the growth of finance, financial innovation, and systemic risk lecture 2 bgse summer school in...

TRANSCRIPT

The Growth of Finance, Financial Innovation, and

Systemic Risk

Lecture 2

BGSE Summer School in Macroeconomics, July 2013

Nicola Gennaioli, Universita’ Bocconi, IGIER and CREI

The Size of Finance2

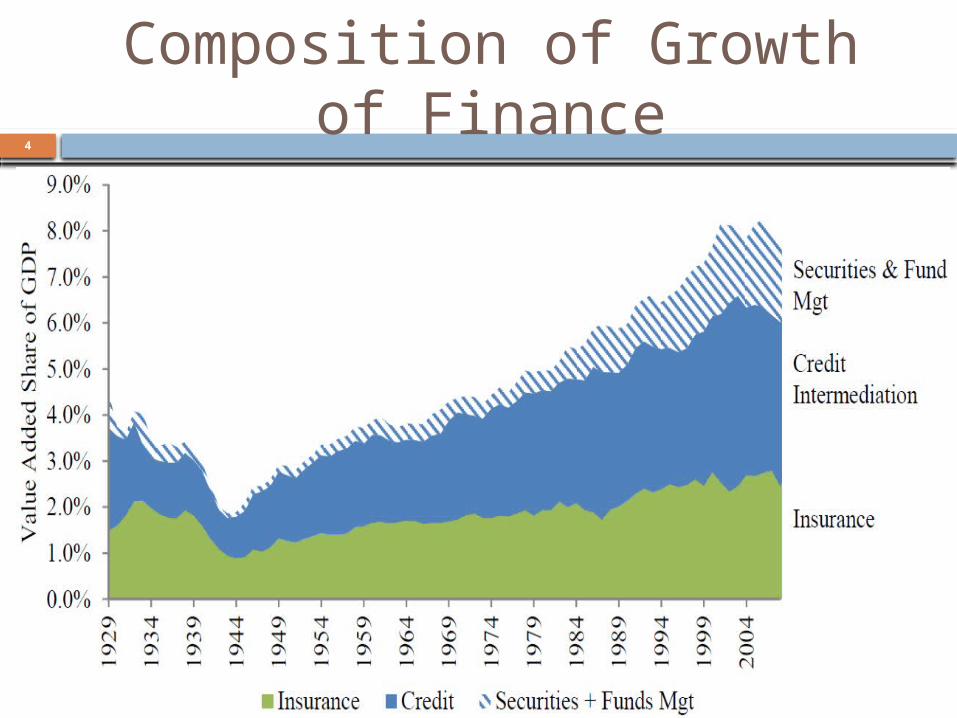

Astonishing rise of the share of U.S. GDP coming from the financial sector since World War II (Philippon 2012)

This pattern is common to many other countries (Philippon and Reshef 2013)

Much of this expansion comes from services to consumers such as asset management and credit intermediation (Philippon 2012, Greenwood and Scharfstein 2013)

