the indian automotive sector - indiaitaly.com · produced in 2003-04 to 14 million in 2009-10, ......

TRANSCRIPT

Automotive38

The Indian automotive manufacturing industry, along with the service sector, has been one of

the crucial drivers of India’s recent economic growth.In spite of the industry being one of the most advanced in India it liberated itself from the limitations of closed economy, insufficient supply, outdated models and limited number of players, which lasted upto the end of ‘80s.The first turning point occurred, in 1981, when the Government of India (GoI) opened up the possibility of foreign investments and signed a JV with Suzuki to form Maruti Udyog. After this, the liberal reforms of the ‘90s further opened up the sector, which was de-licensed, where major Original Equipments Manufacturers (OEM) started assembling in India and imports began to

be allowed. By the new millennium, the number of players had grown to 36 companies. The country’s low manufacturing costs due to economies of scale and low R&D, its proximity to fast growing Asian and African markets and the cost-effectiveness of shipping from India to Europe constitute the fundamental advantages of the industry. The figures related to the recent history are clear: the production of vehicles has almost doubled, from 7.2 million units produced in 2003-04 to 14 million in 2009-10, from 6.8 million units sold to 12.3 million in 2009-2010, at an annual growth rate of 10% (table 1 and 2). The Foreign Direct Investments (FDI) inflow in 2009–2010 for the auto components sector was recorded at US$ 1.2 million, equal to 4% of the total FDI inflow in the country.

The great dynamism of the industry has also allowed the constitution of several automotive and auto-component clusters throughout the country (Map 1): in the North (Delhi-Gurgaon-Faridabad), West (Mumbai-Pune-Nashik-Aurangabad), South (Bangalore-Chennai-Hosur) and East (Kolkata-Jamshedpur).

Markets StructureWith around 10.5 million vehicles produced in 2009-10, the two-wheelers market is undoubtedly the driving force of the industry and has made India the second largest market for this product worldwide (table 2). With regards the other items, with 2.3 million items produced the passenger vehicles

The Indian Automotive SectorIl settore indiano dell’automotive

Automotive 39

Map 1: Indian Automotive ClustersMappa 1: Distretti indiani dell’automotive

Source/Fonte: IBEF Report, Nov 2010

Automotive40

segment is the 3rd largest in Asia, 5th largest for bus and truck and 4th largest for commercial vehicles in the world.

The two-wheelers market is in fact a duopoly, with the domination of the two players Hero Honda (a JV between the Indian Hero Group and Japanese Honda Motor Company), with almost 60% of the entire market share and the Indian Bajaj Auto, with a stake of more 24% in the market.

From 2003 to 2010 the passanger vehicles (PVs) production envisaged a threefold growth, and it is estimated that this trend will continue, thus making India the 6th largest PV market and the 5th largest PV producer in the world by 2012. At present the PVs segment is dominated by passenger cars, mainly of small dimensions, that account for an 85% share of the market. Maruti Suzuki ranks 1st in terms of PVs market share, with almost the 50%.Apart from the slight decline in the production trend in 2008-09, the commercial vehicles segment (CVs) has witnessed a steadily growth in the last years, making India the 4th largest CVs market in the world.

The CVs industry is mainly divided between Light CVs and Medium-Heavy CVs goods carriers, respectively with 49.7% and 36% of the total market share, and it is absolutely dominated by local players, such as Tata Motors whose market stake is almost 64% in the M&HCVs and almost 59% in the LCVs, and Mahindra&Mahindra (M&M) that owns a 30% stake in the LCVs market.After a decline in the two-year-period 2007-2009, the three wheelers market saw a positive growth trend in the FY 2009-10, with 0.62 million of units produced. Piaggio has the first-largest market share in this segment, 41.1%, followed by Bajaj Auto, the world’s 4th largest two- and three- wheelers manufacturer.

Automotive 41

Indian clusters in the R&DIndia wants to prominently position itself in the forefront of the global automotive market.For this purpose the GoI, a number of State Governments and the Indian Automotive Industry joined hands to create one of the largest initiatives in the Automotive sector: a state of the art Testing, Validation and R&D infrastructure network in the country (Map 2).The Project, with its hubs in Tamil Nadu, Assam, Maharashtra, Haryana, Madya Pradesh and Uttar Pradesh, aims at creating core global competencies in the sector in India and facilitating integration of Indian Automotive industry with international companies.In the upcoming years India will become the new frontier in R&D, with centres of excellence, able to answer to the needs of international players such as low-costs, skilled and educated manpower, product-development capacities and access to the emerging neighboring countries. Foreign players will not only outsource to India, but will also establish their own R&D centres in the country.

