the great reset and a foxy futurist view of the future

TRANSCRIPT

1 © BMI-BRSCU

The “Great Reset” and a “Foxy Futurist” view of the future of the Building Industry.

Dr. Llewellyn B. LewisDr. Llewellyn B. LewisNovember 2010November 2010

THE STRATEGIC FORUMTHE STRATEGIC FORUM

A place of assembly for strategic conversations

THE STRATEGIC FORUMwww.strategicforum.co.za

BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

Reg. No. 2002/105109/23

•BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

•BMI

•BMI

•BMI

•BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

Reg. No. 2002/105109/23

•BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

•BMI

•BMI

•BMI

•BMI

•BMI

•BMI

•

2 © BMI-BRSCU

THE STRATEGIC FORUMwww.strategicforum.co.za

CREATING THE FUTURE

CREATIVE TENSIONCREATIVECREATIVE TENSIONTENSIONSEEKS RESOLUTION : RESULTS IN ACTION

STRATEGIC ACTION PLANS PERFORMANCE GUIDELINES

BUDGETS

DONE BY MANAGEMENT

SEEKS RESOLUTION : RESULTS IN ACTIONSEEKS RESOLUTION : RESULTS IN ACTION STRATEGIC ACTION PLANSSTRATEGIC ACTION PLANS PERFORMANCE GUIDELINESPERFORMANCE GUIDELINES

BUDGETSBUDGETS

DONE DONE BY MANAGEMENTBY MANAGEMENT

STRATEGIES STRATEGIES A LOGIC AND FIRST LEVEL A LOGIC AND FIRST LEVEL

OF DETAIL, FOR HOW OF DETAIL, FOR HOW THE VISION CAN BE ACHIEVEDTHE VISION CAN BE ACHIEVED

DEVELOPED DEVELOPED BY LEADERSHIP BY LEADERSHIP CONTEMPORARY ANALYSTCONTEMPORARY ANALYST

20152010

CURRENT REALITYCURRENT REALITYINFORMED BY INFORMED BY MEMORIES OF MEMORIES OF

THE PASTTHE PAST(HISTORY)(HISTORY)HISTORIANHISTORIAN

VISION INFORMED BY MEMORIES OF THE FUTURE(SCENARIOS)

PROPHET

CONTEXT : A COMPELLING PICTURE OF THE FUTURE WE WANT TO CREATE.

CREATED BY LEADERSHIP

CONTEXT : A COMPELLING PICTURE CONTEXT : A COMPELLING PICTURE OF THE FUTURE WE WANT TO CREATE.OF THE FUTURE WE WANT TO CREATE.

CREATED BY CREATED BY LEADERSHIPLEADERSHIP

3 © BMI-BRSCU

“Management and leadership are two different things, he says, and too many business people do not realise this. Management is the nitty-gritty, the day-to-day planning; leadership is inspiration and motivation: "They are two entirely different things and too many people try to mix them up. "

THE STRATEGIC FORUMwww.strategicforum.co.za

PHENOMENON: Business coach Brad Sugars's ActionCOACH franchise has been rated as the top business- coaching franchise in the world, as well as one of the top 100 franchises overall.

4 © BMI-BRSCU

Available on Amazon.comTHE GREAT RESET

www.strategicforum.co.za

about Richard Florida

author and thought-leader

Richard Florida is author of the global best-seller The Rise of the Creative Class and Who's Your City? a national and international best seller and amazon.com book of the month.

His new book, The Great Reset explains how new ways of living and working will drive post-crash prosperity.researcher

Florida is Director of the Martin Prosperity Institute and Professor of Business and Creativity at the Rotman School of Management, University of Toronto.

Previously, Florida has held professorships at George Mason University and Carnegie Mellon University and taught as a visiting professor at Harvard and MIT.

Florida earned his Bachelor’s degree from Rutgers University and his Ph.D. from Columbia University. His research provides unique, data-driven insight into the social, economic and demographic factors that drive the 21st century world economy.

5 © BMI-BRSCU

Prolonged ECONOMIC DOWNTURNS like

• the Great Depression of the 1930s and

• the Long Depression of the late nineteenth century, are viewed in terms of the crisis and pain they cause.

OPPORTUNITIES

• to remake our economy and society and

• to generate whole new eras of economic growth and prosperity.

In terms of innovation, invention and energetic risk-taking, these periods of creative destruction have been some of the most fertile in history and the changes they put into motion can set the stage for full-scale recovery.

THE GREAT RESETwww.strategicforum.co.za

6 © BMI-BRSCU

The real point of looking backward is to learn from the future and we have much to learn from the crises and recoveries of the past.

THE GREAT RESETwww.strategicforum.co.za

7 © BMI-BRSCU

Economic development expert Richard Florida, examines these previous ECONOMIC EPOCHS, OR RESETS.

He distills the DEEP FORCES that have altered physical and social landscapes and eventually reshaped economies and societies.

LOOKING TOWARD THE FUTURE, he identifies the patterns that will drive the next Great Reset and TRANSFORM virtually every aspect of our lives – from how and where we live, to how we work, to how we invest in individuals and infrastructure, to how we shape our cities and regions.

These forces, when combined, will spur a fresh era of growth and prosperity, define a new geography of progress and create surprising opportunities for all.

THE GREAT RESETwww.strategicforum.co.za

8 © BMI-BRSCU

Among these forces will be: New patterns of consumption and new attitudes toward ownership that are less centred on houses and cars The transformation of millions of service jobs into middle-class careers that engage workers as a source of innovation New forms of infrastructure that speed the movement of people, goods and ideas A radically altered and much denser economic landscape organized around megaregions that will drive the development of new industries, new jobs and a whole new way of life

THE GREAT RESETwww.strategicforum.co.za

9 © BMI-BRSCU

LESSON FROM THE FUTUREStanding in 2010

We see Michelangelo Towers completed and the Gautrain operational.

15 minutes from Sandton to the concourse at Jan Smuts Airport.

TRENDS IN THE RESIDENTIAL PROPERTY MARKET (SF MAY 2003)

THE GREAT RESETwww.strategicforum.co.za

10 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

11 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

We have weathered tough times before. They are a necessary part of economic cycles, giving us a chance to clearly see what is working and what’s not.

Societies can be reborn in such crises, emerging fresh, strong, and refocused.

Now is our opportunity to anticipate what that brighter future will look like and to take the steps that will get us there faster.

12 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

“This economic crisis doesn’t represent the cycle, it represents a reset. It’s an emotional, raw, social, economic reset.” (General Electric CEO Jeffrey Immelt) “People who understand that, will prosper; those who don’t will be left behind.”

13 © BMI-BRSCU

“You can have the world's best product and if you have no sales and marketing strategy, it's nothing”

"I'm proud of growing myself into a good citizen of the world but, business-wise, in 2007 I was named among the top 50 entrepreneurs in the US.

"That's a pretty darn nice achievement for an Aussie kid." (Business Day, 22 November 2010)

THE GREAT RESETwww.strategicforum.co.za

14 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

Great resets are broad and fundamental transformations of the social order; involve much more than strictly economic or financial events; It transforms, not simply the way we innovate and produce but also ushers in a whole new economic landscape; As it takes shape around new infrastructure and systems of transportation, it gives rise to new housing patterns, realigning where and how we live and work; Eventually, it ushers in a whole new way of life.

15 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

We have reached the limits of what George W Bush used to call “the ownership society”. Owning your own home made sense when people could hope to hold a job for most of their lives. In an economy that revolves around mobility and flexibility, a house that can’t be sold becomes an economic trap, preventing people from moving freely to economic opportunity. The American dream has grown dark, and it’s also clear that financial excess in the housing sector was one of the central causes of the economic crisis. Housing sucked up far too much of the nation’s and the world’s capital and too many people – already over-extended by the purchase of outsized houses – used those homes like virtual ATMs to finance carefree consumption. Every great reset has seen our system of housing change and this one is no different.

16 © BMI-BRSCU

STRATEGIC DRIFT AND REINVENTIONwww.strategicforum.co.za

Every American President including George Bush promoted Home Ownership

Housing was a major source of national wealth for decades, and home equity, however sadly diminished, is still the biggest single piece of wealth many Americans

Have. (Fortune, 15 November 2010)

17 © BMI-BRSCU

THE GREAT RESETwww.strategicforum.co.za

The rate of home ownership has been on the decline for some time now. Many of those who still buy homes will choose smaller ones, while many more will opt for rental housing.