The Size of Finance (cont’d)3

Composition of Growth of Finance

4

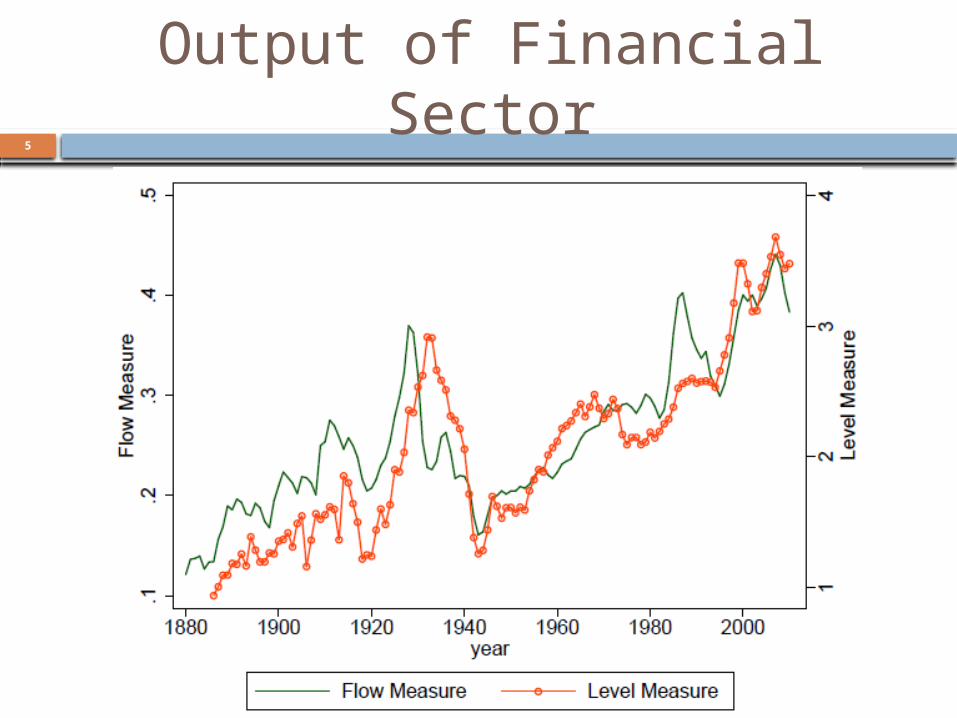

Output of Financial Sector5

Unit Cost of Finance (Income/Output)

6

The Size of Finance (cont’d)7

This growth has proven difficult to explain: Maybe relative cost of finance rose due to low

productivity. However, wages in finance grew faster than elsewhere.

Conventional explanations: socially unproductive innovation and rent seeking (e.g. Philippon 2012, Greenwood and Scharfstein 2013)

Source of Finance Income?

Key Question: Where do financial market players obtain their remuneration from?

Standard theory: remuneration to specific asset managers comes from their superior performance.

Problem: Professional money managers underperform passive strategies net of fees (Jensen 1968) Average mutual fund underperformance of 65 b.p. a

year. Investors pay substantial additional fees to brokers and

advisors.

8

Professional Money Management

9

Performance is only part of what managers seek to deliver Managers/advisors mostly advertise trust, dependability,

not past performance (Mullainathan et al. 2008). Some studies argue advisors provide intangible benefits or

“babysitting”

GSV’s “Money doctors” paper (2013) presents a model where this perspective is taken seriously.

Trust and Money Management

10

Key assumption: investors are too anxious to take risk on their own. They need to hire a manager they trust. Managers might have skills and knowledge, but in addition

they provide investors with comfort/peace of mind Finance is a service, and like many services is not only about

performance

Trust describes confidence in the manager based on: Personal relationships, familiarity, connections to friends and

colleagues, communication and schmoozing, advertising... Trust does not derive from past performance Trust is not only security from expropriation (Guiso, Sapienza,

Zingales, 2004, 2008) Analogy with medicine, another service

Main results

Each manager can charge fees to his trusting investors. Managers underperform the market net of fees. Fees are higher in riskier asset classes. Rational expectations: trust boosts risk taking

and welfare.

If investors erroneously think that some assets are “hot”: Trusted managers pander to beliefs to charge

higher fees. They let investors chase returns by proliferating

products Trust reduces the benefit of being contrarian by

reducing mobility of investors across differently performing managers

11

Finance and the Preservation of Wealth GSV (2013) “Finance and the Preservation of

Wealth” paper uses the idea of trust to study the growth of finance.

More benign view: the growth of finance is a natural by product of a maturing economy. Embody our previous model of asset management

(GSV 2012) into a Solow-style growth model with diminishing returns to capital

Use the model to shed light on the dynamics of intermediation, financial sector income, and the unit cost of finance

12

The Basic Mechanism13

Financial risk taking plays two functions: “Wealth preservation”: allows savers to move wealth forward “Growth”: allow savers to access growth opportunities

Key assumption (GSV 2012): Investors need trusted financial intermediaries to take advantage of these investments. On their own, people utilize inefficient self-storage ( e.g. cash in

mattresses or gold). Savers are willing to delegate risky investment to a trusted

intermediary (“money doctor”) who gives them peace of mind. Trust reduces the investor’s cost of bearing unfamiliar risks.

As the economy matures, K/Y rises. Savers are willing to pay more for wealth preservation. This drives growth of finance.

