the ifc corporate governance methodology: application...

TRANSCRIPT

1

THE IFC CORPORATE GOVERNANCE

METHODOLOGY:Application to Financial

Institutions

Investor and Corporate PracticeCorporate Governance Department

2

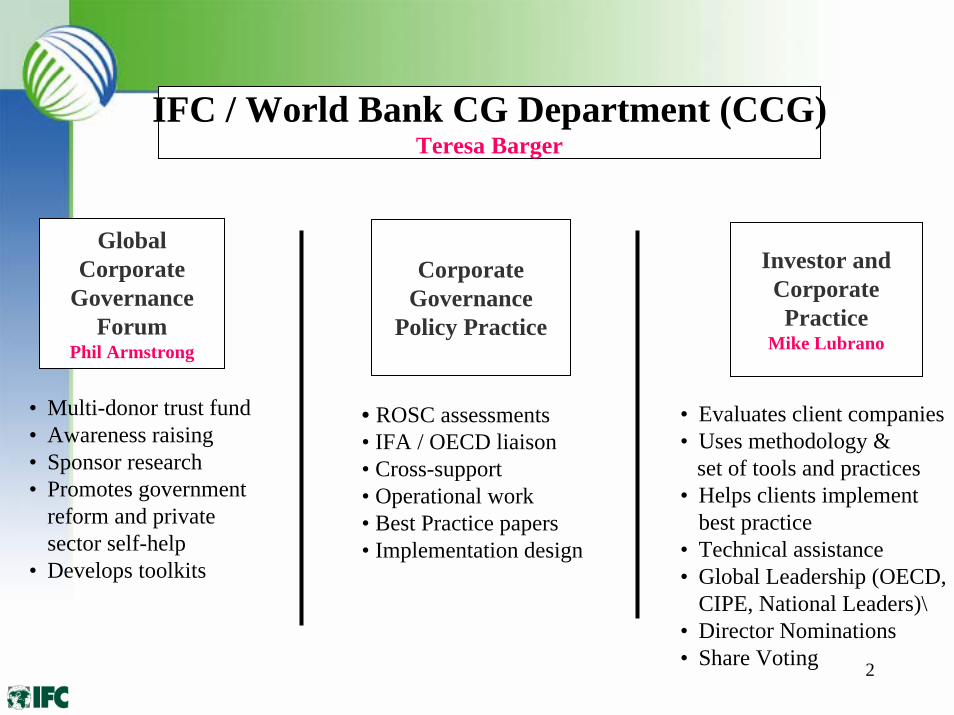

Investor and Corporate Practice

Mike Lubrano

• Evaluates client companies• Uses methodology &

set of tools and practices• Helps clients implement

best practice• Technical assistance• Global Leadership (OECD,

CIPE, National Leaders)\• Director Nominations• Share Voting

• ROSC assessments• IFA / OECD liaison• Cross-support• Operational work• Best Practice papers • Implementation design

• Multi-donor trust fund• Awareness raising• Sponsor research• Promotes government

reform and private sector self-help

• Develops toolkits

Corporate Governance

Policy Practice

Global Corporate

Governance Forum

Phil Armstrong

IFC / World Bank CG Department (CCG)Teresa Barger

3

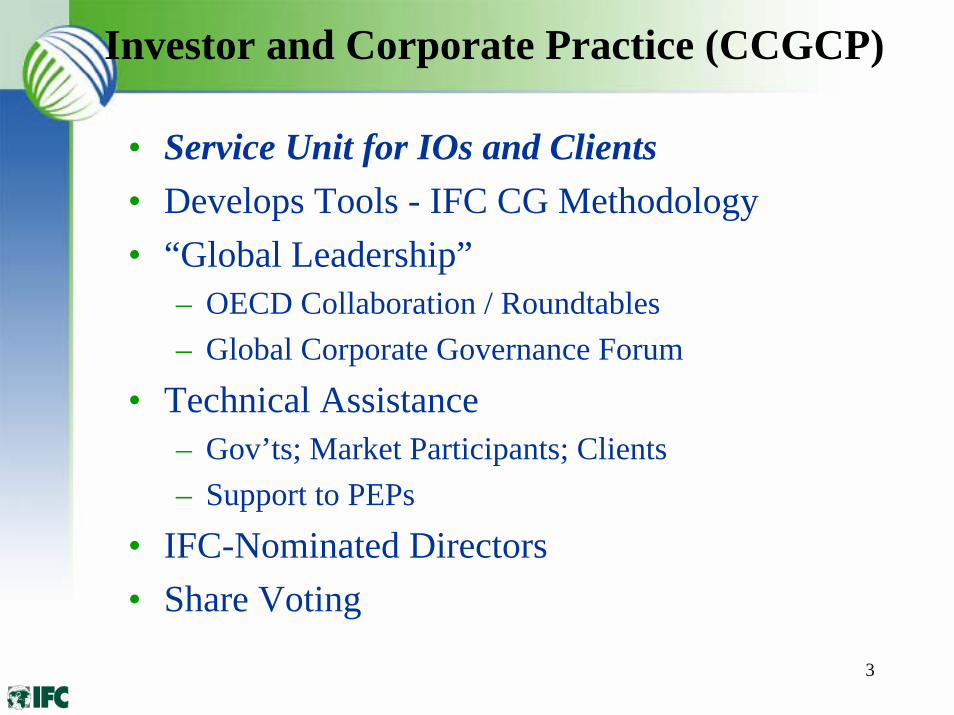

Investor and Corporate Practice (CCGCP)

• Service Unit for IOs and Clients• Develops Tools - IFC CG Methodology• “Global Leadership”

– OECD Collaboration / Roundtables– Global Corporate Governance Forum

• Technical Assistance– Gov’ts; Market Participants; Clients– Support to PEPs

• IFC-Nominated Directors• Share Voting

4

IFC Portfolio – Types of Companies

• Approximately 250 New Commitments Per Year; 1500 Portfolio Companies

• Existing Publicly-Listed / Unlisted Companies (All Industrial Sectors and Financial Sector)

• Unlisted Founder / Family Controlled Enterprises (Board = Shareholders = Managers)

• Privatizations and Newly-Privatized• Three-way Joint Ventures (Board =

Shareholders Meeting)

5

Why Does IFC Care About CG?

