the impact of change in financial power trading · the impact of change in financial power trading...

TRANSCRIPT

NASDAQ OMX

THE IMPACT OF CHANGE IN FINANCIAL POWER TRADING

DANISH ENERGY DAY COPENHAGEN 2015

Bjørn Sibbern

Global Head Nasdaq Commodities and

President Nasdaq Copenhagen

NASDAQ OMX

NASDAQ: WHO WE ARE

IGNITE YOUR AMBITION 2

Over the past decade, Nasdaq has transformed its business from a U.S.‐based equities exchange to a diversified global financial technology company. Today, the company is firmly established as a leading provider of trading, exchange technology, information and public company services across six continents.

NASDAQ TICKER SYMBOL: NDAQMEMBER OF S&P 500

OUR MISSION >We provide market‐leading technology solutions and intelligence to help businesses and investors succeed in today’s global capital markets.

OUR VISION >We connect business, capital and ideas to advance today’s global economies.

MAR

REMIT

EMIR

MIFID

MIFID II

EMIRBANK GUARANTEES STATUS / GOING FORWARD

4

Bank Guarantees on the Nordic/Baltic Power Market

ACTIONS ON BANK GUARANTEES ‐ LOBBY PROCESS

Where are we:• Support from 7 Nordic and Baltic Governments (have written a letter to the Commission)• Nasdaq has together with other parties (EFET, Eurelectric, UK Energy, CEER, EACH) included bank guarantees in the EMIR review consultation where we have asked for a prolonging of the exception when included in the review. The goal is a permanent solution

• Support from The Council of European Energy regulators (CEER) that also responded to the EMIR review consultation. CEER represents 33 European national energy regulators including the EU 28 Member States.

• Nordic FSAs written a supporting letter to ESMA in August 2015

Going forward• Must stay close to the Nordic Ministries to keep up the political pressure.• Stay close to other European countries where we have support and try to get support from additional European countries (Portugal, Spain and Poland have confirmed support).

• Keep up the pressure towards the Commission, MEPs and ESMA. • The commission is now reviewing the EMIR submissions. When will the EMIR review report be sent to the European Parliament and council?

6

OBJECTIVE: SECURE THAT NON‐FINANCIAL COUNTERPARTIES CAN USE NON FULLY BACKED BANK GUARANTEES BEYOND MARCH 2016

ACTIONS ON BANK GUARANTEES – PLAN B

7

• Work in parallel with good solutions for our members to reduce negative effects from the loss of bank guarantees, e.g. GCM banks

• Listing Nordic electricity futures Q3‐15Will DS Futures be preferred by hedgers due to accounting principles (IFRS)? And/or retail needs? DS Futures will not be taken out for nowDual listing of DS futures and futures & avoid fragmentationDo we need to list futures in order to attract more financial players to the market?

Nasdaq and our members will cooperate together on these issues to create the best solutions

