the impact of the financial crisis and the recession on...

TRANSCRIPT

The impact of the financial crisis and the recession on insurance/reinsurance

Thomas Hess

Chief Economist, Swiss Re

Head of Economic Research & Consulting

SORS - Sarajewo18 June 2009

Agenda

Capital market and economic situation

Alternative scenarios

Prospects for global insurance markets

SORS - Sarajewo18 June 2009

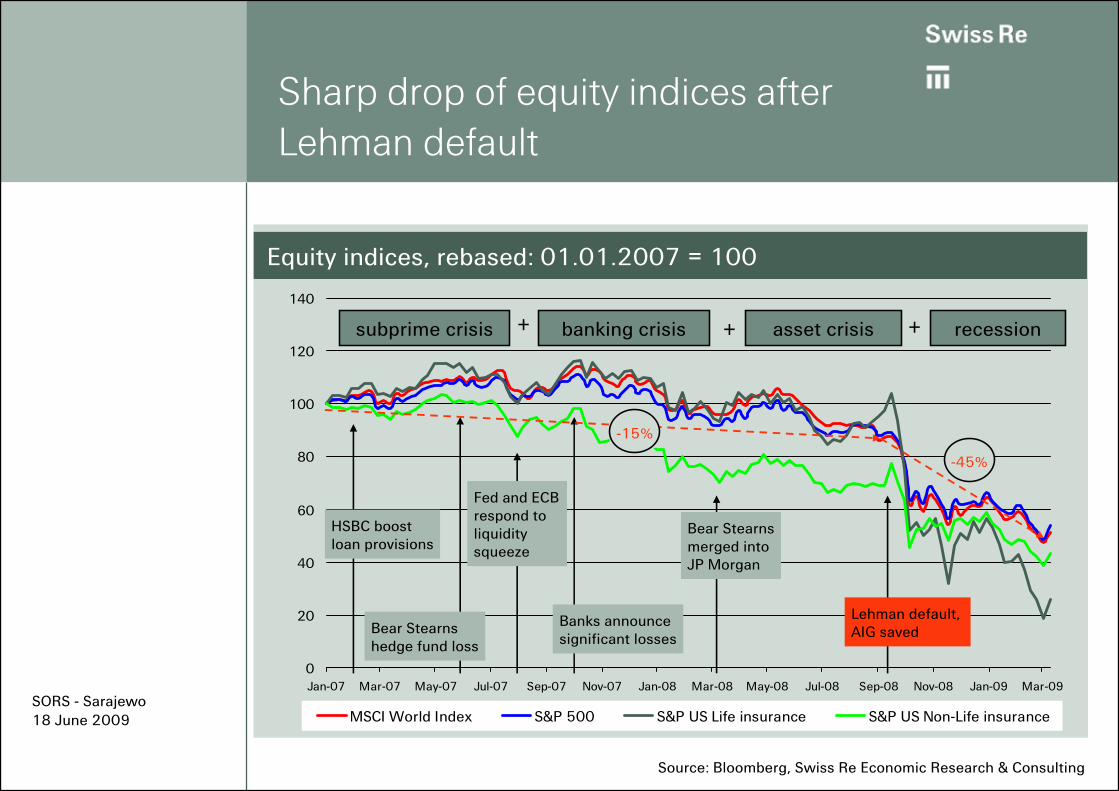

Sharp drop of equity indices after Lehman default

0

20

40

60

80

100

120

140

Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09

MSCI World Index S&P 500 S&P US Life insurance S&P US Non-Life insurance

Source: Bloomberg, Swiss Re Economic Research & Consulting

Equity indices, rebased: 01.01.2007 = 100

-45%

HSBC boost loan provisions

Bear Stearns hedge fund loss

Banks announce significant losses

Fed and ECB respond to liquidity squeeze

Bear Stearns merged into JP Morgan

Lehman default, AIG saved

subprime crisis banking crisis recessionasset crisis+ + +

-15%

SORS - Sarajewo18 June 2009

Global speculative-grade default rates

Sharp decline in corporate bond and equity values

European equities, (June 2007=100)

0

20

40

60

80

100

120

Jan

07

Apr

07

Jul 0

7

Okt

07

Jan

08

Apr

08

Jul 0

8

Okt

08

Jan

09

Apr

09

Banking sector Life insurance Non-life insurance DJ Euro Stoxx 50

+9% -2%

-53%

+-0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08Global speculative grade default rate

Pessimistic scenario

Moody's forecast:Baseline scenario

Optimistic scenario

Source: Moody’sSource: BloombergSORS - Sarajewo18 June 2009

Where are the deeper problems?