Roadmap

Basic Setup (Households, Money Managers, Production)

Equilibrium Analysis with a fixed number of money managers: Dynamics of the Capital Stock Predictions on the Dynamics of Finance Shocks to Trust and Productivity

Endogenous entry of intermediaries Dynamics of Fees and Unit Cost of Finance

14

Households

Overlapping generations of (measure 1 of) young and old Young at supply their unit labor at wage Wage is fully saved by investing in two assets:

Safe storage, which yields at time Risky asset yielding an average return and

variance

Risky investment needs management. If saver hires manager at fee , his consumption at is:

15

.

Households (cont’d)

Mean variance preferences over portfolio return:

Risk aversion is manager-specific and decreases in trust

Optimal delegated portfolio share with manager :

Decreases in fees, return from storage, risk Increases in expected return and trust

16

.

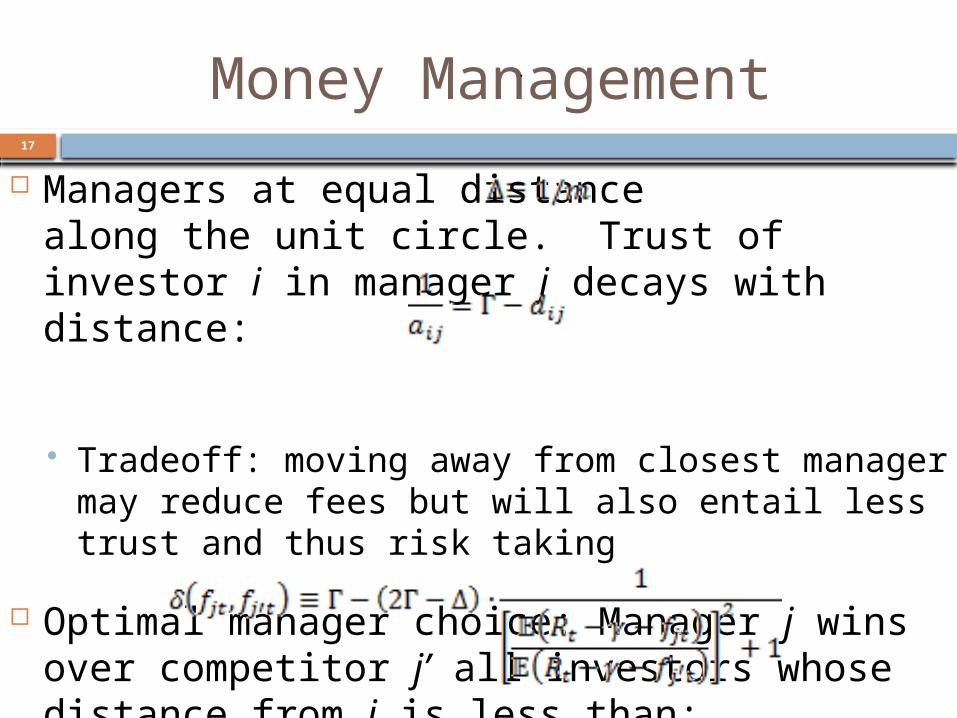

Money Management

Managers at equal distance along the unit circle. Trust of investor i in manager j decays with distance:

Tradeoff: moving away from closest manager may reduce fees but will also entail less trust and thus risk taking

Optimal manager choice: Manager j wins over competitor j’ all investors whose distance from j is less than:

17

.

Money Management (cont’d)

At symmetric equilibrium , the profit of j is equal to:

The optimal (equilibrium) fee is equal to:

Sharing rule: fee increases in excess return Falls in “generalized trust” , increases in

specific trust

18

.

Production

At t firms produce:

Value added plus un-depreciated capital : shock to value added and to capital stock,

and

Before learning , firms hire workers at fixed wage , and pledge to money managers (capital suppliers) the rest:

19

.

Production (cont’d)

Given the aggregate supplies and , equilibrium factor returns at time t are:

The variance of the risky return is

Key properties: The wage is the marginal product of labor The average return of the risky asset is 1 + the

average marginal product of capital

20

.

