the impact of canadian floriculture imports on the u.s. floriculture industry bruce w. smith center...

TRANSCRIPT

The Impact of Canadian Floriculture

Imports on the U.S. Floriculture Industry Bruce W. Smith

Center for Regional DevelopmentDepartment of Geography

Bowling Green State UniversityBowling Green, Ohio 43403

Neil ReidUrban Affairs Center

Department of Geography and PlanningThe University of Toledo

Toledo, Ohio 43606

Michael C. CarrollCenter for Regional Development

Department of EconomicsBowling Green State University

Bowling Green, Ohio 43403

Presented to the Annual Meeting of the Association of American Geographers, San Francisco, California, April 17-21, 2007

Presentation Outline

• Purpose

• Economic Context

• Canadian Competition

• Causes of Growing Canadian Imports

• Conclusions

Purpose

• Describe changing pattern of Canadian floriculture imports into the U.S.

• Identify the context and causes of those changes.

Industry Definition

Floriculture Production Definition

• Floriculture Production

• NAICS Code 111442

• establishments primarily engaged in growing and/or producing floriculture products such as

– cut flowers– bedding plants– hanging baskets– house plants

Economic Context

Top Agricultural Products Sold by Market Value, 2002

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

Catt

le &

calv

es

Gra

ins,

oil

seed

s,

dry

bean

s,

& d

ryp

eas

Po

ult

ry &

eg

gs

Mil

k &

oth

er

dair

y p

rod

ucts

fro

m c

ow

s

Nu

rsery

,g

reen

ho

use,

flo

ricu

ltu

re,

&so

d

Fru

its,

tree

nu

ts,

&b

err

ies

U.S

. D

ollars

Source: USDA, 2003

Top U.S. Floriculture Producing States,2004

• The top two producing states are California (20.5%) and Florida (16.5%)

• No other state has over 5% of national production

FloridaCaliforniaMichiganTexasOhioOther

Source: USDA, 2005

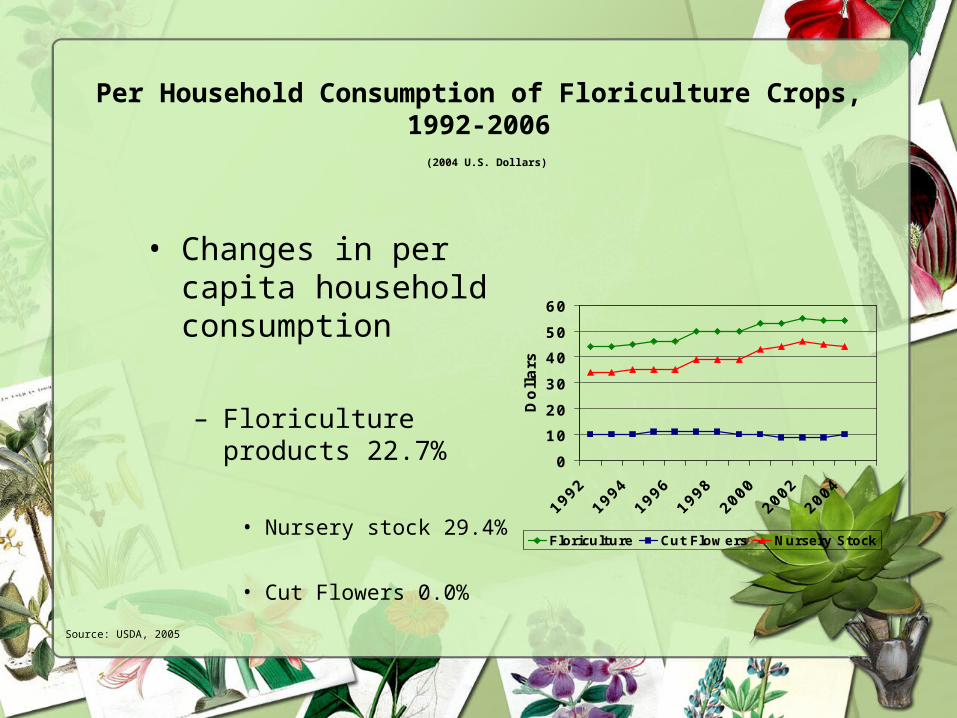

FloricultureA Growing Market

• Per household consumption of floriculture products increased from $44 to $54 between 1992 and 2004