Too expansionary monetary policy in the US

Financial innovation

Irresponsible underwriting of US mortages

High leverage of banks (also off balance sheet)

Insufficient risk management of banks

Expectations that banks will be bailed out lead to excessive risk taking

Renumerations schemes

Problematic role of rating agencies

Problematic role of supervisorsSORS - Sarajewo18 June 2009

For many countries, the main transmission channel of the crisis is now the contraction of trade

80

85

90

95

100

105

110

115

120

125

2006 2007 2008 2009

World trade volumes in goods EurolandJapan USAUK Germany

Rapid global expansion Financial crisis Economic crisis

World trade volumes and Industrial Production in selected countries (Jan 2006=100)

Sources: CPB, DatastreamSORS - Sarajewo18 June 2009

Positive prospects for profits and growth of P%C insurers

-15

-10

-5

0

5

10

15

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Primary insurance Reinsurance

Source: Swiss Re, Economic Research & Consulting, March 2009 forecasts

additional volume 2009 and 10 due to large transactions

Back to moderate growth (yoy %, infl adj.) Insurance results improve 2010/ 12

* *

*) % of premiums

% %

-15

-10

-5

0

5

10

15

20

99 00 01 02 03 04 05 06 07 08 09 10 11 12

Underwriting result Investment resultOperating result ROE after tax

%

*)*)

*)

SORS - Sarajewo18 June 2009

The need to bolster demand makes large public policy actions indispensable…

0

1

2

3

4

5

6

Saud

i Ara

bia

Spai

n

Sout

h A

fric

a

US

Aus

tral

ia

Kor

ea

Chi

na

Ave

rage

G2

0

Japa

n

Rus

sia

UK

Mex

ico

Ger

man

y

Can

ada

Indo

nesi

a

Arg

entin

a

Fran

ce

Indi

a

Bra

zil

Ital

y

Turk

ey

Discretionary fiscal stimulus Automatic stabilisers

G20: Estimated cost of discretionary measures and automatic stabilisers (% of GDP, 2008-2009)

Sources: IMF, “The State of Public Finances: Outlook and Medium-Term Policies After the 2008 Crisis”, Swiss Re ER&C

0

200

400

600

800

1'000

1'200

1'400

1'600

1'800

2000 2001 2002 2003 2004 2005 2006 2007 2008

US Euroland

Monetary base (bn local currency)