Our new way of life will depend a lot less on the car. Many people are reassessing their automobile ownership. After more than a century, in which an automobile represented the American Dream, car enthusiasm may no longer be a part of Americans’ DNA.

Traffic and gridlock have become a dead-weight time cost on the economy.

The great reset will involve new consumption patterns that are less centred around houses and cars; new forms of infrastructure that again speed the movement of people, goods and ideas and a radically altered and much denser economic landscape that will provide the springboard for a whole new way of life and drive the development of new industries and jobs.

18 © BMI-BRSCU

THE CRISIS MOST LIKE OUR OWNwww.strategicforum.co.za

The historian, Scott Reynolds Nelson, writes that today’s crisis most closely resembles the Long Depression of 1873. That 19th century downturn began as a banking crisis, brought on by insolvent mortgages and complex financial instruments (sound familiar?) quickly spread to the entire economy, leading to widespread and prolonged unemployment.

19 © BMI-BRSCU

THE MOST TECHNOLOGICALLY PROGRESSIVE DECADEwww.strategicforum.co.za

The spectre of the Great Depression of the 1930s hovers over us to this day. It’s difficult to read today’s headlines about the bankruptcies of once great corporations, whether they are venerable investment banks or automobile companies and not feel haunted by the Stock Market crash of 1929 and the subsequent bank failures that wiped out both personal and corporate wealth – some nine-million Americans saw their savings evaporate - and brought the economy to a standstill.

The biggest single source of wealth for many people – their home equity – has fallen almost 50% from its peak in 2006 . . . Loss $6,5 Trillion

US Stocks are still down 25% from their peak in 2007, their 75% gain in the past 19 months notwithstanding.Cost: $4,8 Trillion

Then there are the 7,7 million lost jobs with their associated lost income, lost wealth, and lost consumer spending.Cost: Untold Trillions

20 © BMI-BRSCU

SUBURBAN SOLUTIONwww.strategicforum.co.za

The second reset was propelled by rising home-ownership. Home-ownership became a cornerstone of economic life, primarily because decades of policy put it there. The American Dream meant one thing: economic opportunity. However, the second reset redefined and broadened that dream, making your own home the central part of it. Home-ownership radically transformed the way people consumed. The amount of money the average family spent on food, fell from almost half at the turn of the 20th century to one-third in 1950 and less than a fifth by the mid-1980s. Spending on basic needs – food, shelter and clothing combined – declined from more than three-quarters of family budgets at the turn of the century to less than half by 1960. Spending on home furnishings and equipment increased from 4% during the depression to 70% by 1950, while vehicle expenses climbed from around 5% to 12% in 1950 over the same period before reaching almost one-quarter of the family’s spending by 1970.

21 © BMI-BRSCU

THE FIX IS INwww.strategicforum.co.za

The idea of the spatial fix was first advanced by the geographer, David Harvey, in the mid-1970s. “To describe capitalism’s insatiable drive to resolve inner crises, through spatial expansion and geographical restructuring.”Spatial fixes take a long time to come together and an even longer time before they can reset the economy. The bubble was so big in the 1920s, that after it popped during the Great Depression, it would take 22 years for non-residential construction investment to regain its precrash peak and 24 years for real spending on residential construction to recover to its pre-crisis highs. Anyone who thinks we’ll be able to reset the current housing market quickly, needs to pay close attention to this.

22 © BMI-BRSCU

FIRE STARTERwww.strategicforum.co.za

A decade or two ago, many experts argued that a broad economic sector, dubbed Fire – FINANCE, INSURANCE AND REAL ESTATE – was the next stage in the evolution of capitalism.The current crisis was not merely a crisis of banking and finance, but a broader crisis of Fire as a whole As the venture capitalist, Eric Janszen, wrote in Harper’s, “As more and more risk pollution rises to the surface, credit will continue to contract and the Fire economy – which depends on the free-flow of credit, will experience its first near-death experience since the sector first rose to power in the 1980s.”

23 © BMI-BRSCU

THE RESET ECONOMYwww.strategicforum.co.za

Our society is changing in deep and fundamental ways – all of our habits and behaviours, from how we shop and what we buy to how we spend our free time and to the values that govern our lives – this is what it means when we talk about a reset in our values. There is a rise of a new frugality as people shift away from conspicuous consumption to simpler, more basic priorities, from a lifestyle where people thought they could purchase their way to happiness, to something better and more real. Americans have certainly begun to save more and rely less on credit, partly because credit has become much more difficult to get. Recovery from both the Long Depression of the 1870s and the Great Depression of the 1920s – the first and second resets – took the better part of two or three decades.For the third reset, we can identify a set of forces, playing out in our society that will almost certainly power a great reset and a more sustainable new way of life. We can see them in new consumption patterns; new ways of organizing and managing businesses and the factors which determine where and how we live.

24 © BMI-BRSCU

THE RESET ECONOMYwww.strategicforum.co.za

A new spatial fix – a new geography of working and living – will be the only path back to renewed economic growth, confidence and prosperity. The Long Depression was a product of the first industrial revolution and the Great Depression, a product of the second industrial revolution. The current crisis is bound up with the third industrial revolution – the shift from an economy of making things to one that revolves around knowledge and creativity. Today’s reset will affect our society at a deeper level than did the resets of the past. We are living through an even more powerful and fundamental shift; from an industrial system to an economy which is increasingly powered by knowledge, creativity and ideas.Instead of reinforcing the economy, the financial system started to undermine it: funneling capital which could have been used to create new technologies and industries into real estate of shaky financial instruments, sucking up huge amounts of talent and ultimately generating the series of bubbles that got us into this mess in the first place.

25 © BMI-BRSCU

THE RESET ECONOMYwww.strategicforum.co.za

The role of finance changed from being, in the words of William Black, a servant of the economy to a predator. It has grown too large. “The finance sector is an intermediary – essentially a ‘middle man’” he writes. “Like all middlemen, it should be as small as possible, while still being capable of accomplishing its mission. Instead of supporting the real wealth-producing parts of the economy, it has become a parasite on them. Rather than putting capital together with enterprise as a middleman should do, finance itself became the target enterprise; its only product being more capital.”

26 © BMI-BRSCU

THE NEW NORMALwww.strategicforum.co.za

It’s ironic that public discourse is so limited to breathing life back into the old housing-auto complex – baling out banks, mortgage lenders and auto-makers – when these are the very institutions that helped spark the crisis in the first place. It is exactly those products and services that now have to reinvent themselves and become more efficient and more affordable. We need to radically shrink our expenditure on houses, cars and energy to free up spending for newly emerging goods and services – everything from new biotechnologies and powerful computers to new forms of personal development and new experiences. Will the current crash cause people to consume less and to save more? Will it usher in a new era of thrift and introspection, of caution and frugality?This much is clear: the crash caused American consumers to significantly scale back their spending, reduce their use of credit and to save more and not just in the short run.More and more people are ditching their cars and taking public transport or moving to more walkable neighbourhoods where they can get by without them or by occasionally using a rental car.

27 © BMI-BRSCU

BIG FAST AND GREENwww.strategicforum.co.za

Congestion and the fear of being stuck in traffic dissuade people from driving their cars. Traffic jams can actually be environmentally beneficial if they turn subways, buses, car pools, bicycles and walking to work into more attractive options.We’ll need to invest in a wide range of transportation options, from rail, subways and buses to new kinds of developments where people can choose to live closer to where they work. Every great reset has been spurred on by new infrastructure that can speed the movement of goods, people and ideas.

28 © BMI-BRSCU

THE VELOCITY OF YOUwww.strategicforum.co.za

Today, the highways of major cities and mega regions are veritable parking lots; at the same time, ideas can travel all around the world almost instantaneously on a digital highway and if you are willing to pay enough, you can send a package anywhere virtually overnight. A single key stroke can send insight and creativity spreading through society, and that single phenomenon has revolutionized the way we live. The looming challenge is to speed the physical movement of goods, services and people – the tangible bits of the real world – so that they are more in line with the lightning fast flow of electronic information in the virtual world.

Mark Zucherberg, 26, founder and CEO of Facebook,500 million users, $25 Billion valuation

29 © BMI-BRSCU

THE VELOCITY OF YOUwww.strategicforum.co.za

Our lives will become profoundly and intensely local; daily life will be far less about mobility and much more about staying where you are. In today’s idea-driven economy, the cost of time is what really matters. With the constant pressure to innovate, it makes little sense to waste countless collective hours commuting so the most efficienct and productive regions are those where people are thinking and working, not sitting in traffic.More and more people are choosing to take the subway, train or bus or even walk or bike to work and go about their daily business – providing they live in an environment that allows for such choices. In Manhattan, 82% of workers get to work by public transport, on bicycle or by foot. 60% of Americans surveyed in 2005 said they want to live in walkable communities with shops, restaurants, movie theatres, schools and churches nearby.