• Portfolio Performance– Poor Governance Increases Risk– Improving Governance is a Value Proposition

(Private Equity Funds; BCR; Hikma)• Development Mission (Sustainable

Development – Along with Social, Environmental,and other Elements of Sustainability)

• Reputational Risk / Reputational Agent

6

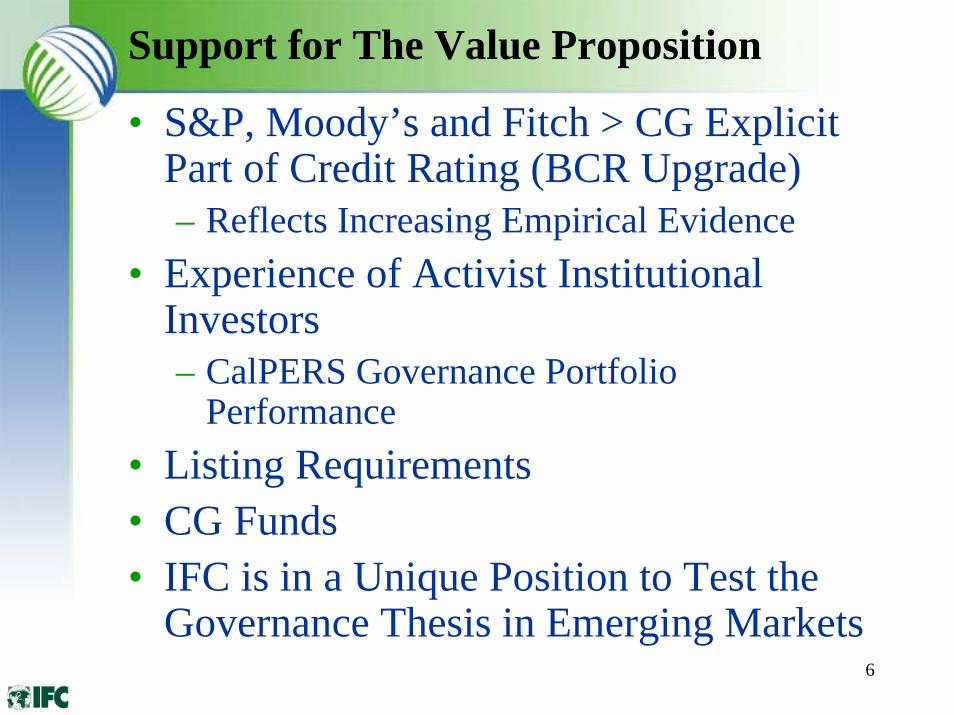

Support for The Value Proposition

• S&P, Moody’s and Fitch > CG Explicit Part of Credit Rating (BCR Upgrade)– Reflects Increasing Empirical Evidence

• Experience of Activist Institutional Investors– CalPERS Governance Portfolio

Performance• Listing Requirements • CG Funds• IFC is in a Unique Position to Test the

Governance Thesis in Emerging Markets

7

Developing a Workable Methodology

• Create a Common Definition/Vocabulary• Be Consistent with the IFC Mission:

Sustainability / Value Added• Tailored to Institution’s Unique and

Diverse Portfolio• Fit with Existing Operating Procedures

(Project Prep and Decision Meetings)– Bank Evaluation Model / Due Diligence

• Usable and Accessible to IOs (website)• Avoid Formalism / Box Ticking

8

CG is a Natural Fit for IFC• Participation in Governance Worldwide in All

Types of Companies, Industries – Access to Data– Skills, Experience to Deliver

• “Grass Roots”/PEP Projects– Bank Governance Projects in Ukraine and Russia

• Capital Markets Development Focus• Global Partners

– OECD– Global CG Forum / Private Sector Adv. Group– Regional Partners– National advocacy, business schools, training institutes

• IFC-Nominated Directors

9

What is a Workable Definition for Us?

OECD Principles Provide an accepted/supported Framework:

• Financial Stakeholders (e.g., Shareholders)

• Checks and Balances (Boards of Directors)

• Control Environment• Transparency and

Disclosure

A Practical Investment-Driven Definition

Distinguish from:• Corporate Citizenship• Corporate Social

Responsibility• Socially Responsible

Investing• Other Elements of

Sustainability• Political Governance• Business Ethics• Anti-Corruption / AML

(But CG does reinforce all of these!!!)

10

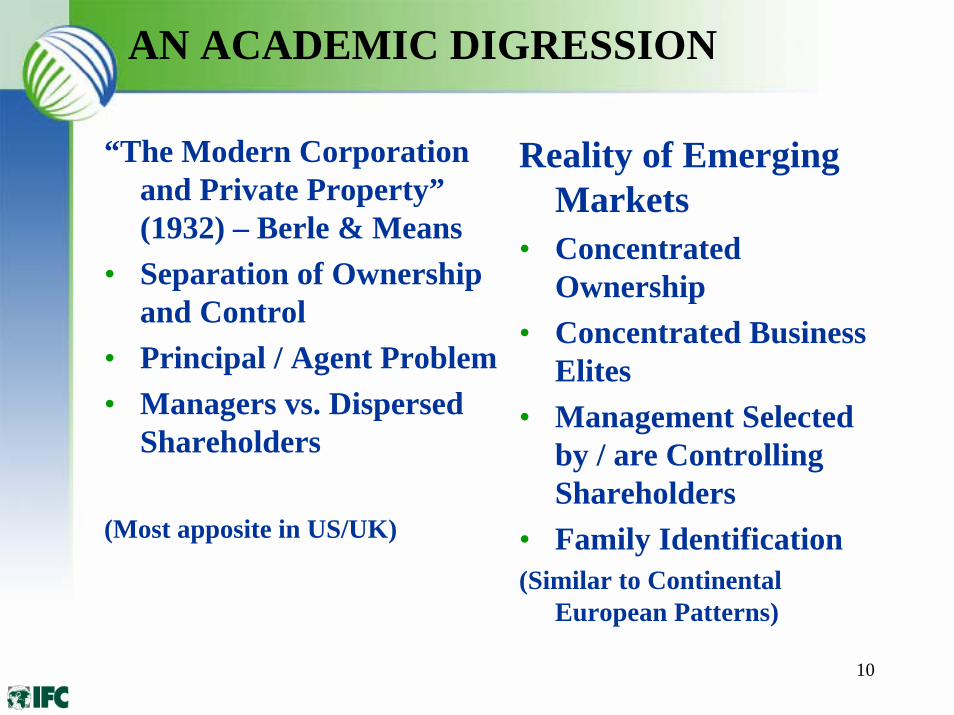

AN ACADEMIC DIGRESSION

“The Modern Corporation and Private Property”(1932) – Berle & Means

• Separation of Ownership and Control

• Principal / Agent Problem• Managers vs. Dispersed

Shareholders

(Most apposite in US/UK)