Automotive42

Source/Fonte: IBEF Report, Nov 2010* Map outline for illustration purposes only.

Map 2: Indian clusters in the R&D

Automotive 43

Lo sviluppo dell’industria indiana dell’automotive, insieme al terziario, è stato uno

dei fattori trainanti della recente crescita economica dell’India.Nonostante sia in India uno dei più avanzati, il settore si è affrancato solo recentemente dai limiti im-posti da un’economia chiusa – come quella indiana – fino alla fine degli anni 80: carenza di attrezzature e materiali adeguati per la produzione, design obsoleti e un limitato numero di aziende attive.Il primo importante cambiamento è avvenuto nel 1981, quando il governo indiano ha aperto il mercato agli investimenti stranieri e ha siglato la joint venture con Suzuki per dare vita alla Maruti Udyog.Successivamente, il settore si è aperto ulteriormente con la liberalizzazione economica dell’India av-venuta negli anni ’90, con la quale è stato rimosso l’obbligo di licenza per l’apertura di un attività, le principali OEM (original equipment manufacturer) hanno cominciato ad assemblare in India, ed è stato concessa l’importazione di prodotti dall’estero.Nel nuovo millennio le aziende attive sono salite a

36. I bassi costi di produzione, dovuti ad economie di scala, e della R&D, la prossimità a mercati in rapida crescita quali quelli di Asia e Africa, e l’economicità delle spedizioni via nave dall’India verso l’Europa, costituiscono un vantaggio fondamentale per la crescita del settore.Le cifre relative al recente passato del settore sono chiare: la produzione di veicoli è quasi raddoppiata, da 7,2 milioni di unità prodotte nel 2003-04 a 14 milioni nel 2009-10; dai 6,8 milioni di unità vendute nel 2003-04 ai 12,3 milioni nel 2009-10, con un tasso di crescita annuo del 10% (tabelle 1 e 2).Nel 2009-10 gli investimenti diretti esteri (IDE) in India per il settore della componentistica auto, sono stati 1,2 milioni di US$, pari al 4% del totale.

Il grande dinamismo dell’automotive ha dato vita ad una serie di distretti industriali per l’automotive e componentistica auto in tutto il Paese: a Nord - Delhi-Gurgaon-Faridabad, ad Ovest - Mumbai-Pune-Nashik-Aurangabad, a Sud - Bangalore-Chennai-Hosur, e ad Est - Kolkata-Jamshedpur (Mappa 1).