30 © BMI-BRSCU

FASTER THAN A SPEEDING BULLETwww.strategicforum.co.za

In the future, as flexible working hours, working from home and telecommuting become even more common than they are today, high-speed rail holds the promise of connecting declining places to thriving ones, greatly expanding the economic options and opportunities to their residents.Its time to start thinking of transit and infrastructure projects less in political terms and more as a set of strategic investments as fundamental to the speed and scope of our economic recovery as they are to the emerging shape of the economy, society and communities of the future.Past investment in railroad lines and highways, spurred development of real estate and of industries that far outstripped anything that could be imagined at the time. Infrastructure provides a skeleton on which to grow a new economic model. The infrastructure investments we make now will determine the kind of economy we have in the future.

31 © BMI-BRSCU

RENTING THE DREAMwww.strategicforum.co.za

In 1931, in the depths of the Great Depression, the historian, James Trusloe Adams, introduced the expression “The American Dream”, defining it as the “Dream of a land in which live should be better, richer and fuller for everyone, with opportunity for each according to ability or achievement.” For the past half century, ownership of a single family home has been one of the cornerstones of that dream.However, a study by the Wharton School of Business found that after controlling for income and demographics, home-owners are no happier than renters. Less surprisingly, home-owners report considerably higher levels of stress than renters. That makes perfect sense: their financial burden is higher and upkeep of a home is a chore. There’s a reason people refer to their houses as money pits; they are time pits as well.Historically, one of the greatest allures of home-ownership was that it represented wealth. That era ended when the housing bubble burst. Now instead of people making money on their homes, millions of people have lost a bundle and millions more are stuck with homes whose mortgages exceed their value.

32 © BMI-BRSCU

RENTING THE DREAMwww.strategicforum.co.za

According to one study, 30% of people aged 45 – 54 and 18% of those between 55 and 64 were under water in their homes in 2009. Except for some exceptional boom periods, housing has never been a good financial investment. Yale University’s Robert Shiller, the world’s leading student of bubbles, housing and otherwise, found that from “1890 – 1990, the rate of return on residential real estate from just about zero after inflation.”Mobility and flexibility are key principles of the modern economy; home-ownership limits both. According to one important study, cities with higher home-ownership rates also suffer from higher unemployment rates. It is ironic that housing for so many Americans has gone from being their shelter to being their burden.

33 © BMI-BRSCU

RENTING THE DREAMwww.strategicforum.co.za

We are already beginning to see some signs of a shift towards rental. With all the turmoil in the housing markets, many people have delayed buying With tightened credit standards, (requiring a modest down-payment and a reasonable credit rating) its becoming much more difficult for those who don’t have their financial house in order to buy. Across the United States, some 36-million people are renters. About one-third of all occupied homes are rentals. Rental is much more prevalent in metro areas such as New York, where 66% of residents are renters, as well as DC and Chicago, where more than half rent their homes.

34 © BMI-BRSCU

RESETTING POINTwww.strategicforum.co.za

Resets take time. If the past is any guide, there are complex processes that unfold over two or three decades. Today’s economic troubles share much more with the Long Depression of the late 19th century, the so-called First Reset. Now, as then, we are in the midst of a tectonic shift to a fundamentally new economic order: the shift from an agricultural to an industrial economy then; the shift from an industrial to an idea-driven creative economy now. The challenge is to accelerate the transition from the old to the new order and simultaneously spur the transition to a new geographic framework in which new living and work habits can take shape.

The “rule of thumb” is seven years down and seven years up. Apply that rule to the national market, where the bubble popped in 2006, and we’re talking about a sustained recovery starting in 2013, and taking until 2020. That’s pretty grim, but probably realistic. (Fortune, November 15, 2010)

35 © BMI-BRSCU

RESETTING POINTwww.strategicforum.co.za

Efforts must concentrate on actively building the economy of the future.Instead of infusing scarce capital into the very banks and financial system that brought us to the brink in the first place or trying to reinvigorate the housing and mortgage markets which pushed us over the edge and instead of baling out mismanaged old economy companies, we must use whatever resources are available to accelerate the transition to an idea-driven economy, while improving the jobs that have survived or are being created.A simple undeniable first principle is that every single human-being is creative. The real key to economic growth lies in harnessing the full creative talents of every one of us.THERE’S AN URGENT NEED TO CREATE NEW JOBSWe need to support the growth of higher paying knowledge, professional and creative jobs and ensure that greater numbers of workers are prepared for them. This implies the need to overhaul the education system. A new learning and development system is required that is in sync with the new creative economy.

36 © BMI-BRSCU

RESETTING POINTwww.strategicforum.co.za

A new kind of social compact is required. It needs to be reworked in the light of the demands and challenges of the knowledge driven economy. In the more mobile and flexible economic system, people change jobs much more frequently than in the past. The key is to expand the very concept of a social safety net from one that just provides material wellbeing to one that provides real opportunity for every person.We need to build the infrastructure of the future, not just patch up that of the past. We must make intelligent investments in new infrastructure that can move beyond the constraints of the current energy-inefficient environmentally destructive, time-devouring infrastructure. We need to increase the velocity of moving people, goods and ideas.

37 © BMI-BRSCU

RESETTING POINTwww.strategicforum.co.za

The traditional notion of ownership itself may well be outmoded. Ironically, the once-vaunted ownership society appears to be giving way to a new form of rentership society. Car purchases, which long ago gave way to car leases are now being replaced by access to rental cars. More and more people are choosing to rent their homes and growing numbers of home-owners are shifting to rentals.The promise of the current reset is the opportunities for a life made better not by ownership of real estate, appliances, cars and all manner of material goods, but by greater flexibility and lower levels of debt; more time with family and friends; greater promise of personal development and access to more and better experiences.

38 © BMI-BRSCU

RESETTING POINTwww.strategicforum.co.za

Home ownership under threat Rental preferred to ownership Transition to the Knowledge Economy Infrastructure Investment crucial New forms of public transport commuting New types of inner cities with people walking to work More job mobility requiring flexibility Traffic congestion and gridlock forcing new working and living models Spatial fix involves Integrated, Sustainable developments where people live work and play

39 © BMI-BRSCU

FOXY FUTURISTSwww.mindofafox.com

Clem Sunter was born in Suffolk, England on 8th August 1944 and was educated at Winchester College. He went to Oxford where he read Politics, Philosophy and Economics before joining Charter Consolidated as a management trainee in 1966.

Since 1987, he has authored 14 books some of which have been bestsellers. His other main interest is seeking to mobilise the private sector in the war against HIV/AIDS.

He was recently awarded an Honourary Doctorate by the University of Cape Town for his work in the field of scenario planning. He was also voted by leading South African CEOs as the speaker who has made the most significant contribution to, and impact on, best practice and business in South Africa. In 2006, he was invited to give a scenario presentation at the Central Party School in Beijing - a rare privilege for a foreigner. He also facilitated sessions on global warming in New Delhi and London.