Source: Datastream

SORS - Sarajewo18 June 2009

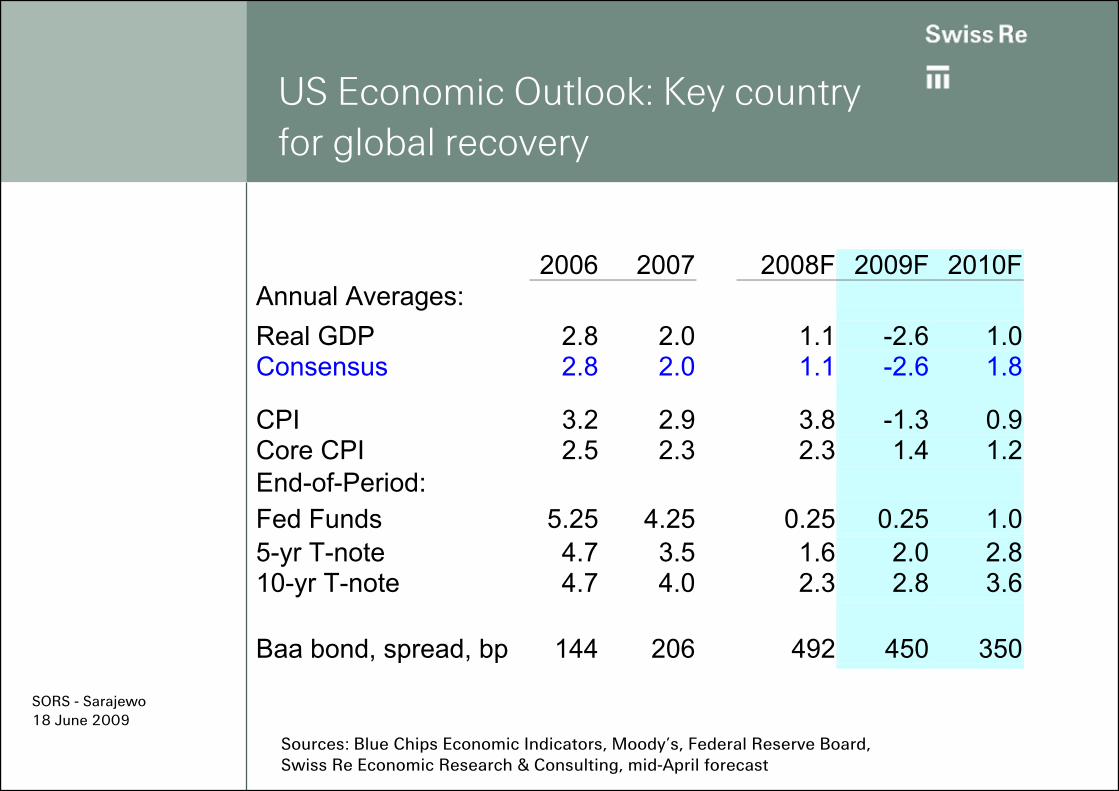

2006 2007 2008F 2009F 2010F

Annual Averages:

Real GDP 2.8 2.0 1.1 -2.6 1.0 Consensus 2.8 2.0 1.1 -2.6 1.8

CPI 3.2 2.9 3.8 -1.3 0.9 Core CPI 2.5 2.3 2.3 1.4 1.2 End-of-Period: Fed Funds 5.25 4.25 0.25 0.25 1.0 5-yr T-note 4.7 3.5 1.6 2.0 2.8 10-yr T-note 4.7 4.0 2.3 2.8 3.6 Baa bond, spread, bp 144 206 492 450 350

Sources: Blue Chips Economic Indicators, Moody’s, Federal Reserve Board, Swiss Re Economic Research & Consulting, mid-April forecast

US Economic Outlook: Key country for global recovery

SORS - Sarajewo18 June 2009

2007 2008 2009F 2010F

Real GDP growth Euroland 2.6 0.9 -3.4 0.3

UK 3.1 0.8 -4.1 -0.1Japan 2.0 -0.4 -6.3 0.4

Inflation Euroland 2.1 3.3 0.9 1.1

UK 2.3 3.6 1.2 1.0Japan 0.1 1.4 -0.9 0.5

Policy rates (eop) Euroland 4.00 2.50 1.0 1.25

UK 5.50 2.00 0.50 0.75Japan 0.46 0.10 0.05 0.75

Yields 10-yr govt bond Euroland 4.3 2.9 3.0 4.2

UK 4.5 3.1 3.1 3.6Japan 1.5 1.2 1.3 1.9

Sources: Swiss Re Economic Research & Consulting, mid-April forecast

Global overview: Down in 2009, weak recovery in 2010

SORS - Sarajewo18 June 2009

Global economic outlook

What gets us out of the recession?

– Substantial Central Bank easing, low interest rates

– Fiscal stimulus

– Lower oil/commodity prices, reduced inflation

– US consumers and housing will likely lead the way

SORS - Sarajewo18 June 2009

What happens in the recovery?

Temporary investment opportunities: Credit and equities

– Late in recession, early recovery

Government bond yields likely to remain low

– But likely to rise in 2010, 2011

Risk of inflation rises, but low inflation most likely

– Risk is low through end-2010, may not be a problem until 2012 or later

– Fiscal/monetary restraint will keep growth moderate

– Central banks are familiar with how to tighten monetary policy

– Risk is essentially political

SORS - Sarajewo18 June 2009

The crisis will cause medium term trend growth to drop slightly

GDP

GER

FR

IT

Spain

CH

AT

Real

2009

-5.6

-3.0

-4.4

-3.0

-3.7

-3.0

2010

-0.4

0.4

-0.4

- 0.7

-0.3

0.2

2014

2.3

2.4

1.9

2.0

1.5

2.3

Real GDP (yoy %-growth)

Source: IMF forecasts, April 2009

Key differentiating issues

Size and situation of the banking system

Indebtness of consumers

Extent of overvaluation of real estate prices

Importance of the export sector

Solidness of public finances

SORS - Sarajewo18 June 2009

Agenda

Capital market and economic situation

Alternative scenarios

Prospects for global insurance market

SORS - Sarajewo18 June 2009

What can happen differently?