• This represents an increase of 22.7%

Per Household Consumption of Floriculture Crops, 1992-2006 (2004 U.S. Dollars)

• Changes in per capita household consumption

– Floriculture products 22.7%

• Nursery stock 29.4%

• Cut Flowers 0.0%

0

10

20

30

40

50

60

Do

llars

Floriculture Cut Flowers Nursery Stock

Source: USDA, 2005

Floriculture Average Sales Per Acre,1993-2004

0

20000

40000

60000

80000

100000

120000

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

Sale

s p

er

Acre

($

)<$100,000 sales >$100,000 sales All growers

Change1993-2004

Grower Type

Number Percent

All Growers $5,149 6.5%

<$100,000 sales

-$12,382 -28.9%

>$100,000 sales

$8,311 9.7%

Source: USDA, 2005

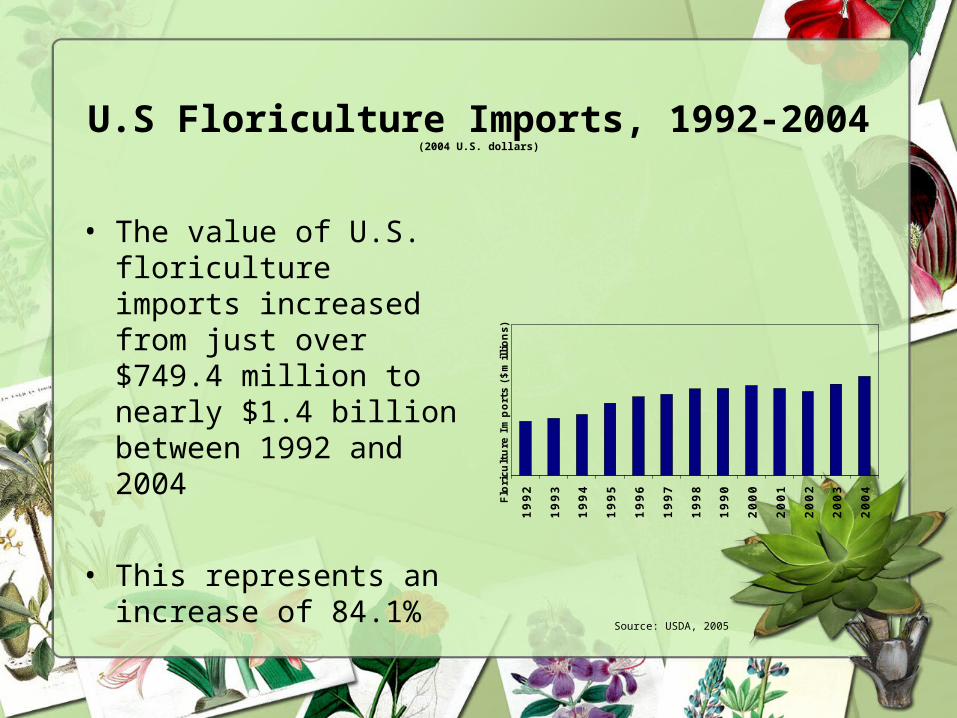

U.S. Floriculture Imports

U.S Floriculture Imports, 1992-2004(2004 U.S. dollars)

• The value of U.S. floriculture imports increased from just over $749.4 million to nearly $1.4 billion between 1992 and 2004

• This represents an increase of 84.1%

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

90

20

00

20

01

20

02

20

03

20

04

Flo

ricu

ltu

re I

mp

ort

s ($

million

s)