40 © BMI-BRSCU

FOXY FUTURISTSwww.mindofafox.com

20%30%

10%40%

41 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

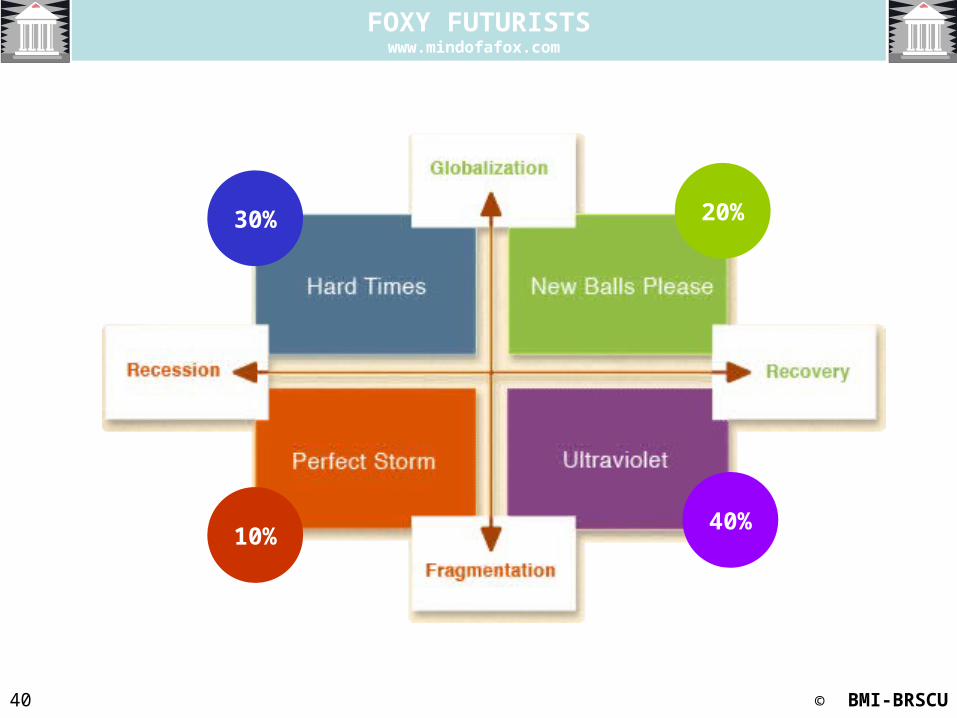

Hard Times

(Globalization/Low Economic Growth)This is a scenario of conventional global recession, probably initiated by a US economic downturn and the knock-on effect it has on the other economies. India and China are not spared as the interdependencies created by globalization and international trade turn against them. Asset prices (property and equities), the improvement of which has over recent years allowed consumers to borrow more to spend, suddenly reverse. The downward spiral is reinforced when commodity prices plummet except for gold, which does well in light of the uncertainties around paper currencies and paper assets. Eventually the bloodletting ends, green shoots start springing up in the burnt landscape and a recovery gets underway, which returns the world to the top right-hand quadrant. The length of the recession is relatively short, i.e. it is more like a 'V' than a 'U', but the depth of the 'V' is unknown. The crucial difference between Hard Times and Perfect Storm is that globalization remains intact in the former scenario, while it is seriously compromised by political and military events in the latter one. The rebound in the second case therefore takes much longer.

42 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Going clockwise from top left, we start with "Hard Times" continuing for the world economy for another three to five years. It's a "U" scenario across the globe. The reason this scenario has credibility is that the problem which created the "Hard Times" in the first place - the magnitude of debt owed by governments, businesses and consumers - has not gone away. All it has done is change in nature from a private sector problem concerning the solvency of the banks to a public sector problem concerning governments which are running up large budget deficits, and racking up an unacceptably high level of national debt.

The latter problem is more difficult to solve. Whereas governments could justify bailing out the banks because taxpayers might lose their bank deposits, it is a much harder case to argue when governments start bailing each other out. Moreover, while a superfund may solve the liquidity problem of financially strapped governments in the short term, it does nothing to resolve the competitiveness of those nations in the long term. Indeed, it can even undermine any industrial renaissance by allowing the recipient nation to defer tough decisions. All in all this scenario presumes the mess takes a long time to clean up.

43 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Sunter and Illbury attach a 30% probability to "Hard Times" and 40% to "Ultraviolet", the flag differentiating the two being the near-term performance of the Chinese economy.

If China has a wobble because of labour problems or the property bubble bursting there (as it did in Japan in 1990), it's "Hard Times" or double-dip for all.

Otherwise it's a "UV" world; and, with the Chinese authorities having the confidence to allow a limited float for the Yuan, this is looking increasingly likely.

44 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Long Boom/New Balls Please

(Globalization/ High Economic Growth)The world has been located in this scenario for most of the 1990s and so far in this century, • Driven by the conversion of most countries to free market economics and the spectacular rise of China and India.• Inflation and interest rates remain low, the Chinese and Indian economies continue to defy gravity and stock markets continue to boom.• The world still has conflict zones but the impact of these is completely overridden by the unstoppable force of globalization. • One day either global warming, a growing scarcity of raw materials, the latter causing a general rise in inflation rates, or a new global health epidemic could moderate the boom. • A Long Boom scenario envisages the centre of gravity of the world economy moving East, meaning that Western institutions like the IMF and the World Bank will have to revise their mode of operation. • The G8 will become the G10 with the addition of China and India as new members.

45 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

New Balls Please (named after Wimbledon where a new game requires new balls)

(Globalization/ High Economic Growth)

Currently backed by Tim Geithner and Ben Bernanke.• We're over the worst, 2010 is a year of transition, 2011 will see a mild recovery and 2012 we're back in the game. • It is a V-shaped recovery rather than a U-shaped recession.

There are four critical differences between the old and new game:

• the banks will be more heavily regulated; • credit will be harder to get; • the East will be the economic equivalent of the West; • and more effective resource supply/ utilisation in the face of growing scarcities of metals, oil, food and water will be the basis of the next wave of technology.

46 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

New Balls Please

(Globalization/ High Economic Growth)

At present, Sunter and Illbury give only a 20% chance to "New Balls Please" because two of the three flags which would indicate the scenario is in play are firmly down and only one is half up.

• The two flags down are a serious reduction in unemployment and in debt worldwide. • The one half up is an improvement in property values and stock markets, but not to pre-recession levels.

47 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Divided World

(Fragmentation/High Economic Growth)The world develops into a more hostile place as regional conflicts intensify and trading spats/cases of protectionism multiply.• The anti-globalization lobby grows stronger while an increasing number of countries reject the 'Washington Consensus', revert to old-style Socialist policies (South America) and become more nationalistic about the resources they possess (Russia). • Nevertheless, just as no terrorist incident or war in the recent past has been a showstopper (not even 9/11), the global economy shrugs off all these problems because of the sheer momentum caused by the two most populous nations on earth simultaneously going through an industrial revolution. • Whereas in the Long Boom companies can invest virtually anywhere in the world because the tide is rising everywhere, they have to be more circumspect in Divided World because of the emergence of more 'failed states'.

48 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Divided World/Ultra Violet

(Fragmentation/High Economic Growth)

• Called "Ultraviolet" or "UV" to indicate a two-speed world, some regions going through a "U" while others experience a "V". • We would nominate Europe, the UK and Russia for a "U" and Brazil, Africa, China and India for a "V". • Japan could go either way having undergone a 20 year "U". • America likewise in light of the government there having to rectify its budget deficit.

49 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Perfect Storm

(Fragmentation/Low Economic Growth)

• Represents a confluence of negative events in both the political and economic arenas, which could lead to a huge change in the fortunes of the world. • It is a reprise of the 'roaring' 1920s, which was followed by the depression of the 1930s and the rise of Nazi Germany. • The party ends just as spectacularly - only the script and the actors are different. • Potential triggers could be nuclear terrorism in a Western city, a major war between Iran and Israel/the West over its nuclear programme, a new fall-out between America and Russia as Russia reverts to authoritarianism, or a financial meltdown in China followed by widespread unrest. • Recovery from this scenario proves agonizingly slow as business confidence has to be rebuilt from scratch. • Stocks on Wall Street only recovered pre-1929-crash values nearly 20 years later (having shed 85% by 1934). It was a long drop!

50 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Perfect Storm

(Fragmentation/Low Economic Growth)

"Perfect Storm", is a seriously deep "U" triggered by a combination of political and economic events, including another major war, nuclear terrorism, widespread national defaults or an upsurge in protectionism. It portrays an unstable, hostile world where recession is replaced by depression.

51 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Perfect Storm

(Fragmentation/Low Economic Growth)

Sunter and Illbury treat "Perfect Storm" as a wild-card scenario, giving it odds of 10%.

The rising tension between North and South Korea, the standoff between the West and Iran over its nuclear programme and the continuing war in Afghanistan are all potential flags.

Nevertheless, as they say to clients, please disagree with the flags and probabilities if you feel they are wrong.

It is more sensible to have a structured debate around scenarios, flags and probabilities than to bet the whole shop on a single projection, however expertly it is crafted.