Downside scenario 25% - deeper recession - lower interest rates 2010, credit spreads tighten later and worse stock-market

Upside scenario 15% - recession less deep; - higher interest rates 2011; credit spreads tighten earlier and better stock-markets

Bumpy: Overstimulation leads to inflation 2012-14 - recovery stronger and inflation rises to 5% or more for several years - monetary tightening will cause another recession - tightening of credit spreads followed by another widening; higher interest rates 2011-2014; stock-markets better then worse

Baseline 60%

May be combined with different

scenarios above!

The downside scenario is most severe for companies with elevated asset risks, risks for life companies are substantially increased The overstimulation scenario provides a window of opportunity to sell risky assets; it is also more positive for life companies, but causes a period of claims inflation

SORS - Sarajewo18 June 2009

Agenda

Capital market and economic situation

Alternative scenarios

Prospects for global insurance markets

SORS - Sarajewo18 June 2009

New April 2009 IMF credit loss estimates

Credit losses have been revised upwards to 4000bn

Banks losses are estimated to be 2400 bn, which is 60% of the total

Insurers have losses of 301bn (US: 218/ EU: 75bn, Japan 8 bn), which is 7% of the total of credit related losses (revised downwards!)

In addition insurers face losses from equity investments, alternative assets, real estate and participations

ER&C forecasts of 500 bn (25%) losses on shareholder capital is consistent with IMF figures (total losses on assets are higher as they are shared with life policyholders)

SORS - Sarajewo18 June 2009

In 2009-2010, a key issue will be the recapitalisation…

60

70

80

90

100

110

Dec 06 Jun 07 Dec 07 Jun 08 Dec 08E

Shareholder’s EquityIndex Q2 2007=100, USD*

Sources: Annual Reports, Bloomberg, Swiss Re Economic Research & Consulting

+10%

-26%

*26 large Insurers

In 2008, the non-life insurance industry lost about 20% and the life insurance industry between 30-40% of the capital base

SORS - Sarajewo18 June 2009

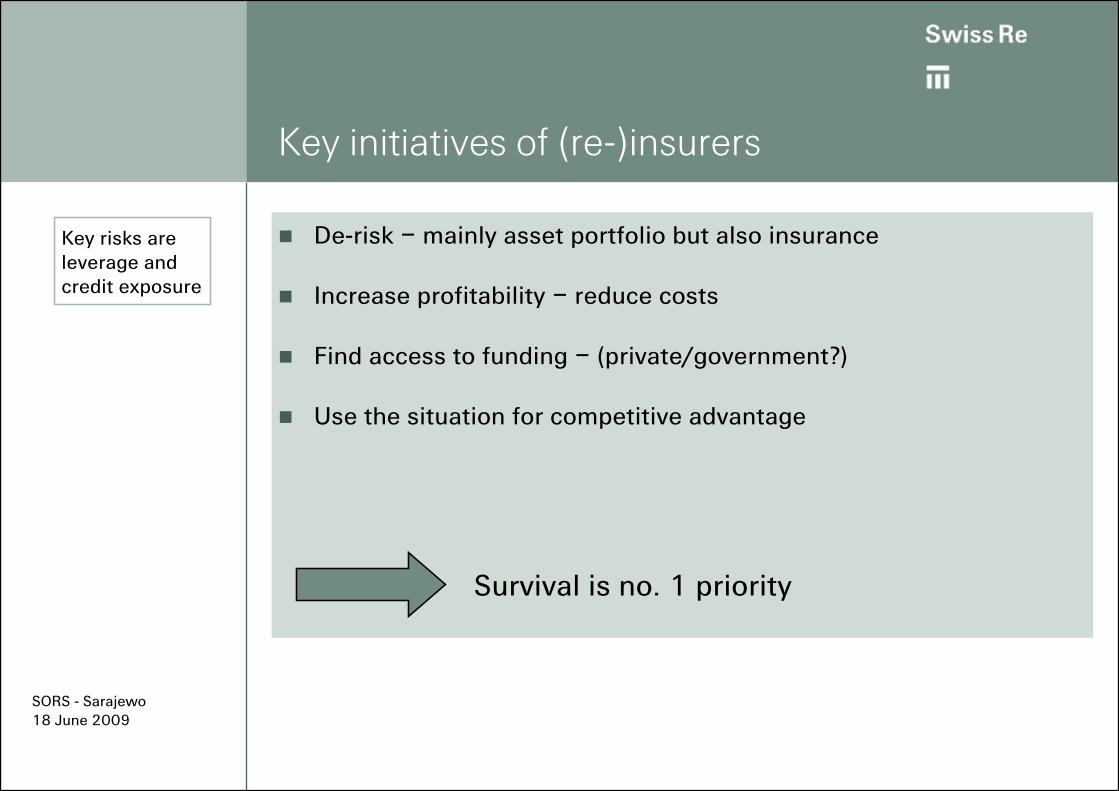

Key initiatives of (re-)insurers

De-risk – mainly asset portfolio but also insurance

Increase profitability – reduce costs

Find access to funding – (private/government?)