Source: USDA, 2005

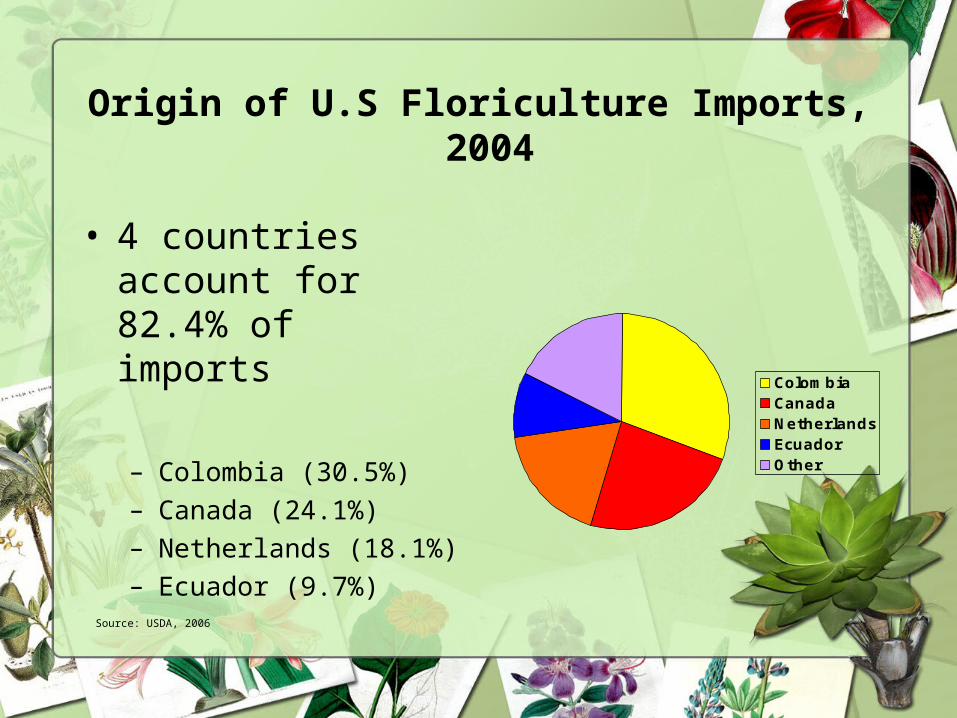

Origin of U.S Floriculture Imports, 2004

• 4 countries account for 82.4% of imports

– Colombia (30.5%)– Canada (24.1%)– Netherlands (18.1%)– Ecuador (9.7%)