52 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

70%

30%

53 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

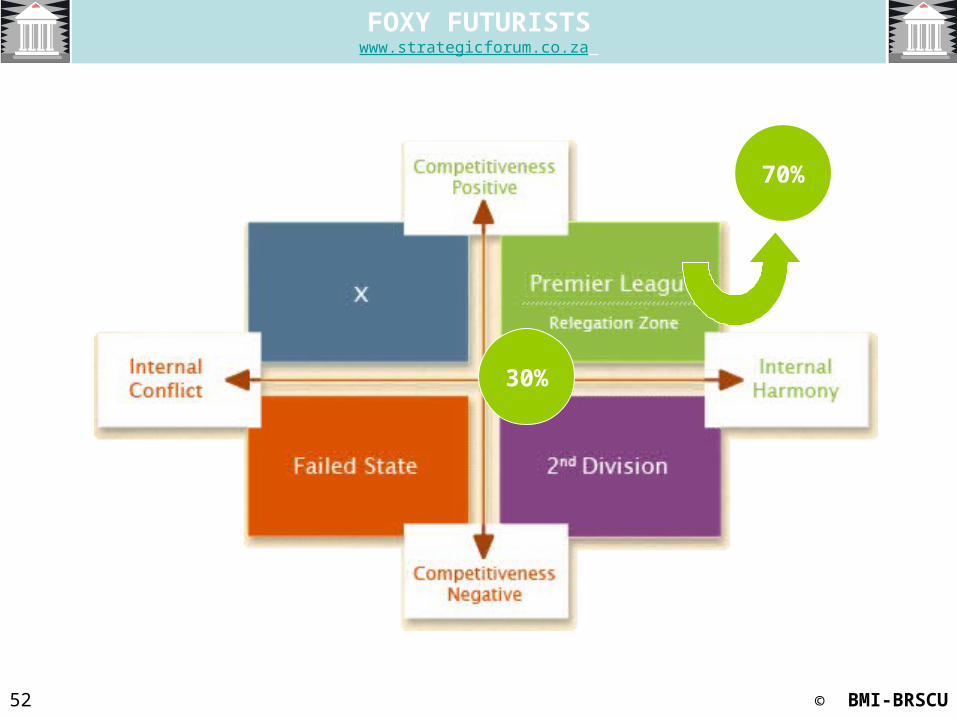

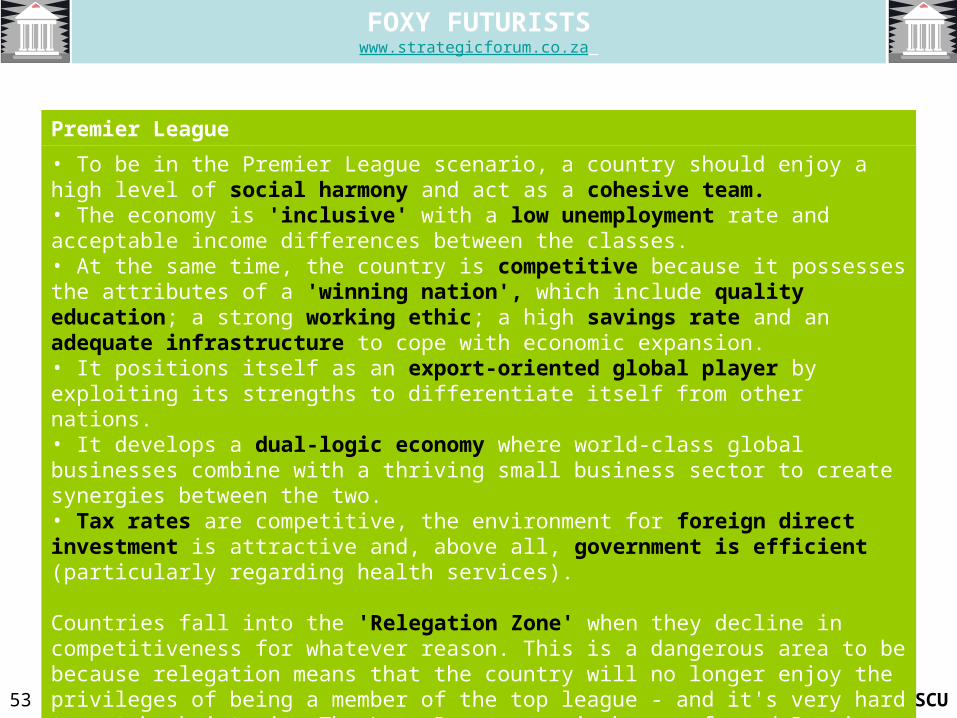

Premier League

• To be in the Premier League scenario, a country should enjoy a high level of social harmony and act as a cohesive team. • The economy is 'inclusive' with a low unemployment rate and acceptable income differences between the classes. • At the same time, the country is competitive because it possesses the attributes of a 'winning nation', which include quality education; a strong working ethic; a high savings rate and an adequate infrastructure to cope with economic expansion. • It positions itself as an export-oriented global player by exploiting its strengths to differentiate itself from other nations. • It develops a dual-logic economy where world-class global businesses combine with a thriving small business sector to create synergies between the two. • Tax rates are competitive, the environment for foreign direct investment is attractive and, above all, government is efficient (particularly regarding health services).

Countries fall into the 'Relegation Zone' when they decline in competitiveness for whatever reason. This is a dangerous area to be because relegation means that the country will no longer enjoy the privileges of being a member of the top league - and it's very hard to get back into it. The Long Boom scenario has conferred Premier League status on quite a few developing countries - particularly resource-rich ones - that have taken advantage of the positive economic climate.

54 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Premier League

Let's apply this process to the possibilities for South Africa in light of the country's 2009 General Election (and against the backdrop of the global economy in recession).

We have been in the 'Premier League' scenario since 1994 - the year of our first truly democratic election.

For most of the time since then, we have resided in the middle of the league, which is where we should be. We are not a Manchester United (about to beat America, Japan, Germany and China). We are more like a West Ham or Manchester City.

Nevertheless, according to some global surveys, we have lost considerable ground in the rankings, which puts us perilously close to the 'Relegation Zone'. Reasons given are that violent crime is driving talent out of the country; HIV/AIDS is shortening the lifespan of the average South African; our infrastructure is showing signs of disrepair; and some of our industries (such as our textile industry) are looking distinctly uncompetitive compared to Eastern players.

55 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Premier League

Given our current predicament, there are three alternative scenarios.

The first one is that we get relegated to the 'Second Division', where the bulk of the Third World resides - poor but peaceful.

Companies will still make money (as they do in plenty of Third World countries); and they will always have the option of extending their geographical footprint into other African countries, or even overseas.

By contrast, for the Government the scenario is an unmitigated disaster because they can't change clubs! Certainly their tax revenue will be a whole lot less than they received when they were in charge of a Premier League nation; and they won't have the same access to international capital.

Altogether it makes the perfectly honourable maxim of 'a better life for all' seriously harder to achieve.

The flag for this scenario is that we disappear from the 'A' list according to an increasing number of internationally accredited surveys.

56 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

2nd Division

This scenario is for countries that are poor but peaceful. They remain 2nd Division players either because they have no ambition to move up to the Premier League or they are quite bereft of mineral resources or Nature is harsh in terms of climate or soil.

But they get by and, human spirit being what it is, people lead relatively contented lives.

The 2nd Division also contains ex-Premier-League nations that once were rich but whose income per head has declined for any number of reasons including bad leadership.

They don't wield much influence in global affairs and seldom obtain anything prestigious like a seat on the UN Security Council. They may even possess some of the attributes of a 'winning nation' but somehow they simply cannot get their entire act together.

57 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Premier League or Second Division

The odds at the moment are 70% to a U-Turn in the 'Premier League' and 30% to being relegated to the 'Second Division'.

This may sound optimistic to some; but we're probably out of the 'Relegation Zone' already, not because we've gone up but because the rest of the world has gone down.

A positive flag is that in the 2009 World Competitiveness Yearbook, produced by the International Institute for Management Development, South Africa has risen to 48th out of 57 countries, compared to 53rd out of 55 last year.

Reasons given include our resilience to the global financial crisis and our recovery from the rolling electricity blackouts experienced at the beginning of 2008.

Indeed, our financial and insurance sectors have almost escaped the whole toxic debt tsunami unscathed; and we are relatively unencumbered by debt as a nation.

58 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Premier League or Second Division

In addition, despite the dramatic decline in our GDP, we shall probably experience a shallower 'V' than Europe and the US.

All these sporting events on our calendar act as an excellent gap-filler. On top of that, Zimbabwe has every chance of resurrecting its economy in the near future, for which we will act as a gateway.

On the other hand, we have to make tangible progress in the areas where we rank lowest in the 'Premier League' - unemployment, brain drain, available skills, life expectancy/health problems, pupil-teacher ratios in secondary schools and organised crime!

In conclusion, we feel that South Africa is not a bad place to see out the global economic 'Hard Times', or even the 'Perfect Storm' if it looks like engulfing the world.