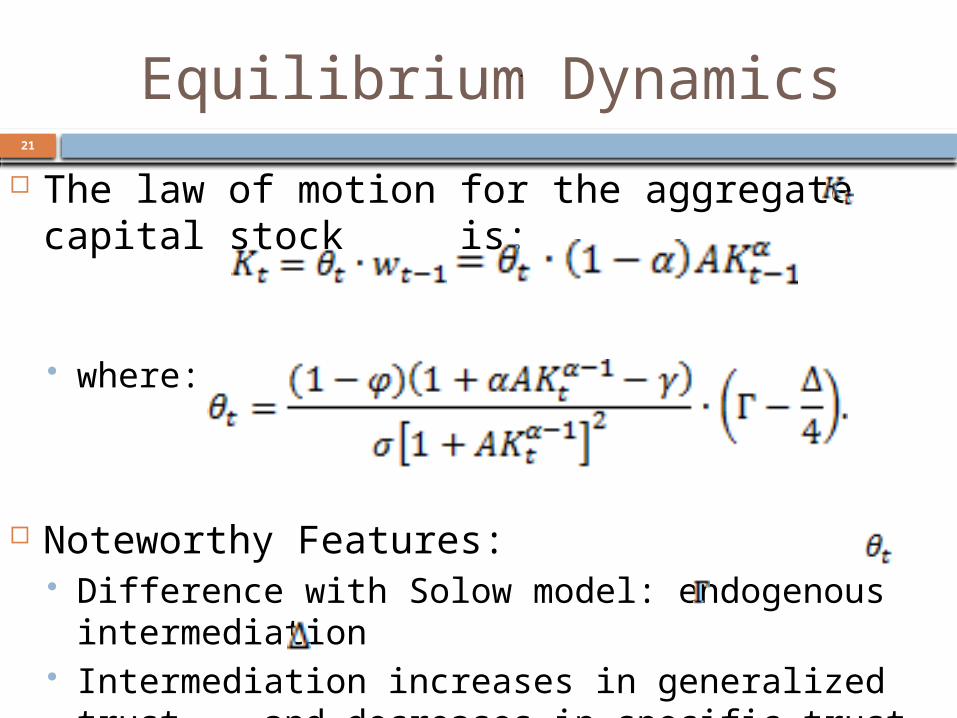

Equilibrium Dynamics

The law of motion for the aggregate capital stock is:

where:

Noteworthy Features: Difference with Solow model: endogenous

intermediation Intermediation increases in generalized trust

and decreases in specific trust (increases in the number of managers)

21

.

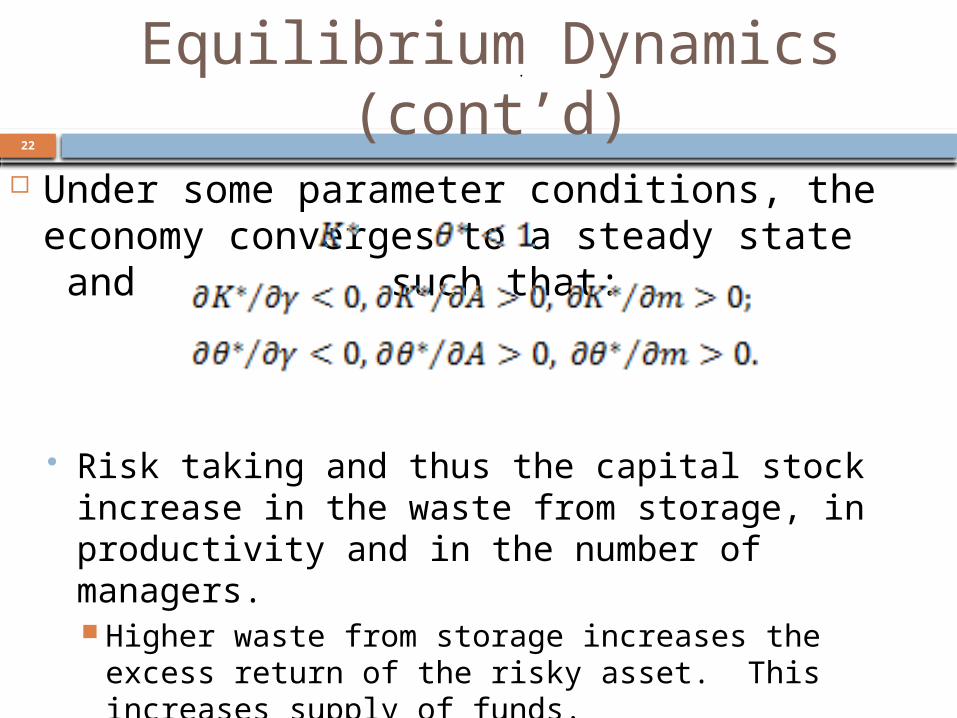

Equilibrium Dynamics (cont’d)

Under some parameter conditions, the economy converges to a steady state and such that:

Risk taking and thus the capital stock increase in the waste from storage, in productivity and in the number of managers. Higher waste from storage increases the excess return

of the risky asset. This increases supply of funds. Higher productivity increases the excess return of the

risky asset and the real wage. This increases demand and supply of funds.