Reality of Emerging Markets

• Concentrated Ownership

• Concentrated Business Elites

• Management Selected by / are Controlling Shareholders

• Family Identification(Similar to Continental

European Patterns)

11

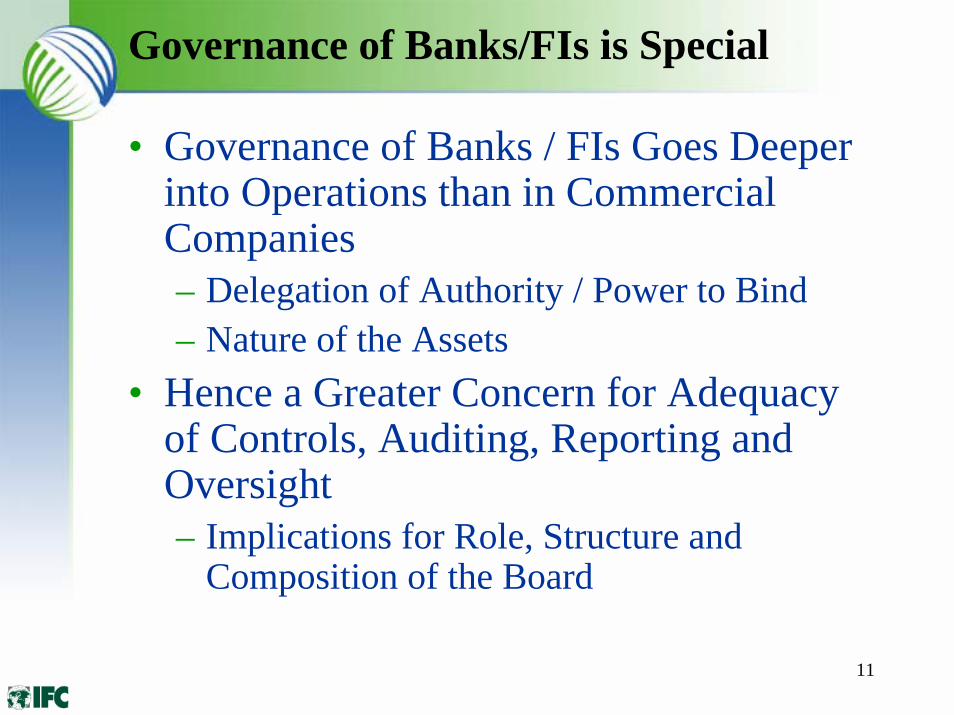

Governance of Banks/FIs is Special

• Governance of Banks / FIs Goes Deeper into Operations than in Commercial Companies– Delegation of Authority / Power to Bind– Nature of the Assets

• Hence a Greater Concern for Adequacy of Controls, Auditing, Reporting and Oversight– Implications for Role, Structure and

Composition of the Board

12

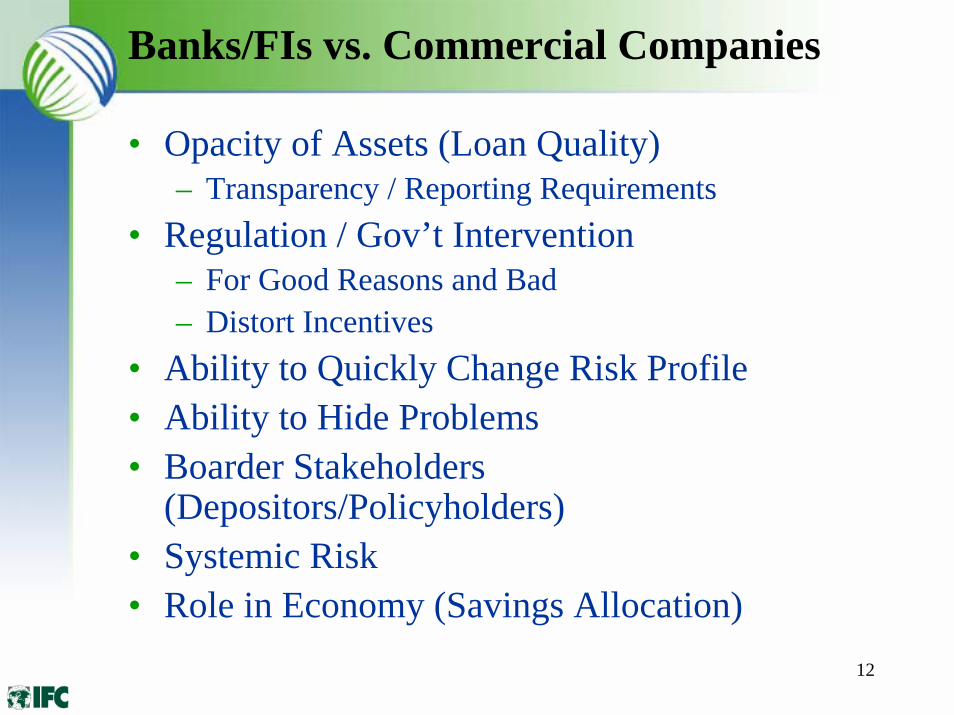

Banks/FIs vs. Commercial Companies

• Opacity of Assets (Loan Quality) – Transparency / Reporting Requirements

• Regulation / Gov’t Intervention– For Good Reasons and Bad– Distort Incentives

• Ability to Quickly Change Risk Profile• Ability to Hide Problems• Boarder Stakeholders

(Depositors/Policyholders)• Systemic Risk• Role in Economy (Savings Allocation)