Obviously quite a few young South Africans living overseas agree with us. They are returning home.

59 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

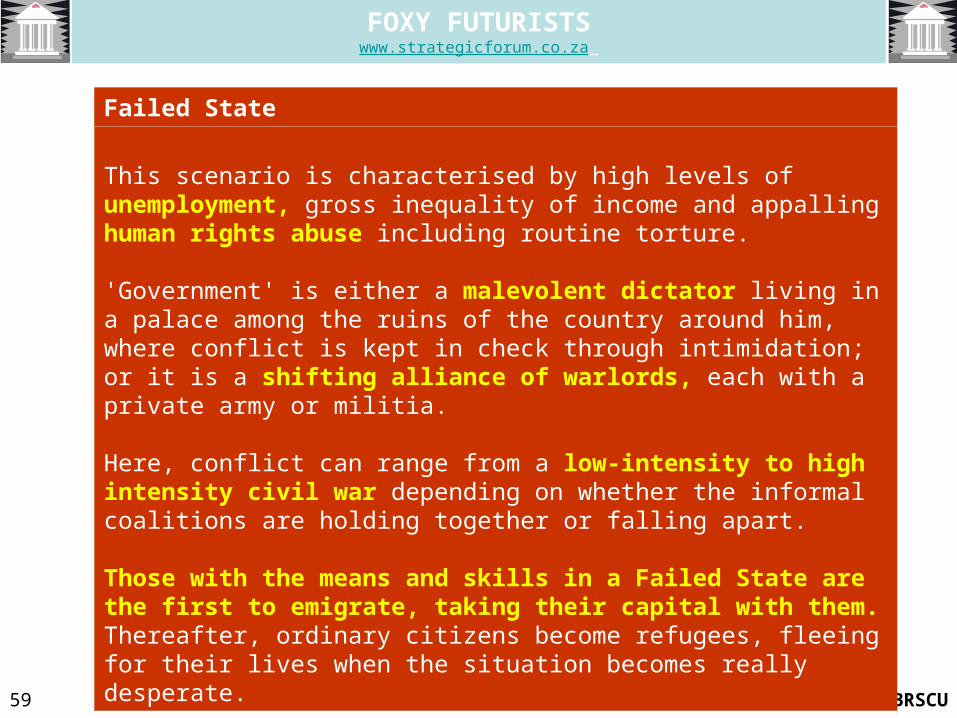

Failed State

This scenario is characterised by high levels of unemployment, gross inequality of income and appalling human rights abuse including routine torture.

'Government' is either a malevolent dictator living in a palace among the ruins of the country around him, where conflict is kept in check through intimidation; or it is a shifting alliance of warlords, each with a private army or militia.

Here, conflict can range from a low-intensity to high intensity civil war depending on whether the informal coalitions are holding together or falling apart.

Those with the means and skills in a Failed State are the first to emigrate, taking their capital with them. Thereafter, ordinary citizens become refugees, fleeing for their lives when the situation becomes really desperate.

60 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Failed State

The second scenario is 'Failed State' into which the principal flag for entry is widespread political or criminal violence. Examples of countries either in or on the border of 'Failed State' are Somalia, Pakistan and Iraq. Nothing trashes a national brand like violence. The world turns its back on you.

The peaceful nature of the 2009 elections in South Africa means that the current odds on this scenario are negligible. It is more like a cautionary tale. This leaves the third scenario that South Africa returns to the middle of the Premier League - comfortably outside the 'Relegation Zone'.

There are three flags associated with this scenario. The first one is inclusive leadership. The last thing that South Africa ought to be in the global 'Hard Times' scenario is a divided team.

Inclusivity means on the one hand keeping the rich minority - who have the capital and a fair measure of skills - on side; but also creating the opportunities for the marginalised poor to become part of the mainstream economy. In other words, it's a delicate balancing act, and it's reassuring that Jacob Zuma has made inclusivity central to his initial presidential theme.

61 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Failed State

The second flag is to show tangible results in rectifying the problems that have caused South Africa's recent slide in the Premier League.

This has nothing to do with ideology on the Left or the Right, and everything to do with back-to-basics management. The best way for South Africa to raise this second flag is for all of us to recognise the pockets of excellence that exist in our midst and then benchmark other similar organisations against those pockets of excellence.

For example, while there are many complaints against service delivery in the public sector, there is one world-class Government department - the South African Revenue Service. It is as good as any revenue collection service in the world. All other departments should be benchmarked against the excellence of delivery of SARS.

In the health sector, a pocket of excellence is the Red Cross Children's Hospital in Cape Town. It shows that a properly managed state hospital can combine state-of-the-art equipment with medical care for children only obtainable at the best hospitals in Western capital cities.

62 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Failed State

The third flag is about the evolution of a dual-logic economy consisting of an outward-looking economy that earns enough foreign exchange to cover the country's export bill (which is real issue since the current account deficit is around 7% of GDP); and an inward-looking economy that creates enough new jobs to make a dent on our appalling unemployment rate of 23,5%.

The success of the outward-looking economy revolves around choosing one's spaces carefully in light of how competitive the global economic game is.

South Africa has three spaces where it can dominate: mineral and agricultural resources, but we need to add more value here before we export them (a pocket of excellence being our wine industry); tourism, which can benefit from our ability to host major sporting events; and playing the gateway role into a continent that is opening up for business.

South Africa is the 'America' of Africa in that it produces 30% of the continent's GDP with a little less than 5% of the continent's population. Such a position confers huge competitive advantage in this particular trading space.

63 © BMI-BRSCU

FOXY FUTURISTSwww.strategicforum.co.za

Failed State

The success and inclusivity of the inward-looking economy will very much depend on the growth of small business in South Africa and overcoming the problem of a 'two worlds' economy.

We have a First World formal sector and a Third World informal sector with virtually no linkage between the two. Yet a glance at the 'Premier League' reveals that the three countries that made it to the top fastest all began their ascent with an entrepreneurial burst of energy - Japan and Germany after the Second World War and China after 1978. They are now respectively the 2nd, 4th and 3rd largest economies in the world.

Family-owned businesses were a critical element in the lift-off. Consequently a flag that will demonstrate progress in this area will be the transformation of the micro-lending industry. Why not invite Nobel Laureate Dr Muhammad Yunus, who founded the Grameen Bank in Bangladesh, to be a consultant on what we should do here? A second flag comprises more generous tax incentives to compensate for the risk of starting a small business, e.g. offering a complete tax holiday on profit up to a cumulative total of R1 million and exemption from capital gains tax for investors in businesses below a certain size.

64 © BMI-BRSCU

DECLINE

Credit andCapital markets

CLOSED

GROWTH

Credit andCapital markets

OPEN

FOXY FUTURISTSwww.strategicforum.co.za

High Road

Low Road

Lower MiddleRoad

Upper Middle Road

10%40%

30% 20%

65 © BMI-BRSCU

Declin

eD

eclin

e

Property a POOR Investment• Industry has no leadership, no vision, muddles along;• Competition fierce, no cooperation;• Industry operates in SILOS, adversarial and confrontational;• Confidence very low;• Private Sector Investment < 50%% of Total Investment in Building; • CPI > 12%;• Real Interest Rates > 10%;• Building Industry growth negative;• Construction Industry growth negative;• FTHB Subsidies < 1% of Budget;• Infrastructure spend inadequate;• GFCF < 15% of GDP;• Investment in Building and Construction < 25% of GFCF

Property a GOOD Investment• Industry has good leadership, some vision, well intended;• Confidence fairly low;• Private Sector Investment 60-75% of Total Inv in Bldng; • CPI > 6% < 10%;• Real Interest Rates > 5% < 7,5%;• Building Industry growth 3,5% - 6,5%;• Construction Industry growth 5% - 7,5%;• FTHB Subsidies < 2,5% of Budget;• Infrastructure spend R500 - R780 Billion by 2015;• GFCF 20% - 25% of GDP;• Investment in Building and Construction 25% - 50% of GFCF

Property PREFERRED Investment• Industry has strong leadership and an igniting vision; • High Confidence;• Private Sector Investment 75-80% of Total Investment in Building; • CPI in 3-6% range;• Credit readily available;• Real Interest Rates < 5%;• Building Industry growth > 6,5% pa;• Construction Industry growth > 7,5% pa;• FTHB Subsidies 2,5-5% of Budget (R350 Billion by 2020);• Infrastructure spend of R800 Billion pa by 2015;• GFCF > 25% of GDP;• Investment in Building and Construction > 50% of GFCF

