the governmental accounting system in argentina

TRANSCRIPT

Occasional Paper No. 7 January 2004

Public Sector

Committee

The Governmental Accounting System in Argentina

This Occasional Paper was approved for publication by the Public Sector Committee of the International Federation of Accountants. It was published in January 2004.

Information about the International Federation of Accountants can be found at its web site http://www.ifac.org.

The approved text of this Occasional Paper is that published in the English language.

Copies of this Paper may be downloaded free of charge from the IFAC internet site.

International Federation of Accountants

545 Fifth Avenue, 14th Floor

New York, NY 10017 USA

Fax: +1 212-286-9570

Email: [email protected]

Copyright © January 2004 by the International Federation of Accountants. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the International Federation of Accountants.

ISBN: 1-931949-17-4

Acknowledgement The Public Sector Committee (PSC) of the International Federation of Accountants (IFAC) is indebted to Carmen Giachino Palladino for preparing this Occasional Paper. The views expressed are those of the author and are not necessarily those of the PSC or IFAC.

Carmen Giachino Palladino is a member of the PSC. The former Accountant-General of Argentina, Carmen is a consultant to the Inter-American Development Bank for government accounting in Latin America. She is also the Argentine representative of the Peacekeeping Missions Working Group which is organized by the United Nations and the Chairperson of the Public Sector Committee of the Federación Argentina de Consejos Profesionales de Ciencias Económicas (FACPCE). She now teaches at the Technical College of the Argentine Army and the Postgraduate Institute of Governmental Economists, Public Budget Argentine Association and previously has taught at the Training and Investigation Center of the Secretariat of Financing.

Preface This Occasional Paper describes the major reforms affecting the federal government of Argentina and the Governmental Accounting System in its migration to accrual accounting. It traces the steps taken in the development and implementation in governmental financial administration in Argentina from 1993 as a consequence of the Government’s decision to prepare the financial statements on the accrual basis. The reforms are part of an ongoing evolution to improve and increase efficiency in financial reporting in the public sector.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

CONTENTS

EXECUTIVE SUMMARY........................................................................................................................................................1

1. BACKGROUND AND INTRODUCTION............................................................................................................................2

1.1 GOVERNMENT AND THE PUBLIC SECTOR ACCOUNTING PROFESSION IN ARGENTINA...........................2

1.2 PREVIOUS LEGISLATION AND CURRENT REFORM.........................................................................................2

2. CURRENT SITUATION......................................................................................................................................................4

2.1 REFORM OF THE GOVERNMENTAL FINANCIAL ADMINISTRATION.............................................................4

2.1.1 THE ROLE OF THE NATIONAL ACCOUNTING OFFICE....................................................................................5

2.1.2 REFORMS AT THE NATIONAL LEVEL ................................................................................................................8

2.1.3 PROVINCIAL LEVEL AND GOVERNMENT OF THE CITY OF BUENOS AIRES.................................................8

2.1.4 INTERNATIONAL PARTICIPATION.......................................................................................................................8

2.1.5 REGIONAL LEVEL................................................................................................................................................8

3. THE GOVERNMENTAL ACCOUNTING SYSTEM ....................................................................................................... 10

3.1 THE ACCOUNTS PLAN (CHART OF ACCOUNTS ) AND ITS RELATIONSHIP WITH THE BUDGETARY PROCESS ........................................................................10

3.2 THE ACCRUAL BASIS IN ARGENTINA...............................................................................................................10

3.3 GOVERNMENT ASSETS ........................................................................................................................................12

3.4 INVESTMENT ACCOUNT......................................................................................................................................13

3.5 FINANCIAL STATEMENTS OF THE FEDERAL GOVERNMENT CENTRAL ADMINISTRATION...................14

4. OBJECTIVES FOR FUTURE DEVELOPMENT IN THE GOVERNMENTAL ACCOUNTING SYSTEM ..................... 16

5. CONCLUSION.................................................................................................................................................................. 17

APPENDIX I: SUMMARY OF FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION OF THE ARGENTINE GOVERNMENT .............................................................................................................................. 18

EXECUTIVE SUMMARY

Executive Summary The Paper provides a background of the development of the accounting profession in Argentina and its influence in the public sector. It also provides an overview of the evolution of the public sector accounting system in Argentina from the onset of the Argentine Confederation. The cash basis of accounting was adopted in 1859 and in 1947, the financial statements were modified to include recognition of expenses on a commitment basis. (For the purpose of this Paper, the “commitment basis” refers to a basis which recognizes the total contract value upon contract signature by all parties.) In 1993, a decision was made to adopt accrual accounting in the federal government.

The Paper outlines the weaknesses in the public sector accounting system which led to the Reform of the Governmental Financial Administration and, consequently, the adoption of accrual accounting in 1993. This reform first focused on the Central Administration, decentralized bodies, state universities and government business enterprises and public societies, but will be extended to provincial and municipal governments in the near future. The reform, overseen by the Ministry of Economy and relevant ministries, includes maintaining a newly developed Governmental Accounting System and coordinating with the professional bodies and academics to ensure that the system is appropriately maintained and updated.

The governmental accounting and budget systems are largely integrated, that is, they utilize the same type of accounts, except for certain accounting transactions. Where there are differences between the accounting transactions and the government budget appropriations, a comparison table is generated to explain the differences. The reform has brought about a positive impact in the Government Financial Administration, including an increase in efficiency and effectiveness in public administration, and delivered more accurate information to support political decision-making.

The Paper also outlines other challenges and issues that arose in data collection, practice and culture. In this context, it is noted that the current information system does not have sufficient data to accurately determine reliable information for receivables arising from tax revenues for the current period. Therefore, the Argentine financial statements are prepared on the accrual basis, except for tax revenue which is recognized on a cash basis. The Government is currently considering mechanisms to enhance disclosure on tax receivables.