13

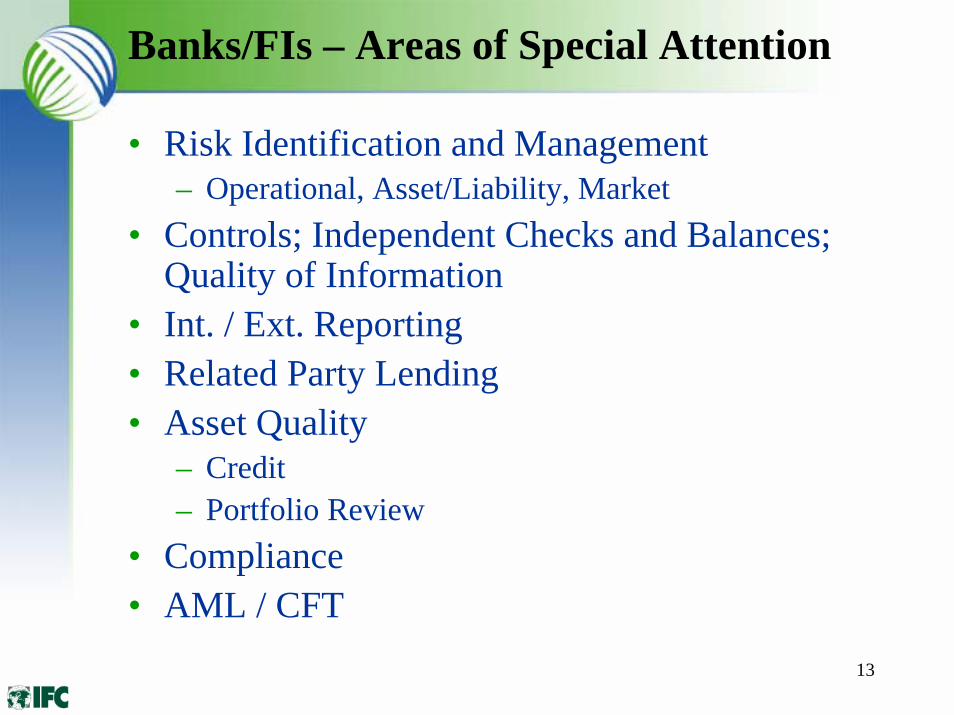

Banks/FIs – Areas of Special Attention

• Risk Identification and Management– Operational, Asset/Liability, Market

• Controls; Independent Checks and Balances; Quality of Information

• Int. / Ext. Reporting• Related Party Lending• Asset Quality

– Credit– Portfolio Review

• Compliance• AML / CFT

14

FIs – The Structural Dimension

• Role of the Board– Balance of Strategic and Oversight Roles– Defining Role of Board vs. Management– Executing Board’s Responsibility; Committee Structure– Management vs. Board vs. Mixed Committees

• Accountability / Checks at Key Functions– Credit– Compliance– Portfolio / Asset Quality– Risk Management– Accounting / Auditing,Controls, Int/Ext Reporting

• Responsibilities of Boards, Bd. Committees, Management at Holding and Sub. Levels

• Human Resource Limitations May Drive Structure, Procedures!!!

• GFM/CCGCP Bank Governance Toolkit

15

Making Methodology Useable by IOs

Break Governance Into Digestible Bits• Company archetypes, paradigms (non-exclusive):

– Listed companies– Family- or Founder-Owned Unlisted Companies – Financial Institutions– Transition Economy Companies

• Five attributes of effectiveness.

• Four levels, from “acceptable” to “leadership.” We call this our Progression Matrix. This approach parallels the approach taken in the other areas of sustainability (social and environmental).

16

Fit with the Appraisal / Supervision Process

How should staff evaluate client companies and work with them to add value to their governance?

By following a series of steps -- from first impressions to follow-up -- that fit into existing appraisal / supervision patterns

The time and effort involved in each step varies in nature depending on the type of enterprise – listed companies, family/founder firms, financial institutions, and companies in Transition economies (the paradigms).

The intensity of project team effort depends on risk and opportunity.

17

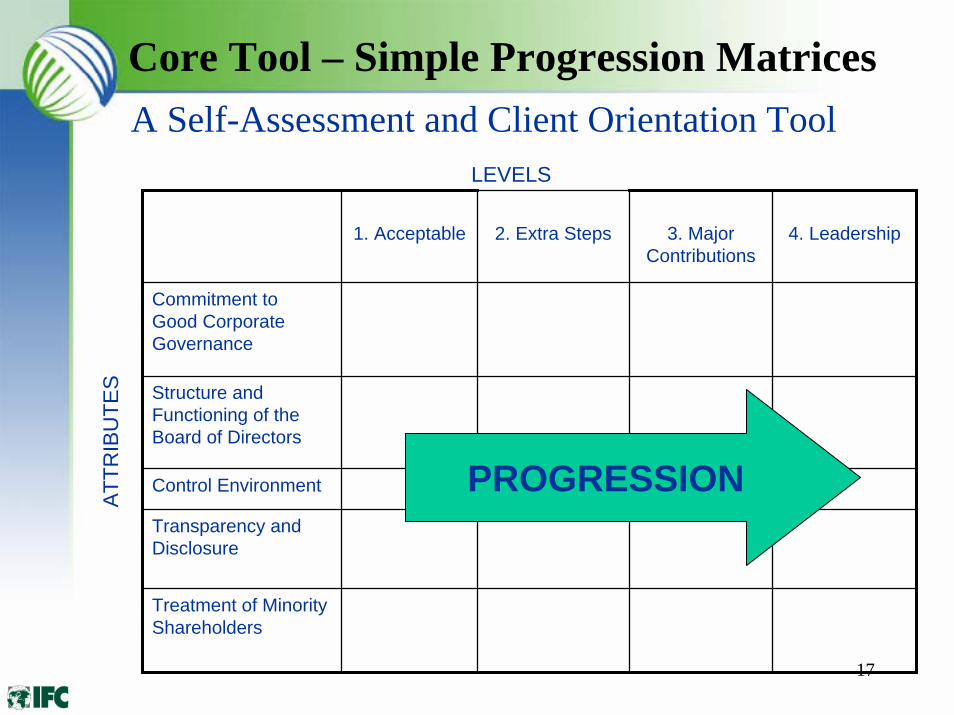

Core Tool – Simple Progression MatricesA Self-Assessment and Client Orientation Tool