Use the situation for competitive advantage

Survival is no. 1 priority

Key risks are leverage and credit exposure

SORS - Sarajewo18 June 2009

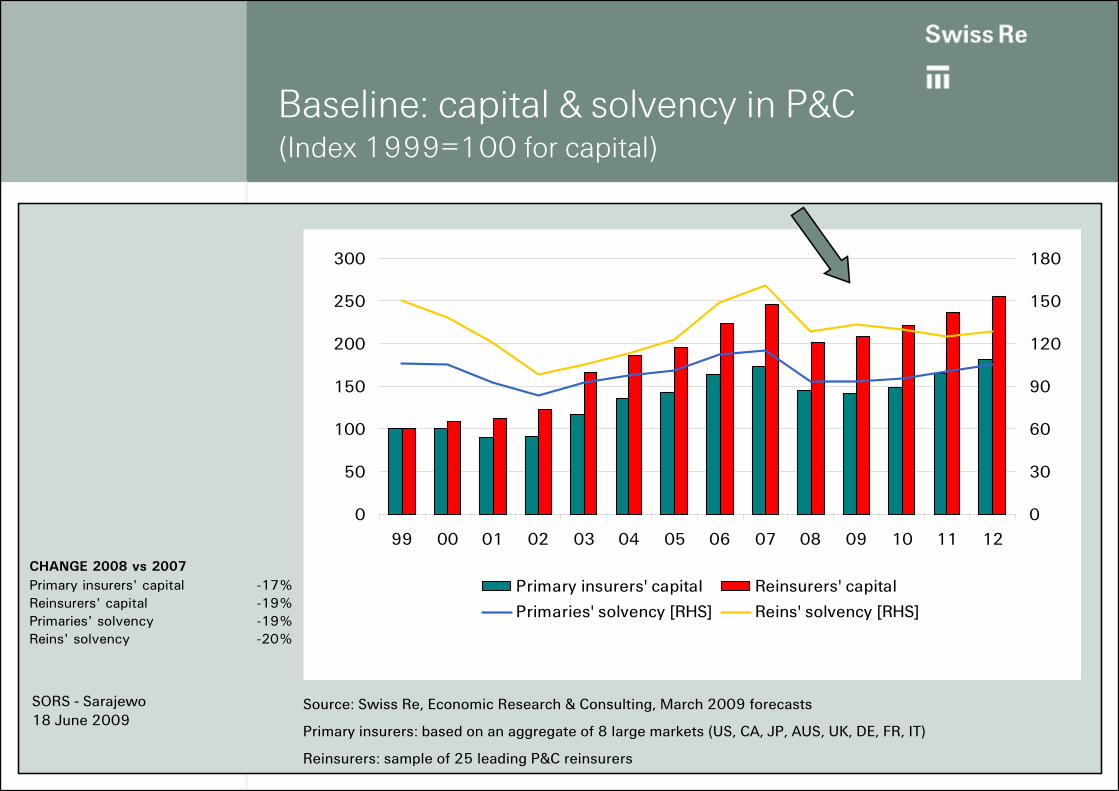

Baseline: capital & solvency in P&C (Index 1999=100 for capital)

0

50

100

150

200

250

300

99 00 01 02 03 04 05 06 07 08 09 10 11 120

30

60

90

120

150

180

Primary insurers' capital Reinsurers' capital

Primaries' solvency [RHS] Reins' solvency [RHS]

CHANGE 2008 vs 2007Primary insurers' capital -17%Reinsurers' capital -19%Primaries' solvency -19%Reins' solvency -20%

Source: Swiss Re, Economic Research & Consulting, March 2009 forecasts

Primary insurers: based on an aggregate of 8 large markets (US, CA, JP, AUS, UK, DE, FR, IT)

Reinsurers: sample of 25 leading P&C reinsurers

SORS - Sarajewo18 June 2009

Positive prospects for growth and profitability non-life

-15

-10

-5

0

5

10

15

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Primary insurance Reinsurance

Source: Swiss Re, Economic Research & Consulting, March 2009 forecasts

Back to moderate growth (yoy %, infl adj.)