Finally, the Paper outlines anticipated future developments in the Governmental Accounting System. These include improving the management accounting of the public sector to further enhance decision-making, consolidation of all public sector entities, creating a continuous training program for public sector employees and harmonizing the Argentine public sector generally accepted accounting principles with International Public Sector Accounting Standards (IPSASs).

The Governmental Accounting System is now considered a significant tool in providing accountability and transparent financial information in the public sector.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

1. Background and Introduction The objective of this Paper is to present the reforms undertaken within the Financial Administration area of the Argentine Government and the progress achieved in relation to the Governmental Accounting System.

1.1 Government and the Public Sector Accounting Profession in Argentina Argentina is organized into independent provinces under the Federal and Republican Constitution. The accounting profession in Argentina was first recognized as an independent accounting profession in legislation in 1945.

It is organized in “Professional Councils” who are responsible for the accounting profession in each province. The “Professional Councils” in turn merge into the national body of accounting — the Federación Argentina de Consejos Profesionales de Ciencias Económicas (FACPCE, Argentine Federation of Economic Science Professional Councils). The FACPCE is responsible for setting the accounting standards and rules for the private sector. The accounting profession in Argentina has always been oriented to the private sector with no influence in the public sector. The National Accounting Office, which is a government body, is responsible for setting the accounting standards and regulations for the public sector. In 1993, the decision was made to adopt accrual accounting, and the first balance sheet was prepared at the end of the 1998 fiscal year. Before 1993, the accounting profession in the public sector was primarily focused on the legal aspects of recording transactions, and monitoring compliance with contractual and other obligations. During this period, lawyers were more prominent in the profession than accountants.

Significant development of the profession in the public sector occurred with the implementation of the accounting principles in 1995. After 1998, the academic sector started to work together with both sectors (public and private) to provide expert assistance in accounting issues.

1.2 Previous Legislation and Current Reform The National Accounting Office was created in 1826 to be responsible for developing and implementing the governmental accounting system. Since 1826, several legal frameworks have been implemented to address accounting issues. The earliest of these was passed at the beginning of the Argentine Confederation and was in operation from 1859 to 1870 (Law # 217). Other Laws relating to account ing were passed for the periods: 1870 to 1947 (Law # 428), 1947 to 1956 (Law # 12.961), and 1956 to 1992 (Law # 23.354). The current Law, “Financial Administration and Control Systems of the National Public Sector”, has been in force since 1993. The major features of these are attached in figure 1.

BACKGROUND AND INTRODUCTION

Figure 1: The progressive change of the principal accounting regulations that ruled the Argentine public sector accounting systems

The first regulations had a positive influence on financial management and reporting and allowed for certain developments, such as the law of 1870 (# 428) which implemented the double entry system on a cash basis and drafted out clear responsibilities of public officers. However, it was only with the current law (# 24.156) that the principle of “accrual” was implemented.

The design of the National Accounting Law applying from 1956 to 1992 (Law #23.354) reflected political as well as judicial needs for information for the control of legal and third party matters. However, it did not require the establishment of a chart of accounts or the preparation of consolidated financial statements and management reports. Therefore, it did not provide an overview of the financial situation. As a consequence, the final product — the General Accounts of the Fiscal Year — did not apply comprehensive and homogeneous criteria for the recognition of revenues, expenses, assets and liabilities or for the consolidation of the financial statements. Consequently, the information was not prepared on a consistent basis and was not drawn together in the consolidated statements.

Period which Law Applies

Law Criteria

1859–1870 # 217 • Cash basis — no payments without budget approval

1870–1947 # 428 • Cash basis — Double entry system • Budget uniformity throughout the public sector • Only budget information reported to the public. Budget

reported on a cash basis.

1947–1956 #12.961 • Cash basis for revenue — Commitment basis* for expenses

1956–1992 # 23.354

National Accounting Law

• Cash basis for revenue — Commitment basis * for expenses

• Preparation of Asset Accounting started

1993 # 24.156

Financial Administration and Control Systems of the National Public Sector

• Accrual basis for non-tax revenue — Accrual for expenses — Cash for tax revenue

• Accrual basis — Double entry system • Implementation of the Accounting Principles —

Financial Statements

*For the purpose of this Paper, the “commitment basis ” is used to refer to the recognition of the total contract value upon contract signature by all parties.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

2. Current Situation

2.1 Reform of the Governmental Financial Administration Before the 1993 Reform, there were weaknesses in the Financial Administration of the National Government. These weaknesses are summarized below.

• The system did not generate complete, reliable information about the financial management of the resources managed on behalf of the community. It reported only cash and near cash resources.

• There was no department or office in charge of the administration and regulation of the national debt, which was growing both internally and externally. This meant that there were no regulations governing the Public Credit System or an entity in charge of its management.

• The Treasury undertook the administrative tasks of cash payments without being involved in the management of the monetary or financial aspects of the National Public Sector.

• The amount of public assets, as well as actual liabilities and contingent liabilities, were unknown.

• There was little commitment to training the workforce for financial management and reporting in the public sector.

This situation required a major change in order to achieve the objectives of the Governmental Financial Administration which was to operate the economy in an efficient and effective manner.

As a consequence, a reform program was initiated in 1993 with the support of the World Bank. This project called “Reform of the Governmental Financial Administration” was overseen by the Ministry of Economy with direct involvement from the Secretary of Finance and the Budget Undersecretary. The reform process commenced with legislation enacted in 1992 and implemented in 1993.