1. Acceptable 2. Extra Steps 3. Major Contributions

4. Leadership

Commitment to Good Corporate Governance

Structure and Functioning of the Board of Directors

Control Environment

Transparency and Disclosure

Treatment of Minority Shareholders

LEVELS

ATTR

IBU

TES

PROGRESSION

18

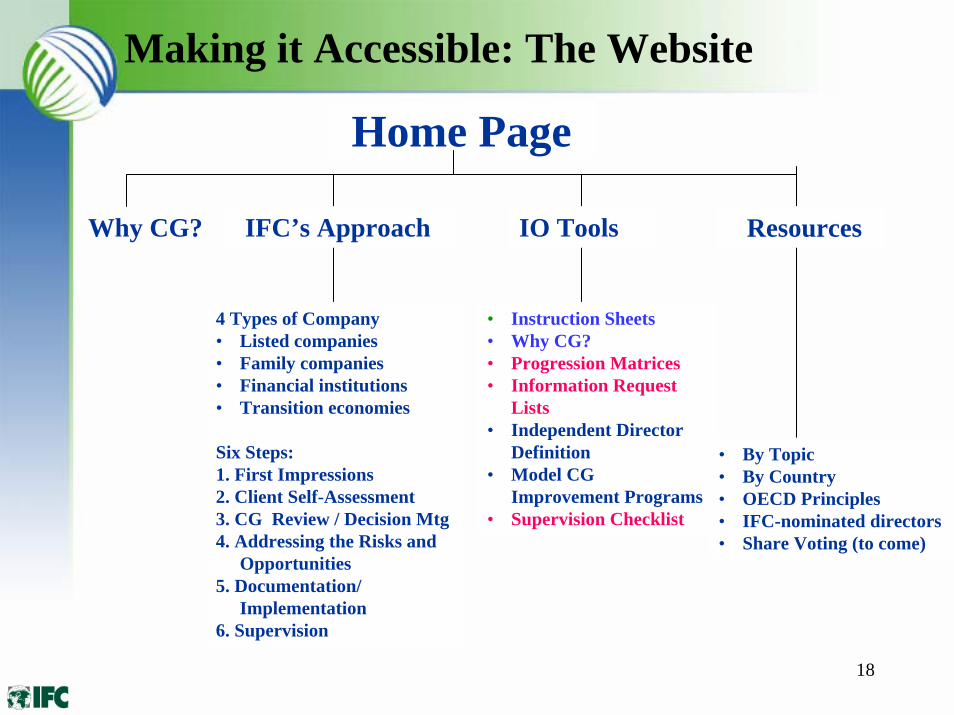

Making it Accessible: The Website

Home Page

Why CG? IFC’s Approach IO Tools Resources

4 Types of Company• Listed companies• Family companies• Financial institutions• Transition economies

Six Steps:1. First Impressions2. Client Self-Assessment3. CG Review / Decision Mtg4. Addressing the Risks and

Opportunities 5. Documentation/

Implementation6. Supervision

• Instruction Sheets• Why CG?• Progression Matrices• Information Request

Lists • Independent Director

Definition• Model CG

Improvement Programs• Supervision Checklist

• By Topic• By Country• OECD Principles• IFC-nominated directors• Share Voting (to come)

19

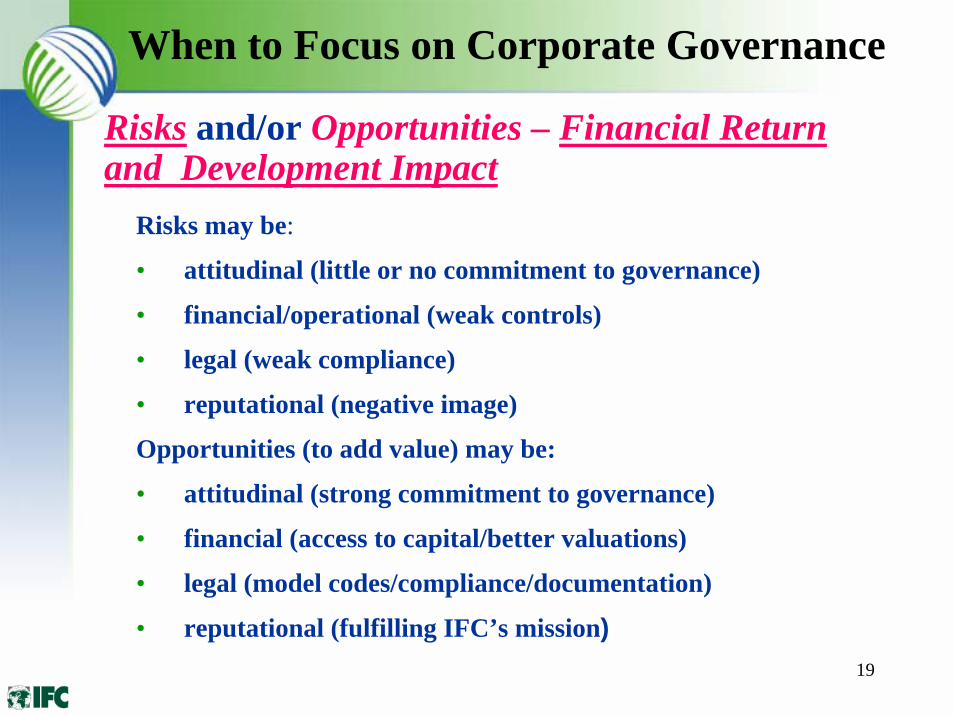

When to Focus on Corporate Governance

Risks and/or Opportunities – Financial Return and Development Impact

Risks may be:

• attitudinal (little or no commitment to governance)

• financial/operational (weak controls)

• legal (weak compliance)

• reputational (negative image)

Opportunities (to add value) may be:

• attitudinal (strong commitment to governance)

• financial (access to capital/better valuations)

• legal (model codes/compliance/documentation)

• reputational (fulfilling IFC’s mission)