The higher is the number of managers, the higher is competition among them. This reduces fees, risk taking and intermediation.

22

.

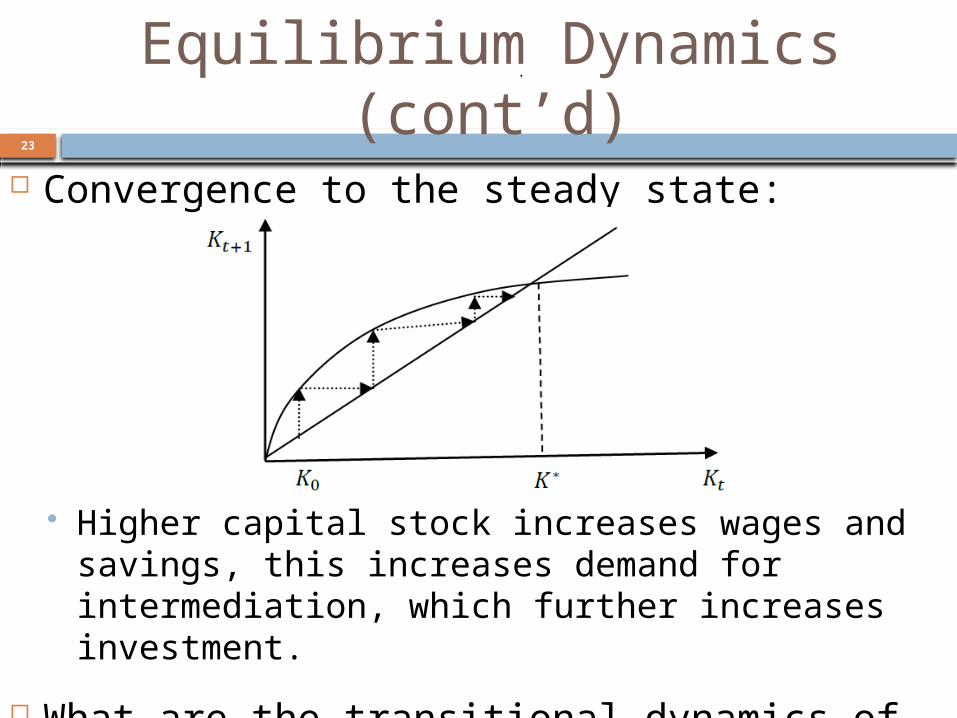

Equilibrium Dynamics (cont’d)

Convergence to the steady state:

Higher capital stock increases wages and savings, this increases demand for intermediation, which further increases investment.

What are the transitional dynamics of the financial sector?

How does the financial sector react to shocks?

23

.

Transitional Dynamics

Equilibrium fees fall as capital increases toward its s.s.:

The income share of finance goes up as capital increases towards its s.s.:

Both results are due to decreasing returns to capital: growing role of capital preservation vs. growth services as K/Y increases toward the steady state

24

.

Reaction To Shocks

Suppose that capital is initially at steady state :

If productivity permanently drops to : on impact the income share of finance increases, and goes to its original level in the long run. The s.s. capital stock falls.

If trust permanently drops to : on impact the income share of finance drops, and it continues to drop until the new steady state. The s.s. capital stock falls.

Productivity and trust shocks exert opposite short run effects. Lower productivity renders capital preservation more important, lower trust less important.

25

.

Empirical Predictions

The finance income share increases over time with an economy’s wealth to income ratio

The finance income share fluctuates with changes in investor trust (goes down when trust in finance drops)

Unit fees for specific products fall over time Consistent with the evidence in Greenwood

and Scharfstein (2012) for equity and bond funds.

26

Empirical Predictions

Dynamics of Wealth to income ratio for U.S.: 27

.