The first stage of the reform was undertaken in the non-financial public sector as a whole — that is, the Central Administration, decentralized bodies, state universities and government enterprises and public societies. The reform process will also be extended to provincial and municipal administrations in the future through their acceptance of the modernization and updating processes which are already under way. The reform program includes the development of the following integrated systems:

• Budget System;

• Public Credit System;

• Treasury System;

• Accounting System;

• Contracts System (governing all government purchases of assets and services); and

• Assets Administration System.

CURRENT SITUATION

The Contracts and Assets Administration Systems referred to above have not been formally legislated. This means that they do not have a legal framework yet but are necessary for the government to continue to operate and comply with relevant rules and regulations.

This reform program has had a positive impact on all the systems of the Governmental Financial Administration. Its impact includes an increase in efficiency of public administration and interrelated systems at all levels. It also means that better information is generated to support informed political decision-making and a more effective administration system is developed to implement the decisions.

2.1.1 The Role of the National Accounting Office The National Accounting Office is responsible for developing and maintaining the Governmental Accounting System as well as the issuance of the applicable accounting regulations.

Law # 24.156, enacted in 1993, requires that the Governmental Accounting System be developed to present the following general characteristics. The system should:

• Be common, unique, uniform and applicable to all the entities within the National Public Sector. This system only affects the federal government; it does not include either municipalities or provinces within the Argentine Federal and Republican Constitution jurisdiction. The Federal Government includes:

? The Central Administration (Ministries and State Secretaries);

? Decentralized organizations (i.e., National Assessment Tribunal);

? Social security institutions;

? State universities; and

? Government business enterprises.

• Integrate budget, assets management and treasury information within each entity, and with the National Accounts.

• Present the budgetary execution, movements and financial position of the Treasury and public institutions.

• Enable cost assessment of public operations. This aspect of the system has to be further developed since it is a pending issue which will be considered in the future.

• Be based on the generally accepted accounting principles, applicable to the public sector, and developed by the National Accounting Office. Those principles require that the budget and accounting systems be integrated; that is, the budget and accounting system use the same principles of recognition, terminology and concepts. They also require that the accrual principle be implemented and applied to register expenditures and non-tax resources, and tax resources be effectively registered on a cash basis. The cash basis is used for tax resources because it is very difficult to pinpoint the exact taxable event which affects the reliability of measurement.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

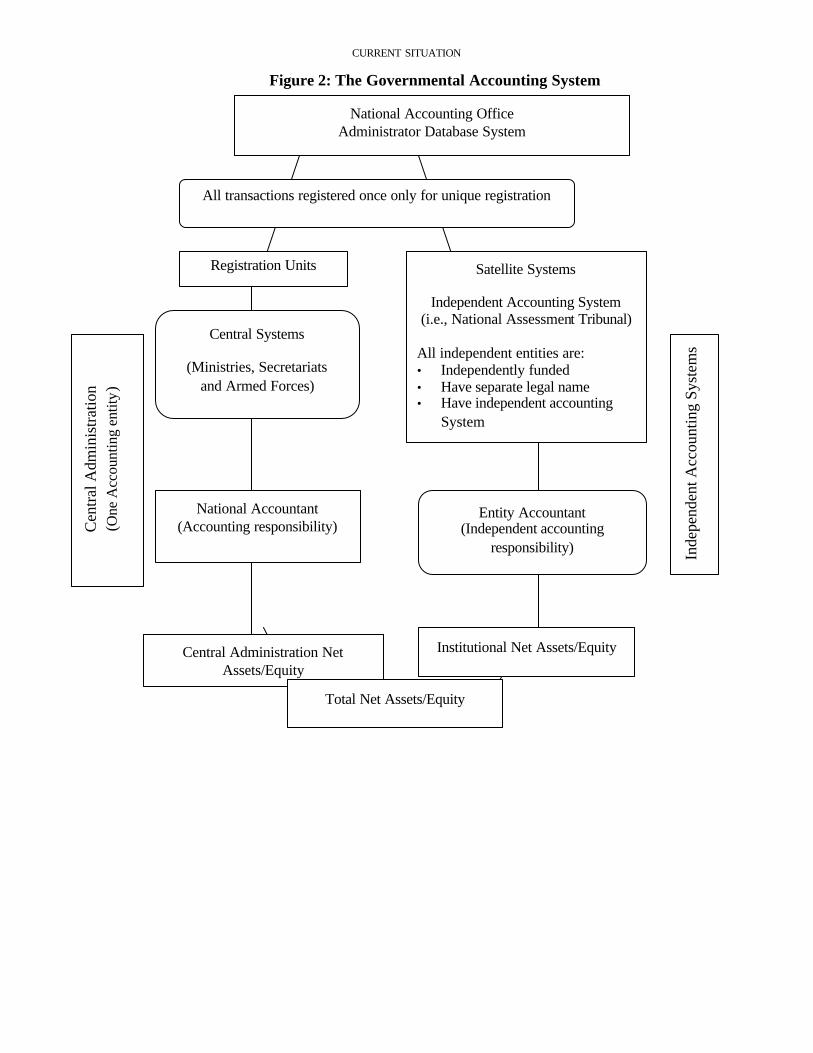

In relation to the organization of the system itself, the main methodological aspects are as follows:

• Within the national public sector, there are two different types of accounting entity: one is the Central Administration and the other is related to Decentralized Organizations or Institutions. Each entity is a separate legal entity – this means that each entity has a separate legal name, independent funding and independent accounting system.

• The departments responsible for managing the accounts of the institutions are technically dependent on the National Accounting Office (that is, they follow the regulations developed and used by the office), and the Operating Accounting Systems follow the design determined by this Central Body.