20

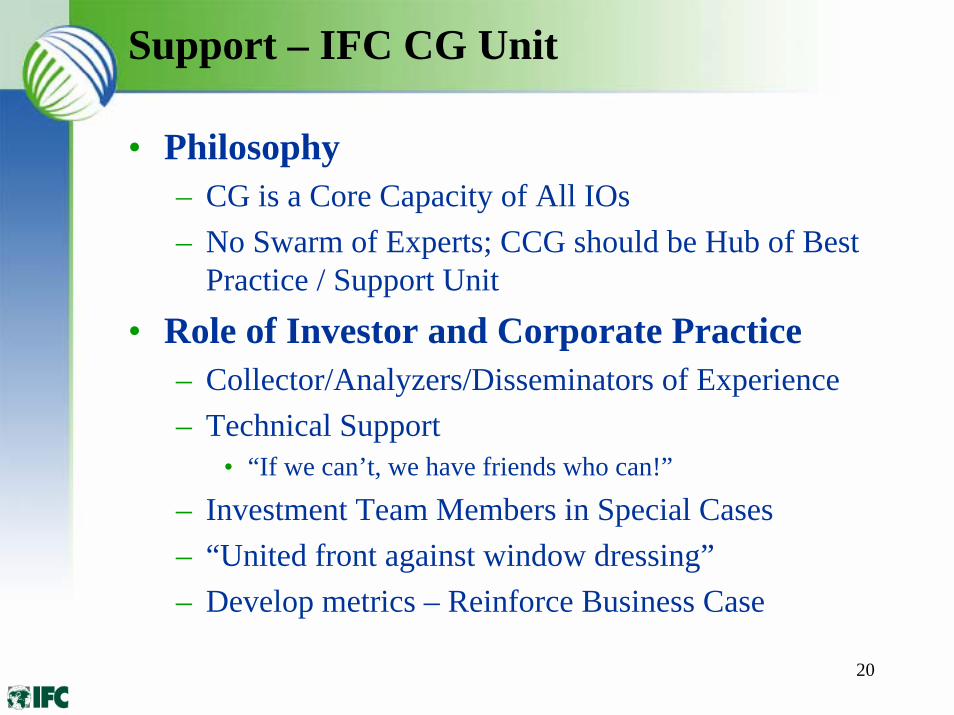

Support – IFC CG Unit

• Philosophy– CG is a Core Capacity of All IOs– No Swarm of Experts; CCG should be Hub of Best

Practice / Support Unit

• Role of Investor and Corporate Practice– Collector/Analyzers/Disseminators of Experience– Technical Support

• “If we can’t, we have friends who can!”

– Investment Team Members in Special Cases– “United front against window dressing”– Develop metrics – Reinforce Business Case

21

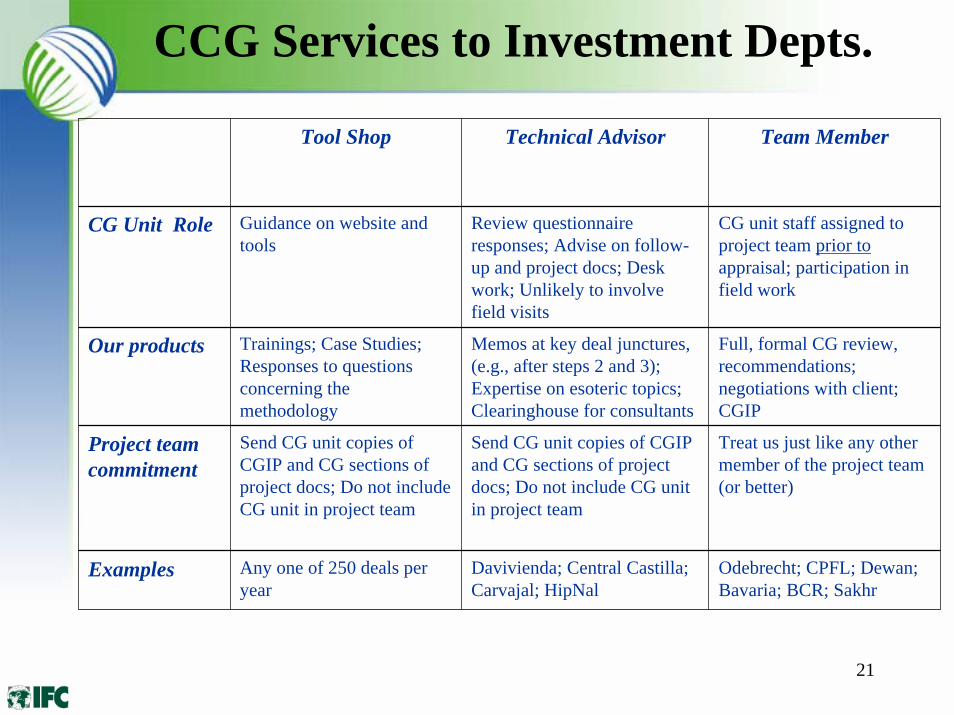

CCG Services to Investment Depts.

Tool Shop Technical Advisor Team Member

CG Unit Role Guidance on website and tools

Review questionnaire responses; Advise on follow-up and project docs; Desk work; Unlikely to involve field visits

CG unit staff assigned to project team prior toappraisal; participation in field work

Our products Trainings; Case Studies; Responses to questions concerning the methodology

Memos at key deal junctures, (e.g., after steps 2 and 3); Expertise on esoteric topics; Clearinghouse for consultants

Full, formal CG review, recommendations; negotiations with client; CGIP

Project team commitment

Send CG unit copies of CGIP and CG sections of project docs; Do not include CG unit in project team

Send CG unit copies of CGIP and CG sections of project docs; Do not include CG unit in project team

Treat us just like any other member of the project team (or better)

Examples Any one of 250 deals per year

Davivienda; Central Castilla; Carvajal; HipNal

Odebrecht; CPFL; Dewan; Bavaria; BCR; Sakhr

22

How IFC works with clients on Governance

Use the CG Tools

• CG Progression Matrices

• Instruction Sheets

• CG Information Request Lists

• Why Corporate Governance?