ColombiaCanadaNetherlandsEcuadorOther

Source: USDA, 2006

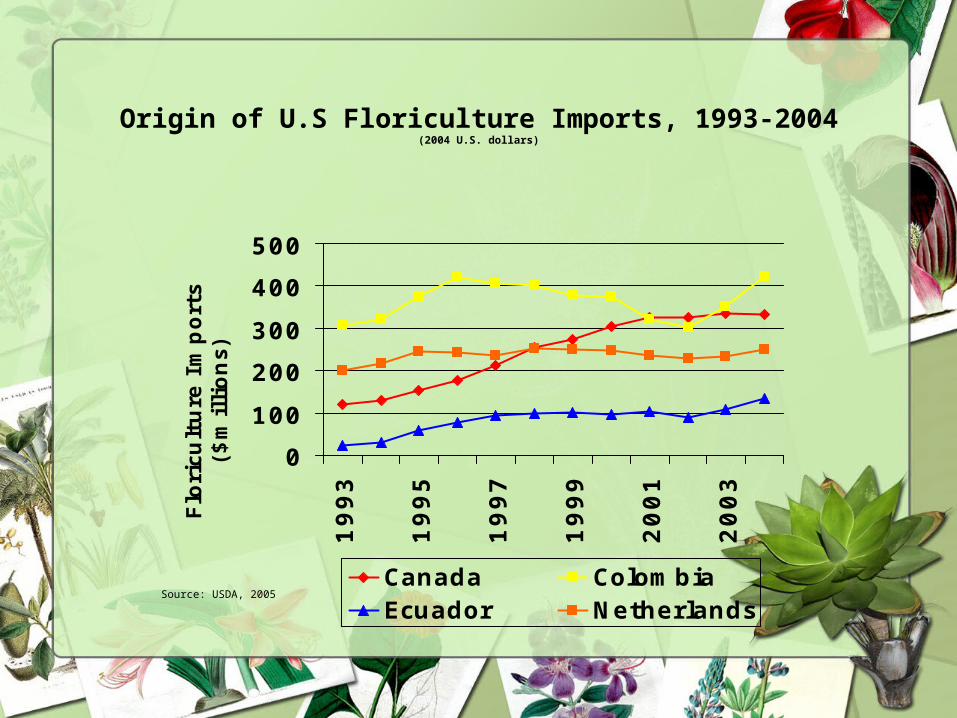

Origin of U.S Floriculture Imports, 1993-2004(2004 U.S. dollars)

0

100

200

300

400

500

19

93

19

95

19

97

19

99

20

01

20

03

Flo

ricu

ltu

re I

mp

ort

s ($

million

s)

Canada ColombiaEcuador Netherlands

Source: USDA, 2005

Cut Flowers and Nursery Stock Share of U.S. Imports, 1992-2004

0

1020

30

40

5060

70

1992

1994

1996

1998

2000

2002

2004

Perc

enta

ge o

f Im

port

s

Cut Flowers Nursery StockSource: USDA, 2005

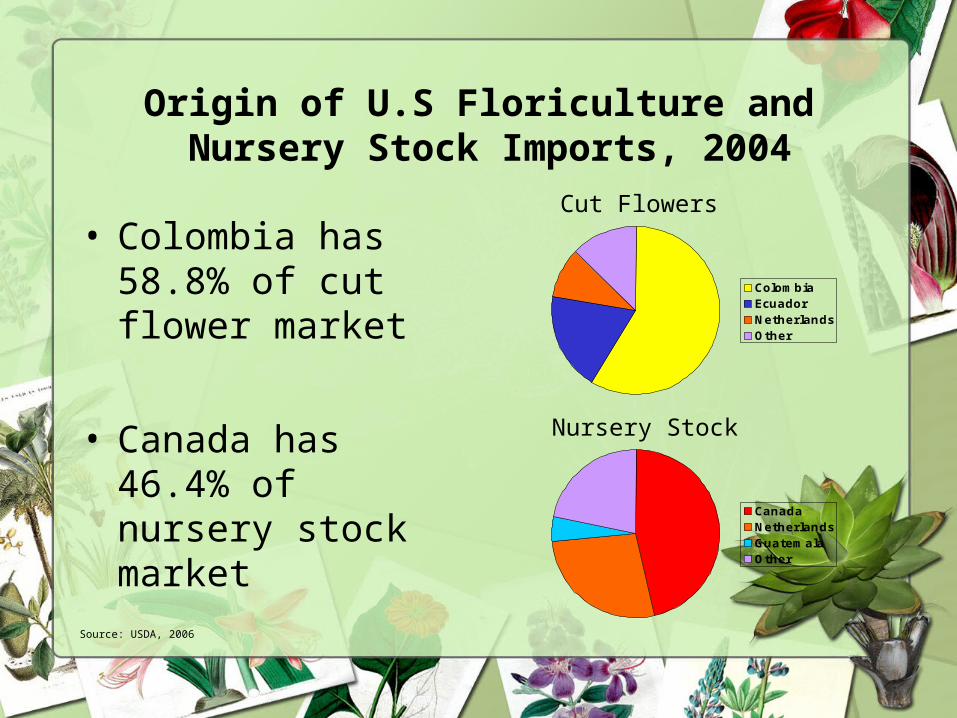

Origin of U.S Floriculture and Nursery Stock Imports, 2004

• Colombia has 58.8% of cut flower market

• Canada has 46.4% of nursery stock market

ColombiaEcuadorNetherlandsOther

CanadaNetherlandsGuatemalaOther

Source: USDA, 2006

Cut Flowers

Nursery Stock

Canadian Competition

Canada-U.S Floriculture Trade,1992-2004

• Canada’s trade surplus with the U.S. in floriculture products increased from $1.5 million to $35.3 million