• Within the Central Administration, the accounting system is organized as follows:

? Registration Units are established as satellites of the system. Registration Units are those organizational centers where economic events of the institutions originate and are accounted for (i.e., Ministries, Secretariats, Armed Forces, etc.) by the National Accounting Office (as the administrator of the central database of the system). The National Accounting Office governs the Decentralized Organizations, that is, it sets the rules to be followed and is a part of Registration Units.

? The data necessary to produce the information outputs which are required by the National Accounting Office are transferred to the central database of the system. Within the Registration Units, the information administered is unique for each particular unit.

? The Registration Units centralize and accumulate the information provided by lower level offices, which are responsible for the basic budget, treasury and assets operations.

? The system requires that transactions are registered only once, and the outputs of information required for accounting purposes, either at central or satellite level, are obtained from this unique registration.

CURRENT SITUATION

Figure 2: The Governmental Accounting System

National Accounting Office Administrator Database System

Satellite Systems

Independent Accounting System (i.e., National Assessment Tribunal)

All independent entities are: • Independently funded • Have separate legal name • Have independent accounting

System

Registration Units

Central Systems

(Ministries, Secretariats and Armed Forces)

Central Administration Net Assets/Equity

Total Net Assets/Equity

Institutional Net Assets/Equity

All transactions registered once only for unique registration

Entity Accountant (Independent accounting

responsibility)

Cen

tral A

dmin

istra

tion

(One

Acc

ount

ing

entit

y)

Inde

pend

ent A

ccou

ntin

g Sy

stem

s

National Accountant (Accounting responsibility)

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

2.1.2 Reforms at the National Level

The Financial Administration 1993 reform also led to (based on Law # 24.156 and its supplementary regulations) the requirement of the National Accounting Office to interact with the following representative professional bodies in order to coordinate and combine efforts to update the accounting system: Economic Science Professional Council of the City of Buenos Aires Government (Consejo Profesional de Ciencias Económicas del Gobierno de la Ciudad de Buenos Aires, CPCE); the Argentine Federation of Economic Science Professional Councils (Federación Argentina de Consejos Profesionales de Ciencias Económicas, FACPCE); and the academics.

A priority of the National Accounting Office has been the training of staff of the satellite units. This has been accomplished through the coordinated efforts of the public and private universities, together with the Training Center of the Secretariat of Finance. The training was to achieve the objective of enhancing the economy, implementing efficiency and effectiveness principles in the collection and application of public revenue.

2.1.3 Provincial Level and Government of the City of Buenos Aires A working program has been prepared and is being implemented with the objective of promoting and coordinating the application of integrated systems of the Governmental Financial Administration which apply the principles ruling at national level with: the Provinces, the Government of the City of Buenos Aires and, through the Provinces, with the municipalities.

Once the program is completed as planned, Argentina will be ready to activate an information system which provides up-to-date information on an ongoing basis that provides constant consultation on the management of individual components and on the consolidated position of the Argentine Public Sector as a whole. This system will allow the analysis and assessment of the performance of the public sector to be undertaken from an economic, financial and social point of view. Of a total of 23 provinces, only the province of La Rioja has issued financial statements similar to the ones issued by the National Government of Argentina. The rest of the provinces are in the process of change and/or financial administrative reform.

The National Accounting Office, together with the Provincial Accounting Offices, created the Argentine Association of General Accountants (Asociación Argentina de Contadores Generales) with the purpose of improving the management of the accounting resources of the Argentine Public Sector.

2.1.4 International Participation The development of the Governmental Accounting System has been enhanced by the participation of the National Accounting Office in the Iberoamerican Forum of Public Accounting. A public sector expert representing FACPCE is now a member of the IFAC Public Sector Committee (PSC).

2.1.5 Regional Level Other countries in the region also develop accounting systems in managing their governmental accounting system. The following chart (figure 3) shows a comparison among five South American countries on the integration of the accounting and budget systems and their recognition criteria.

CURRENT SITUATION

Country Comparative Chart: (Perú, Paraguay, Brazil, Argentina and Uruguay) Figure 3: A Comparison among Five South American Countries on the Integration

of the Accounting and Budget Systems and their Registration Criteria for the transactions.

Perú Paraguay Brazil Argentina Uruguay

Integration of Accounting and Budget

Not integrated

Integrated Not integrated

Integrated Not integrated

Registration Criterion of transactions

Accounting Accrual Modified accrual (**)

Accrual Modified accrual (**)

Budget Information

(***)

Budget Cash Basis Modified accrual (**)

Commitment basis (*)

Modified accrual (**)

Modified accrual (**)

(*) Commitment basis : Recognition of total contract value upon Contract Signature of both parties.

(**) Modified Accrual: Accrual principle to recognize expense and non-tax revenues. Cash basis for recognition for tax revenues.

(***) Currently, the Uruguayan government does not prepare general purpose financial statements. It only prepares and publishes budget information. However, Rule #81/2002 was recently passed by the Accounting Tribunal — it provides that IPSASs will be adopted.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

3. The Governmental Accounting System

3.1 The Accounts Plan (Chart of Accounts) and its Relationship with the Budgetary Process A substantial aspect of the reforms which have been implemented is the establishment of an appropriate relationship between budget and accounts. This relationship occurs automatically through the Financial Information Integrated System (Sistema Integro de Información Financiera, SIDIF). The following outlines the major features considered when developing the system:

• The application of the concepts of universality and budget unity — that is the same system is to be applied throughout the public sector and the accounts are to articulate with the budget designation.

• The links between the budget registrations and the chart of accounts, such that recognition of amounts “accrued” and “paid”, trigger an automatic conversion matrix of the budget registrations into general accounting registrations.