• Sample CG Improvement Programs

• Indicative Independent Director Definition

• Supervision Checklist

23

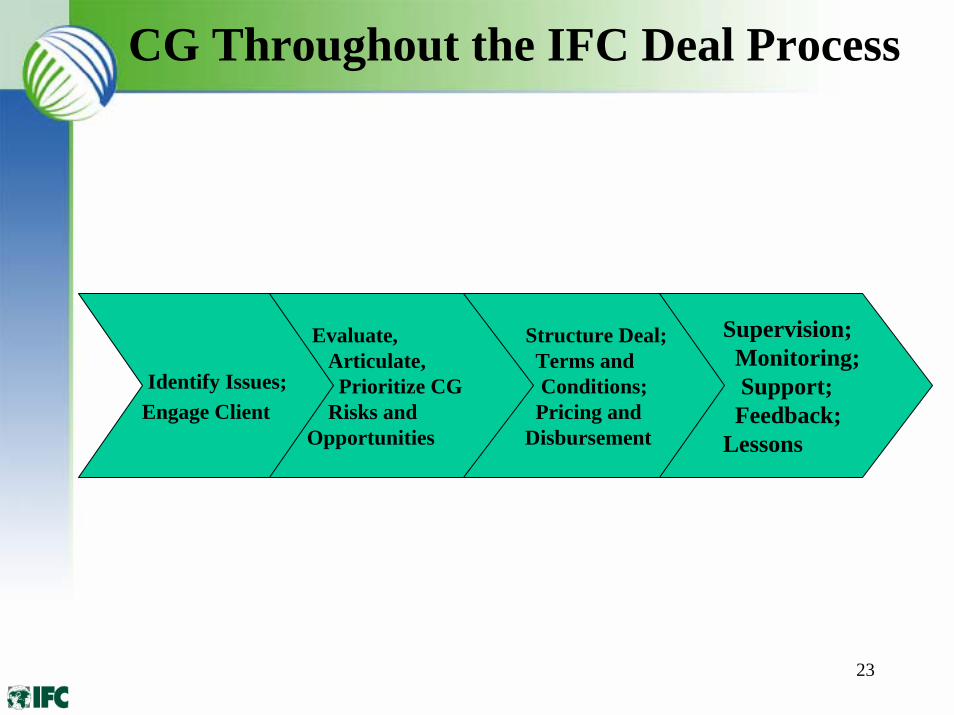

CG Throughout the IFC Deal Process

Supervision;Monitoring;Support;Feedback;

Lessons

Structure Deal;Terms and Conditions;Pricing and

Disbursement

Evaluate, Articulate,Prioritize CG

Risks and Opportunities

Identify Issues;Engage Client

24

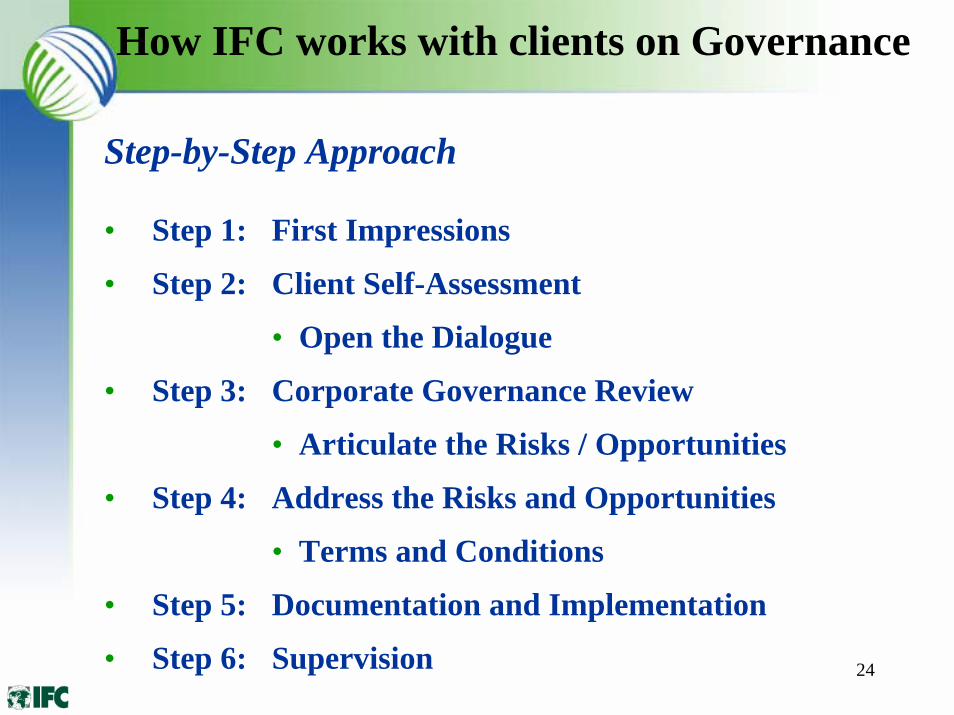

How IFC works with clients on Governance

Step-by-Step Approach

• Step 1: First Impressions

• Step 2: Client Self-Assessment

• Open the Dialogue

• Step 3: Corporate Governance Review

• Articulate the Risks / Opportunities

• Step 4: Address the Risks and Opportunities

• Terms and Conditions

• Step 5: Documentation and Implementation

• Step 6: Supervision

25

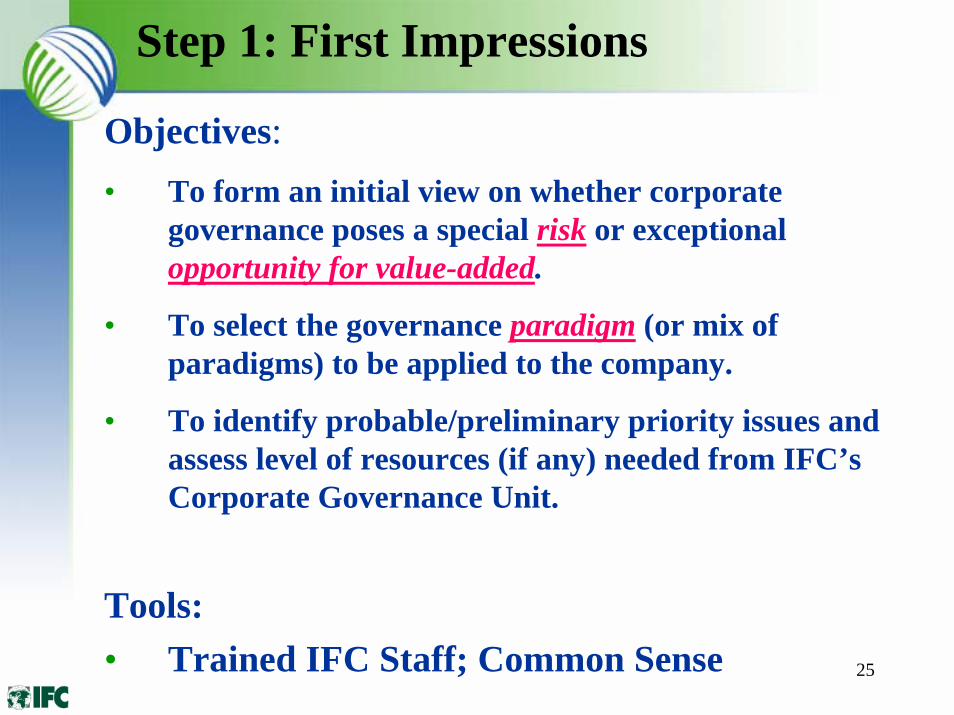

Step 1: First Impressions

Objectives:• To form an initial view on whether corporate

governance poses a special risk or exceptional opportunity for value-added.