0

10000000

20000000

30000000

40000000

50000000

60000000

70000000

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

$U

S

CAN>US US>CAN

Source: Industry Canada 2006

Imports by State*

*States accounted for 64% of US total in 2004.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

1,00

0's

of U

S D

olla

rs New York

Michigan

Washington

Massachusetts

Maine

New Jersey

Exports by Province*

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

1,00

0's

of D

olla

rs Total

Ontario

British Columbia

New Brunsw ick

Quebec

*Provinces accounted for 96% of total in 2004.

Changing Import Patterns

Causes of Growing Canadian Imports

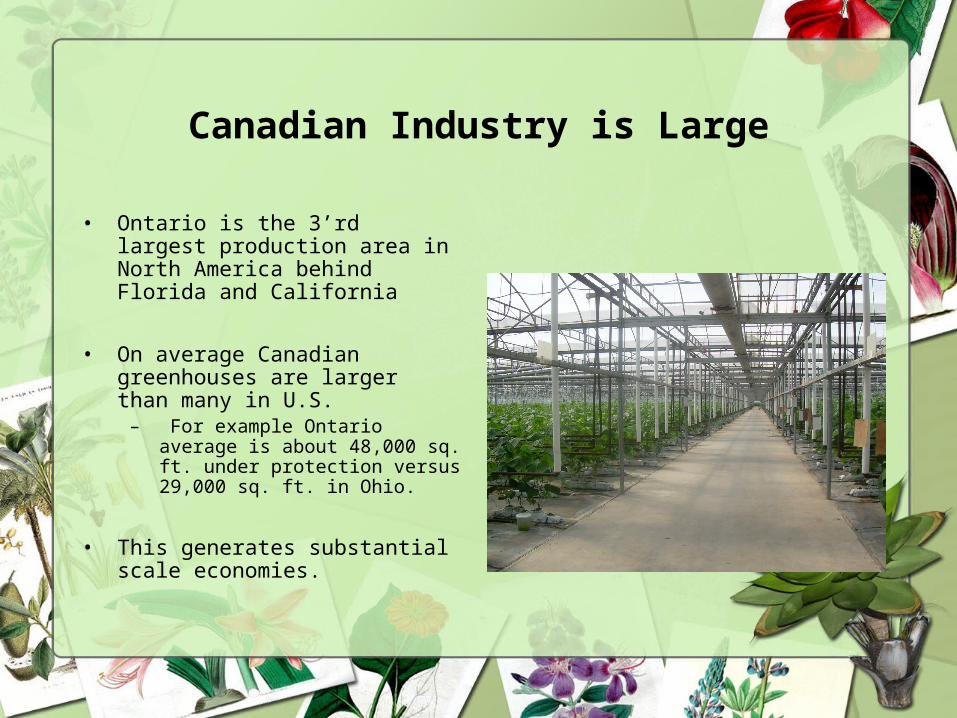

Canadian Industry is Large

• Ontario is the 3’rd largest production area in North America behind Florida and California

• On average Canadian greenhouses are larger than many in U.S.

– For example Ontario average is about 48,000 sq. ft. under protection versus 29,000 sq. ft. in Ohio.

• This generates substantial scale economies.

Southern Ontario

• Good location.

• 50% of U.S. urban population within 8 hour drive.

U.S. Growers

A grower invested little profits back into the family business. He was complacent. He had halfhearted promotions and short hours. The greenhouse layout, lighting, displays and merchandising were virtually unchanged since construction. He was slow to incorporate new trends and follow customers’ changing needs and preferences.”