-30

-20

-10

0

10

20

30

99 00 01 02 03 04 05 06 07 08 09 10 11 12

U/w result Investment resultOperating result RoE after tax

%Reinsurance results improve 2010/ 12

* *

*) % of premiums

% %

SORS - Sarajewo18 June 2009

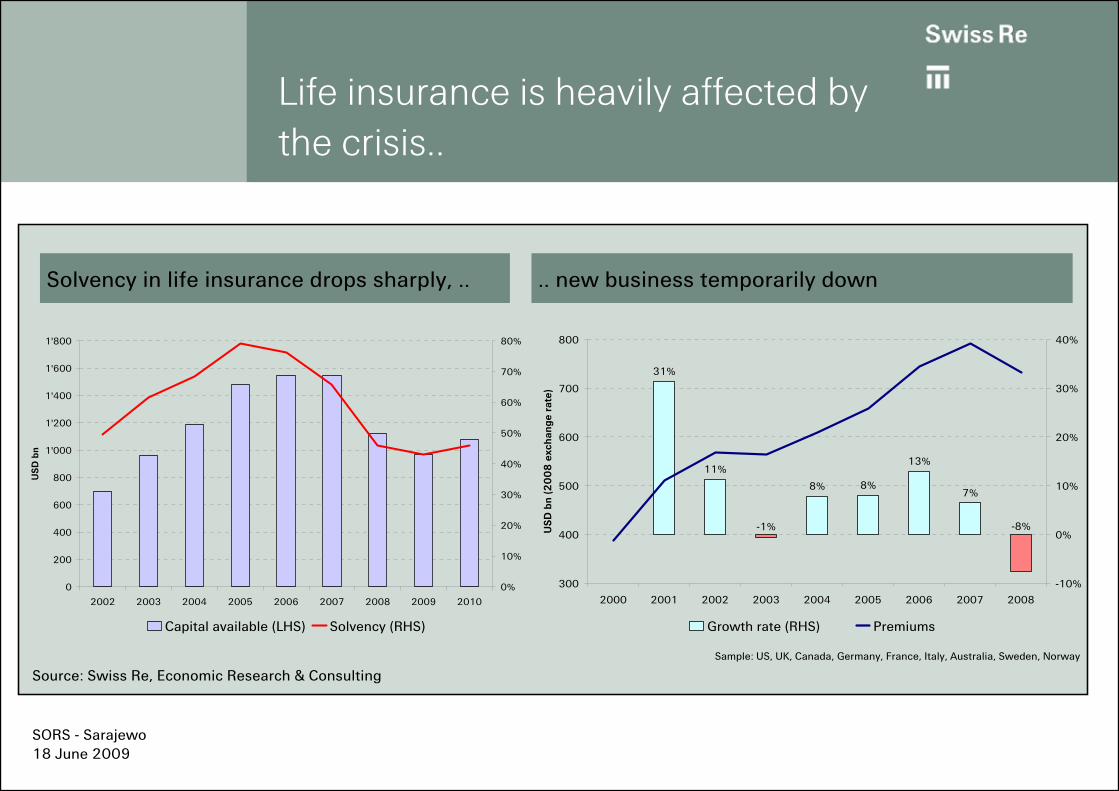

Life insurance is heavily affected by the crisis..

Solvency in life insurance drops sharply, .. .. new business temporarily down

Source: Swiss Re, Economic Research & Consulting

0

200

400

600

800

1'000

1'200

1'400

1'600

1'800

2002 2003 2004 2005 2006 2007 2008 2009 2010

USD

bn

0%

10%

20%

30%

40%

50%

60%

70%

80%

Capital available (LHS) Solvency (RHS)

Sample: US, UK, Canada, Germany, France, Italy, Australia, Sweden, Norway

31%

11%

8% 8%

13%

7%

-8%-1%

300

400

500

600

700

800

2000 2001 2002 2003 2004 2005 2006 2007 2008

USD

bn

(20

08

exc

hang

e ra

te)

-10%

0%

10%

20%

30%

40%

Growth rate (RHS) Premiums

SORS - Sarajewo18 June 2009

.. and lots of companies face severe solvency issues

BVPS PriceGenworth Financial -33% -89%Hartford -50% -81%ING -24% -73%China Life -12% -68%Lincoln National -30% -68%Prudential (US) -39% -67%Principal Financial -67% -67%Protective Life -69% -65%Allianz -30% -49%Sun Life 2% -49%Manulife 6% -49%Friends Provident -20% -47%Metlife -37% -43%AXA -20% -42%Aviva -15% -42%Prudential (UK) -19% -42%Legal & General -29% -41%Generali -27% -37%Zurich -24% -32%Standard Life 5% -20%Source: Bloomberg