Automotive44

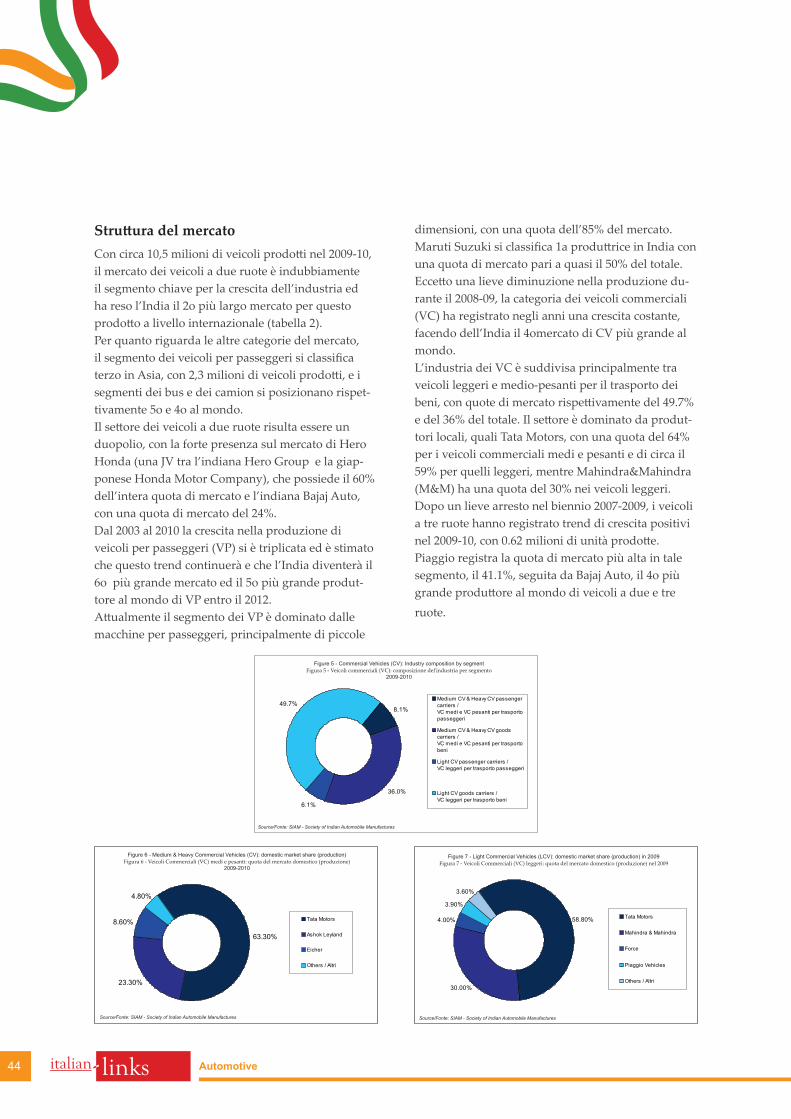

Struttura del mercatoCon circa 10,5 milioni di veicoli prodotti nel 2009-10, il mercato dei veicoli a due ruote è indubbiamente il segmento chiave per la crescita dell’industria ed ha reso l’India il 2o più largo mercato per questo prodotto a livello internazionale (tabella 2).Per quanto riguarda le altre categorie del mercato, il segmento dei veicoli per passeggeri si classifica terzo in Asia, con 2,3 milioni di veicoli prodotti, e i segmenti dei bus e dei camion si posizionano rispet-tivamente 5o e 4o al mondo.Il settore dei veicoli a due ruote risulta essere un duopolio, con la forte presenza sul mercato di Hero Honda (una JV tra l’indiana Hero Group e la giap-ponese Honda Motor Company), che possiede il 60% dell’intera quota di mercato e l’indiana Bajaj Auto, con una quota di mercato del 24%.Dal 2003 al 2010 la crescita nella produzione di veicoli per passeggeri (VP) si è triplicata ed è stimato che questo trend continuerà e che l’India diventerà il 6o più grande mercato ed il 5o più grande produt-tore al mondo di VP entro il 2012.Attualmente il segmento dei VP è dominato dalle macchine per passeggeri, principalmente di piccole

dimensioni, con una quota dell’85% del mercato. Maruti Suzuki si classifica 1a produttrice in India con una quota di mercato pari a quasi il 50% del totale.Eccetto una lieve diminuzione nella produzione du-rante il 2008-09, la categoria dei veicoli commerciali (VC) ha registrato negli anni una crescita costante, facendo dell’India il 4omercato di CV più grande al mondo.L’industria dei VC è suddivisa principalmente tra veicoli leggeri e medio-pesanti per il trasporto dei beni, con quote di mercato rispettivamente del 49.7% e del 36% del totale. Il settore è dominato da produt-tori locali, quali Tata Motors, con una quota del 64% per i veicoli commerciali medi e pesanti e di circa il 59% per quelli leggeri, mentre Mahindra&Mahindra (M&M) ha una quota del 30% nei veicoli leggeri.Dopo un lieve arresto nel biennio 2007-2009, i veicoli a tre ruote hanno registrato trend di crescita positivi nel 2009-10, con 0.62 milioni di unità prodotte. Piaggio registra la quota di mercato più alta in tale segmento, il 41.1%, seguita da Bajaj Auto, il 4o più grande produttore al mondo di veicoli a due e tre ruote.

Automotive 45

Distretti indiani per l’R&DL’India è decisa ha posizionarsi in prima linea nel mercato globale dell’automotive. A tale scopo il governo centrale, alcuni governi statali e l’industria dell’automotive indiani si sono uniti per fondare una delle più ampie iniziative nel settore: NATRiP - Na-tional Automotive Testing and R&D Infrastructure Project). Il progetto, con sedi in diversi stati indiani (Tamil Nadu, Assam, Maharashtra, Haryana, Madya Pradesh and Uttar Pradesh), ha l’obiettivo di creare una rete di centri d’eccellenza per test, validazione e R&D nel settore dell’automotive (Mappa 2), per aumentare l’expertise tecnologica e dare impulso alla crescita del settore in India. Il progetto vuole inoltre sviluppare una maggiore integrazione dell’industria indiana dell’automotive con le aziende internazi-onali.

Nei prossimi anni l’India si proporrà come la nuova frontiera dell’R&D, con centri d’eccellenza, capaci di rispondere alle necessità delle aziende internazi-onali, quali manodopera a basso costo e profes-sionale, capacità di sviluppo dei prodotti e accesso ai mercati emergenti dei Paesi limitrofi. Le stesse aziende straniere non solo utilizzeranno l’India per la produzione, ma apriranno in futuro i propri centri R&D nel Paese.

Automotive46

Source/Fonte: IBEF Report, Nov 2010* Map outline for illustration purposes only.

Mappa 2: Distretti indiani per l’R&D