Greenhouse Product News, 2006

Canadian Ownership

“The Ontario Greenhouse Alliance’s vision is to provide an infrastructure and approach that will integrate all the current resources and future potential of the Ontario greenhouse stakeholders into a community and international marketplace presence, with the synergy and standards to be a world leader in greenhouse operations”

The Ontario Greenhouse Alliance

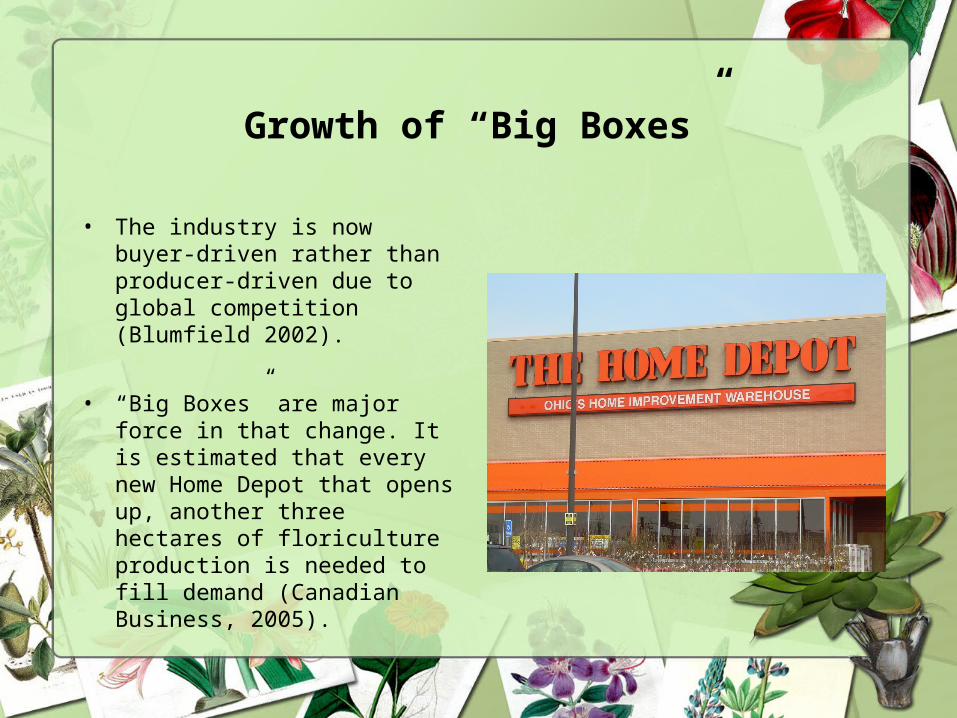

Growth of “Big Boxes”

• The industry is now buyer-driven rather than producer-driven due to global competition (Blumfield 2002).

• “Big Boxes” are major force in that change. It is estimated that every new Home Depot that opens up, another three hectares of floriculture production is needed to fill demand (Canadian Business, 2005).

Growth of Home Depot

0

500

1000

1500

2000

25001

97

9

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

Sto

re N

um

be

rs

Growth of “Big Box” Retailers

Conclusions

Market Segmentation

• Growers are increasingly being segmented into those producing for the big chain stores, and those who direct market or sell to independent garden centers.

• Canadian imports are major competitor in the “big box” market.

Impact of Competition

• Northwest Ohio greenhouse industry

– Next 5 years

• 40% - industry less profitable

• 15% planning to downsize or close

Source: Grower Survey 2004

Continued Import Growth

• Continued growth of Canadian imports can be expected.

• Those imports are a major driver in moving the industry to being a buyer-driven supply chain and fostering the transition of the industry from a “cottage industry” to a large-scale commercial agricultural industry.

Trade Barriers

• In contrast to other industries, NAFTA has had little impact on this trade.

• Instead currency exchange rates and border issues related to Homeland Security seem to be more influential.

Acknowledgements

• This research is funded by the following grants from the U.S. Department of Agriculture:

– CSREES 2003-06230

– CSREES 2004-06222

– CSREES 2005-06269