• In relation to the wider concept of inflow and outflow of funds, the system recognizes receipts being generated either from:

a. traditional current income;

b. the sale (decrease) of assets; or

c. the increase of liabilities.

On the other hand, the system recognizes expenditures being generated from:

a. current expenses;

b. the purchase (increase) of assets; or

c. the decrease of liabilities.

• The unique nature of each transaction will require each operation to be registered only once, at its input, which will then feed through the rest of the systems.

However, not every accounting operation, transaction or event is included in government budgets, i.e., amortizations. Therefore, there are differences between the budgets and the accounts at closing date of each fiscal year. Thus, the National Accounting Office has developed a “Contrast Table” which generates and explains the movement from the budgetary result (surplus or deficit) to the accounting result.

3.2 The Accrual Basis in Argentina Resolution # 25/95 of the Secretariat of Finance establishes the following General Accounting Principles which encompass matters such as: the economic entity, going concern, reporting period, financial assets, local currency, valuation at cost or fair value, explanation/note disclosures, materiality, universality, consistency, prudence and the accrual basis.

The accrual principle as recognized in IPSASs is that transactions and events are recognized when they occur (and not only when cash or its equivalent is received or paid). Therefore, the transactions

THE GOVERNMENTAL ACCOUNTING SYSTEM

and events are recorded in the accounting records and recognized in the financial statements of the periods to which they relate. This is consistent with the underlying principles of accrual accounting as adopted in Argentina. (See Figure 4 below.)

Figure 4: The Accrual Principle

In Argentina, the accrual principle is described as follows:

“Reconocimiento de las Transacciones”: “…la concurrencia de hechos económicos-financieros motivo de las transacciones que afecten a los entes, las que determinan modificaciones en el patrimonio como así también en los resultados de las operaciones, deben ser reconocidos, a través de las registraciones contables, en el momento que se devengan…”

In English, this translates as follows:

“…the occurrence of economic-financial events giving rise to the transactions affecting entities, which modify the patrimony (net assets/equity) as well as the result of the operations, shall be recognized, through accounting registrations, at the moment of accrual…”

The reason why the accrual basis is adopted for recognition in the budget and in the general purpose financial statements, is because it reflects the time at which the budgetary credit is executed and also the time at which general accounts are affected, either in respect of assets and liabilities or from revenues and expenditures and therefore the operating result.

The criteria for expenditures to be recognized are as follows:

• When the expenditures are authorized by the budget process, they are recognized in the financial statements as expenditures. Examples of such expenditures include donations and subsidies.

• A change in the net assets/equity component of each entity, arising from specific occurrence. Examples of such expenditures include those incurred when making capital assets purchases and other transactions which have economic or financial effect.

• The incurrence of an obligation to make a payment due to the acceptance of goods or services hired in the course of business.

While the timing of recognition of the expenditure is clear, it is not so clear in the case of revenue. In the public sector, revenues arise from tax and non-tax sources such as fines/fees, contributions, grants, property rentals and exchange transactions. Determining the timing of recognition of each of these is complex.

When analyzing the circumstances under which each of the items arise, it can be seen that the amount and date of collection of certain revenue (rates, rentals, sale of assets, etc.) are clear because there is a basis of calculation (a table of charges, the provision of goods or services) and the precise identification of the beneficiary, and thus of the debtor.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

The situation becomes more complex when there are miscellaneous factors affecting the basis of recognition of the revenue and of its respective debtor. This is the case for tax revenue and other transactions and events which are declared in tax statements. The determination of the amount of these can depend on a number of factors (i.e., other revenues and expenses of the taxpayer) not connected with the Administration.

In these cases, even if the date at which the Government’s right to receive tax revenue arises can be clearly identified, the operative procedures of the information systems do not receive the data until the taxpayer settles the debt with the Tax Office. At that point, the revenue is accrued. Therefore, the accrual coincides with the amount “collected”. To this end, the basis of “accrual” reflected in the government data collection systems requires recognition when there is “objective” knowledge of the right. [IPSASs identify that the criteria for recognition is reliable measurement. Currently the position adopted is that adequate reliable measurement only arises when objective knowledge arises. The PSC has also formed a Steering Committee to contribute in the development of guidance on the accounting treatment of revenue from non-exchange transactions (including taxes and transfers). An Invitation to Comment (ITC) on this topic will be issued in January 2004.] Nevertheless, there is concern on the part of the Administration, in relation to this approach — in particular, that the information system does not record information on tax revenue until payment is received. Mechanisms to disclose information about tax receivables prior to the receipt of cash and broad enhancements to the system are currently under review, including enhancements which will impact on the information providers — that is the taxpayer, as a way of improving the accounting disclosures, and also as a tool to control incomplete data or tax evasion.

It is hoped that in the future, a tax data system might be developed to analyze the information gathered from the tax statements submitted and, at that stage, recognize the Government’s right as a receivable.

Summing up, the Governmental Accounting System is based on the “accrual principle”, except for the particular characteristic of tax revenue, which can be defined as a mix of accrued and collected taxes.

3.3 Government Assets The reforms undertaken for property, plant and equipment began with a revaluation of infrastructure assets. This was undertaken jointly by the National Accounting Office and the National Assessment Tribunal, which is the ruling body on real estate valuation issues.

This revaluation has proved beneficial since it provided an up-to-date inventory of the current stock of infrastructure assets and enabled the coordination of records displaying physical characteristics of these assets (asset registers) with accounting records. Furthermore, the useful life of property, plant and equipment can be more readily identified and assessed. This enables proper amortization and the recognition of improvements and enhancements to the stock of infrastructure on an ongoing basis. This information is entered in the system through the scanning of files, to connect it with the deeds and inventory registrations kept by the National Accounting Office. This process assures the faithful representation and reliability of the financial statements.