Property an AVERAGE Investment• Industry has mediocre leadership, lacks vision;• Confidence low;• Private Sector Investment 50% - 60% of Total Investment in Building; • CPI 10% - 12%;• Real Interest Rates 7,5% - 10%;• Building Industry growth < 3,5%;• Construction Industry growth < 5%;• FTHB Subsidies 1% - 2,5% of Budget;• Infrastructure spend R300 – R500 Billion by 2015;• GFCF 15% - 20% of GDP;• Investment in Building & Construction 15% - 25% of GFCF

Credit and Capital markets openCredit and Capital markets open

Gro

wth

Gro

wth

(Source: The three Keys to success in uncertain times: Business Flexibility, Awarenes and Resilience: www.gibsreview.co.za)(Source: The three Keys to success in uncertain times: Business Flexibility, Awarenes and Resilience: www.gibsreview.co.za)

Credit and Capital markets closedCredit and Capital markets closed

MAKING SENSE OF THE FUTURE: FLAGSwww.strategicforum.co.za

66 © BMI-BRSCU

THE HIGH ROAD (UBUNTU): MEDIUM TO LOW PROBABILITY• Route 1 (The High Road) can be described as a type of SA Capitalism which

recognises the responsibility of the rich helping the poor, but also acknowledges that this can only be achieved through economic growth. It is therefore based on the DUALISTIC principle of Growth through Redistribution and Redistribution through Growth

• This is a world in which government policy accentuates competitive market solutions and they work. Policies that allow market-based solutions, though initially painful produce the quickest and most stable results. Real cost and values are allowed to play out. Innovation results and all forms of housing investment recovers on a base of sound private management.

• This requires courageous political leadership based on an IGNITING VISION, a collaborative mindset and the PRODUCTIVE CAPABILITY to fund and build 5 million Affordable houses eliminating the housing backlog by 2020 and creating 300 000 new jobs annually.

• The strategy for Sustainable Integrated Housing Settlements is visionary and achievable.

• SA has demonstrated the productive ability to succeed through the Soccer World Cup and can continue to do so, provided all the resources of the GOLDEN TRIANGLE are deployed.

• The rewards will be a healthy building industry acting as an engine for economic growth, wealth creation and nation building through home ownership, with SA a world model of a reconciled, winning Nation.

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

67 © BMI-BRSCU

THE UPPER MIDDLE ROAD (Long walk to freedom);MEDIUM TO HIGH PROBABILITY• Route 2 (The Upper Middle Road) can be described as a type of SA

democracy verging on socialism.• There is a desire to uplift the populace through the provision of housing,

health and education, but the low growth scenario results in increasing unemployment.

• This is a world in which a balanced combination of government intervention and competitive market initiatives are put in place. This leads to a moderate return of private investment in long term housing finance by some institutions, but also buffers some of the harsh impacts of total free-market solutions.

• Bubble-based economic growth is avoided but government spending and deficits remain an issue, with housing subsidies increasing steadily to 2020.

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

68 © BMI-BRSCU

THE LOWER MIDDLE ROAD (Pretoria will provide):HIGH PROBABILITY• Route 3 is a world of muddling along in which government policy

accentuates affirmative action and BEE solutions with a result that the “rich get richer.” Social justice is part of core SA values but political will subverts application. Government focuses on PUNITIVE TAXES of the limited number of tax payers to fund spending. An expanded ghetto-ization of SA housing results.

• It is characterised by an entitlement culture based on redistribution with or without growth and at any cost.

• The entitlement culture is funded by the increasing tax BURDEN of the limited number of taxpayers in the country supporting a disproportionately large and growing army of dependents through social grants.

• In the long run this scenario is unsustainable and the risk of deterioration to the Low Road is ever present. SA could continue muddling along with some half hearted attempts at cooperation between Government and the Private Sector and end up on the Low Road with SA failing to live up to its potential.

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

69 © BMI-BRSCU

THE LOW ROAD (Cry the beloved Country):MEDIUM TO LOW PROBABILITY• Route 4 (The Low Road) can be described as a type of SA Socialim

verging on Communism with SA becoming a Third World POPULIST Country like Zimbabwe.

• Corruption is out of control and housing delivery is almost non-existent and backlogs unmanageable.

• The majority of people end up in unserviced squatter camp ghettos without any hope of home ownership.

• The inability to deliver because of corruption, nepotism, cadre deployment, tender-preneurs, Affirmative Action and BEE results in the continued deterioration of Provincial and Local Government Services, infrastructure, health and education AND INCREASING HOUSING BACKLOGS.

• The risks for endemic social unrest and violence increases progressively, and the environment will be supportive of populist leaders.

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

70 © BMI-BRSCU

Investment ClimateInvestment Climate

The STRATEGIC FORUMSTRATEGIC FORUM ScenariosFOR THE BUILDING INDUSTRY: 2010-2020

BOUYANT GROWTH> 5 % PA

GDFI > 25 % OF GDP

SUBSIDIES3 - 5 % OF BUDGET

AVERAGE GROWTH 2 - 5 % PA

GDFI 20 - 25 %OF GDP

SUBSIDIES2 - 3 % OF BUDGET

LOW GROWTH0 - 2 % PA

GDFI 15 - 20 %OF GDP

SUBSIDIES1 - 2 % OF BUDGET

NEGATIVE GROWTH< 0 % PA

GDFI < 15 %OF GDP

SUBSIDIES< 1 % OF BUDGET

NO

CO

NF

IDE

NC

E

L

OW

A

VE

RA

GE

HIG

H C

ON

FID

EN

CE

Ris

k A

vo

ida

nc

e

Ris

k A

ve

rsio

n

Ris

k T

ole

ran

ce

R

isk

Ta

kin

g

PROPERTY A POOR INVESTMENT / AVERAGE / GOOD / A PREFERRED INVESTMENTParadigm Regression Paradigm Paralysis Paradigm Shift Paradigm Reinvention

HIGH ROAD HIGH ROAD COLUMBUS SCENARIOCOLUMBUS SCENARIO

Property a PREFERRED InvestmentHome Ownership PREFERRED

BUOYANT GROWTHBacklogs eliminated by 2020

UPPER MIDDLE ROAD UPPER MIDDLE ROAD APOLLO SCENARIOAPOLLO SCENARIO

Property a GOOD InvestmentHome Ownership DESIRED

AVERAGE GROWTH Erosion of Backlogs

LOWER MIDDLE ROADLOWER MIDDLE ROAD SOYUZ SCENARIOSOYUZ SCENARIO

Property an AVERAGE InvestmentHome Ownership QUESTIONED

LOW GROWTHKeeping pace with Population

LOW ROAD LOW ROAD CHALLENGER SCENARIOCHALLENGER SCENARIO

Property a POOR InvestmentHome Ownership AVOIDED

NEGATIVE GROWTHIncreasing BACKLOGS

Inve

sto

r C

on

fid

ence

Inve

sto

r C

on

fid

ence

Trends in the Building Industry are inextricably responsive to, and influenced by INVESTMENT

CLIMATE, INVESTOR CONFIDENCE and PROPERTY DELIVERY.

Trends in the Building Industry are inextricably responsive to, and influenced by INVESTMENT

CLIMATE, INVESTOR CONFIDENCE and PROPERTY DELIVERY.

Property

delivery

Property

delivery

THE STRATEGIC FORUM SCENARIOSwww.strategicforum.co.za

71 © BMI-BRSCU

The Major GAMEBREAKING POTENTIAL lie in the following areas:

An igniting vision of nation-building through home-ownership, property as a preferred investment and building as an engine for growth and wealth-creation;

Interest Rates falling further by 2-3 percentage points;

The Banks relaxing their stringent lending criteria and promoting Home Ownership as an Engine for Growth and Wealth Creation;

Return of Investor Confidence, Banks first and then Consumers;

Reinvented Investment Climate. (Source: BMI-BRSCU)

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

72 © BMI-BRSCU

TOTAL BUILDING ACTIVITY: 2000-2009 THE STRATEGIC FORUM SCENARIOS: 2010-2020

(Source: SARB, StatsSA, MFA, BMI-BRSCU Workings)

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

R M

ILL

ION

S (

2009

VA

LU

ES

)

TOTAL BUILDINGS : 2000-2007: LOWER MIDDLE ROAD SOYUZ SCENARIO: 2000-2007

1984 PEAK LEVEL OF INVESTMENT

TOTAL BUILDINGS HIGH ROAD COLUMBUS SCENARIO

TOTAL BUILDINGS LOW ROAD CHALLENGER SCENARIO

TOTAL BUILDINGS HIGHER MIDDLE ROAD APOLLO SCENARIO

TOTAL BUILDINGS LOWER MIDDLE ROAD SOYUZ SCENARIO

1984 PEAK LEVEL OF INVESTMENT

CURRENT MOST LIKELY FUTUREBETWEEN LOWER MIDDLE ROAD SOYUZ AND

LOW ROAD CHALLENGER SCENARIOS

The High Road Scenario will not require a major miracle to be realised.But . . . Political will and Leadership is essential.