Change in

Book value and stock prices end 08/07Life insurers are hit much harder than non-life insurers due to their higher asset leverage

SORS - Sarajewo18 June 2009

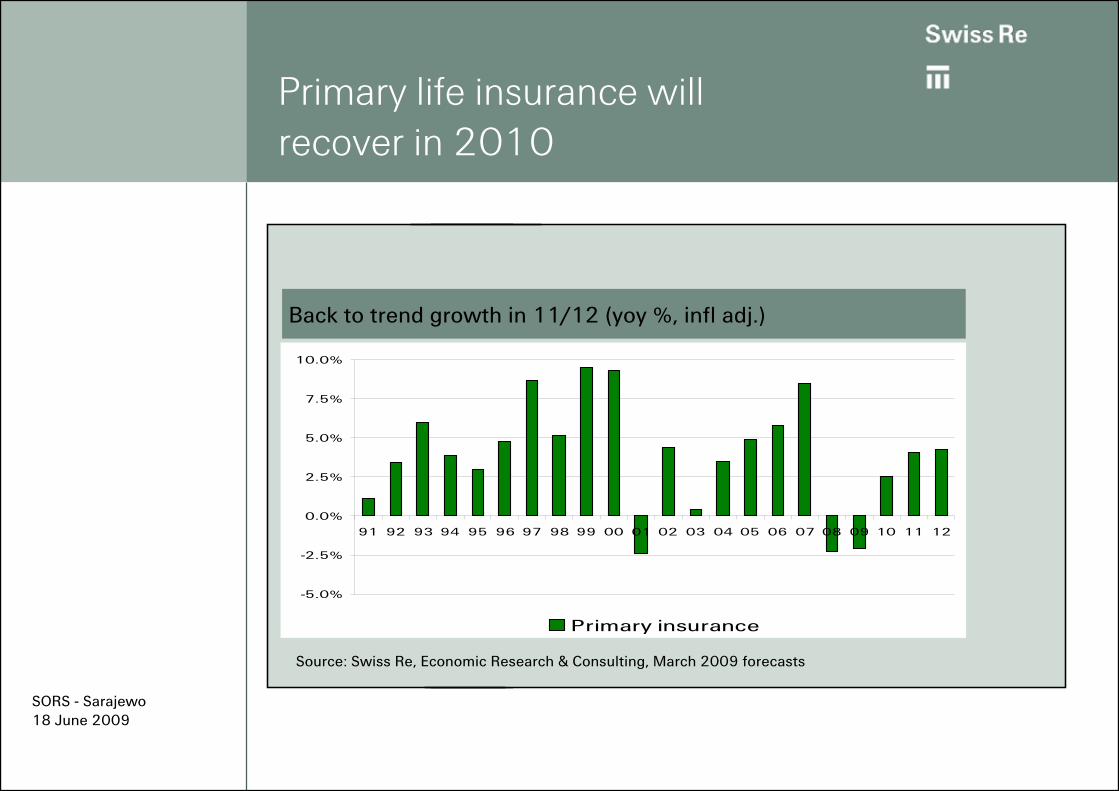

Primary life insurance will recover in 2010

Source: Swiss Re, Economic Research & Consulting, March 2009 forecasts

Back to trend growth in 11/12 (yoy %, infl adj.)