THE GOVERNMENTAL ACCOUNTING SYSTEM

Currently, property, plant and equipment including infrastructure assets and military equipment, are recognized and valued at their “acquisition or construction cost”, according to the requirements (Resolution # 25/95) of the Secretariat of Finance. Where such

valuations are not available or current, all assets measurement bases that can be used are: fiscal valuation (Resolution # 47/97 of the same Secretariat), a value determined by the tax office and “appraisal valuation” (Administrative Decision # 56/99), a value given by an independent appraiser, will in turn, update the previous valuation. After initial recognition as an asset, property, plant and equipment will be depreciated and that amount will be disclosed in the notes to the financial statements.

It is important to note that this new approach to the recognition and measurement of property, plant and equipment has resulted in a revision of the treatment given to “Infrastructure Assets”. Previously the assets were recognized as they were being constructed and then derecognized when they were put into use, notwithstanding that they have service potential for many future periods, such as in the case with roads and bridges. This approach has given rise to certain anomalies and, arguably, misrepresentations when financing assets through, for example, foreign loans. This is because, consistent with this treatment, when the asset is “activated” and “derecognized” from the financial statements while the emerging debt is kept, it does not represent an accurate and reliable picture of the net asset position. Moreover, if we consider the case of roads and bridges acquired through grants or granted in concession, the entity would recognize and report the revenue but not the assets.

In response to these problems, the accounting regulations have been amended (Accounting Office Provision # 19/02) so that these assets could be recognized. The process of recognition of infrastructure assets is set out below:

• Infrastructure assets, including assets which are under construction or recently completed assets at the closing of the fiscal year, will remain as part of the Government assets.

• Next, in 2002, the existing infrastructure assets will be recognized as part of the Government assets as appropriate, consistent with the modification of the chart of accounts as necessary.

• All infrastructure assets which were not recognized in previous years will be valued in the future with the National Assessment Tribunal.

More reliable valuation and disclosure of Infrastructure Assets will help reflect the basic equation: Assets = Liabilities + Net Position. Currently, the net position shows a negative result which affects the ability of the government to raise foreign debt and also suffers from the distortion which results from not recognizing these assets but recognizing the debt incurred to develop and maintain them. Once the accounting reform has been achieved, a more reliable and better disclosure of financial statements will result.

3.4 Investment Account The Investment Accounts are prepared according to the regulation issued in 1993 (article 95 of Law # 24.156). Major features of the Investment Account are the following:

• Financing-Investment -Savings Account : relates the economic classification of public revenue with the economic classification of public expenses, allowing for the calculation of the following results:

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

? Operative: Current revenue - Current expenses (Debt interest is not included).

? Economic: Current revenue - Current expenses (Debt interest is included).

? Financial: Total revenue (Current revenue + capital income) - Total expenses (Current expenses + capital expenses).

• Statement of the Treasury of the Central Administration: presents the changes of the balances of the Treasury’s cash and cash equivalents.

• Statement of the Public Debt of the Central Administration: presents changes of the Public Debt classified in domestic, foreign, direct and indirect. Direct Public Debt is debt contracted by the Central Administration. Indirect Public Debt is debt contracted by any public or private entity endorsed by Central Administration.

• Financing-Investment -Savings Account of the non-financial national public sector: presents the operative, economic and financial results at each Institutional Level.

• Budgetary execution of revenue and expenses: reports budget approved by law and its execution.

• Information on contributions to the Treasury and pending amounts: reports contributions to the Treasury by centralized and decentralized organizations and the revenue distributable balance at the close of the fiscal year by decentralized organizations.

• Management Result: reports the financial and physical results.

• Financial Statements: Balance Sheet, Statement of Current Results, Statement of Changes in Net Position, and Statement of Origin and Application of Funds. See Appendix I for an example of the format used to present the financial statements or visit the National Accounting Office (CGN) web page http://www.mecon.gov.ar/hacienda/cgn/cuenta/.

3.5 Financial Statements of the Federal Government Central Administration For the first time in the history of the National Public Sector in Argentina, the Public Accounts for fiscal year 1998 included the financial statements of the Central Administration, in which the net position of decentralized bodies, social security institutions, national universities and government business enterprises were combined.

The first financial statements were prepared at the close of the 1998 fiscal year. They inherited the opening balance of the 1993 fiscal year from the previous system, following the Accounts Plan implemented by the new system. As part of this process, it was necessary to implement a review process of balances and changes of valuation of the assets to ensure that the amounts reflected were reliable and justifiable. The tasks undertaken were the following:

• Review of old credit (creditors) and debt (receivables), and a reliable valuation of those amounts for disclosure.

• Changes in methodology for the valuation of infrastructure assets to reflect the actual economic situation (fair value).

THE GOVERNMENTAL ACCOUNTING SYSTEM

• Combination of the net assets of decentralized bodies, social security institutions, national universities and government business enterprises as non current assets of Central Administration at the close of the financial year. The process of combination is

listed below:

1) For the balance at the closing of the fiscal year, every credit or debt movement between the parties is eliminated from the Net Assets of the combined entities. The remaining balances are then accounted for as “Contributions and Capital Shares” account as Non Current Assets in the Financial Statement of the Central Administration.

2) The difference between the balance at beginning and the end of the fiscal year of the Net Assets of the combined entities is adjusted in the Result of the Central Administration.

• New disclosure of public debt and accrued interest at the closing of the fiscal year.

• Analysis of any claim involving the Government as a party, so as to estimate their effect on the financial position of the Government and to include relevant information on contingent liabilities in the notes to the financial statements.

It should be noted that there are no standards or regulations that require the recognition of the effects of a hyperinflationary economy in the financial statements. Therefore, the effects of hyperinflation are not reflected in the financial statements.