THE ART OF QUANTUM PLANNINGwww.strategicforum.co.za

73 © BMI-BRSCU

Stage 1Hubris bornOf success

Stage 2Undisciplined

Pursuit of More

Stage 3Denial of Risk

and Peril

Stage 4Grasping for

Salvation

Stage 5Recovery and

Renewal

WELL FOUNDED HOPE

STRATEGIC DRIFT AND REINVENTIONwww.strategicforum.co.za

?

What will it take?

(Source: Based on Collins: How the Mighty Fall: 2009)

19

93

/01

19

93

/06

19

93

/11

19

94

/04

19

94

/09

19

95

/02

19

95

/07

19

95

/12

19

96

/05

19

96

/10

19

97

/03

19

97

/08

19

98

/01

19

98

/06

19

98

/11

19

99

/04

19

99

/09

20

00

/02

20

00

/07

20

00

/12

20

01

/05

20

01

/10

20

02

/03

20

02

/08

20

03

/01

20

03

/06

20

03

/11

20

04

/04

20

04

/09

20

05

/02

20

05

/07

20

05

/12

20

06

/05

20

06

/10

20

07

/03

20

07

/08

20

08

/01

20

08

/06

20

08

/11

20

09

/04

20

09

/09

New mortgage loans and readvances by month and application: 1993-2009 (September)(Source: SARB, BMI-BRSCU Workings)

74 © BMI-BRSCU

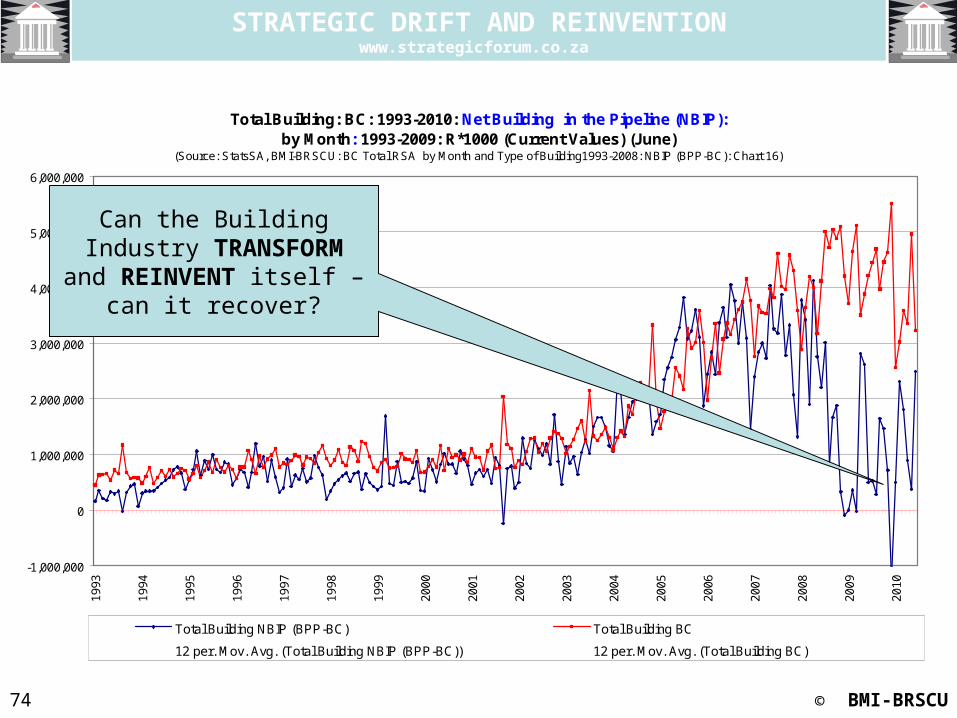

Total Building: BC: 1993-2010: Net Building in the Pipeline (NBIP): by Month: 1993-2009: R*1000 (Current Values) (June)

(Source: StatsSA, BMI-BRSCU: BC Total RSA by Month and Type of Building1993-2008: NBIP (BPP-BC): Chart 16)

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Total Building NBIP (BPP-BC) Total Building BC

12 per. Mov. Avg. (Total Building NBIP (BPP-BC)) 12 per. Mov. Avg. (Total Building BC)

STRATEGIC DRIFT AND REINVENTIONwww.strategicforum.co.za

Can the Building Industry TRANSFORM and

REINVENT itself – can it recover?

75 © BMI-BRSCU

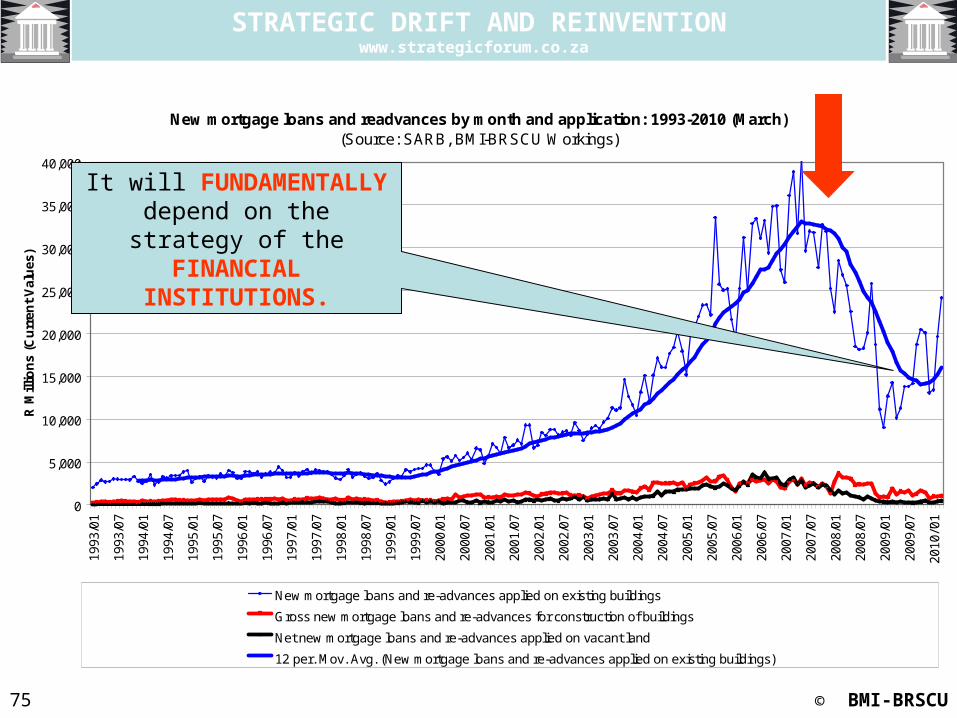

New mortgage loans and readvances by month and application: 1993-2010 (March)(Source: SARB, BMI-BRSCU Workings)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1993

/01

1993

/07

1994

/01

1994

/07

1995

/01

1995

/07

1996

/01

1996

/07

1997

/01

1997

/07

1998

/01

1998

/07

1999

/01

1999

/07

2000

/01

2000

/07

2001

/01

2001

/07

2002

/01

2002

/07

2003

/01

2003

/07

2004

/01

2004

/07

2005

/01

2005

/07

2006

/01

2006

/07

2007

/01

2007

/07

2008

/01

2008

/07

2009

/01

2009

/07

2010

/'01

R M

illio

ns

(Cu

rren

t V

alu

es)

New mortgage loans and re-advances applied on existing buildings

Gross new mortgage loans and re-advances for construction of buildings

Net new mortgage loans and re-advances applied on vacant land

12 per. Mov. Avg. (New mortgage loans and re-advances applied on existing buildings)

STRATEGIC DRIFT AND REINVENTIONwww.strategicforum.co.za

It will FUNDAMENTALLY depend on the strategy of

the FINANCIAL INSTITUTIONS.