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Primary insurance

SORS - Sarajewo18 June 2009

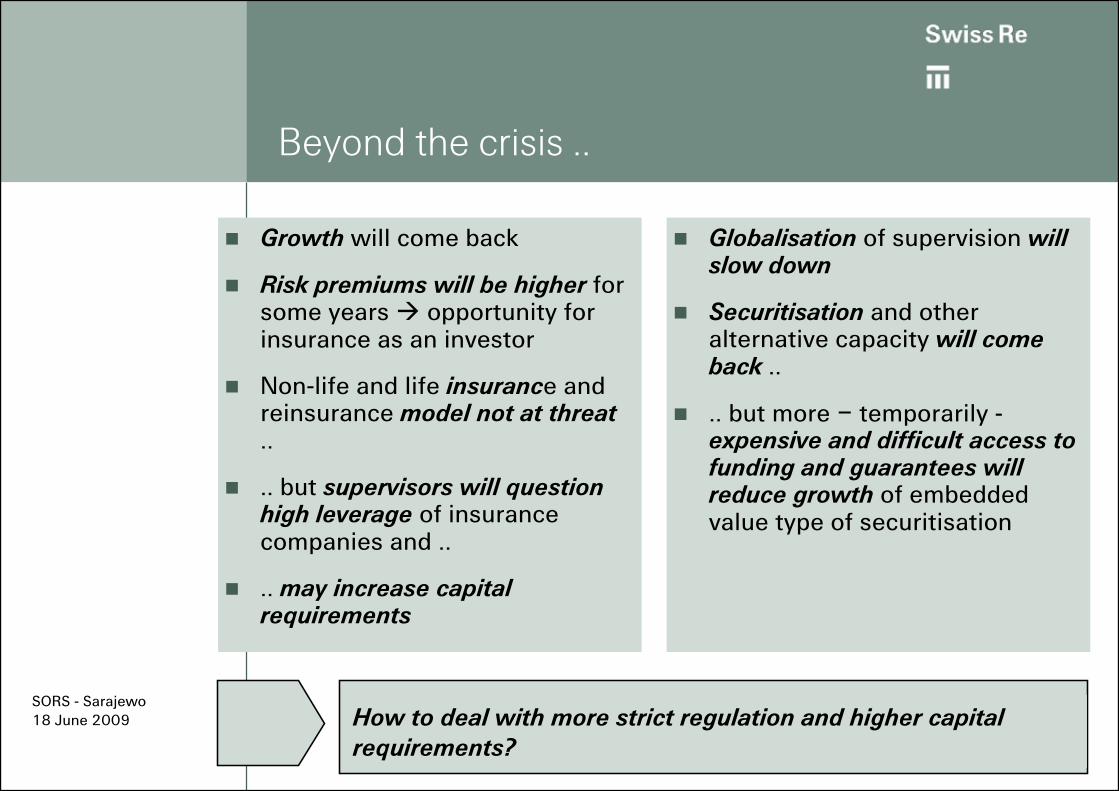

How to deal with more strict regulation and higher capital requirements?

Beyond the crisis ..

Growth will come back

Risk premiums will be higher for some years opportunity for insurance as an investor

Non-life and life insurance and reinsurance model not at threat ..

.. but supervisors will question high leverage of insurance companies and ..

.. may increase capital requirements

Globalisation of supervision will slow down

Securitisation and other alternative capacity will come back ..

.. but more – temporarily -expensive and difficult access to funding and guarantees will reduce growth of embedded value type of securitisation

SORS - Sarajewo18 June 2009

Huge demand ..

Reinsurance is a superior risk mgmt tool (flexible, quickly available and discreet)

Solvency problems of companies increases need for reinsurance

.. but they may not afford it

Lack of alternative risk and capital mgmt instruments

.. in particular for companies hard hit resp. smaller companies

Reinsurance will play an important role in coping with the crisis

… may not be fully met

Lack of capacity, including alternative sources of reinsurance capacity

Risk transfer may involve transfer of problematic assets

Reinsurers will play an important role in managing the crisis and in the recapitalisation process

Parts of the alternative risk transfer suffer from the crisis

What works?- CAT bonds non-life and life- ILW (insuance linked warrants)- Weather derivatives

What doesn‘t wirk so well?- Embedded value securitisation life- Side car capacity

Prospect remain favorable - questions marks regarding embedded value securitisation life

SORS - Sarajewo18 June 2009

Limited effects of the crisis on (re-) insurance risk transfer …

Insurance and reinsurance markets continue to work

Capacity declined but there is no shortage

Policyholders kept trust in the industry

Alternative risk tranfer was affected but will recover - ILS- ILW- Sidecars- Insurance derivative markets- Embedded value securitisation life (?)

SORS - Sarajewo18 June 2009

… but credit related activities will be more closly monitiored in future

Monoliners will hardly provide financial guarantees for capital market products in future

ALM will get even more important

Embedded options in Life insurance will get more attention, the same for market risks of investments

Supervisors will pay more attention to tail risk, liquidity risk and leverage of insurers (also related to derivatives)

SORS - Sarajewo18 June 2009

Conclusion

The economic environment remains challenging and demands for strict risk management

Low interest rates and the need for recapitalisation ask for solid underwriting results

As soon as financial markets stabilise profitability will improve; the recovery will be bumpy

Non-life will do better than life insurance until we see capital markets forcefully bouncing back

Insurance and reinsurance business model is not at stakeSORS - Sarajewo

18 June 2009