MiFID II IMPACT ON COMMODITIES

99© Oliver Wyman

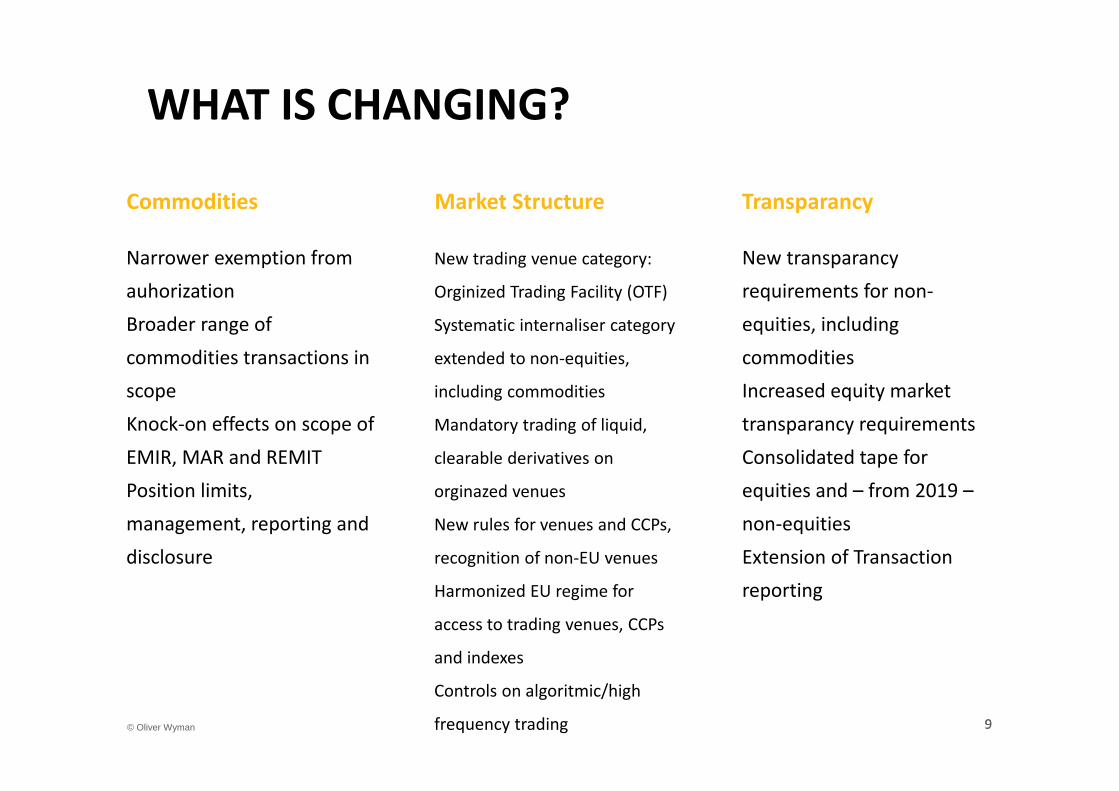

WHAT IS CHANGING?

Narrower exemption from auhorizationBroader range of commodities transactions in scopeKnock‐on effects on scope ofEMIR, MAR and REMITPosition limits, management, reporting and disclosure

New trading venue category:

Orginized Trading Facility (OTF)

Systematic internaliser category

extended to non‐equities,

including commodities

Mandatory trading of liquid,

clearable derivatives on

orginazed venues

New rules for venues and CCPs,

recognition of non‐EU venues

Harmonized EU regime for

access to trading venues, CCPs

and indexes

Controls on algoritmic/high

frequency trading

New transparancyrequirements for non‐equities, includingcommoditiesIncreased equity market transparancy requirementsConsolidated tape for equities and – from 2019 –non‐equitiesExtension of Transaction reporting

Commodities TransparancyMarket Structure

MARKET IMPACT

10

CLEARED VOLUMES NORDIC POWER

11

Low volatilityLow pricesOversupplyFunds and banks exitingRegulationsPolitical influence

0

500

1 000

1 500

2 000

2 500

3 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cleared volumes Nordic Power Yearly 2005‐2015 (TWh)

On Orderbook Off Orderbook

BANKS RESTRUCTURING OR PULLING OUT OFCOMMODITIES –BUT FOR HOW LONG?

12

TERMINATED «FUNDS»

• Adapto Advisors • Alfakraft• Interkraft Energy Fund• NK Funds• Electris Energy Fund• Navitas Power Fund• Elexir (MK)• Norden Absolute Energy• Orkla Energy Fund• Plenum Power Surge• European Energy Fund• NEF Nordic Power index• Kortlongs

Majority of their investments were allocated to Nordic Power.

Earlier in periods with low volatility, positions were increased in the Nordic power market for the investment companies to meet return targets.

Today we see increased competition from other commodities/ asset classes in periods were volatility is hovering on low levels.

WHAT HAPPENED TO THE OPTIONS VOLUME?

• The low volatility combined with several banks and funds out of the market have had a big impact on Option and Delta volumes.

• Existing power funds have not delivered good enough returns to get attention from potential investors.

• Less use of options in hedging.

Historically options represented between 15‐20% of total cleared volumes, in 2014 1%.