The National Public Sector of Argentina requires the presentation in t he Financial Statements which are similar to the format of IPSASs. As noted in section 4, further developments proposed in Argentina include the adoption of all the requirements of IPSASs as well as the presentation formats.

A table identifying the Financ ial Statements required by IPSAS 1 and the Financial Statements

prepared by the Argentine Government follows.

Since fiscal year 1998, the National Accounting Office has continued analyzing and enhancing the presentation of the Financial Statements elaborated for fiscal years 1999, 2000 and 2001.

IPSAS 1 Financial Statements of Argentina

Balance Sheet (or Statement of Financial Position) Balance Sheet (or Statement of Financial Position)

Statement of Financial Performance Statement of Current Results (Resources and Expenditures)

Statement of Changes in Net Assets/Equity Statement of Changes in Net Position

Cash Flow Statement Statement of Origin and Application of Funds

Accounting Polic ies and Notes to the Financial Statements

Valuation Regulations and Notes to the Financial Statements

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

4. Objectives for Future Development in the Governmental Accounting System Further objectives which the Government has committed to achieving to optimize Governmental Accounting System for the coming years are stated below.

• Costs System

The costing system is to be further developed to enable calculation of costs by activity.

• Management Accounting

The development and enhancement of “systems” and reports for management and for decision makers at higher levels.

• Consolidation of Financial Statements

The preparation of consolidated financial statements for all entities. A training plan has been undertaken by the decentralized organizations of the Central Administration to enable proper implementation of the accounting regulations within all the entities in the public sector. It will include consolidation of all the financial statements of the public sector within the different provinces of the country.

• Training

Further improvements of the permanent training process of public sector employees. Additional training will be undertaken by the Universidad de Buenos Aires (UBA, University of Buenos Aires), private universities, and the FACPCE (Argentine Federation of Economic Science Professional Councils).

• International Standards

To continue to the process directed at harmonizing Argentine public sector generally accepted accounting principles with all the IPSASs.

CONCLUSION

5. Conclusion

The objective of the Governmental Accounting System in Argentina is to maintain an appropriate record of the transactions of the government and its agencies, and is to be a key tool to achieve greater transparency in the information and disclosure of the accounts of the public sector.

In Argentina, it is considered a matter of the utmost importance that the Governmental Accounting System has an even more relevant role than the one given to the Budgetary System, that is to achieve the objectives of accountability and transparency. This implies a change of concepts within the organizational culture of the public sector and recognition of the role and benefit of financial reporting.

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

Appendix I: Summary of Financial Statements of the Central Administration of the Argentine Government

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION BALANCE SHEET AS OF DECEMBER 31/2003 — IN PESOS

Fiscal Year 2003 Fiscal Year 2002 Assets Current Assets

Cash and other monetary assets X X Short-term credits X X Inventory and related property X X Total of Current Assets (A) X X Non-current Assets Long-term credits X X Property, plant and equipment X X Intangibles X X Contributions and Capital Shares X X Other assets to be allocated X X Total of Non-Current Assets (B) X X Total Assets (F)=(A) + (B) X X Liabilities Current Liabilities

Short-term debt X X Third parties and collateralized debt X X Deferred Liabilities (prepayments) X X Forecasts X X Other liabilities X X Total of Current Liabilities (C) X X Non-current Liabilities Long-term debt X X Deferred Liabilities (prepayments) X X Contingencies/ Provision X X Other liabilities to be allocated X X Total of Non-Current Liabilities (D) X X Total of Liabilities (E)=(C)+(D) X X

NET POSITION (F) -(E) X X

Total of Net Position — according to Statement X X Total of Liabilities and Net Position X X

Note: The financial statements of the Central Administration integrate the net position of decentralized organizations, social security institutions, national universities and governmental business enterprises, but not the independent provinces and the City of Buenos Aires. The financial statements are prepared on the accrual accounting basis, except for tax revenue which is recognized on a cash basis.

APPENDIX I: SUMMARY OF FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION OF THE ARGENTINE GOVERNMENT

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION STATEMENT OF CURRENT RESULTS (RESOURCES AND EXPENDITURES)

FOR THE TERM ENDED DECEMBER 31, 2003 IN PESOS

Fiscal Year 2003 Fiscal Year 2002 Resources Tax revenue X X Contributions to social security X X Sales of goods and services of public administration X X Transfers received X X Other revenue X X Total Revenue (a) X X Expenditures Excise expenditures X X Rent on goods X X Social security services X X Transfers granted X X Other losses X X Total Expenditures (b) X X

ECONOMIC RESULT OF CENTRAL ADMINISTRATION (a) — (b)