• To select the governance paradigm (or mix of paradigms) to be applied to the company.

• To identify probable/preliminary priority issues and assess level of resources (if any) needed from IFC’s Corporate Governance Unit.

Tools: • Trained IFC Staff; Common Sense

26

Step 2: Client Self-Assessment

Objectives:Introduce our Corporate Governance Methodology

Develop Governance Consciousness

Orient the client about our definition of, and approach to, corporate governance

Guide the client in assessing its own governance, using the Progression Matrices

Tools:“Why Corporate Governance?”

Corporate Governance Progression Matrix

27

Step 3: Corporate Governance Review

Objectives:An informed analysis of the client company’s governance

On-site evaluation with the company’s senior managers

Help the company understand strengths and weaknesses of its own governance in a structured way

Decide whether the client needs to undertake a Corporate Governance Improvement Program

Identify any need for further resources, e.g., additional support from IFC’s Corporate Governance Unit

Tools:Corporate Governance Progression Matrix

Information Request List

Conscientious Department Directors!!!

28

Step 4: Addressing Risks / Opportunities

Objectives:Reflect Assessment in Structuring of Deal

Terms and Conditions - A program of specific practical and meaningful improvements

Achieve client “buy-in”

Agree on a timetable and methods for implementation

Identify areas where IFC can help

Tools:Sample CG Improvement Programs

Numerous other Resources on specific topics or countries, e.g. Independent Director Definition, Exchange Listing Rules

Serious Department Directors!!!

29

Sample Diagnoses - Responses

• Concentrated Ownership Issues

• Minority Shareholder Mistreatment

• Founder/Family Business Issues

• Conflicts of Interest• Ineffective Boards

– Poor Capacity– Passive Approach

• Transparency– Internal Controls– Audit Function

• Clearly Articulated Shareholder Treatment Policies

• Strengthen Boards • Succession Planning• Committees and other

mechanisms to handle conflicts

• Audit Committees– Internal Audit– Financial Professionals

• Accounting and Auditing Improvements

30

Step 5: Documentation and Implementation

Objectives:

Memorialize what is agreed

Decide upon the appropriate form of legal enforceability of the CG Commitments

Identify need for continuing assistance

Tools:

Sample CG Improvement Programs; Company Codes; Term Sheets; Loan Covenants; Shareholders Agreements

31

Step 6: Supervision

Objectives:Adherence to the agreed Terms and Conditions / Agreed CG Improvements

Identify further corporate governance assistance from IFC and outsiders (e.g., consultants, director sourcing/training, etc.)

Communicate Quality to the Markets: Disseminate good examples for wider development influence/impact

Feedback on effectiveness of the Methodology / Individual CG Improvement Program

Tools:• Supervision Checklist

32

Bank Gov. Tool Kit Bank Gov. Tool Kit -- PurposePurpose

• To Complement the “Financial Institutions” Component of the IFC CG Methodology– GFM’s Non-Business Specific Questionnaire

• To Drill Deeper into Best Practices for Boards and Senior Management of Financial Institutions– Appraisal– TA Projects

• To Suggest Specific Paths for Improvement– More Value-Added

33

Bank Gov. Toolkit - Phase One

• Board Charter• Audit Committee• Compensation Committee• Nomination/CG Committee• Risk Policy Committee• Code of Ethics

Completed

34

Bank Gov. Toolkit - Phase Two

• CEO / President ToR• Chief Compliance Officer ToR and

Reporting• Chief Risk Officer ToR and Reporting• Head of Internal Audit ToR and

Reporting

• Training Module• Dissemination – CCGCP Website / GFM?

Completion Date – June 30, 2006

35

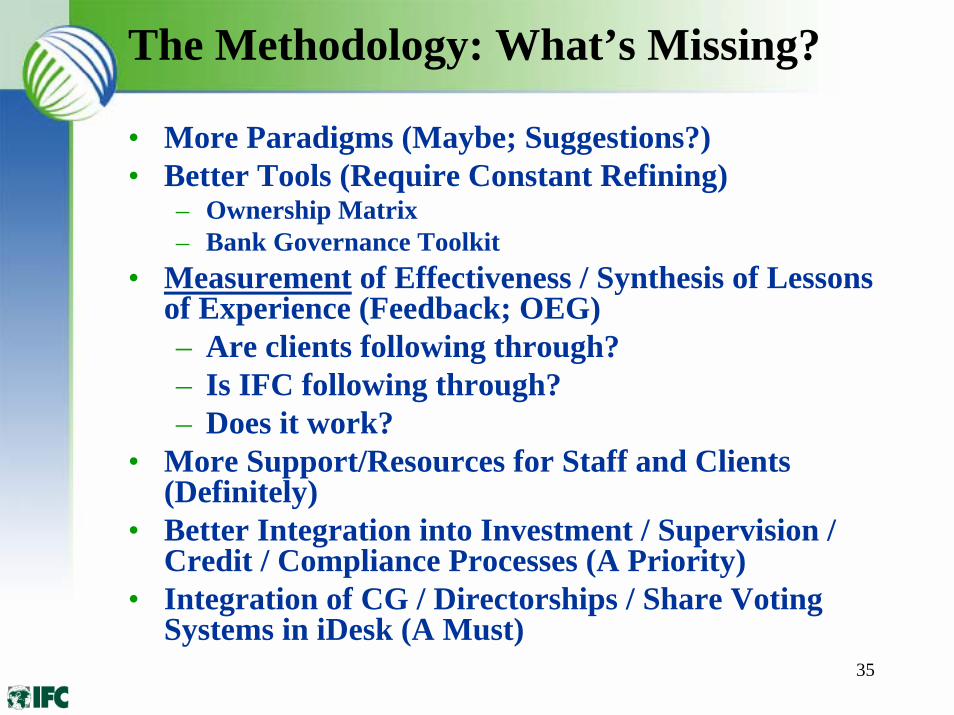

The Methodology: What’s Missing?

• More Paradigms (Maybe; Suggestions?)• Better Tools (Require Constant Refining)

– Ownership Matrix– Bank Governance Toolkit

• Measurement of Effectiveness / Synthesis of Lessons of Experience (Feedback; OEG)– Are clients following through?– Is IFC following through?– Does it work?

• More Support/Resources for Staff and Clients (Definitely)

• Better Integration into Investment / Supervision / Credit / Compliance Processes (A Priority)

• Integration of CG / Directorships / Share Voting Systems in iDesk (A Must)