OPEN INTEREST TWH

15

Open Interest MWENOYR‐16 9227ENOYR‐17 7062ENOYR‐18 3152ENOYR‐19 1396ENOYR‐20 451

0

100

200

300

400

500

Open Interest Nordic Power Monthly (TWh)

Series1

MARKET SHARE PER COUNTRY

16

Non‐Nordic members market share in 2007 = 17% / 2014= 33%

MARKET SHARE PER PRODUCT CATEGORY

17

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percentages of Cleared volumes for Different Nordic Power Product Categories Yearly 2006‐2015 (TWh)

Year Week Quarter Month Day

MARKET SHARE PER CUSTOMER CATEGORY

18

0.00

30.00

60.00

90.00

120.00

150.00

180.00

210.00

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Jan‐11

Mar‐11

May‐11

Jul‐1

1

Sep‐11

Nov

‐11

Jan‐12

Mar‐12

May‐12

Jul‐1

2

Sep‐12

Nov

‐12

Jan‐13

Mar‐13

May‐13

Jul‐1

3

Sep‐13

Nov

‐13

Jan‐14

Mar‐14

May‐14

Jul‐1

4

Sep‐14

Nov

‐14

Jan‐15

Mar‐15

TWh

On Orderbook traded Market Share per Customer CategoryMonthly 2011‐2014

Turnover Credit Institution Finance/Fund Fundamental

FOCUS AREAS EUROPE

19

Bank Guarantees• Continued support for both Direct and GCM Membership models• Product structure: Future vs Forwards (DS Futures)

Distribution• Onboard GCM – Financial members outside the Nordics often prefer GCM• New ISV

Product development• Asian options• Average weighted monthly futures • Nordic power futures• Renewable production index• New Markets – Continue our success on German Power• More short term contracts?

Capital efficiency• Reduced no. of lead days• Inter Commodity Spread Credit (ICSC) on EPADs

GLOBAL STRATEGY AND GROWTH APPROACH

GTMS Strategy ‐ 201520

• Nasdaq Commodities’ strategy is to expand into a global unit

• Be a leading Global Commodity exchange and clearing house

• Our geographical extension include NFX (Nasdaq Futures, Inc.) in the US, Asian Strategy for Freight and Steel, the German Power initiative and soon other European Power markets

• Continue to build a global product portfolio

• Advantage of Nasdaq’s global brand

• Increase distribution through GCMs / FCMs

21

THE NASDAQ MARKET MODELGLOBAL PRODUCTS - SCANDINAVIAN EXCHANGE AND CCP

21

Europe

Asia

US

Global Clients Norwegian Exchange

Swedish Clearinghouse

p

The Nasdaq business model is also used by the other competing exchanges and ccps

Nasdaq Commodities Product offering

22 ants

EXISTING PRODUCTSEXISTING PRODUCTS

ELECTRICITY• Nordic • German• UK• Dutch• El‐Cert• NFX: US Futures ofElectricity, Oil, Nat Gas

ELECTRICITY• Nordic • German• UK• Dutch• El‐Cert• NFX: US Futures ofElectricity, Oil, Nat Gas

EMISSIONS• EUA • EUAA• CER

EMISSIONS• EUA • EUAA• CER

GAS• UK Gas• Spark spreads

GAS• UK Gas• Spark spreads

FUTURE DEVELOPMENTSFUTURE DEVELOPMENTS

• Nordic Futures • Continental energy markets• Renewables• Steel

• Nordic Futures • Continental energy markets• Renewables• Steel

FREIGHT• Dry• Tankers • Fuel Oil• LPG• Iron ore

• Coal

FREIGHT• Dry• Tankers • Fuel Oil• LPG• Iron ore

• Coal

SEAFOOD• SalmonSEAFOOD

• Salmon

NASDAQ FUTURES NFX – PRODUCT SCOPE

• Energy Trading is highly concentrated in a limited number of contracts (key benchmarks).

• Nasdaq Futures (NFX) are targeting the key Energy benchmarks in oil, U.S. Natural Gas, and U.S. Power

• The oil products includes the critical distillates needed to support the trading of the “whole” barrel

• Due to the power production mix in the U.S., there is a tight trading relationship between power and natural gas

and our initial product suite will meet the hedging needs of the vast majority of the market participants

• We intend to expand the product suite beyond the initial scope within the first 12 months based on

customer feedback and demand

23

Benchmark Oil Complex:1. WTI Crude Oil (CME)

1. Futures and options2. Brent Crude Oil (ICE)

1. Futures and options3. Fuels ‐ Heating & Gasoil, Gasoline

1. Futures

Benchmark U.S. Natural Gas: 1. Henry Hub

Futures and Options2. Natural Gas Basis to Henry Hub

Futures

Benchmark U.S. Electricity (Power): 1. All major Independent System Operators (grid operators) including:

1. Pennsylvania/Jersey/Maryland (PJM), New England, Mid‐West, California