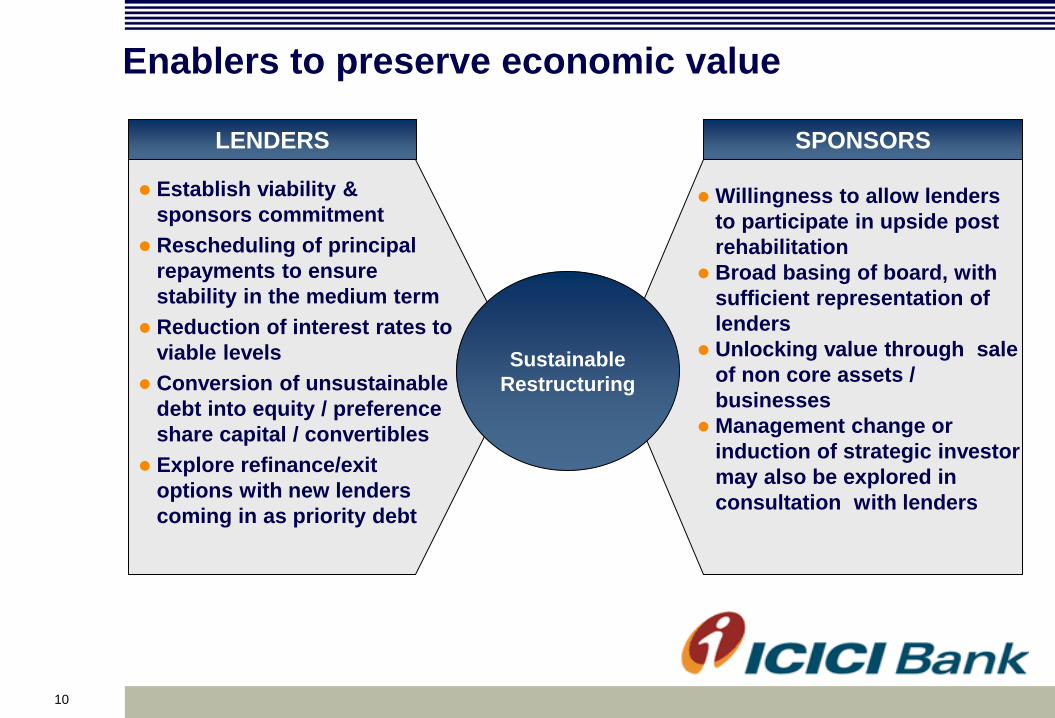

Enablers to preserve economic value

LENDERS

Establish viability &

sponsors commitment

Rescheduling of principal

repayments to ensure

stability in the medium term

Reduction of interest rates to

viable levels

Conversion of unsustainable

debt into equity / preference

share capital / convertibles

Explore refinance/exit

options with new lenders

coming in as priority debt

Willingness to allow lenders

to participate in upside post

rehabilitation

Broad basing of board, with

sufficient representation of

lenders

Unlocking value through sale

of non core assets /

businesses

Management change or

induction of strategic investor

may also be explored in

consultation with lenders

Sustainable

Restructuring

SPONSORS

11

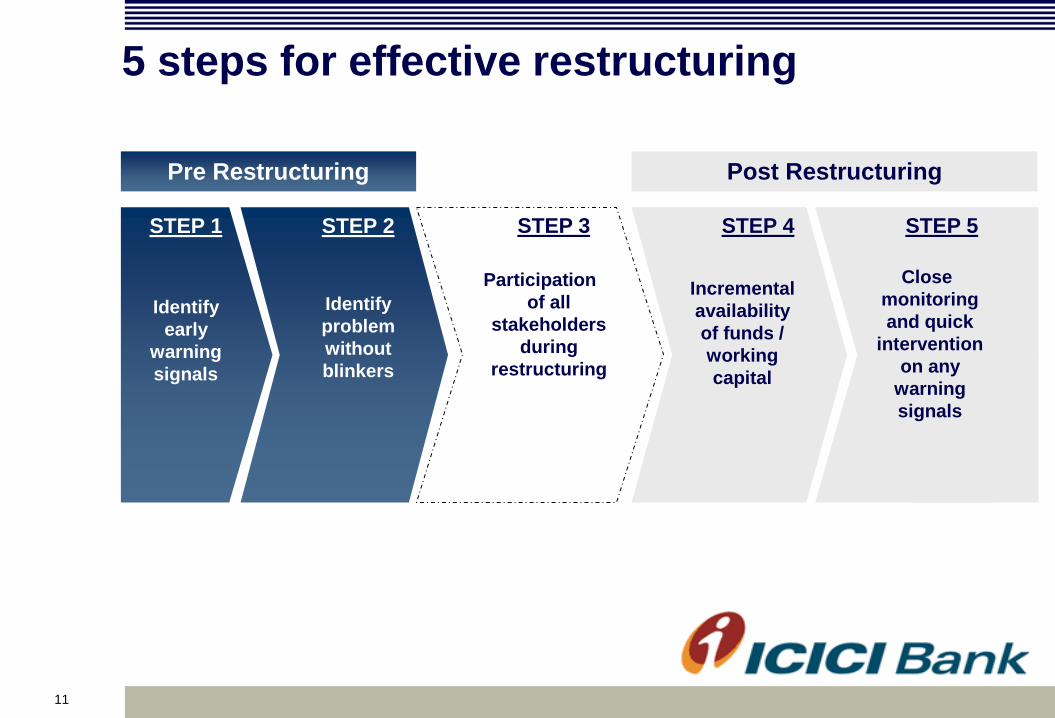

5 steps for effective restructuring

STEP 1

Identify

early

warning

signals

STEP 2

Identify

problem

without

blinkers

STEP 3

Participation

of all

stakeholders

during

restructuring

STEP 4

Incremental

availability

of funds /

working

capital

STEP 5

Close

monitoring

and quick

intervention

on any

warning

signals

Pre Restructuring Post Restructuring

12

To judge the success of a restructuring it is important to judge the performance of companies across the industry cycle post

restructuring…………

13

Thank you