X

X

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

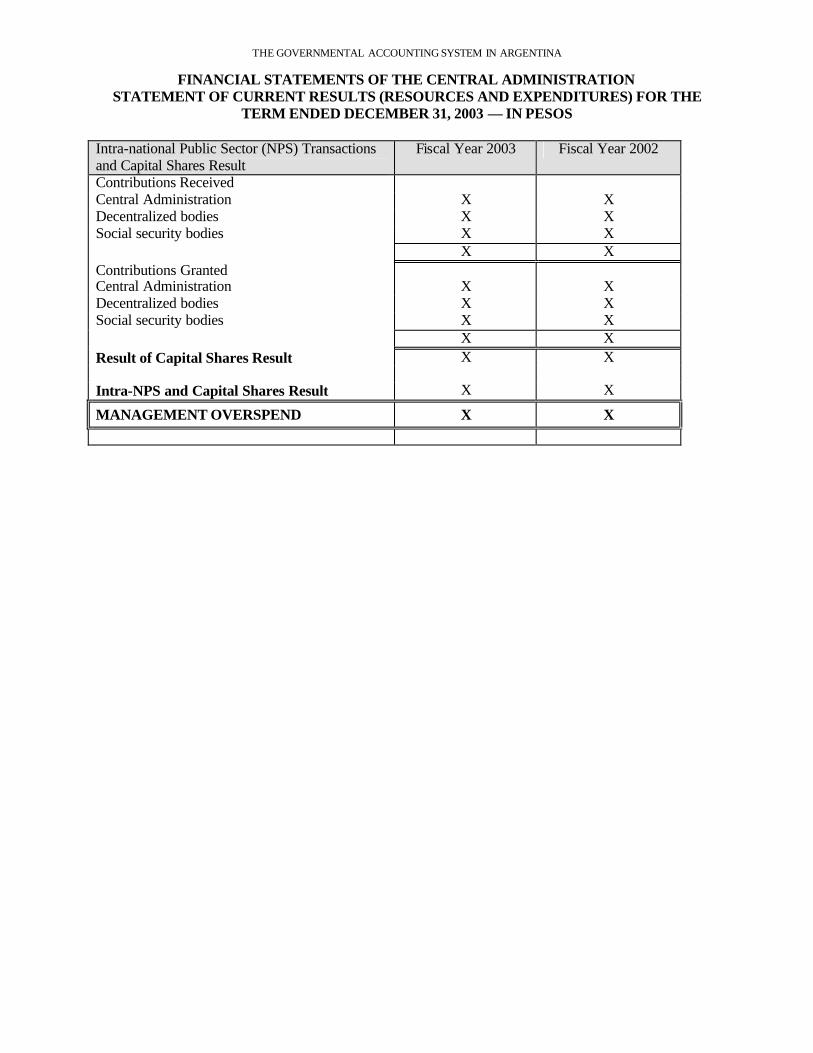

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION STATEMENT OF CURRENT RESULTS (RESOURCES AND EXPENDITURES) FOR THE

TERM ENDED DECEMBER 31, 2003 — IN PESOS

Intra-national Public Sector (NPS) Transactions and Capital Shares Result

Fiscal Year 2003 Fiscal Year 2002

Contributions Received Central Administration X X Decentralized bodies X X Social security bodies X X X X Contributions Granted Central Administration X X Decentralized bodies X X Social security bodies X X X X Result of Capital Shares Result X X Intra-NPS and Capital Shares Result X X

MANAGEMENT OVERSPEND X X

APPENDIX I: SUMMARY OF FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION OF THE ARGENTINE GOVERNMENT

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION STATEMENT OF CHANGES IN NET POSITION

FOR FISCAL YEAR ENDED DECEMBER 31, 2003 — in Pesos

CURRENT ACCOUNT RESULTS

CONCEPT

FISCAL CAPITAL

(1)

RECEIVED CAPITAL TRANSFERS AND CONTRIBUTIONS

(2) PREVIOUS

FISCAL YEARS OF

FISCAL YEAR TOTAL

(3)

PUBLIC FINANCE

(4)=(1)+(2)+(3)

PUBLIC PROPERTY

(5) TOTAL (6)=(4)+(5) Balance — beginning of period X X X X X X Over financial statements of previous fiscal year X X X X X X Change of balance X X X X X X Balances changed at beginning of fiscal year X X X X X X Fiscal Year increase X X X X X X Fiscal Year decrease X X X X X X Fiscal Year Result X X X X X X Balance at closing of fiscal year X X X X X X

THE GOVERNMENTAL ACCOUNTING SYSTEM IN ARGENTINA

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION STATEMENT OF ORIGIN AND APPLICATION OF FUNDS FOR THE PERIOD ENDED 31 DECEMBER 2003 — In Pesos

BALANCE OF MONETARY ASSETS AT BEGINNING OF PERIOD X

ORIGIN OF FUNDS

ANNUAL FLOW X Management saving/overspend X Provisions variations and technical reserves X Fiscal Year Amortizations X NET ASSET POSITION X Increase of Fiscal Capital X Adjustment of Results of Previous Fiscal Years X ASSETS VARIATIONS X Decrease of Current Assets X Financial X Credits X Real X Inventory and Related Property X Decrease of Non Current Assets X Financial X Financial Investment X Contributions and Capital Shares X LIABILITIES VARIATIONS X Increase of Current Liabilities X Debts X Other liabilities X Increase of Non Current Liabilities X Debts X Other liabilities X TOTAL OF ORIGIN OF FUNDS X

APPENDIX I: SUMMARY OF FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION OF THE ARGENTINE GOVERNMENT

FINANCIAL STATEMENTS OF THE CENTRAL ADMINISTRATION STATEMENT OF ORIGIN AND APPLICATION OF FUNDS

FOR THE PERIOD ENDED 31 DECEMBER 2003 — In Pesos (CONT.)

APPLICATION OF FUNDS

NET ASSET POSITION Increase of Fiscal Capital

Adjustment of Results of Previous Fiscal Years ASSETS VARIATIONS X Increase of Current Assets X Financial X Financial Investment X Other assets X Increase of Non Current Assets X Financial X Credits X Real X Property, Plant and Equipment X Intangibles X Other Long Term Assets X LIABILITIES VARIATIONS X Decrease of current liabilities X Guarantee and Third Parties Funds X Deferred Liabilities X TOTAL APPLICATION OF FUNDS X

FINAL BALANCE OF MONETARY ASSETS X The classifications and adjustments at beginning performed during fiscal year 2003 have been segregated so as to reasonably disclose the Origin and Application of Funds of the fiscal year. The Notes and Annexes are an integral part of these Statements.