28

Dynamics of Wealth to income ratio for other countries…

Empirical Predictions (cont’d)

Growing finance income share in the postwar period is common to many countries (Philippon and Reshef 2013), just as W/Y seems to be increasing for many countries (Piketty and Zuckman 2012)

29

.

Empirical Predictions (cont’d)

Decline of finance after adverse shock to trust:

It took decades to rebuild the U.S. financial sector, much longer than to rebuild productivity

30

.

Puzzling Feature

Unit costs (finance income/financial assets) has increased despite falling unit fees:

31

.

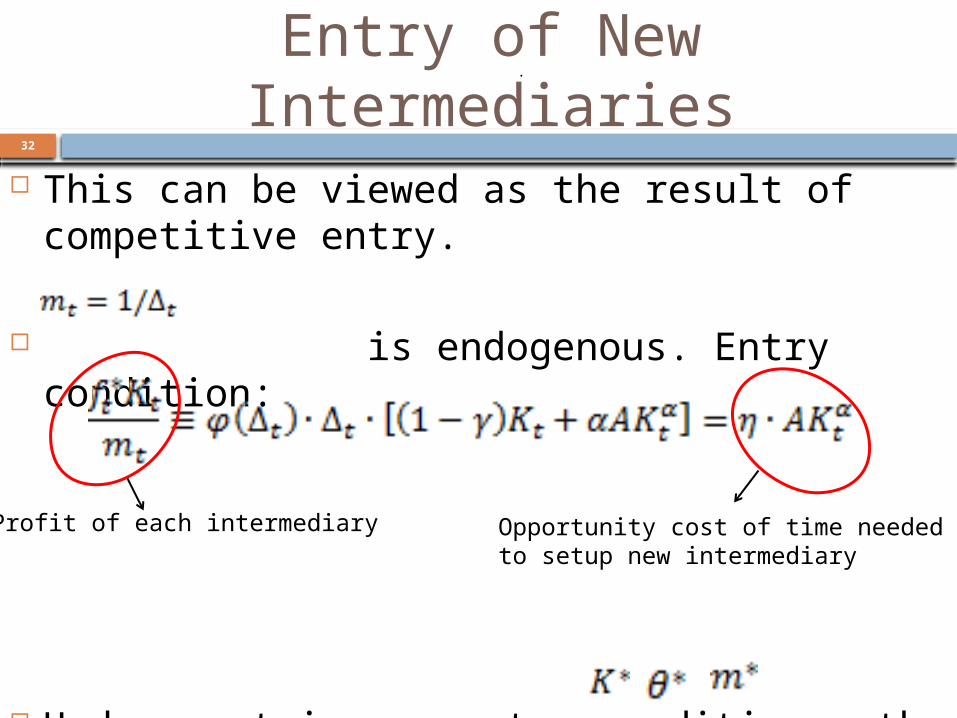

Entry of New Intermediaries

This can be viewed as the result of competitive entry.

is endogenous. Entry condition:

Under certain parameter conditions, the model with entry converges to a unique steady state , ,

32

.

Opportunity cost of time needed to setup new intermediary

Profit of each intermediary

Entry of New Intermediaries (cont’d)

Rewrite entry condition as:

As the capital stock increases toward the

steady state: The unit profit for wealth preservation goes up Entry of new intermediaries takes place

(/customization) Management fees fall (owing to decreasing

returns and entry) Income share of finance increases

33

.

Entry and Unit Cost of Finance

Finance income over financial wealth (which includes managed risky assets and non-intermediated storage) is:

Fees decrease over time, risk taking increases as closer (more trusted) managers become available through entry

As new managers enter, the composition of investment shifts toward higher fee/higher risk products (for which proximity with manager is more important)

34

.

Robustness

Results are Robust to:

Productivity and population growth

Irreversibility of transformation of consumption into capital (trading of capital between the elderly and the young)

35

Conclusions

By incorporating in a neoclassical growth model the idea that savers are willing to pay fees to take financial risk with trusted money managers we obtain: Growth of finance income share of GDP as W/Y

grows Fluctuation in size of finance with changes in

investor trust Entry of financial intermediaries and

customization Decline in fees Increase in unit cost of finance (fees x risk taking)

Without denying agency and other problems, finance should grow as the economy matures, for preservation of wealth becomes increasingly important

36